BTCFi: From Retail to Institutions, from Institutions to Starknet

Table of Contents

1. The Institutionalization of Bitcoin Ownership

2. Custody as the Institutional On-Ramp to BTCFi

3. Why Institutions Converge on Starknet

4. BTCFi Season: Incentives as Economic Design

5. Conclusion: The Growth Potential of Starknet with BTCFi

1. The Institutionalization of Bitcoin Ownership

Bitcoin’s market capitalization exceeds the combined market capitalization of all cryptocurrencies excluding Bitcoin. Despite its scale, however, the majority of Bitcoin remains confined to basic functions such as holding and transferring; only 0.37% of total supply is currently deployed in DeFi. As the gap between latent potential and realized usage has become increasingly apparent, many projects have focused on persuading long-term holders and large-scale holders, commonly referred to as Bitcoin maximalists, to bring capital on-chain. This cohort views Bitcoin as the only asset that fully embodies censorship resistance and scarcity, anchoring its core value in store of value and self-custody.

From this perspective, Bitcoin is fundamentally an asset to be directly held and transferred when necessary. Actively deploying it to generate yield is often regarded as a deviation from Bitcoin’s philosophical foundations. As a result, smart-contract-based activity is structurally distrusted, and participation in DeFi, lending, or staking is avoided in principle. On-chain behavior has therefore remained overwhelmingly concentrated in holding and transfers, reinforcing the widespread assessment that onboarding Bitcoin maximalists into DeFi is, in practice, extremely difficult.

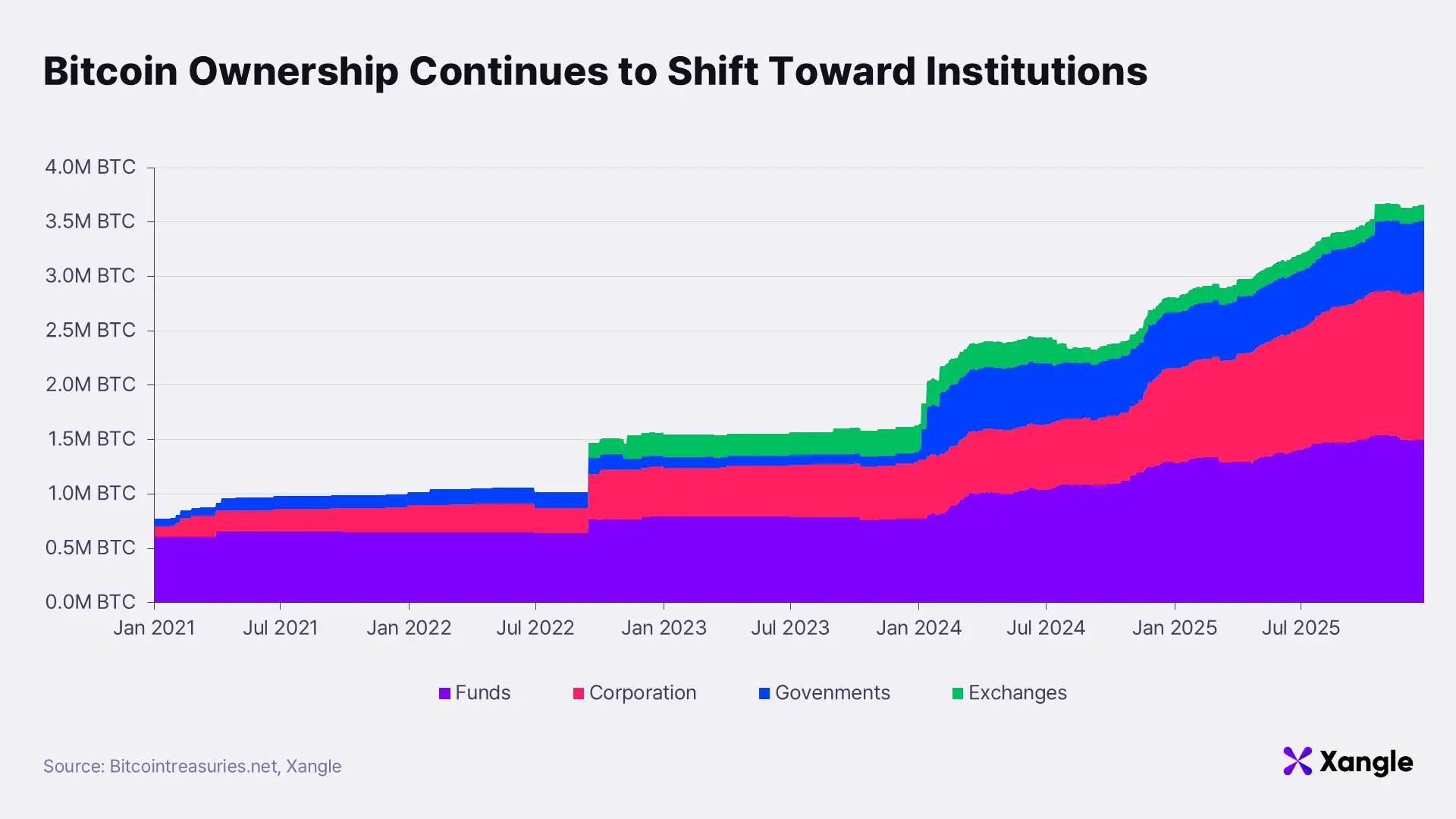

A closer examination of Bitcoin’s ownership distribution points to a materially different trajectory for BTCFi growth. According to Bitcointreasuries.net, institutional Bitcoin holdings across corporations, funds, exchanges, and governments increased from approximately 0.8M BTC just prior to the first Bitcoin ETF approval in January 2021 to roughly 3.66M BTC within five years. This corresponds to 18.3% of the total circulating supply of around 19.96M BTC, and the upward trend remains steep.

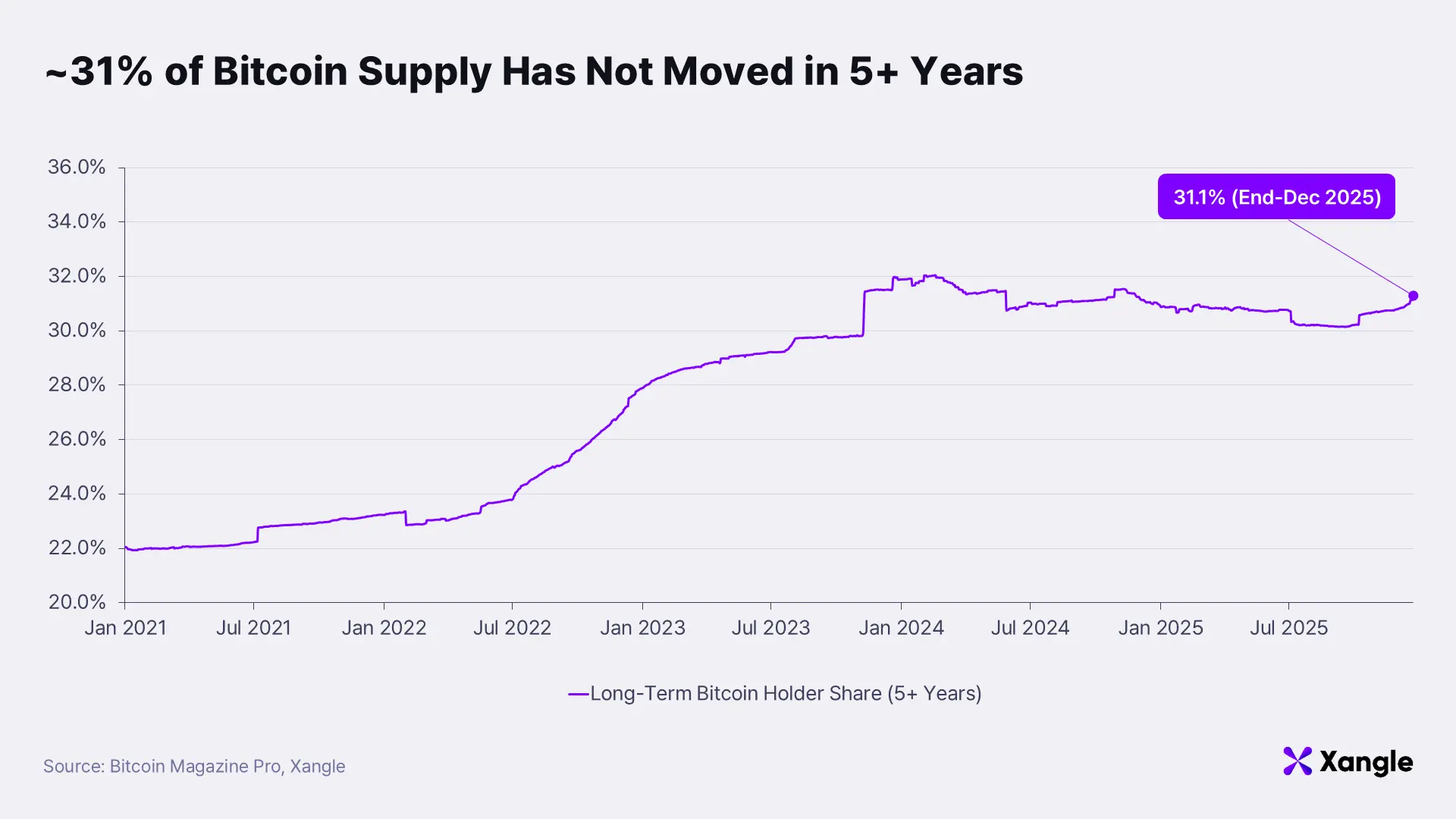

Bitcoin held by long-term individual holders, effectively representing Bitcoin maximalists and defined as BTC that has not moved for more than five years, is estimated at approximately 31% based on data from Bitcoin Magazine Pro. Even if Bitcoin DeFi were to become active, this supply would be the last to re-enter circulation and should therefore be excluded from any realistic assessment of market liquidity. On this basis, the effective liquid Bitcoin supply stands at roughly 69%; institutional holdings of 18.3% translate to approximately 26.5% when recalculated on a liquid-supply basis.

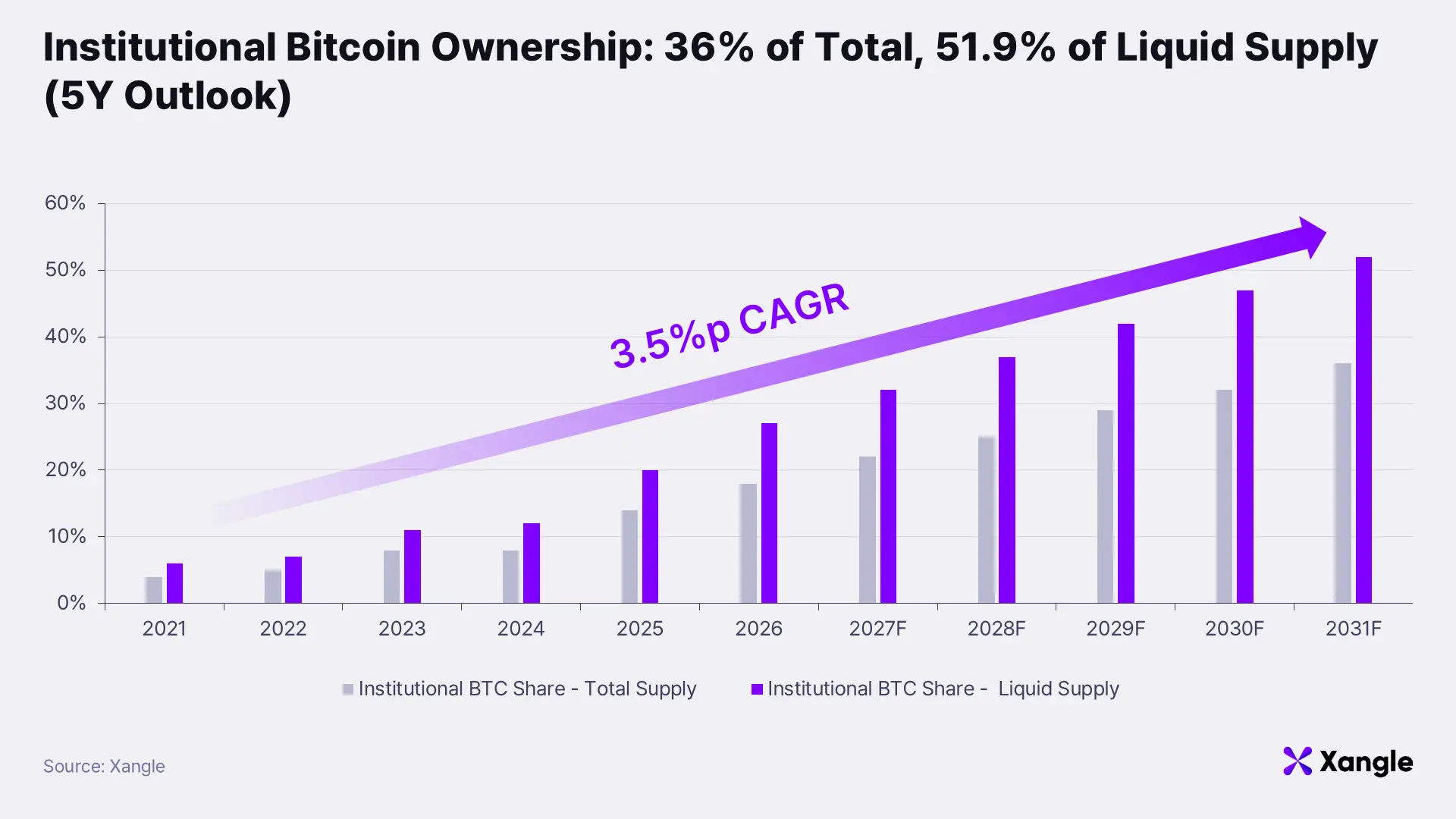

Viewed from this angle, institutions already control more than one quarter of Bitcoin that is realistically available for circulation. Over the past five years, institutional ownership has expanded by roughly 17.5 percentage points, equivalent to an average increase of 3.5 percentage points per year. If this pace continues, institutional holdings could reach approximately 25% of total supply within the next two to three years, exceeding 35% on a liquid-supply basis. Extending the same trajectory further, institutional ownership could rise to around 36% of total supply within five years, surpassing 51.9% of liquid supply. Such dynamics indicate that the early expansion phase of BTCFi is structurally more likely to be driven by institutional capital rather than individual participation.

https://x.com/EricBalchunas/status/1991257411483537813?s=20

https://x.com/EricBalchunas/status/1991257411483537813?s=20

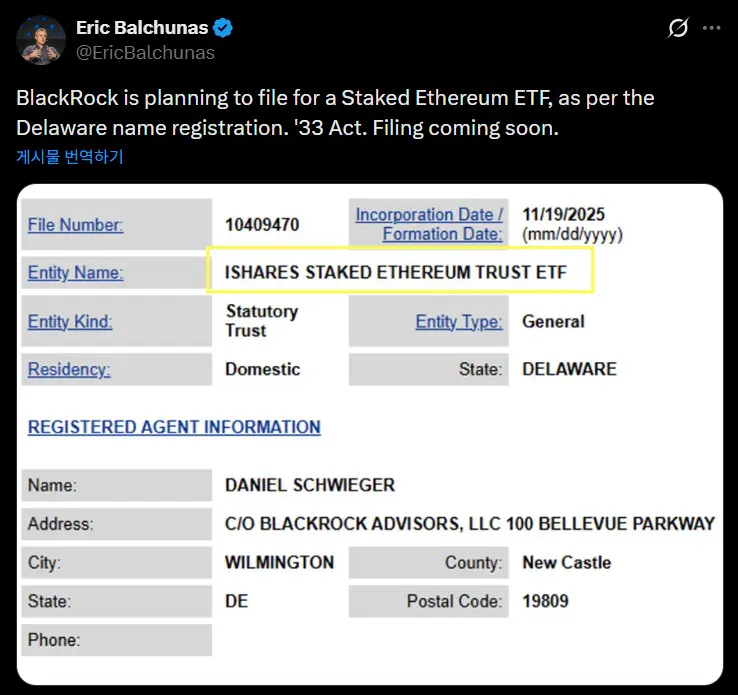

These shifts in ownership structure are unfolding alongside changes in the traditional financial regulatory landscape. BlackRock’s submission of Ethereum staking ETF registration filings to the SEC, followed by the SEC’s determination that Ethereum and liquid staking do not constitute securities, signals that DeFi primitives such as staking are gradually being absorbed into established regulatory frameworks. From an institutional perspective, regulatory uncertainty around DeFi is easing incrementally; over the longer term, this also opens the possibility that institutional discussions around yield-bearing digital assets may extend beyond Ethereum to Bitcoin-based architectures.

Even so, large-scale institutional participation in BTCFi remains constrained. Regulatory clarity is still incomplete, while concerns around asset safety and operational and security risks have yet to be fully resolved. In effect, although institutions already hold Bitcoin at scale, the conditions required to deploy it actively on-chain have not yet fully matured.

2. Custody as the Institutional On-Ramp to BTCFi

As outlined earlier, Bitcoin’s ownership structure is already shifting rapidly from an individual-driven market to an institution-driven one. Despite holding substantial amounts of Bitcoin, institutions have yet to transition meaningfully toward active on-chain utilization. This gap reflects not a lack of demand for BTCFi, but rather the absence of sufficiently developed access pathways that align with institutional operating models and prevailing regulatory frameworks.

Within this context, digital asset custody emerges as the critical inflection point. Custody allows institutions to deposit and manage Bitcoin within infrastructure they already understand and trust, while simultaneously serving as a foundation from which on-chain utilization can be expanded over time. In practical terms, custody functions as the first effective checkpoint and the core gateway through which institutionally held Bitcoin can transition into BTCFi.

2-1. Custody as Core Institutional Infrastructure

https://www.grandviewresearch.com/industry-analysis/digital-asset-custody-market-report

https://www.grandviewresearch.com/industry-analysis/digital-asset-custody-market-report

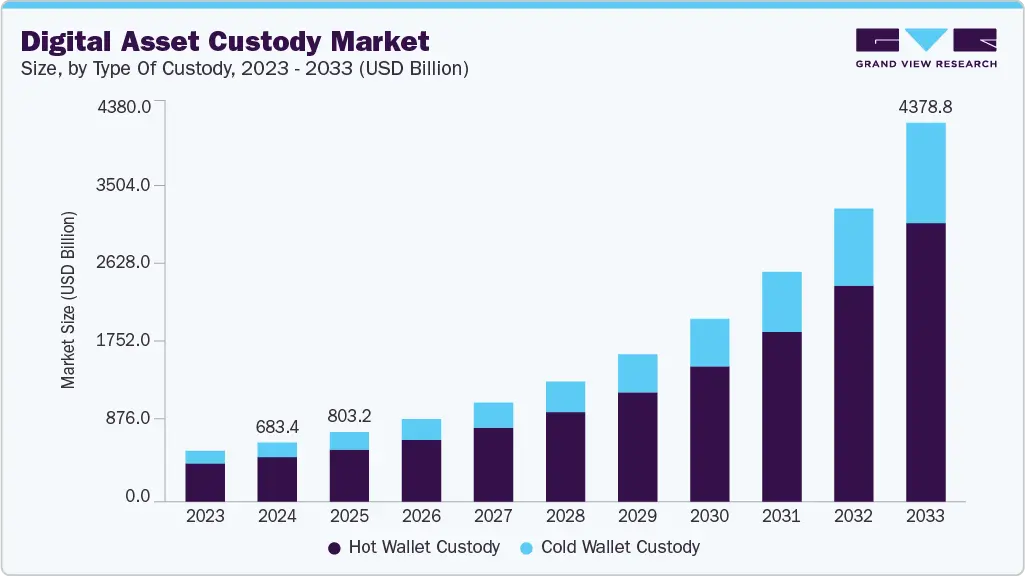

Institutional approaches to BTCFi diverge materially from those of individual participants. Rather than operating on-chain wallets directly and absorbing the associated operational and security risks, institutional investors show a clear preference for indirect access channels mediated by regulated digital asset custodians operating within established compliance frameworks. As a result, the global institutional digital asset custody market has expanded rapidly in recent years, with growth driven not only by rising asset prices but also by structural adoption.

According to Grand View Research, the digital asset custody market is estimated to reach $803B in size by 2025, with an expected compound annual growth rate of 23.6%. This expansion reflects growing institutional demand for compliant infrastructure capable of supporting large-scale digital asset holdings.

Bitcoin’s strong long-term holding characteristics further reinforce the central role of custody. For institutions, custody extends well beyond passive safekeeping; it serves as a core operational layer that enables Bitcoin deployment under controlled conditions. By maintaining custody-level frameworks for asset safekeeping, permissioning, auditing, and risk management, institutions can incrementally expand the scope of asset utilization without abandoning regulatory or operational discipline. For this reason, the custody environment has effectively become the starting point through which institutional capital enters the BTCFi ecosystem.

2-2. The U.S. Regulatory Perimeter and Anchorage’s Role

In a custody-driven approach to BTCFi, the United States represents the most critical market. It concentrates a substantial share of global institutional capital, while regulatory interpretations and policy decisions formed in the U.S. tend to shape market practices well beyond its borders.

https://bitcointreasuries.net/countries/united-states/private-companies

https://bitcointreasuries.net/countries/united-states/private-companies

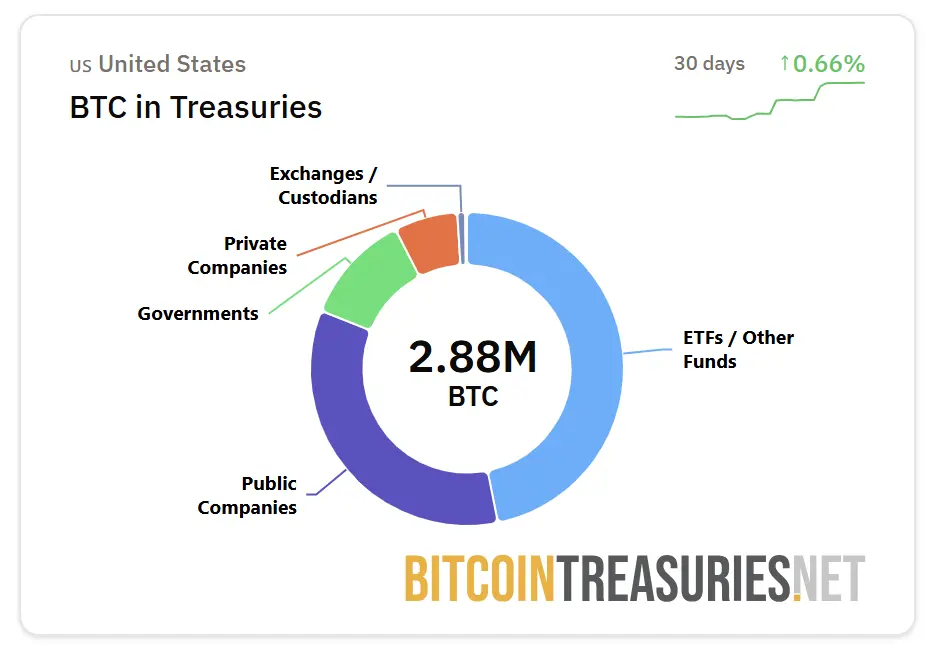

Data from Bitcointreasuries.net illustrates this concentration clearly. Bitcoin holdings attributable to the U.S. government and U.S.-based entities, including corporations and ETFs, amount to approximately 2.88M BTC, representing nearly 78.7% of total global institutional holdings of 3.66M BTC. As a result, the availability of legally compliant digital asset custody operating within the U.S. regulatory framework becomes a decisive factor in determining whether institutions can realistically participate in BTCFi.

Against this backdrop, Anchorage Digital Bank occupies a structurally distinct position. Anchorage is currently the only digital asset bank in the United States operating under a federal charter granted by the Office of the Comptroller of the Currency (OCC). It is therefore not merely a digital asset custody provider, but a financial institution fully embedded within the U.S. federal banking regulatory regime. This distinction sets Anchorage apart from the majority of digital asset custodians, which typically operate under state-level trust company licenses or specialized custody charters. Federal charter status carries meaningful implications. Anchorage is subject to the same regulatory obligations as traditional banks, including capital requirements, internal control standards, risk management frameworks, audit obligations, and ongoing regulatory reporting. For institutional participants, this alignment significantly reduces legal and operational uncertainty when engaging with digital assets.

Anchorage’s regulatory footprint extends beyond the United States. The firm has also secured a Digital Payment Token (DPT) license from the Monetary Authority of Singapore (MAS), enabling it to operate within a coordinated regulatory framework spanning both the U.S. and Asia. This dual-jurisdiction positioning reinforces Anchorage’s appeal to institutions that prioritize regulatory consistency and institutional durability over specific products or features.

2-3. Custody as a Filter for Institutional Capital

Within this framework, a critical point emerges: BTCFi participation routed through regulated custody does not merely expand access, but brings about observable changes in actual capital flows. Regulated custodians do not integrate all BTCFi chains uniformly; integration is selective, based on regulatory compatibility, risk structure, and operational stability. As a consequence, custody support itself functions as a filter that determines which BTCFi pathways institutional capital can realistically access.

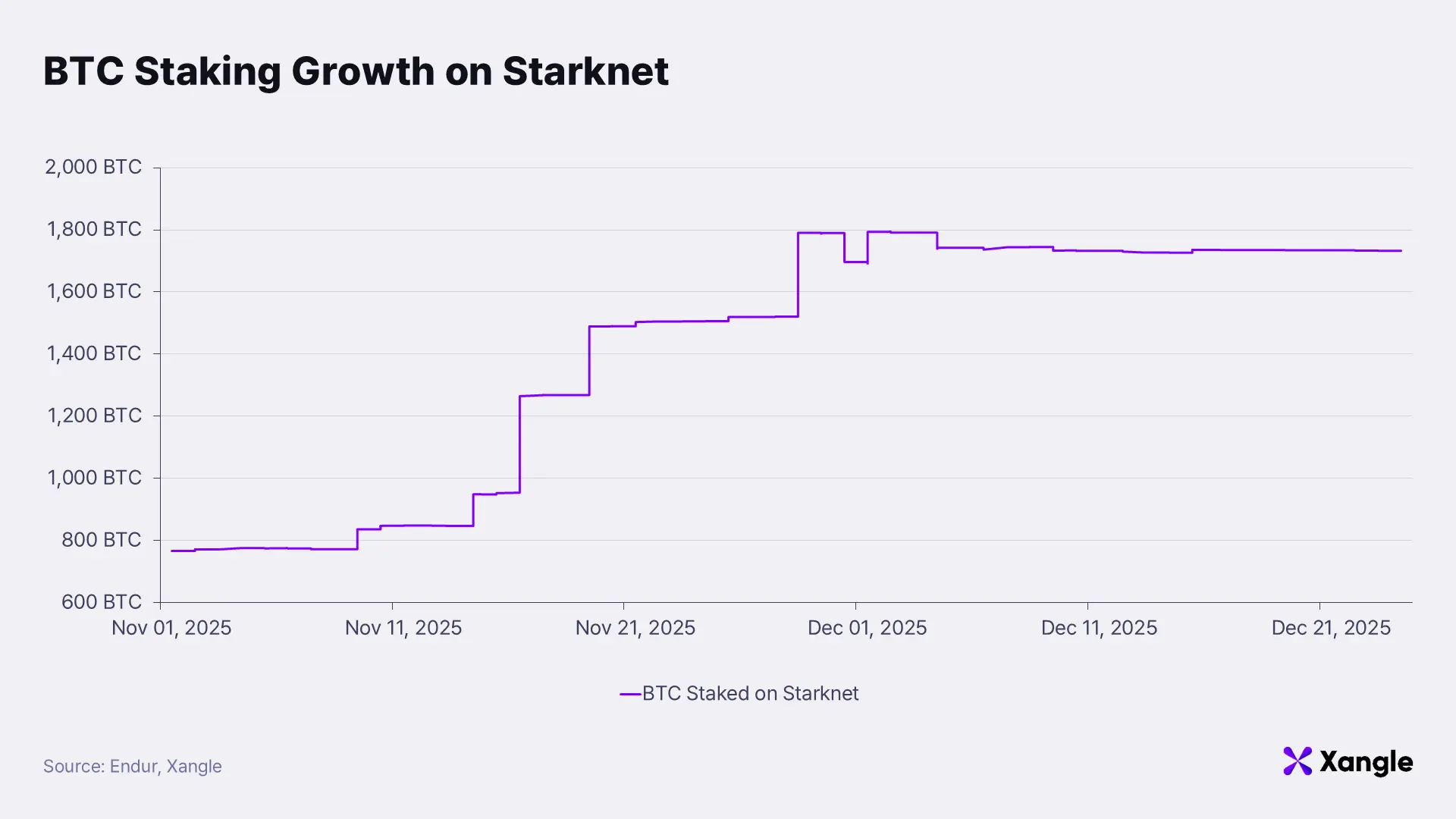

This dynamic became visible in November, when Anchorage officially began supporting Starknet-based BTC staking. At the beginning of the month, the number of BTC staking positions remained around 700; by the end of November, that figure had risen to over 1,700. The increase indicates that institutional inflows routed through regulated custody have moved beyond latent interest and entered a phase where capital deployment can be observed through concrete, on-chain data.

The implications extend beyond headline participation metrics. Institutional inflows via custody do not simply add new participants to the BTCFi ecosystem; they act as a catalyst for the initial phase in which capital begins to circulate meaningfully. As regulatory custody approval converges with measurable capital movement, the BTCFi market is shifting away from proof-of-concept and toward a stage where institutional capital is actively engaged and operational.

3. Why Institutions Converge on Starknet

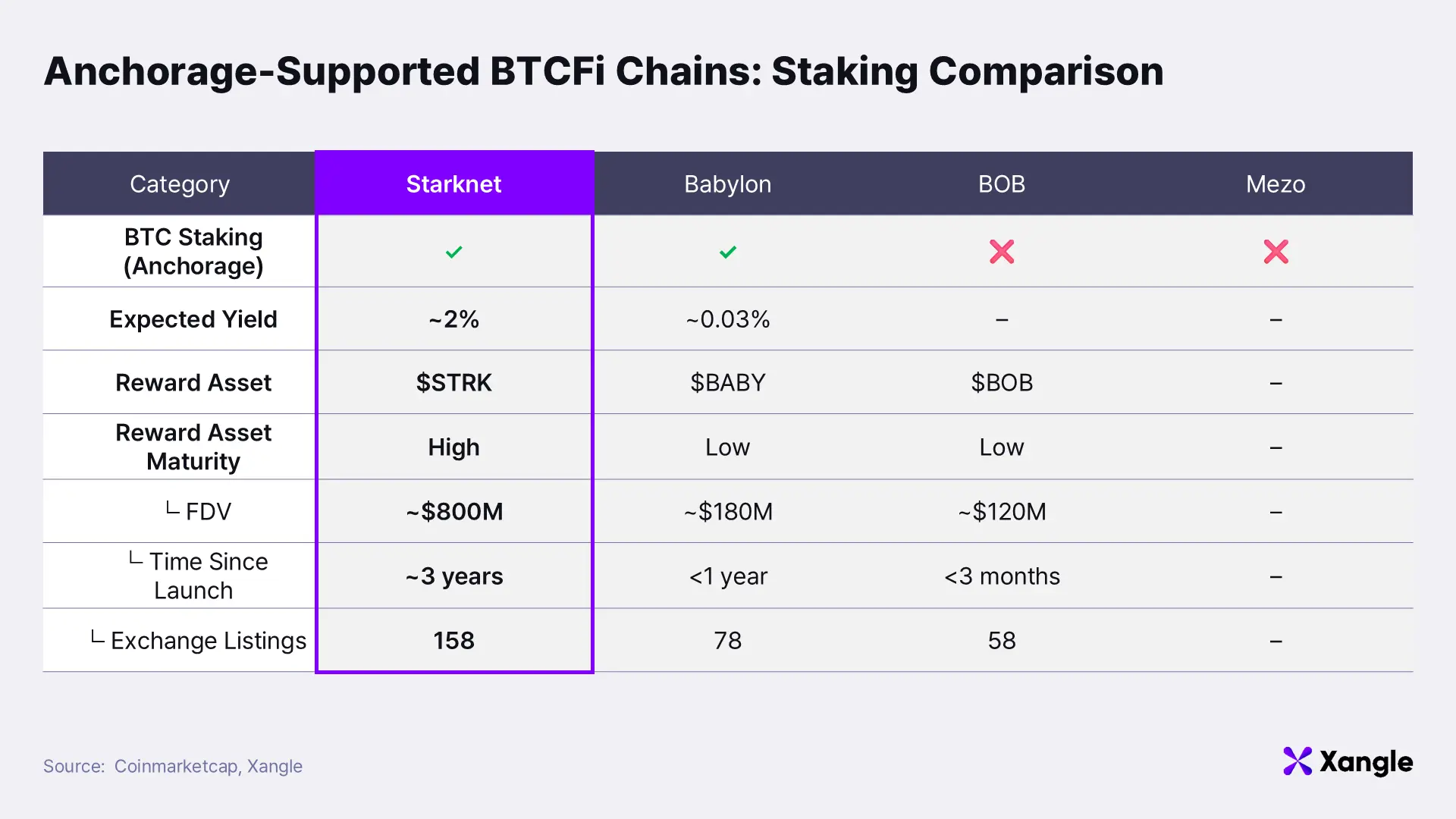

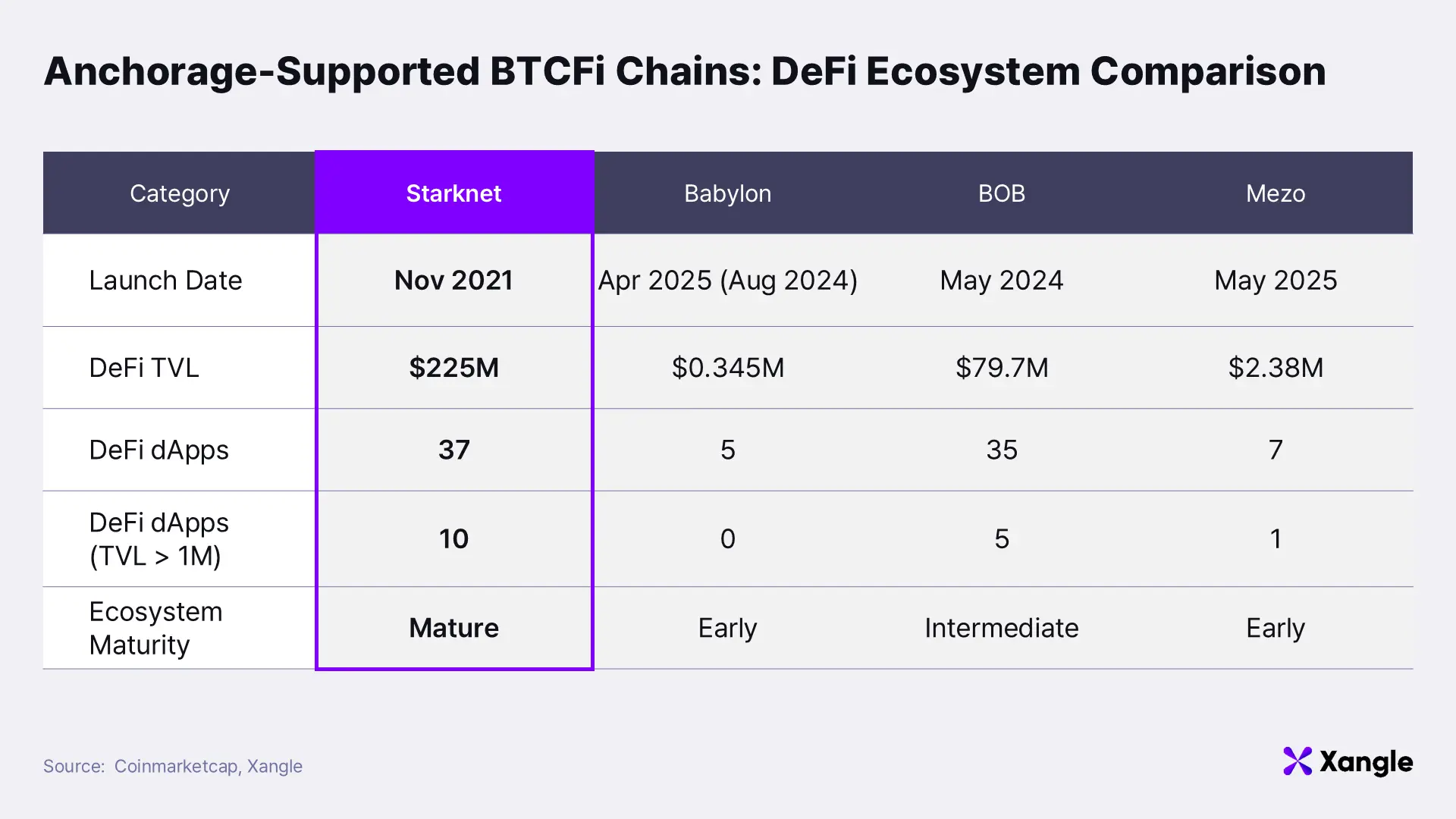

As institutional capital inflows routed through regulated custodians such as Anchorage become observable in practice, the BTCFi discussion is shifting away from a phase centered on theoretical feasibility toward a more concrete evaluation of which chains meet institutional standards. At present, Anchorage provides custody support for four BTCFi-related chains: Starknet, Babylon, BOB, and Mezo. Among them, Starknet stands out as the chain that most clearly satisfies institutional requirements across three dimensions: yield structure, reward asset stability, and post-staking operational extensibility.

3-1. Yield Competitiveness and Reward Asset Maturity

From a yield perspective, Starknet’s relative competitiveness is unambiguous at the current stage. Expected returns from Babylon-based BTC staking remain around 0.03% when excluding participation in BABY co-staking, while BTC staking on Starknet, designed to secure a PoS-based chain, offers yields of approximately 2%. BOB does not yet support BTC staking, and Mezo likewise lacks a native BTC staking mechanism. Even when viewed purely through the lens of headline yields, Starknet therefore represents the most competitive option among currently supported BTCFi chains.

Beyond headline yield, Starknet’s reward structure further reinforces its institutional appeal. BTC staking rewards are distributed in $STRK, a mature native asset that has traded in open markets for nearly three years and has undergone meaningful liquidity formation and price discovery. For institutions that prioritize predictability and seek to minimize volatility and liquidity risk in reward assets, this translates into a materially more stable yield profile.

By contrast, Babylon’s $BABY (FDV $180M) and BOB’s $BOB (FDV $120M) remain in early circulation phases, with limited market depth relative to the scale of institutional capital. The fact that $STRK maintains an FDV exceeding $800M and is listed across major global exchanges makes this divergence particularly salient. In institutional portfolio construction, the maturity and liquidity of the reward asset are not secondary considerations; they are foundational to determining whether a staking strategy can be deployed at scale.

3-2. Staking as Security, Not Yield Engineering

Staking is not defined solely by yield generation; its core function lies in how effectively capital contributes to network security. On Starknet, BTC staking is directly integrated into a PoS-based security model. As the volume of staked BTC increases, the economic cost required to attack or disrupt the network rises in parallel. The incentive structure therefore shifts decisively: incremental staking makes hostile behavior progressively more uneconomical, transforming staking from a passive yield mechanism into an active pillar of network stability.

Across the broader BTCFi landscape, including chains supported by Anchorage, structures in which Bitcoin is meaningfully deployed for chain security remain limited. At present, only a small subset of networks, such as Babylon and Core, satisfy this criterion. In most BTCFi implementations, Bitcoin functions as one asset among many within DeFi applications, without a direct linkage to base-layer security. Starknet diverges from this pattern. BTC staking is explicitly designed to reinforce chain security, with Bitcoin deployed toward a clearly defined objective and rewarded through a predictable compensation framework.

Security-contributive staking structures exhibit characteristics that align closely with institutional preferences for durability and stability. Because rewards are directly anchored to a non-optional network function, their economic rationale remains transparent, and the mechanism itself is likely to persist as long as the network remains operational. Within the BTCFi landscape, Starknet therefore represents one of the few cases where real utility and reward distribution are tightly coupled. From the perspective of regulated custodians, this alignment materially strengthens the case for viewing Starknet’s BTC staking as a long-term, predictable, and institution-compatible staking structure.

3-3. An Execution Environment for Institutional BTC Strategies

Institutions do not select chains based solely on headline yields. Asset managers and professional investment firms with established operational capabilities and risk management frameworks also evaluate how assets can be deployed beyond initial staking, as well as whether the underlying chain offers long-term operational scalability. Staking, in this context, represents only the entry point of institutional BTCFi participation; the availability of an execution environment capable of supporting sustained and diversified operations becomes a decisive criterion.

https://www.anchorage.com/insights/porto-by-anchorage-digital-your-wallet-our-security

https://www.anchorage.com/insights/porto-by-anchorage-digital-your-wallet-our-security

This assessment framework is already reflected in institutional infrastructure. Through Porto, its institutional self-custody wallet, Anchorage enables on-chain DeFi access while preserving custody-grade security and control. Porto is designed to allow institutions to engage directly in on-chain activity without materially compromising asset safety, permissioning, or risk controls. As a result, direct on-chain execution becomes compatible with institutional governance and regulatory standards rather than existing outside them.

Within this framework, the scale and maturity of a DeFi ecosystem emerge as central considerations. Starknet has been operational since 2021, accumulating both network stability and technical credibility over approximately four years. In parallel, it has developed a DeFi ecosystem with demonstrable real-world usage. This combination provides the foundation for extending asset deployment beyond BTC staking into lending, liquidity provision, and structured strategies.

DefiLlama data highlights clear disparities in DeFi maturity across BTCFi-related chains. Babylon Genesis records a TVL of $0.345M, with no dApps exceeding $1M in TVL, placing it at an early stage as a DeFi execution layer. BOB reports a TVL of $79.7M with five dApps above $1M, indicating a constrained growth phase, while Mezo remains smaller with a TVL of $2.38M and only one dApp above $1M. By contrast, Starknet holds a TVL of $225M and supports ten dAppswith TVL exceeding $1M, positioning it as the most mature ecosystem in terms of both scale and depth.

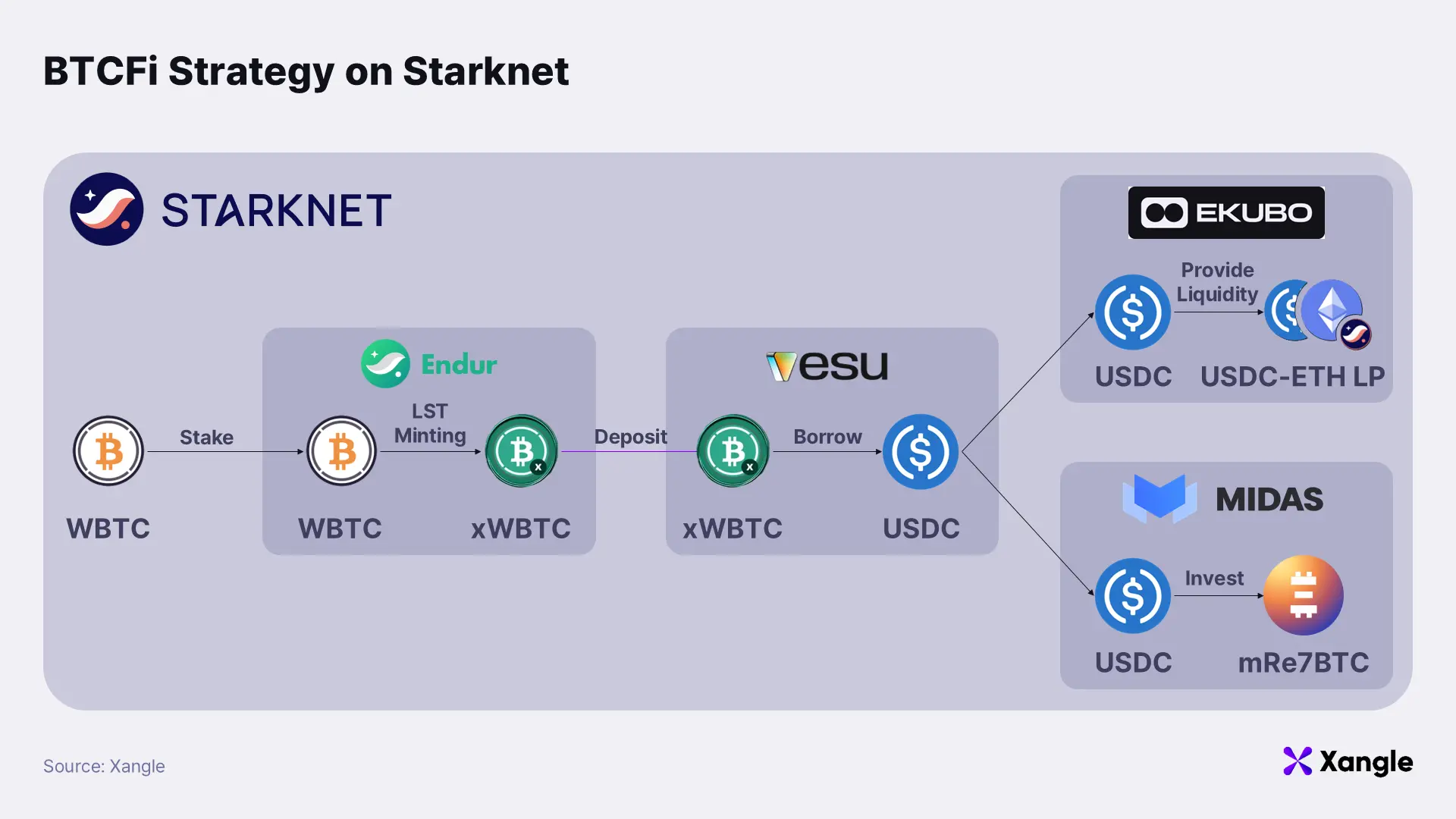

On Starknet, DeFi infrastructure centered on BTC assets is already in place. Ekubo, a concentrated-liquidity AMM, enables large-scale capital deployment with minimal slippage. Endur facilitates the liquidity of staking positions through BTC-based liquid staking tokens (LSTs). Vesu operates as a lending and leverage layer that accepts these LSTs and stablecoins as collateral. In parallel, Midas offers tokenized BTC and structured strategies designed by operators such as Re7, creating standardized access points through which institutional capital can gain indirect exposure.

These components support composable operational strategies. For example, an institution can stake WBTC via Endur to mint an LST token (xWBTC), deposit xWBTC into Vesu to generate yield, then use it as collateral to borrow USDC. The borrowed liquidity can be deployed on Ekubo or allocated to tokenized Re7 strategies through Midas, allowing yield structures to be expanded without exiting the ecosystem.

Beyond individual protocols, Starknet functions as an environment in which institution-grade BTC strategies are actively designed and validated through collaboration with on-chain asset managers such as Re7 Capital and 0D Capital. Institutional products developed by operators like Re7 incorporate features such as redemption controls and NAV reporting, aligning with requirements for operational control, transparency, and reporting. This approach diverges from short-term, incentive-driven models and instead reflects institutional strategies focused on systematically diversifying yield while maintaining BTC exposure.

The same ecosystem supports multiple participation models. Institutions with in-house execution and risk management capabilities can use Starknet directly as an execution layer for on-chain strategies. Those less comfortable with direct execution can access BTCFi exposure indirectly through fund-style or structured products offered by managers such as Re7 Capital or 0D Capital. More conservative institutions may limit exposure to Starknet-based BTC staking within custody environments, securing a constrained but stable form of BTCFi participation.

4. BTCFi Season: Incentives as Economic Design

Starknet has already established an execution environment in which BTC staking serves as the entry point for broader asset utilization. The remaining question is whether Starknet’s BTCFi framework can sustain institutional-scale liquidity while preserving yield efficiency as capital inflows grow. The core issue is not the ability to attract liquidity in the short term, but whether the structure can evolve into a revenue model that remains functional and durable over time.

It is against this backdrop that Starknet introduced BTCFi Season. The program is deliberately distinct from conventional liquidity mining initiatives designed to rapidly bootstrap capital. Starknet’s BTCFi strategy prioritizes the conversion of BTC from idle collateral into continuously productive capital, rather than short-lived incentive extraction.

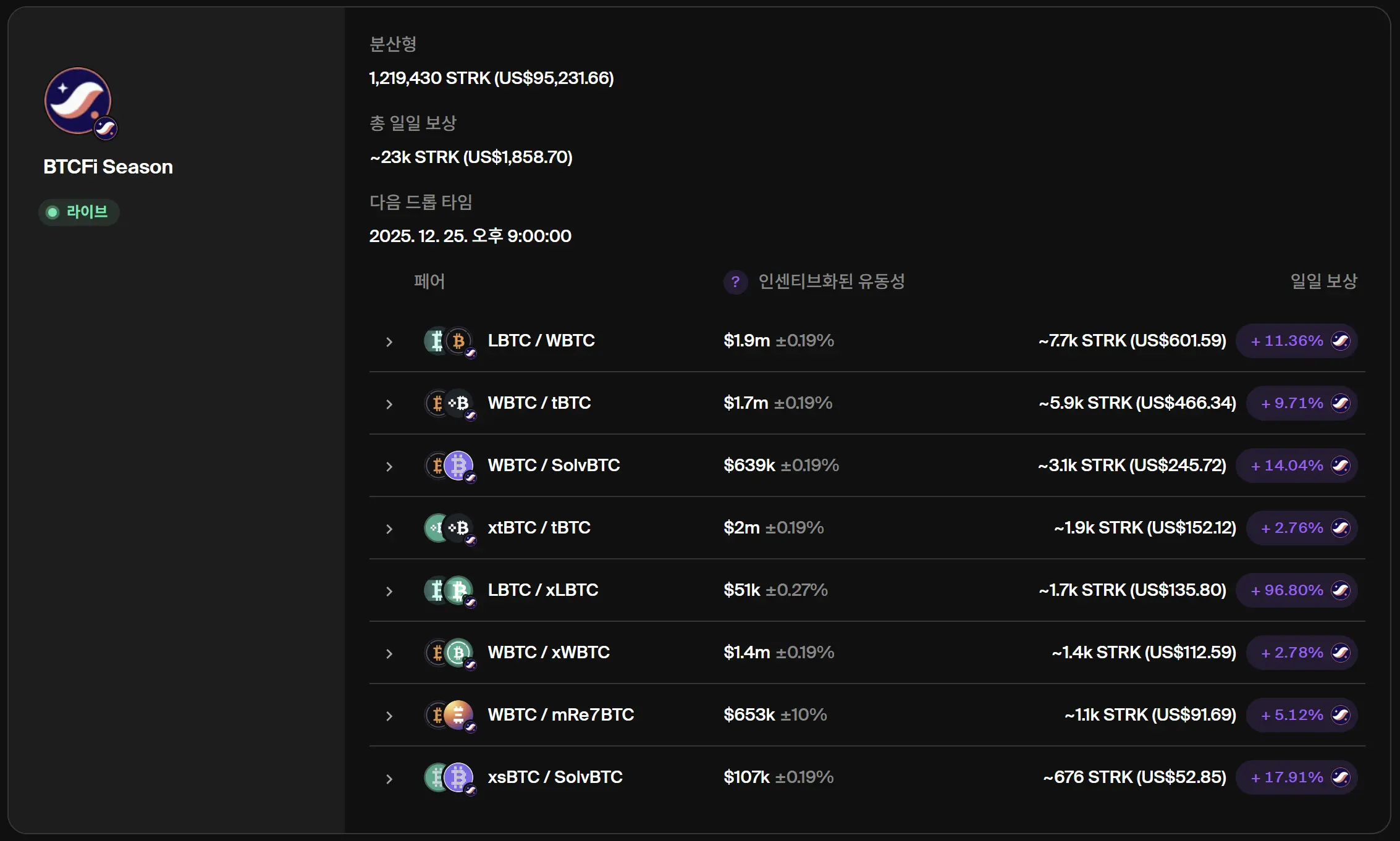

A total incentive budget of 100M STRK has been allocated to BTCFi Season. Importantly, these incentives are not distributed evenly across all deposited assets; rewards are concentrated on activities that generate actual economic output, including deposits, borrowing, and liquidity provision.

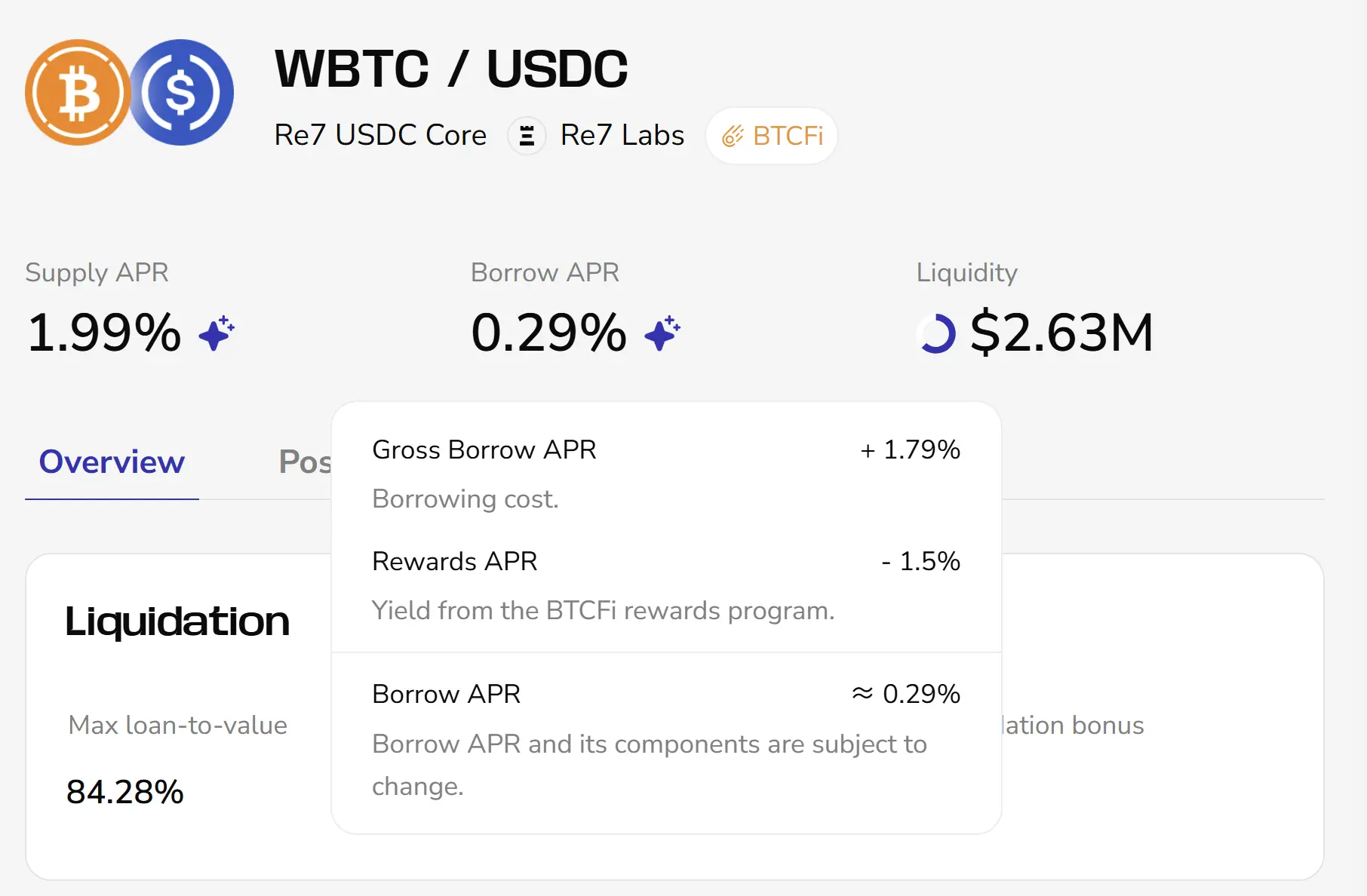

Vesu provides a representative example. Users can deposit WBTC and borrow USDC against it. Depositing WBTC earns approximately 1.99% APR, while borrowing USDC is also subsidized through incentives. Instead of paying the nominal borrowing rate of around 1.79%, borrowers receive rewards equivalent to roughly 1.5%, resulting in an effective net borrowing cost of approximately 0.29%. This structure actively encourages the use of lending functions where real borrowing demand and economic costs exist.

Borrowed USDC can then be deployed across the Starknet ecosystem, contributing to broader liquidity expansion. By incentivizing this full sequence of actions, BTCFi Season targets genuine liquidity growth and yield generation rather than passive capital parking.

At a structural level, this design transforms BTC into productive capital circulating through borrowing, LP provision, and vault strategies. Once BTC enters Starknet, it participates in a continuous economic loop: staking → deposit and borrowing → LP or vault deployment → fee generation. Over time, the primary source of returns shifts away from incentives toward recurring cash flows derived from borrowing demand and trading fees.

Incentives extend beyond lending into liquidity provision. On Ekubo, one of Starknet’s core DeFi protocols, LPs supplying liquidity to BTC pairs such as LBTC, WBTC, tBTC, and SolvBTC receive STRK rewards. This deepens liquidity across BTC markets and enables large swaps to be executed with minimal slippage. The resulting effects are structural:

- 1. Improved oracle price reliability,

- 2. Enhanced liquidation efficiency, and

- 3. Expanded liquidity across BTC pairs, supporting smoother BTCFi activity overall.

In this sense, Starknet’s incentive design is not a mechanism for indiscriminate liquidity attraction. Incentives are deployed selectively to reinforce system functionality, improve risk management, and strengthen the operational integrity of the BTCFi ecosystem.

Taken together, BTCFi Season functions less as a rewards campaign and more as an economic architecture that ensures BTC remains actively deployed where real demand exists. Rather than inflating short-term metrics, Starknet is constructing a yield framework capable of retaining institutional capital over the long term. Through this approach, Starknet consistently advances its positioning as a central hub for sustainable Bitcoin yield.

5. Conclusion: The Growth Potential of Starknet with BTCFi

If institutional Bitcoin holdings continue to expand along the current trajectory, and if BTC increasingly transitions from a passive store of value to an actively deployed yield-bearing asset, the addressable opportunity for Starknet becomes substantial. Based on the trends outlined in Section 1, institutional ownership could reach approximately 36% of total circulating supply within five years, equivalent to roughly 51.9% on a liquid-supply basis.

Applied to the current circulating supply of approximately 19.96M BTC, this implies around 7.2M BTC held by institutions. Even if only 20% of that supply were deployed into BTCFi, roughly 1.44M BTC could enter the market as yield-generating capital. At a BTC price of $87,000, this translates into a potential BTCFi market of approximately $125B.

Under a conservative assumption in which Starknet captures 10% of this market, BTCFi TVL on Starknet alone could reach approximately $12.5B; this represents nearly 55× its current DeFi TVL of $225M. Applying a typical 2–3% annual yield relative to TVL, the Starknet ecosystem could support an estimated $250M–$375M in annual revenue capacity.

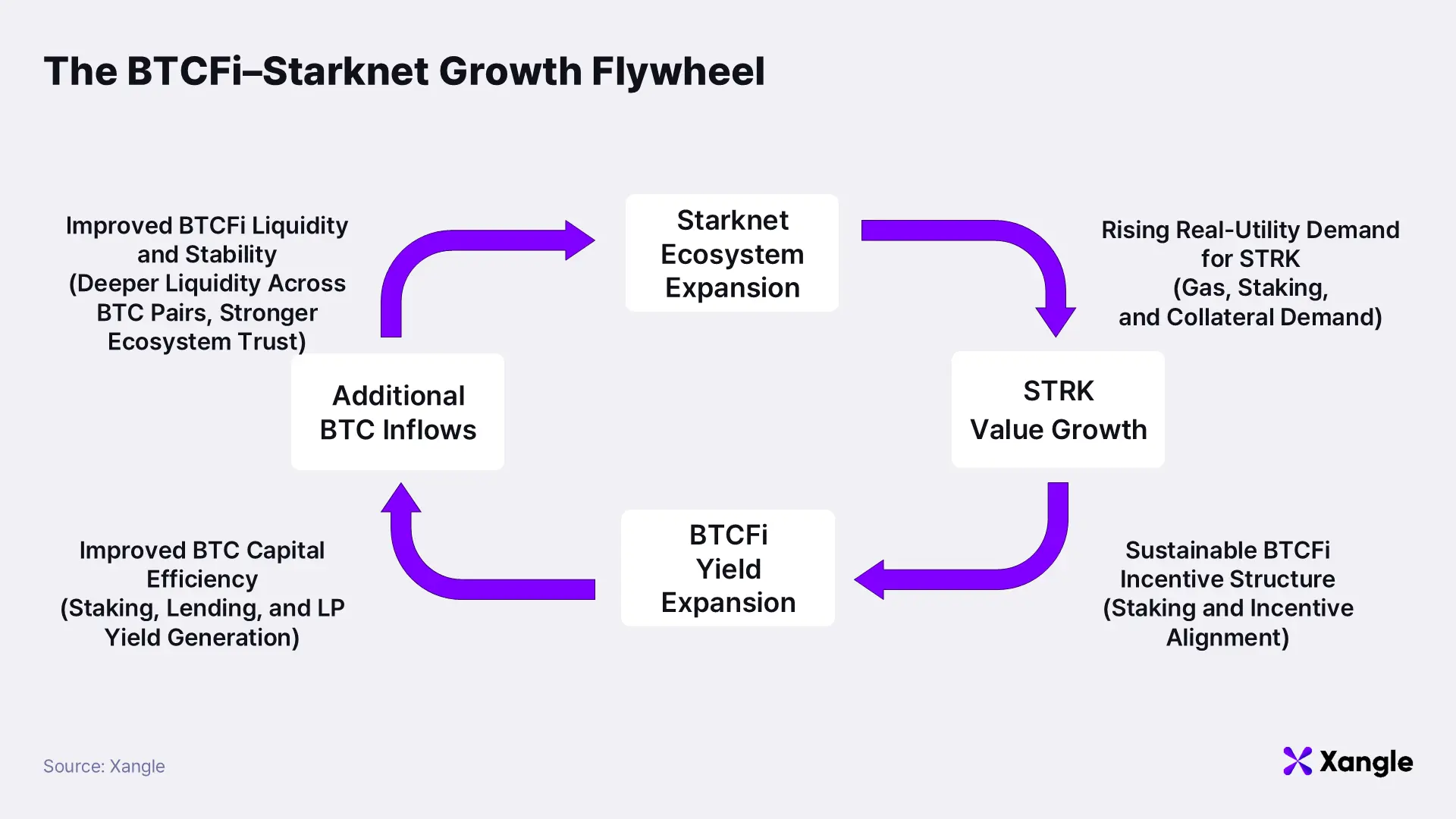

Crucially, this growth is not confined to headline TVL expansion. As activity on Starknet increases, structural demand for STRK rises across gas fees, staking, collateral usage, and governance participation. Should STRK burn or buyback-and-burn mechanisms—prioritized in the September 2025 community discussions—be implemented, higher network utilization would translate into a reduction in effective STRK supply. This dynamic reinforces BTC staking and BTCFi profitability, encouraging additional BTC inflows and forming a self-reinforcing BTC–STRK dual flywheel: BTC inflows raise on-chain asset value, strengthen security and stability, and further enhance yield potential.

At present, the absence of a native BTC bridge remains a constraint. BTCFi activity on Starknet relies on wrapped BTC assets, which some institutions may view as a barrier to entry. In the near term, this limitation is mitigated through regulated custody and insurance structures. Over the medium to long term, the roadmap points toward a structural resolution via a trustless BTC bridge.

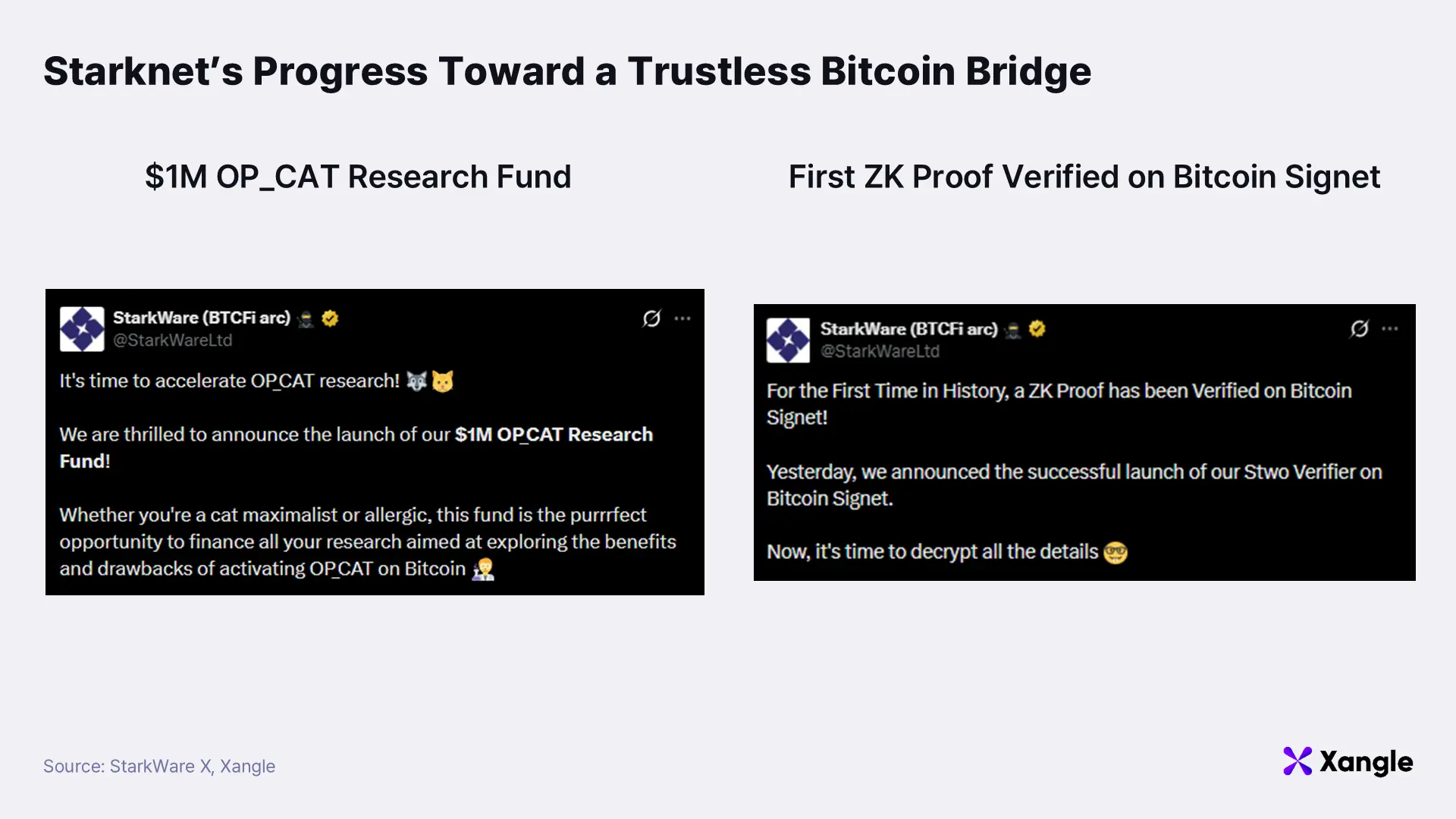

The introduction of OP_CAT opens a path toward such a solution. Once the Bitcoin network itself can verify computational results, including STARK proofs, Starknet becomes one of the few execution layers capable of supporting dual settlement across both Ethereum and Bitcoin. Starknet and its parent company, StarkWare, possess deep technical expertise in proof systems, recursive proofs, and proof compression; this includes a $1M allocation to OP_CAT-related research and the first successful implementation of ZK proofs on the Bitcoin testnet. This level of technical readiness positions Starknet to be among the earliest platforms capable of realizing a trust-minimized BTC bridge.

In that scenario, BTC would no longer rely on custody intermediaries or multisig federations for mobility. Instead, it could function on Starknet as a trust-minimized collateral asset verified directly by the Bitcoin chain, materially improving the risk profile for large-scale institutional deployment.

Taken together, Starknet’s BTCFi strategy is coherent across three dimensions: a custody-compatible capital inflow pathway, a sustainable yield structure grounded in real economic activity, and a forward-looking technical roadmap toward trustless BTC. In the short term, Starknet provides institutions with a realistic entry point via regulated custody while supporting yield generation through borrowing, liquidity, and trading. Over the medium to long term, the implementation of a trustless BTC bridge aims to resolve structural trust constraints entirely. In this context, Starknet stands out as an execution layer structurally prepared to absorb institutional capital as BTCFi enters its next phase of expansion.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article was written at the request of Starknet. All content in this article was written independently by the author(s), and neither CrossAngle nor Starknet had any editorial control or influence over the content. The author(s) may hold the cryptocurrencies mentioned in this article at the time of writing.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.