Polygon as the Base Rail of Finance

Table of Contents

1. Real Money Still Resides in Traditional Finance

2. Global Payments Across Asia

3. Open Money Stack: Polygon’s Strategy for 2026

4. Traditional Finance Partnerships: Integration into Payment Infrastructure

5. Conclusion: Polygon as the Base Settlement Rail

1. Real Money Still Resides in Traditional Finance

1-1. Crypto vs. Traditional Finance: Scale Asymmetry

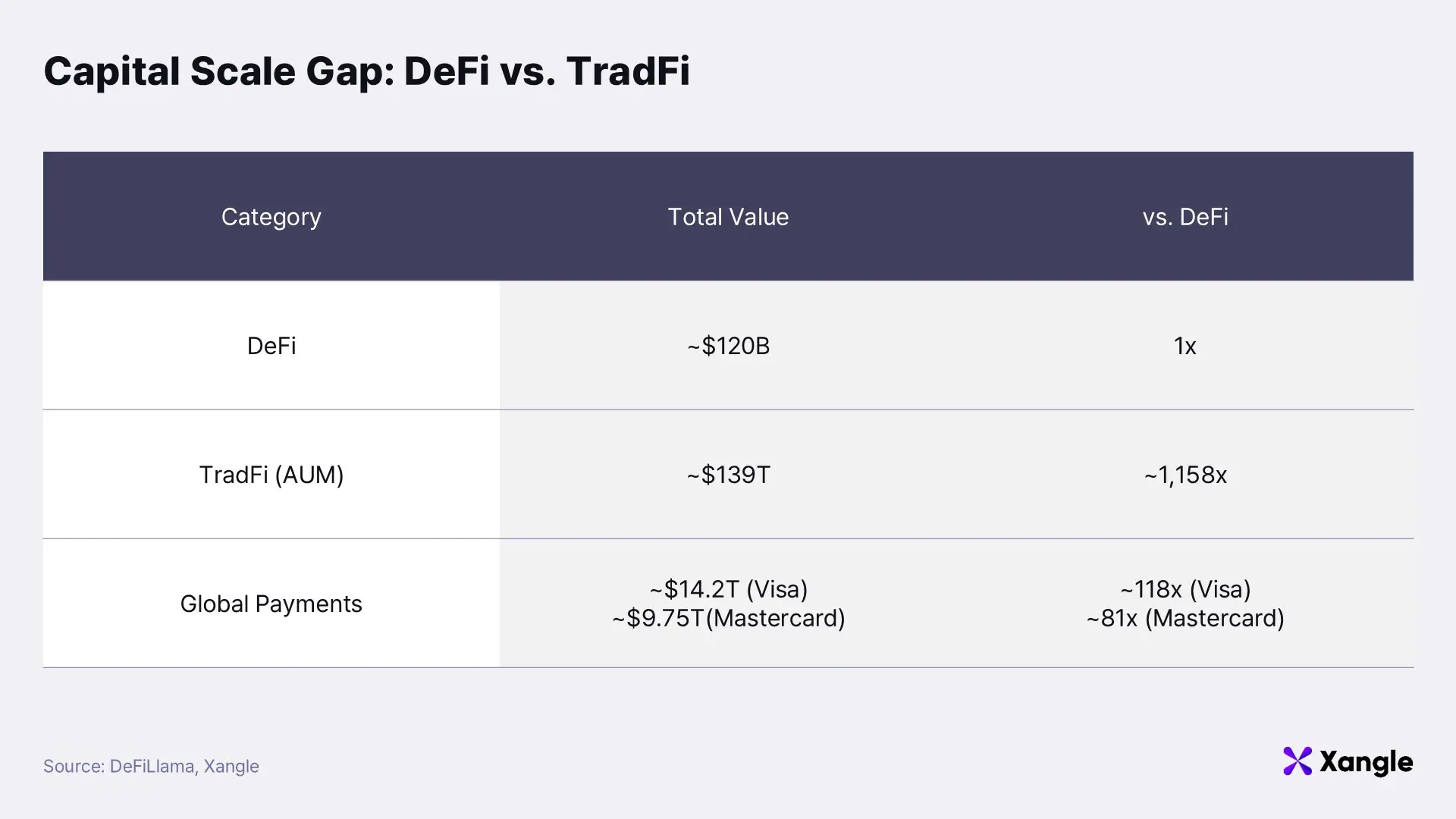

Crypto emerged from a narrative centered on replacing traditional finance. A comparison of capital allocation today reveals a structurally asymmetric reality: traditional finance continues to dominate in scale. According to DeFiLlama, total capital deployed across the crypto DeFi ecosystem remains at approximately $120B in TVL. By contrast, traditional financial assets managed by global asset managers are estimated at roughly $139T, implying a scale gap of nearly 1,000x.

The scale gap reframes where meaningful growth opportunities reside. Rather than competing over constrained liquidity within crypto-native markets, the more consequential opportunity lies in connecting the capital pools embedded in traditional finance to on-chain settlement environments. Achieving this connection represents one of the clearest paths to expanding crypto’s effective market size.

Polygon’s strategic pivot beginning in 2024 should be read against this backdrop. As outlined in the prior research, “Polygon (POL)’s Counterattack Begins,” the network moved beyond a generic Layer 2 positioning and accelerated its transition toward a finance-infrastructure-centric role alongside the token rebranding from MATIC to POL. Stablecoins, payments, and real-world asset (RWA) tokenization were defined as the primary vectors for establishing direct exposure to traditional financial capital flows.

1-2. Enterprise Adoption: Polygon’s Public-Chain Positioning

Enterprise trust in Polygon did not emerge by coincidence. It reflects an infrastructure strategy shaped early around operational reliability, regulatory compatibility, and real-world deployment requirements rather than purely crypto-native experimentation.

Enterprise collaborations involving Polygon illustrate how this positioning took form over time. These integrations were not framed as short-term pilots or marketing exercises; instead, they accumulated incrementally as Polygon demonstrated viability in live production environments.

Operational validation has been central to this process. Full EVM compatibility allowed Polygon to leverage an established developer ecosystem, while low fees and predictable settlement mechanics aligned the network with the needs of ongoing service operations.*

RWA adoption further reinforces this trajectory. BlackRock’s selection of Polygon for its BUIDL fund signals more than partnership alignment; it confirms that a public blockchain can satisfy the operational, settlement, and compliance standards expected by traditional financial institutions. As of January 2026, Polygon-based RWA TVL is estimated at approximately $1.1B, up from $400M in January 2025.

Around-the-clock liquidity and integrated cross-chain settlement via AggLayer materially reduce the constraints imposed by operating hours and jurisdictional boundaries. Tokenized assets such as government bonds, real estate, and private funds are therefore shifting from static issuance instruments toward assets that can be actively settled and transacted within a unified financial infrastructure.

2. Global Payments Across Asia

Polygon’s recent expansion has been most visible in stablecoin-based payments. Rather than pursuing higher TVL or short-term liquidity inflows, Polygon’s payments strategy is oriented toward sustained, everyday usage. The intended end state is not institution- or high-net-worth–driven activity, but an environment in which stablecoins are repeatedly used by ordinary users across daily economic transactions. From this perspective, Polygon’s position in payments is better assessed through usability metrics—such as active stablecoin addresses and transaction counts—than through aggregate stablecoin supply.

The regions where stablecoin payments transition into real-world usage most quickly differ markedly from mature financial markets. Adoption has accelerated first in Asia and emerging markets, where remittance costs remain high and currency fragmentation is pronounced. Polygon has deliberately concentrated on these markets, prioritizing a network environment optimized for high-frequency, low-value, cross-border payments through low fees and fast settlement. As a result, stablecoin usage on Polygon has accumulated earlier and more consistently in these regions. This pattern reflects strategic alignment with market structure rather than organic or incidental diffusion.

This section examines how Polygon’s approach materializes across on-chain indicators and region-specific usage data, highlighting the relationship between network design choices and observable payment behavior.

2-1. What Stablecoin Metrics Reveal About Polygon

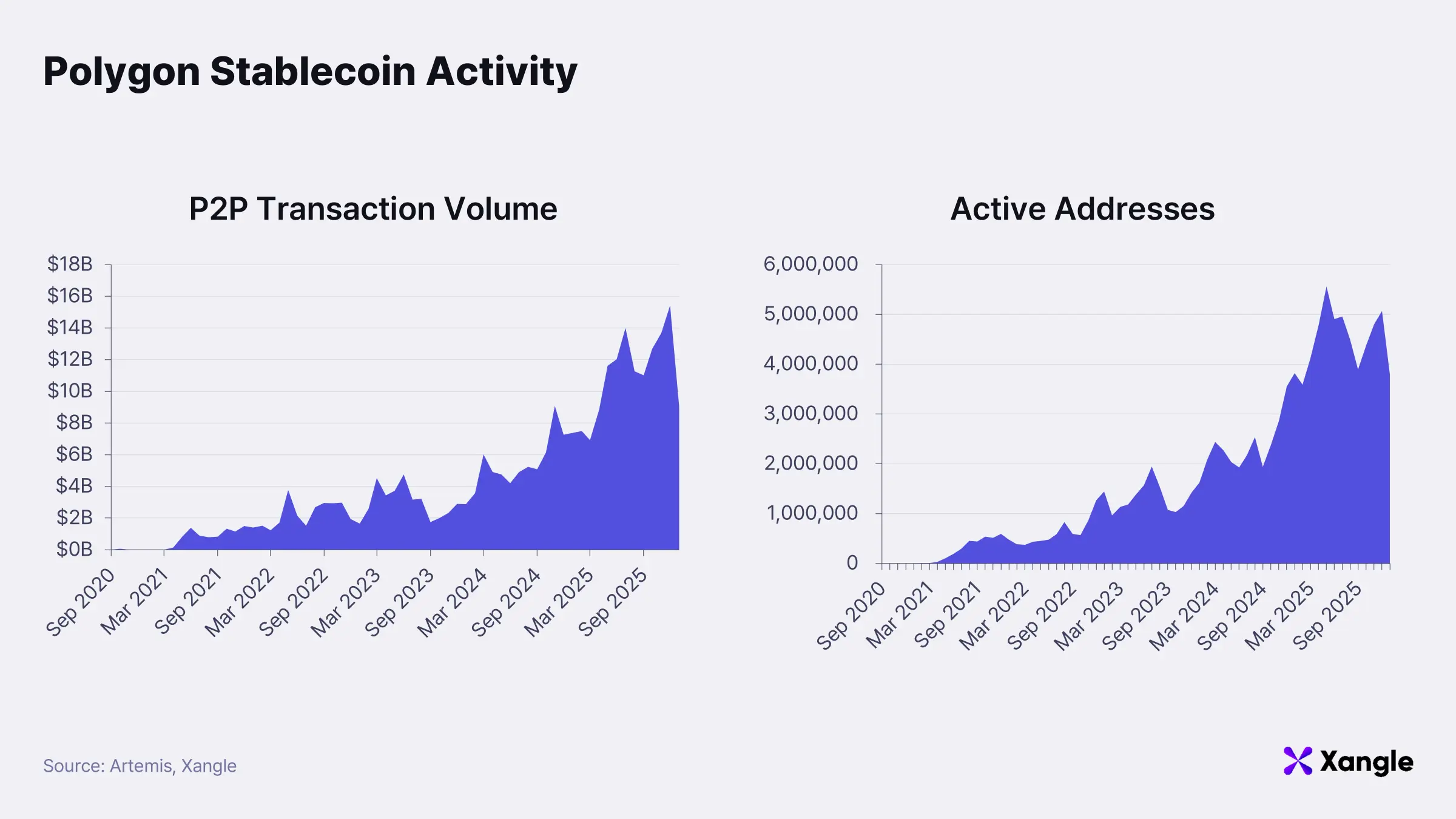

Polygon’s stablecoin on-chain metrics point to a clear direction in how the network is being used as payments infrastructure. Activity observed on Polygon is shaped less by large-scale capital deposits or short-term liquidity rotations, and more by transactions tied to repeated, everyday usage. Over an extended period, both P2P transaction volume and the number of active addresses have increased gradually, while baseline activity levels have continued to rise. This pattern suggests sustained usage by existing participants, rather than transaction growth driven solely by short-term user inflows.

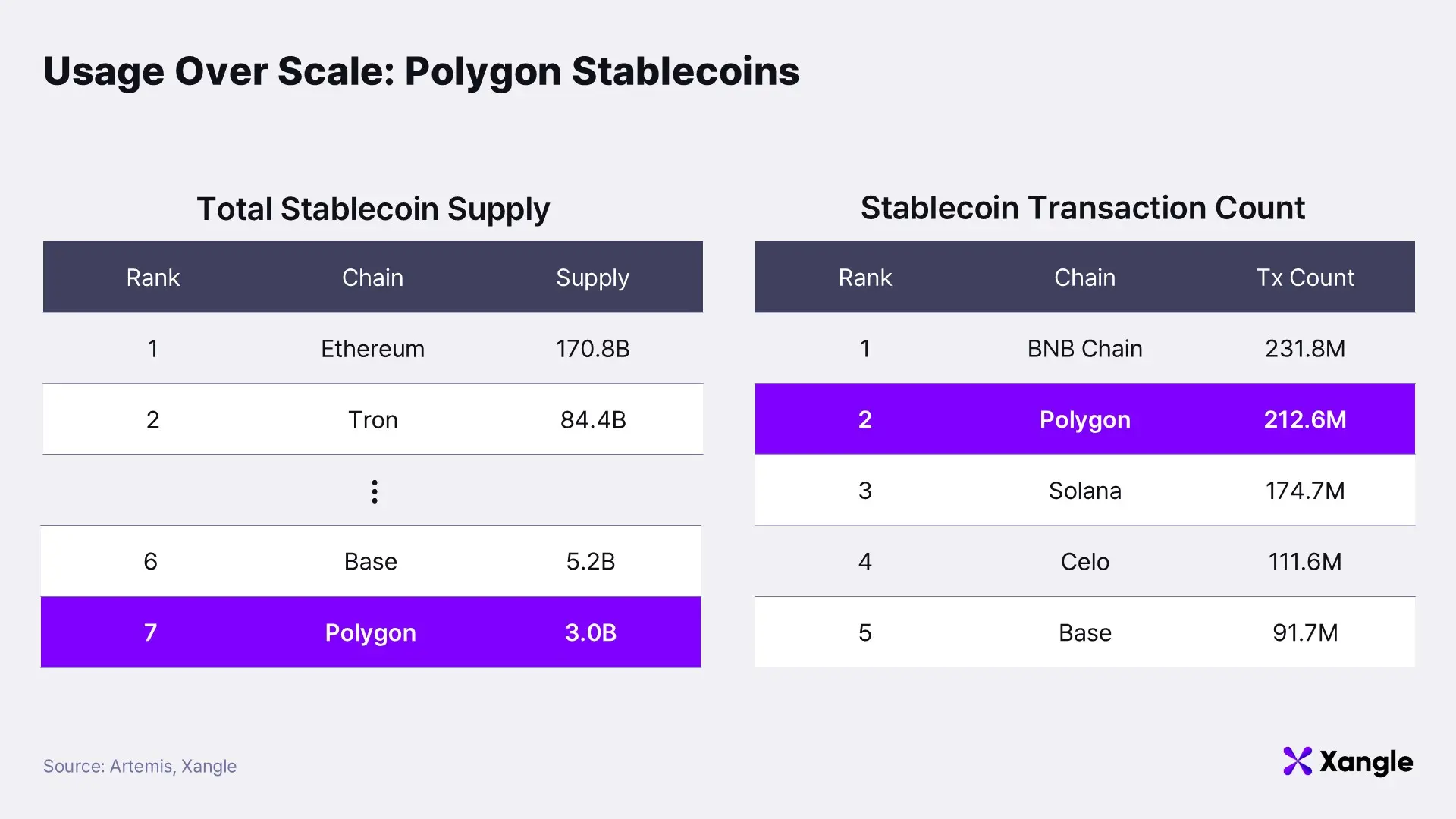

A comparison across chains further clarifies this positioning. In terms of total stablecoin supply, Polygon remains relatively lower-ranked than leading chains. By transaction count, however, it consistently holds a top-tier position, ranking second overall. The divergence between supply and transaction activity indicates that stablecoins on Polygon function less as long-term stores of value and more as transactional currencies actively used for payments and transfers.

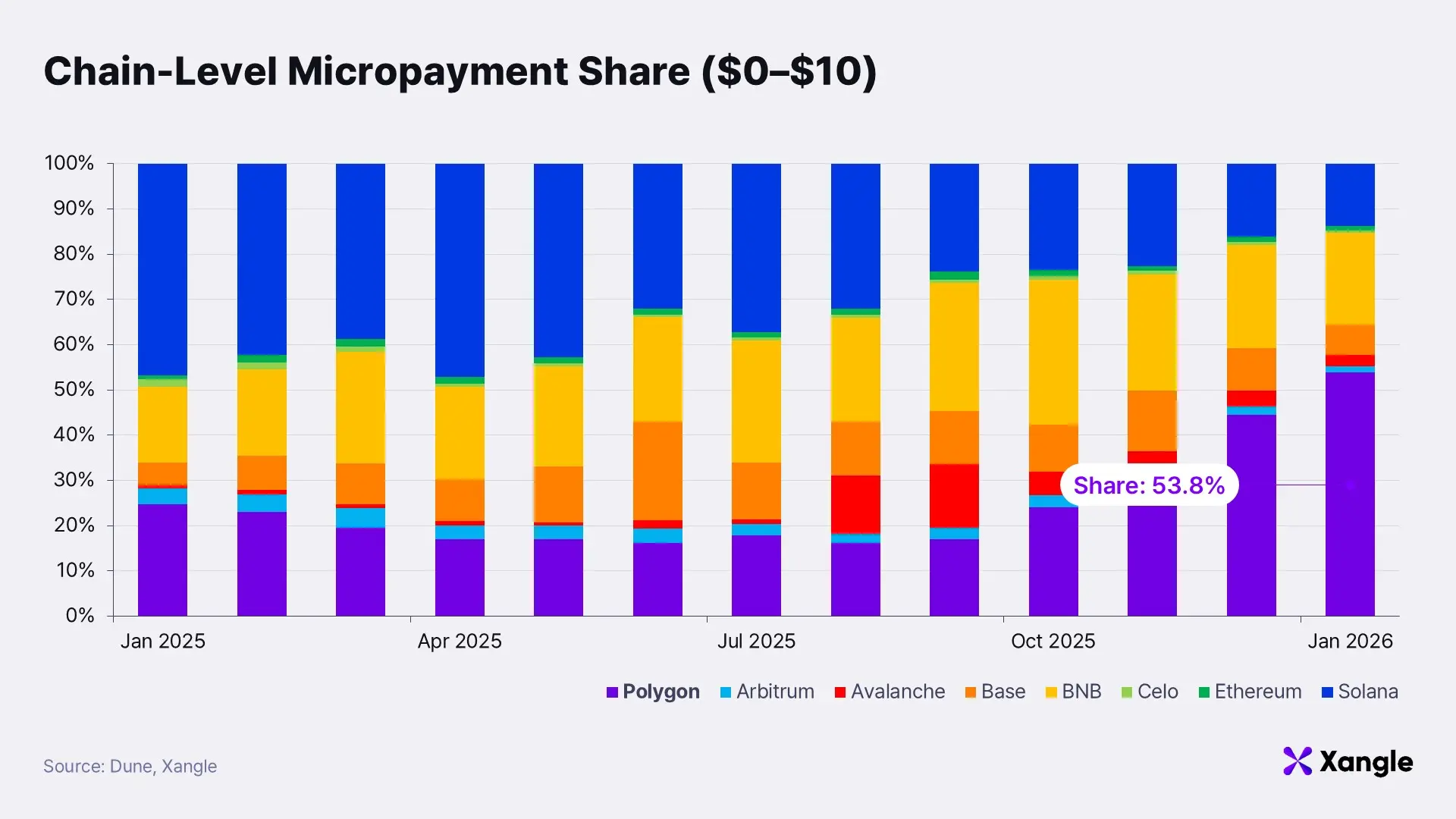

Usage patterns in the micropayment segment reinforce this interpretation. When transaction volumes in the $0–$10 range are broken down by chain, Polygon accounts for the largest share among the networks analyzed, representing 53.8% of total activity. This concentration reflects how Polygon’s technical characteristics, notably low fees and fast processing speeds, translate directly into user behavior and support frequent, small-value transactions.

Taken as a whole, these metrics position Polygon not as an asset custody–oriented chain, but as a usage-centric network where payments and remittances occur repeatedly in practice. Such a profile aligns closely with the structural conditions of Asia and emerging markets, where financial infrastructure remains fragmented and sensitivity to transaction costs is high. Within this context, Polygon’s stablecoin activity forms a structural foundation for its expansion as a global payments layer.

2-2. Asia’s Emerging Non-USD Stablecoin Network

Polygon’s presence extends beyond USD-denominated stablecoins into the non-USD segment, where it has established comparatively strong traction. This pattern reflects how on-chain settlement tends to gain practical adoption first in emerging markets, where inefficiencies in payment and remittance infrastructure remain unresolved, rather than in large and fully mature financial systems. Asia, in particular, combines high non-USD currency usage with concentrated cross-border remittance demand, creating favorable conditions for early network formation around stablecoin-based payments.

Within this environment, Polygon has secured a leading position in Singapore dollar (SGD)–denominated stablecoins, one of the region’s primary financial hub currencies. High adoption in SGD positions Polygon as a core settlement layer for non-USD stablecoin payments in Asia. Given the importance of early network effects in stablecoin and payments markets, this positioning carries strategic significance that extends beyond short-term activity metrics.

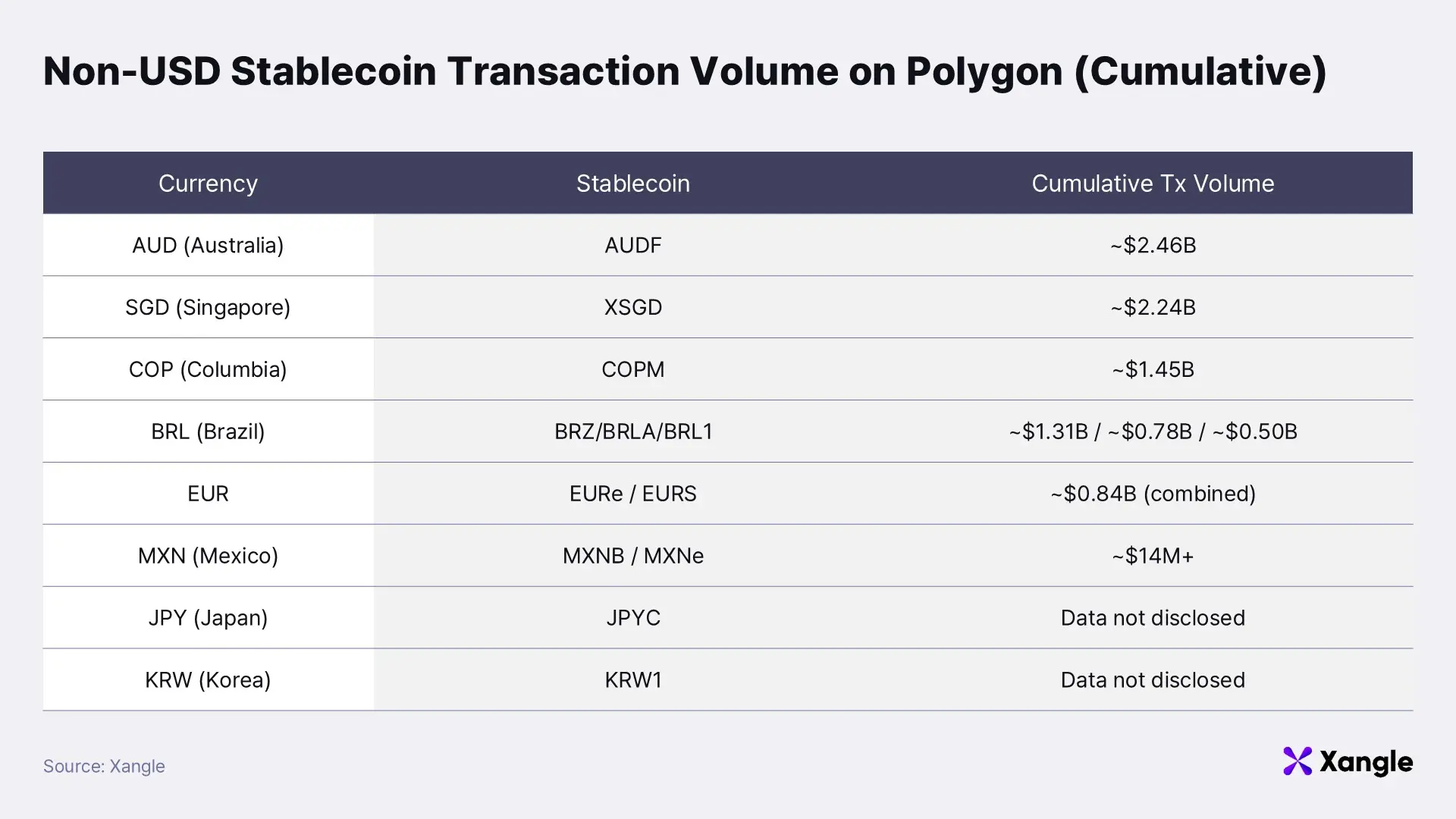

Local-Currency Stablecoin Adoption

Data released by Polygon in December 2025 shows cumulative non-USD stablecoin transfer volume on the network exceeding $11.1B, accounting for more than 43% of total non-USD transfers across major public blockchains. The significance of this figure lies not in dominance within a single currency or geography, but in the simultaneous accumulation of transactions across multiple local-currency stablecoins on a shared network.

Southeast Asia illustrates this concentration most clearly. XSGD represents more than 70% of non-USD stablecoin transactions in the region, and as of Q4 2025, over 60% of all XSGD transactions are processed on Polygon. At the same time, stablecoins denominated in Australian dollars (AUD), Colombian pesos (COP), Brazilian reals (BRL), euros (EUR), Mexican pesos (MXN), Japanese yen (JPY), and Korean won (KRW) are actively used in parallel. This breadth indicates that non-USD payment activity on Polygon is not confined to a single country or corridor, but is expanding concurrently across multiple currency zones.

Observed usage patterns reinforce the view that non-USD stablecoins on Polygon are functioning as payment infrastructure rather than speculative instruments. While USD stablecoins continue to play a central role in global liquidity and value storage, real-world commerce and remittance flows favor alignment between payment currency and accounting currency for cost and settlement efficiency. Transaction volumes in AUD-, SGD-, COP-, BRL-, EUR-, and MXN-denominated stablecoins on Polygon demonstrate that this demand is increasingly met without routing through USD.

Equally important, non-USD usage on Polygon is not concentrated in a single stablecoin or market. Multiple local currencies operate simultaneously on the same public infrastructure, indicating that Polygon functions as a shared settlement rail rather than a collection of isolated payment projects. Once established, payment routes and liquidity can extend rapidly to additional currencies and regions. This cumulative effect creates structural advantages that are difficult for later entrants to replicate within a short timeframe.

3. Open Money Stack: Polygon’s Strategy for 2026

https://polygon.technology/vision-open-money-stack

Payment and remittance activity observed on Polygon no longer fits the profile of short-lived campaigns or isolated application success. Stablecoin transfer volumes, non-USD currency usage, and repeated small-value transactions concentrated in Asia and emerging markets point to a network already operating as a payment rail in practice. The question now is not whether this usage exists, but how it can be scaled and sustained as long-term financial infrastructure. This section examines Polygon’s answer to that question through the “Open Money Stack” strategy announced in December 2025.

3-1. Polygon as a Financial Infrastructure Stack

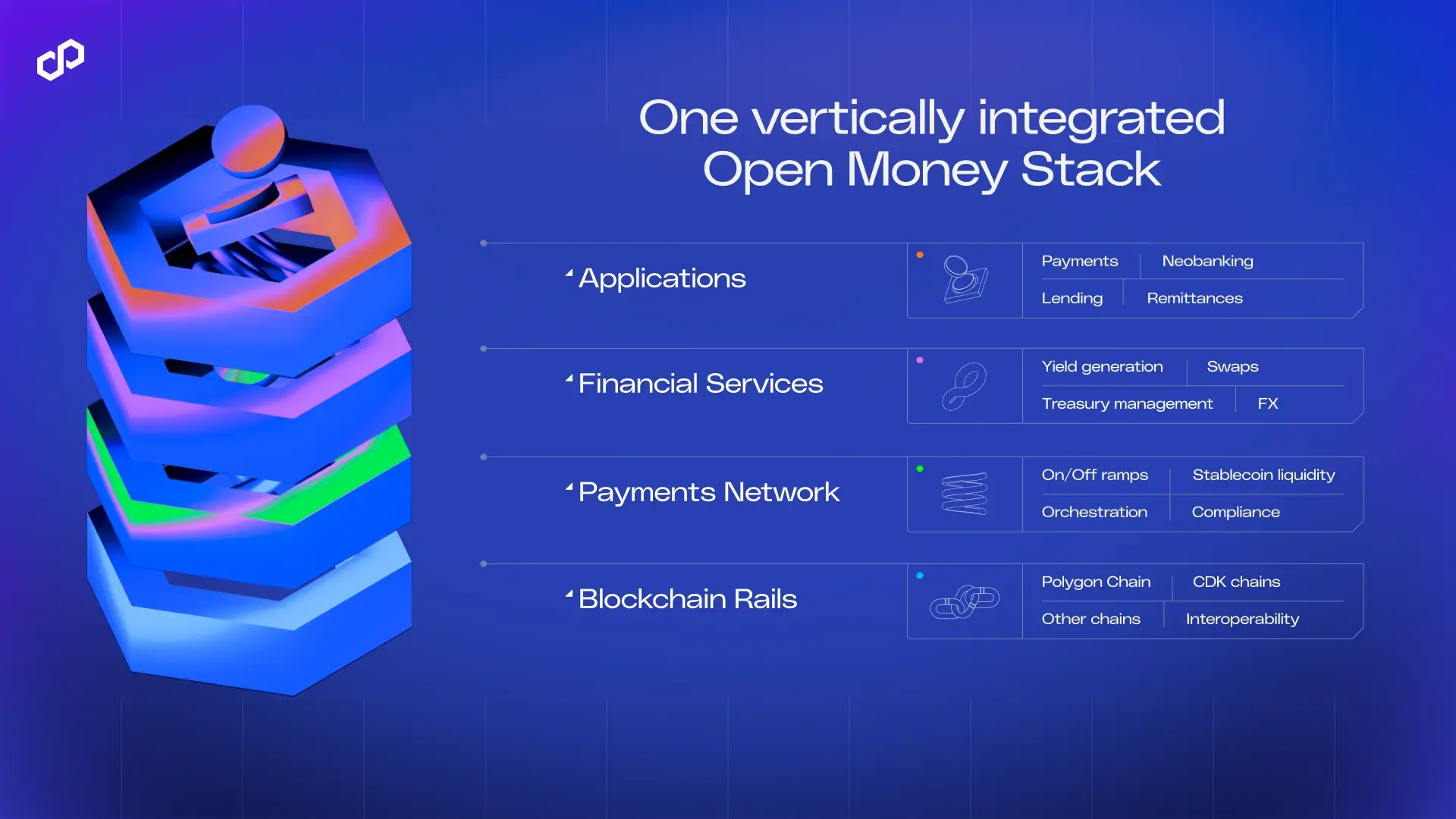

The Open Money Stack is designed to shift the default state of payments and remittances to on-chain execution. Its defining feature is the unification of the full financial flow: funds are brought on-chain through onboarding, securely stored via wallets, routed automatically across chains and assets through orchestration and cross-chain mechanisms, and settled in compliance with regulatory requirements. Rather than offering discrete tools, the Open Money Stack presents this process as a single, cohesive infrastructure layer in which payment and settlement operate natively on-chain.

Limited adoption of on-chain payments in global financial systems has stemmed less from blockchain performance or fee structures than from operational friction at the point of integration. Enterprises introducing on-chain payments are required to build and manage wallet infrastructure, connect on- and off-ramps across jurisdictions, and address cross-chain settlement and regulatory compliance as separate challenges. Under such conditions, on-chain payments are often viewed not as efficiency upgrades, but as sources of additional cost and execution risk.

The Open Money Stack addresses these constraints at the infrastructure level. On-chain payments are positioned not as a standalone service, but as a layer that integrates directly into existing financial workflows. The intended outcome is an environment in which enterprises can adopt on-chain settlement without explicitly selecting, operating, or managing blockchain components. At its core, the Open Money Stack represents a form of structural standardization, allowing on-chain payments to function as a native extension of conventional financial infrastructure rather than an external system layered on top.

3-2. From Fragmentation to a Unified Payment Stack

Operational friction becomes most visible when on-chain payments are introduced into live services. On- and off-ramps remain fragmented across jurisdictions and currencies, frequently breaking payment continuity. Wallet user experience continues to lag behind conventional payment systems, while cross-chain bridges add cost and operational overhead. As transaction volumes scale, regulatory compliance and operational management burdens increase in parallel. These constraints interact with one another, limiting the effectiveness of improvements made at the level of individual components.

Polygon approaches these challenges as a single infrastructure problem rather than a set of isolated issues. The Open Money Stack consolidates wallets, on- and off-ramps, cross-chain settlement, and regulatory compliance into one integrated stack. The objective is not incremental optimization of individual features, but a reduction in complexity and cost at the system level for adopting on-chain payments.

This architectural shift changes the role enterprises play in payment execution. Responsibilities related to wallet management, user onboarding, and regulatory handling move away from individual companies and into the infrastructure layer itself. On-chain payments can therefore be evaluated as an extension of existing payment systems, rather than as a parallel stack that requires dedicated operational ownership.

The Open Money Stack is structured across four layers:

-

Applications

A modular payment execution layer that projects can integrate directly into products and services. Standardized interfaces allow higher-level financial functions, including payments, remittances, lending, and neobanking, to be implemented without bespoke design. Developers can assemble service-level financial experiences with minimal additional infrastructure work.

-

Financial Services

A core financial functionality layer accessed through a unified developer API and toolset. Post-payment fund flows such as asset exchange, foreign exchange (FX), treasury management, and yield generation are handled in a standardized manner, removing the need for projects to implement complex financial logic internally.

-

Payment Network

An execution layer responsible for global payment connectivity and regulatory operations. It encompasses on- and off-ramps, stablecoin liquidity, orchestration, and compliance, ensuring reliable fund movement and settlement across multi-currency and multi-jurisdiction environments.

-

Blockchain Rails

The final settlement layer where financial activity is recorded and finalized. Support extends beyond Polygon chains to external networks, enabling flexible stablecoin settlement and cross-chain interoperability without requiring higher layers to manage chain selection or interoperability directly.

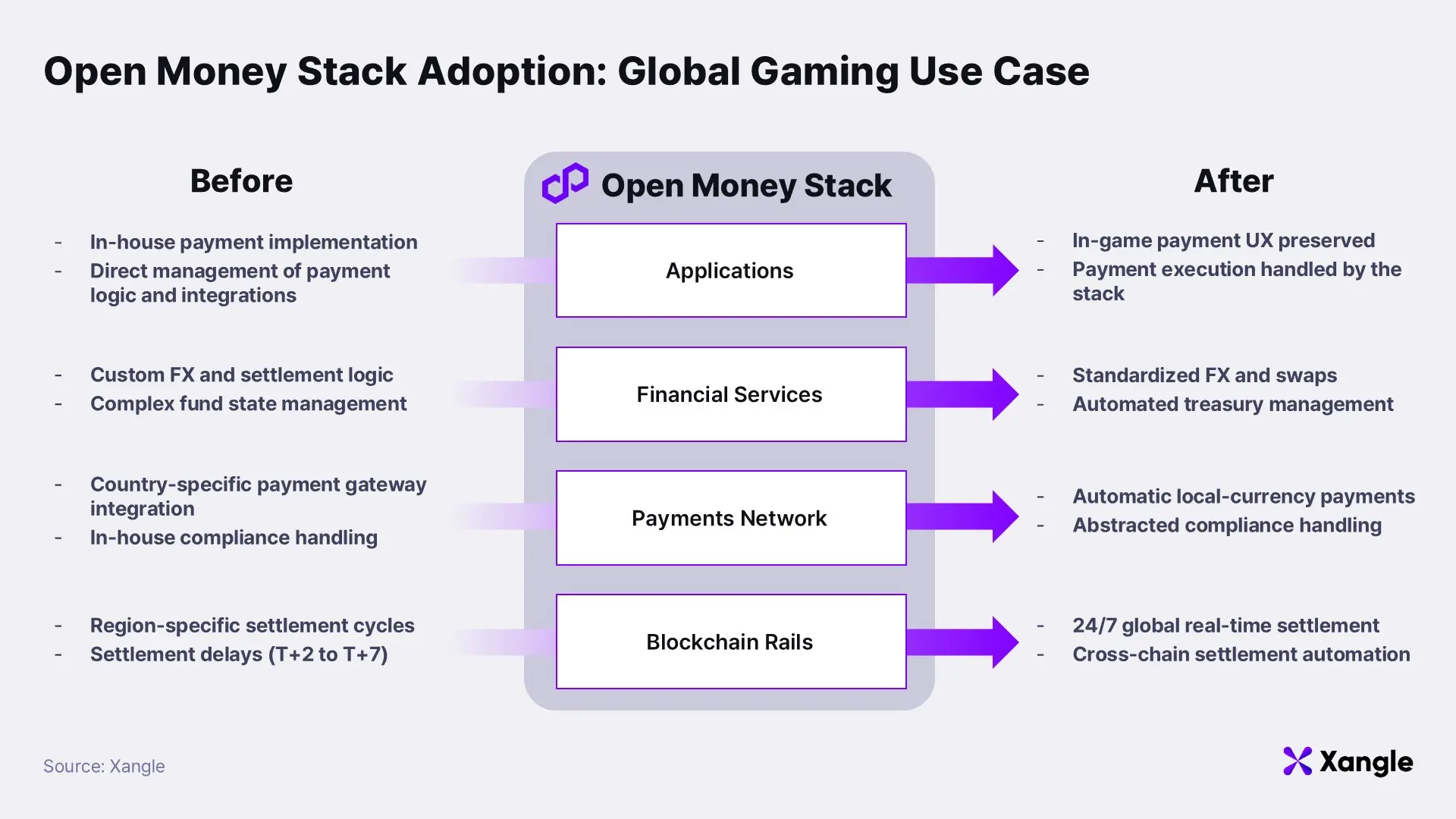

The implications of this structure become clearer when applied to a real-world use case. Consider a global gaming company operating simultaneously across Southeast Asia and South America. Payment flows range from in-game item purchases to creator payouts and regional publisher settlements. Each market introduces its own payment methods, currencies, settlement cycles, and regulatory requirements. Under conventional architectures, local payment gateways must be integrated market by market, while FX and settlement logic are handled separately. Settlement delays of several days and inconsistent regional settlement cycles are common, increasing operational complexity and cost.

Adopting the Open Money Stack alters this operating model. The game maintains its existing in-game payment user experience, while payment execution is handled internally through the stack. Standardized execution via the Applications layer removes the need for the game to design or manage chains, wallets, or payment routes.

Post-payment fund handling is managed within the Financial Services layer. Funds entering in different local currencies are automatically converted using FX or swap functions, and treasury operations are processed in a consistent manner. Exchange timing and fund state management no longer require direct oversight by the game operator.

Jurisdictional differences in payment infrastructure and regulation are absorbed at the Payment Network layer. Local on- and off-ramps and local-currency payments are handled automatically, while regulatory and compliance requirements specific to each country are addressed within the same layer. The need for country-by-country payment gateway integration or bespoke compliance workflows is removed.

Final settlement occurs through the Blockchain Rails layer on a continuous, 24/7 basis. Regional settlement delays and inconsistent settlement cycles are eliminated, and cross-chain transactions settle through a unified process.

The core logic of this model is straightforward. Product teams focus on payment experience and content, while execution, financial processing, and global settlement are handled by standardized infrastructure layers. As a result, global expansion shifts from a payment infrastructure challenge to a problem of content distribution and user acquisition.

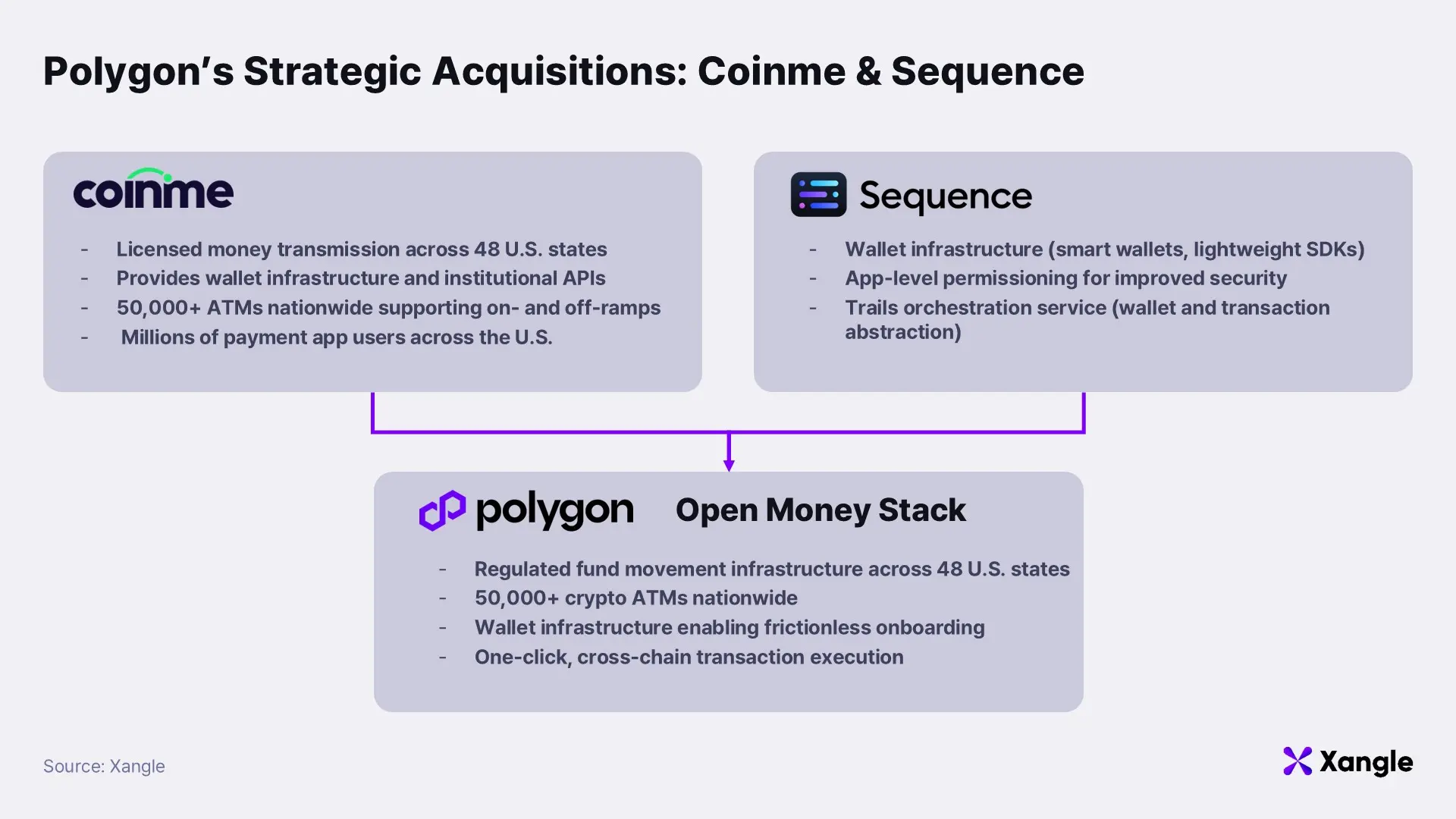

3-3. Internalizing the Payment Stack: Coinme and Sequence

The acquisitions of Coinme and Sequence in January 2026 clarified that the Open Money Stack is not merely a conceptual or aspirational framework. By acquiring Coinme, which covers on- and off-ramps and regulatory execution, and Sequence, which provides wallets, account abstraction, and orchestration, Polygon Labs directly internalized the core components required to deliver payment services within the Open Money Stack.

Coinme anchors the regulated fiat entry and exit layer. Operating under licenses valid across 48 U.S. states, Coinme provides on- and off-ramps and fiat payment services, while supporting cash-to-crypto and crypto-to-cash conversion through a nationwide network of more than 50,000 ATMs. The acquisition gives Polygon a direct, regulated pathway for moving capital on-chain and back off-chain within the United States. Capital inflows and outflows are therefore no longer distributed across external providers, but are managed within Polygon’s own payment stack.

Sequence addresses the wallet and execution layer of the payment flow. Users can create wallets and execute transactions without managing chain selection, gas payments, or bridging steps. Cross-chain payments are coordinated through Trails, an orchestration engine that executes transactions across multiple chains as a single, continuous flow. As a result, payment interactions resemble conventional digital payment experiences rather than explicit blockchain operations.

Together, these acquisitions internalize the two most critical segments of the payment lifecycle: regulated capital onboarding and user execution. With these layers brought under direct control, the Open Money Stack takes shape not as a loose aggregation of features, but as a payment infrastructure that banks, fintech companies, and enterprises can adopt without custom integration at each layer. Polygon’s trajectory is therefore better understood not as that of a platform offering a blockchain, but as a provider of an on-chain payment stack designed to operate within regulated financial environments.

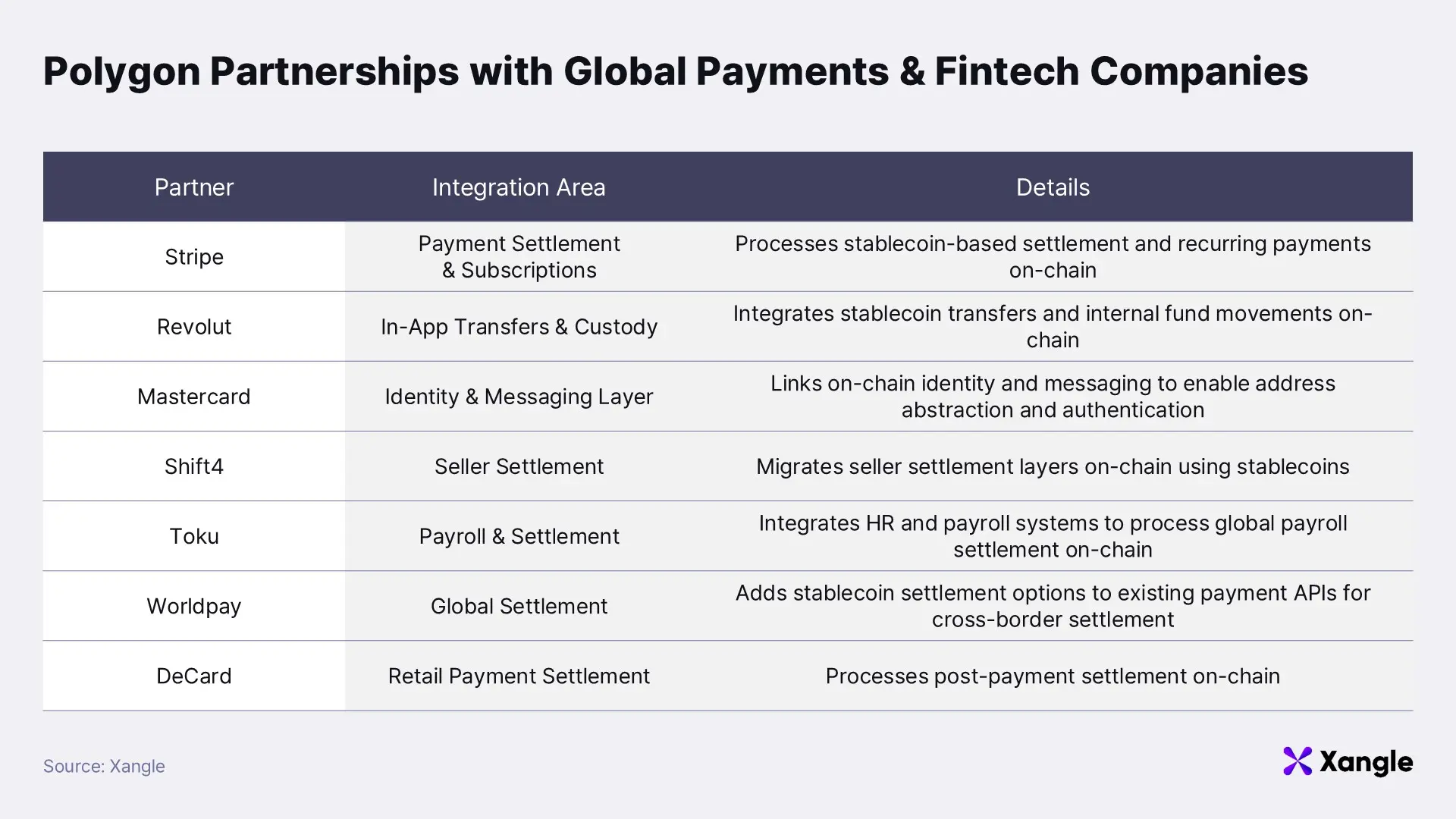

4. Traditional Finance Partnerships: Integration into Payment Infrastructure

The Open Money Stack frames payment activity not as a short-term traffic signal, but as a financial flow that accumulates continuously over time. This perspective shifts the focus from isolated usage metrics to infrastructure design. Against this backdrop, Polygon’s partnerships with traditional financial institutions and payment companies illustrate how the Open Money Stack is being connected to, and executed within, real-world financial workflows.

4-1. Integrating On-Chain Settlement with Global Fintech

Polygon’s collaboration with global payment and fintech firms positions on-chain infrastructure as a settlement backend rather than a user-facing payment layer. The integration model preserves existing frontends and user experiences, while routing post-payment settlement, custody, and fund movement through on-chain systems.

Across these partnerships, existing payment flows remain intact, with stablecoins and on-chain infrastructure introduced at the internal settlement layer. End users continue to transact through familiar card networks, applications, and POS environments. On-chain execution operates beneath these interfaces, improving settlement speed and cost efficiency once payments have been processed.

Within this structure, Polygon functions as infrastructure optimized for continuous settlement. Twenty-four-hour availability, low transaction fees, and fast finality make on-chain settlement particularly effective in contexts where efficiency matters most, including recurring payments, subscription billing, and cross-border settlement. In these areas, on-chain execution complements legacy financial systems rather than displacing them.

The role of on-chain infrastructure in these cases remains deliberately abstracted from the user interface. Payment, transfer, and custody experiences are owned by incumbent payment providers and fintech platforms, while Polygon is integrated underneath as a technical settlement layer. This pattern highlights how the Open Money Stack is expanding by embedding on-chain settlement within existing payment infrastructure, rather than attempting to replace payment companies or consumer-facing workflows.

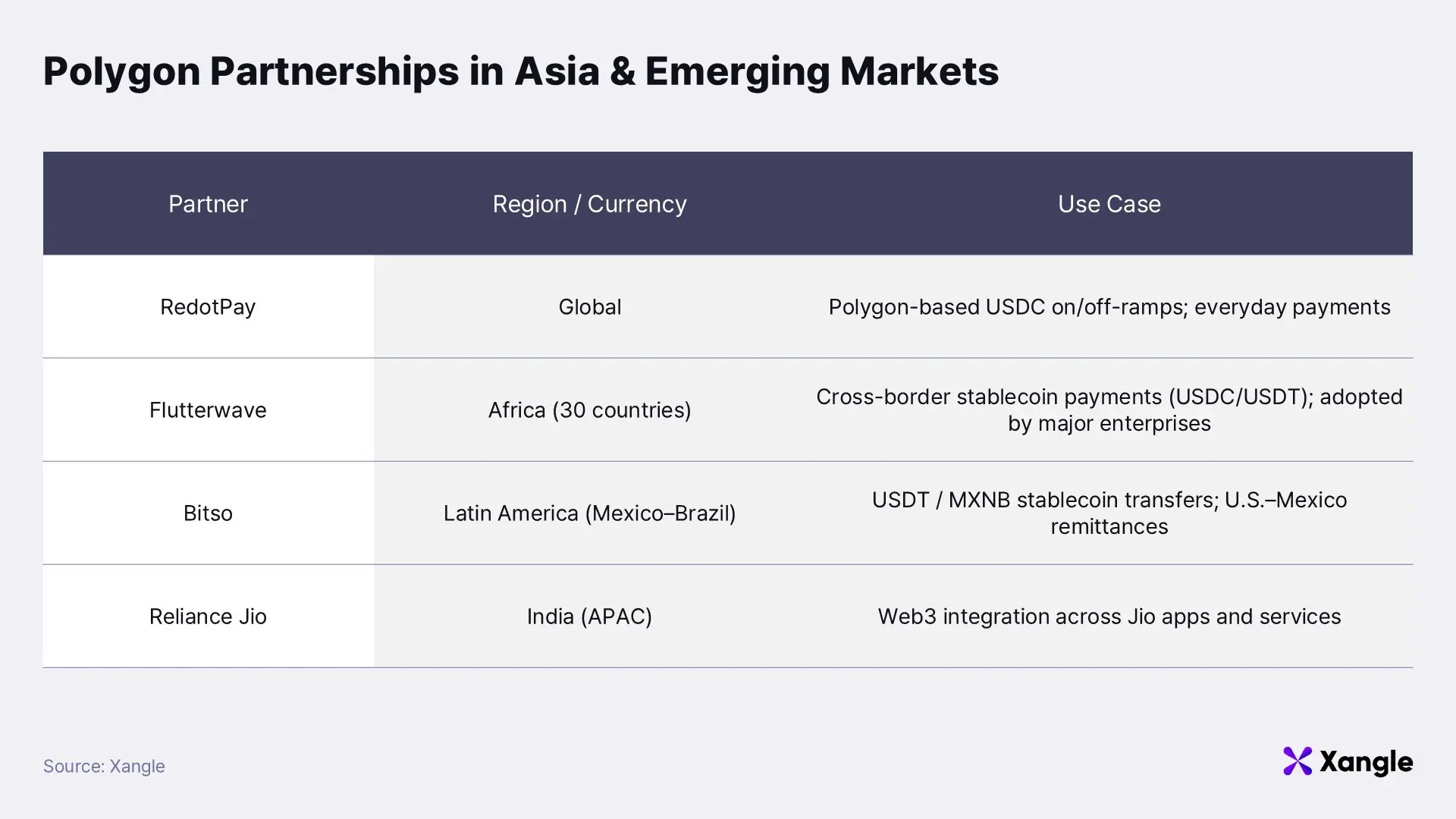

4-2. On-Chain Payments in Asia and Emerging Markets

Asia and emerging markets have emerged as the earliest environments where on-chain payments transition into sustained real-world usage. High cross-border remittance costs, persistent demand for non-USD currencies, and fragmented financial infrastructure coexist in these regions, creating structural conditions where on-chain settlement offers immediate practical advantages. Within this context, Polygon has partnered with payment and remittance providers and is being used as a practical payment rail for low-value, high-frequency transactions.

These partnerships concentrate on transaction flows such as everyday consumer payments, payroll distribution, and cross-border remittances, all of which require reliable handling of small amounts at high frequency. As with Polygon’s integrations in mature markets, existing applications and payment channels remain unchanged. Stablecoins and Polygon’s on-chain infrastructure are introduced at the settlement and fund transfer layer, preserving user-facing workflows while improving backend efficiency.

Cost and settlement speed play a decisive role in regions such as Africa and Latin America. Compared with traditional bank transfers, lower fees and faster settlement make on-chain execution a practical alternative for routine financial activity. In Asia, adoption is progressing through payments and settlement using local-currency-denominated stablecoins, reflecting the region’s diverse currency landscape and cross-border payment needs.

Usage patterns across these regions indicate that on-chain infrastructure is embedded within everyday payment and remittance flows rather than deployed through isolated campaigns or temporary initiatives. In this operating environment, the Open Money Stack functions as infrastructure that processes post-payment fund movement and settlement, supporting continuous financial activity rather than episodic transaction spikes.

5. Conclusion: Polygon as the Base Settlement Rail

Polygon’s strategic focus lies outside crypto-native liquidity and instead targets payment and settlement flows in traditional finance that have yet to transition on-chain. Rising stablecoin payment transaction counts, expanding real-world usage of non-USD stablecoins across Asia and emerging markets, and repeated adoption across RWA and payment use cases collectively indicate that Polygon is increasingly embedded in the pathways through which capital already moves.

The Open Money Stack is designed to prevent this momentum from remaining episodic and instead convert it into durable financial infrastructure. By delivering wallets, on- and off-ramps, financial services, cross-chain settlement, and regulatory compliance as a unified stack, on-chain execution becomes less of a discrete technical experiment and more of a functional extension of existing financial systems. The acquisitions of Coinme and Sequence further underscore this direction, marking a shift beyond partnership-level integration toward direct control over the core segments of payment execution and settlement.

From this perspective, Polygon is better understood not as a standalone blockchain, but as foundational financial infrastructure that enables capital to move faster, at lower cost, and with greater frequency in ways that remain largely invisible to end users. The competitive benchmark Polygon addresses is therefore not other Layer 2 networks, but the structural inefficiencies embedded in legacy financial infrastructure, including limited operating hours, national boundaries, and settlement delays. Viewed toward 2026, Polygon’s direction is more accurately interpreted not as an expansion of chain capacity or a contest for liquidity, but as a process of redefining the core mechanics of finance through on-chain execution.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article was written at the request of Polygon. All content in this article was written independently by the author(s), and neither CrossAngle nor Polygon had any editorial control or influence over the content. The author(s) may hold the cryptocurrencies mentioned in this article at the time of writing.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Solana RWA: A Look at the Key Players](https://resource.xangle.io/files/content/F779A005246C0299246537AACB3A39F2_1782287059970.webp)