The Tokenomics Chronicle

TLDR;

-

-

Three Generations of Tokenomics:

- Gen 1 (ICOs): Early projects like Ethereum used ICOs to raise capital, but this model faced issues like fraud and regulatory crackdowns.

- Gen 2 (Airdrops): Airdrops like Uniswap's $UNI helped projects gain users but struggled with long-term retention as many sold tokens immediately.

- Gen 3 (Grant-Based Models): Projects like Arbitrum have moved to grant-based models to fund long-term ecosystem growth, using structured funding tied to milestones

- Utility-centric Tokenomics:

- Future tokenomics will have to prioritize governance, and indirect profit-sharing models (like Binance's $BNB), ensuring sustainable demand and help projects maintain user engagement in the long term. The legal landscape around profit-sharing remains a challenge, particularly regarding SEC scrutiny.

-

1. The Web3 Token Economy

Tokenomics is a compound word combining “token” and “economics,” - referring to the economic system in Web3 projects where tokens serve as a medium of exchange within an ecosystem. Projects primarily design their tokenomics to acquire users, build ecosystems, and ensure long-term sustainability as a protocol. In doing so, they consider not only the method of issuance, initial allocation, and long-term utility but also legal regulations and market conditions when establishing a tokenomics strategy.

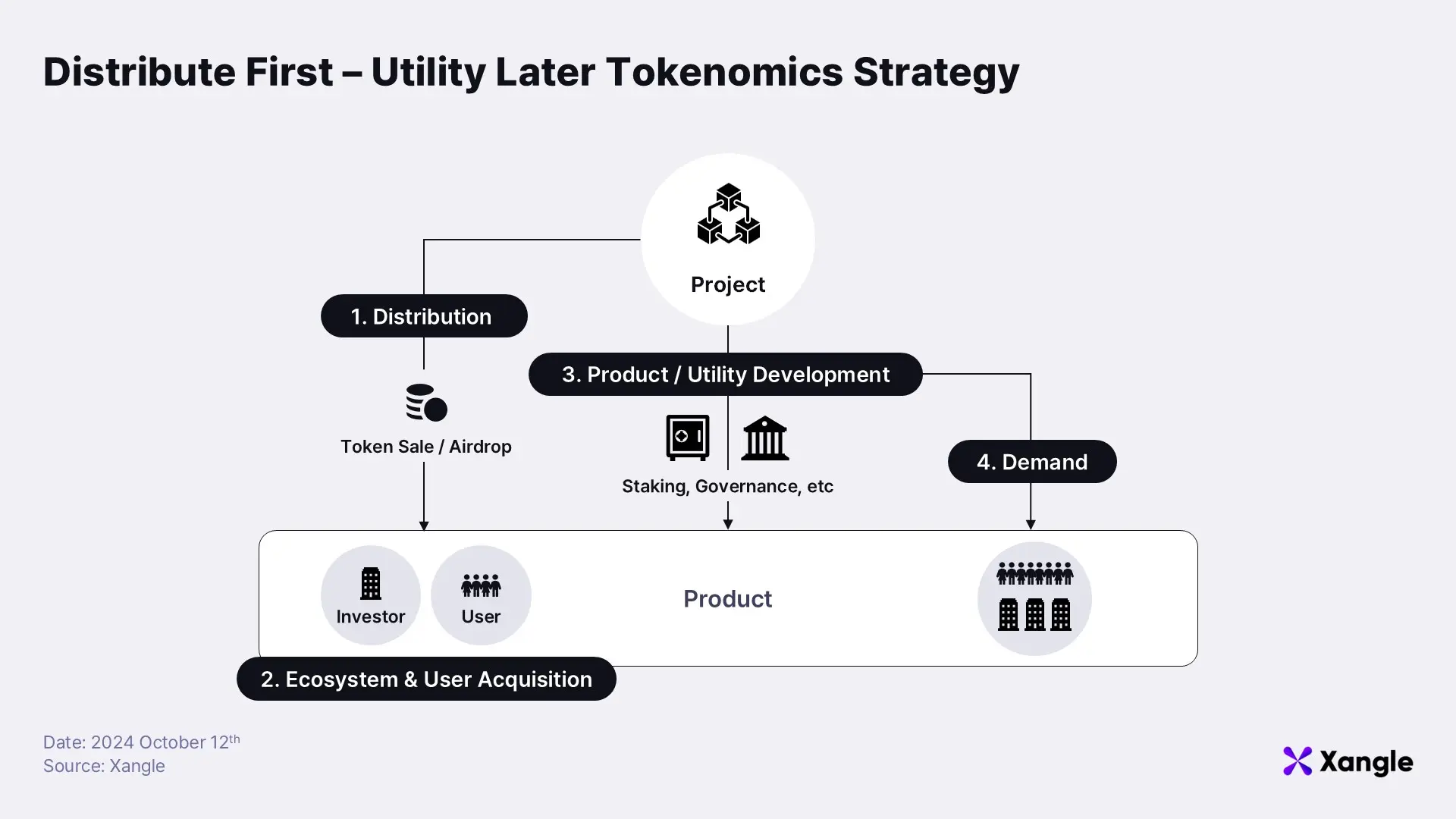

Two-Step Tokenomics Strategy: Distribution & Utility

Among the most common and broad tokenomics strategies, one often sees the following structure: 1) expanding the ecosystem and acquiring users through token distribution methods, such as token sales or airdrops, and then 2) assigning proper utilities to the token, such as staking or governance, alongside product improvements. The core of a tokenomics strategy can thus be summarized as creating a sustainable ecosystem by balancing supply through token distribution and generating a long-term demand through utility.

While the overall framework hasn’t changed much since the introduction of Bitcoin and Ethereum, up to more recent token projects like Scroll ($SCR), there have been differences made in the specifics of distribution method, the timing of TGE, and token utility. This article explores different generations in tokenomics, mainly focusing on the execution method used to distribute tokens.

2. Tokenomics Across Generations

The earliest form of tokenomics appeared with Bitcoin: a system with a total supply cap, difficulty adjustments, and halving cycles to limit the total issuance to 21 million tokens. In July 2014, Ethereum launched and, while Bitcoin’s tokenomics were limited to rewarding miners for securing the network through transaction fees, Ethereum opened up new horizons by providing an infrastructure for generalized contract execution through its Ethereum Virtual Machine. This allowed dApps to customize their own tokenomics, with each application capable of adjusting its own economic model.

2-1. 1st Generation Tokenomics (~2019): ICO (Initial Coin Offering)

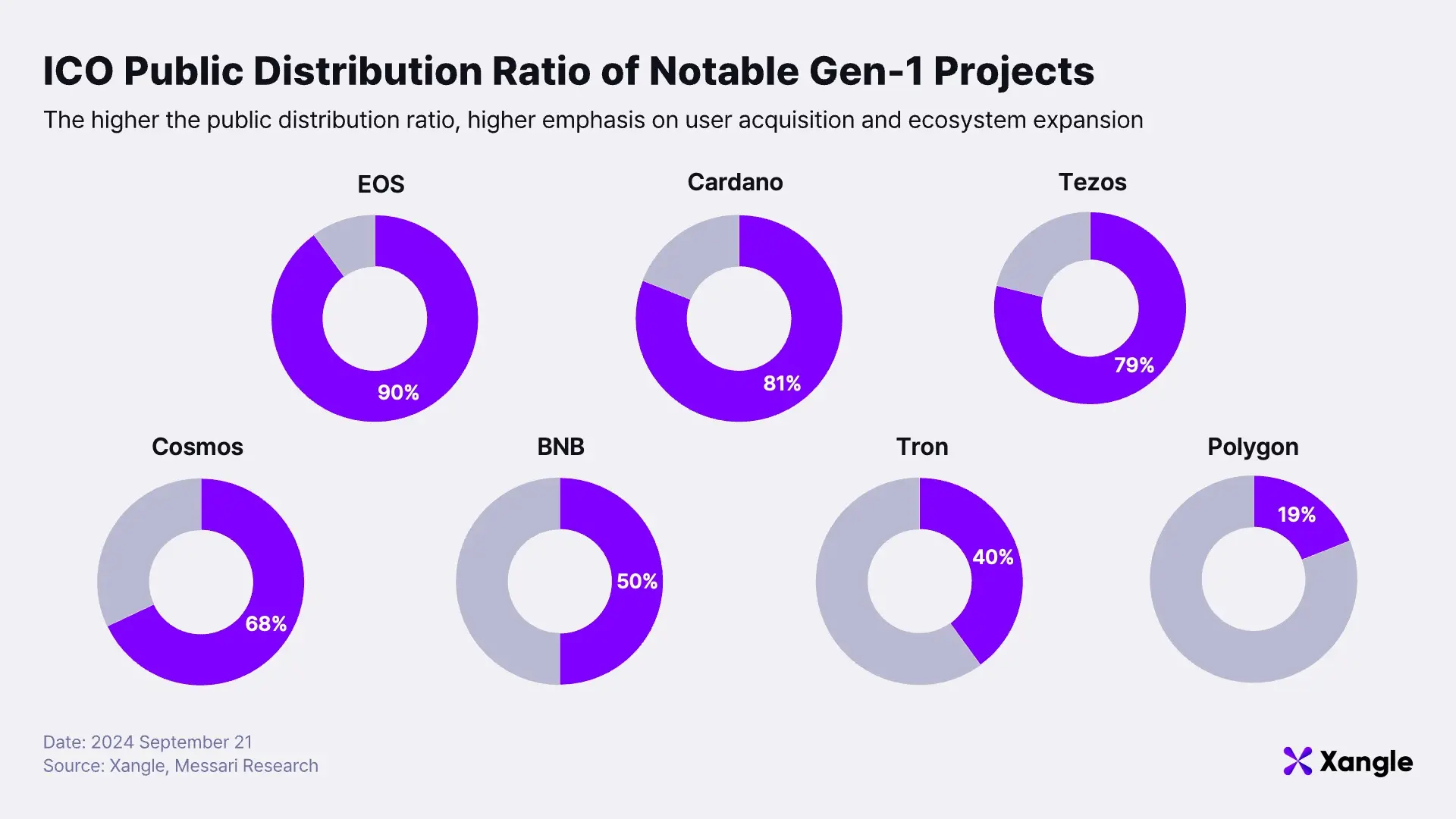

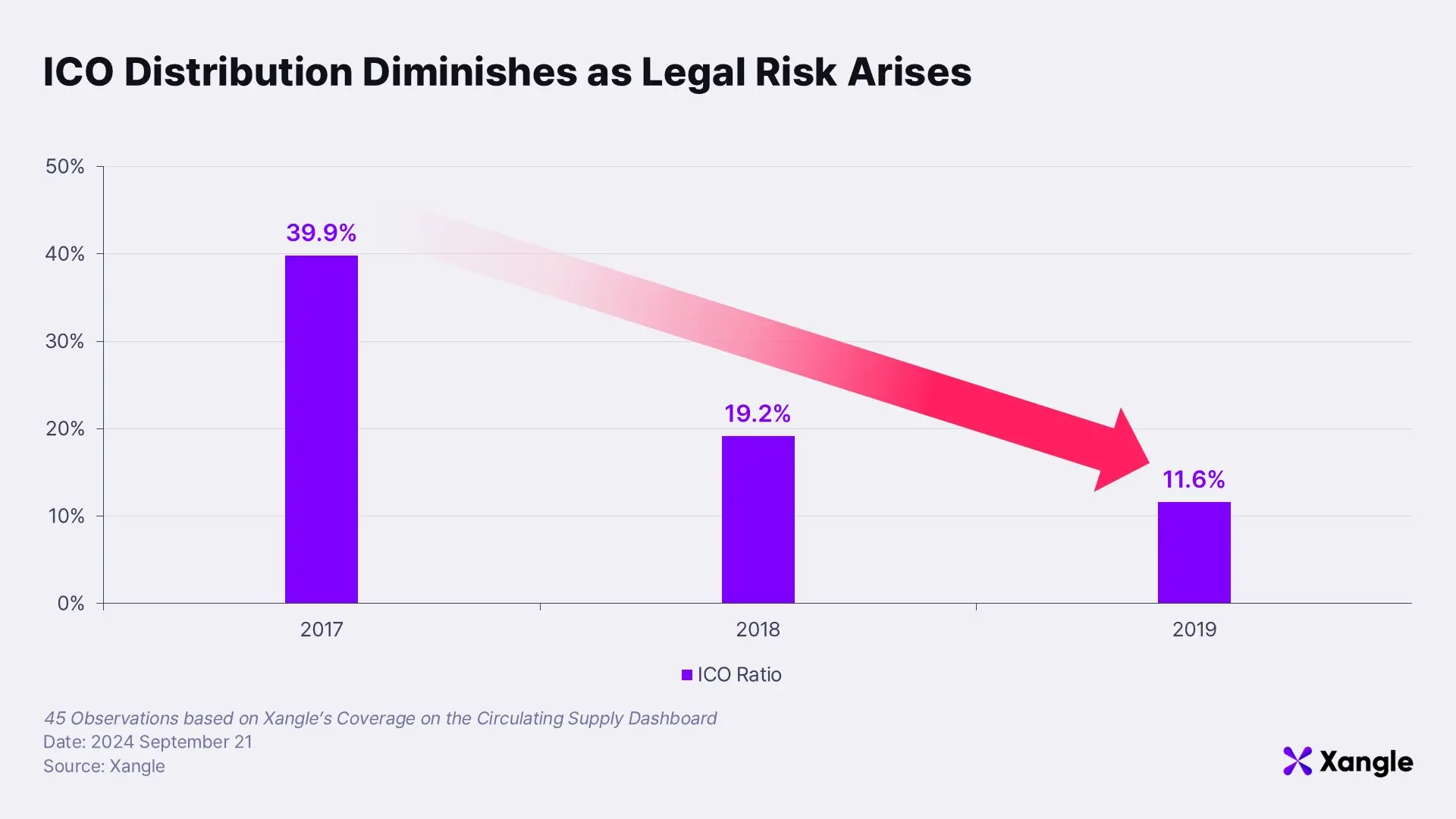

Ethereum spearheaded the first generation of token distribution strategies with its ICO (Initial Coin Offering) model. ICOs typically involved publishing a project’s vision in a whitepaper, raising funds by collecting Bitcoin or other native assets in a specific blockchain wallet, and selling most of the token supply via smart contracts. For example, in the case of Ethereum, 80% of the tokens were distributed through public sale. Similarly, Cardano (2017) and EOS (2018) also followed this model, selling 80% and 90% of their tokens, respectively, on the open market.

The ICO model, by opening up investment opportunities to anyone globally, allowed projects to secure a broad user base early on, which they could then leverage to build out their ecosystem. However, most projects struggled to create meaningful demand for their tokens due to a lack of essential dApps or useful token utilities, with tokens like Ethereum and Binance Coin (BNB) being notable exceptions. As a result, many tokens became nothing more than speculative investment tools.

Furthermore, the ease of participating in ICOs also carried legal risks. Because ICOs allowed anyone from anywhere in the world to invest without proper screening, they became breeding grounds for cross-border fraud. Eventually, regulators like the SEC and Korea’s Financial Services Commission moved to ban ICOs.

*According to a Bloomberg report, 80% of ICOs conducted by June 2018 ultimately ended up as financial fraud.

**In 2017, the SEC (July) and Korea’s Financial Services Commission (September) banned all forms of ICOs that raise funds through digital tokens.

2-2. 2nd Gen Tokenomics (2020–2022): Airdrops

With the widespread ban of ICOs, the proportion of tokens distributed through public sales drastically diminished, reducing the amount of tokens available to retail investors. Despite this drop, the Layer 1 infrastructure that was initially bootstrapped through ICOs had matured. In addition, as the DeFi summer on Ethereum began with the launch of Compound, the number of dApps rapidly increased.

As the market grew, projects increasingly needed to secure users and retain them in their ecosystems. With ICOs no longer a viable token distribution method, another approach was needed—this is where airdrops came into play. Airdrops, where tokens were directly distributed to users based on their activity, emerged as a new solution.

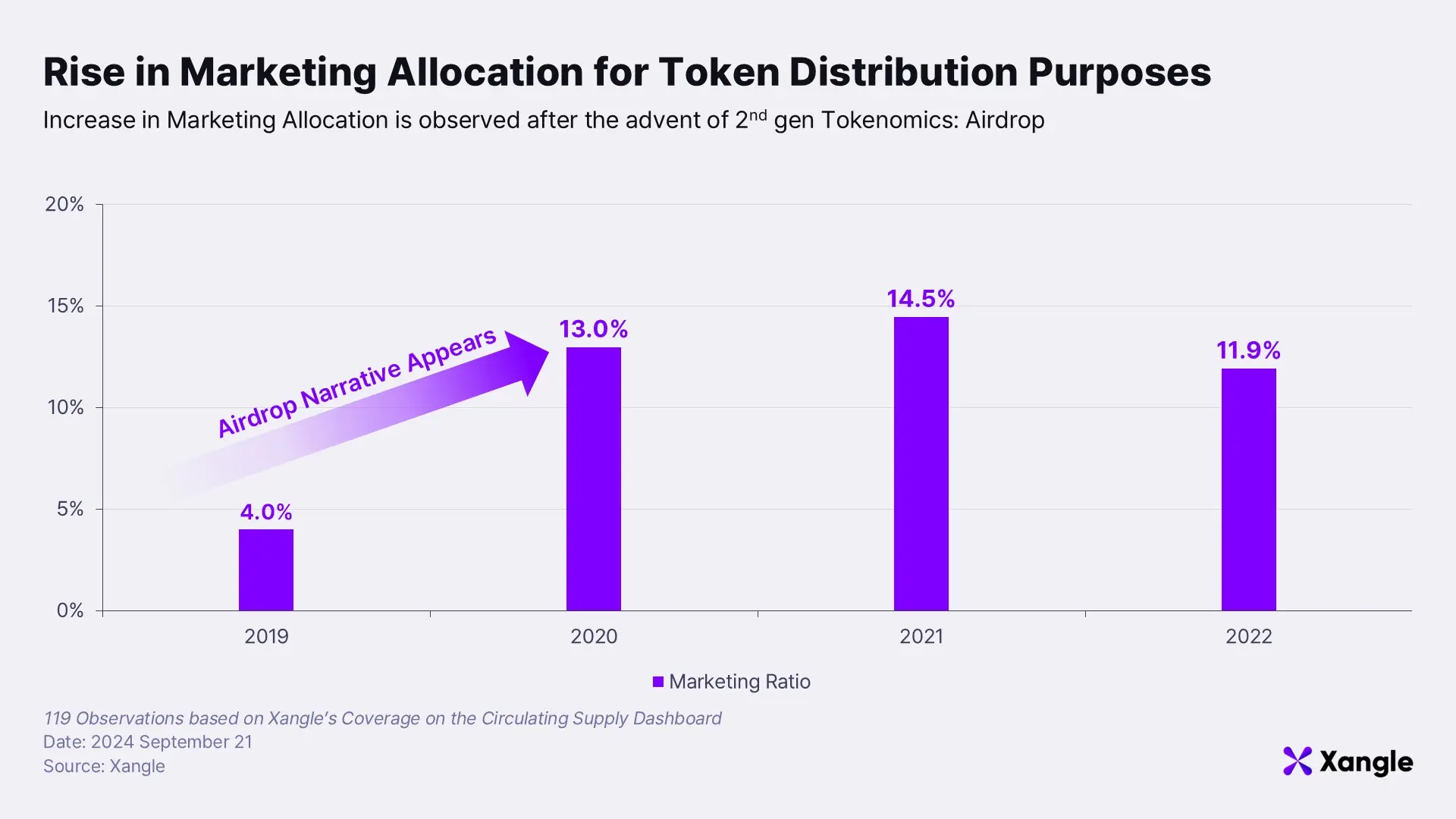

During this time, decentralized finance (DeFi) projects grew rapidly, introducing new models for token distribution and utility. For instance, liquidity mining—a reward mechanism where users are given tokens for providing liquidity—was introduced to attract users, offering utilities such as liquidity provision and staking for user lock-in. Therefore projects in the second generation shows higher marketing allocation through aggressive use of airdrops while also trying to provide utility to maximize user retention.

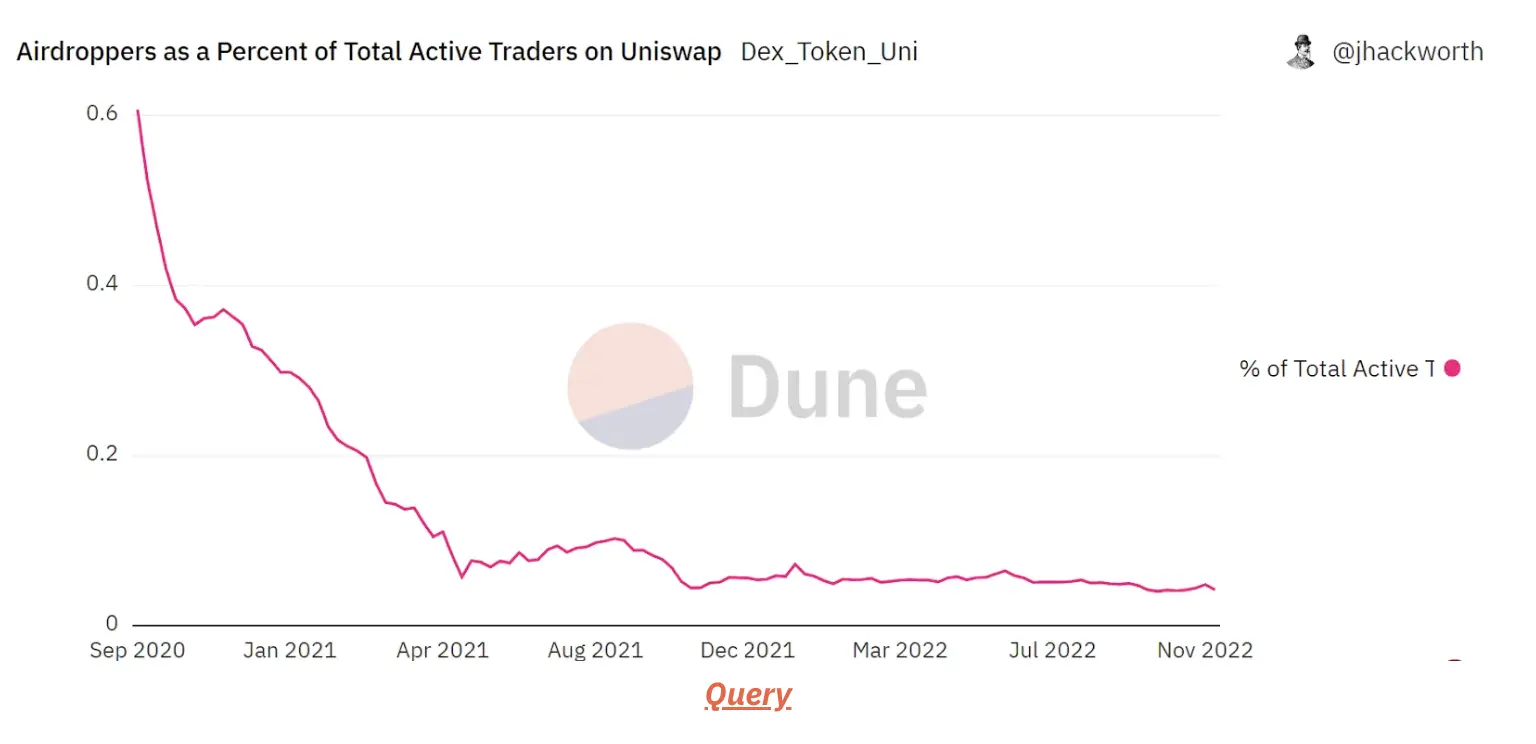

However, as mentioned in the previous report Airdrops and Cobra Effect, many users who received airdropped tokens simply sold them for profit and left. According to research on The Uniswap Airdrop, while 60,000 users received the tokens, this figure dropped to 10,000 a year later and less than 4,000 after two years, highlighting the limited retention effects of airdrops.

As mentioned in the Web3 Airdrop Playbook, airdrops faced additional challenges. These included the risk of Sybil attacks (where users create multiple wallets to claim airdrops repeatedly), market shifts following airdrops, higher-than-expected customer acquisition costs (CAC), and the difficulty of responding to airdrops from competitors.

2-3. 3rd Generation Tokenomics (2023~): Grants

The third generation of tokenomics still uses airdrops but with distinct changes in distribution methods. In this era, tokens are distributed based on specific user activities and dApp transactions defined by the project, and tokens are rewarded upon completion of those activities.

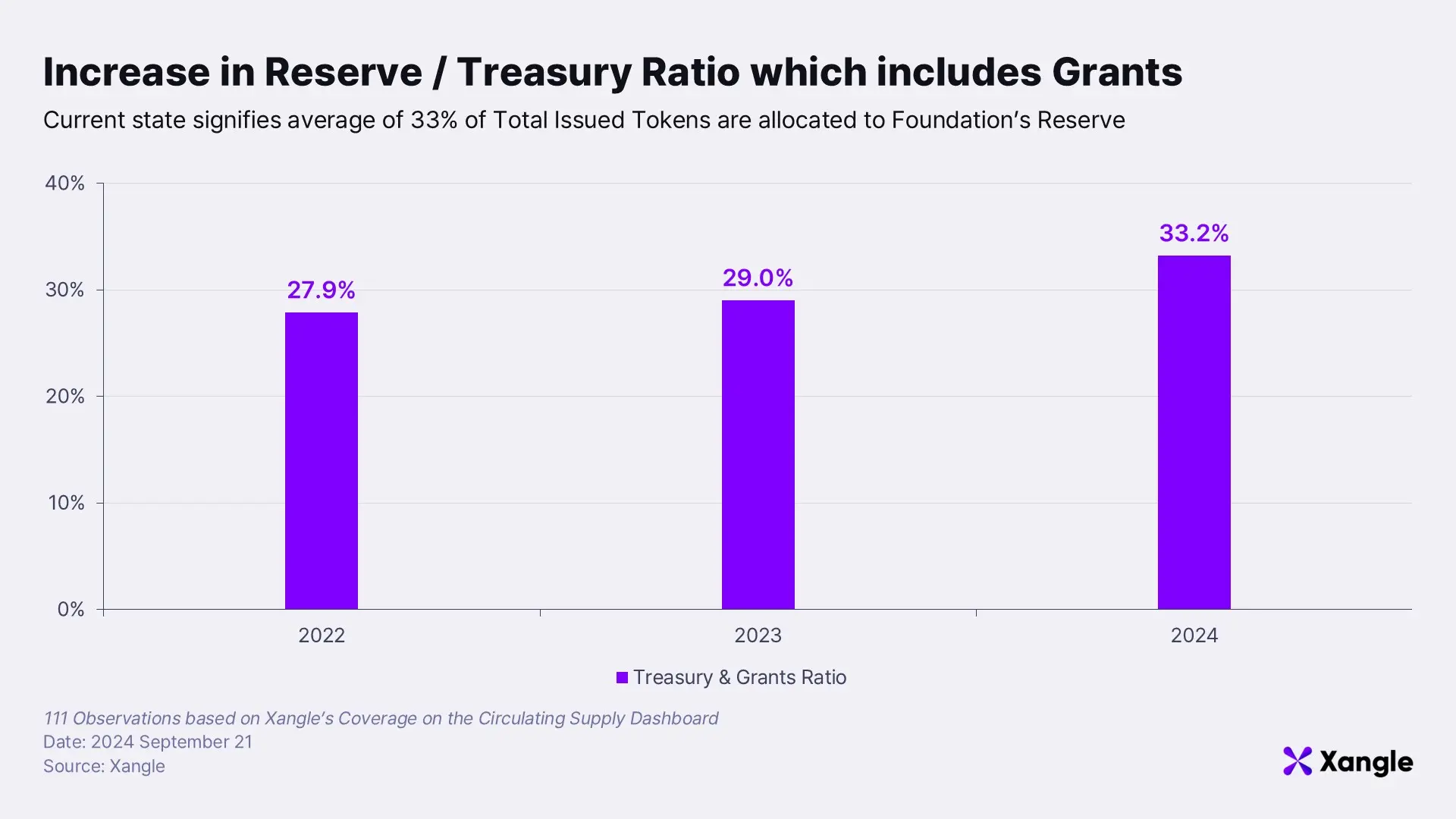

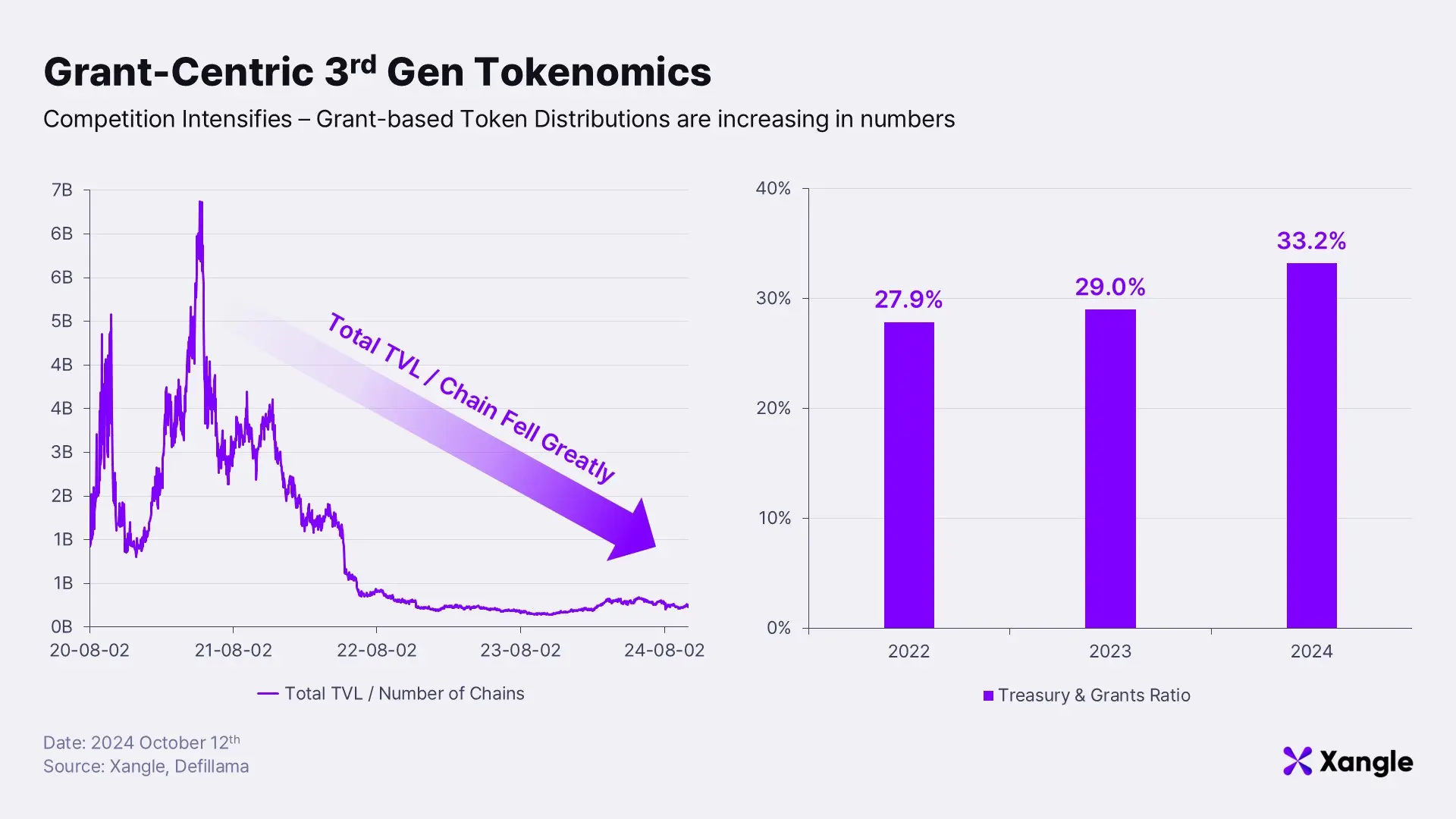

A noticeable change in this generation is the shift in allocation ratios. A larger portion of tokens is now allocated to the foundation’s reserves to manage potential variables after the airdrop phase. Additionally, grants are frequently used to secure partners, focusing on distributing tokens to help expand the ecosystem.

Changes in Tokenomics: Survival Instinct

These shifts can be seen as survival strategies in an increasingly fragmented market. Projects continue to use airdrops to attract users, but it’s become harder to find users who remain loyal to a single project, as seen in the Uniswap example. This problem has worsened with the rise of "airdrop hunters" who only target projects before their launch. As the inefficiencies of airdrops have become more apparent, newer projects have adopted strategies to expand their ecosystems by offering grants from their reserves to trusted individuals and partners, rather than indiscriminately distributing tokens to a large, undefined user base.

In summary, airdrops may be suitable for bootstrapping users in the early stages of a project, but other methods must be employed for long-term partnerships and ecosystem expansion. Currently, most projects are supplementing airdrops with grant programs that actually contribute greatly to the ecosystem.

3. Case Studies Across Generations

We have now examined the characteristics of tokenomics across three generations: (1) ICOs, (2) Airdrops, and lastly (3) Grants. In this section, we will look at examples of both successful and unsuccessful projects from each era along with a qualitative analysis.

3-1. ICOs

The token distribution model primarily used in the first generation, ICOs, maintained the decentralization of crypto and allowed projects to introduce themselves, receive investments, and offer investment opportunities to anyone around the globe. However, the absence of legal regulation placed ICOs in a gray area - allowing Ponzi schemes and fraudulent projects to proliferate, leading retail investors to invest in scams and result in financial losses.

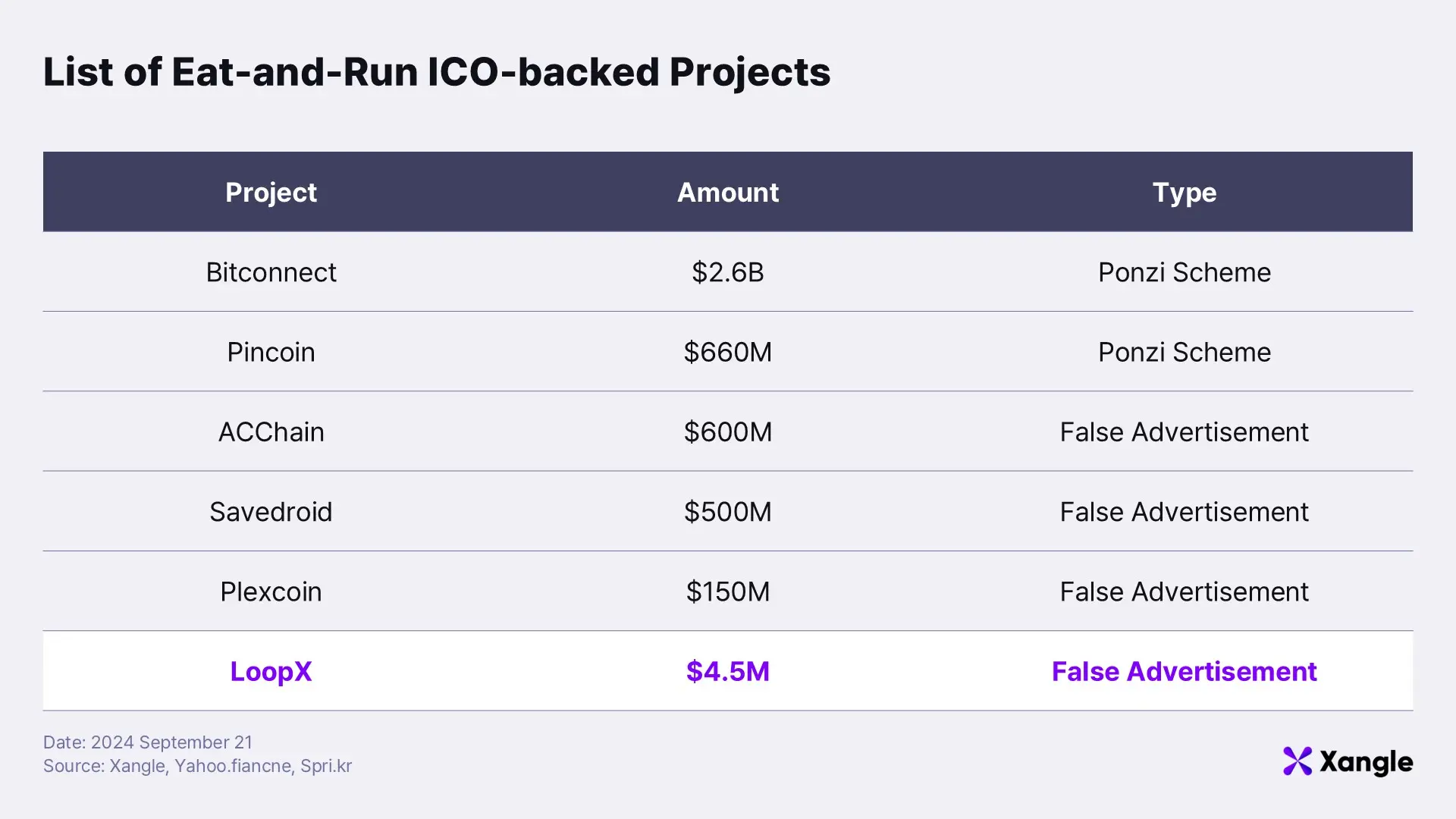

3-1-1. ICO Case Study: LoopX

LoopX was one such ICO project, raising $4.5 million in February 2018 before disappearing without a trace. As there were no regulatory frameworks in place to protect retail investors from frequent ICO frauds back then, the decentralization and anonymity that were core values of crypto ironically fostered a breeding ground for crime.

*The project lured investors by falsely claiming through its whitepaper and website that it would build a P2P trading platform using a proprietary algorithm, which would generate returns shared with members, guaranteeing 10% weekly profits. The website and social media accounts were shut down suddenly, and the project vanished with the funds.

3-1-2. ICO Case Study: Ethereum

However, not all projects funded through ICOs failed. A prime example of success is Ethereum, which raised $18.4 million through its ICO in July 2014 and has remained a dominant force in the blockchain space to this day. Ethereum launched its mainnet in July 2015, becoming one of the most successful Layer 1 blockchains.

Ethereum's success can be attributed to its fair token distribution, with 80% of the ICO funds allocated to public. On top of that, strong project development with key updates like EIP-1559 in August 2021 and the Merge in September 2022 constantly added new utility features at the protocol level.

*EIP-1599 introduced a token burn mechanism to increase long-term sustainability, and the Merge transitioned Ethereum to a Proof of Stake model, adding staking as a core new utility at the protocol level.

3-2. Airdrops

The second generation marked the beginning of crypto adoption, shifting from simple network-tokenomics model to an actual product-tokenomics and users. Airdrop-based token distribution in this era showed clear differences in outcomes depending on the utility of the token and the product offering. While some projects successfully captured demand with unique token utilities, others saw only one-off performances. Let’s examine two cases to understand the synergy between product and tokenomics strategies.

3-2-1. Airdrop Case Study: SushiSwap

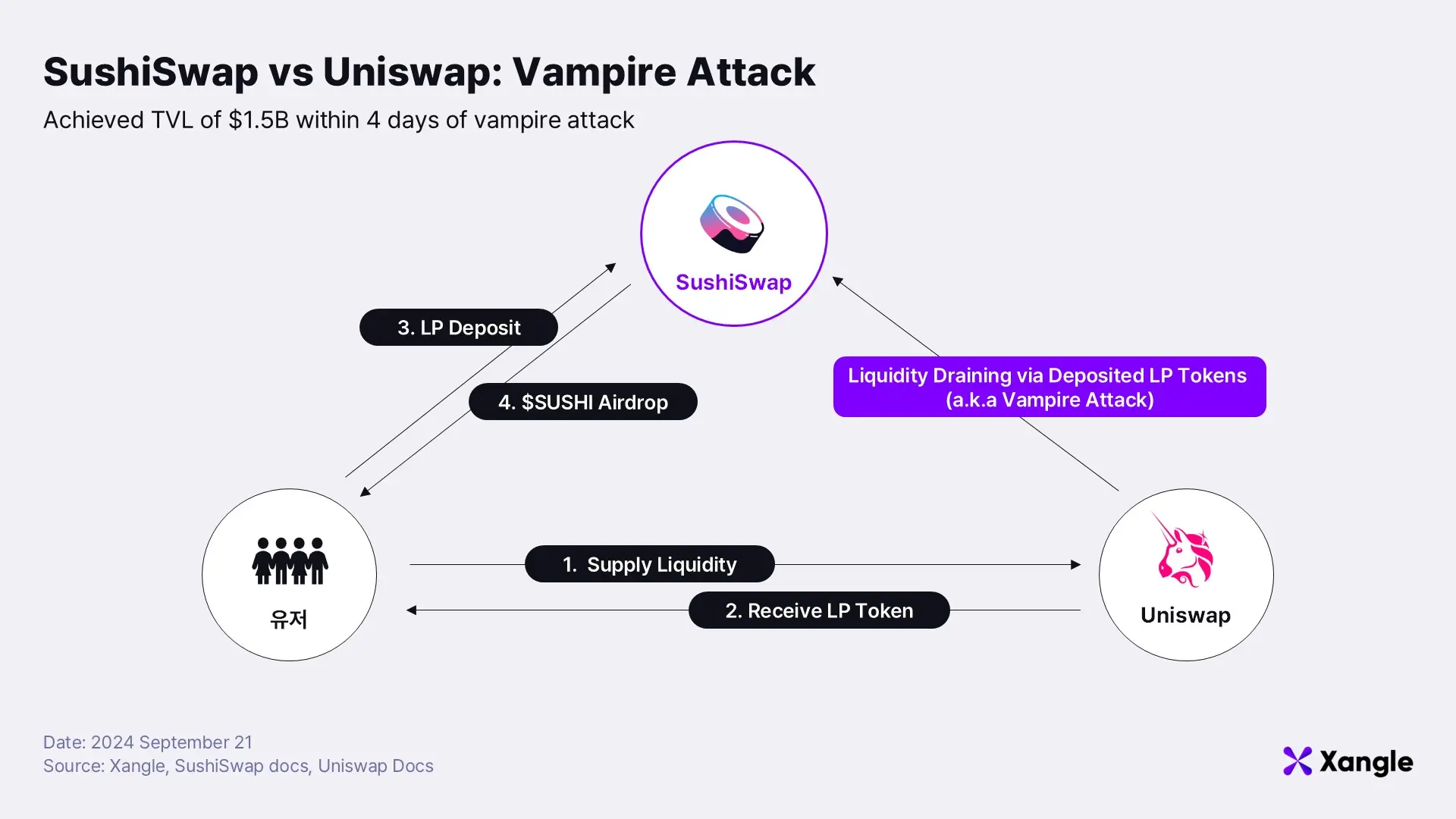

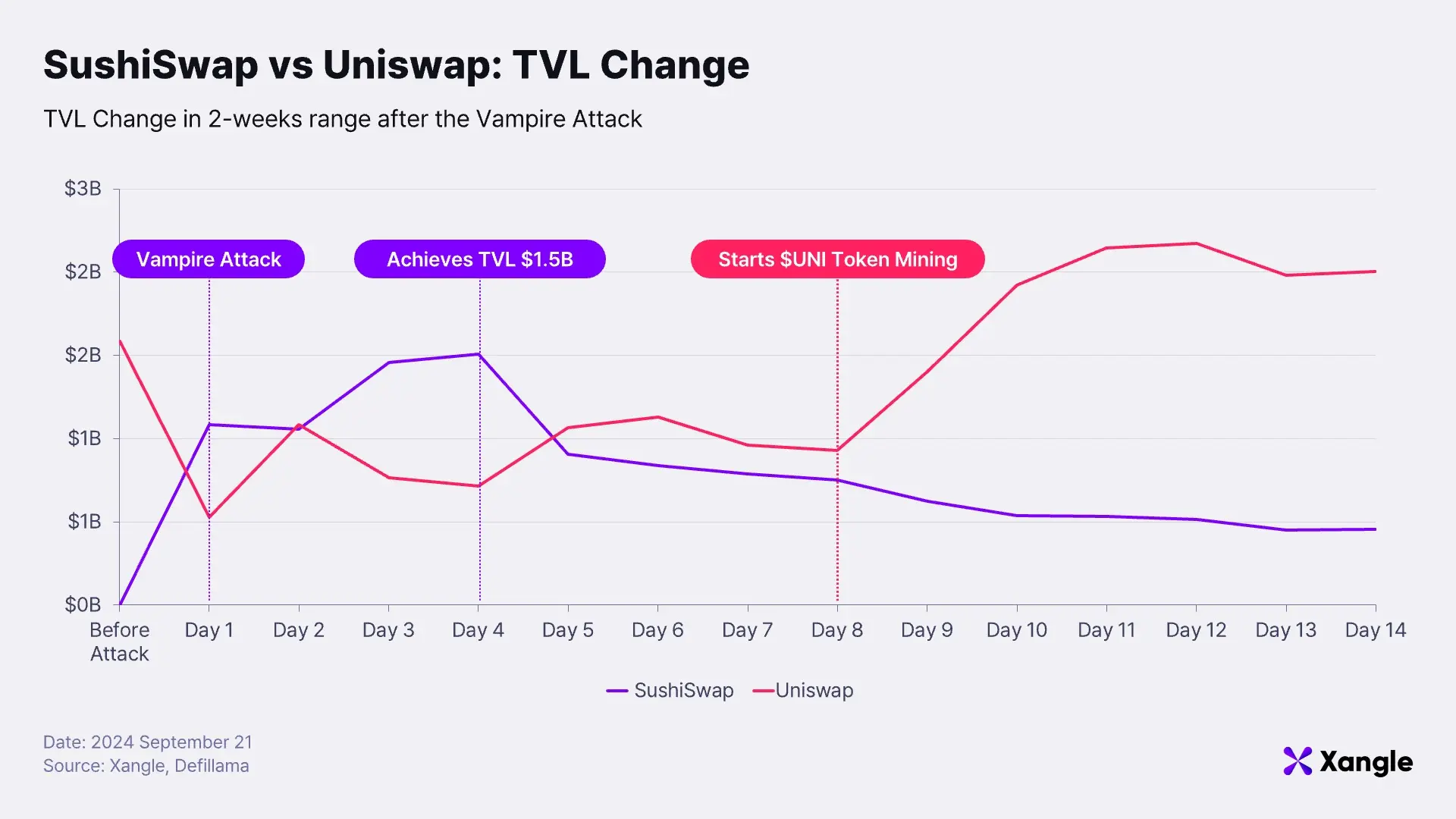

SushiSwap, one of the leading decentralized exchanges (DEXs) during the DeFi summer, began as a fork of Uniswap V2 but used airdrops as an incentive to siphon liquidity from its competitor in what’s referred as “vampire attack.” Uniswap dominated the market in terms of TVL and trading volume but did not yet have its own token. SushiSwap seized this opportunity by offering $SUSHI tokens to Uniswap's liquidity providers (LPs) in exchange for shifting their liquidity to SushiSwap.

Specifically, users were rewarded with $SUSHI tokens for staking Uniswap LP tokens in SushiSwap, allowing SushiSwap to capture control of Uniswap’s liquidity pools. Within four days, SushiSwap’s TVL skyrocketed to $1.5 billion. SushiSwap further differentiated itself by offering 0.25% of swap fees to liquidity providers and distributing 0.05% to $SUSHI stakers, giving the token meaningful utility.

Uniswap’s comeback & Lacking Product

While the vampire attack was a sharp strategy exploiting Uniswap’s lack of tokenomics, Uniswap responded just eight days later with a liquidity mining program that airdropped $UNI tokens to users, successfully reclaiming much of its liquidity. SushiSwap’s TVL subsequently fell by 83%, dropping to $250 million.

Another issue was that beyond its tokenomics strategy, SushiSwap lacked other competitive advantages, including technical innovation compared to other DEXs. Although its unique tokenomics led to strong initial performance, the effects were short-lived.

3-2-2. Airdrop Case Study: Curve Finance

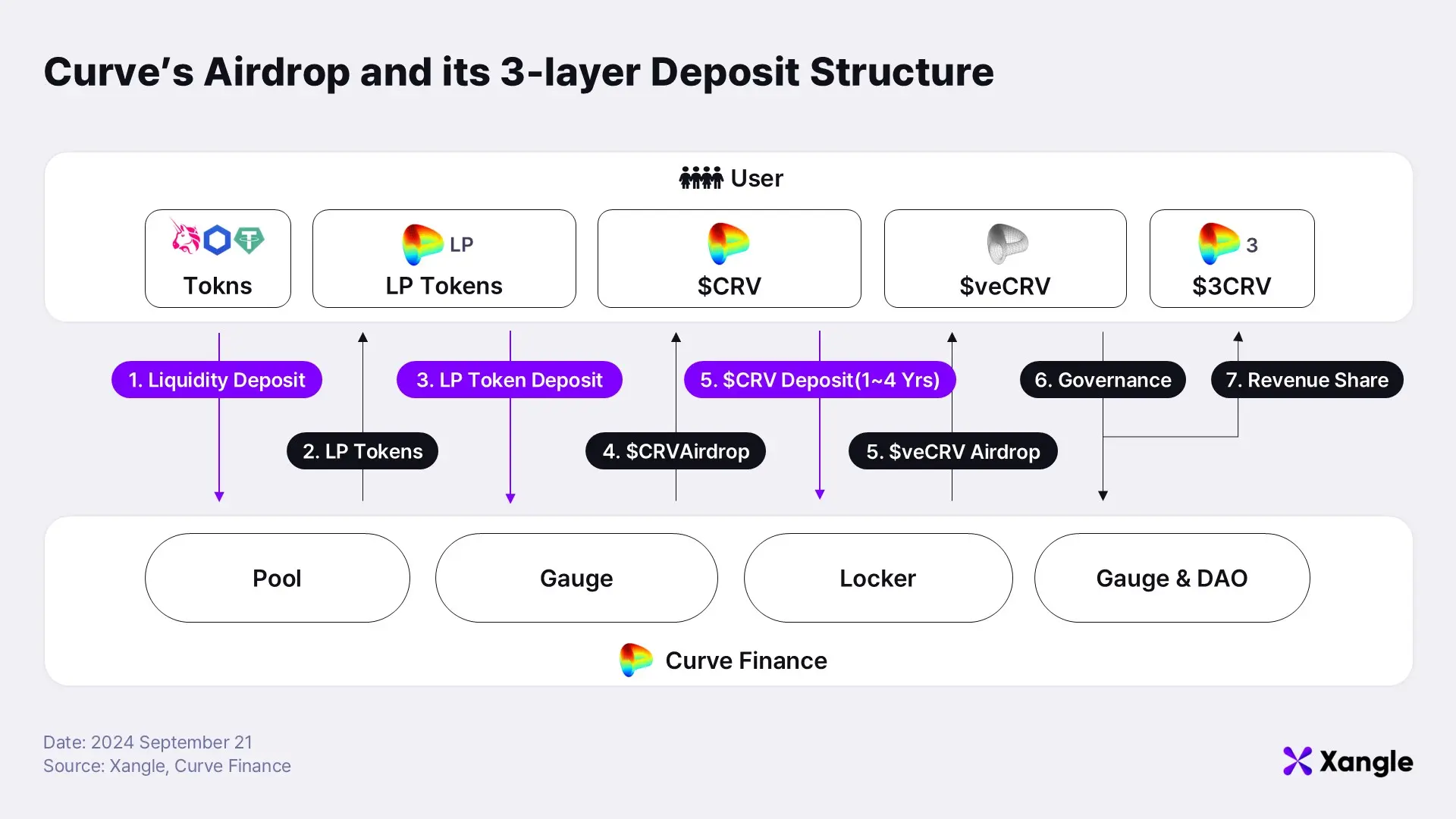

A successful case from this era is Curve Finance (CRV), a stablecoin-optimized DEX with their unique stableSwap curve. Curve implemented a three-tier staking model that incentivized liquidity providers to lock in their tokens for extended periods, offering higher rewards for longer commitment periods, with staking periods lasting up to four years.

This strategy successfully locked in long-term liquidity, positioning Curve as the DEX with the second-largest TVL as of September 21, 2024. The project’s continuous efforts to improve its product are also notable. Curve introduced the StableSwap model to mitigate slippage in stablecoin trades and later released an upgraded StableSwap V2 with dynamic peg ratio, demonstrating its long-term sustainability.

*Curve’s three-tier liquidity staking system operates as follows:

1. Liquidity providers receive LP tokens and a share of fees from the liquidity pool.

2. When LP tokens are staked, liquidity providers earn more $CRV proportional to the staking period, with the option to stake for up to 4 years for 2.5x the amount of $CRV.

3. Staking $CRV tokens earns $veCRV (Vote Escrow CRV) in a 1:1 ratio, with staking periods of up to 4 years. $veCRV holders receive protocol-wide fee shares and governance participation rights.

3-3. Grants

The third generation of tokenomics introduced grant-centric strategies as projects faced increasing competition and market fragmentation. By focusing on long-term partnerships and ecosystem expansion, projects aimed to support valuable contributions and promote ecosystem growth through grants.

3-3-1. Grant Case Study: Finschia

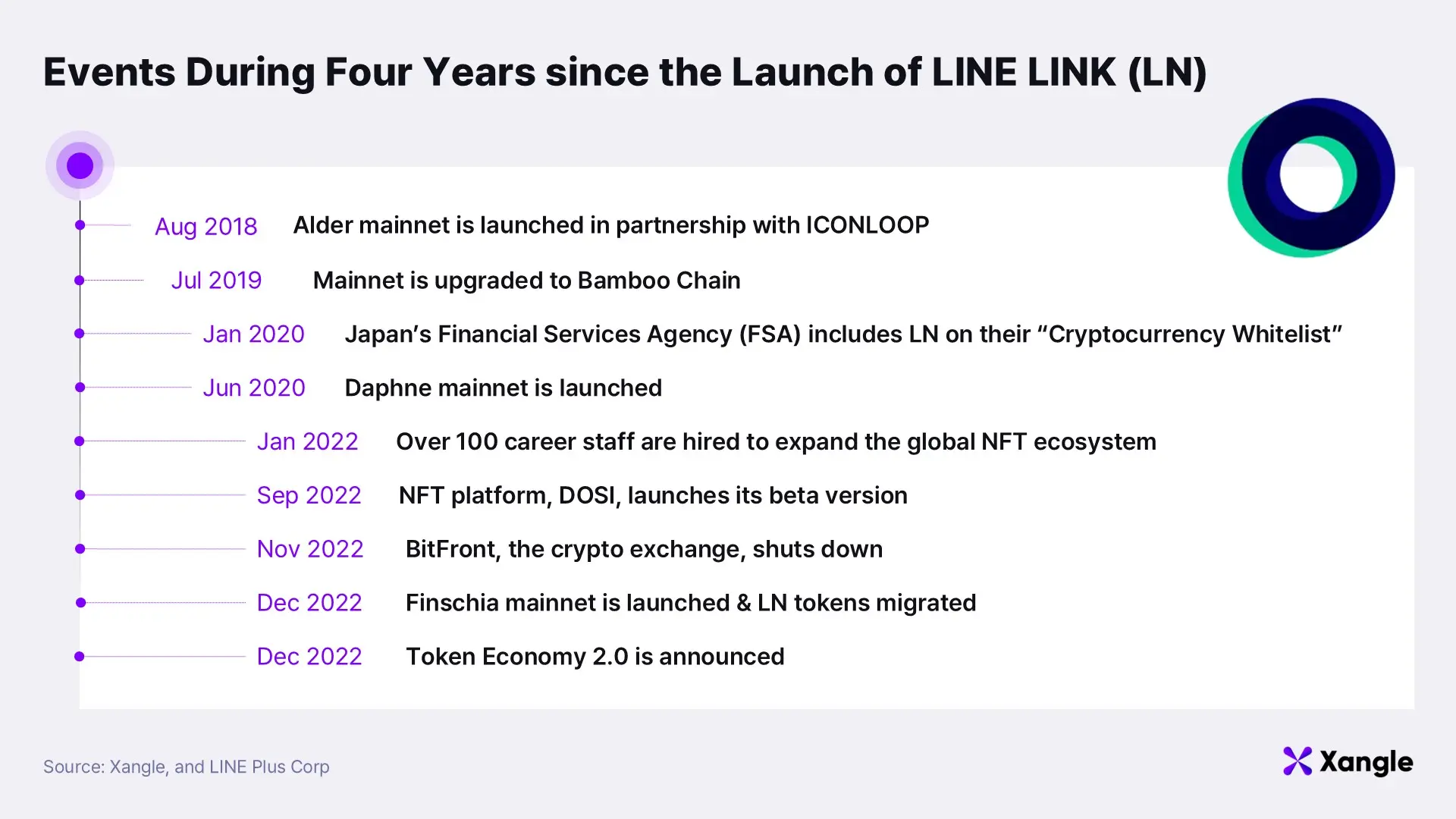

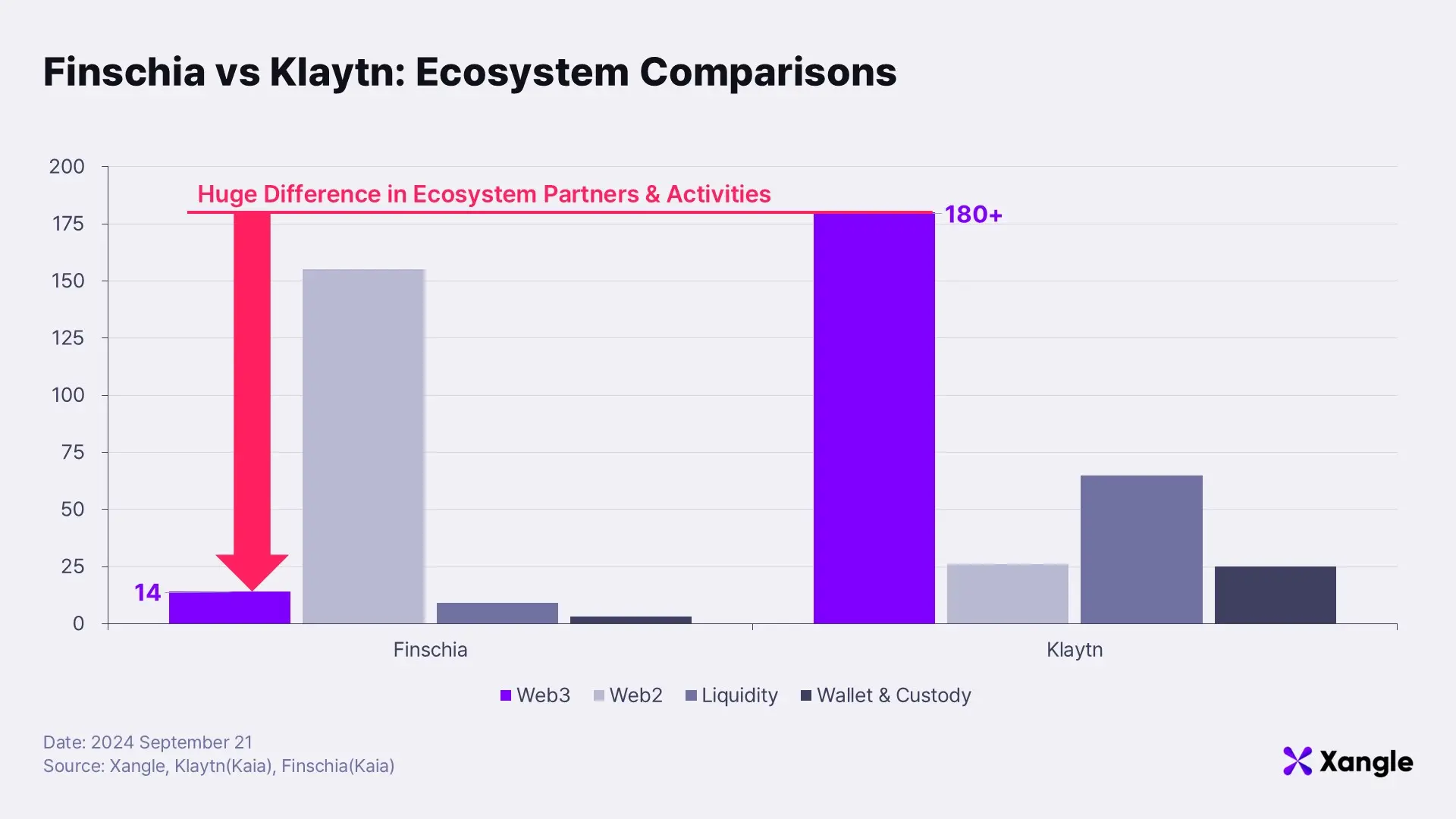

Finschia, formerly known as Line-Link (LN), was launched in 2018 as a Layer 1 project. With its adoption of a zero-reserve model, tokens were distributed through airdrops. However with strong regulations in Japan and a the nature of a closed, private chain architecture combined, hindered ecosystem growth. While typical Layer 1 blockchains operate as public chains that allow anyone to develop dApps and onboard users, Finschia’s closed nature made ecosystem development difficult from the start.

After four years of internal restructuring, Line-Link rebranded as Finschia and launched its mainnet as a public chain on December 22, 2022, introducing a zero-reserve strategy. This approach limited additional token issuance beyond the block rewards, with inflation initially set at 15% and planned to reduce to 5% over time. 20% of block rewards were reserved by the foundation for research and development (R&D).

Finschia’s Zero-Reserve Didn’t Age Well

Finschia rejected grant-centric approach as issues of miscommunication in token distribution status were fierce in local regulatory environment. However, this zero-reserve strategy became a hindrance to ecosystem growth in the long-term, leading to Finschia's decision to merge its mainnet with Klaytn just a year after its launch. Unlike other third-generation tokenomics projects, which used reserves to promote partnerships and ecosystem growth, Finschia’s zero-reserve strategy limited its ability to secure necessary funding and support ecosystem expansion.

Their web3 ecosystem consisted of just 14 dApps, therefore lacking essential infrastructure such as a DEXs within the network. Had Finschia operated an active grant program using its reserves to build the ecosystem, it might have grown into a major chain encompassing both Web2 and Web3 ecosystems.

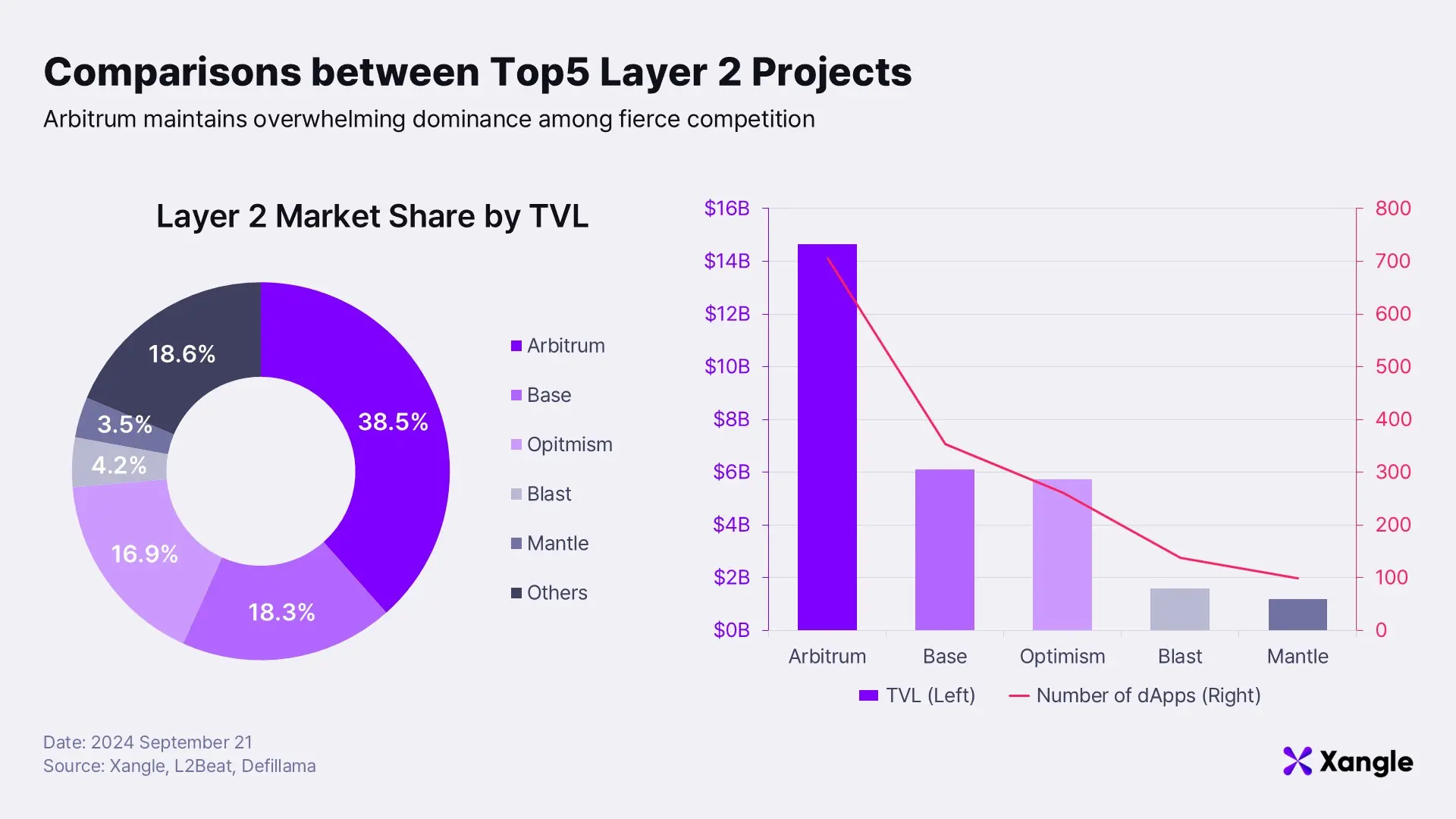

3-3-2. Grant Case Study: Arbitrum

Arbitrum, a Layer 2 blockchain designed to address Ethereum’s scalability issues, was developed to reduce gas fees while improving speed, satisfying both users and developers.

Arbitrum’s Expansion Strategy

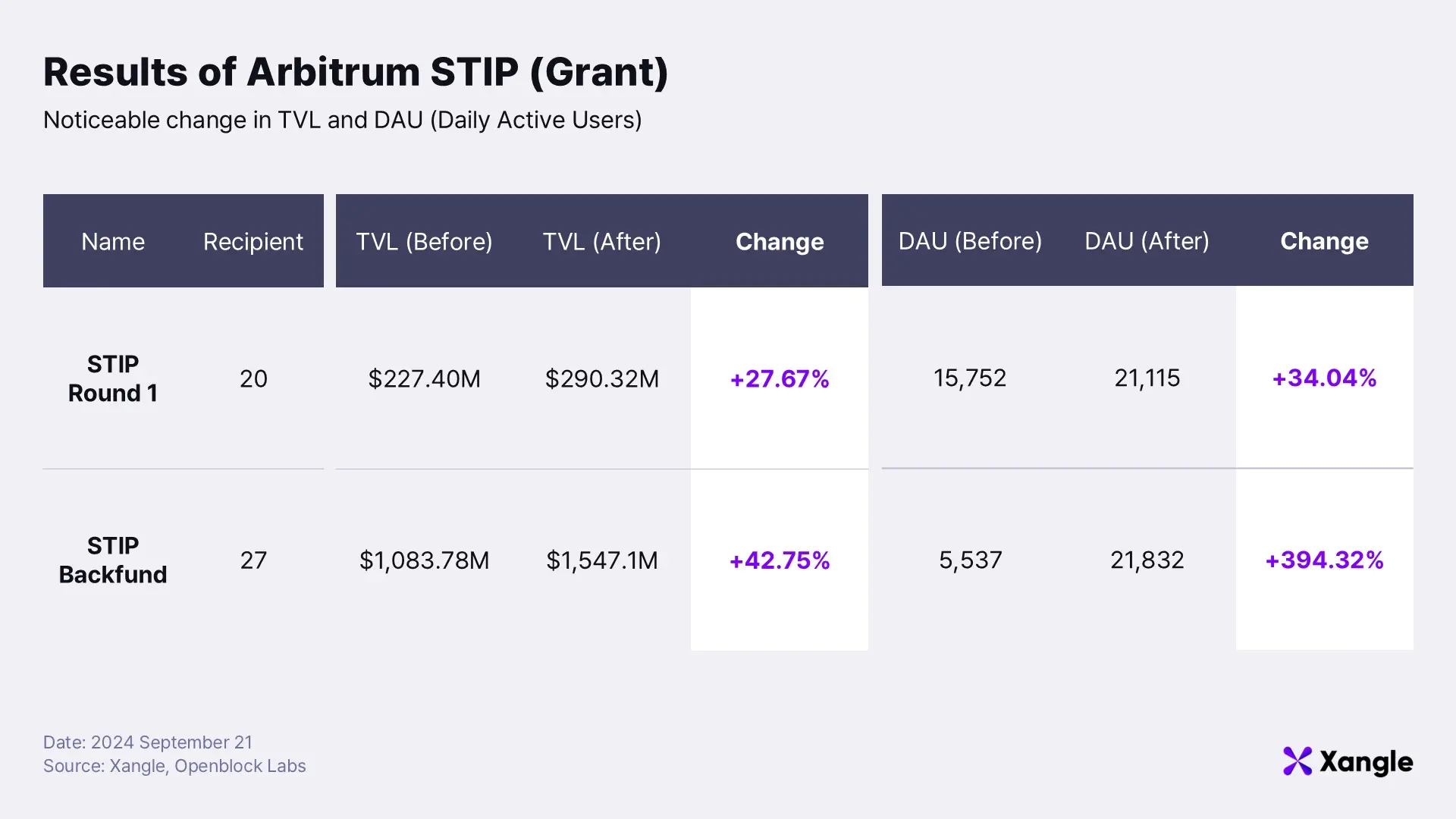

As a leading project of the third generation of tokenomics, Arbitrum has operated various grant programs, using a DAO-based decision-making process to expand its ecosystem. Its Short Term Incentive Program (STIP), the first of these grant programs, was designed to quickly deploy incentives to projects within the Arbitrum ecosystem, encouraging user acquisition and ecosystem growth.

Projects that received grants through STIP saw their TVL rise by up to 42%, with daily active users increasing by as much as 394%, demonstrating the effectiveness of grants in expanding the ecosystem. Arbitrum has continued to aggressively grow its ecosystem by launching additional grant programs based on such metrics.

In addition to diversifying the ecosystem through grants, Arbitrum has implemented structured management and improvement programs including community-driven expert programs like Quest Book and Pluralistic Grant Programs.

*Long-Term Incentive Program (LTIPP): An improved version of STIP, LTIPP uses 35 million $ARB for long-term support (86 projects).

Game-Changing Program (GCP): A $200 million grant program aimed at expanding Web3 gaming, with a focus on game onboarding and development infrastructure.

UAGP: A 9-month Uniswap-Arbitrum ecosystem developer grant program, distributing 1.1 million $ARB to 12 projects.

QuestBook: A developer onboarding support program with $1 million in grants across four domains.

Arbitrum Foundation Grants Program: A grant program for dApp development to foster growth in the Arbitrum ecosystem.

Request for Proposal (RFP): A program offering 3 million $ARB in grants for new initiatives.

Pluralistic Grant Program: A decentralized and transparent grant program aimed at experimenting with different decision-making models.

4. The Future of Tokenomics

The Missing Piece: Token Utility

So far, we’ve explored the overarching tokenomics strategies of (1) acquiring users and building ecosystems through token distribution and (2) generating ongoing demand through token utility and product improvements. We divided tokenomics into generations, focusing on distribution methods through ICOs, airdrops, and lastly grants - while analyzing the successes and failures of each. Tokenomics continues to evolve by addressing its limitations and amplifying its strengths. What does the future hold for tokenomics? As many projects reach maturity, it has become more important than ever to capture real value through distributed tokens. This calls for a new focus on (1) governance and (2) profit-sharing, and also other utilities that provide additional benefits to token holders.

4-1. Governance

One of the most basic and essential utilities is governance, providing token holders with a fundamental utility—ownership and activating the community and enabling the expansion of token-based ecosystems.

Governance utility can take various forms depending on the nature of the decisions being made. For instance, MakerDAO ($MKR) recently rebranded as Sky ($SKY) and is renowned for its sophisticated on-chain governance model with DAO-SubDAO structures.

On the other side, we have incentive-specialized models like those in DeFi protocols. Examples include OlympusDAO’s (3,3) strategy, Curve Finance’s veTokenomics, and Fantom’s Solidly. These models focus on sustaining long-term engagement within the protocol even after token distribution. A prominent case is Aerodrome ($AERO) on the Base chain, which has incorporated elements from veTokenomics and Solidly’s virtuous cycle. As of October 11, 2024, Aerodrome maintains a TVL of $1.23 billion, driven by Base’s large user base.

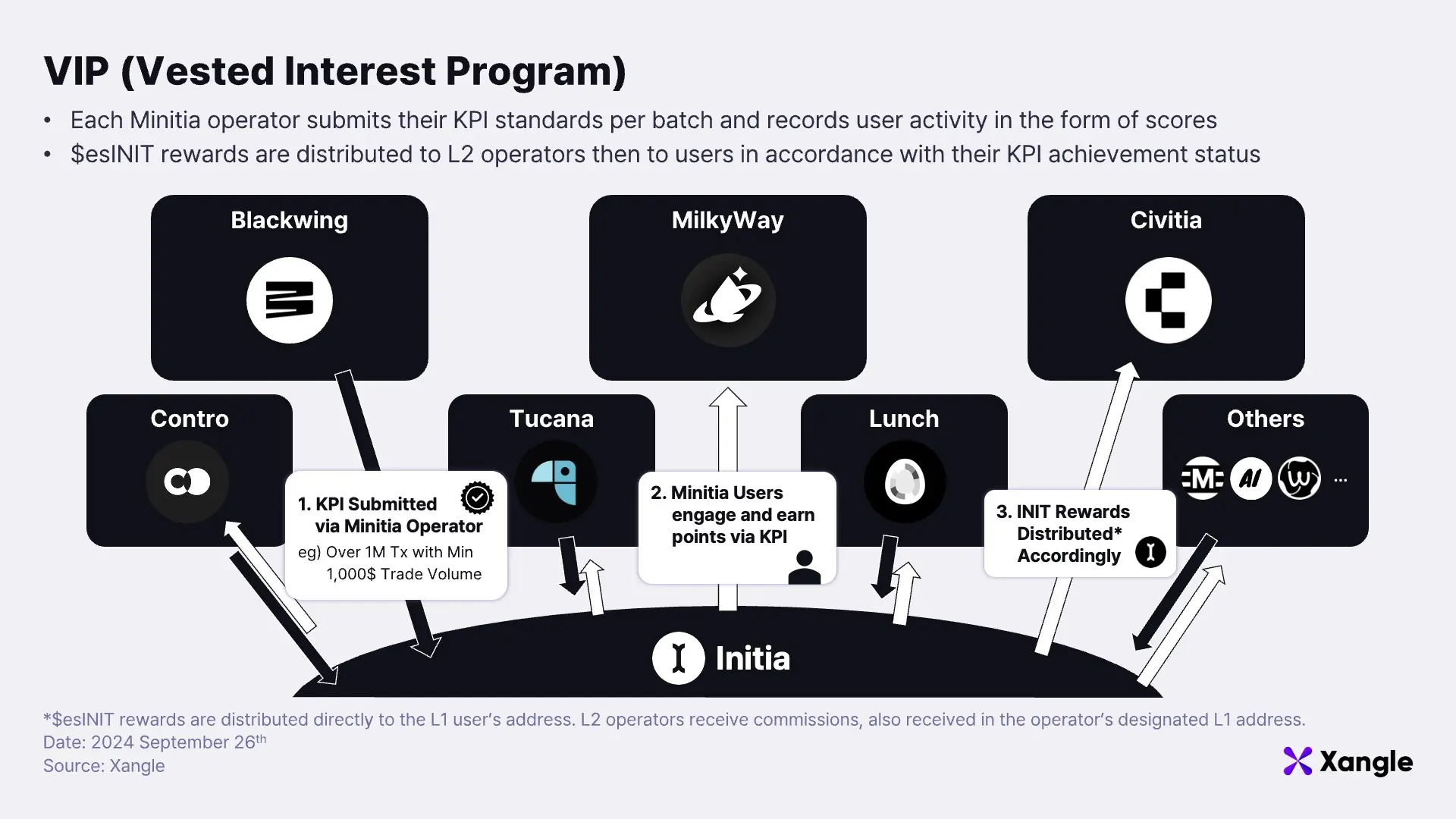

On the other hand, some projects use a mixed model that combines decision-making and incentive distribution. For example, Initia ($INIT), which operates in a rollup-centric appchain ecosystem, has implemented the Vested Interest Program (VIP), a governance model that allows voting rights to be delegated to appchains, determining chain-level decisions such as rollback, parameter settings, and new chain support. Based on the outcome of these votes, new INIT tokens are distributed to its user and the onboarded appchains, named Initia.

Low Governance Participation and Governance Attacks

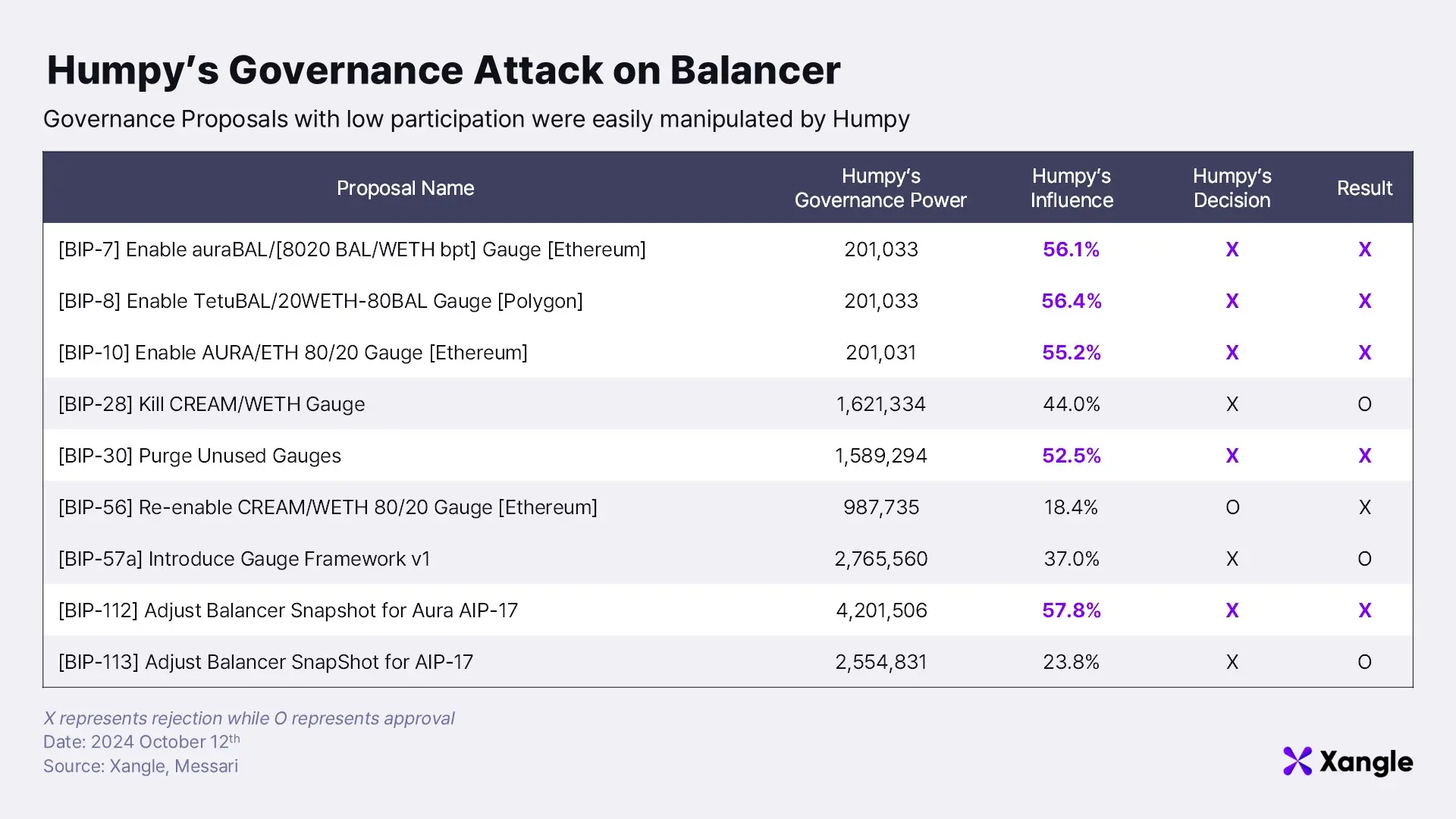

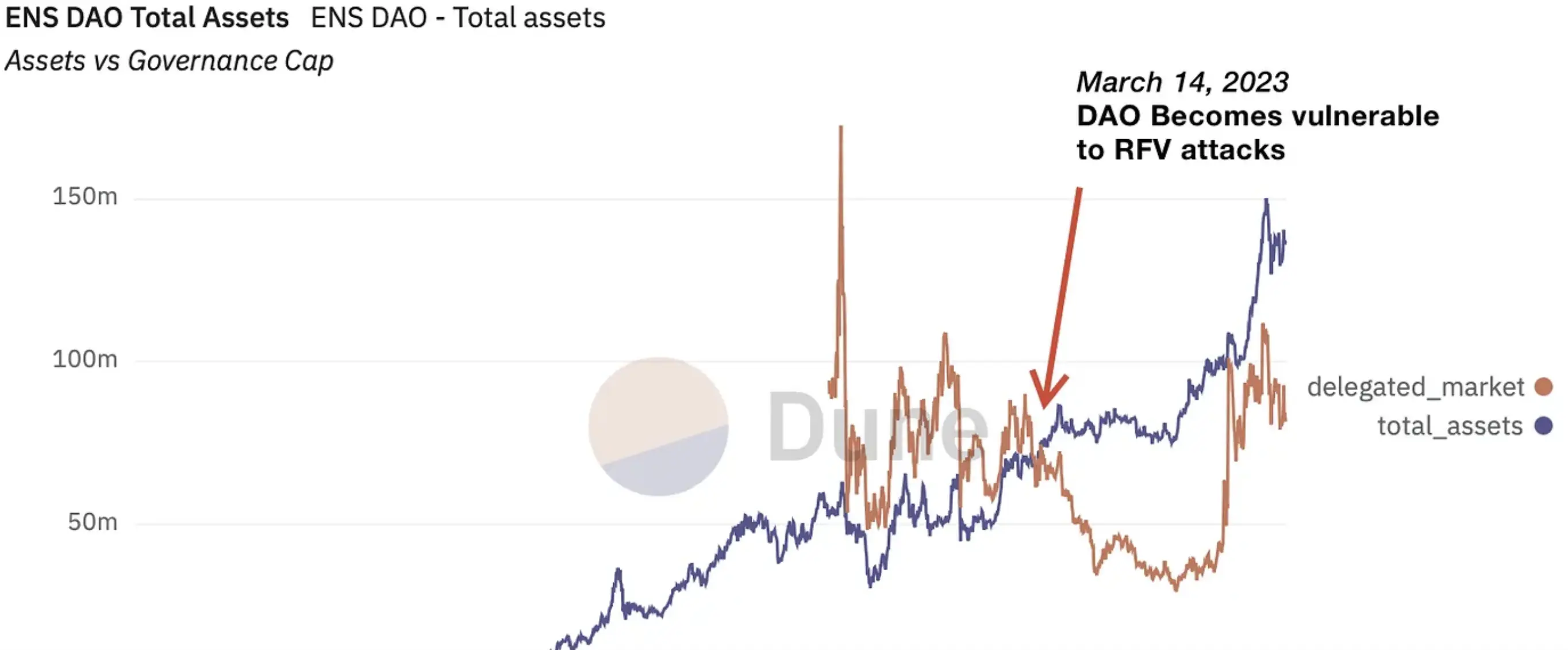

A common challenge across all above models is low participation rates in governance. Low voter turnout in on-chain governance can make protocols vulnerable to “governance attacks.” One prominent example occurred with Balancer in 2022. As Balancer uses $veBAL for governance, Humpy a single investor who held 35% of the circulating $veBAL exercised his voting power to manipulate the protocol by opposing on governance proposals for personal reasons or excessively rewarding his own liquidity pool. Similar attacks have occurred in protocols like Ethereum Name Service (ENS) and Beanstalk, underscoring the need for high participation rates when implementing governance utilities.

*In March 2023, the market cap of $ENS delegated to governance ($83 million) fell below the value of the DAO’s treasury ($137 million), exposing the protocol to potential attacks. To defend against this risk, ENS Labs and other key stakeholders created the veto.ensdao.eth wallet, which holds 45.5% of the total supply of $ENS, and is authorized to veto any malicious proposals.

For Higher Governance Participation

The root cause of these governance attacks is that the cost of attacking the protocol is relatively low compared to the value or influence of the foundation’s reserves. As a solution, recent efforts have focused on improving governance utility to encourage participation. For instance, Jupiter ($JUP) offers Active Staking Rewards (ASR) as an incentive for governance participants. Arbitrum ($ARB) introduced $stARB, a liquid governance token, to share profits with token holders. Optimism’s fifth airdrop required users to delegate governance rights to the foundation to receive the airdrop, concentrating governance power in the hands of the foundation. These various methods are emerging to increase governance participation and strengthen token demand, while also providing resistance to governance attacks.

4-2. Profit Sharing for Token Holders

Another emerging utility is profit-sharing for token holders. Like traditional financial models (e.g., the Gordon Growth Model or Discounted Cash Flow analysis) that are based on cash flows, token utilities could derive their value from protocol revenue or user benefits on using the protocol / product. However, we Xangle believe that it will take significant time before profit-sharing becomes a mainstream utility, mainly due to (1) legal risks and (2) the fact that only few protocols currently generate sufficient revenue.

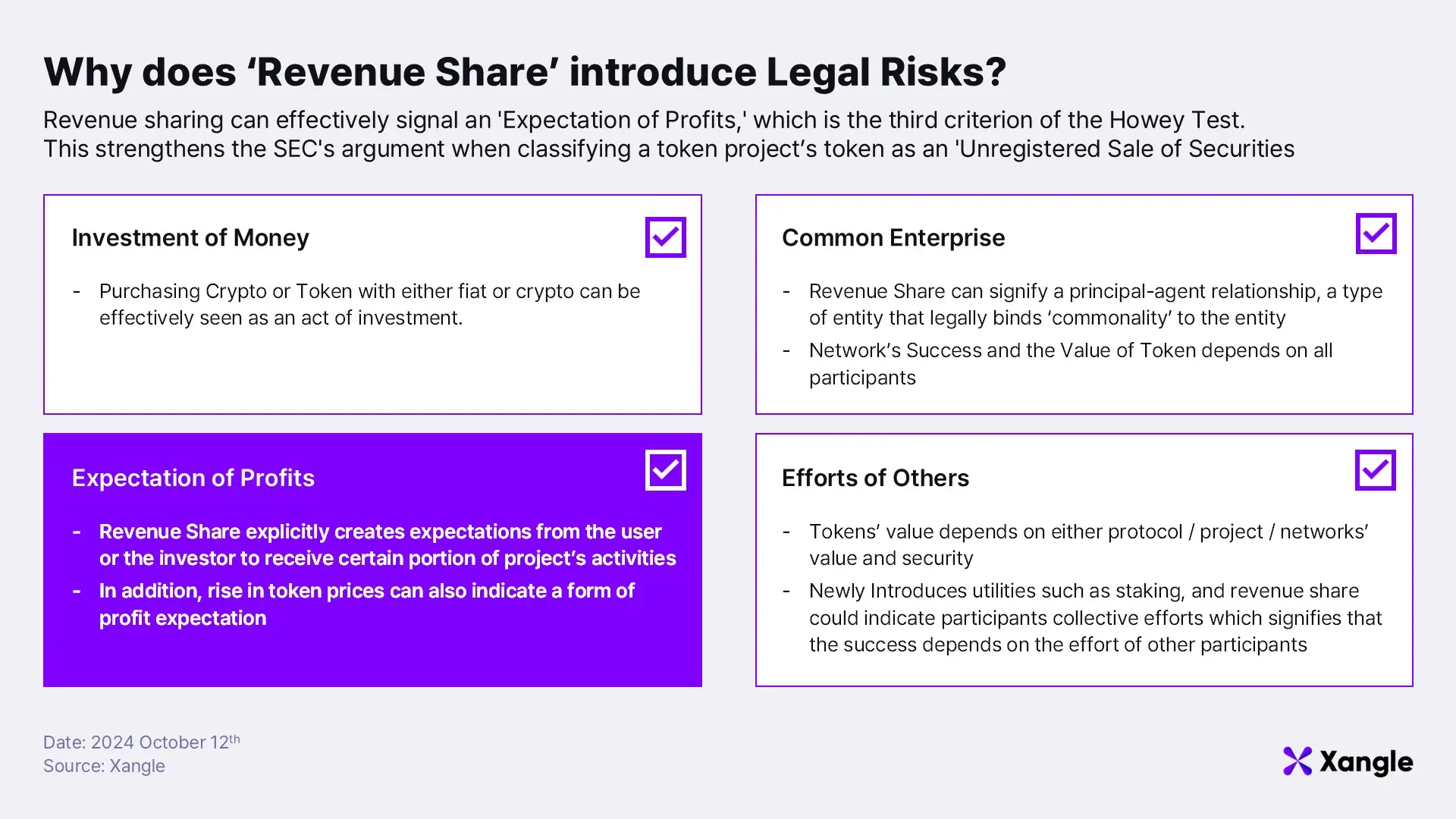

Scapegoat: Legal Risks upon Profit Sharing

Profit-sharing introduces legal risks, as it could lead to tokens being classified as securities. While tokens themselves are not anymore being considered as securities as their nature, how they are utilized can confer characteristics of securities. Token models that mimic stock dividends by distributing shared profits could significantly increase the likelihood of tokens being considered securities, which could impose substantial legal and operational costs on token projects.

For instance, in 2017, the DAO token issued on Ethereum offered a profit-sharing utility that gave token holders a share of the profits from funded projects. The SEC used the Howey Test to determine that the DAO token violated securities laws, issuing a report in response. Ongoing legal battles involving Ripple (XRP), Uniswap (UNI), and Lido (LDO) further illustrate the risk of profit-sharing utilities being classified as securities. Although the Ripple ruling in July 2023 rejected the notion that tokens themselves are securities, more definitive legal precedents will need to be established before profit-sharing can be fully realized as a token utility without non-security features.

*The DAO was a decentralized autonomous organization launched on Ethereum in 2016 that raised $150 million through a token sale. Following a re-entrancy attack that drained $50 million, the Ethereum community was split on how to address the incident, leading to the creation of Ethereum Classic ($ETC) and what we now know as Ethereum.

**In July 2023, after a three-year legal battle between Ripple and the SEC, Judge Analisa Torres ruled that XRP tokens sold on secondary markets (e.g., exchanges) did not qualify as securities. However, the decision also established that how a token is used may confer securities status.

***The U.S. presidential election in November 2024 could also impact this issue, especially if crypto-friendly Trump wins. If Trump is elected, there may be a leadership change at the SEC, which could lead to more favorable conditions for crypto projects. As of October 14, 2024, Trump leads with a 54% chance of winning, compared to Harris’ 45.4%, according to Polymarket.

The Root Cause: Weak Revenue

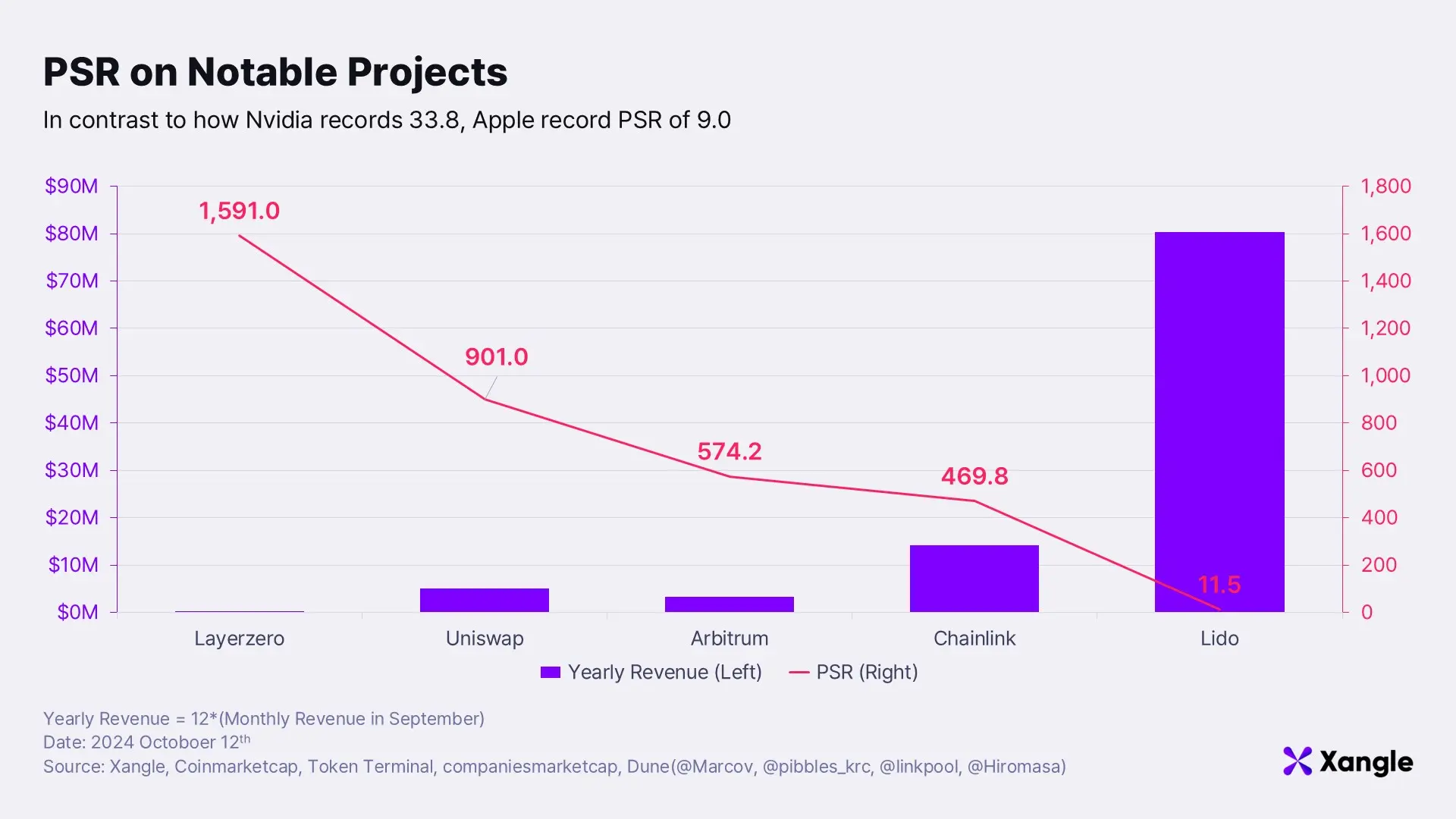

At the heart of the problem, however, is the fact that most projects do not generate enough revenue to enable meaningful profit-sharing. We analyzed the Price-to-Sales Ratio (PSR) of four major projects across different sectors.

Compared to companies in traditional financial markets, such as Nvidia (33.8 PSR) and Apple (9.05 PSR) on NASDAQ, Web3 projects are heavily overvalued relative to their earnings. Although there clearly exists Web2 comparable revenue makers like Lido ($LDO), which has a PSR of 11.5 after its token distribution phase ended - it may be too early to rely on this as a long-term valuation method for projects since new narratives and competitors rapidly emerge and influence the value of a project the most in crypto - like restaking and chain abstraction.

*PSR is calculated by dividing market cap by annual revenue. A higher PSR indicates overvaluation, while a lower PSR suggests undervaluation.

**LayerZero’s PSR stands at 1591, meaning that for every $1591 of LayerZero tokens in circulation, the protocol generates only $1 in annual revenue. Although there are differences in performance between traditional finance, Web3, high-growth sectors, and low-growth sectors, we concluded that these tokens are generally overvalued.

Rule-of-a-thumb: Indirect Value Accrual

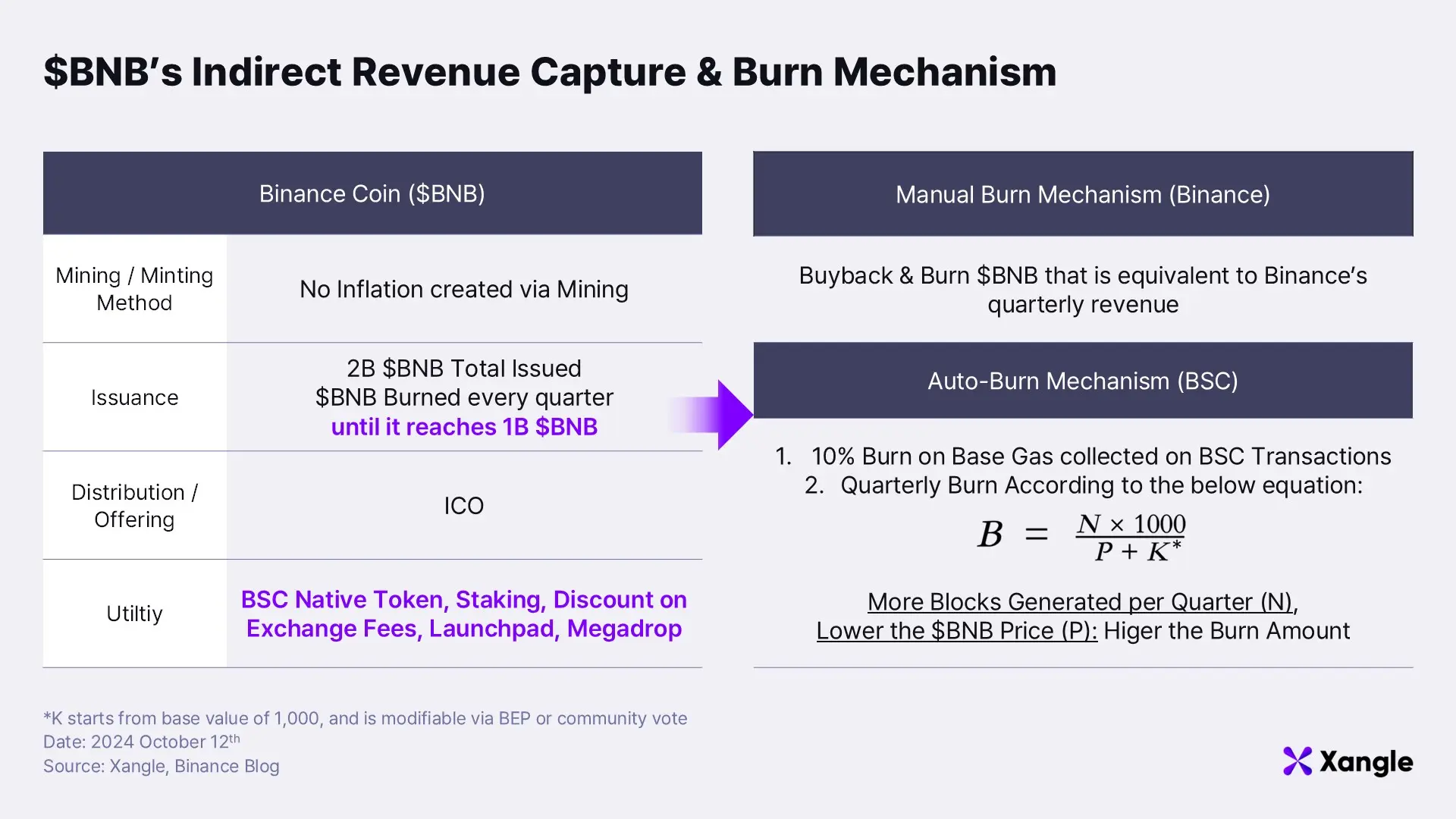

For these reasons, direct profit-sharing is unlikely to become widespread any time soon. Until the external factors are resolved, indirect profit-sharing models, like those used by Binance Coin (BNB) and Burn Auction by Injective Protocol (INJ), are expected to remain popular.

$BNB is used throughout the Binance Smart Chain (BSC) ecosystem, offering utility in the form of discounted trading fees, access to launchpads, and other benefits exclusive to token holders. Binance has also adopted a deflationary model, burning 50% of the total supply over time, providing indirect profit-sharing for holders. This increases token demand, supporting its price while naturally locking users into the exchange and driving sustained growth within the BSC ecosystem.

5. Conclusion

The Tokenomics Evolution will Prevail

Tokenomics is composed of the token distribution strategy at the time of the Token Generation Event (TGE) and the utility that ensures long-term sustainability. We can classify token distribution strategies into three generations: (1) ICOs in 2017, (2) Airdrops from 2020–2022, and (3) Grant-centered strategies in the current phase. As tokenomics moves forward, enhanced utility will become increasingly important. Utilities like governance and profit-sharing will need to interact organically to create a sustainable economic system, proving a project’s value as a “protocol.”

The Token Is ‘Also’ Your Product

Probably the only working value of Web3 has been the value of of tokens as an investment vehicle making tokens themselves as also - a product. On top of that, projects raise funds based on their tokens and unless long-term sustainability is assured in the token prices - users won’t remain within the ecosystem and so are projects backed with token-based treasuries.

The relationship between product and tokenomics is like the chicken-and-egg dilemma—one cannot come first and one will inevitably introduce the other some day or another. If you haven’t launched a token with a working web3 product - you will have to someday, and vice versa. Here the harmony becomes the key challenge.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Circulating Supply Series #2] Addressing Ongoing Circulating Supply Controversies](https://resource.xangle.io/content/thumbnails/1680/content_1680_thumbnail_f66b905b.webp)

![[Circulating Supply Series#1] Circulating Supply: The Canary in the Crypto Mine](https://resource.xangle.io/content/thumbnails/1672/content_1672_thumbnail_cf1d70cd.webp)