2024 Crypto Outlook: Winner Winner, Chicken Dinner

Table of Content

1. Intro

2. Macro: Spring Will Come

2-1. Economy: Soft landing, check!

2-2. Interest Rates: Higher rates persist, but expectations for a cut in 2H remain strong

2-3. Market drivers: The perfect storm of one-offs and structural momentum

3. Evolving Regulatory Landscape: Ushering in a More Favorable Environment with Promising Opportunities

3-1. Global regulatory outlook: Unlocking opportunities through comprehensive legalization of crypto assets

3-2. Current state of crypto regulations in Korea: Advancing toward the institutionalization of cryptocurrencies

3-3. Embracing Challenges for Future Growth

4. Blockchain Infrastructure Making Strides

4-1. Cosmos' Appchain vision realized in Ethereum rollup ecosystem

4-2. Alt-L1s will discover PMF centered on scalability and ease of development

5. Major Services Are Poised to Ascend Atop Core Infrastructure; Forthcoming Trends Will Become Evident in 2024

5-1. Gaming: Anticipating a shift in 2024!

5-2. DeFi: Redefining boundaries between DeFi and TradFi

5-3. NFTs: Evolving as a means to improve and expand existing business models

6. Closing Thoughts

1. Intro

"Winner Winner, Chicken Dinner." It’s the famous celebrative victory phrase of the game, PUBG: Battlegrounds. It's a message for those who survived a grueling battle, and it's a message we at Xangle Research would like to dedicate to crypto market participants who are poised to take another leap forward after a long stagnation.

We are pleased to be able to deliver a positive message to crypto builders and investors in this annual outlook report unlike last year. In 2024, we believe that the crypto market will experience an early spring after a long and cold winter due to a variety of internal and external factors, as we predicted in our "2023 Crypto Outlook: Antifragile" report.

From a macroeconomic perspective, we expect the U.S. economy to continue its soft landing and the Federal Reserve to start cutting interest rates in the second half of the year, injecting liquidity back into the market. In the meantime, structural momentum, such as the approval of Bitcoin spot ETFs, halving, progress on legislation, and the weakening of the dollar's hegemony, will drive new funds into the crypto asset market, mainly from institutional investors. Fundamentals will also continue to grow meaningfully as blockchain infrastructure continues to improve and content and services are released on top of it. The fourth quarter of 2023 saw the crypto market ignite on the back of a number of expectations, and we don't see this trend slowing down in the coming year.

We’ve endeavored to make this year’s annual outlook report as informative as possible, as always, and we hope you enjoy reading it.

2. Macro: Spring Will Come

In our 2023 Outlook, we noted that institutional investors are increasingly investing in the crypto asset market due to (1) improved access to investment as infrastructure develops, (2) increased utility of crypto assets, and (3) reduced volatility. We also noted that Bitcoin, the leading crypto asset, is increasingly in correlation with risk assets such as real estate, high-yield bonds, and NASDAQ.

While these three trends held true in 2023, the influx of institutional money into the crypto asset market is increasing with the potential approval of a number of Bitcoin spot ETFs, including BlackRock’s. At the same time, the correlation between Bitcoin and risk assets is at a two-year low, which signals that Bitcoin is finding its place as a fully-fledged asset class in its own right, beyond a simple “investment tool.”

While institutional investors have so far viewed Bitcoin as a risk asset and portfolio booster, it appears that they may gradually begin to utilize it as an alternative to fiat currencies and as a standalone asset with no ties to the TradFi system. While macroeconomic factors such as economic growth and interest rates that influence investor sentiments in general will continue to be important in determining the price movement of the crypto asset market including Bitcoin, the unique dynamics of the crypto market will also play a major role.

We believe that the U.S. economy will make a successful soft landing in 2024 and that the Fed will be able to start cutting rates in the second half of the year. As investor sentiment in crypto assets revives, we expect to see more short-term favorable developments such as the Bitcoin halving and the approval of spot ETFs, as well as structural factors undermining the dollar's hegemony, such as the deteriorating U.S. fiscal position and the growing uncertainty around Fed monetary policy. We believe, with cautious optimism, that 2024 will lay the groundwork for another bull market as the crypto asset market slowly warms up after two long years of crypto winter.

2-1. Economy: Soft landing, check!

We expect that the U.S. will see slower economic growth in 2024 but will avoid recession. Gross domestic product (GDP) can be seen as a sum of consumption (68%), investment (17%), government spending (17%) and net exports (-2%; the U.S. is a net importer and its contribution to GDP is (-) and can considered a constant due to its small share in GDP; Bureau of Economic Analysis, as of July 2023), and it seems there are too few ingredients to accelerate growth. However, we believe also that consumption, investment, and government spending will not deteriorate and remain at healthy levels, allowing the U.S. economy will be able to sustain a soft landing for the reasons below:

2-1-1. Consumption: Solid consumption outlook based on stabilizing housing costs and improving real incomes

The recent U.S. unemployment rate is at 3.9%, and presenting a slight rebound, but remains close to full employment (3%). According to the Bureau of Labor Statistics, the gap between the number of the unemployed and the number of job openings in the U.S. is 3 million, meaning that demand is still higher than supply.

This is largely due to a decline in labor force participation rate in the U.S., which we believe is a structural trend. Chairman Powell also stated in a Fed statement late 2022 that the U.S. economy is experiencing a "structural labor shortage." In particular, the share of adults aged 55 and older retiring early since the pandemic has increased from 48.1% in the 3Q 2019 to 50.3% in 3Q 2021, many of whom have benefited from the post-pandemic surge in asset prices, accumulating wealth and refinancing to make their mortgages more affordable. Thus, with sufficient assets, we think they are unlikely to rejoin the labor market.

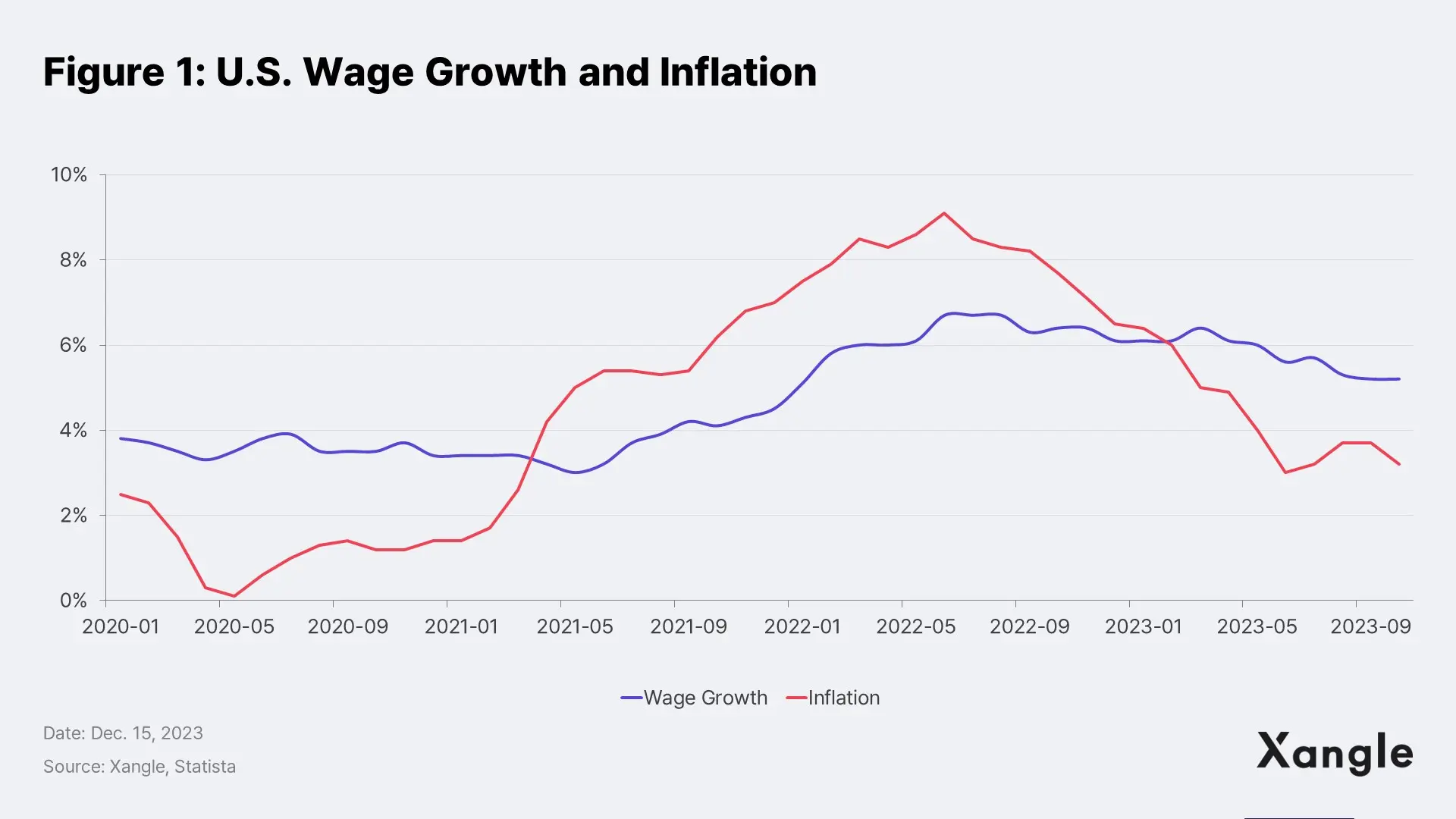

It looks like wage growth is likely to remain at current levels, given the increased bargaining power of workers as a result of these structural changes mentioned above and the rigidity of wages. Also, real wages and purchasing power are likely to be further supported by the recent stabilization of prices across a range of items, including housing and energy. The strong wage growth of the past two years has been diluted by higher inflation, and has not resulted in significant increase in real purchasing power (Figure 1).

The stabilization of housing costs is also noteworthy. Housing accounts for about a third of the CPI basket and is the largest component of U.S. household consumption. This means that stable housing costs are prerequisites for maintaining robust consumption. There are mainly two routes that housing costs can affect household spending:

- Mortgage Rate: Lower mortgage rates reduce interest costs, resulting in increased consumption.

- Wealth Effect: Increased spending due to real estate appreciation.

For homeowners, the burden of housing cost has been significantly eased by (1) lower mortgage interest through refinancing and (2) limited home price declines.

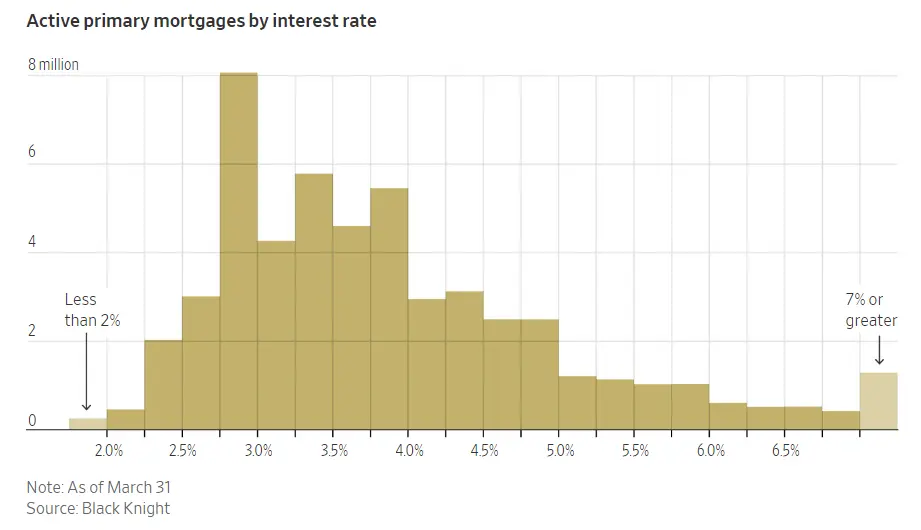

The strain of mortgage interest has subsided since many homeowners refinanced during the low interest rate environment of 2020-2021, which significantly reduced their burden of interest. According to mortgage data firm Black Knight, nearly two-thirds of all mortgages were at rates below 4% (Figure 2), and about 73% were at fixed rates within 30-year maturities at the end of the first quarter of last year. This means that the vast majority of homeowners have effectively locked in a long-term mortgage at rock-bottom rates.

Figure 2: Distribution of mortgage rates across the U.S.

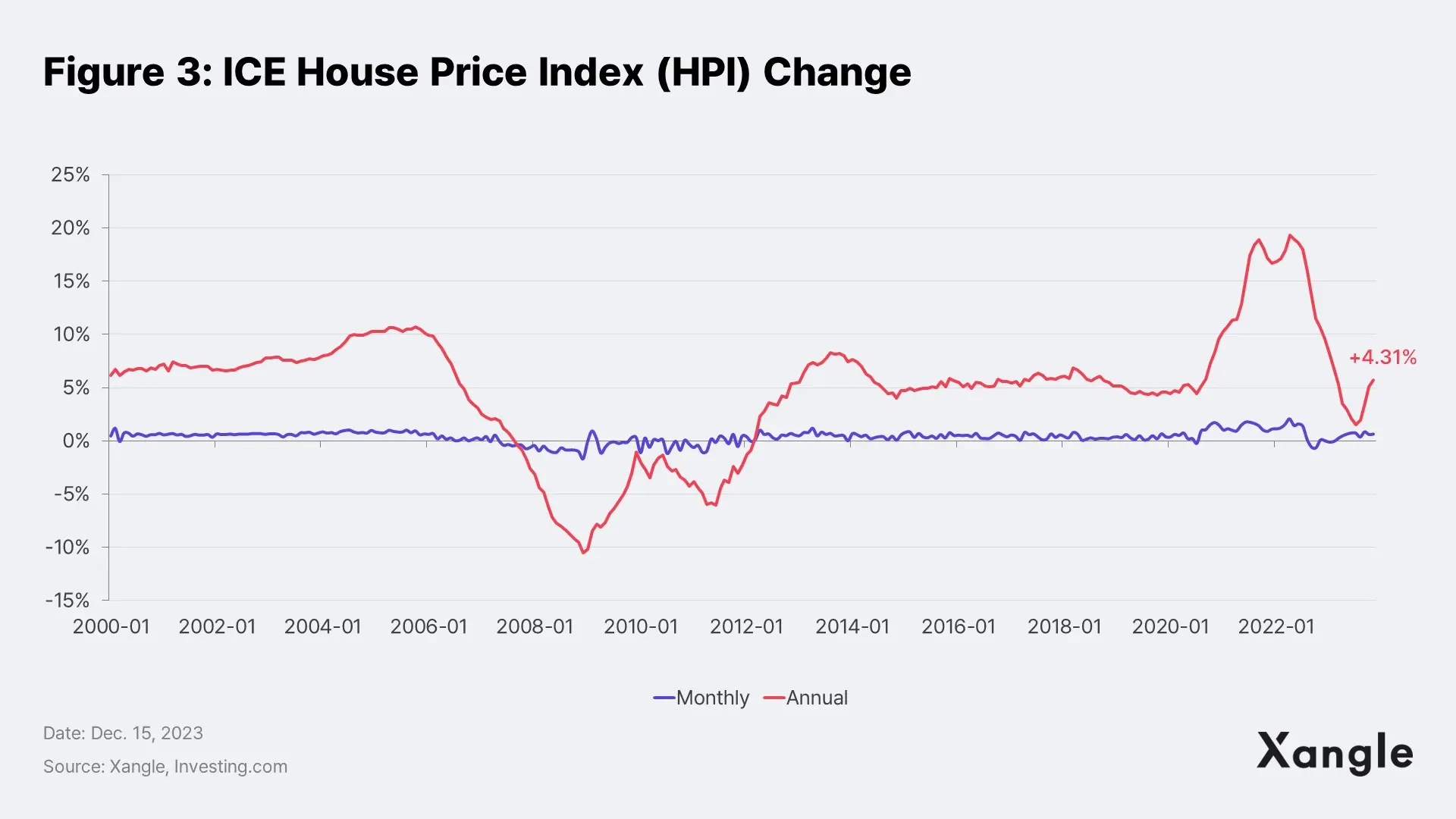

We also believe that house prices have limited downside (Figure 3). This is because while interest rate hikes have caused sharp rise in mortgage rates and significantly dampened demand, there has also been a significant reduction in supply. As we've seen, the majority of all mortgages in the U.S. are set at 30-year fixed rates below 4%, and few people would sell their homes at the cost of resetting their mortgages to a higher rate of nearly 8%. Additionally, many people have moved out of urban centers and into the suburbs due to the introduction of telecommuting during the pandemic, and there is little incentive for them to move elsewhere with the majority of businesses still working from home.

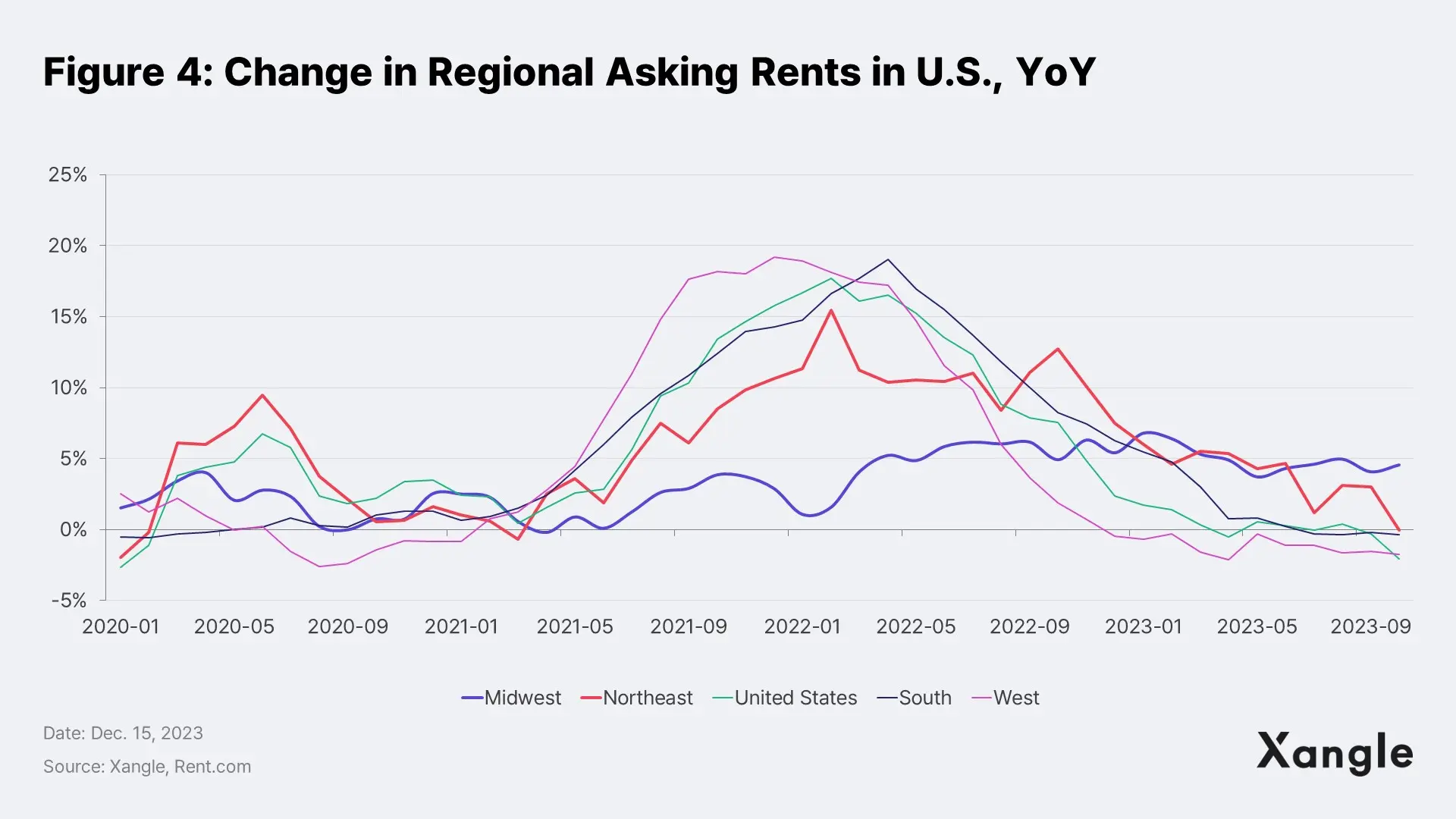

Conversely, for those who don't own a home, housing affordability is easing as rents subside. The national rent growth rate in the U.S. has been subdued since mid-2022 and has been declining rapidly in the second half of 2023, with six consecutive months below 1% due to lower-than-usual demand and rising inventory.

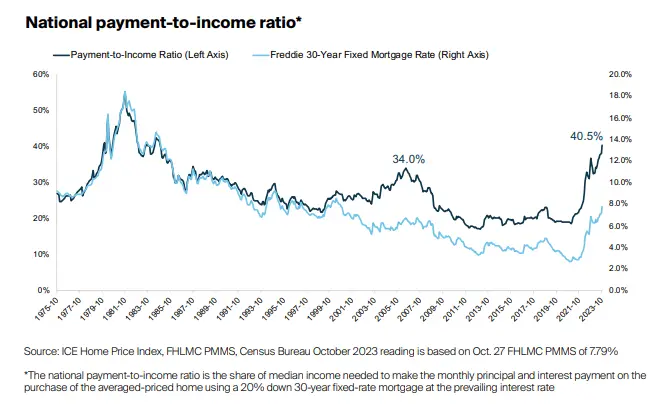

Furthermore, burdensome mortgage rates have created little incentive to buy a home. According to the Federal Home Loan Mortgage Corporation (FHLMC), the 30-year fixed rate was 7.79% at the end of October, putting the monthly principal and interest cost for a buyer to purchase a median-priced home at more than $2,500. That's more than 40% of the median U.S. household income, nearly double the amount year-on-year and the highest since 1984 (Figure 5). And it looks like the situation is likely driving up on goods and services other than housing.

Figure 5: Principal/interest ratio against income across U.S.

That's not to say we'll see a repeat of last year's explosive consumption-led growth. However, we expect consumption activity to remain flat, with improving real incomes and stabilizing housing conditions helping to soften the landing.

※ Risk: Exhausting excess savings

The excess savings of U.S. households accumulated during the pandemic have been steadily declining since the reopening. Increased demand for durable goods such as furniture and vehicles as people worked from home in 2020 and 2021, and increased demand for services such as dining and travel with the reopening in 2022 and 2023, have driven consumption, but we are unlikely to see a further explosive expansion this year as these drivers have been exhausted.

2-1-2. Investment: Manufacturing inventory restocking and reshoring spur investment activity

The manufacturing sector experienced an initial surge in demand during the pandemic due to the adoption of work-from-home and the resulting move of dwellings, but it began to slow down after the reopening and is currently in a downturn. However, we believe that this is a normalization of an overheated manufacturing sector from deferred demand and that the trough has been passed.

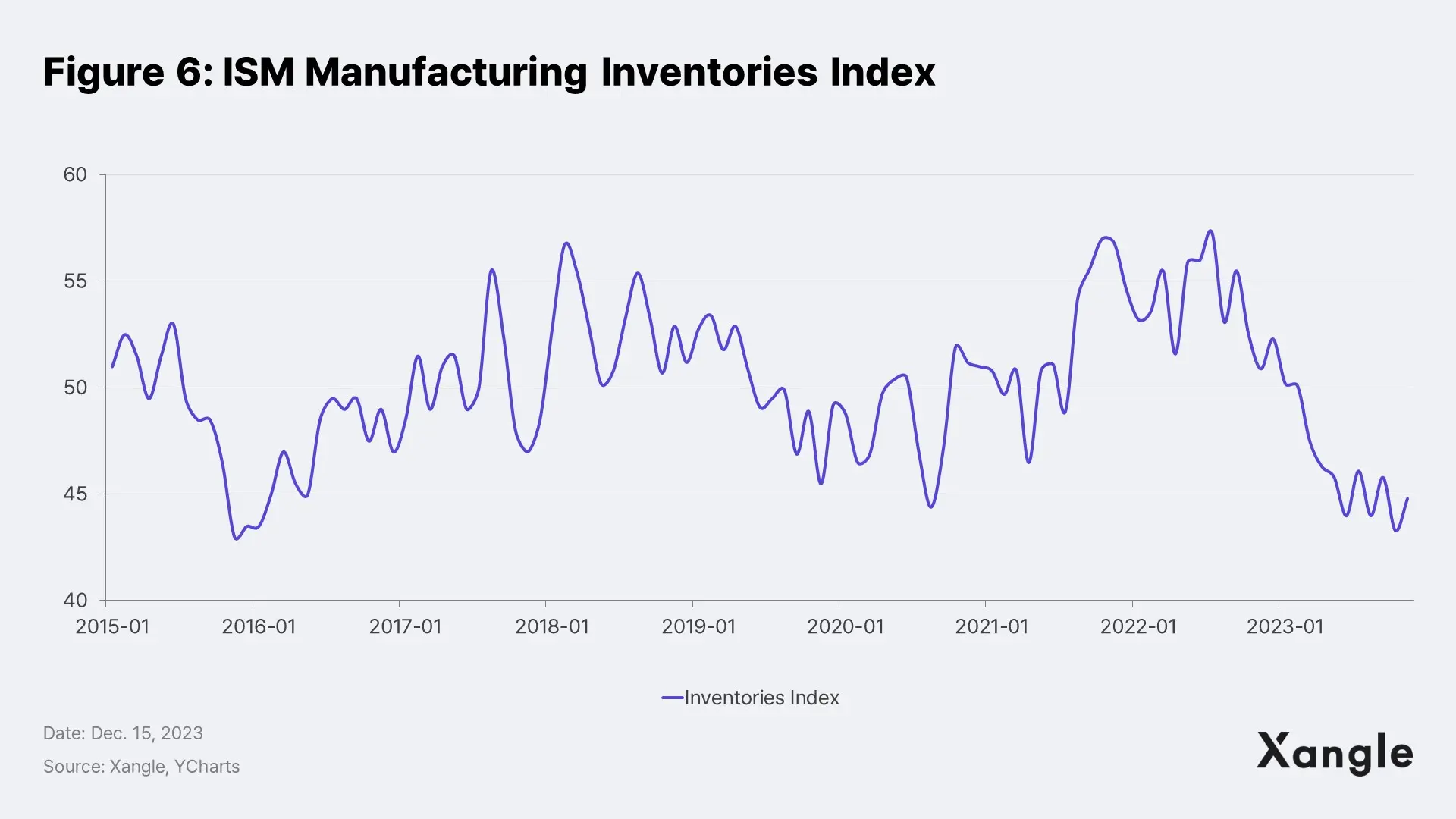

First, the U.S. ISM Manufacturing Inventories Index is now below its post-pandemic level. The combination of the residual effects of supply chain disruptions, labor shortages, and the anticipated recession has kept production activity conservative, while consumption has remained unexpectedly robust, leading to rapidly depleting inventories. We believe that the restocking cycle in manufacturing could spur enough economic activity to dilute the strength of the overall contraction, provided that household consumption does not come off sharply as noted above.

Furthermore, the "re-shoring" movement among many global companies to bring production back to their home countries has become a structural trend, highlighting the need for new infrastructure. According to Bank of America, references to reshoring in S&P 500 earnings releases increased 128% year-over-year in the first quarter of 2023, outpacing the capital markets' biggest buzzword of the year, "artificial intelligence."** We believe the reshoring sentiment in the U.S. will serve as momentum for the manufacturing rebound.

Global supply chain disruptions have emerged as top risk for companies during the pandemic, which brought on unforeseen circumstances such as border closures and transportation disruptions—a direct result of increased reliance on overseas production networks. This prompted many companies to relocate production back home to ensure a stable and fast supply chain.

The recent Russia-Ukraine war, the Israeli-Palestinian conflict, and even the China-Taiwan conflict have further heightened geopolitical risks. Thus, the reshoring trend is likely to intensify as more companies seek to reduce their reliance on overseas supply chains that are sensitive to global events.

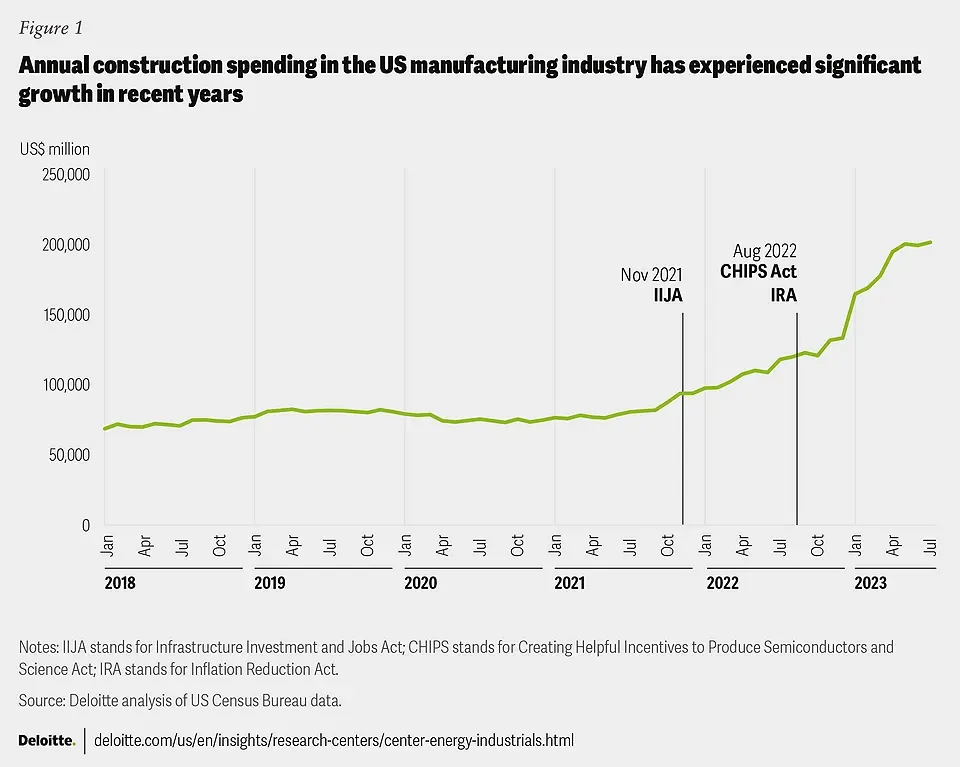

In the U.S., policy support from the Biden administration's Infrastructure Investment and Jobs Act (IIJA), Creating Helpful Incentives to Produce Semiconductors (CHIPS), and Inflation Reduction Act (IRA) bills are providing incentives for reshoring. According to Deloitte, 200 new green manufacturing projects totaling $88 billion have been announced since the passage of the IRA, potentially creating more than 75,000 new jobs. In fact, manufacturing construction spending has increased significantly since the passage of the three bills - IIJA, CHIPS, and IRA (Figure 7). Annual manufacturing-related construction spending is up 70% year-over-year to $210 billion as of July, paving the way for a manufacturing rebound.

Figure 7: Investment volume for construction in manufacturing industry

※ Risk: Interest rate risk and green investment slowdown

As interest rates rise, investment declines along the curve of marginal efficiency of capital. With the minimum cost of capital for companies, i.e., the base interest rate, at 5.5%, companies will be reserved in their investment decisions unless they can expect a return that exceeds it. This could constrain investment activity this year.

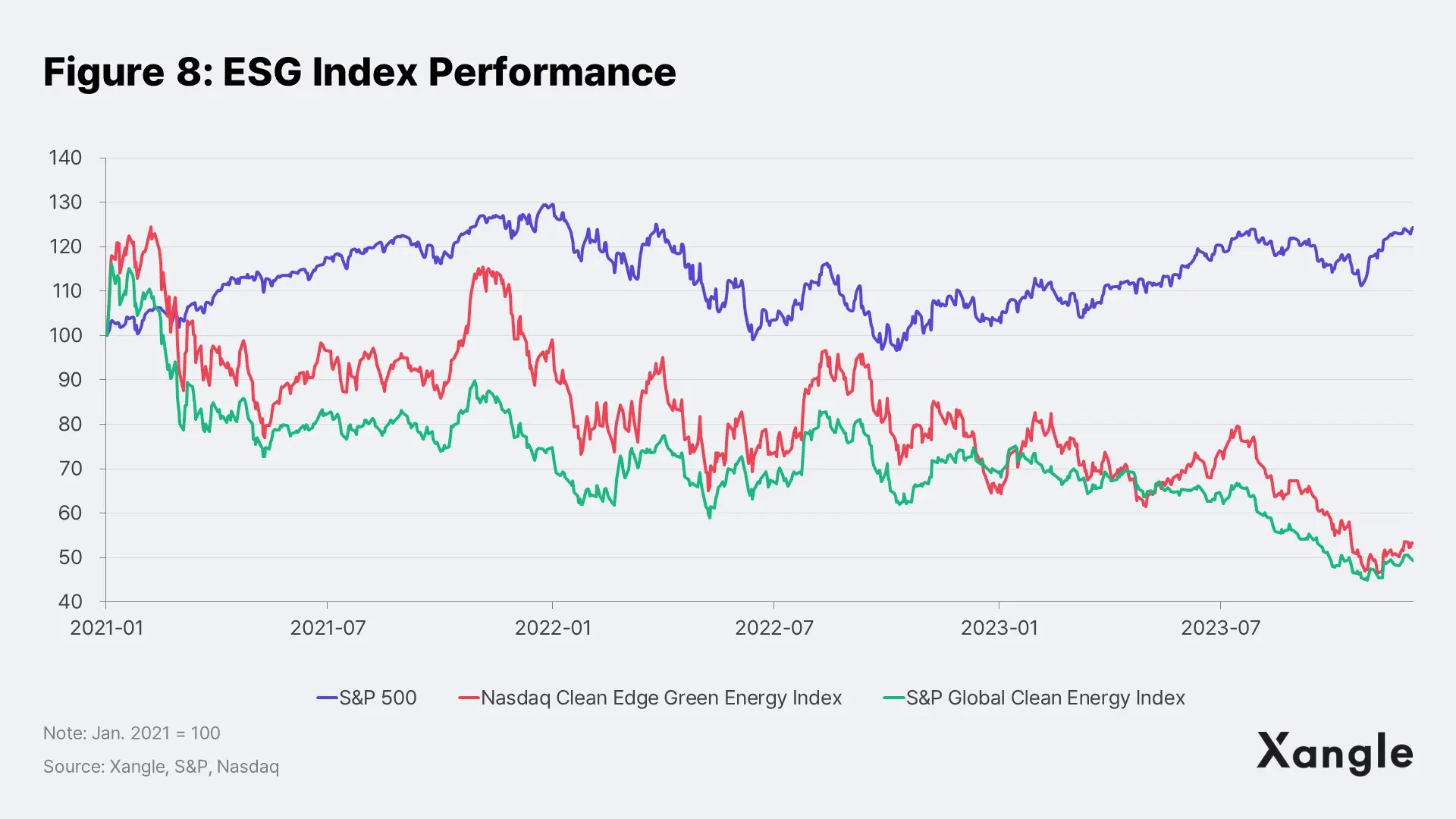

In addition, interest in and investment in the green consumer trends that emerged in the wake of the pandemic is quickly fading. Demand for electric vehicles has fallen short of expectations, major automakers have scaled back production plans in favor of share buybacks, and offshore wind developers have pulled out of one project after another. And the S&P Global Clean Energy Index reflects this and continues to underperform, down 30% this year alone (Figure 8).

2-1-3. Government spending: Significant reduction unlikely before presidential election

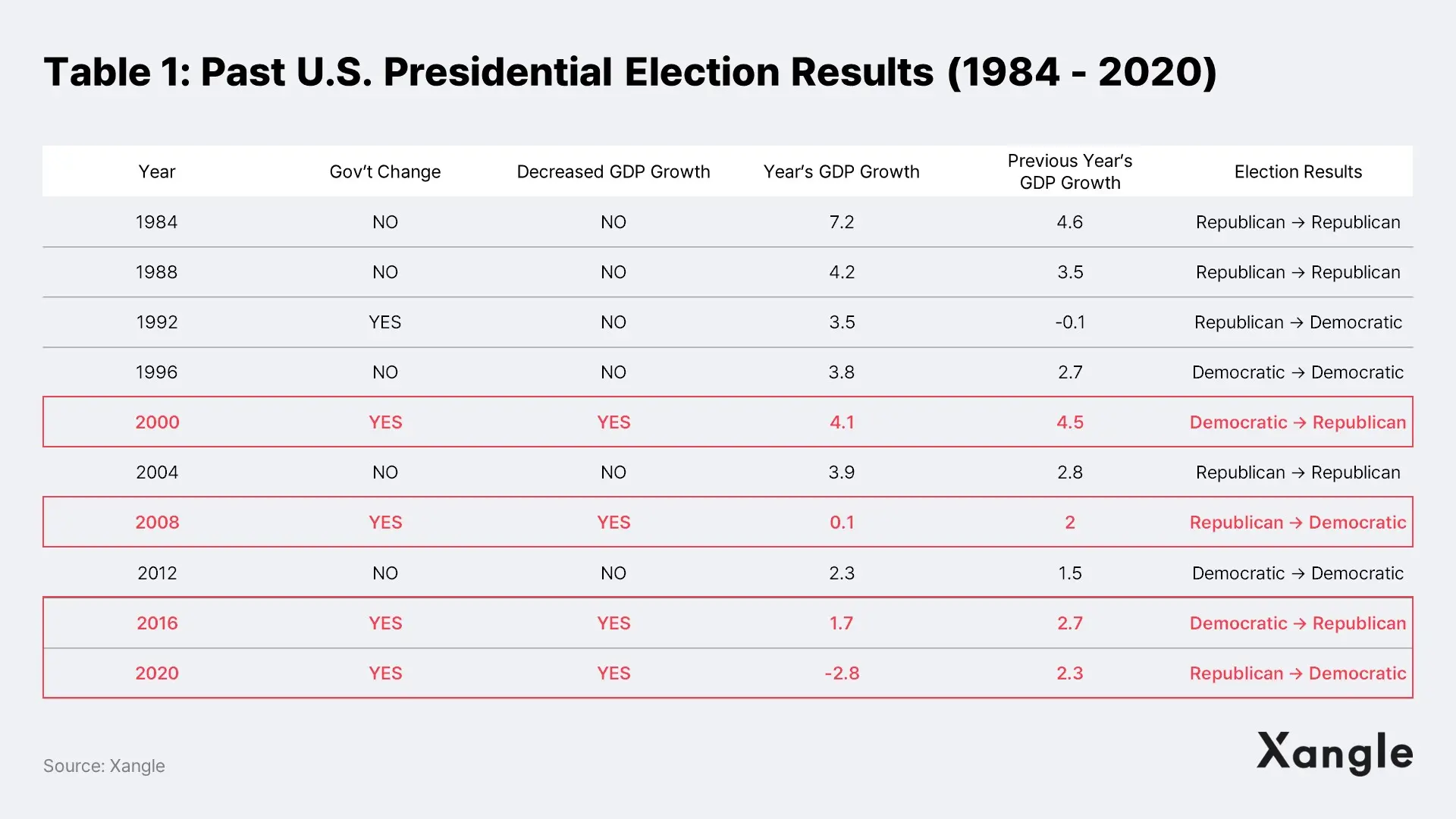

The U.S. presidential election is scheduled for November. Looking back at the results of the last 10 U.S. presidential elections, a change of party in power has always occurred when GDP growth rate in the year of the election was below the previous year's (2000, 2008 2016, 2020) (Table 1). This suggests that voters are very sensitive to the economy, and the Biden administration will want to maintain the solo economic growth trend of the U.S. that it has been enjoying until the end of this year.

The recent outbreak of the Israeli-Palestinian war has led to criticism of failed diplomacy in the Middle East, which has spilled over into social conflicts in the United States. So it is likely that the administration will try to keep voters' attention on the economy as much as possible. As such, we believe it will be difficult for the Biden administration to reduce spending this year.

※ Risk: Fiscal health concerns

According to the U.S. Treasury Department, the U.S. deficit is projected to be $1.7 trillion in 2023. Normally, deficits are considered sustainable if they can support GDP growth and tax revenues through fiscal expansion. But the U.S. is hanging in the balance in that respect. The U.S. federal government's total debt is $33 trillion, nearly 123% of GDP, and the interest burden is too high for it to expand fiscal spending, as it must issue bonds at high interest rates for debt maturing this year and beyond. While symbolic, Fitch's downgrade of the U.S. credit rating in August also reflects concerns about the unsustainability of fiscal policy.

Nevertheless, amid widespread speculation of a slowdown in financial markets, U.S. stock indices, a leading barometer of investor sentiment, have continued to be on an upturn. The S&P 500 reached its highest level since March of 2022, while the Nasdaq Composite hit its highest level since July of last year. The VIX index, a measure of market participants' expectations for future stock market volatility and commonly referred to as the fear gauge, also hit a yearly low, reflecting overall optimism about the U.S. economy.

2-2. Interest Rates: Higher rates persist, but expectations for a cut in 2H remain strong

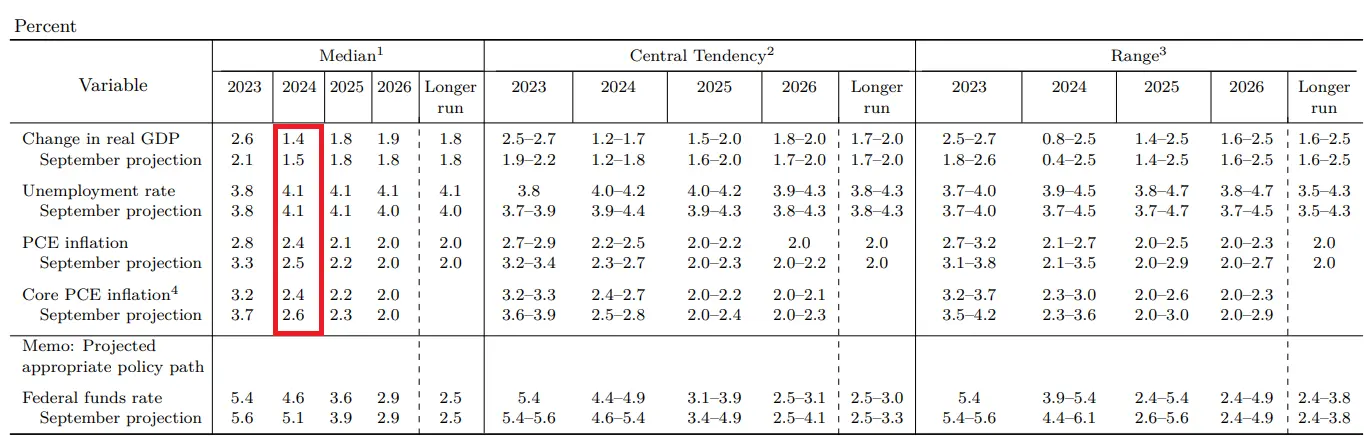

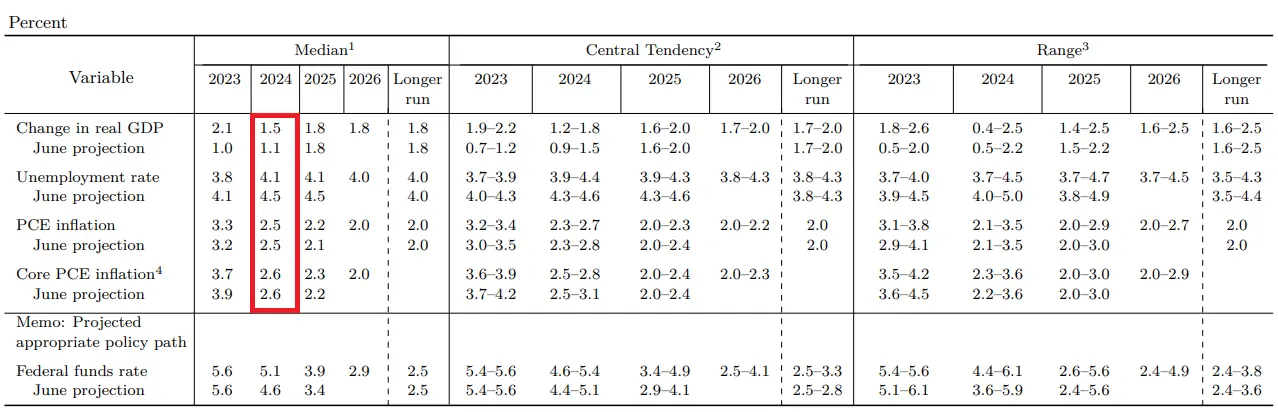

In its September Summary of Economic Projections, the Fed raised its 2024 GDP growth forecast and lowered the unemployment rate. This assumes a soft landing for the U.S. economy, and it's hard to imagine a radical rate cut to stimulate the economy under this scenario, so rates will remain high for longer. However, we believe that the expectation of a rate cut in the second half of the year remains valid (Figure 9).

Figure 9: Summary tables of the Fed's September (above) and December (below) economic projections

Expectations for a rate cut should be dealt with care. While markets recently cheered when hawkish Fed governor Christopher Waller hinted at a possible rate cut in the coming months, with the probability of a March rate cut as reflected in CME fed funds futures breaking through the 50% mark, we view this as "selective attention". Given the Fed's repeatedly hawkish rate hike signals to combat inflation, we believe the market was unusually sensitive to news of a possible pivot. After Waller's comments, New York Fed President John Williams and Chair Powell both said in public that monetary policy would remain accommodative for the time being, a sentiment drowned out by market jubilation. But at the end of the day, the Fed's ultimate goal is to stabilize prices and employment (stabilize, not stimulate), not stimulate the economy.

Inflation is coming down. The U.S. CPI for October, released in mid-November, appears to be on a steady downward trajectory at 0% MoM and 3.2% YoY. Service prices, which have been a stubborn inflation driver, are subsiding as the labor market tightness eases a bit. Growth in housing price is also slowing due to falling rents. In the case of commodity prices, mainly durable goods, the Wall Street Journal recently reported that we are moving beyond disinflation (slowing price growth) to deflation (falling prices). Nevertheless, given the slowdown in the economy and unemployment below 4%, inflation is likely to settle into the mid-2% range by the end of 2024, with the Fed's 2% target unlikely to be fully achieved this year.

On the employment front, the U.S. is likely to see modest job growth in 2024, with unemployment growth constrained by a structural decline in the labor force and the economic soft landing.

Under the soft-landing scenario, we believe the Fed will begin to taper in the second half of 2024, as suggested in the September dot plot. While rates would remain "constrained" in the mid-to-high 4% range, the Goldilocks achievement of the U.S. economy and the re-injection of liquidity into the market would provide a foothold for a revival in investor sentiment.

2-3. Market drivers: The perfect storm of one-offs and structural momentum

With investor sentiment expected to remain largely intact from a macroeconomic perspective, there are plenty of ingredients to trigger the cryptocurrency market this year.

As mentioned in the introduction, the crypto market is in the early stages of establishing itself as a distinct financial asset class. This means that market endogenous variables will come into play, and we expect that market participants will start to pay attention to the unique features of cryptocurrencies, such as decentralization and censorship-resistance, and start to seriously consider investing in cryptocurrencies as an alternative to fiat currencies, rather than just as a speculative asset.

2-3-1. One-offs

A. Bitcoin spot ETF approval

The SEC's final response to BlackRock's application for Bitcoin spot ETF was due in January, with final approval expected in 1Q24. In October, the U.S. Court of Appeals for the D.C. Circuit reversed the SEC's denial of Grayscale's application for a spot Bitcoin ETF, effectively ending the litigation, significantly weakening the case for denying approval to other managers. While the 2000s saw the launch of ETFs for a variety of non-equity asset classes, including gold (SPDR Gold Trust; 2004), crude oil (United States Oil Fund; 2006) and emerging market bonds (iShares J.P. Morgan USD EM Bond ETF; 2007), we believe the approval of the Bitcoin spot ETF marks a milestone for an asset class less than 20 years old to be ETFized and recognized as a financial asset. This will significantly improve access to Bitcoin investing.

First, because Bitcoin ETFs are regulated by financial authorities such as the SEC, institutional investors will not need to hold separate private keys, and the risk of hacking or theft will be significantly reduced because asset managers will have surveillance sharing agreements with cryptocurrency exchanges. Logistical burdens will be greatly reduced.

In addition, individual retirement accounts (IRAs) and corporate pension accounts (401Ks) that are restricted from investing in cryptocurrencies will be able to gain Bitcoin exposure through ETFs. The total size of IRA and 401K funds in the U.S. is approximately $22 trillion, so even a 0.5% portfolio allocation would represent an inflow of $100 billion. Given that Bitcoin's market capitalization is currently around $800 billion, we can expect modest upside.

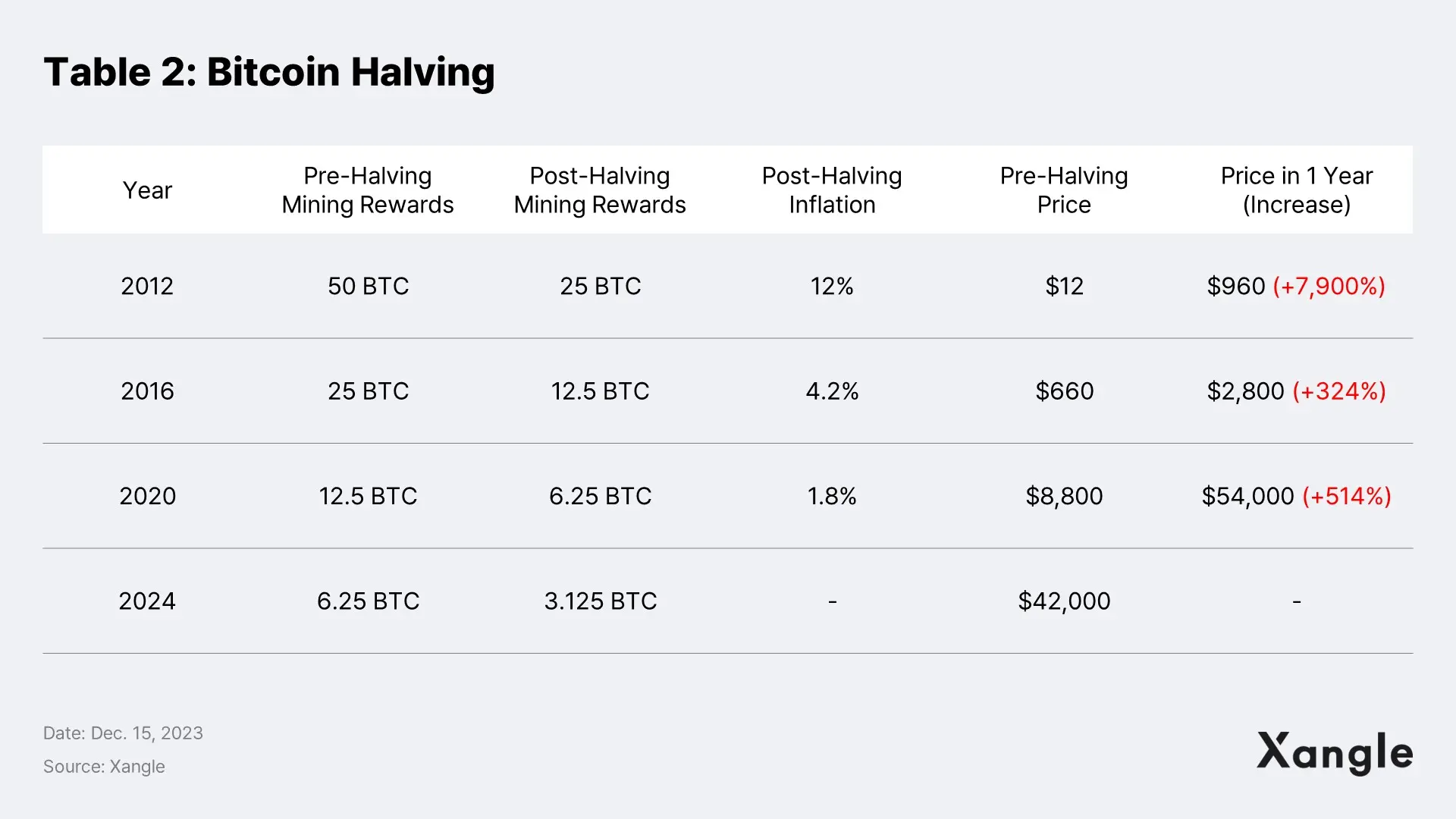

B. Halving

Since Bitcoin was first issued, there have been a total of three halving events—2012, 2016, and 2020. A halving is when the reward for mining is halved according to the code embedded in Bitcoin's protocol, which naturally drives up the price as the supply shrinks (Table 2).

Looking back over the past three halving cycles, the price has risen in response to reduced supply. However, the upcoming halving in 2024 will only have 3.125 mining rewards, which is an absolute drop in supply compared to past halvings. As such, it's hard to expect a substantial price increase due to the reduced supply.

However, we believe that the combination of historically rising halving prices, the approval of a spot ETF, and expectations of lower interest rates will act a catalyst for capital inflows into the crypto asset market.

2-3-2. Structural momentum

A. Centralization of funds within TradFi system

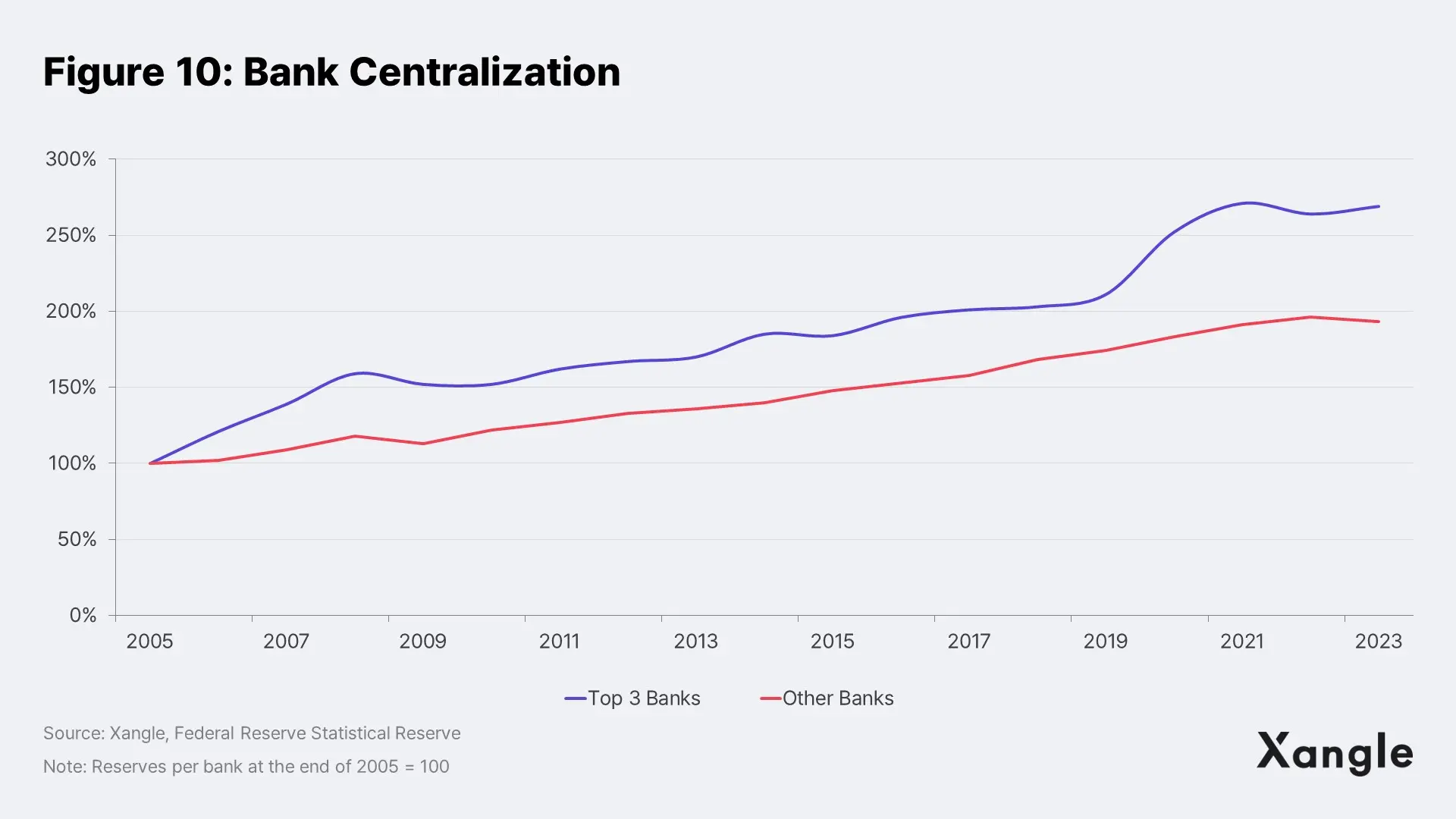

In the 14 years since the Fed first introduced quantitative easing in the wake of the 2008 financial crisis, a sustained low interest rate environment has injected massive amounts of liquidity into the market, but it has been asymmetrically channeled to a small number of large institutions. Looking at the number of commercial banks in the U.S., both the number of banks and the size of their holdings have increased significantly, from 1,563 banks/8 USDt in 2005 to 2,116 banks/22 USDt in 2023. Average reserves per bank roughly doubled from 5 USDb in 2005 to 10 USDb in 2023, with the top three banks (JP Morgan Chase, Bank of America, and Citibank as of 2023) nearly tripling their average reserves from 934 USDb to 2.5 USDt (Figure 10).

The flight to large financial institutions is expected to accelerate since the beginning of 2023. Since 2022, the Fed's aggressive rate hikes have led to the collapse of a number of mid-sized banks, such as Silicon Valley Bank (SVB), that had overextended their long-term debt positions, which has significantly undermined confidence in small and mid-sized banks. As a result, a large amount of individual and institutional money has moved out of small and mid-sized banks and into large financial institutions—a trend that is likely to continue. At the time of SVB's collapse, the Financial Times reported that "executives at large financial institutions, including JPMorgan Chase and Citigroup, are facing the biggest movement of deposit in more than a decade, speeding up the ‘onboarding’ process to accommodate it.”

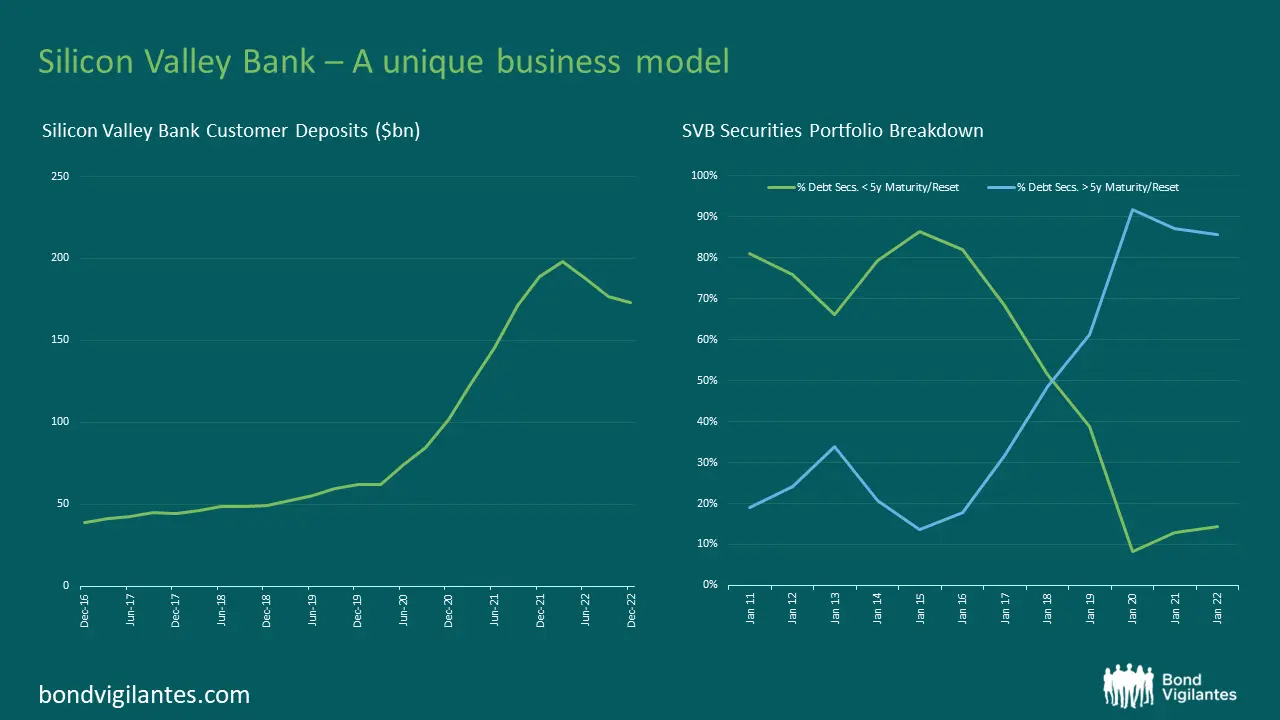

Behind SVB's failure is a dissonance between U.S. administration and central bank policies. The SVB was able to increase its reckless investment in long-term debt outside of regulatory oversight because the Economic Growth, Regulatory Relief, and Consumer Protection Act, passed by the Trump administration in 2018, deregulated small and mid-sized banks by rolling back the Dodd-Frank Act. The Dodd-Frank Act, which was introduced in response to the 2008 financial crisis, tightened regulation of financial institutions with more than $50 billion in assets, by raising the threshold to $250 billion, allowing smaller institutions like SVB to fall off the radar. In fact, if we look at SVB's portfolio composition, it wasn't until 2018 that the share of long-term bonds (>5 years) exceeded the share of short-term bonds (<5 years) (Figure 11).

Figure 11: SVB customer deposit and portforlio

While bloated long-term debt holdings increased the duration risk (sensitivity to interest rate changes) of many institutions, the Fed may not have fully grasped the changes in the balance sheets of small and mid-sized banks resulting from the administration's policy changes or underestimated the ripple effect. Major small and mid-sized banks split, and bank runs occurred. And while the Fed belatedly established the Bank Term Funding Program (BTFP), it had the effect of funneling funds to a small number of Too-Big-to-Fail institutions.

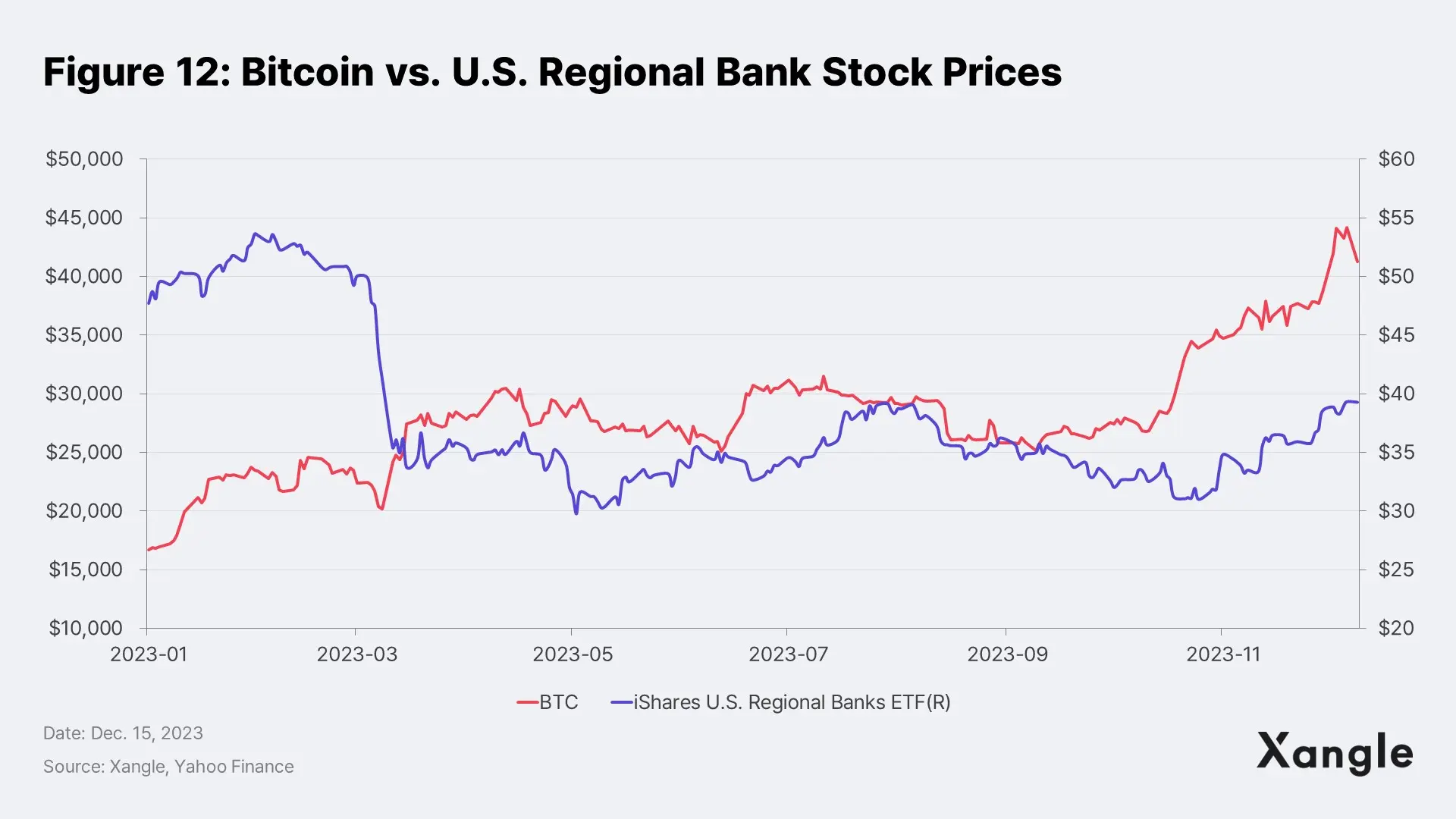

There are a growing number of structural factors that could lead to the concentration of market liquidity in a small number of institutions, raising the systemic risk of a cascading collapse of the entire TradFi system, as happened during the global financial crisis. We believe that interest in cryptocurrencies will only grow as this caution spreads, which is supported by the inverse correlation between small and mid-sized bank share prices and the price of Bitcoin in 2023 (Figure 12).

B. Undermining U.S. fiscal health

The disconnect between the U.S. administration and central bank policy is also undermining U.S. fiscal health. Whereas the U.S. federal government and the Fed worked together to stimulate the economy with both fiscal and monetary expansion in 2020 and 2021, the Fed has recently gone it alone, pushing the federal government's interest burden to unsustainable levels.

The U.S. federal debt is approaching 97% of GDP due to a surge in fiscal spending, including the $1.9 trillion American Rescue Plan (ARP), the largest stimulus package ever approved by the Biden administration in 2021. When the ARP was passed, the federal government was able to issue debt relatively easily until 2021 because the Fed was maintaining zero interest rates, but interest costs now must be considered as it began to tighten monetary policy.

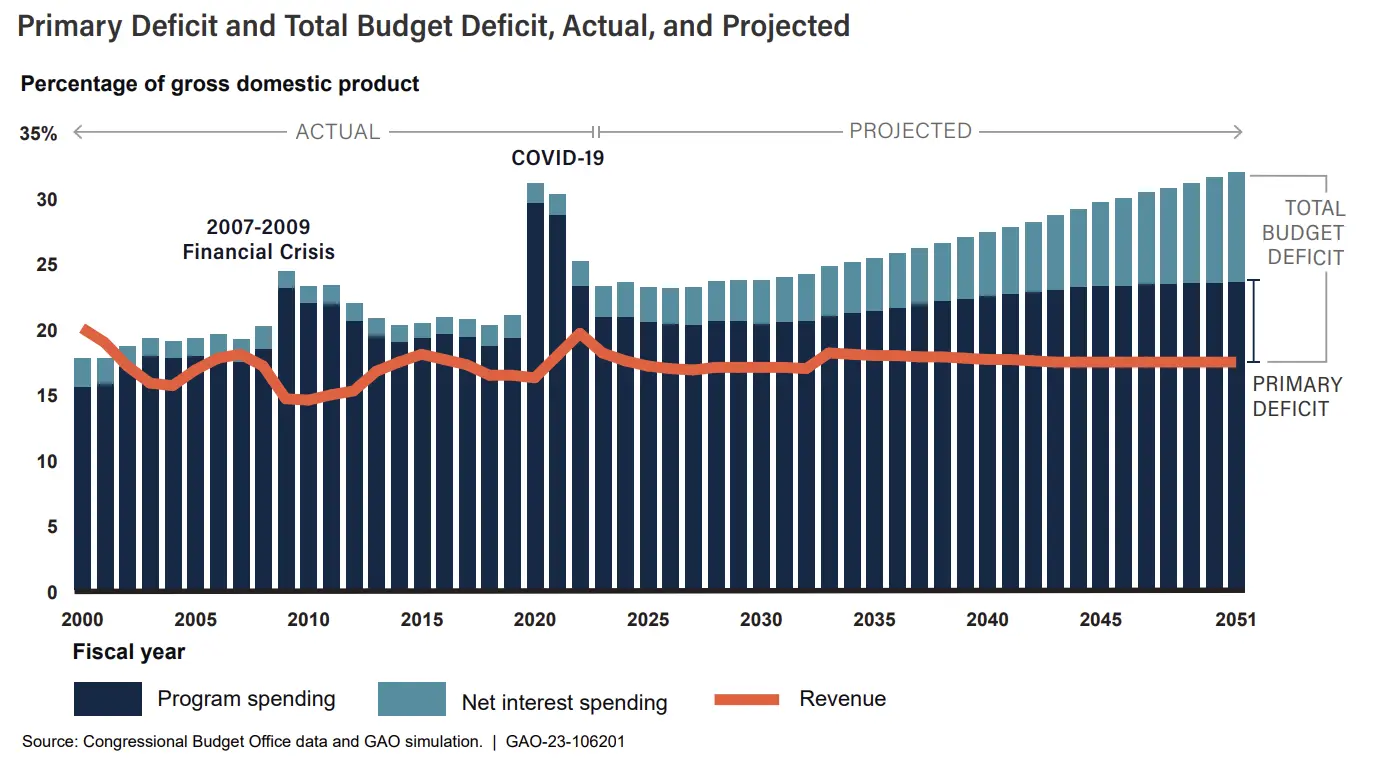

According to the U.S. Government Accountability Office, the federal government's average net interest expenditure over the past two decades has been just 1.5% of GDP, but it is projected to rise to 8.4% by 2051, reaching a whopping $6.6 trillion, given the rapid growth of the national debt in recent years and the continuation of high-interest monetary policy (Figures 13,14).

Figure 13: U.S. debt to GDP ratio

Figure 14: U.S. debt principal and interest

As we've mentioned, the Biden administration is unlikely to make significant reductions in fiscal spending, given the upcoming presidential election in November. We also analyze the Treasury Department's announcement in November that it will slow down the issuance of long-term bonds with 10- and 30-year maturities and increase short-term bonds as a strategy to maintain fiscal spending but shorten the duration.

In late October, the 10-year U.S. Treasury yield rose to its highest level since August 2007, just before the global financial crisis, as market concerns about the clash between the administration's stimulative stance (continued long-term debt issuance) and the Fed's tightening stance (continued rate hikes) led to a massive sell-off in long-term bonds. Thus, concerns about the U.S. fiscal position and, by extension, the hegemony of the dollar, could provide momentum for alternative crypto markets.

C. Less predictability in monetary policy

The Fed aims to provide financial markets with a clear and consistent message on the direction of money policy through forward guidance, shaping market expectations and stabilizing the economy. Its communications strategy of being as transparent as possible in providing insights into the decision-making process, including the direction of the policy rate, its expected duration, and an analysis of the state of the economy, serves to instill confidence in the efficacy of monetary policy and encourage orderly response from markets. Trust is a critical component of the effectiveness of monetary policy because it influences how market participants interpret and react to Fed signals.

In the same vein, the Fed has been sending a consistent message of tightening to the markets as it has been raising rates since 2022, stating that intense tightening is necessary to fight inflation and hinting at the possibility of further hikes despite the lowering trend of inflation. However, when the ripple effect of the rate hikes led several regional banks failing and unexpected signs of cracks in the financial markets, the Fed hastily created the BTFP to provide liquidity to failing banks. Essentially, the Fed deviated from its previously consistent message of tightening to stabilize prices and reinjected liquidity in response to market concerns. This decision undermines market confidence in the Fed's forward guidance and calls into question its ability to maintain a transparent and predictable monetary policy. This explains why markets are paying more attention to Waller's dovish comments, even as Chairman Powell continues to deliver a message of austerity.

While the SVB outbreak brought the Fed's inconsistency directly to the forefront with its conflicting policies, the Fed's credibility has actually been under scrutiny since Powell took office. A study this year by the Center for Economic Policy Research found that "market volatility is three times higher during press conferences held by current Chair Jerome Powell than those held by his predecessors, and they tend to reverse the market’s initial reactions to the [FOMC]’s statements." Prior to the pandemic, Powell's press conferences typically reinforced the market's interpretation of the FOMC statement, and the market moved in the same direction as the initial reaction to the statement during the press conference. For example, if the market interpreted the FOMC statement as hawkish and stocks fell, the chairman's comments during the press conference supported that interpretation, and stocks fell further. However, since the pandemic, stock and bond markets have tended to move in the opposite direction during the press conference compared to the initial reaction to the FOMC statement.

If we look at the market's reaction to major U.S. economic data releases since 2022, we have seen a "good is bad & bad is good" phenomenon, where even when a release is generally considered bad, such as rising unemployment, the market interprets it as "the Fed will pivot soon to counteract the recession, which is good for stocks" and the market actually rises. We believe this is a result of growing doubts about the consistency of Fed's policy. A loss of confidence in the central authority in charge of monetary policy means that confidence in the soundness of the dollar is being undermined, making cryptocurrencies more attractive.

3. Evolving Regulatory Landscape: Ushering in a More Favorable Environment with Promising Opportunities

2023 marked a pivotal moment as regulatory jurisdictions took a clear shape, notably in the Western nations and key Asian financial hubs as they actively seek to incorporate crypto assets within a regulatory framework. While the global legalization of virtual assets is still in its early stages, promising strides have been made, especially with the European Union (EU) leading the way by implementing the Markets in Crypto Assets (MiCA) as a foundational law for virtual assets. This has set the stage for other major countries to follow suit, presenting expansive business opportunities.

3-1. Global regulatory outlook: Unlocking opportunities through comprehensive legalization of crypto assets

The legislative developments in key international jurisdictions hold profound implications for Korea, underscoring the need for vigilant observation. A retrospective analysis of regulatory landscapes in the EU, the United States, and Japan offers valuable insights into the future trajectory.

3-1-1. EU: MiCA steers crypto assets towards legal clarity

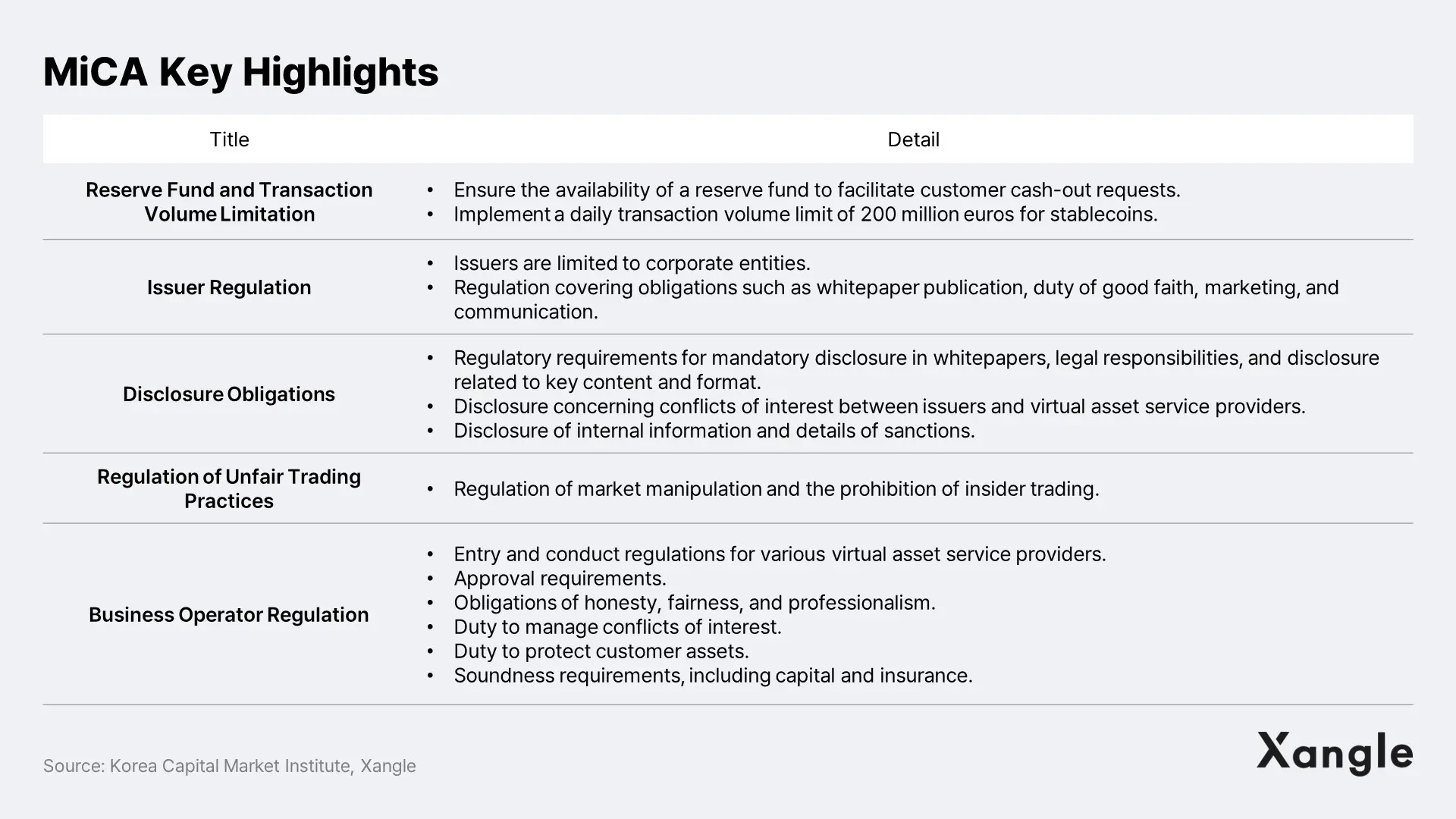

In a significant move on September 24, 2020, the European Commission (EC) proposed MiCA, a comprehensive legislative framework aimed at providing legal stability to crypto assets. MiCA primarily targets stablecoin and crypto-asset service providers operating outside existing regulatory frameworks. The bill, with approval from EU Finance Ministers on May 16, 2023, is set to be implemented gradually from July 2024 to 2026. MiCA stands as the world's inaugural regulatory law governing the virtual asset market, focusing on fostering innovation, ensuring fair competition, protecting investors, and upholding market integrity and financial stability. This legislative milestone is particularly crucial in preventing lapses in investor protection and addressing Anti Money Laundering (AML) violations, as underscored by events like the FTX exchange bankruptcy. While some critics argue that MiCA's stringent regulations on cryptocurrency issuers and stablecoins may initially impede business activation, the silver lining lies in the establishment of a stable regulatory environment. This stability not only addresses the shortcomings revealed in past events but also presents an opportunity for traditional financial players to enter the market with confidence. Ultimately, MiCA serves as a foundation for sustained growth within the ecosystem by providing the necessary protective measures and regulatory clarity.

Key Takeaways

- MiCA stands as the European Union's cornerstone legislation for the entire crypto-asset industry, including stablecoins.

- Crypto-assets are neatly classified into three categories: utility tokens, asset-backed tokens, and e-money tokens. Specific definitions for asset-backed and e-money tokens aim to regulate stablecoins tied to fiat currencies, mitigating risks spilling into traditional markets.

- MiCA imposes strict guidelines on virtual asset white papers. Failure to meet the prescribed format will result in the regulator withholding authorization for trading in the asset.

- The legislation prohibits the offering of interest on asset-backed tokens and e-money tokens containing stablecoins. This restriction may impact the ability to earn interest on stablecoin deposits. However, MiCA's stance on decentralized finance (DeFi) services like Abena Compound remains uncertain, as it does not explicitly define DeFi.

3-1-2. U.S.: Anticipated rise in exchange regulations coupled with jurisdictional separation for legal stability

The U.S. acknowledges the intertwined nature of crypto exchanges with traditional asset markets, prompted by the FTX bankruptcy's ripple effect on Silvergate Bank and Silicon Valley Bank last year. Recognizing the imperative to safeguard exchange-based investors, the U.S. is actively leveraging regulatory influence to establish a robust framework.

Key regulatory bodies, including the Securities and Exchange Commission (SEC), the Commodity Futures Trading Commission (CFTC), and the U.S. Department of Justice (DOJ), have initiated legal actions against major centralized exchanges such as Kraken, Coinbase, and Binance.

In a recent development, Binance, the world's largest exchange, pleaded guilty to charges, including violations of the Bank Secrecy Act (BSA) and the International Emergency Economic Powers Act (IEEPA). This resulted in a substantial fine of $4.3 billion (approximately RMB 5.5 trillion), compelling CEO Changpeng Zhao to resign. The regulatory landscape is expected to persistently evolve until the cryptocurrency market is fully integrated into the existing regulatory regime under the jurisdiction of the SEC and CFTC. While some foresee potential constraints on growth, this regulatory evolution seeks to ensure legal stability and protect investors in this dynamic financial landscape.

However, the United States is positioned to develop a distinct cryptocurrency framework bill, drawing inspiration from MiCA, as relying solely on prosecuting exchanges without additional legislation has inherent limitations. The ambiguous jurisdictional landscape among key regulators, namely the SEC and CFTC, has been a contentious issue. To address this, industry stakeholders advocate for consistent legislation to create a secure and reliable legal framework for investors and participants.

Recent legislative strides, such as the Blockchain Regulatory Certainty Act and The Financial Innovation and Technology for the 21st Century Act, enacted in July 2023, aim to dispel regulatory uncertainty by defining the application of regulation based on transaction engagement. The Blockchain Regulatory Certainty Act is a proactive step to tackle uncertainty and encourage innovation in the blockchain sector. It specifies that blockchain developers and service providers not holding users' cryptocurrency funds are not to be classified as financial institutions. Simultaneously, The Financial Innovation and Technology for the 21st Century Act categorizes digital assets into three groups: digital commodities, restricted digital assets, and stablecoins. It proposes that the CFTC oversees digital commodities, while the SEC oversees restricted digital assets. Despite these advancements, the Clarity for Payment Stablecoins Act of 2023, addressing stablecoin regulation, did not pass. Consequently, discussions surrounding stablecoin regulation are expected to persist in the future.

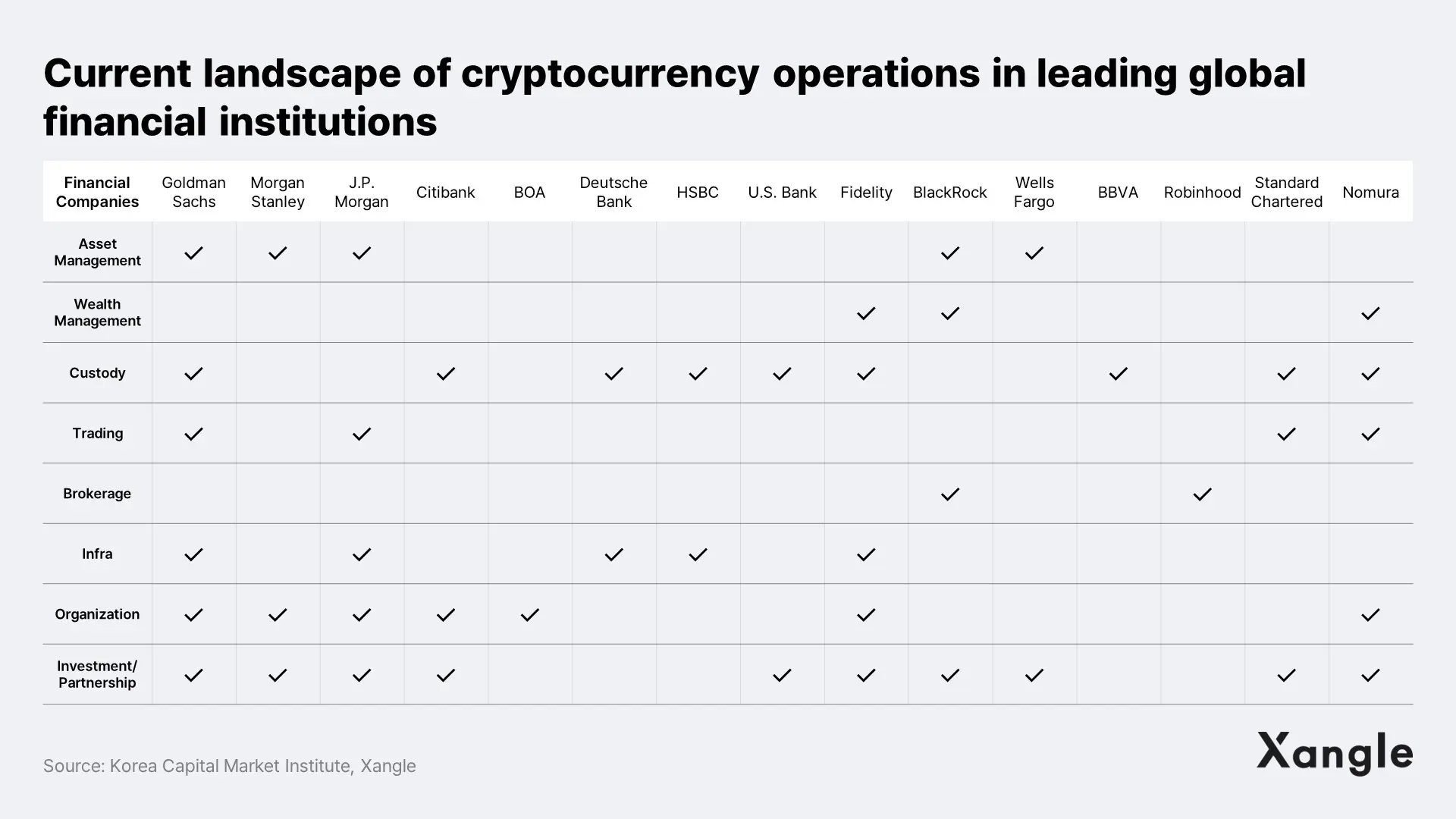

Meanwhile, U.S. financial authorities wield significant influence over the cryptocurrency market, poised to positively impact the financial industry seeking entry into this dynamic space. In anticipation of market institutionalization, major financial institutions are actively positioning themselves within the virtual asset industry. Companies like JPMorgan have already made direct or indirect forays into the crypto market, with plans to further intensify their presence upon system finalization.

Furthermore, a dozen major asset managers, spearheaded by BlackRock, the world's largest asset manager, await approval for bitcoin spot Exchange-Traded Funds (ETFs). Experts in the ETF space anticipate a collective approval by the SEC in January of 2024, signaling a transformative shift. Complementing this trend are various initiatives enhancing the virtual asset industry landscape, including the expansion of commercial activities in regulatory response domains such as operating virtual asset exchanges and supporting the issuance of white papers. Given the profound impact of U.S. regulatory decisions on Korea, vigilant monitoring of future regulatory directions is imperative.

Key Takeaways

- The U.S. is laying the groundwork for a regulatory framework centered on major exchanges.

- Anticipate a sustained, moderately strong regulatory influence from financial authorities during the ongoing transition, potentially tempering growth in the crypto market.

- The unresolved separation of regulatory jurisdictions among existing institutions presents a risk for companies aiming to engage in the crypto market.

- The Financial Innovation and Technology for the 21st Century Act is poised to bring clarity to regulatory authorities like the SEC and CFTC, mitigating uncertainty and bolstering legal stability.

- Traditional financial institutions, including major firms, are progressively making inroads into the crypto space.

3-1-3. Japan aiming to energize the market through crypto-friendly regulations

Following the inauguration of the Kishida administration, Japan has demonstrated a pro-Web3 stance at the core of its new capitalist policy. This shift is reflected in the country's revised regulatory approach, emphasizing the facilitation of emerging businesses like NFTs and metaverses through substantial deregulation. In July 2022, Japan elevated Web3 to a central position in its national growth strategy, establishing the Web3 Policy Office to oversee developments in the blockchain industry.

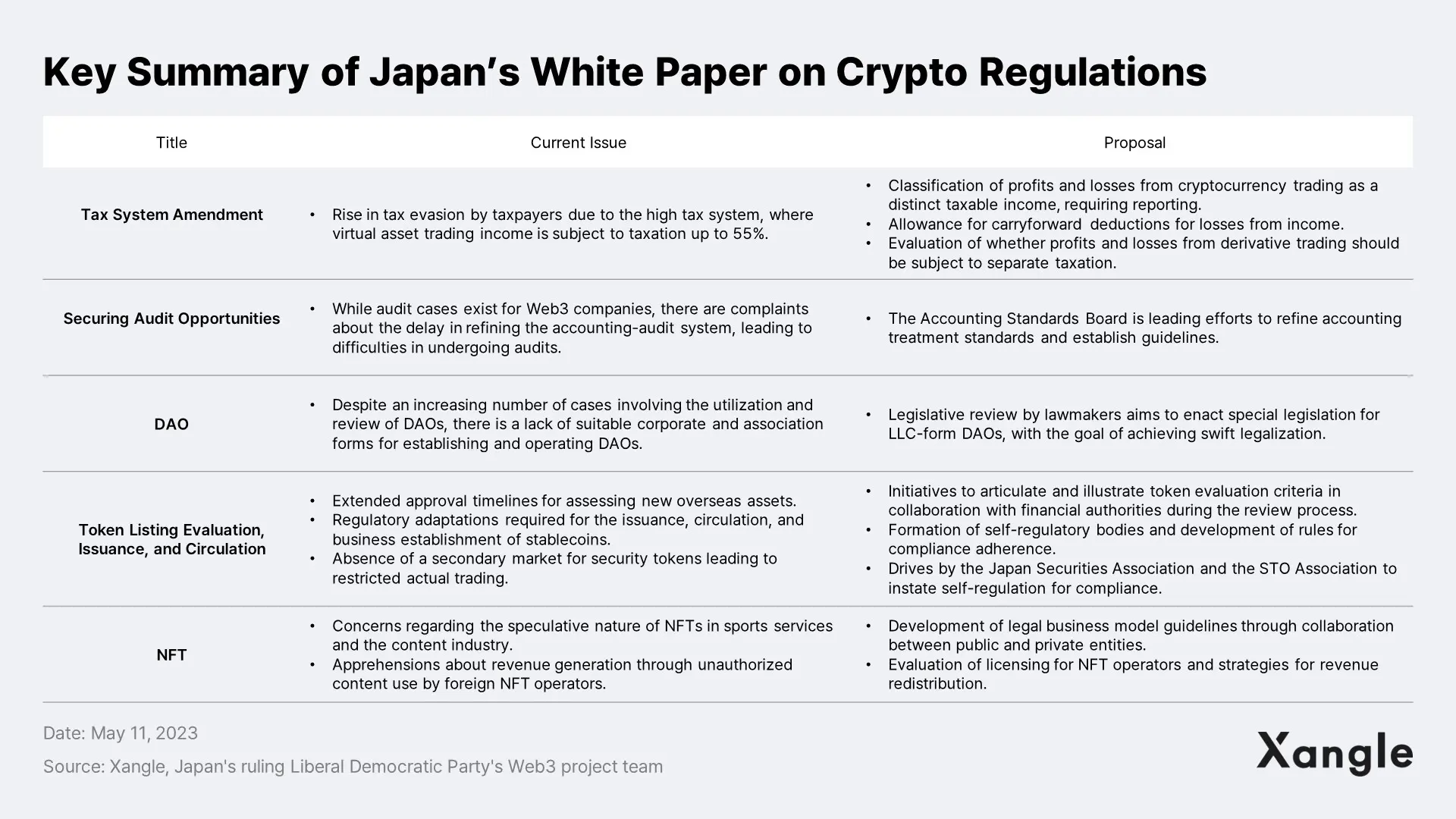

Building on various recommendations, the government-approved the white paper on crypto and blockchain regulations in April 2023. This approval signals an active effort to support ecosystem participants whose growth has been hindered by stringent regulations. Additionally, the Japanese government has implemented measures to alleviate the burden on market participants, proactively preparing for the burgeoning Web3 market. Innovative support measures include permitting the issuance of stablecoins, a 20% reduction in the personal income tax rate, and exempting corporate taxes on tokens self-issued by corporations. With this proactive approach to crypto and corresponding regulations, the Japanese crypto industry experienced significant progress in 2023.

Moreover, a proposal for a bill allowing startups to issue crypto-assets surfaced in September, indicating a potential policy addressing the scalability of new investment funds for startups in 2024. The regulatory clarity provided by the government has not only spurred the involvement of startups but has also prompted large corporations to actively enter the market. A notable instance of this trend is the collaboration between Progmat (a subsidiary of MUFG managing digital asset issuance), a major player in the Web2 financial space, and XRP. Additionally, two of Japan's largest general merchandisers, Mitsui C&T and Sony Group, have ventured into new businesses utilizing blockchain, exemplifying the growing Web3 activity.

Key Takeaways

- In April 2023, the government's approval of the Web3 White Paper unveiled tax incentives and other measures aimed at fostering the industry.

- Legislation facilitating stablecoin operations passed, bringing Japanese financial firms one step closer to issuing and brokering stablecoins. Establishing a stable stablecoin issuance and distribution structure is anticipated to form the bedrock for the growth of the virtual asset market.

- Innovative fostering measures include a 20% reduction in income tax on crypto assets and the non-collection of corporate taxes.

- The Web3 industry is witnessing active participation from both startups and large corporations.

3-2. Current state of crypto regulations in Korea: Advancing toward the institutionalization of cryptocurrencies

The initial phase of Korea’s virtual asset legislation, known as the Act on the Protection of Virtual Asset Users, concentrates on investor protection and does not serve as a foundational law governing the entire market. Aligned with the global trend of integrating virtual assets into institutional systems, the second phase of legislation is anticipated to further accelerate the incorporation of the virtual asset market into the institutional framework.

3-2-1. Implementation of the virtual asset user protection act: Paving the way for institutional integration

On June 30, 2023, the 'Act on the Protection of Virtual Asset Users,' the inaugural phase of the Korean Basic Act on Virtual Assets , successfully passed the plenary session of the National Assembly and is slated for implementation in July 2024. Recognizing the urgent need to safeguard virtual asset users, the National Assembly achieved consensus across party lines, opting for preemptive measures and phased complementary responses rather than awaiting the establishment of international standards. The Act on the Protection of Virtual Asset Users encompasses crucial elements, including: 1) Definition of virtual assets and virtual asset operators, 2) Protection of user assets, 3) Regulation of unfair transactions, 4) Prohibition of arbitrary blocking of deposits and withdrawals related to virtual assets, 5) introduction of obligations, such as monitoring abnormal transactions, 6) Authority of financial authorities to supervise and sanction, and 7) Penalties and fines. These provisions are designed to enhance user protection within the cryptocurrency market.

A pivotal component of the User Protection Act is the regulation of unfair trade, borrowing the structure of unfair trade regulation under the Capital Market Act. Key contents include:

- Prohibiting the use of material nonpublic information

- Prohibiting price manipulation

- Prohibition of fraudulent and deceptive trading behavior

- Prohibition of trading in self-issued coins

- Sanctions for each unfair trade behavior

In the initial phases of cryptocurrency legislation, regulatory authorities initially pursued a legislative process with a foundational or unified legal framework. However, the pressing need for regulations safeguarding cryptocurrency users, exemplified by incidents involving Luna and FTX, prompted the government to pivot its legislative approach to what is commonly referred to as a two-stage strategy. Consequently, the first stage involved the enactment of the Virtual Asset User Protection Act, while the second stage focuses on enacting the Basic Law. Recognizing that the law establishes only minimum standards, there is a necessity to fortify specific standards and provide guidelines through presidential decrees to operationalize the principles outlined in the law. To address this, regulatory bodies such as the Financial Services Commission are reportedly engaged in a study to clarify standards for issuing and distributing virtual assets and to formulate procedures for listing virtual assets.

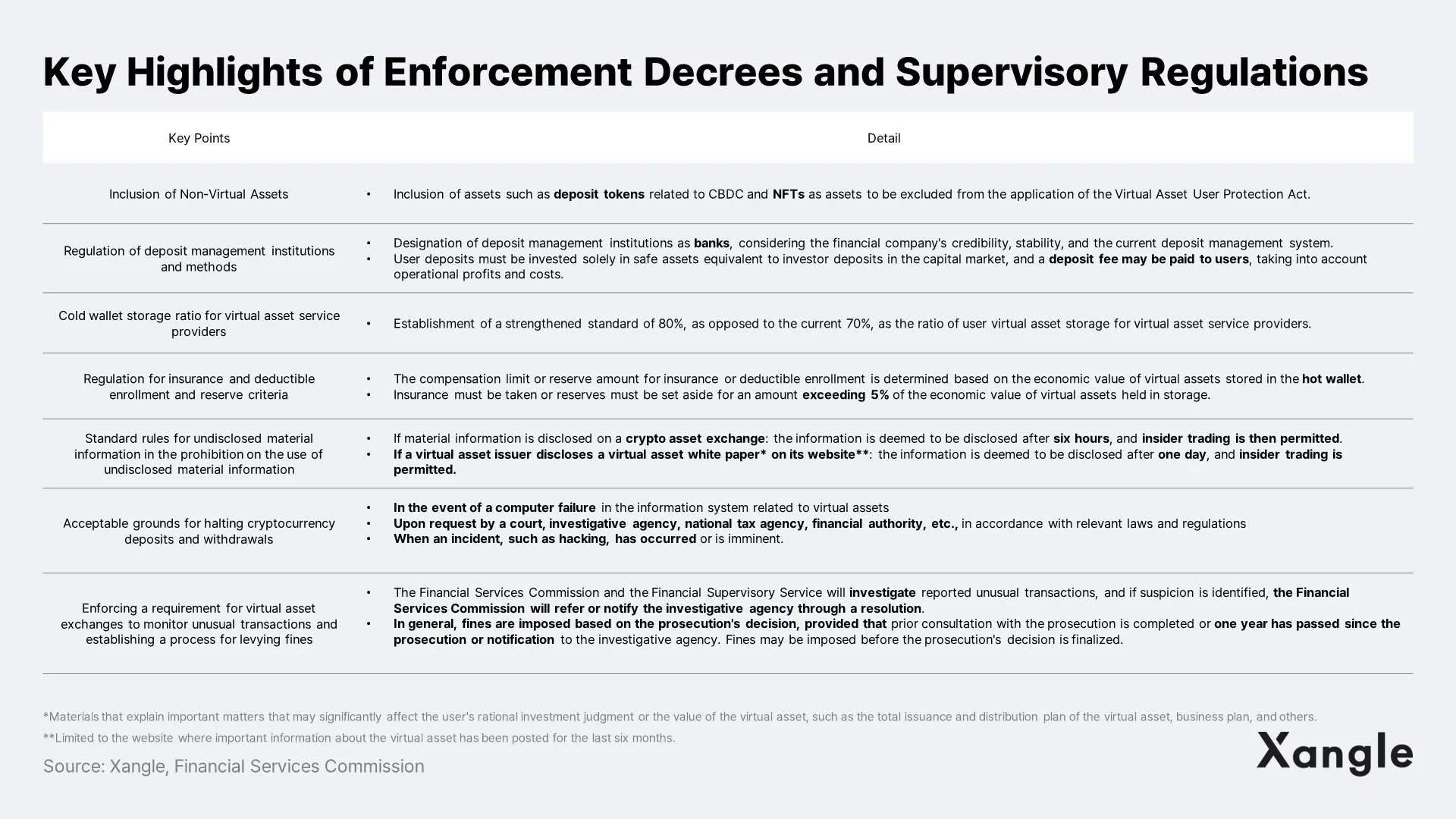

In line with this, the Financial Services Commission issued a legislative preview of the Enforcement Decree and Supervisory Regulations of the Act on the Protection of Virtual Asset Users on December 11, actively seeking input from stakeholders. The released Enforcement Decree and Supervisory Regulations outline the specific requirements mandated by the Act on the Protection of Virtual Asset Users, with the primary contents as follows.

In the upcoming phases, the government plans to enhance the Virtual Asset Act through a second wave of legislation, encompassing regulations pertaining to the issuance and disclosure of virtual assets. Anticipated in this second phase are regulations on issuance and distribution, the oversight of stablecoins, the establishment of a regulatory framework for virtual asset valuation businesses, advisory and disclosure practices, definition of the business scope of virtual asset exchanges, and measures to address conflicts of interest. This legislative progression is poised to pave the way for the involvement of traditional financial market entities in the cryptocurrency arena. Currently, cryptocurrency exchanges bear the responsibility for securities financing, depository settlement, and credit rating in the traditional market. However, as the second phase of legislation delineates procedures for listing virtual assets, defines the business scope of virtual asset exchanges, and establishes a regulatory framework for the virtual asset valuation industry, there is a likelihood that the roles currently held by virtual asset exchanges will undergo separation. This evolution could lead to direct participation in the virtual asset market by traditional financial companies handling securities finance, depository settlement, and credit rating in the traditional market.

A pertinent example is the establishment of EDXM, a virtual asset exchange in the United States led by traditional financial firms such as Citadel, Fidelity, and Charles Schwab. Officially operational for institutional investors in 2023, EDXM showcases a trend where traditional financial players enter the virtual asset market. Korean financial entities should closely monitor the enactment of the Basic Act on Cryptocurrency to identify new business opportunities within the cryptocurrency market.

Furthermore, in July, the Financial Services Commission unveiled draft guidelines for supervising virtual asset accounting and a proposal for mandatory disclosure of annotations. This proactive step aims to enhance accounting transparency in the virtual asset industry and establish practical accounting regulations tailored to the virtual asset ecosystem.

With the submission of last year's semi-annual report, WEMADE has enhanced its disclosures concerning its cryptocurrency, WEMIX ($WEMIX). In addition to promptly adopting financial authorities' accounting guidelines, the company consistently issues separate virtual asset disclosures through the WEMIX team, demonstrating dedicated efforts to ensure transparency. Experts note that the full application of accounting guidelines may require more time due to the lack of specific details for integration with the existing system, numerous ambiguous areas, and the early stage of implementation. Nevertheless, there is optimism about the potential resolution of accounting challenges faced by listed companies engaged in cryptocurrency-related businesses, which were previously unclear, and addressing existing uncertainties.

Key Takeaways

- As a proactive measure to safeguard investors, Korea has enacted the initial phase of legislation, the Act on the Protection of Users of Virtual Assets, and is pursuing a two-phase legislative plan, with the objective of enacting the second phase, the Basic Act on Virtual Assets.

- The first phase of legislation excluded electronic forms of currency issued by the Bank of Korea from the virtual assets' scope, anticipating the future introduction of CBDCs by the government. It primarily focused on unfair trade regulations to protect investors.

- The Enforcement Decree, strengthening Phase 1 legislation, encompasses regulations on depository institutions and management methods, along with standards for undisclosed material information in the prohibition of its use. as well as standards for undisclosed material information in the prohibition on the use of undisclosed material information.

- The government, in collaboration with public-private partnerships, is advancing the second phase of legislation, with the Financial Services Commission and the Financial Supervisory Service actively introducing regulations to establish a virtual asset supervision department.

- Accounting guidelines for virtual assets are undergoing finalization but still exhibit gaps in several areas.

- With the ongoing global trend, there is an expectation that traditional financial entities and various Web2 companies will enter the Web3 industry when the second phase of legislation is earnestly prepared and implemented.

3-3. Embracing Challenges for Future Growth

In our earlier exploration, we reflected on the current state of cryptocurrency regulation across major countries and outlined the anticipated direction for 2024. Describing this journey as a "bumpy ride," it is evident that considerable effort is needed to bring the current cryptocurrency market, marked by its ups and downs, under a robust regulatory framework. However, this process is deemed essential for the market's significant advancement.

While challenges lie ahead, the benefits of regulation are poised to make a substantial impact not only on market liquidity expansion but also on public perception. Regulation signifies the acknowledgment of cryptocurrencies by the public and traditional industries for their intrinsic value, transcending their current reputation as speculative and dubious investments.

Furthermore, the regulatory landscape sets the stage for the emergence of new projects that can foster innovative forms of added value. The aspiration is for regulatory changes to catalyze industry development without compromising the foundational ethos of Web3, opening doors to unimaginable possibilities.

4. Blockchain Infrastructure Making Strides

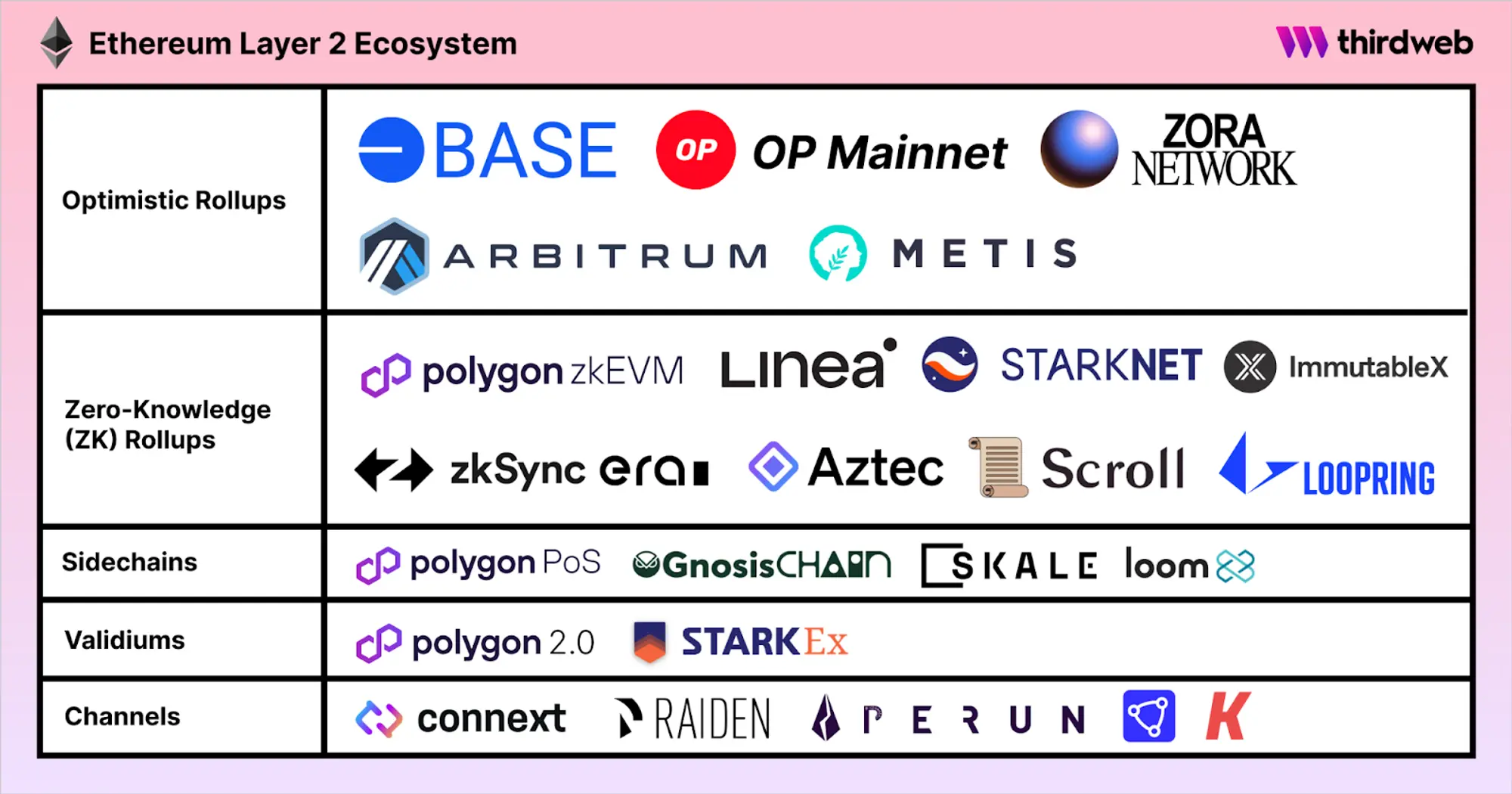

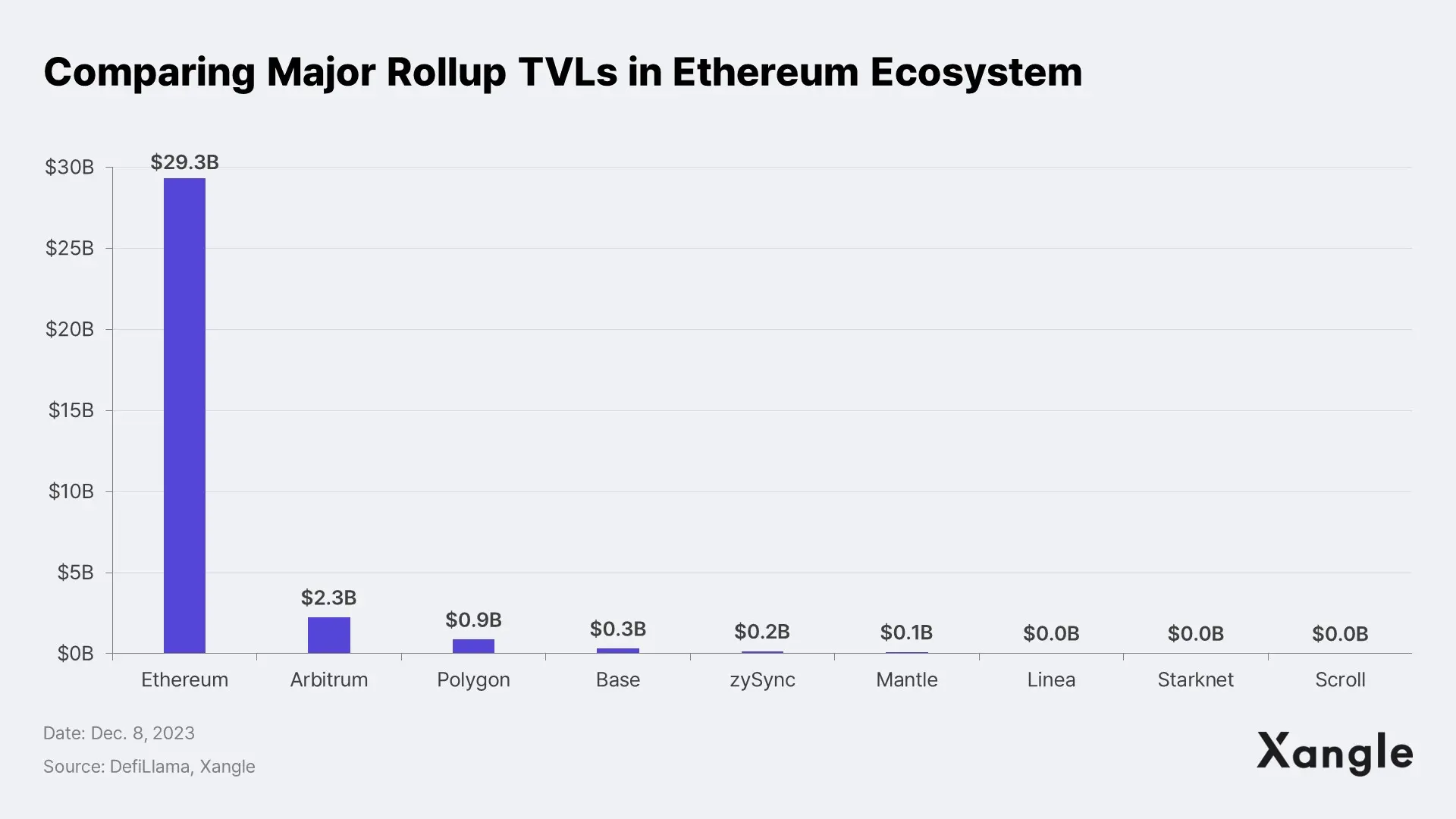

4-1. Cosmos' Appchain vision realized in Ethereum rollup ecosystem

We believe that the Ethereum L2 ecosystem will realize Cosmos’ vision of the interchain future where various appchains are connected and interact with each other. Specifically, here are some of our predictions for the future of Ethereum:

- Rollups will become an increasingly important part of the Ethereum ecosystem.

- Hundreds and thousands of AppRollups will be born around a handful of core general purpose rollups (i.e. Arbitrum, Optimism, Polygon, etc.).

- Evolution of modular frameworks: Time will come when builders will only need to focus on the application layer.

- The next trend will be shared sequencing and interoperability.

4-1-1. Rollups will play an increasingly important role in the Ethereum ecosystem

Ethereum's vision for danksharding is to utilize the shard chain only as a data availability (DA) layer to store rollup data, while delegating execution of transaction to rollups. Thus, Ethereum's major network upgrades are also focused on growing the rollup ecosystem and actively encouraging users to use rollups. Among those upgrades, we’re particularly keeping a close eye on two upgrades: EIP4844 and ERC4337. And we expect more and more economic activity to take place over time on rollups with lower transaction fees rather than on Ethereum L1.

Source: thirdweb

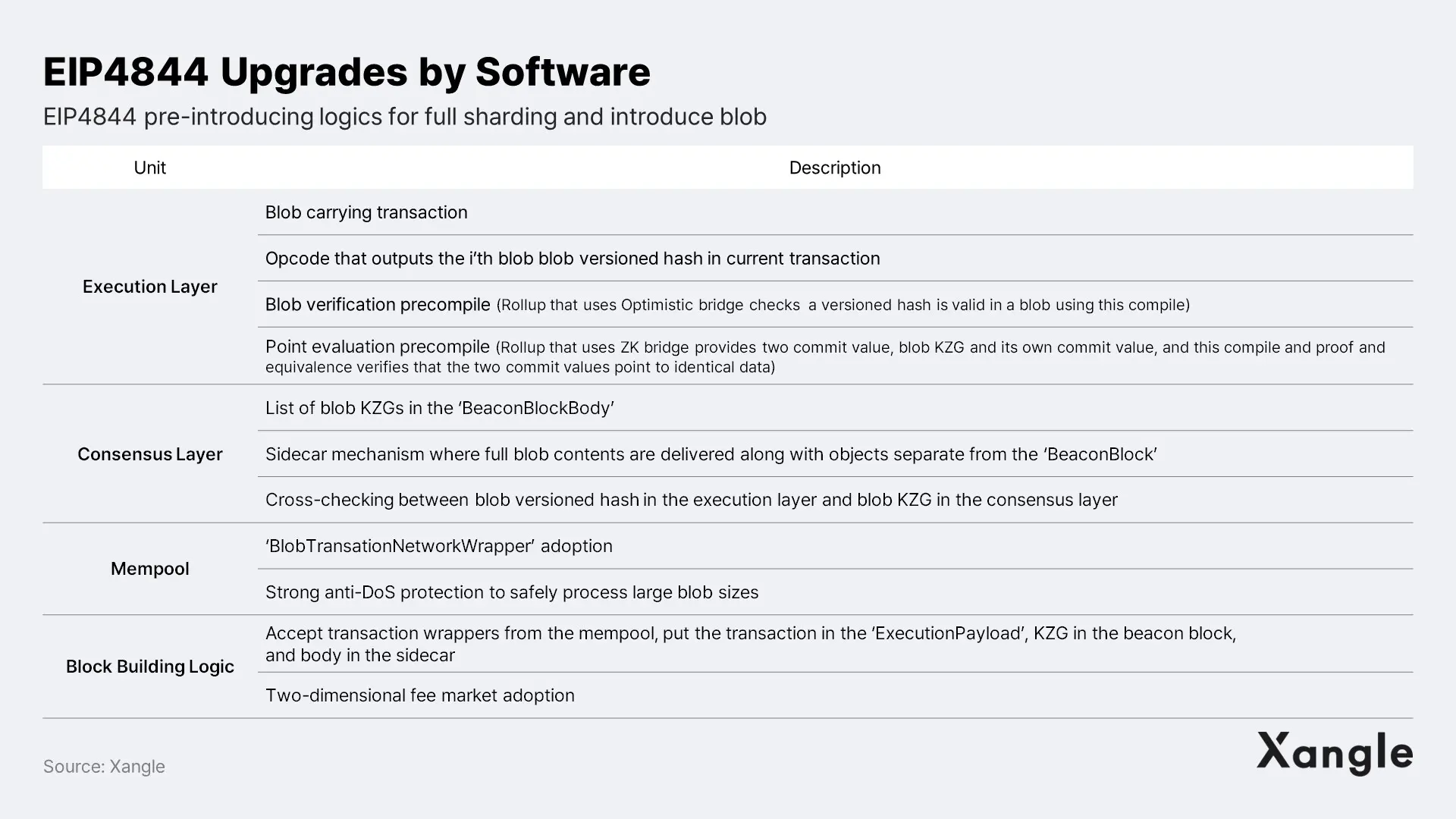

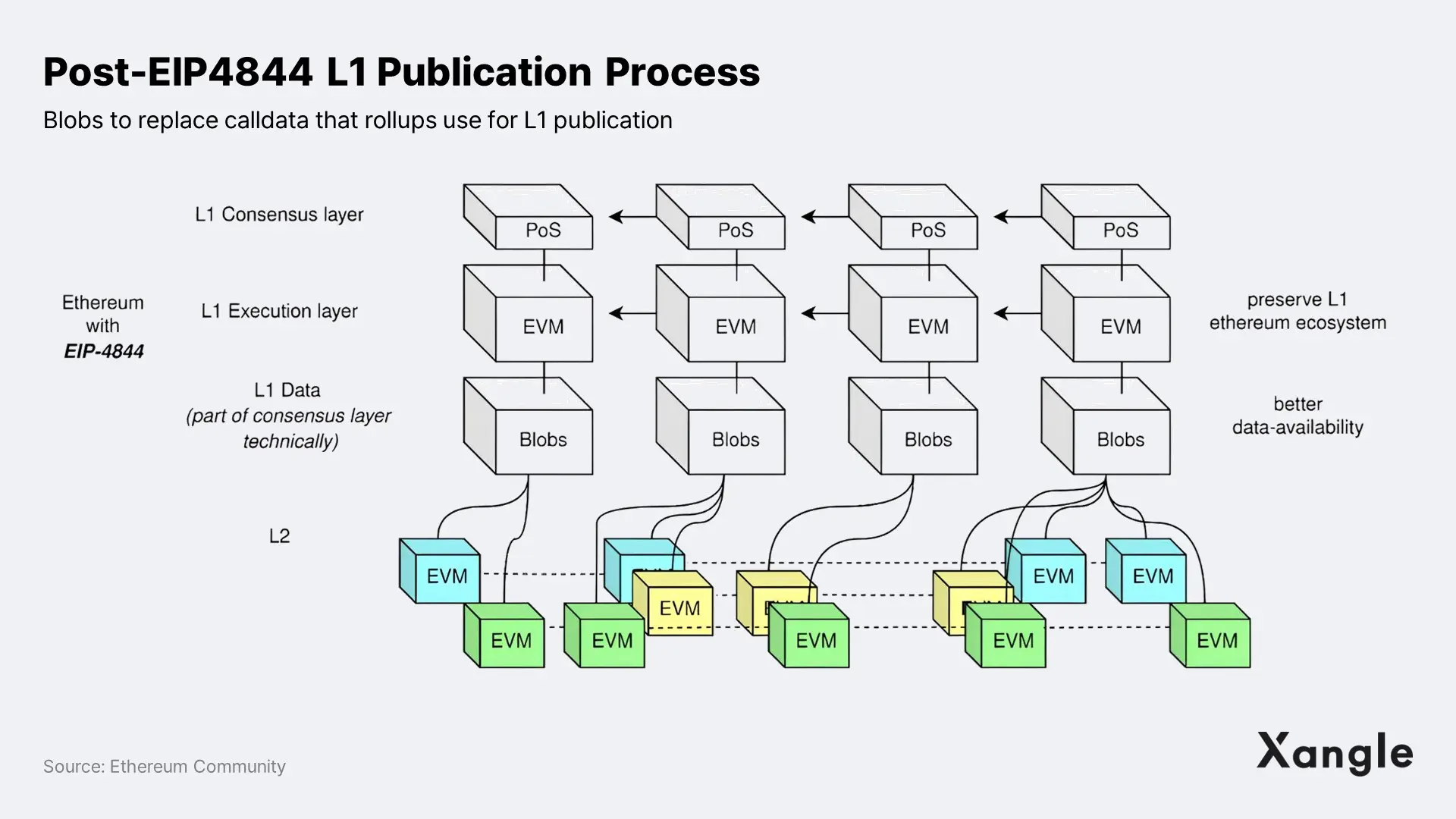

A. EIP4844 expected to significantly lower rollup costs through blobs (binary large objects)

Ethereum's Dencun hard fork, originally expected to be introduced in late 2023, is now expected to launch early this year. The major update to Dencun, EIP4844 (or Proto-Danksharding), will introduce some of the logic needed for future danksharding and add a transaction type that includes blobs. Blobs will replace calldata, effectively reducing the cost of L1 publication (DA), which accounts for the majority of L2 transaction fees. For more details on EIP4844, read our "EIP4844 and Its Impact on Rollup Economics".

Originally, rollups use calldata to store their block data on Ethereum, which is read-only, cheap to use, and has no data size limit. But with the introduction of EIP4844, rollups will be able to store data via blobs. Blob fees are not affected by the demand for blockspace but are determined solely by the supply and demand for blobs in the EIP1559 transaction market. Until the demand for blobs reaches the price discovery zone, blob fees will be effectively zero, which means that L1 publication (DA) fees—90% of the total rollup cost—will be eliminated. In other words, post-EIP4844 rollups storing data as blob carrying transactions will reduce the overall cost by approximately 10x compared to calldata storage.

There is a concern that the cost of blobs could increase exponentially in a short period of time if the demand for blobs reaches the target level, but the current demand for blobs is about 10 times lower than the target, which is expected to take about 1-2 years to reach. There are also discussions about changing the structure of the blob cost blob in preparation for when the target level is reached, so we shouldn't worry about the price rising anytime soon. It is clear that EIP4844 will significantly contribute to cost reduction and mass adoption of rollups, and it is possible that rollups will have the lowest transaction cost on the blockchain immediately after it gets introduced.

B. ERC4337 and its UX innovation to be highly active in the rollup ecosystem

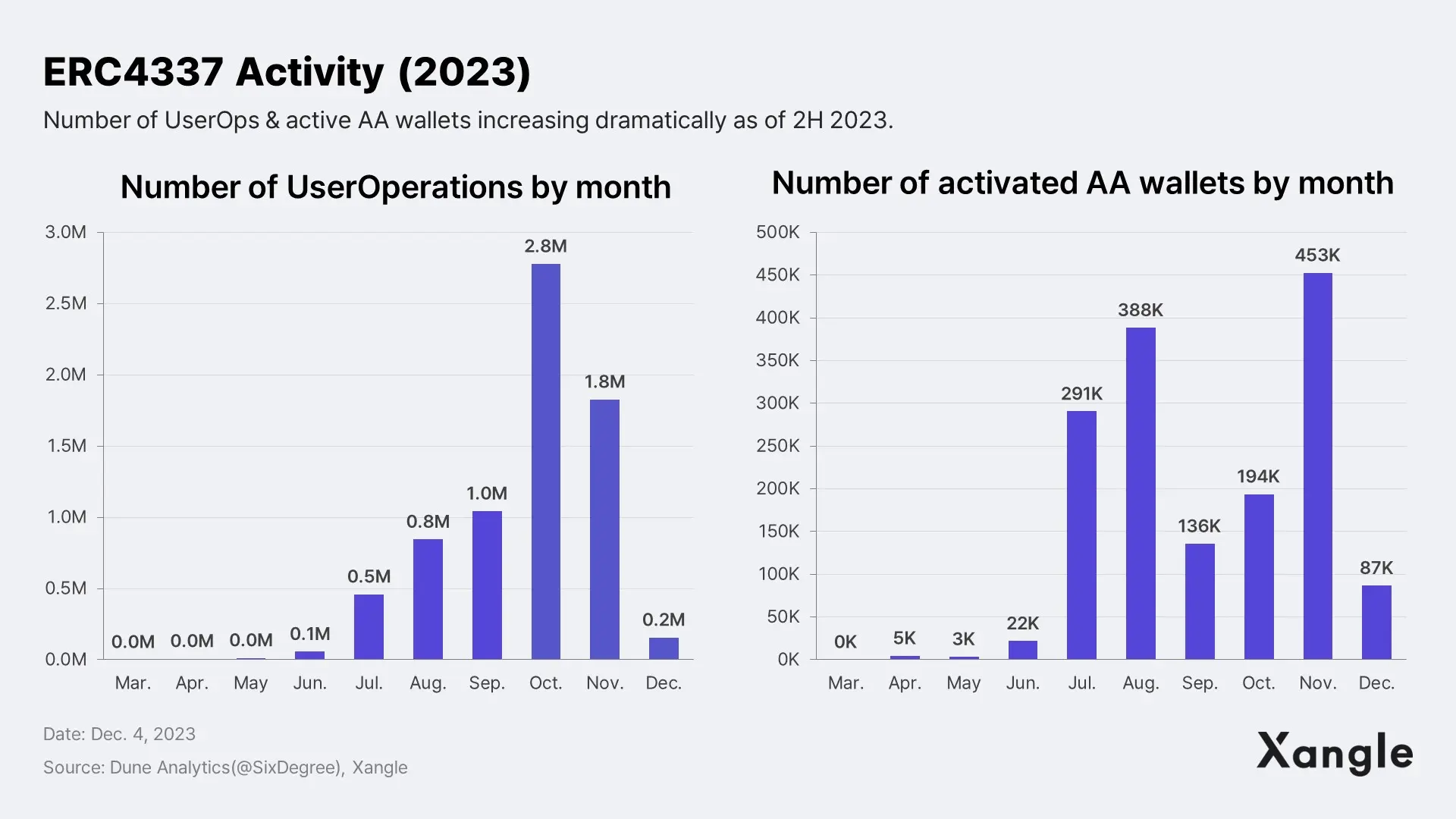

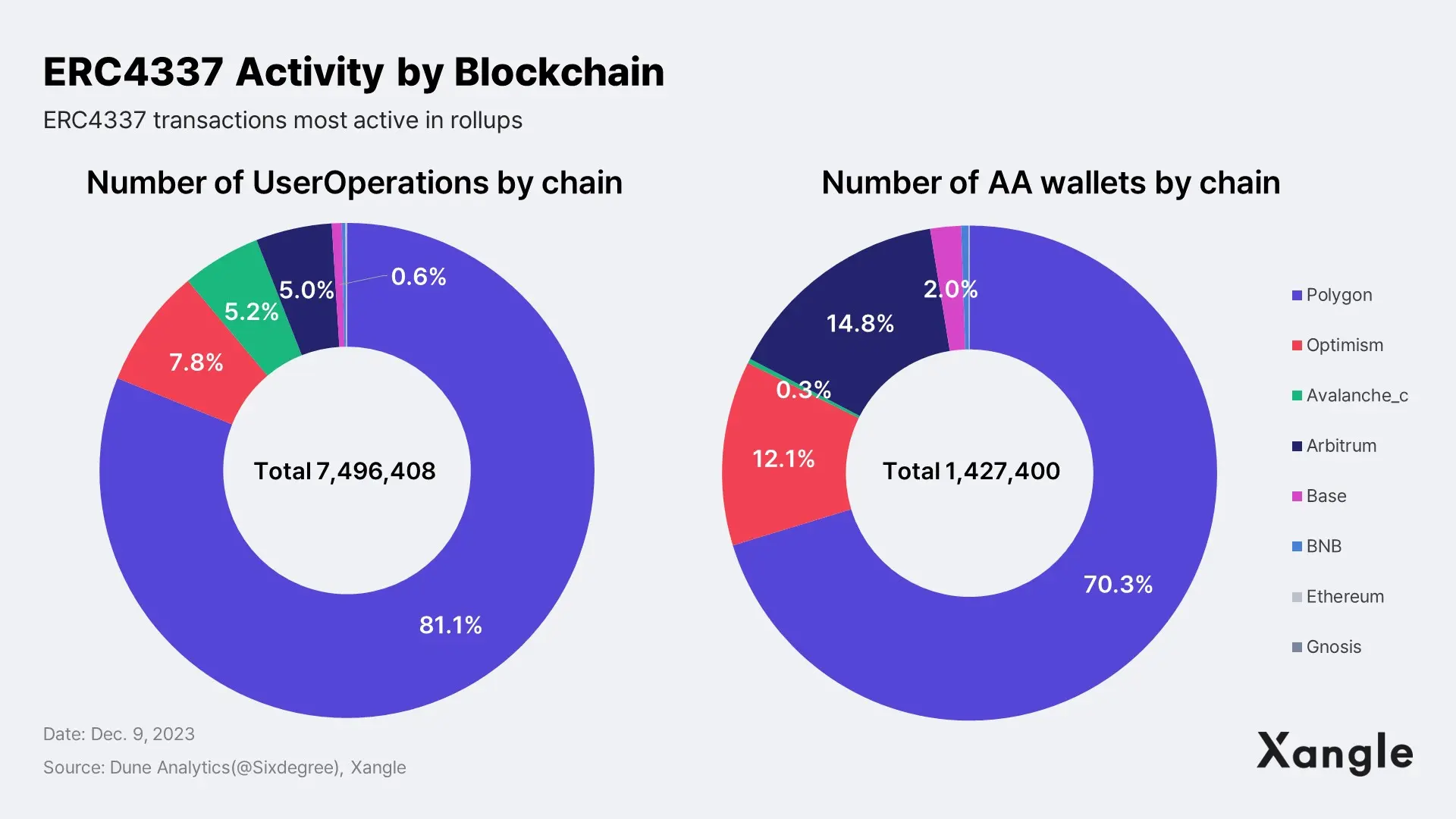

Meanwhile, UserOperations (ERC4337 transactions) introduced for account abstraction (AA) also mostly occur in rollups. With AA gaining traction as a solution to low-level UI/UX and the burden of self-custody, ERC4337 has the advantage of enabling account abstraction without a hard fork. UserOps is happening on major rollups, and the evolution of blockchain UX will continue to be centered around rollups.

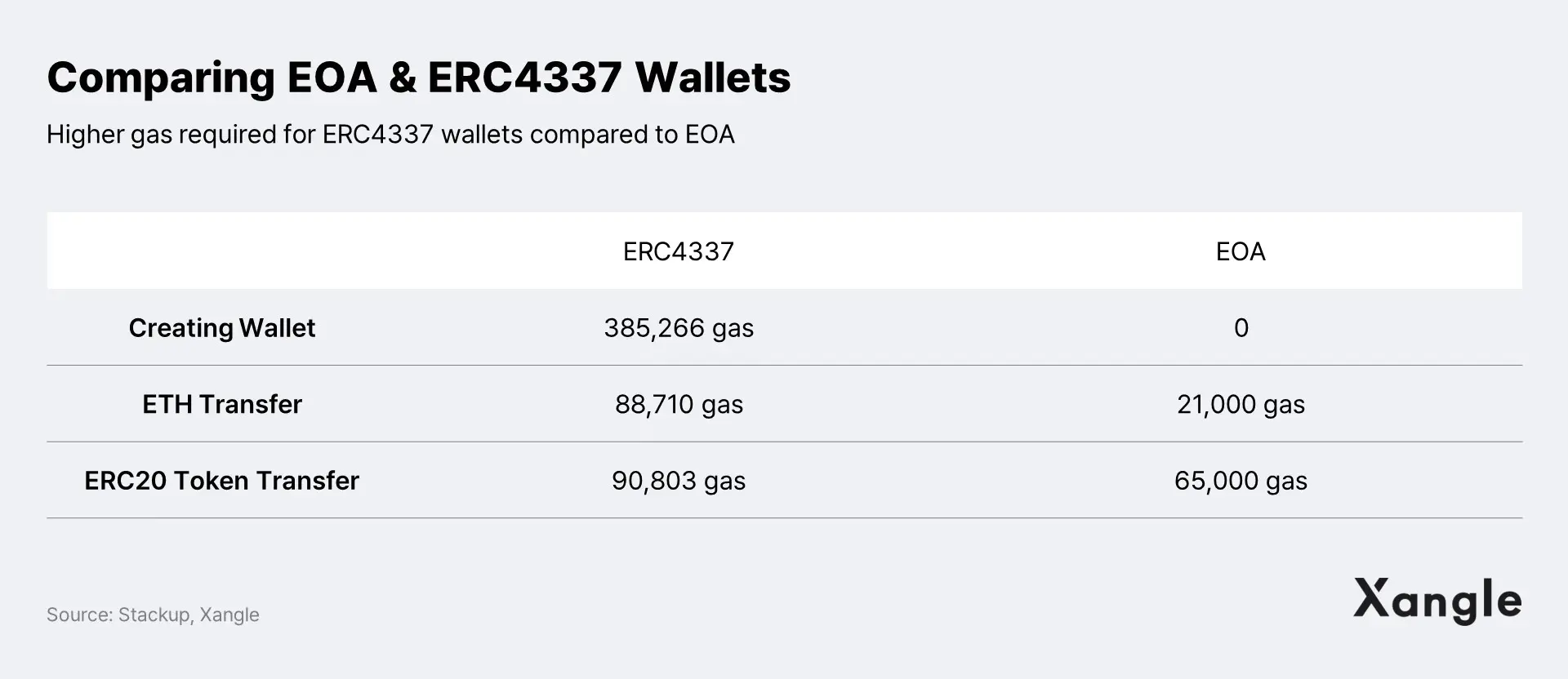

UserOps uses contract wallets rather than EOA, which means that creating a wallet and transferring tokens costs more gas. For example, while EOA can create a wallet for free, creating an AA contract wallet would currently require about 385k gas. In addition, gas fees for token transfers are about 4 times higher for Ethereum and 1.4 times higher for ERC20 tokens, so the cost burden on users is high when using UserOps.

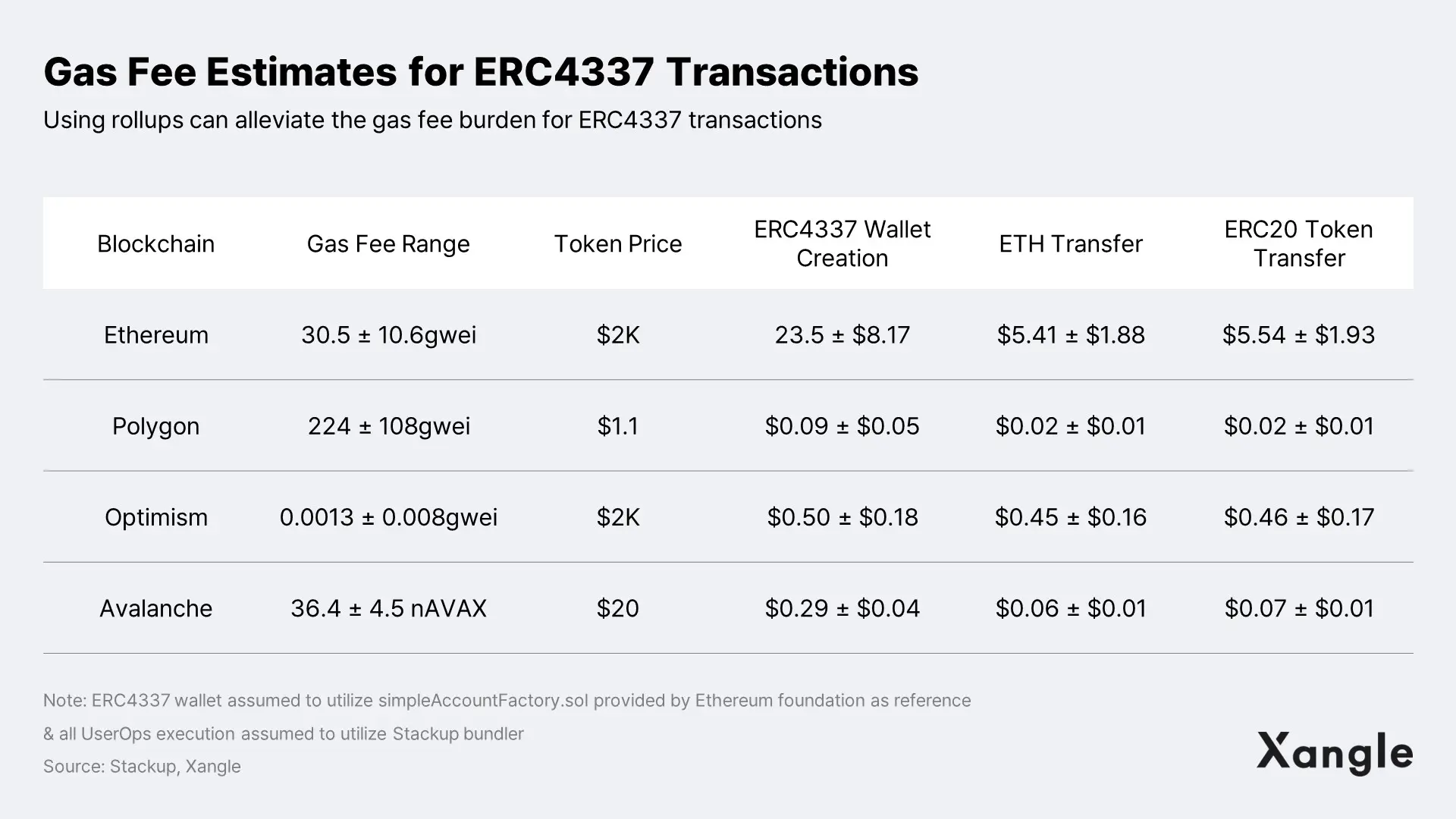

However, the cost of ERC4337 transactions is relatively low in rollups compared to the base layer (Ethereum). In fact, the number of wallets with UserOps and AA features has been steadily increasing since last summer, with low-gas L2 chains such as Polygon, Optimism, and Avalanche dominating the ERC4337 race. In addition, the cost of UserOps will be much lower if rollup data is stored in blobs with the release of EIP4844, so we expect to see blockchain UX improving around the rollup ecosystem. For more details, please refer to “ERC4337, the Epicenter of UX Innovation”.

4-1-2. Countless AppRollups will be born around few core rollup projects

We expect to see hundreds or thousands of AppRollups centered around a few core Rollups that provide open-source SDKs and frameworks in the future. When we say AppRollups, we don't mean general purpose rollups like Optimism or Arbitrum, but rollups that support a single service/application's blockspace, like AppChain.

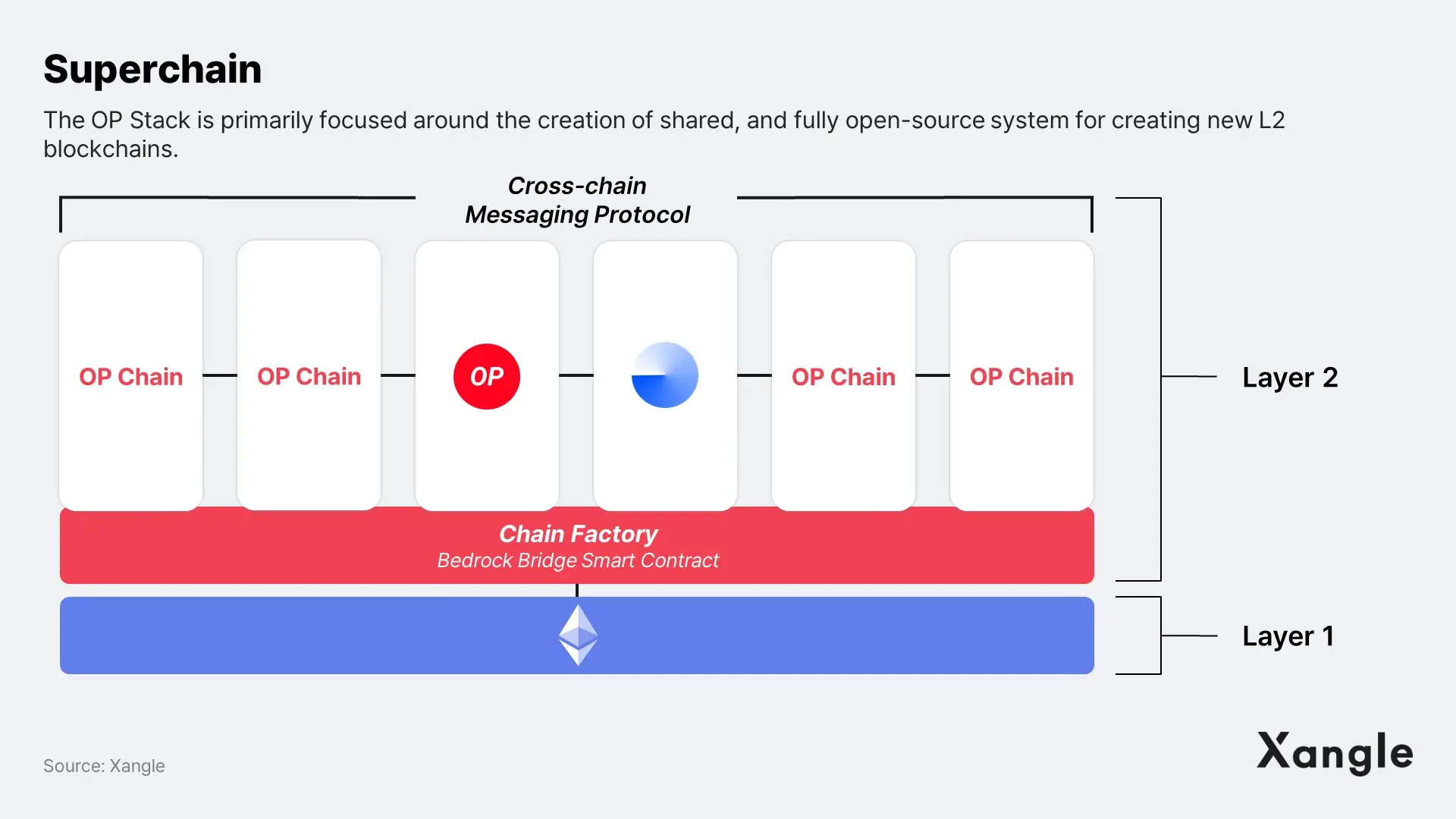

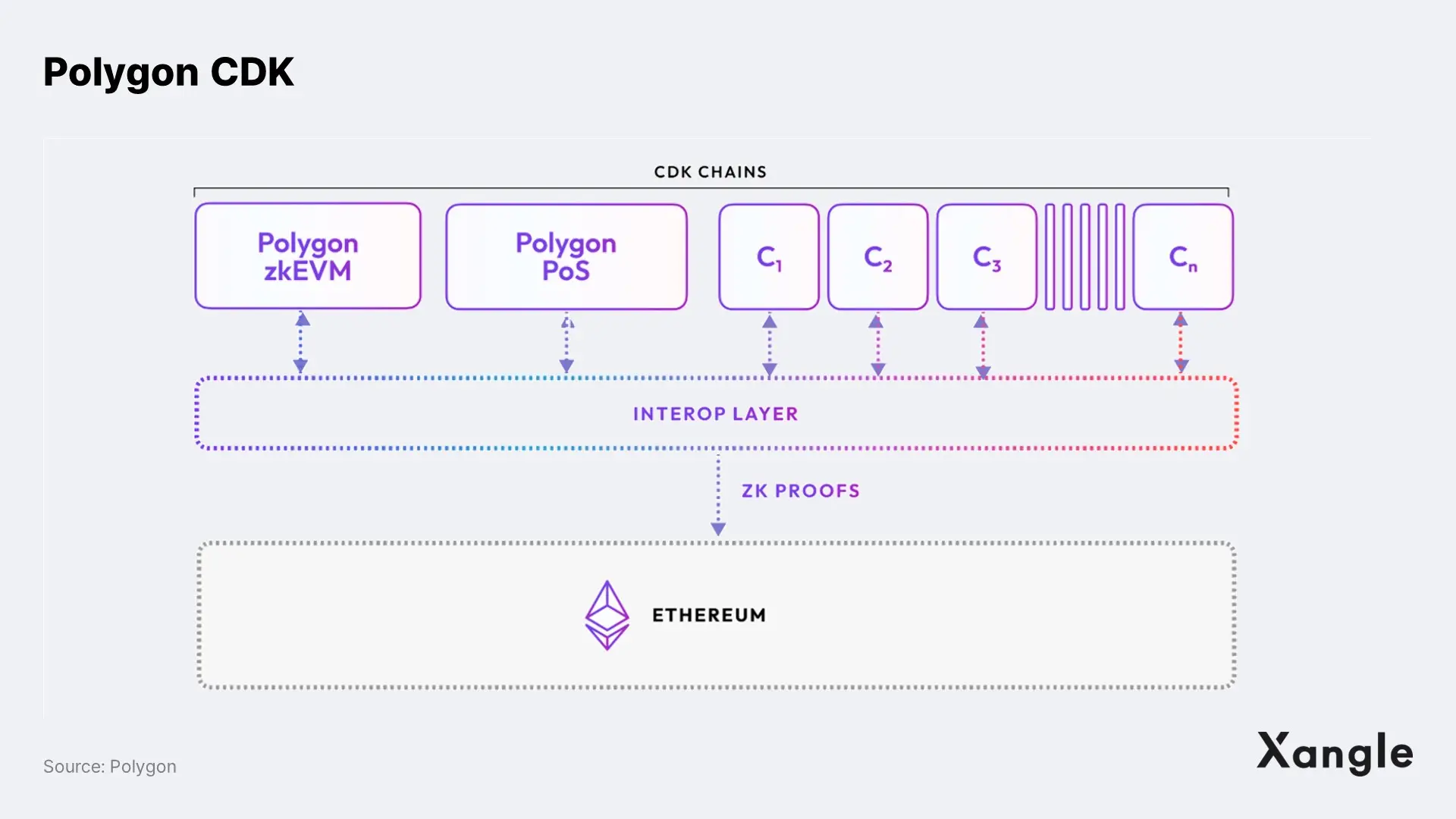

A. Open-source SDKs, frameworks will make it easier to build AppRollups

The currently leading projects in the rollup race are releasing their own open-source SDKs and frameworks, each with their own architecture and vision. These rollups are providing SDKs to make it easier for organizations and projects that are preparing Web3 services to deploy their own AppRollups on these ecosystems. Examples of typical rollup SDKs include Optimism's OP Stack and Polygon's Chain Development Kit (CDK), while Arbitrum (Orbit), zkSync (Hyperchain), and StarkNet are also growing popular.

Regardless of whether the architecture of these rollups is good or bad, the point is that it has become very easy for companies/projects to build their own blockchain on top of Ethereum. Cosmos SDK is a great example of the benefits of providing an open-source SDK for companies to build their own custom chains. And it seems one of the main reasons Com2us (XPLA) and LINE (Finschia) chose Cosmos AppChain was also because Cosmos was the only SDK available at the time. And now that Rollup has its own SDK, we believe it's not unlikely that enterprise demand for the Cosmos SDK will spill over into the rollup ecosystem. In fact, as seen in the cases of Injective Protocol, Canto, and EVMOS, many appchains are leaving Cosmos and migrating to Ethereum (ex. Canto, a Layer 1 blockchain-based DeFi platform, announced in September that it will migrate to Ethereum zk L2 based on Polygon CDK to build a real asset blockchain).

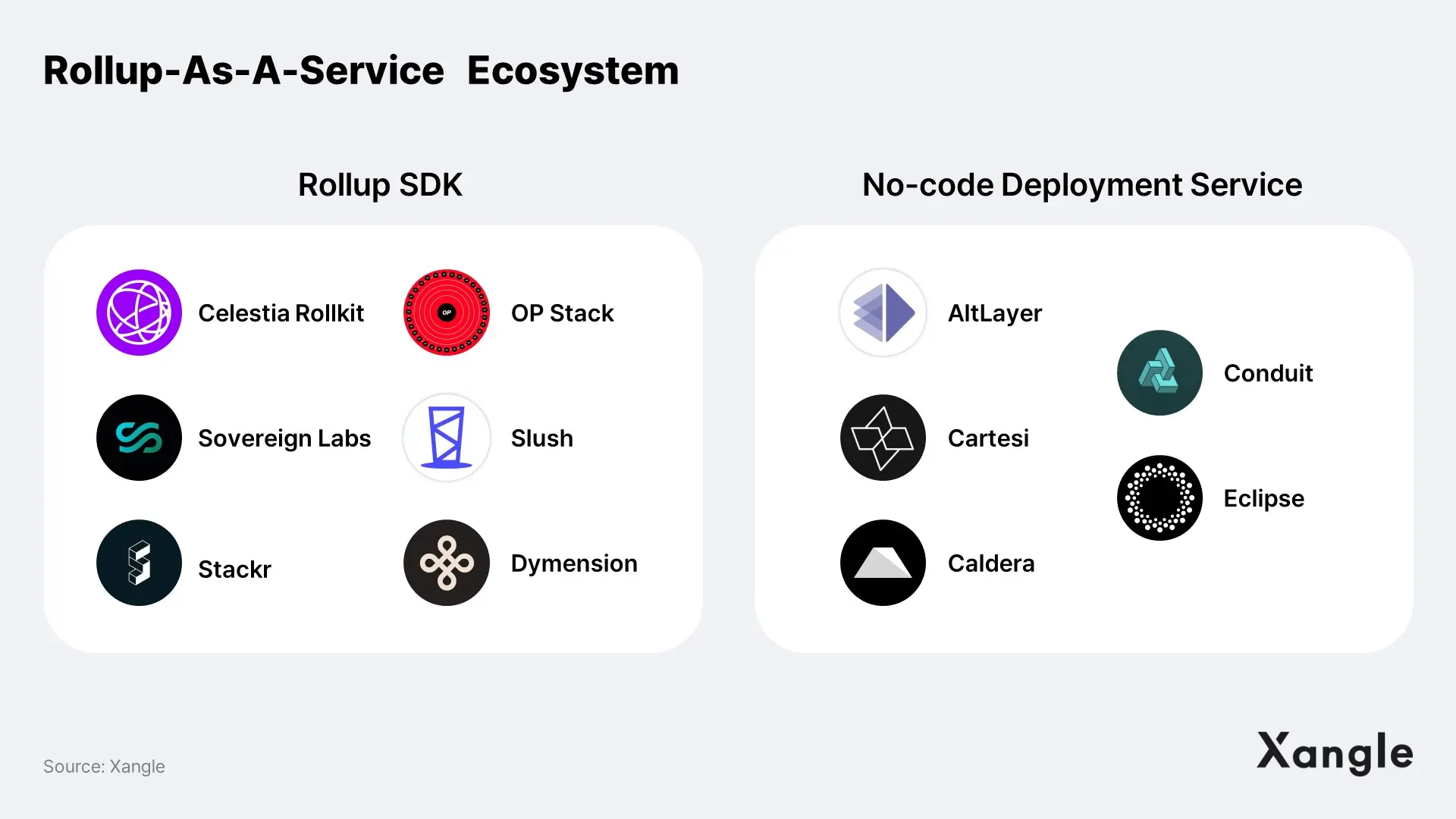

B. Rollup-as-a-Service (RaaS), building rollups will also be outsourced

The emergence of RaaS is also acting as a catalyst to accelerate the flow of approllups. RaaS is a service that makes it easy to deploy, maintain, and manage customized rollups, freeing developers from the technical challenges of mainnet development and allowing them to focus on developing the application layer.

RaaS consists of rollup SDKs and no-code rollup deployment services, and Celestia Rollkit, OP Stack, and Soverign Labs are some examples of rollup SDKs. No-code rollup deployment services allow you to deploy customized rollups with just a few clicks without coding, and examples include Eclipse, Cartesi, Constellation, Alt Layer, Saga, and Conduit. For more details, refer to "Rollup Investment Guide Part1".

4-1-3. Evolution of modular frameworks: Rollups will have more freedom in terms of architecture design

As the modular frameworks are evolving in real time, organizations have more freedom and choice in how and to whom they delegate blockchain roles such as transaction execution, settlement, consensus, and data availability. Eventually, we expect that everything from the basic functionality of the blockchain to the proof system of a rollup will be easily modularized.

A. $10B market cap for $TIA in 1 month of mainnet launch? Data availability (DA) layer is coming

Another modular infrastructure to watch for in 2024 is the DA layer. Examples include Celestia and EigenDA, which recently launched their mainnets, and Polygon is also developing its own DA and consensus layers.

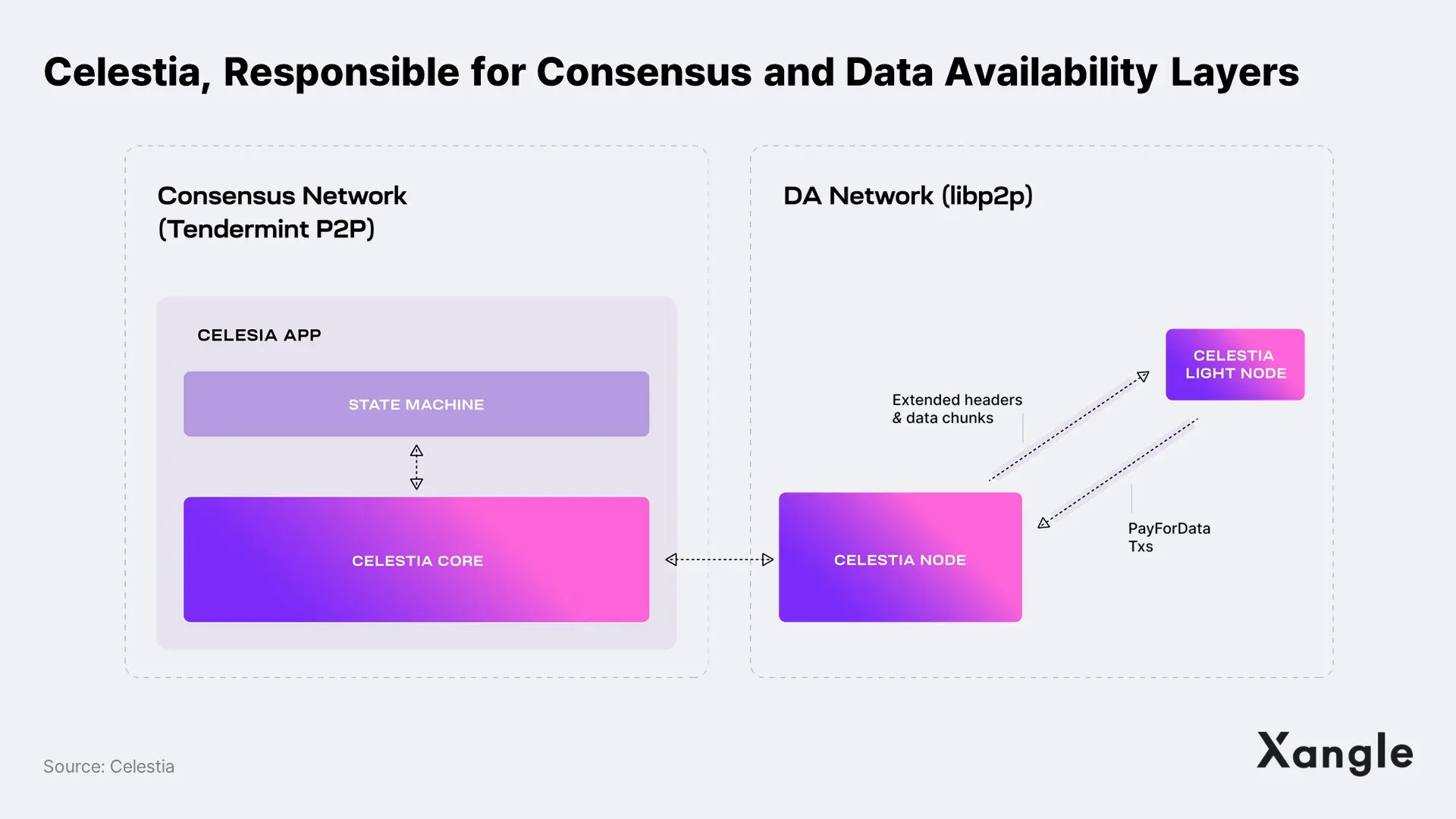

- Celestia: A blockchain for DA and consensus, built on the Cosmos SDK. It is characterized by applying data availability sampling (DAS) and Namespaced Merkle trees (NMT) technology to ensure the reliability of the entire block data when a light node randomly queries the data and receives a valid response to the sampling query. It launched its mainnet on October 31, and as of December 12, $TIA has a market cap of $1.5B ($10.1B FDV).

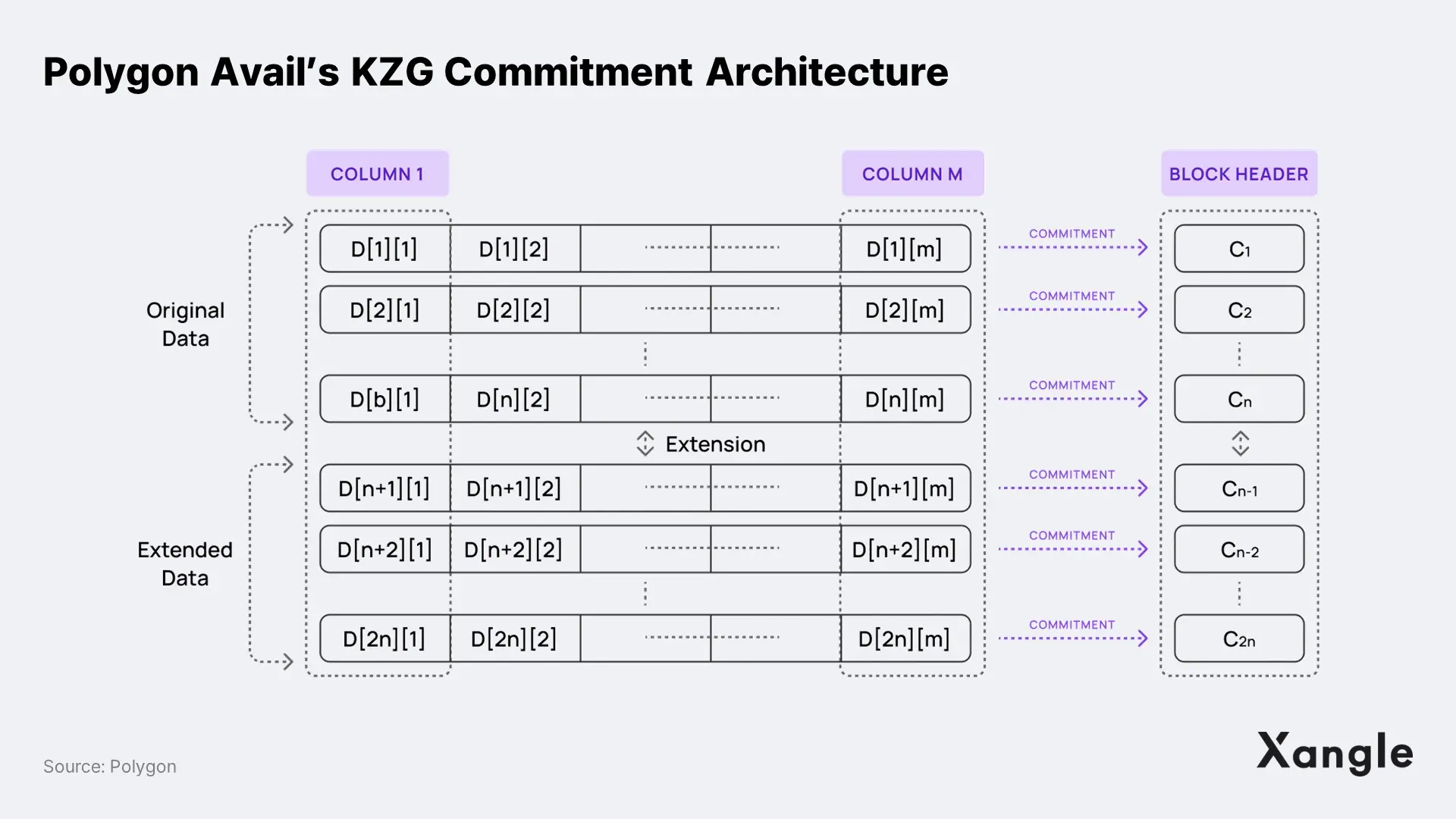

- Polygon Avail: A DA layer in development by Polygon that uses KZG commitments to ensure the authenticity of block body data without requiring light nodes to constantly monitor for malicious data.

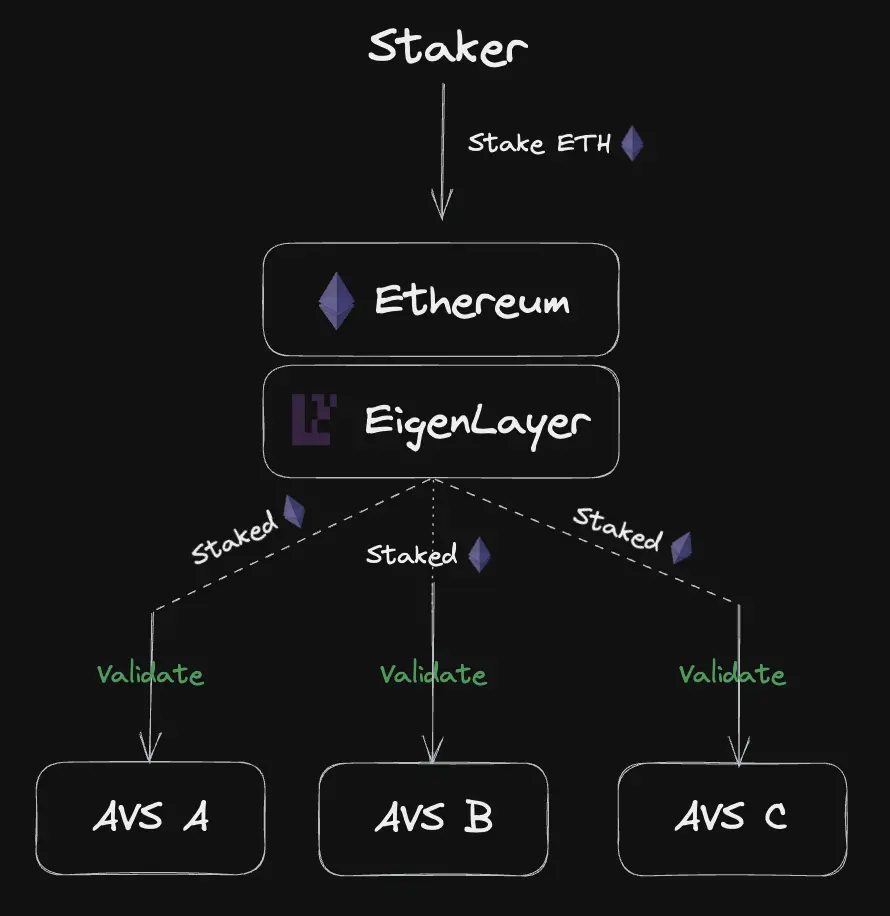

- EigenDA: A DA layer being developed by EigenLayer, preparing a restaking service, that leverages EigenLayer validators to eliminate the need to bootstrap your own validator pool. It is adopted by Mantle, and unlike Celestia and Polygon Avail, it does not provide other functions besides DA.

B. The 'Optimistic Rollup vs. ZK Rollup' debate will be over

When the "Optimal Rollup vs. ZKRollup" debate was at its peak around 2020-2022, it was commonplace for organizations and projects to compare the technical superiority of the two proof systems while onboarding to rollups. However, with the recent spate of attempts within the rollup ecosystem to offer or blend both proof systems, companies/projects looking to onboard to rollups are no longer faced with having to pick one between Optimal Rollups and ZKRollups, and even the definition of ZKRollups is becoming blurred.

For example, the Optimism Foundation recently released a request for proposals (RFP) for a Zero Knowledge Fraud Proof (ZKFP) system, which is an attempt to move away from the traditional fraud proof-only approach to verification and introduce zero-knowledge proofs. And there is currently development for a zero-knowledge fraud proof system for Optimal rollups based on a zero-knowledge proof system (zkVM—no E!) that works in a common execution environment on RISC Zero and LayerN. Similarly, Polygon is developing the Nightfall mainnet, which utilizes both Optimistic and Zero-Knowledge technologies.

While many people categorize rollup chains and evaluate their strengths and weaknesses based on their proof systems, rollups do not monopolize the right to choose different layers in a modular architecture. If written for a sufficiently generalized purpose, a single proof system can also work as a settlement layer for multiple rollups. This means that a proof system can also choose rollups or apply to multiple chains at the same time. Therefore, the good and bad of a rollup chain shouldn’t be assessed by the strengths and weaknesses of the proof system. In the future, the distinction between optimal rollups and zk-rollups will become irrelevant, and it will be more important for projects that consider building approllups to look at the ecosystem activity rather than proof systems.

4-1-4. Next Trend is Shared Sequencing and Interoperability

As already mentioned, there will be a definite need for a solution that can seamlessly connect approllups when a large number of them are created in the future. As such, we expect shared sequencer networks and interoperability solutions to gain traction once the rollup market has matured.

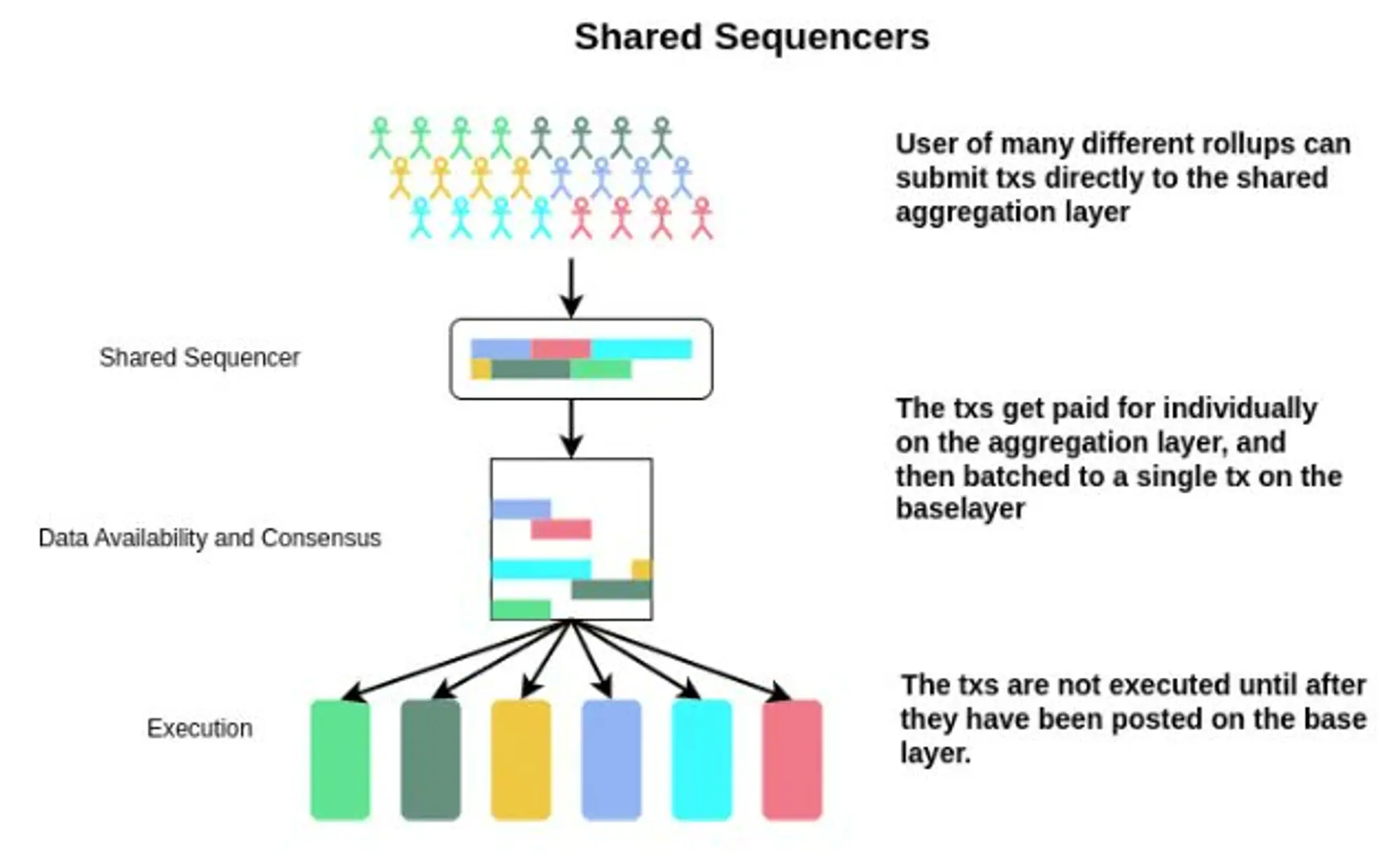

A. The emergence of shared sequencing networks to address sequencer centralization in rollups

Current rollups all use a single sequencer, which poses problems in terms of censorship resistance, MEV, interoperability, and composability. Various methods have been discussed to decentralize sequencers, including Proof-of-Authority (PoA), PoS-based L2 consensus + leader selection, as well as MEV auctions (MEVA). But the solution that got the most attention recently is the shared sequencer network. A shared sequencer network is a middleware blockchain that is responsible for sequencing rollup transactions, such as Espresso Sequencer, Radius, Astria, and SUAVE. For more details, see "Shared Sequencing Network: A Middleware Blockchain for Decentralizing Rollups".

Source: Evan, Celestia Forum, ‘Sharing a Sequencer Set by Separating Execution from Aggregation’

- Espressosys: An EigenLayer-based network developed by Espressosys, funded by Sequoia and Polychain Capital, that utilizes ETH re-stakers within the EigenLayer as sequencers.

- Radius: A project that is developing the first and only Sequencing-as-a-Service (SaaS) solution in Korea, it applies time-locked puzzle encryption technology and PVDE technology utilizing zkproof to its own sequencing layer to ensure the privacy and validity of transactions.

- Metro: A shared sequencer network being developed by Astria, a startup that has raised a total of $5.5M in seed rounds from nine VCs including Maven 11, 1kx, Delphi Digital, and Lemniscap. Astria will utilize Celestia as its DA layer and is building the Astria EVM, inspired by Cevmos and Rollkit.

- SUAVE: A shared mempool and block builder solution and permissionless EVM chain that can be used on any blockchain. It is a multichain extension of MEV-boost, which is not a shared sequencer network, but has similarities and synergies.

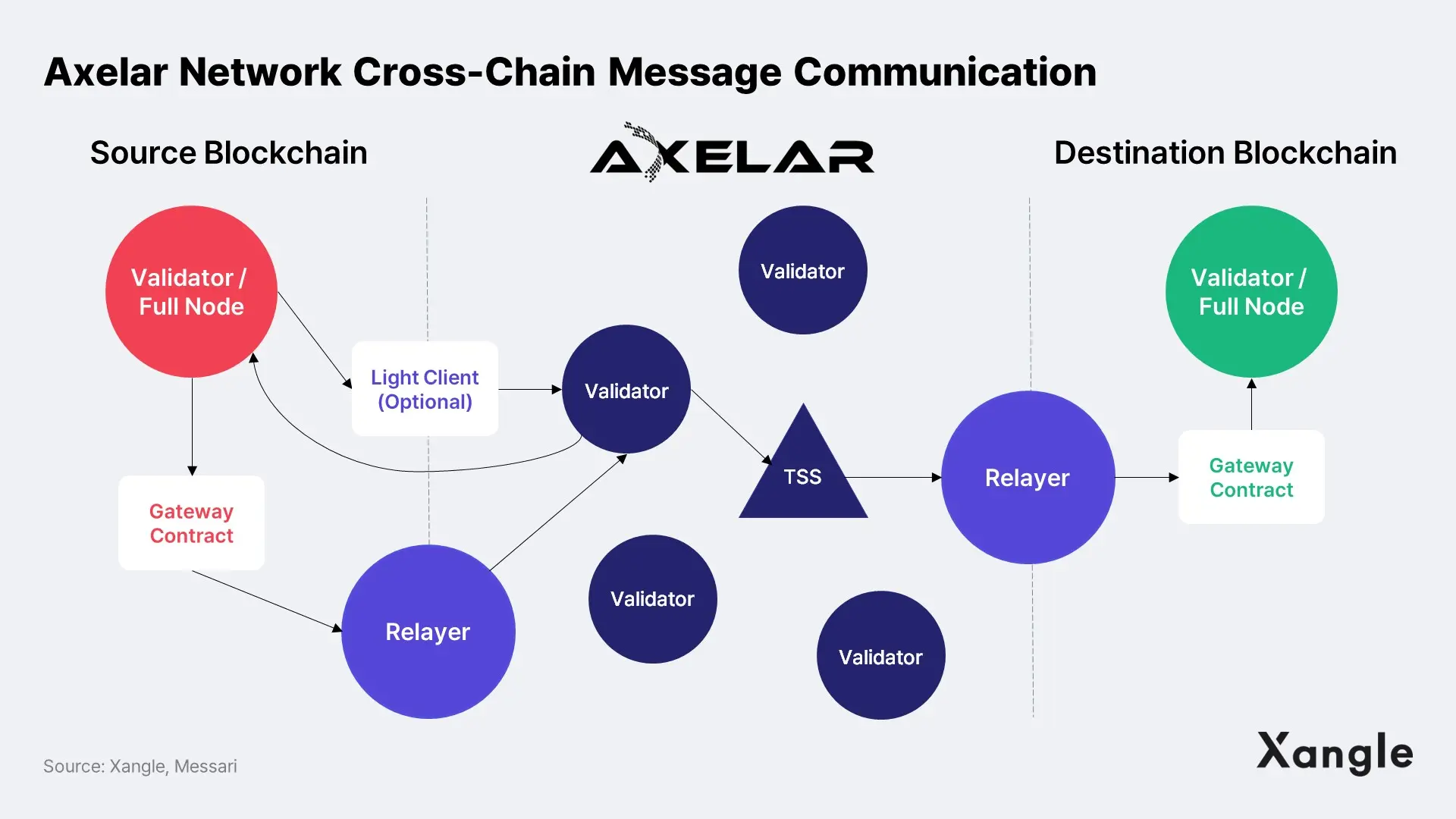

B. The importance of cross-chain solutions to ensure interoperability between blockchains

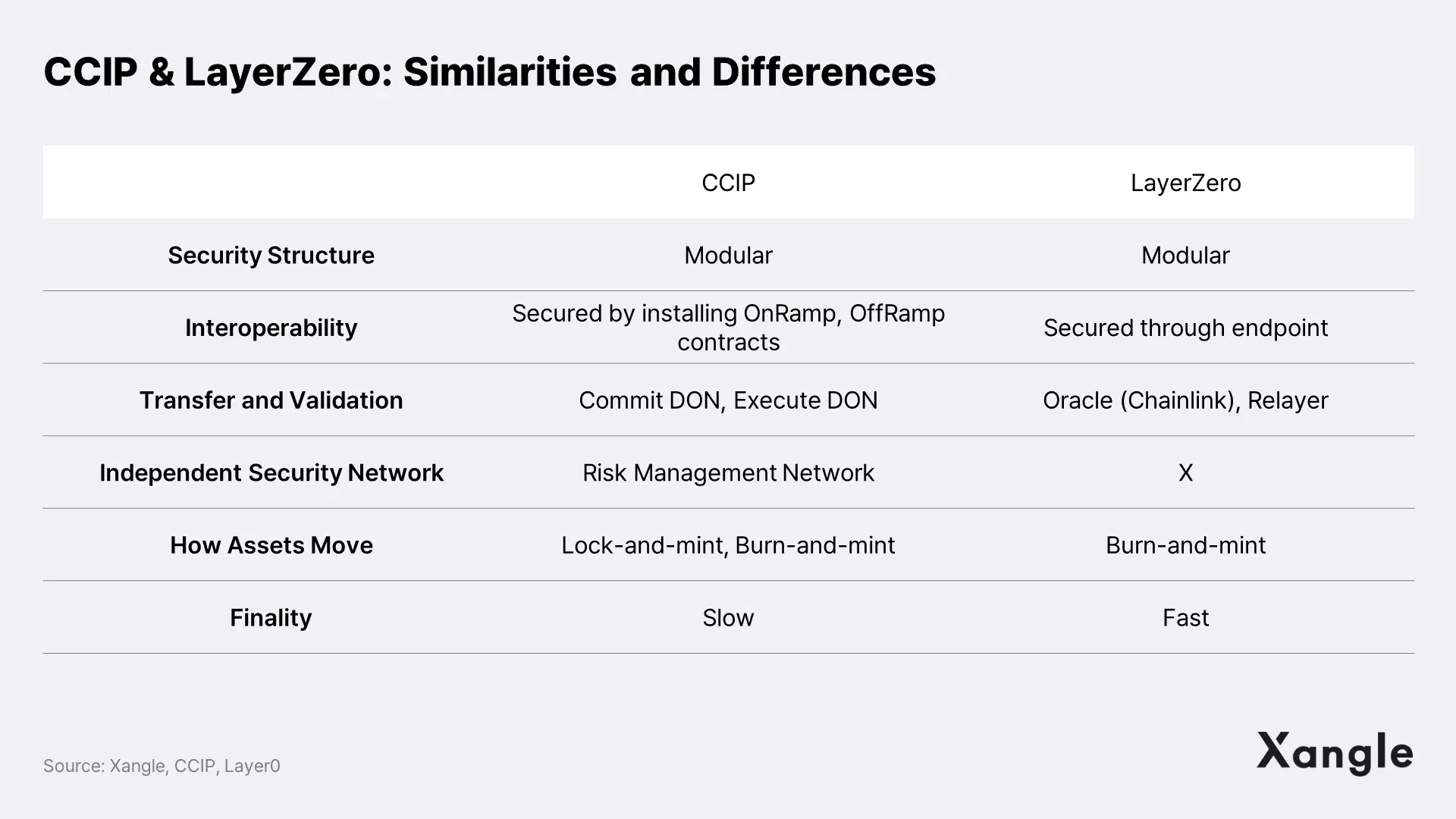

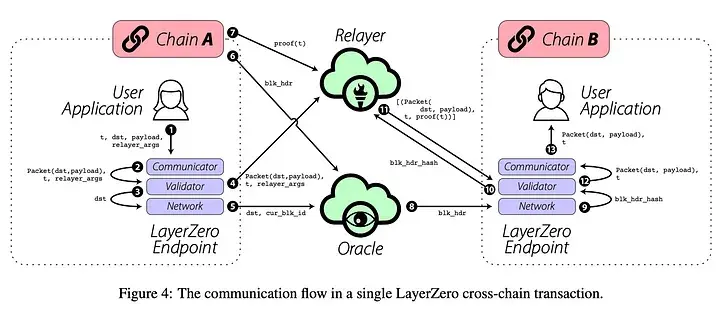

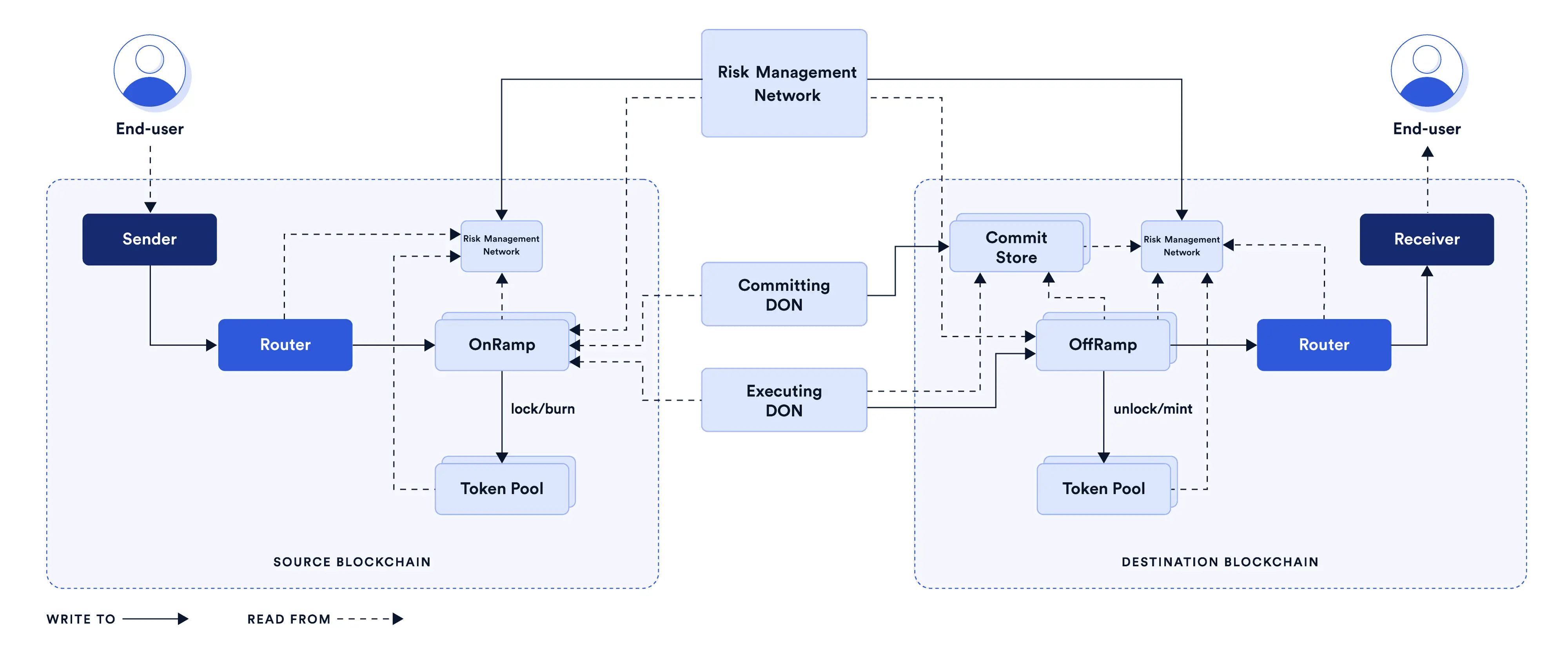

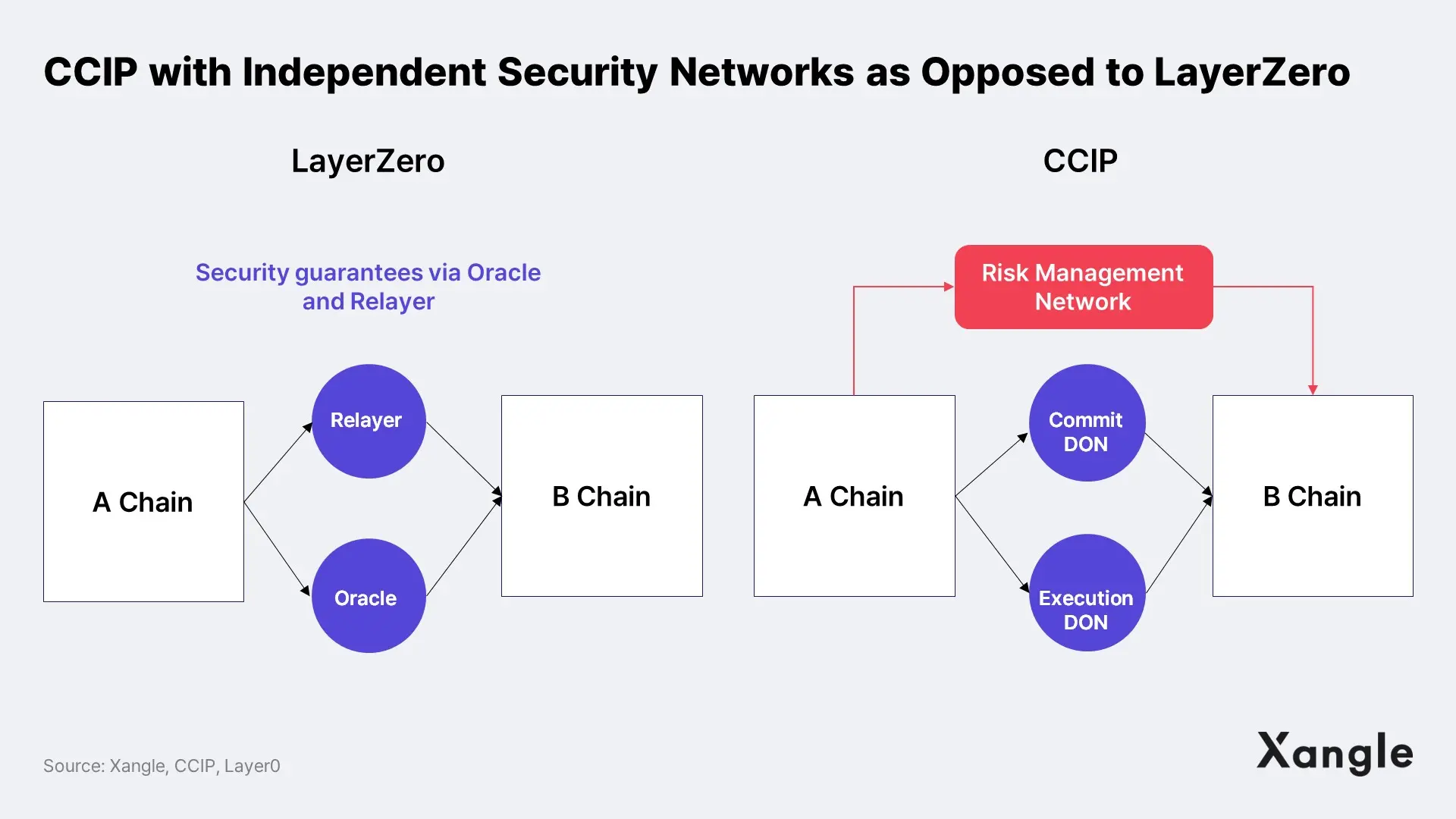

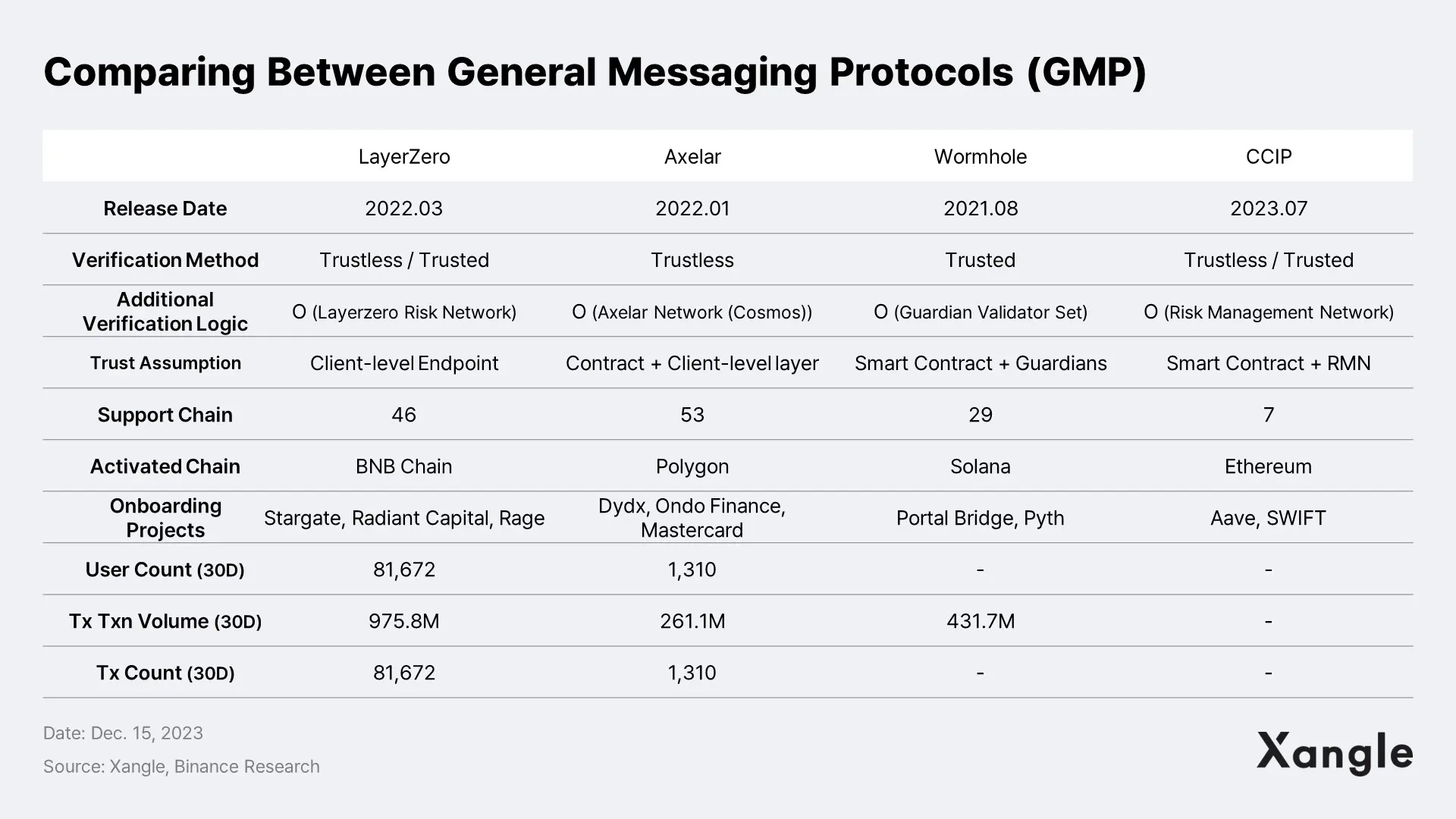

As the number of blockchains grows, the demand for cross-chain infrastructure to ensure interoperability will grow exponentially. While there have been bridging services that support cross-chain fund transfers, they are typically: 1) expensive, inconvenient, and time-consuming; 2) untrustworthy due to multiple hacks, including lock-and-mint-based bridges; 3) provide synthetic assets rather than native assets; and 4) fragmented asset liquidity across multiple chains. Moreover, existing bridges only support the movement of funds between chains, not complex cross-chain messaging. This is where LayerZero and Chainlink's CCIP come in to complement blockchain interoperability and support native cross-chain transactions.

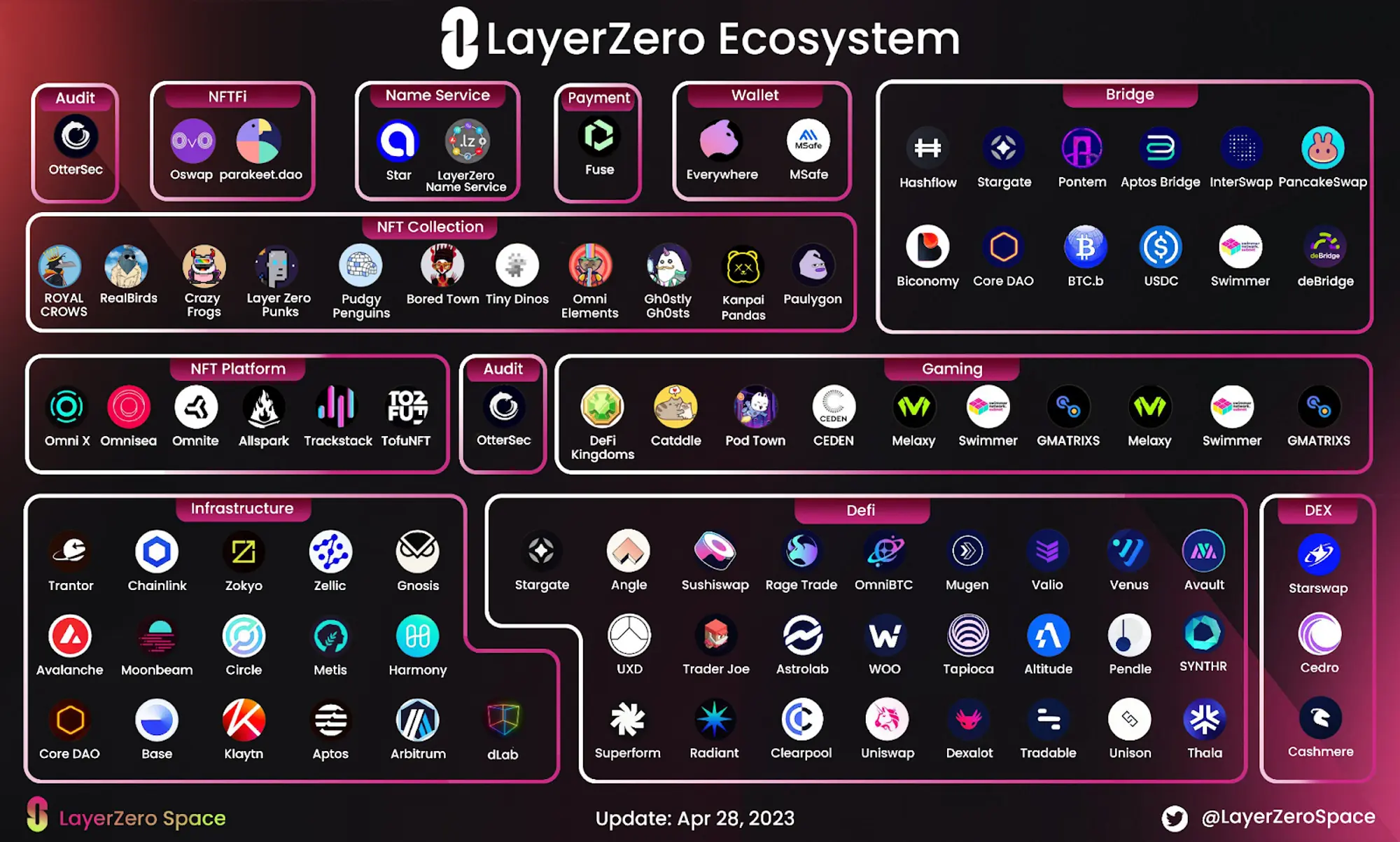

LayerZero is an endpoint running an interoperability protocol, utilizing oracles and relayers to send and receive messages. With strong security in modular form, low fixed and variable costs, and a rapidly growing ecosystem, LayerZero has the potential to become a cross-chain leader that will become a critical core infrastructure.

Source: LayerZeroSpace

In July, Chainlink announced the launch of a testnet for its Cross-Chain Interoperability Protocol (CCIP). Considered a rival to LayerZero, CCIP is rapidly expanding its services by leveraging the already established Oracle network and is positioning itself as a standard cross-chain solution, especially for connecting private chains in TradFi with public chains. And we expect CCIP to become a huge Web2 and Web3 standard in the future.

4-2. Alt-L1s will discover PMF centered on scalability and ease of development

The Ethereum Virtual Machine (EVM) is still a strong narrative in the blockchain market today. When we say EVMs, we don't just mean Ethereum, but blockchains that have forked Ethereum or are Ethereum-compatible. Some prominent examples of EVM chains include Polygon, BNB, Tron, and Klaytn.

The advantage of EVM-compatible chains is their strong interoperability with Ethereum and the EVM-based ecosystem. This allows expanded reach of users and projects, and the widespread use of the Solidity language makes it easy to absorb the developer community. Product development is also facilitated by the availability of a wide range of EVM-based libraries and tools. Thanks to these advantages, EVM chains have a market share of over 90% of the total blockchain market in terms of total value locked (TVL) and users. Solidity is still going strong as the most widely used blockchain programming language.

While it's true that many companies and projects are finding a home in L2 ecosystem based on EVM, there are plenty of opportunities for L1 blockchains other than Ethereum. Blockchain is still a nascent technology with a global penetration rate of around 2-3%, and it's unclear whether Ethereum will be able to achieve the same level of market dominance when the blockchain market begins to scale in the future. Each organization and project will choose a chain that fits their goals and needs, and non-EVM-based "Alt L1s" will be a viable option.

"Alt L1" refers to L1 blockchains that are not EVM-based. Alt L1s are trying to overcome Ethereum's main limitations of scalability and ease of development. Chains are emerging that use VMs that differ from the EVM structure or adopt different consensus algorithms and structures to provide high scalability at high speeds and low fees. There are also chains that provide a more convenient development environment by allowing the deployment of own chains, tokens, and smart contracts through CLI.

As the market continues to evolve, a variety of new requirements emerge. New opportunities are opening up for projects that need to be fast, projects that need development support, developers who prefer programming languages other than Solidity, and long-tail projects that need long-term support. Non-EVM Alt L1s are gaining ground in the market to meet these diverse needs. In this report, we will focus on Solana, Avalanche, and Move-based blockchains (Aptos and Sui).

4-2-1. SOLAVAX, without Luna, will be a major Alt-L1 in 2024

A. Solana

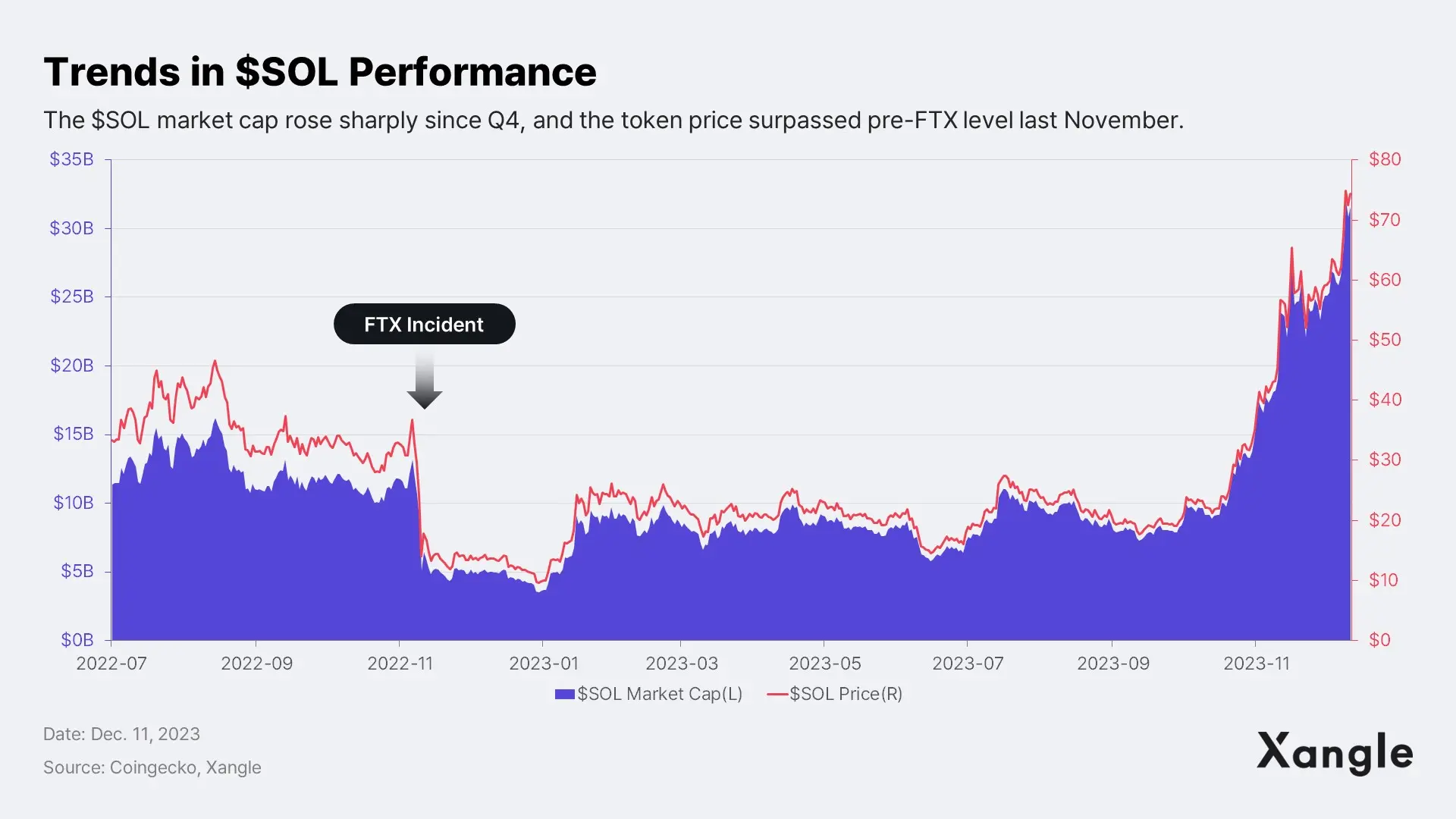

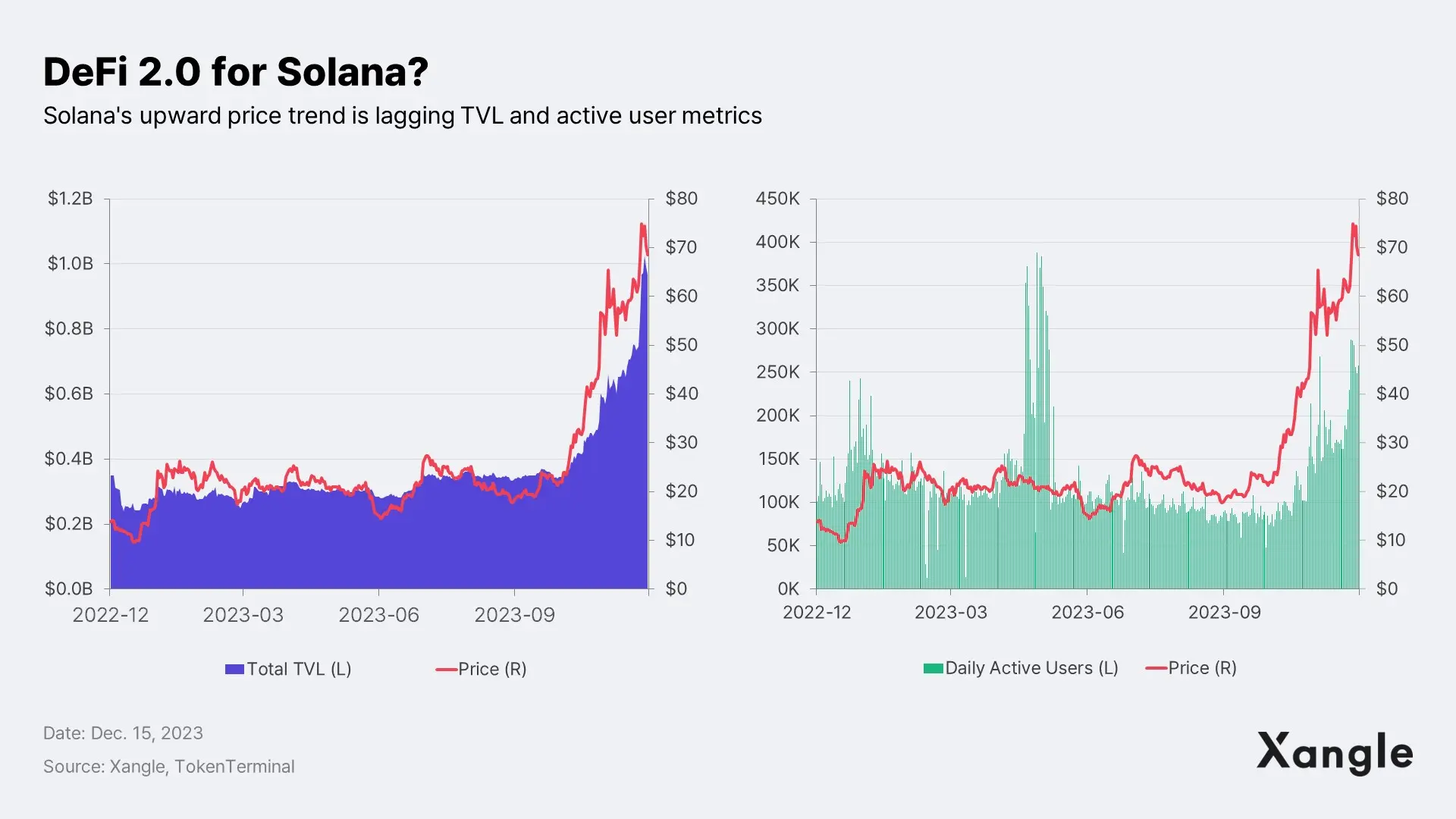

Solana began to be shunned by organizations and projects in 2022 due to ongoing network issues, and to make matters worse, its TVL and coin value plummeted after the FTX debacle in late 2022. However, despite its post-FTX struggles, Solana has proven to be resilient. In 2023, Solana has been the epitome of bottom-up growth, with a solid community built around small and medium-sized projects.

The continued growth of the Solana community has contributed to this recovery. Even during the $SOL price downturn, Solana continued to organize various ecosystem activities centered on real builders and fan base. Signs of a recovery began in January 2023 with the BONK token airdrop to the Solana community. Recently, the foundation and community have been working hard to help Mad Lads, a Solana-based NFT project, reach the top spot in 24-hour trading volume for all NFTs, including Ethereum.

Large-scale hackathons continued to be held, such as Sandstorm, organized by LamportDAO, a builder community of Solana contributors, and the Grizzlython and Hyperdrive hackathons organized by the Solana foundation. The Grizzlython hackathon was particularly well attended, with 10,000 participants and 813 submissions.

Solana's locally based community, Superteam, expanded to the United Kingdom, United Arab Emirates, and more, and the Superteam World Tour showed its commitment to expanding Solana's local community globally. Solana University, which supports student developers, is also active, bringing young developers and users into the ecosystem with global potential.

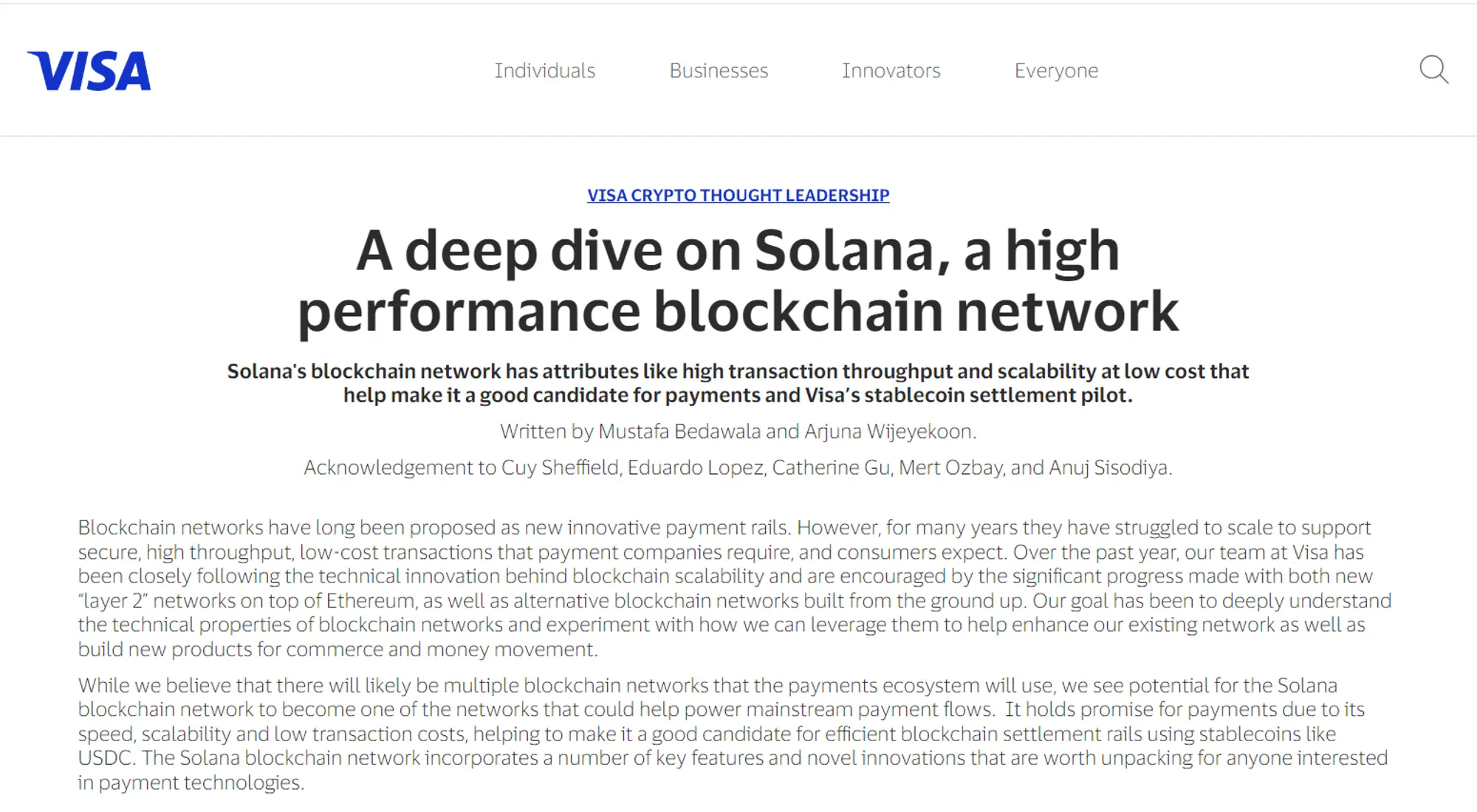

Source: VISA

Source: Solana

The Solana Foundation has also seen some big partnerships with major global companies last year, including Google Cloud, VISA, and Shopify, although they are fewer in number than other chains. These partnerships are a testament to Solana's proven track record of consistently delivering high throughput and low fees as it bounced back from setbacks. Notably, in announcing support for USDC payments on the Solana network, VISA stated that Solana has the potential to support major payment systems like VISA with its high-speed transaction processing, scalability, and low transaction costs. This proven chain performance suggests that Solana remains a technically sound solution for mass adoption.

With such a strong community and business favorability, Solana has been on a recovery trend, with the $SOL price returning to pre-FTX levels by Q4 2023. In 2023, Solana showed how important community and real-world users are to a blockchain, beyond just providing infrastructure and token incentives. With this lesson learned, we expect Solana to continue to grow this year with a developer-first mindset and high scalability.

B. Avalanche

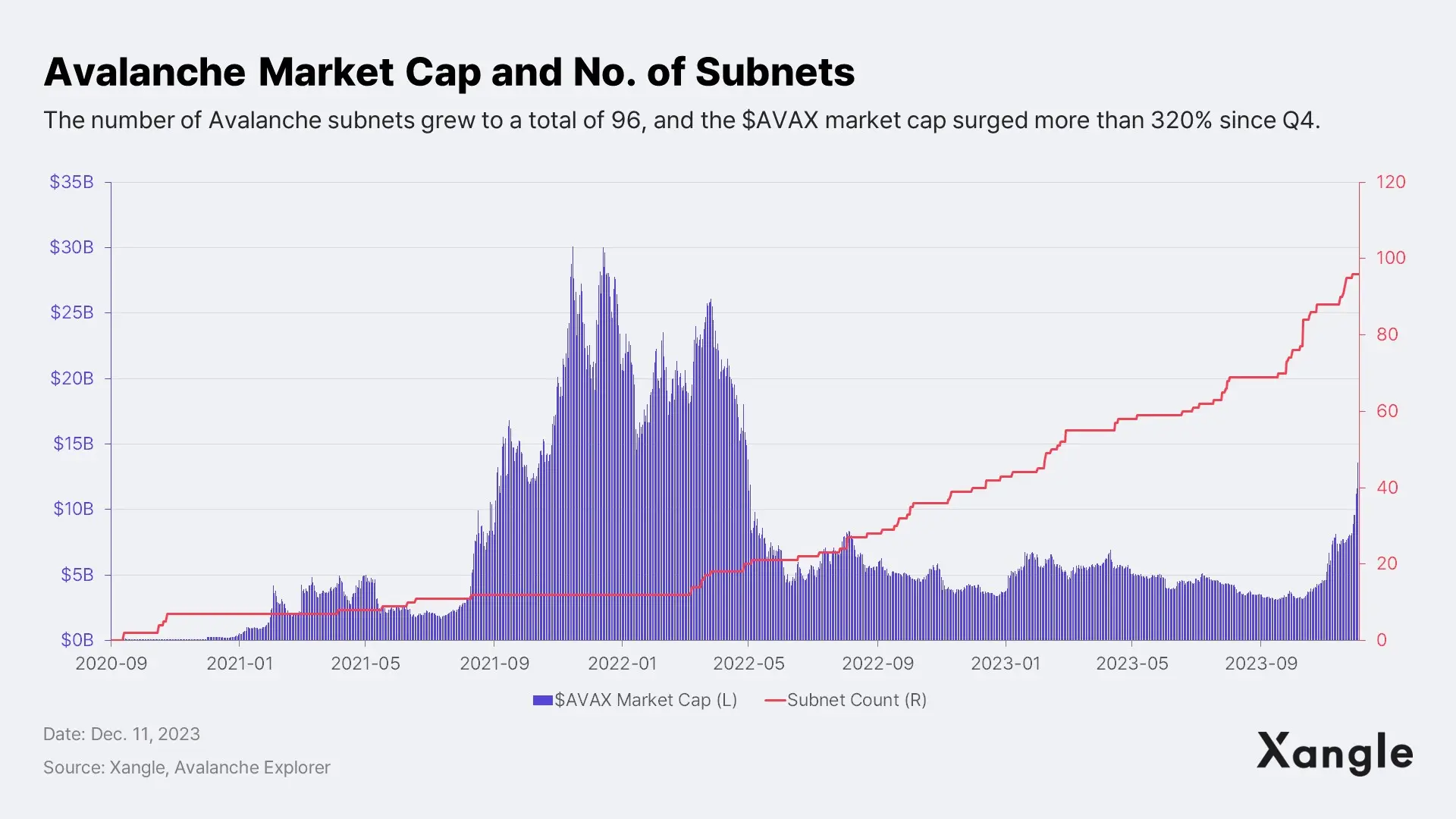

In contrast to Solana, which has an ecosystem centered on small and medium-sized projects, Avalanche is building its ecosystem from the top down, focusing on large enterprises. Avalanche has been actively adopted by global corporations and game companies such as JPM, Citi, SK, Shrapnel, and Off the Grid, among others, for its convenient subnet-centric blockchain development. As of December 10, 2023, the total number of subnets has increased to 96.

Avalanche is particularly strong in the financial sector with its subnet technology. Avalanche has significantly reduced the technical barriers for enterprises/institutions through its Evergreen Subnets to adopt blockchain by offering customized blockchains designed to meet their specific needs and industry-wide considerations. In July of 2023, Avalanche also launched "Avalanche Vista," a real-world asset (RWA) tokenization and investment initiative worth up to $50 million to accelerate the growth of RWA tokenization and on-chain finance.

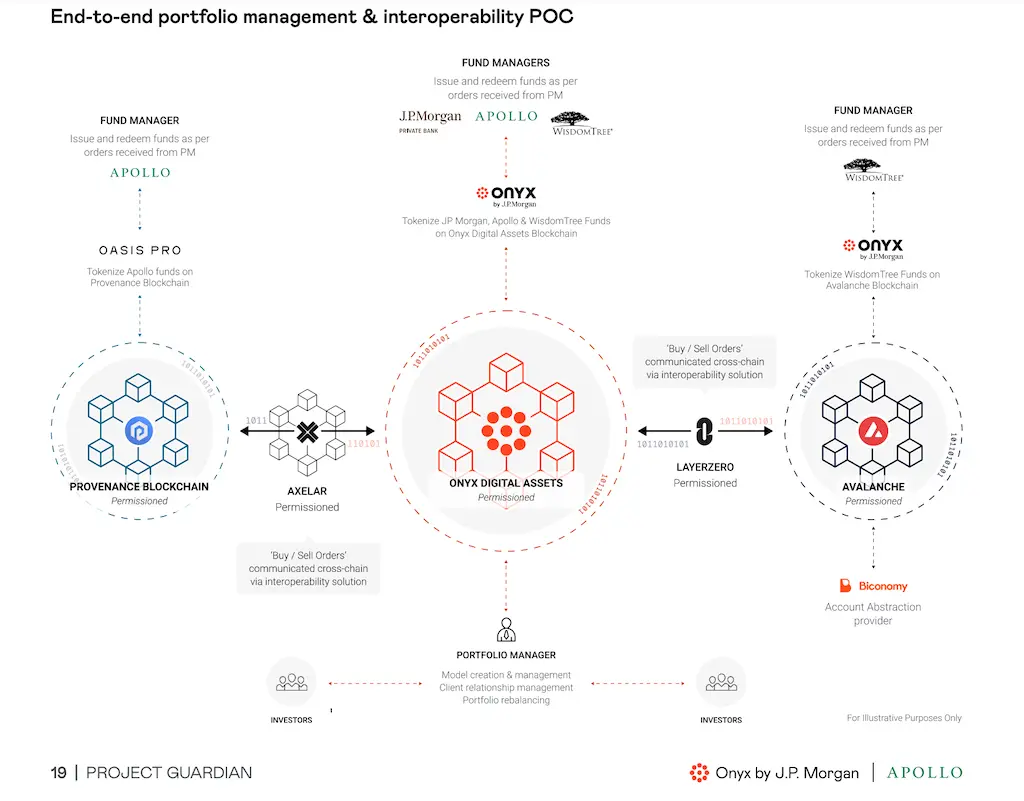

These efforts have led to some big wins in the financial sector last year, including the world's largest private equity firm KKR tokenizing with Avalanche. JPMorgan, participating in the Monetary Authority of Singapore's (MAS) DeFi pilot, Project Guardian, announced a Proof-of-Concept for wealth and asset management innovation utilizing Avalanche's Evergreen subnet, and Citi Group revealed that it has tested foreign exchange (FX) trading using Avalanche's Evergreen subnet.

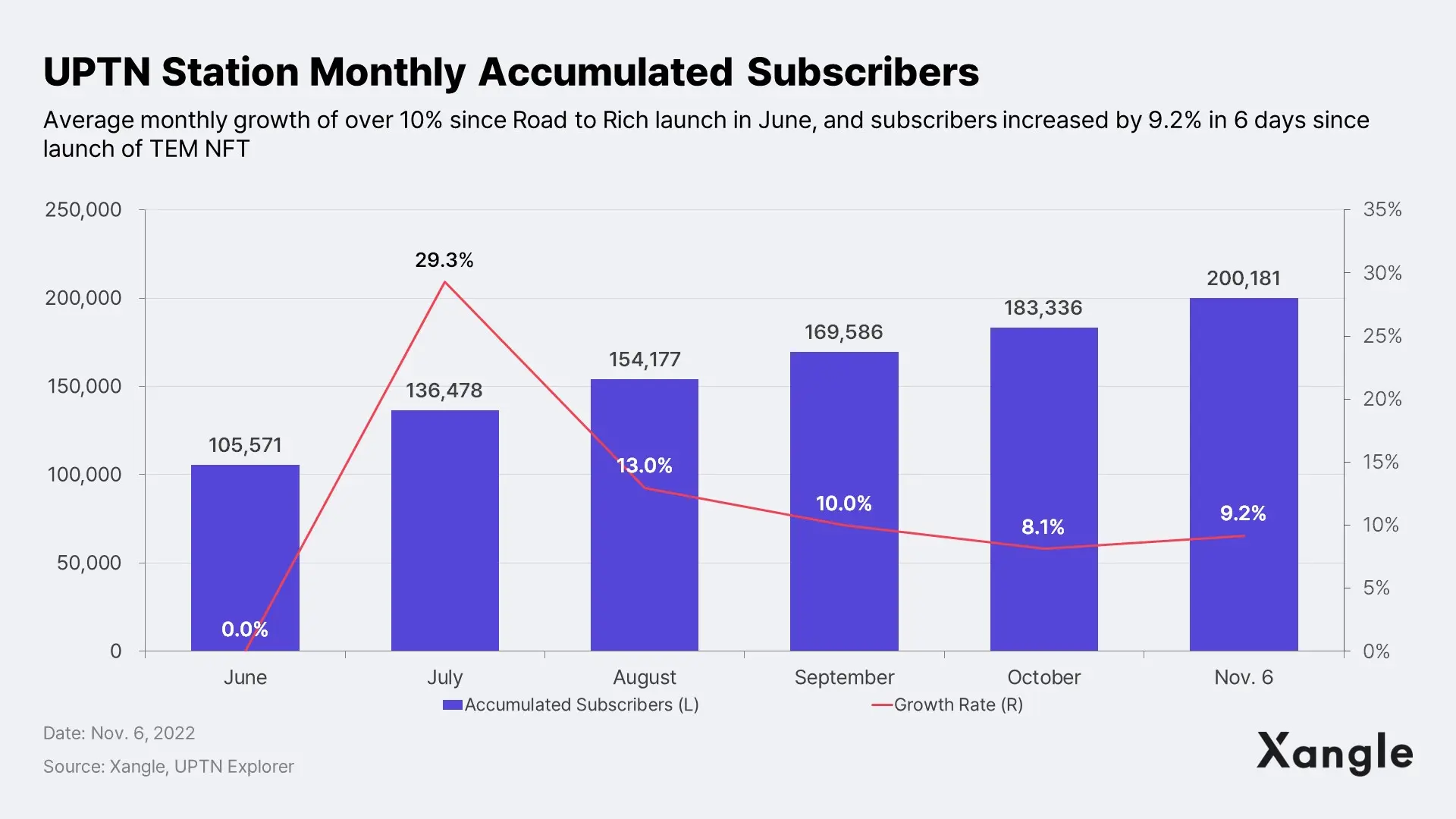

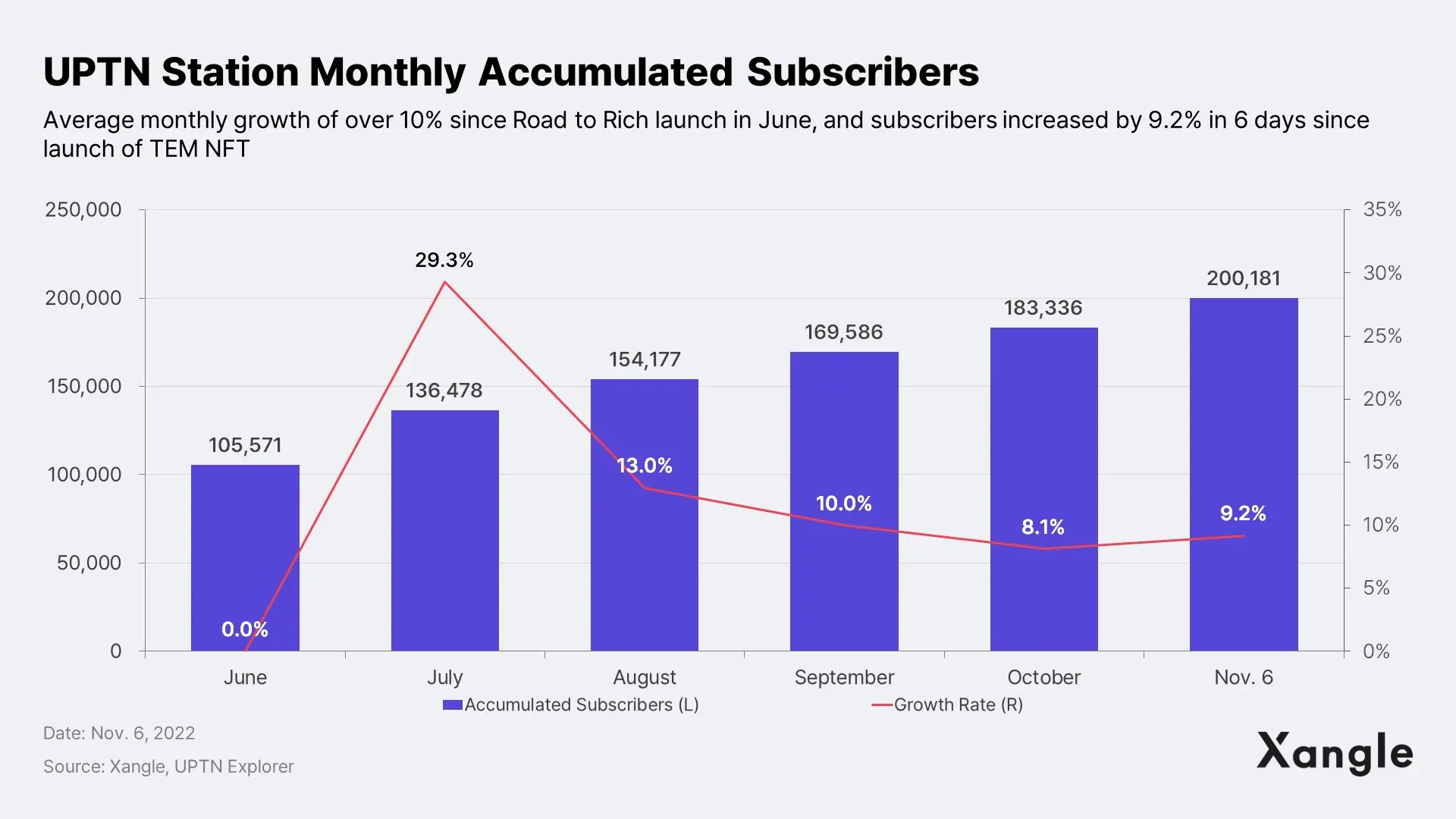

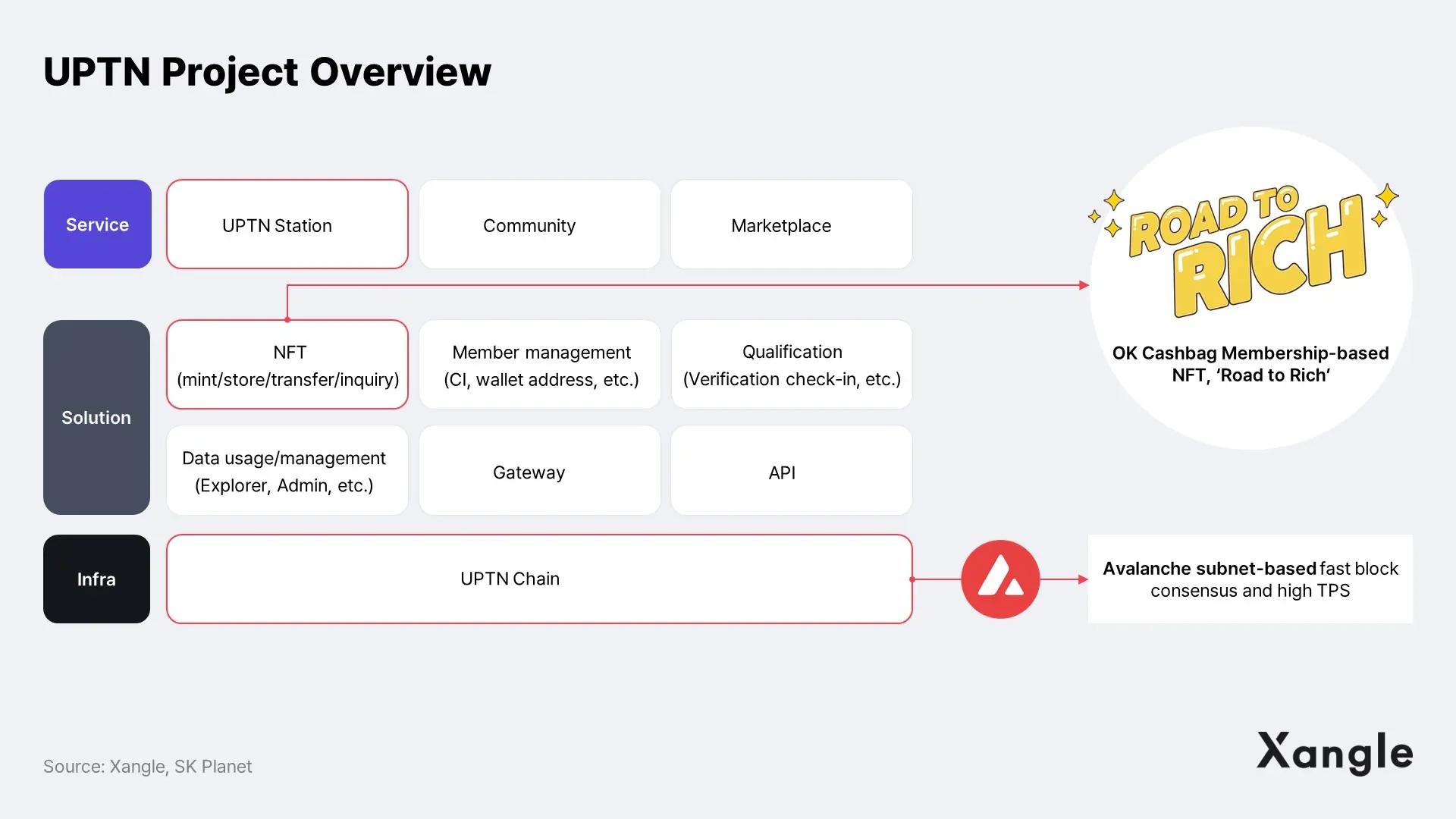

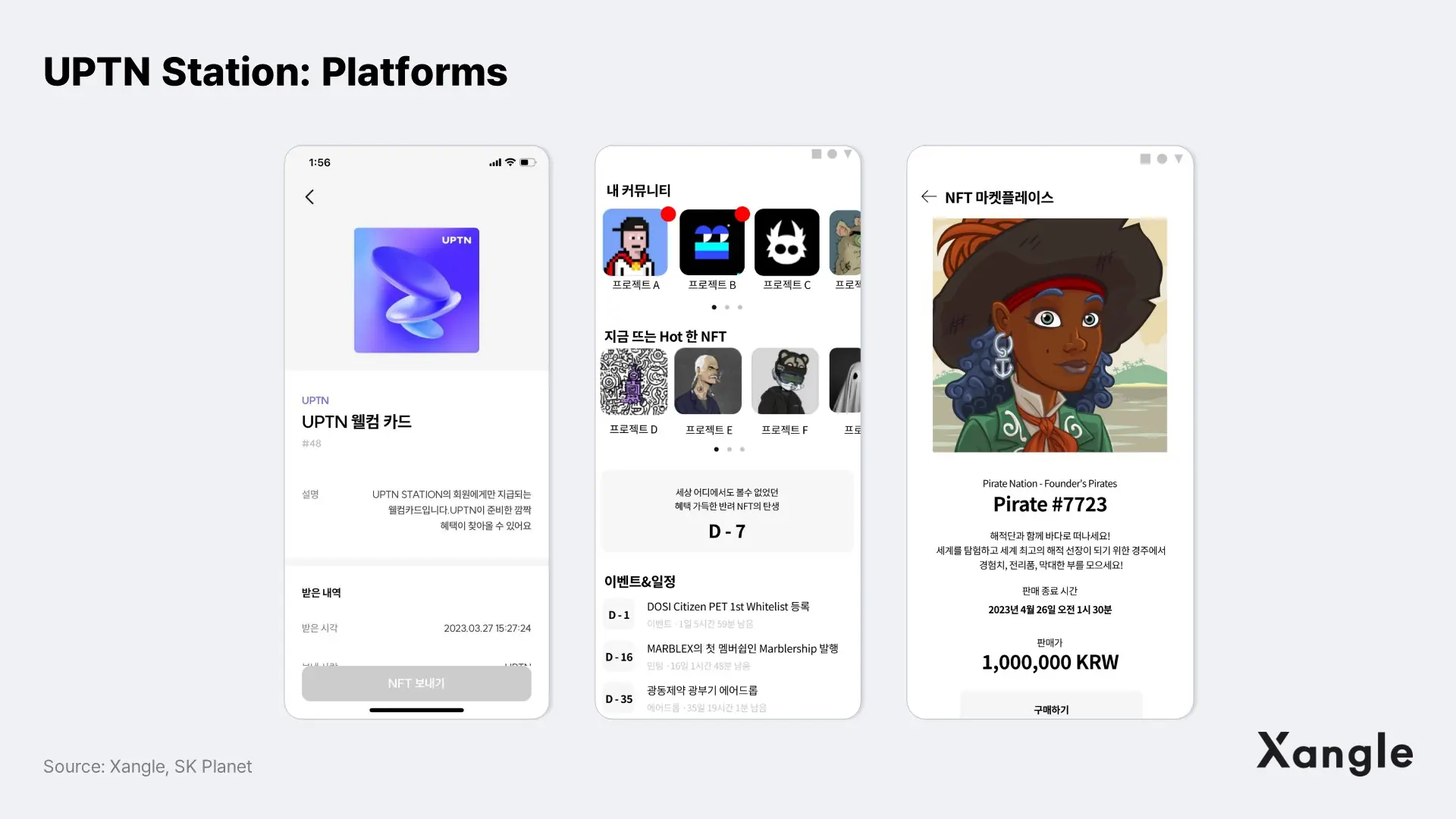

Meanwhile, the Avalanche-based UPTN project, led by SK Planet, is also showing impressive performance. UPTN is a Web3 service that aims to increase the universality of OK Cashbag points and improve profitability, and it plans to launch various services, starting with Road to Rich, to incorporate blockchain into real life. Unlike in PFP project, transaction fees occur in the process of users installing/removing TEM NFTs on Racky and secondary transactions actively occur to acquire desired TEM NFTs. This means Road to Rich is less affected by conditions of the cryptocurrency market and has relatively low revenue volatility and advantageous structure for profitability defense. According to Explorer data, the number of UPTN Station subscribers exceeded 200,000 as of November, six months after the service was launched, and the maximum number of transactions per day was 276k. For more details, please refer to "UPTN Project: SK Planet's Arc Reactor".

Finally, Avalanche is also expanding its ecosystem in the gaming sector by utilizing subnets. We've partnered with major game companies like GREE and Neowiz, and AAA game studios like Sharpnel and Off The Grid are actually building on the subnet. With many game companies like WEMIX, XPLA, Krafton, and others focusing on building their own chains, Avalanche's ability to easily deploy, manage, and build subnets through its Web3 launchpad, Ava Cloud, is a huge advantage.

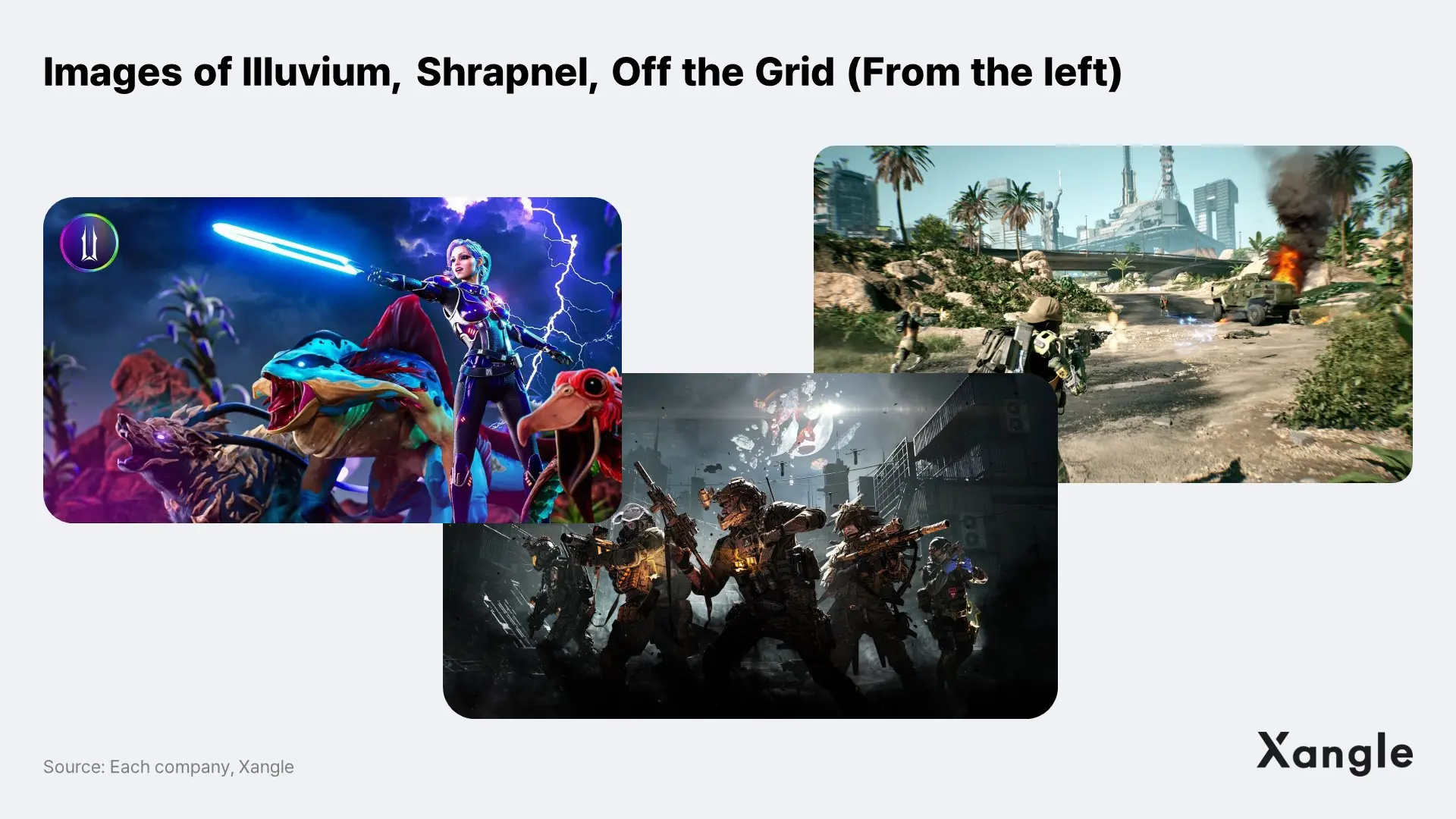

- Shrapnel: This AAA FPS game is built on Unreal Engine 5 and is being developed by the same team that brought us HALO, Call of Duty, and Westworld. Shrapnel has received funding from top VCs such as Polychain Capital and Dragonfly Capital. Set on Earth in 2044, players will be able to extract resources and fight battles in the game while creating content through an NFT economic system. The team behind Shrapnel said they chose the subnet for its customization and security, and are aiming to launch in 2024.

- Off The Grid: A cyberpunk battle royale game being developed by AAA game studio Gunzilla Games. Off The Grid will be integrated into the GUNZ platform, which is based on the Avalanche subnet and will offer an NFT-based digital economy system where players have full ownership. Through its partnership with Ava Labs, Gunzilla Games said it aims to "leverage the high scalability and security of the Avalanche subnet to provide the best possible gaming experience."

- DeFi Kingdoms (DFK): A P2E game originally launched on the Harmony chain, DeFi Kingdoms began supporting the Avalanche subnet with the launch of Crystalvale. As a subnet of DeFi Kingdoms, the DFK chain is generating the highest number of transactions and active addresses of all subnets.

- Dexalot: Dexalot is Avalanche's first Central Limit Order Book (CLOB) DEX, which aims to minimize slippage and custody risk. It is backed by the Avalanche Multiverse program in exchange for achieving subnet milestones and launched its subnet in February of last year.

- Beam: Merit Circle DAO launched this gaming project using the Avalanche subnet. The Beam subnet operates independently and provides customized services for both gamers and game developers. Beam is using Merit Circle DAO's token ($MC) as its gas and the DAO's governance token. The project offers a variety of games and infrastructure products, which will initially include games like Trial Xtreme, Walker World, and Hash Rush.

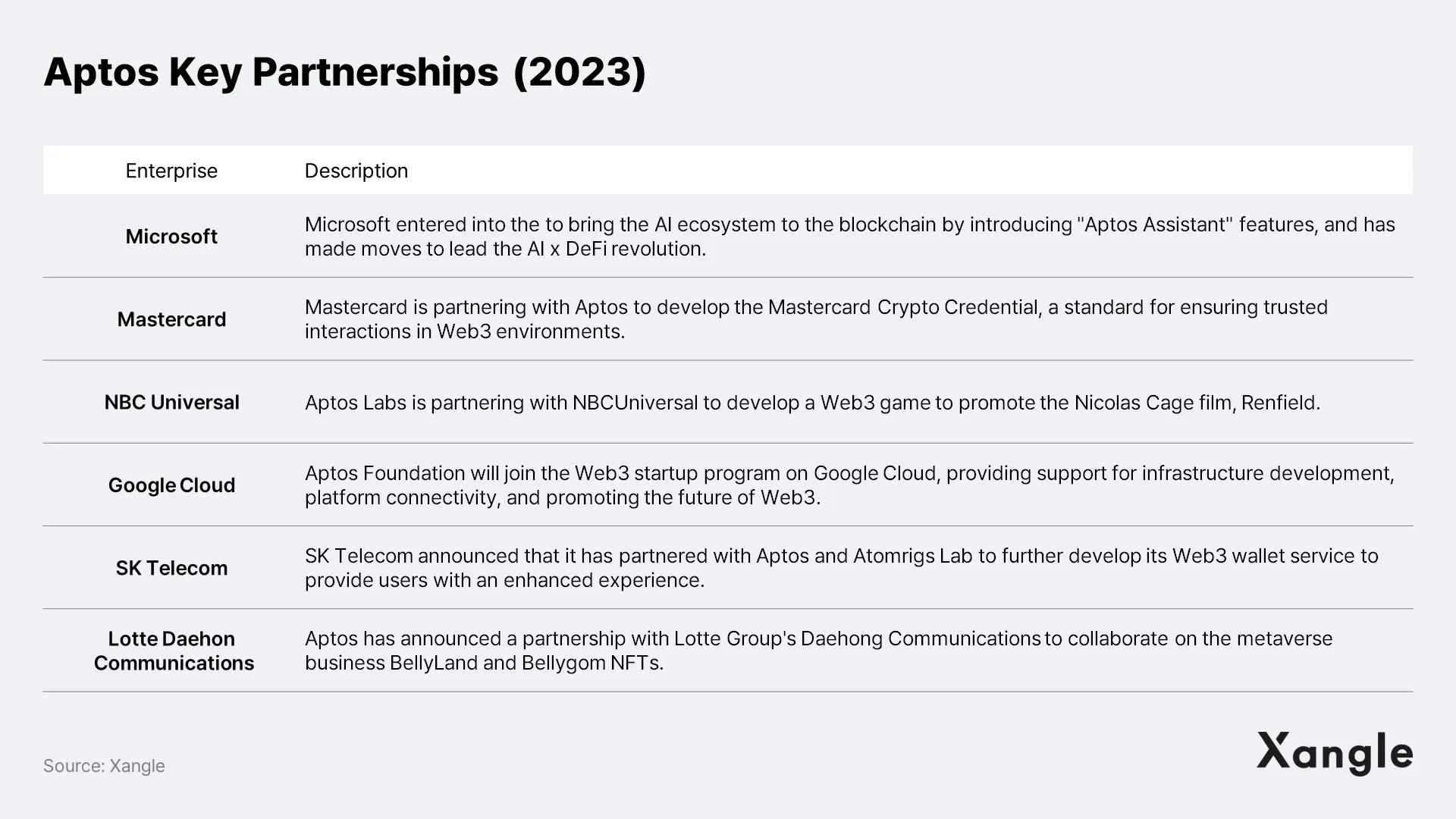

4-2-2. I Like to Move It Move It: Facebook giants surfacing

With the advancement of blockchain technology, new chains have recently begun to gain traction, including Aptos and Sui, part of the Move family of so-called "Next Generation Chains". Aptos and Sui are based on the Move language, which was derived from Meta's (formerly Facebook) blockchain project Diem.