Ethereum Breaks Free: The SEC’s Green Light for Institutional DeFi

Table of Contents

1. The Turning Point: Ethereum Breaks Free from the Security Debate

2. Where the Line Is Drawn: Understanding the Howey Test and Crypto Classification

3. From Crackdown to Clarity: The SEC’s Policy Pivot on Ethereum

4. The Floodgates Open: Institutional Capital Flows into Ethereum

5. The DeFi Liquidity Engine: How Staking Powers Ethereum’s Monetary Layer

6. Building the Backstop: Institutional Capital as Ethereum’s Lender of Last Resort

7. The New Monetary Order: Ethereum’s Rise as the Global Settlement Layer

The Turning Point: Ethereum Breaks Free from the Security Debate

source : Bitcin.com News X

On September 10, 2025, at the OECD Global Financial Markets Roundtable, SEC Chair Paul Atkins delivered a landmark keynote speech that outlined a new regulatory vision for the cryptocurrency industry. He stated that the SEC would allow innovations such as “super-app trading platforms” and emphasized the importance of establishing legally sound frameworks that enable capital formation directly on-chain.

While this alone marked a notable departure from the SEC’s historically conservative stance on digital assets, the more consequential part of Atkins’ remarks addressed the legal classification of cryptocurrencies. “Most crypto tokens are not securities, and we will draw that boundary clearly,” he declared, adding that the SEC intends to “make it possible to raise capital on-chain without endless rounds of legal review.” This was not merely a definitional statement—it was a declaration of intent to remove the single largest regulatory constraint that has long limited the growth of the crypto market.

The agency has already begun putting that commitment into practice, increasingly recognizing that many areas of the crypto ecosystem do not fall under securities regulation. In recent months, the SEC concluded that Ethereum staking does not constitute a security, and subsequently determined that liquid staking also lies outside the securities framework. Understanding the implications of such a shift—why crypto assets and the protocols built upon them are no longer deemed securities—requires a closer look at U.S. securities law and the regulatory trajectory that led to this point.

Where the Line Is Drawn: Understanding the Howey Test and Crypto Classification

Understanding the SEC’s stance on security classification first requires a grasp of how financial assets are regulated in the United States. U.S. assets are categorized as commodities, securities, or trusts. Commodities encompass tangible goods such as agricultural products and minerals, as well as financial instruments like gold, silver, and foreign exchange. Securities, by contrast, are a form of investment contract—financial assets whose expected returns depend on the managerial or entrepreneurial efforts of others.

The distinction matters because each category faces a different regulator and compliance burden. Commodities fall under the Commodity Futures Trading Commission (CFTC), while securities are overseen by the Securities and Exchange Commission (SEC). Being classed as a security triggers disclosure obligations and materially heightens regulatory risk. Most cryptocurrencies lack a centralized operating entity capable of making such disclosures, so a security designation effectively renders them unregistered securities subject to enforcement. That dynamic explains why the ICO boom of the late 2010s was essentially shut down under SEC action.

Institutional adoption of crypto hinges on clarity around security status. The core framework used in the United States is the Howey Test, derived from a 1946 Supreme Court decision defining what constitutes a security. In that case, W.J. Howey Co. sold portions of its Florida citrus groves to investors and offered service contracts to manage the groves and distribute profits. The SEC argued the arrangement amounted to a security because investor returns depended on the company’s efforts, while Howey maintained it was merely selling land, not issuing securities.

The dispute reached the Supreme Court, which articulated four criteria—now known as the Howey Test—for identifying a security: (1) an investment of money, (2) in a common enterprise, (3) with a reasonable expectation of profits, (4) to be derived from the entrepreneurial or managerial efforts of others. Among these elements, the fourth is the fulcrum.

If Howey had sold the land without offering any management services, the purchase would not have been considered a security. However, once the company took on the role of managing the groves and distributing profits to investors, the nature of the arrangement changed. At that point, it became an investment contract—essentially a security—because investors’ returns were now tied directly to the entrepreneurial and managerial efforts of Howey Co.

That logic carries significant implications for crypto. Blockchains are designed without a centralized operator responsible for network management or disclosures, yet sustaining a network still requires ongoing contributions of resources and time by miners, validators, and node operators. Legal ambiguity arises at exactly this point: do such contributions amount to “entrepreneurial or managerial” efforts that could render a token a security?

Bitcoin provides a clear example. Miners and nodes unquestionably incur costs to sustain the network, but there is no direct causal relationship between their actions and the profits of Bitcoin holders. Miners engage in mining for their own economic incentive, and in doing so, they indirectly benefit holders by securing the network and preserving its value. However, Bitcoin holders do not receive profits as a result of the miners’ managerial or entrepreneurial activity. In other words, there is no contractual or investment link between the holders of Bitcoin and those who operate the network, leaving little basis to classify BTC as a security. By the same reasoning, Ethereum under its earlier Proof-of-Work (PoW) model was also more appropriately treated as a commodity rather than a security.

Conditions changed with The Merge, which moved Ethereum from PoW to Proof-of-Stake (PoS). Staking introduces a more direct connection between stakers and rewards than mining does. ETH holders delegate to validators; validators use the staked ETH to secure the network and earn yield, then distribute rewards back to delegators. On that basis, the SEC could contend that staking rewards are profits derived from others’ efforts (e.g., validators or staking-pool operators). Advocates of staking counter that validator activity is fundamentally technical or administrative—security of the protocol—rather than entrepreneurial. Classification ultimately turns on how one characterizes validator work: entrepreneurial/managerial, which points toward security status, or technical/procedural, which supports a non-security conclusion. The outcome shapes Ethereum’s legal posture—and, by extension, the broader trajectory of the crypto ecosystem.

From Crackdown to Clarity: The SEC’s Policy Pivot on Ethereum

During the Biden administration, the SEC pursued a hardline approach that restrained the growth of the cryptocurrency market—particularly the DeFi sector. Then-Chair Gary Wexler maintained that most cryptocurrencies and DeFi protocols qualified as securities, initiating a series of lawsuits against major exchanges and DeFi lending platforms for offering unregistered securities. The agency’s aggressive posture created a chilling effect on institutional engagement. Even when financial institutions launched Ethereum ETFs, they deliberately excluded staking functionality to avoid regulatory repercussions, signaling a broader reluctance to interact directly with DeFi platforms.

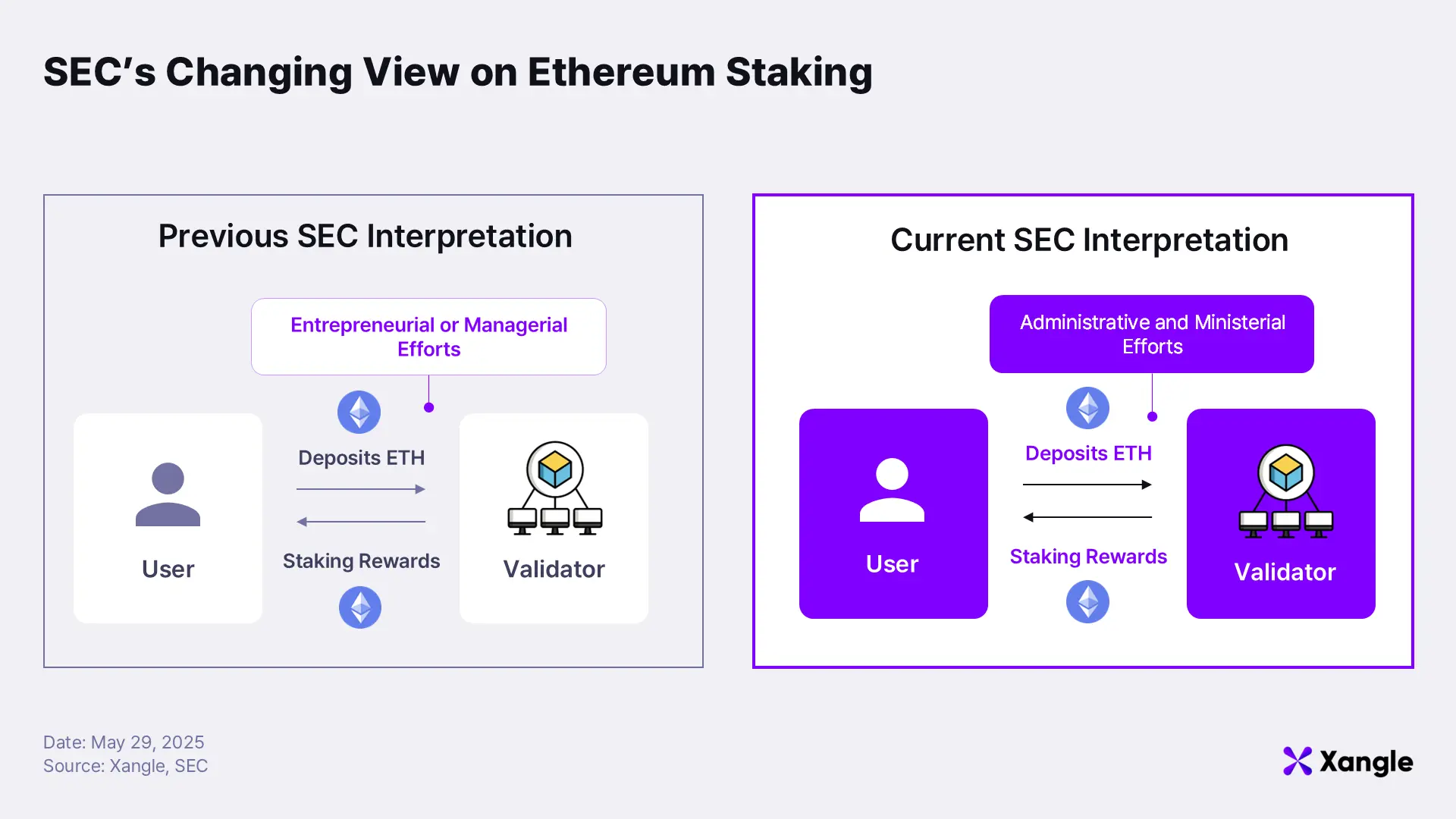

The landscape shifted sharply with the transition to the Trump administration and the appointment of Paul Atkins, a long-time crypto advocate, as the new SEC Chair. Under Atkins, the SEC’s stance on digital assets turned markedly more constructive. Reflecting this policy shift, the SEC issued a pivotal statement on May 29, 2025, clarifying that certain forms of Ethereum staking do not constitute securities. The agency delineated three types of staking activities exempt from securities classification:

(1) validators staking Ethereum directly as node operators;

(2) Ethereum holders delegating ETH to validators and receiving rewards; and

(3) Ethereum holders entrusting ETH to third parties under custody agreements and earning the resulting yield.

In its explanation, the SEC concluded that these three categories do not involve “entrepreneurial or managerial efforts”, but rather “administrative or ministerial activities.” In other words, staking in these contexts represents operational work necessary to maintain Ethereum’s infrastructure, rather than a profit-driven enterprise. Any yield generated is incidental, not the result of managerial labor. Accordingly, staking conducted in these ways does not meet the definition of a security—even when it produces returns for participants.

The shift in tone did not end there. On August 5, 2025, the SEC announced another landmark clarification: liquid staking, too, would not be treated as a security. The Commission reaffirmed that liquid staking involves administrative or managerial functions rather than entrepreneurial activity. Importantly, the SEC also determined that the staking receipt tokens issued through these mechanisms—such as Lido’s stETH—are not securities either. The decision effectively opened the door for institutional integration of liquid staking assets, enabling regulated entities to adopt them within portfolios and structured products without breaching securities law.

The Floodgates Open: Institutional Capital Flows into Ethereum

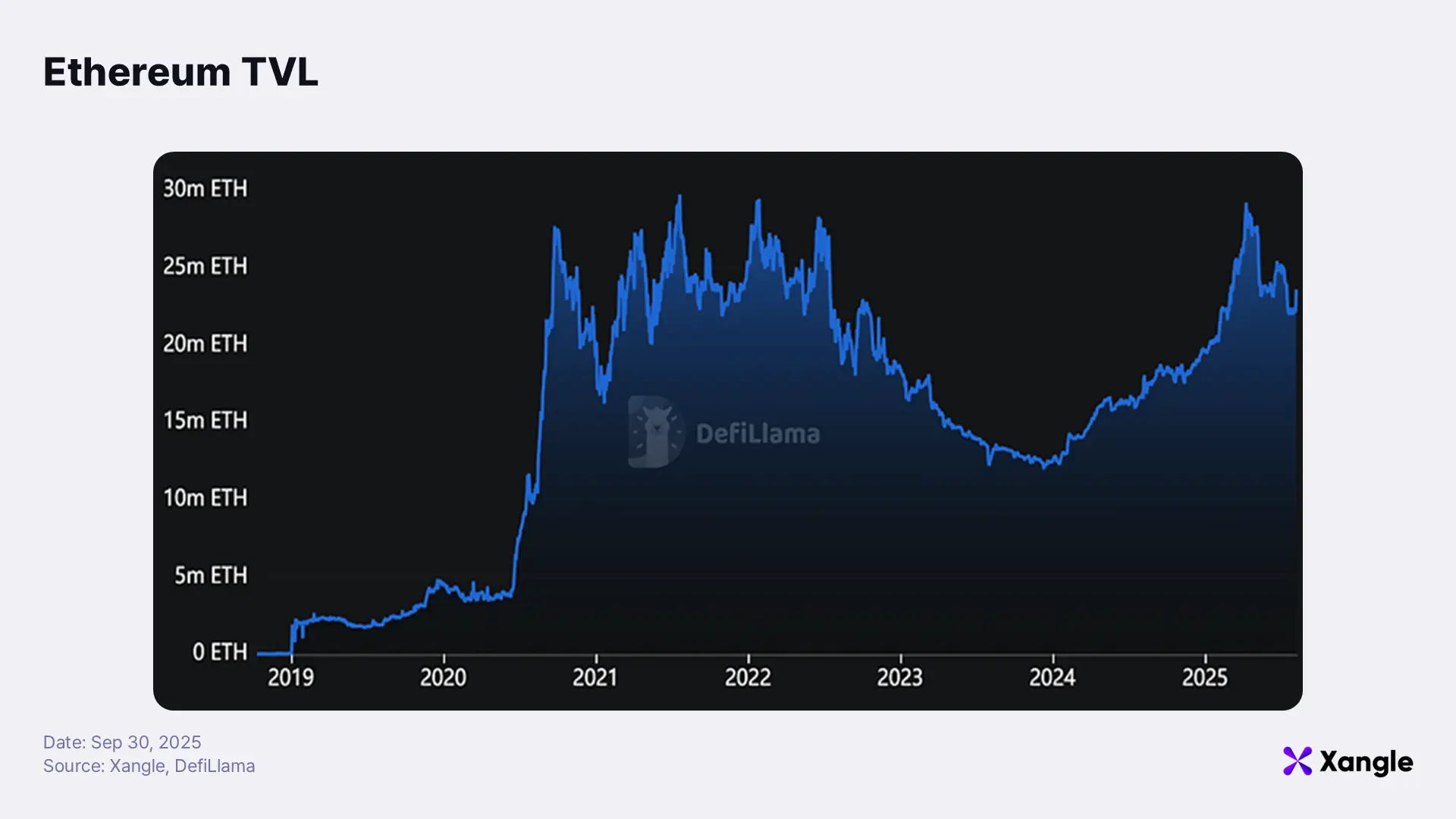

Ethereum’s total value locked (TVL) reached a new all-time high in 2025, surpassing all previous peaks since 2022. The surge reflects several structural shifts that have reshaped the network’s economic base.

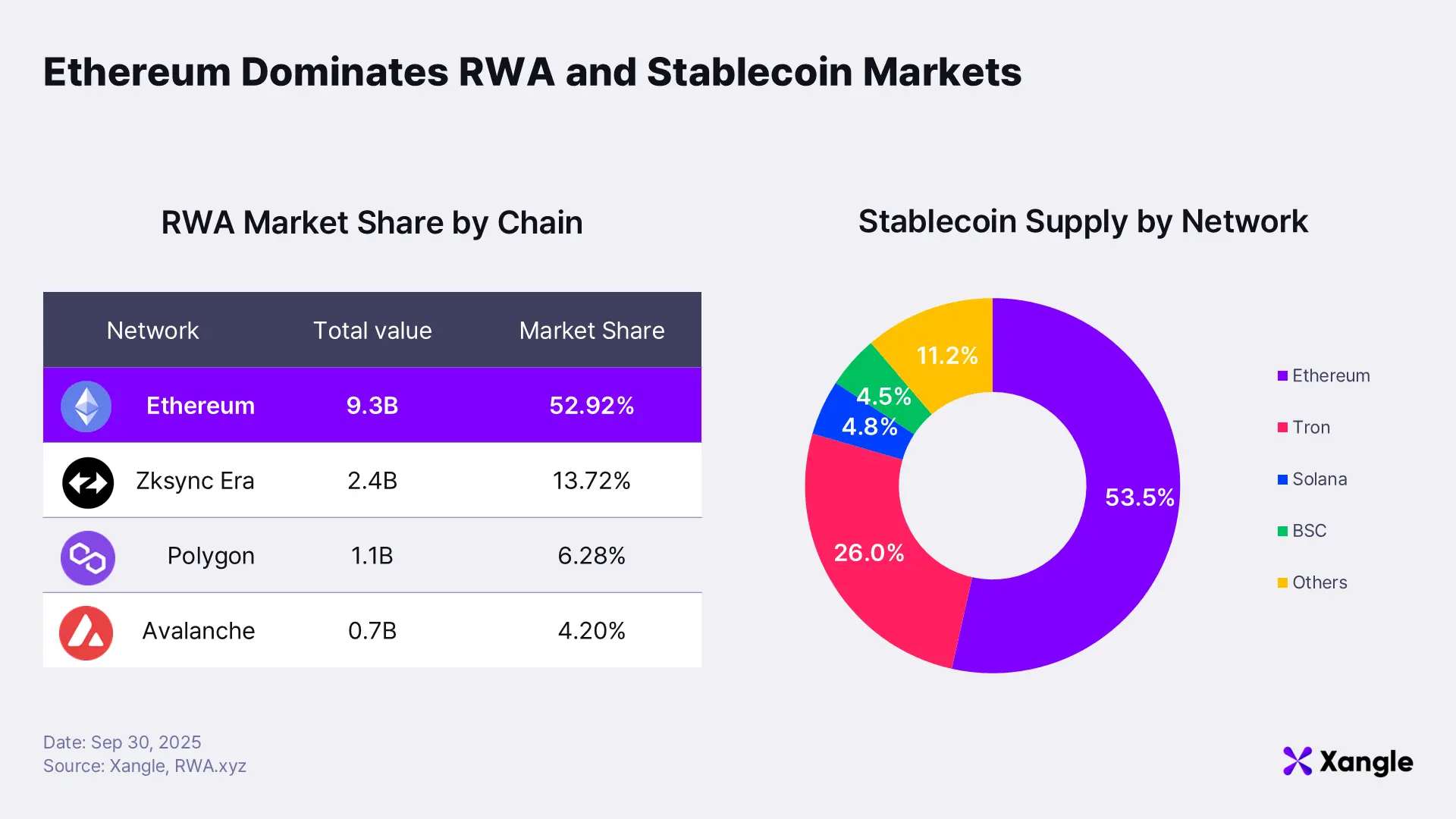

The first driver has been the explosive expansion of the stablecoin market, which injected massive liquidity into the Ethereum ecosystem. A second catalyst came from institutional capital entering through tokenized investment vehicles such as BlackRock’s BUDL Fund and Athena’s USDtb, both of which bridged traditional finance into on-chain markets and enhanced Ethereum’s credibility as a settlement layer. The third factor lies in the evolution of restaking protocols like EigenLayer and Ether.fi, which have enabled ETH holders to deploy their assets across multiple DeFi strategies, generating additional yield beyond simple staking. Together, these developments have propelled Ethereum to command roughly 70% of all blockchain TVL, underscoring its transition from a digital asset network to a core layer of global financial infrastructure.

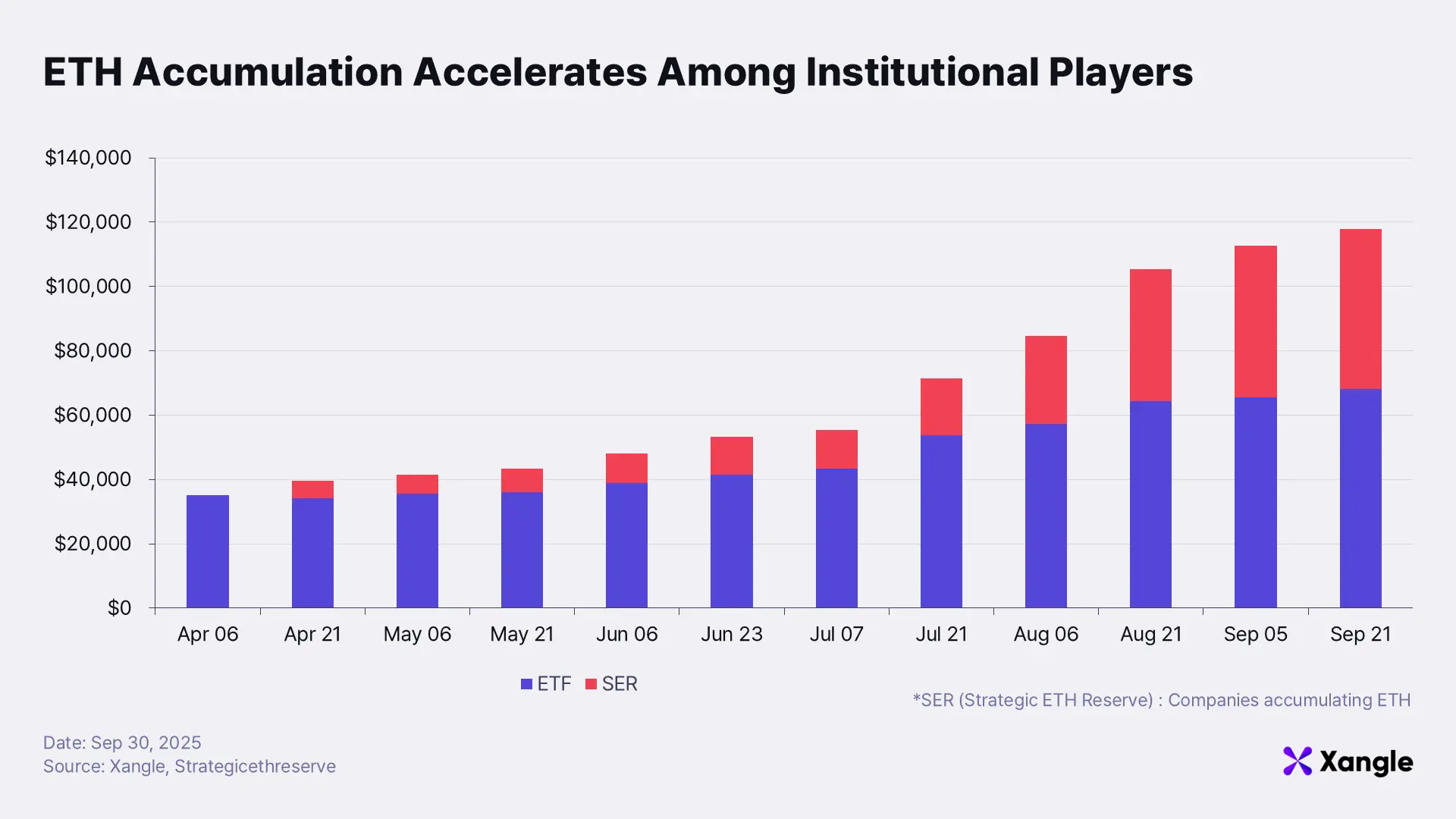

Alongside this liquidity expansion, a second major shift has emerged: the growing institutional ownership of Ethereum. With the rise of Ethereum ETFs and Digital Asset Trusts (DATs), institutions now hold close to 10% of circulating ETH. Until recently, however, this capital remained largely inactive within on-chain markets, constrained by the strict regulatory environment in the United States. As those constraints begin to loosen, institutional ETH reserves are starting to flow into the DeFi economy.

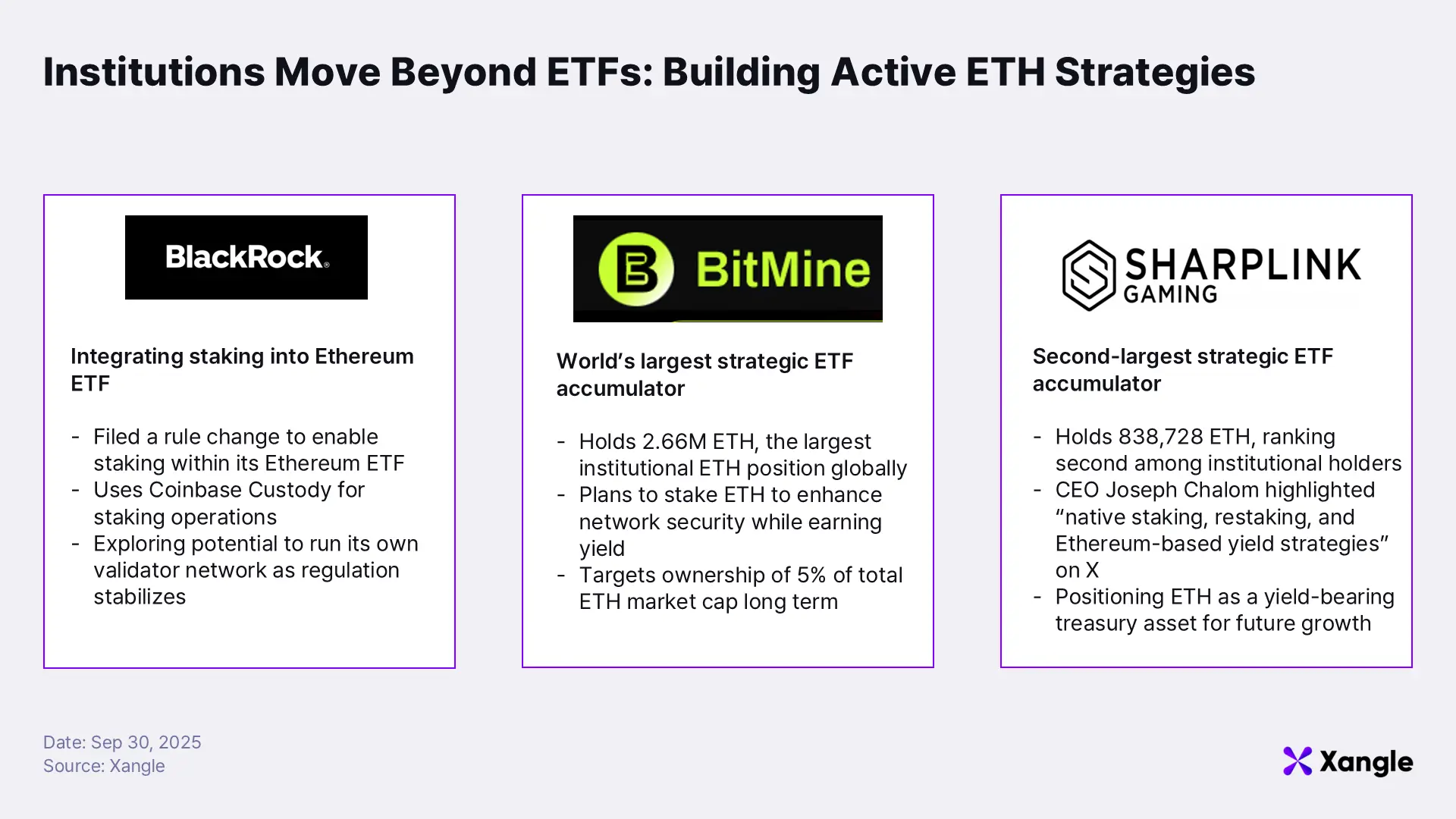

The most prominent mover has been BlackRock. On July 16, 2025, the asset management giant filed a rule-change proposal to add staking functionality to its Ethereum ETF—a sharp departure from earlier filings that excluded staking due to security-classification concerns. The move signaled both a growing confidence in the SEC’s new posture and a clear indication that legal clarity is paving the way for traditional finance to participate directly in crypto markets.

BlackRock’s iShares Ethereum Trust is sponsored by iShares Delaware Trust Sponsor LLC, a BlackRock subsidiary. Coinbase Custody Trust Company serves as the Ethereum custodian, while The Bank of New York Mellon acts as the cash custodian and administrator. By integrating Coinbase’s staking service, the ETF aligns with the SEC’s clarified definition of non-security staking—reinforcing compliance and setting a regulatory benchmark for institutional entrants.

Interestingly, the filing also included a clause stating that “the Sponsor may seek to utilize alternative means to engage in staking activities, subject to its determination that the Trust may do so without undue legal, regulatory or tax risk and consistent with the Corp Fin Statement.” The language implies that as regulatory risks continue to decline, BlackRock could directly participate as a validator or even operate its own validator network—a step that would mark a deeper level of institutional integration within Ethereum’s core infrastructure.

Other firms are now following suit. Sharplink Company, one of the largest Ethereum treasury managers, appointed Joseph Chalom, former Head of Ethereum Strategy at BlackRock, as its Co-CEO. Chalom announced plans to build revenue streams leveraging native staking, restaking, and Ethereum-based yield strategies. Meanwhile, Bitmine has begun developing models to capitalize on Ethereum’s staking-driven yield dynamics, viewing them as a structural advantage over Bitcoin’s passive treasury approach.

Such strategies are opening new financial playbooks for corporates. Beyond traditional bond issuance, companies can now enhance yield by staking Ethereum directly or amplify returns through liquid staking and leverage strategies. This represents a far more sophisticated revenue model than that of Bitcoin treasury firms. The broader impact extends well beyond corporate profitability: institutional liquidity entering Ethereum’s staking economy could become one of the most powerful growth catalysts for the ecosystem itself—fueling liquidity depth, product innovation, and network maturity.

The DeFi Liquidity Engine: How Staking Powers Ethereum’s Monetary Layer

The growing participation of institutions in staking raises a critical question: what does this mean for the Ethereum ecosystem? To understand its implications, it is necessary to first examine how liquidity is actually created within Ethereum’s DeFi environment.

Liquid staking and restaking protocols provide relatively low-risk, stable yields while enabling Ethereum to be deployed in more flexible, composable ways across DeFi. Their real importance, however, lies in their ability to generate liquidity through entirely new mechanisms. In traditional finance, liquidity is typically created through credit expansion—via bond issuance or central bank monetary policy. Ethereum, by contrast, produces liquidity organically, as staking and liquid staking expand the network’s circulating supply. As the Ethereum ecosystem grows, the on-chain economy effectively increases its own monetary base. In this sense, Ethereum functions as a self-sustaining liquidity engine, where money creation scales in tandem with network activity.

Staking thus represents a foundational mechanism for liquidity generation within Ethereum. Although staking yields fluctuate, they serve as the most efficient incentive model for maintaining network security and integrity. In effect, the staking rate operates as Ethereum’s on-chain base rate, comparable to the risk-free rate in traditional markets. Users who are not actively deploying their ETH can delegate it to validators, earning staking rewards in return. This arrangement locks ETH for a period, reinforcing network stability while providing validators with economic incentives to secure the chain.

At the same time, locked ETH is a double-edged sword. While it ensures network resilience, it also limits the amount of circulating liquidity available to the broader DeFi ecosystem—most of which depends on deep, fluid capital pools. As more ETH becomes staked, liquidity tightens, and the growth potential of DeFi protocols becomes constrained. To address this imbalance, a new generation of DeFi protocols has emerged to unlock staked assets and reintroduce them into circulation.

Protocols such as Lido, the dominant liquid staking provider, convert staked ETH into Liquid Staking Tokens (LSTs)that can move freely within the Ethereum network. These tokens function as standard ERC-20 assets—tradable on exchanges, usable as collateral on lending protocols like Aave, or deployable in yield-farming strategies. By allowing users to earn staking rewards without immobilizing capital, liquid staking removes the inefficiency of locked assets and dramatically expands liquidity across the broader crypto economy.

From a financial perspective, liquid staking operates much like asset-backed securities (ABS) in traditional markets: it brings future cash flows into the present, supplying immediate liquidity to participants. This mechanism also enables a range of advanced strategies. For instance, users can stake ETH, receive LSTs, use them as collateral to borrow additional ETH, and then restake that ETH to mint more LSTs—effectively engaging in leverage staking to maximize returns. In doing so, Ethereum’s liquid staking protocols simultaneously reinforce network security and accelerate the growth of DeFi by maintaining a constant flow of on-chain liquidity.

Building the Backstop: Institutional Capital as Ethereum’s Lender of Last Resort

Liquid staking, despite its structural advantages, is not without risk. As with asset-backed securities (ABS) in traditional finance, pulling future cash flows forward through liquidity creation always carries inherent danger—most notably, the risk of cascading liquidations. If the price of Ethereum, the underlying asset, drops sharply, the value of LSTs used as collateral declines alongside it. When users’ collateral ratios fall below required thresholds, lending protocols automatically trigger liquidations. To recover outstanding loans, the protocols sell the seized LSTs on the open market, generating intense selling pressure. This wave of forced selling pushes Ethereum’s price even lower, further eroding collateral values and setting off additional rounds of liquidation in a self-reinforcing spiral.

In such conditions, instability in Ethereum’s price can suddenly choke system-wide liquidity, even when no fundamental insolvency exists. The result is a structural vulnerability that can cascade into a full-scale ecosystem collapse. A clear example came in June 2022, when a major depegging event on Lido led to a sharp decline in Ethereum’s price. Excessive exposure to this kind of systemic fragility remains one of the key bottlenecks preventing DeFi from maturing into a stable, large-scale financial environment.

The equation changes, however, if a participant within the Ethereum ecosystem can assume a function similar to that of a central bank—acting as a lender of last resort to stabilize liquidity during stress events. The introduction of such institutional capital would mitigate risk while enabling the ecosystem to grow on a more sustainable footing.

The presence of a liquidity backstop would have implications far beyond crisis response. For example, during Lido’s past depegging event, a dedicated liquidity provider could have absorbed market shock and prevented the depeg altogether. Because staked Ethereum holds intrinsic value, sufficient liquidity provision would have eliminated the need for panic selling. By supplying liquidity during short-term price dislocations, such institutions could serve as buffers against systemic collapse.

If a financial institution were to establish itself as a stable source of liquidity and a safeguard during market stress, it would substantially reduce the fundamental risks that constrain Ethereum’s DeFi ecosystem. Anchored by this systemic stability, the ecosystem could scale far more rapidly—supporting complex financial products, attracting deeper pools of capital, and driving DeFi’s evolution into a more sophisticated and trusted financial system.

The New Monetary Order: Ethereum’s Rise as the Global Settlement Layer

The SEC’s recent regulatory realignment represents far more than a green light for staking. By resolving Ethereum’s long-standing obstacle for institutions—its security classification—the agency has cleared the path for traditional finance to engage directly with the structural efficiencies of DeFi.

At the center of this shift lies institutional access to liquidity generated across Ethereum’s interlinked layers of lending, liquid staking, and staking activity. The flow of capital within this feedback loop enables the creation of financial instruments analogous to those of traditional markets. Until now, however, institutions could not meaningfully develop such products because of the unsolved issue of liquidation risk during sharp Ethereum price declines. History has shown how this vulnerability repeatedly triggered severe downturns across the crypto market.

The landscape changes entirely if institutions begin to act as an insurance layer—providing capital to absorb those risks and stabilize DeFi’s liquidity structure. With institutional liquidity expanding across the Ethereum economy, the network would evolve beyond a capital-accumulation layer into a self-sustaining, growth-generating financial infrastructure. Ethereum would no longer be just an asset; it would function as the foundation of a global, programmable financial system capable of supporting the next wave of decentralized innovation.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Solana RWA: A Look at the Key Players](https://resource.xangle.io/files/content/F779A005246C0299246537AACB3A39F2_1782287059970.webp)