Polygon (POL)’s Counterattack Begins

Table of Contents

1. Polygon Pivot from Mass Adoption to Financial Meta

2. Polygon as the Global Stablecoin & Payments Hub

3. Wall Street Meets On-Chain: Polygon’s RWA Play

4. AggLayer + PoS: Infrastructure for On-Chain Finance

5. Closing Statement: Polygon Back in the Spotlight for Retail and Institutions

1. Polygon Pivot from Mass Adoption to Financial Meta

In 2022–2023, Polygon captured investor attention by positioning itself around “mass adoption” and enterprise expansion. The focus was on scaling out into NFTs, the metaverse, gaming, and Web3 applications, while partnerships with global giants like Disney, Meta, and Starbucks helped onboard a wide range of projects, cementing Polygon’s image as the go-to “enterprise blockchain.” Building on its PoS foundation and rolling out solutions such as Supernet and zkEVM, Polygon drove significant user inflows and improved accessibility. For a period, it consistently ranked within the top 10 by market capitalization and was regarded as a leading piece of blockchain infrastructure.

That enterprise-heavy strategy, however, hit its ceiling in the bear market that followed the Terra-Luna collapse. As corporates backed away from Web3 initiatives, Polygon’s momentum also slowed. The team responded by resetting its course. With the 2024 launch of the “Polygon 2.0” roadmap and the token rebrand (MATIC → POL), Polygon declared a decisive pivot toward financial infrastructure. The previous Supernet-first approach began to fade, while AggLayer, designed to aggregate cross-chain liquidity and act as a payments hub, stepped into the spotlight. Supernet had been tailored for corporates building appchains; AggLayer, in contrast, represents a next-generation scaling strategy that links multiple chains into a unified liquidity and settlement layer, laying the groundwork for RWAs, payments, and real-time financial transactions.

Over the past two years, Polygon’s core narrative has shifted from corporate partnerships and mass adoption toward on-chain finance and asset tokenization. Since the rebrand, that pivot has produced concrete results: Apollo, BlackRock, Franklin Templeton, and other global financial institutions are already deploying directly on Polygon. This narrative shift aligns with rising expectations around regulatory easing for stablecoins and on-chain finance, and is crystallizing in Polygon’s traction in stablecoins, payment networks, and RWA expansion; pushing the chain back into the market spotlight.

2. Polygon as the Global Stablecoin & Payments Hub

Since the rebrand, Polygon has emerged as a frontrunner in stablecoin payments and micropayments. Its low-fee, high-speed infrastructure is seeing strong traction across APAC and LATAM emerging markets. Combined with a regulatory-friendly stance and an expanding web of global partnerships, Polygon is embedding itself as a cornerstone of payment infrastructure.

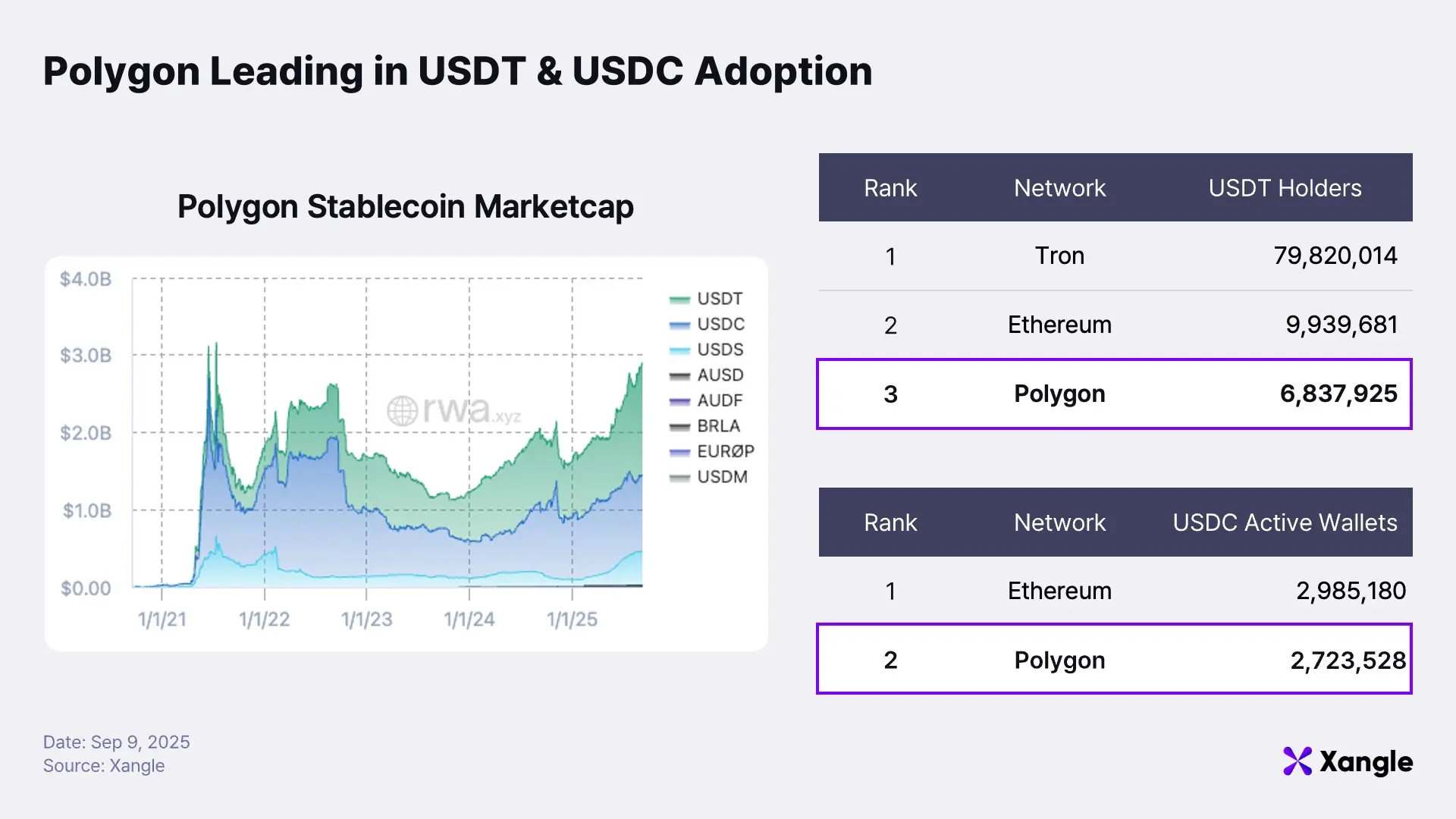

In the stablecoin sector, Polygon leads the industry with the highest number of active USDC wallets and ranks third for USDT, securing a global top-tier position in the USD-pegged stablecoin market. Beyond the dollar, it supports a wide spectrum of non-USD stablecoins—including JPYC (Japanese yen), XSGD (Singapore dollar), BRZ (Brazilian real), EUROP (euro), and MXNe (Mexican peso)—meeting diverse regional payment needs. The launch of JPYC, Japan’s first licensed yen stablecoin, on Polygon highlights its competitive advantage across both the dollar and non-dollar landscapes. More recently, the addition of AUSD (Agora), an institutional-grade stablecoin managed by VanEck and State Street, as a native AggLayer asset has further solidified Polygon’s status as a leading stablecoin hub.

Expanding stablecoin circulation is directly translating into stronger payment metrics.According to AInvest, as of June 2025, Polygon’s monthly micropayment volume surpassed $100 million, capturing over 50% market share. Its share of small-scale payments also reached 42%, rapidly breaking into the everyday payments space where blockchains have historically struggled. In Q2, total payment transaction volume topped $4.3 billion, while the number of active P2P addresses increased by more than 11 million in the first half of the year; proof that Polygon’s payment rails are seeing real-world adoption.

Most importantly, Polygon’s payment partnerships are deepening. Global Web3 payment players like Stripe, AEON, Grab, YellowCard, RedotPay, and Nexo have all integrated with the network, making its ecosystem more resilient. With 97% of all transactions executed via non-custodial wallets, Polygon’s user base is expanding organically, not just propped up by platform partnerships. This signals Polygon’s transition from a blockchain platform into a true global payments network, while also amplifying network effects as it branches further into RWAs and institutional collaboration.

3. Wall Street Meets On-Chain: Polygon’s RWA Play

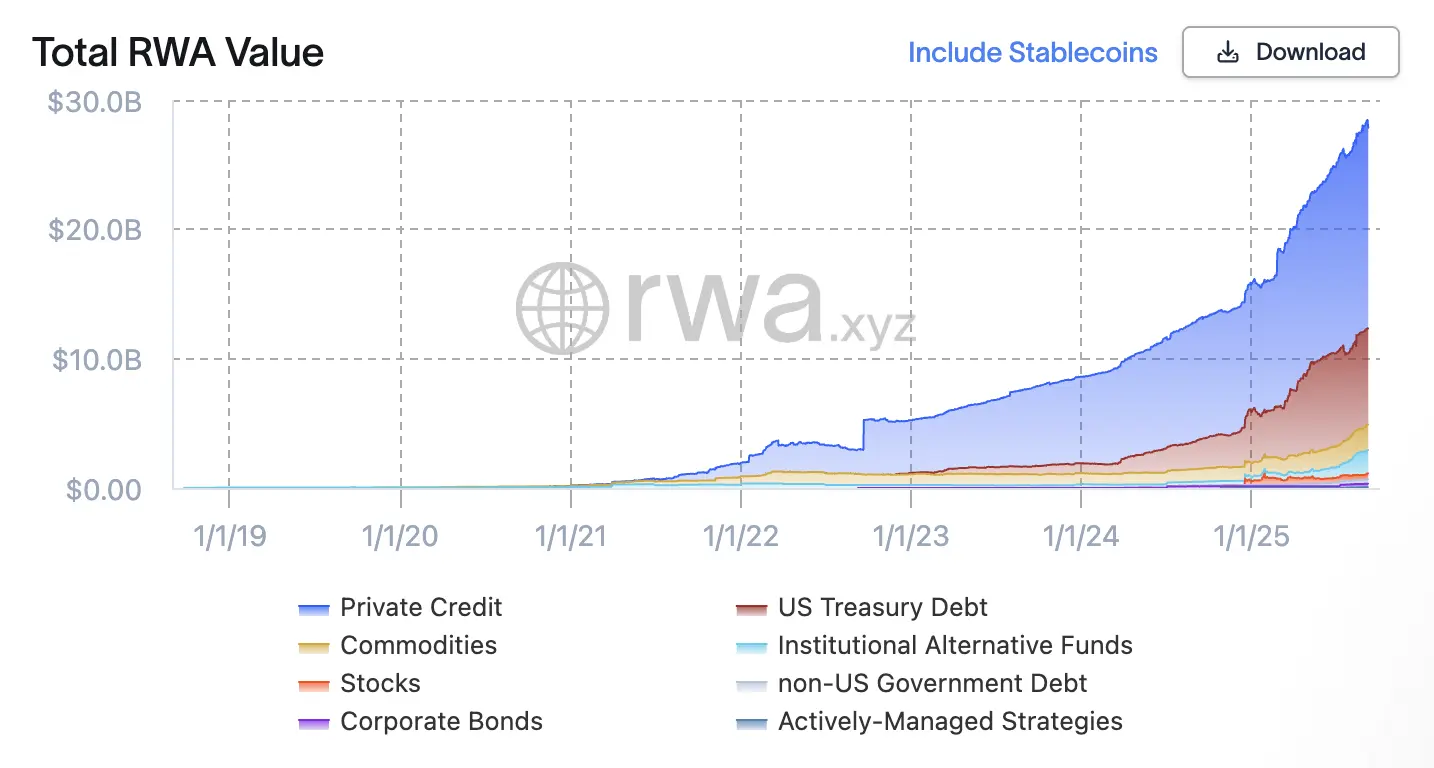

With stablecoin rails now entrenched as the backbone of global payments and settlement, market attention has shifted to the next frontier: Real World Assets (RWAs). Following Trump’s election victory and renewed expectations for regulatory easing, the on-chain RWA market has surged toward the $30 billion mark. Both major institutions and leading protocols increasingly see RWAs as the next growth driver.

RWA market growth nearing $30B post-Trump election

Polygon’s approach to RWAs extends well beyond the basic idea of putting tokenized receipts of assets on-chain. Its ambition is to build infrastructure where assets can circulate and settle natively, directly connecting them to on-chain financial rails, payments, lending, collateralization, and secondary markets, so they function as productive assets. In this role, Polygon has emerged as one of the blockchains traditional finance institutions actually trust and use, steadily building a track record not just of showcasing RWAs but of making them operational at scale.

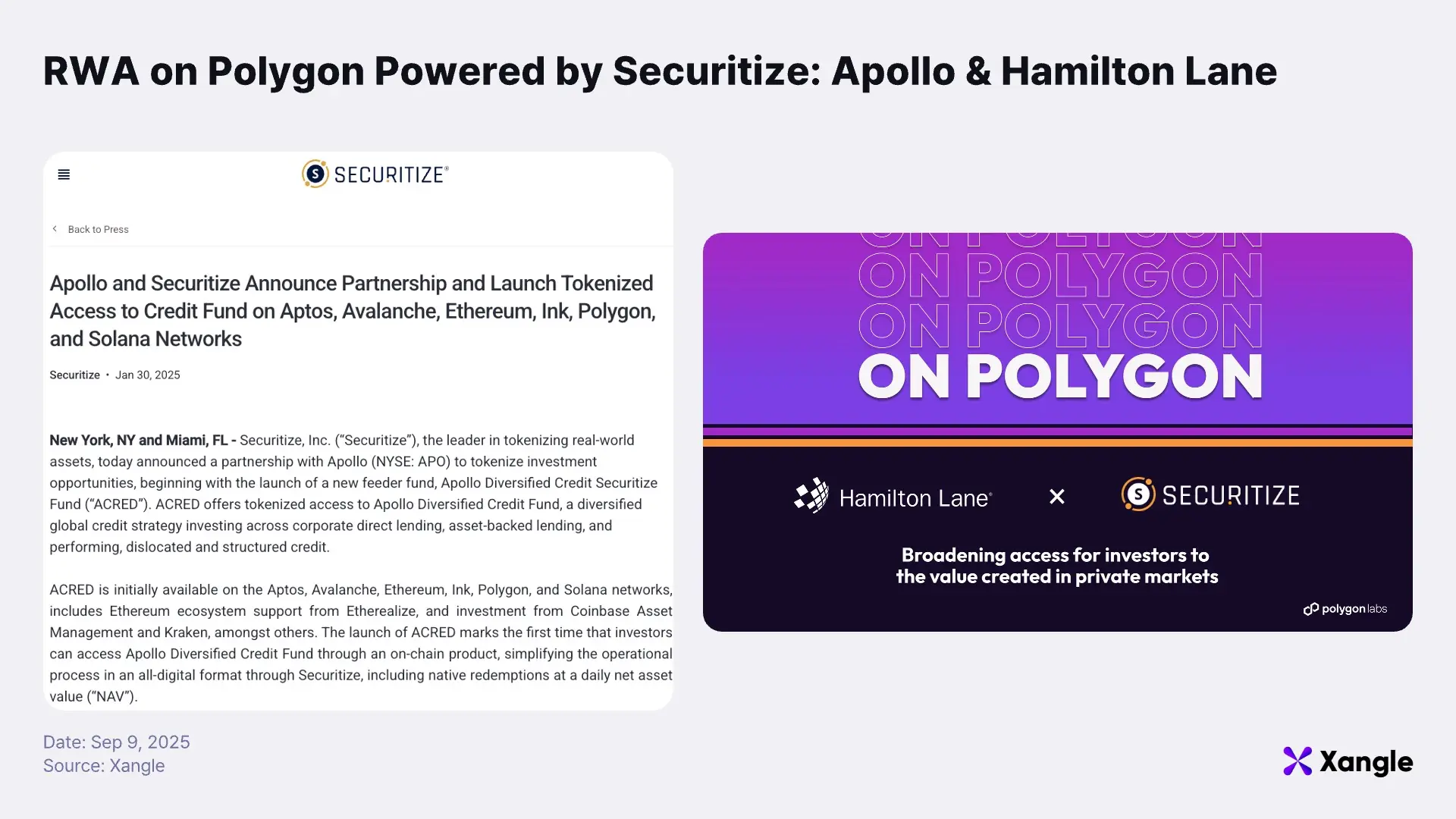

A series of initiatives through Securitize stand out. Apollo, working with Securitize, tokenized its Diversified Credit Fund (ACRED) in a multi-chain setup including Polygon—bringing institutional-grade private credit strategies on-chain. Hamilton Lane likewise used Securitize to tokenize shares of its Equity Opportunities Fund V on Polygon, expanding access for individual investors. By supporting Polygon, Securitize has effectively created the infrastructure for global asset managers to issue and operate RWA products in production.

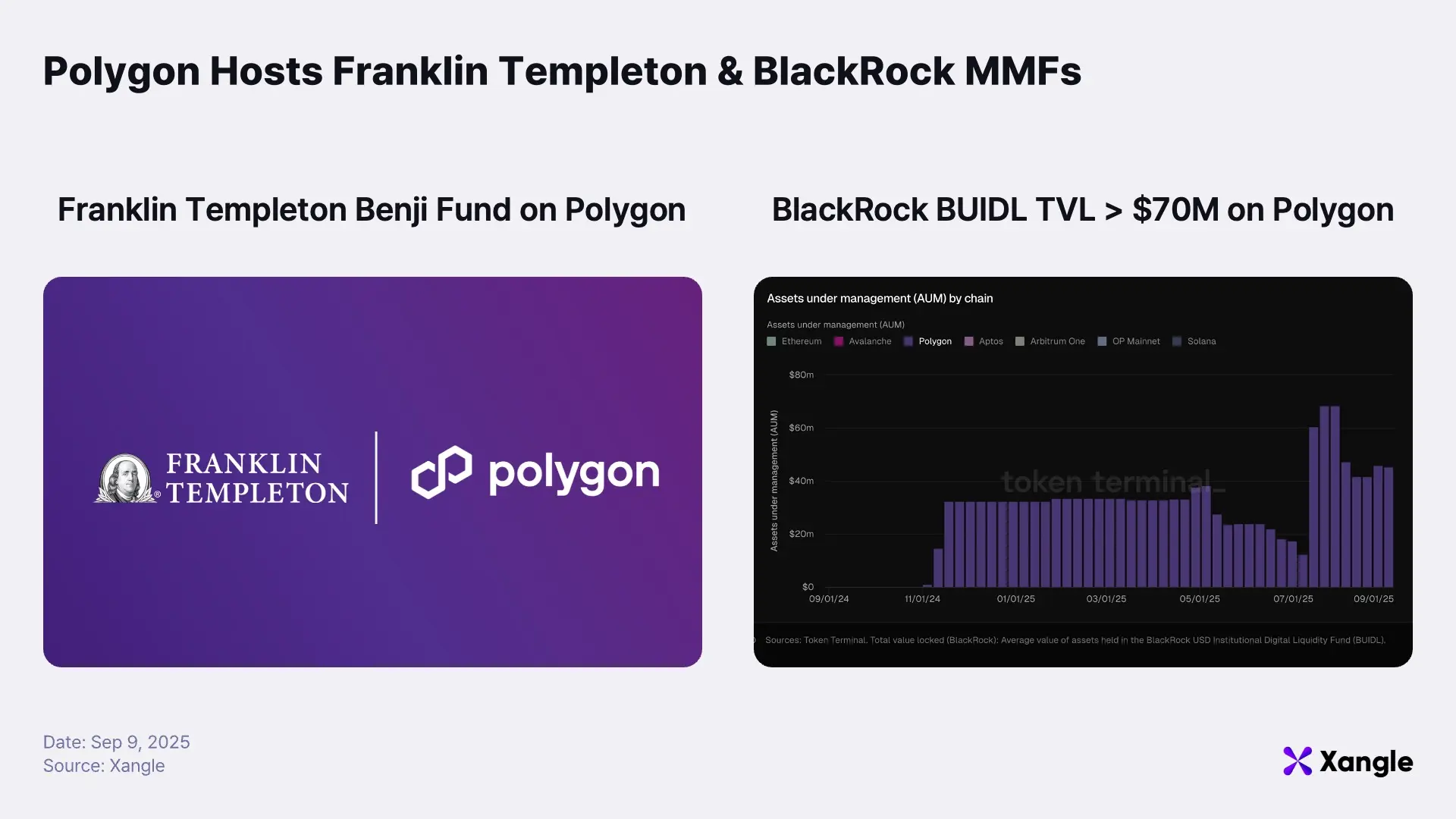

This momentum is now spilling over into money market funds. Franklin Templeton migrated its FOBXX, the world’s first SEC-registered public money market fund, onto Polygon to record transactions and ownership. BlackRock expanded its USD Institutional Digital Liquidity Fund (BUIDL) onto Polygon, widening access to tokenized money market funds. In Europe, Assetera launched a regulated secondary RWA marketplace on Polygon PoS, moving parts of the European asset distribution pipeline fully on-chain.

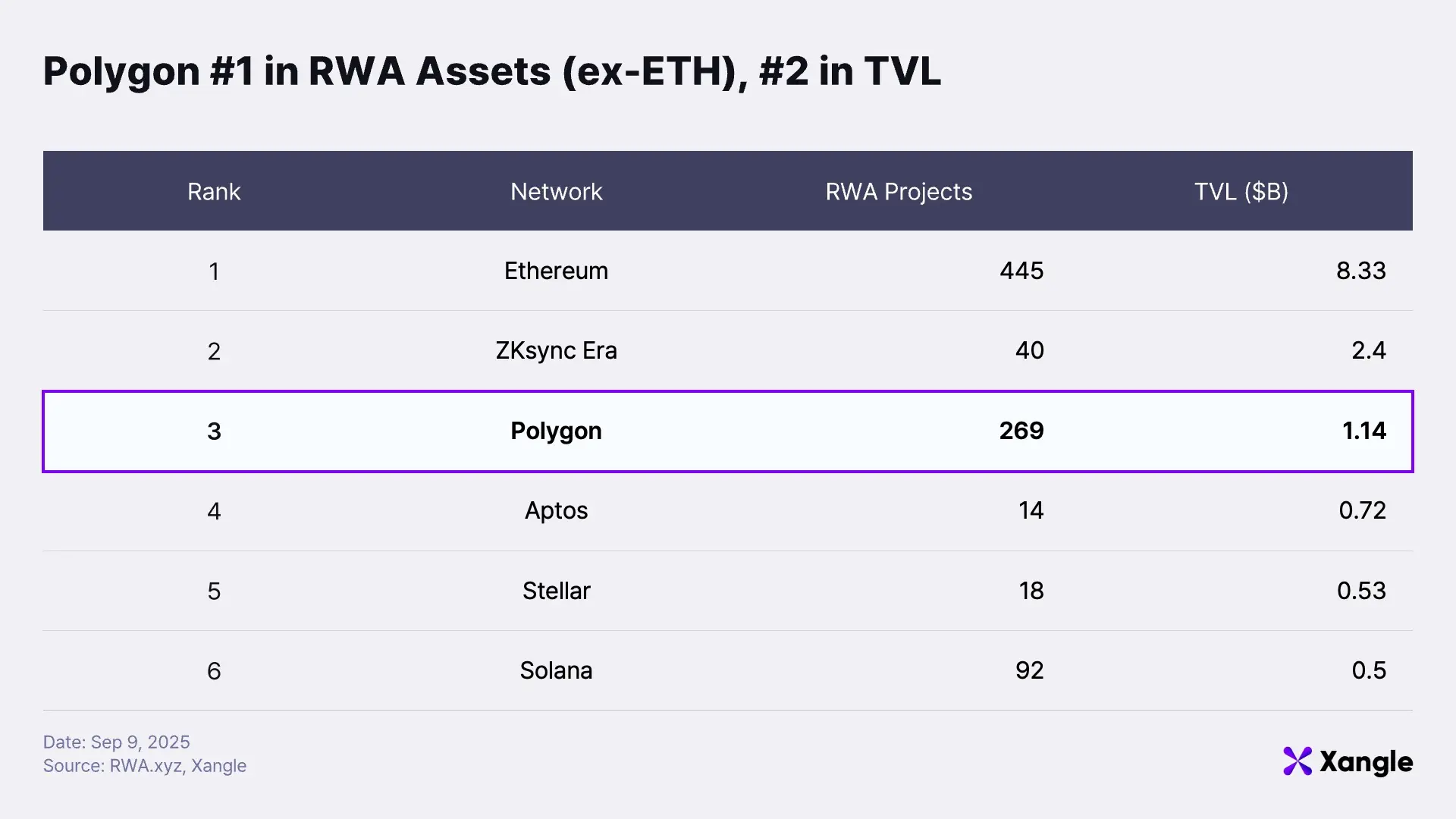

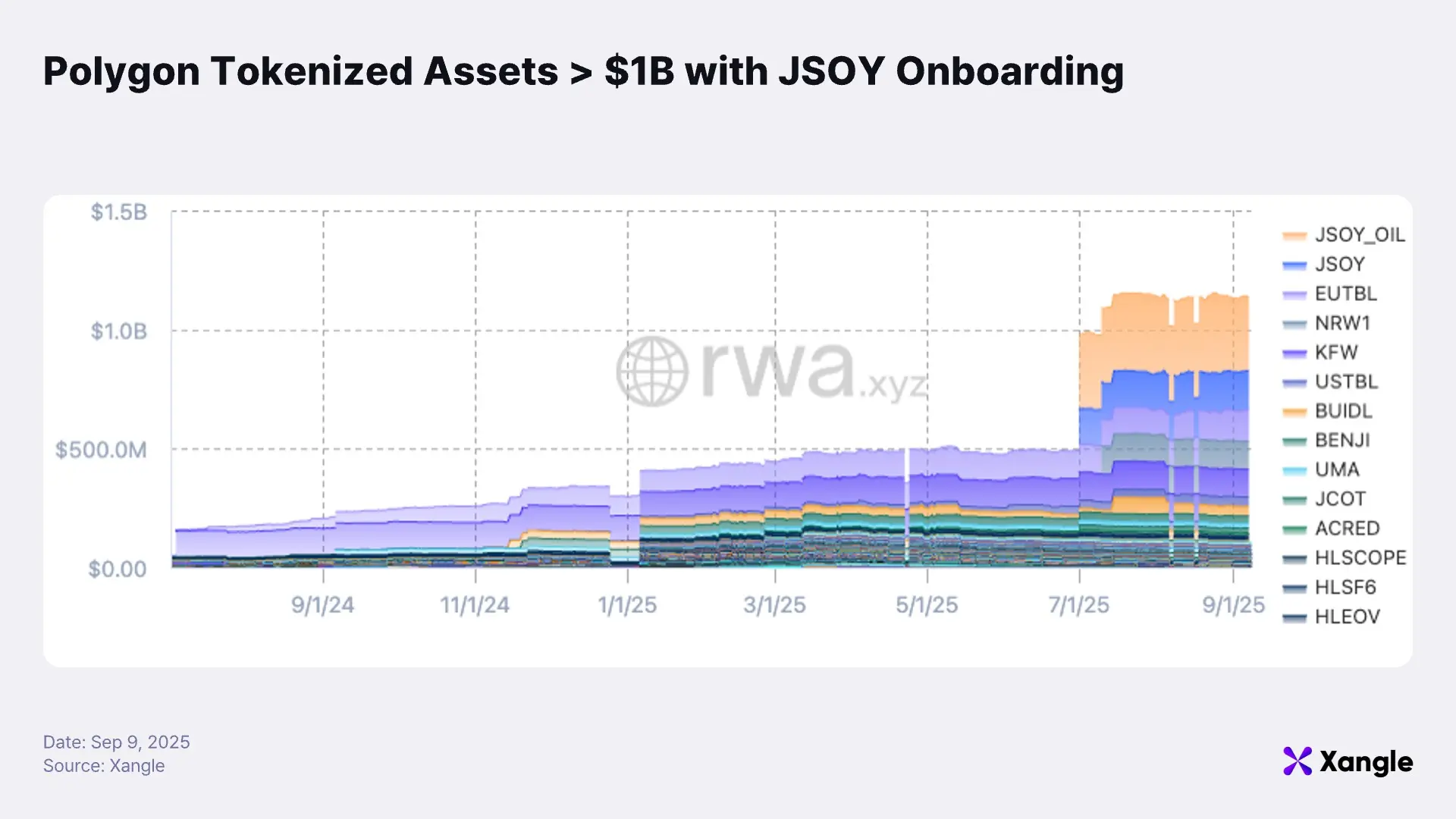

On the back of these wins, Polygon has climbed to No.2 in number of RWA assets and No.3 in TVL globally, according to RWA.xyz—further consolidating its position as an RWA hub. Since July, Polygon has also onboarded commodity-based RWAs such as JSOY (each token representing 1 metric ton of soybeans) and JSOY_OIL (each token representing 1 metric ton of soybean oil). Surging issuance of JSOY in particular has accelerated Polygon’s momentum in the RWA sector.

Polygon’s RWA traction isn’t just about being supported by platforms; integration with its own infrastructure, AggLayer, is also gathering pace. Lumia has connected a Polygon CDK–based RWA chain to AggLayer to tokenize a $220 million real estate project. Other initiatives include FraXion (fractionalized real estate and capital raising), Outsyde (land rights and carbon/biodiversity credits), and Courtyard (custody of physical collectibles like Pokémon cards). AggLayer’s interoperability and liquidity aggregation are proving critical in enabling secondary markets and derivative structures for these assets.

Still, Polygon’s RWA footprint remains smaller than its dominance in stablecoins and payments. Institutional pilots are translating into meaningful results, but the sector needs to move beyond one-off events toward sustained growth in transaction volumes and use cases. To achieve true differentiation, Polygon must convert its headline partnerships, such as Apollo, BlackRock, Franklin Templeton, and beyond, into enduring flows and network effects that prove RWAs are not just a “testnet narrative” but a production-grade financial rail.

4. AggLayer + PoS: Infrastructure for On-Chain Finance

Polygon PoS continues to evolve into a faster and cheaper chain purpose-built for financial infrastructure. With the recent Bhilai upgrade, the network now supports ~1,000 TPS, stabilized gas fees, and account abstraction (EIP-7702). The Heimdall v2 upgrade cut finality down to around 5 seconds. By the end of 2025, Polygon targets 5,000+ TPS with full AggLayer connectivity, and over the long run, its “Gigagas” roadmap aims for 100K TPS—positioning Polygon as on-chain financial infrastructure capable of real-time settlement.

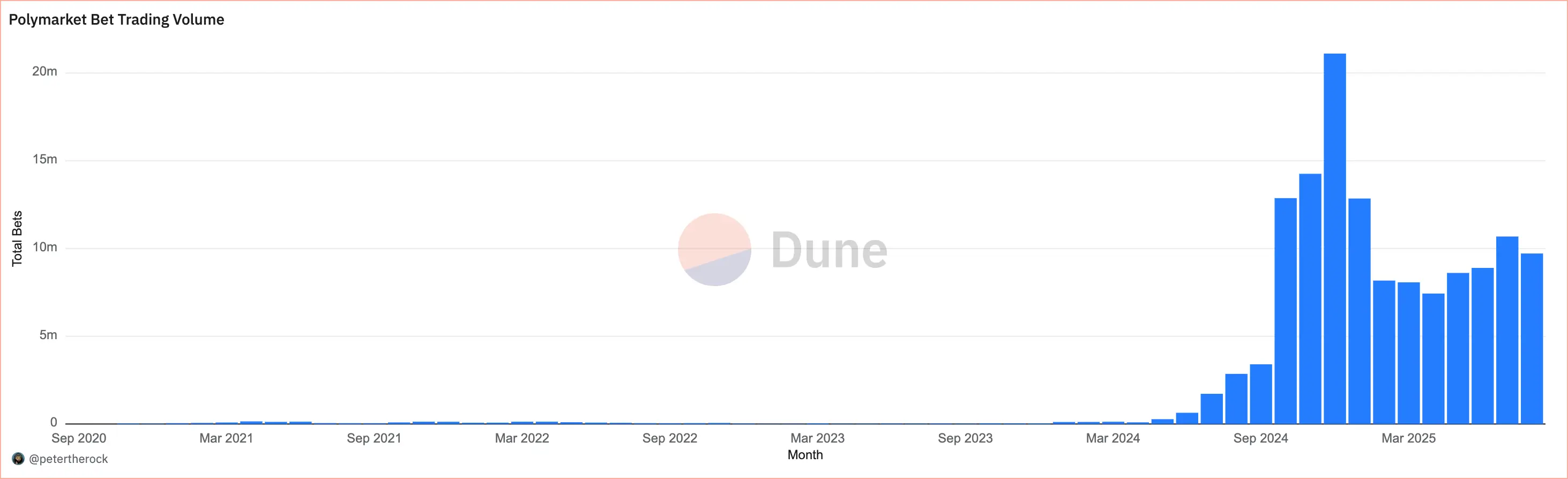

Cumulative betting volume of Polymarket surpasses $17B

On top of these performance upgrades, Polymarket on Polygon PoS has crossed $14B in cumulative trading volumeand was adopted as X’s (Twitter’s) official prediction market partner. Courtyard, meanwhile, has tokenized high-value physical collectibles stored in Brinks vaults, unlocking global liquidity and briefly pushing Polygon’s NFT trading volume above Ethereum’s. Public-sector traction is also building: the U.S. Department of Commerce and the Philippine Department of Finance have recorded data on-chain with Polygon, and the Philippine Senate has even proposed moving the entire national budget onto Polygon.

Two standout dApps in the ecosystem are Moonveil and WiFi Map. Moonveil is building a gamer-focused rewards system and multi-game economy on a Polygon CDK–based L2, onboarding titles such as AstrArk and Bushwhack as it grows into a gaming hub. WiFi Map connects global WiFi hotspots and rewards contributors with $WIFI tokens. As of September 10, it reported 1.59M UAW, making it one of the top DApps in the Polygon ecosystem.

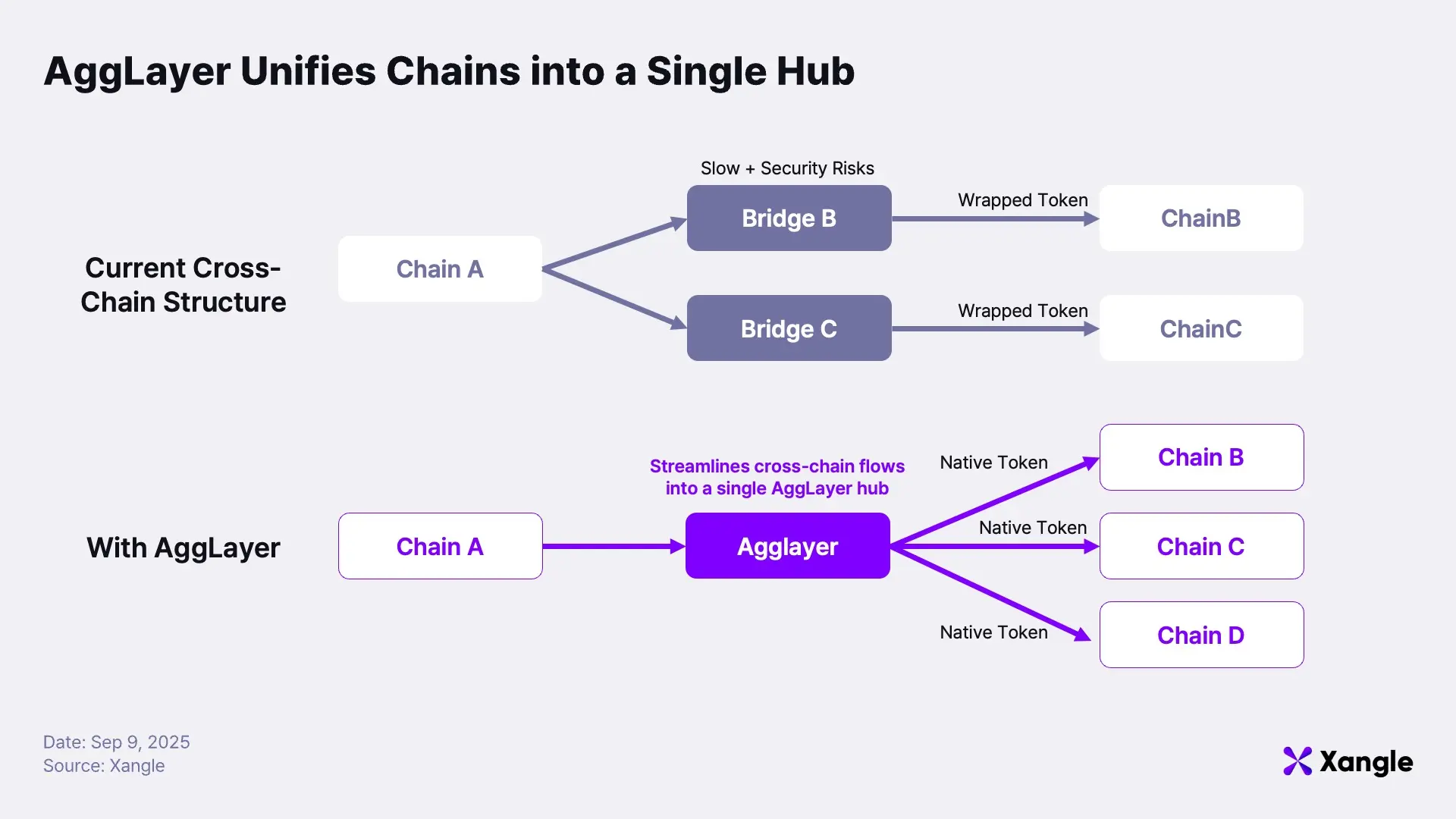

AggLayer represents another cornerstone. Its goal is to unify fragmented blockchains into one seamless experience, akin to how the internet itself operates. Historically, moving value between chains required creating wrapped tokens, introducing latency and security risks. AggLayer removes that friction by enabling tokens to move natively across chains with single-step, secure finality. For users, this means sending and paying without worrying about which chain they’re on. For developers, it means direct access to a unified liquidity pool without the burden of managing multiple chains individually.

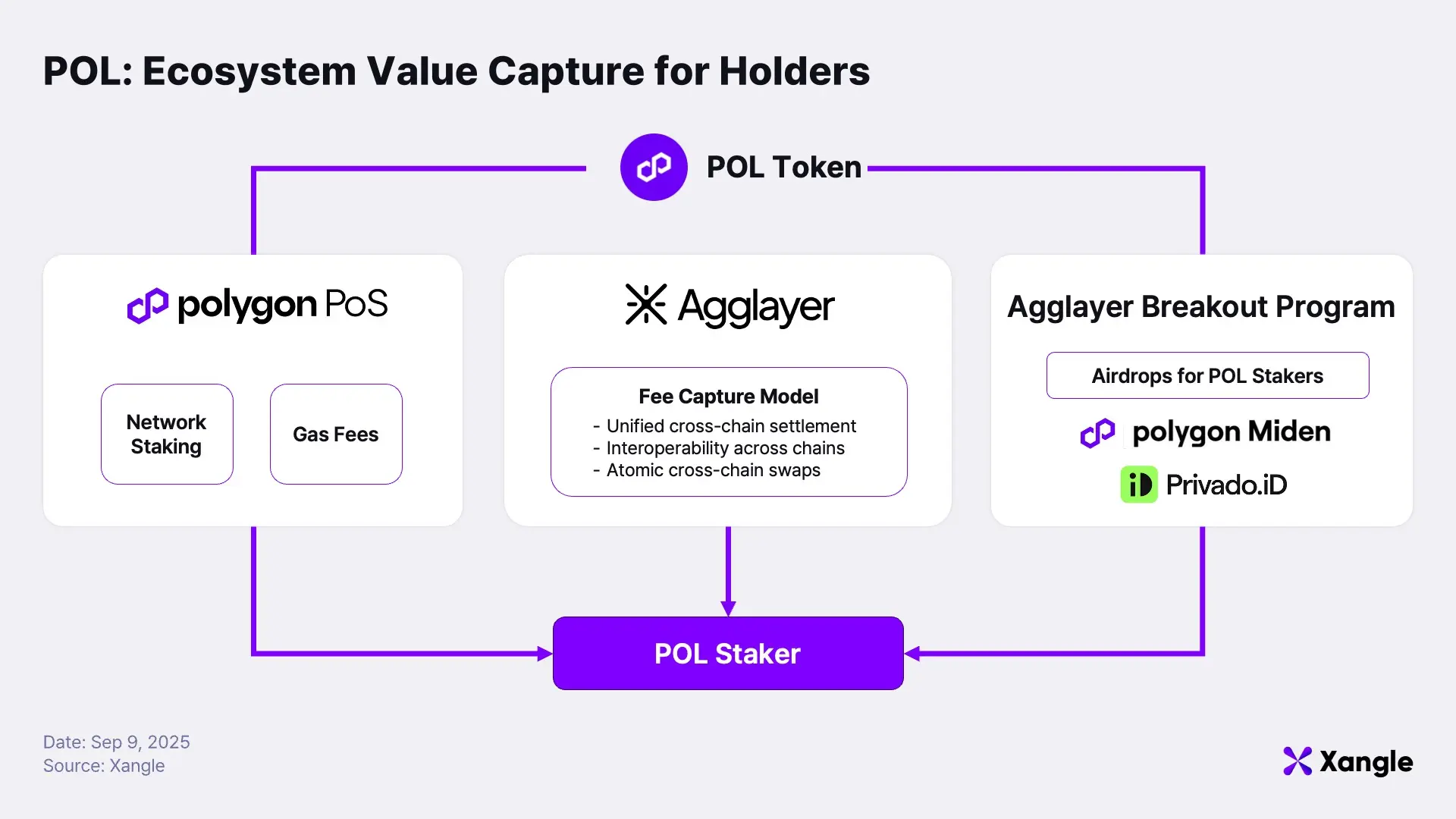

Polygon has recently expanded AggLayer into a multi-stack CDK, opening access to builders from beyond its native ecosystem. AggLayer has also introduced a “common stablecoin” framework, enabling the same settlement asset to be used across all connected chains. Regardless of the underlying chain, users can transact with the same currency in the same wallet, simplifying UX for both end-users and developers. Protocols such as Moonveil, Union, Lumia, and Magic are already connected, while USDC and AUSD have been introduced as native assets, rapidly scaling real-world utility.

These technical and ecosystem advances feed directly into the value loop of the POL token. POL serves as both the “fuel and membership card” of the Polygon ecosystem: staking POL secures the network, powers core functions such as AggLayer, and grants rights to participate in new chain token airdrops. For example, Miden and Privado ID, both part of the AggLayer Breakout Program, plan to allocate 5–15% of total token supply to POL stakers. This design ensures that AggLayer-driven chain expansion translates into increased POL utility. In effect, Polygon ties PoS performance, AggLayer interoperability, and CDK multi-stack tooling directly to POL staking demand, creating a virtuous cycle where ecosystem growth and token value compound together.

5. Closing Statement: Polygon Back in the Spotlight for Retail and Institutions

Polygon is regaining prominence as three pillars—narrative (financial meta), business (stablecoins, payments, RWAs), and infrastructure (PoS, AggLayer)—interlock to reposition it as a top-tier chain for retail users. In stablecoins and payments, Polygon has secured clear market share with global partnerships, support for non-USD currencies beyond the dollar, and a fee model optimized for micropayments. Its broader vision, uniting fragmented ecosystems under AggLayer, is steadily materializing. For retail, this delivers real utility as a low-cost, high-finality payment chain; for institutions, Polygon is increasingly recognized as a regulation-friendly platform capable of issuing and settling RWAs.

Yet RWAs remain an area with work to be done. Despite marquee partnerships with Apollo, BlackRock, and Franklin Templeton, the actual scale of tokenized assets on-chain still lags behind Polygon’s traction in payments and stablecoins. Institutional pilots have been successful, but large-scale settlement, secondary trading, and collateral integration remain limited. Closing this gap will be critical if Polygon is to elevate RWAs from a “testnet narrative” into production-grade financial infrastructure.

Looking ahead, three questions will define Polygon’s trajectory. First, can it sustain leadership in dollar-linked stablecoins while driving fresh traffic through the rollout of localized stablecoins? Second, how quickly will RWAs standardize across the full lifecycle, such as issuance, settlement, collateralization, and secondary markets, and convert into real, scalable flows? Third, how effectively will AggLayer’s inflow of diverse ecosystems and assets, combined with the POL value feedback loop via the Breakout Program, reinforce token demand and network effects? If these three drivers unfold as planned, Polygon is positioned to reemerge as a global on-chain financial infrastructure spanning both payments and RWAs, which is a compelling proposition for retail users and institutions alike.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article was written at the request of Polygon. All content in this article was written independently by the author(s), and neither CrossAngle nor Polygon had any editorial control or influence over the content. The author(s) may hold the cryptocurrencies mentioned in this article at the time of writing.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.