[Circulating Supply Series #3] Circulating Supply Management: Lessons from the Stock Market

Table of Contents

1. Introduction

2. Free Float Ratio, Measure of Circulating Supply in the Stock Market

3. Significance of Free Float Ratio

4. Management of Free Float Ratio

5. The Escalating Significance of Circulating Supply Management in the Cryptocurrency Market

6. Suggestions for Managing Circulating Supply

7. Final Thoughts

1. Introduction

In our previous reports last year, we delved into the significance of circulating supply within the cryptocurrency market with “[Circulating Supply Series #1] Circulating Supply: The Canary in the Crypto Mine" and emphasized the necessity of clear regulation of circulating supply and verified disclosure systems in “[Circulating Supply Series #2] Addressing Ongoing Circulating Supply Controversies." With “[Circulating Supply Series #3] Circulating Supply Management: Lessons from the Stock Market," we aim to examine the significance and management of circulating supply in the stock market, reaffirm the importance of circulating supply management within the cryptocurrency market, and present strategies to manage circulating supply based on examples from the stock market.

2. Free Float Ratio, Measure of Circulating Supply in the Stock Market

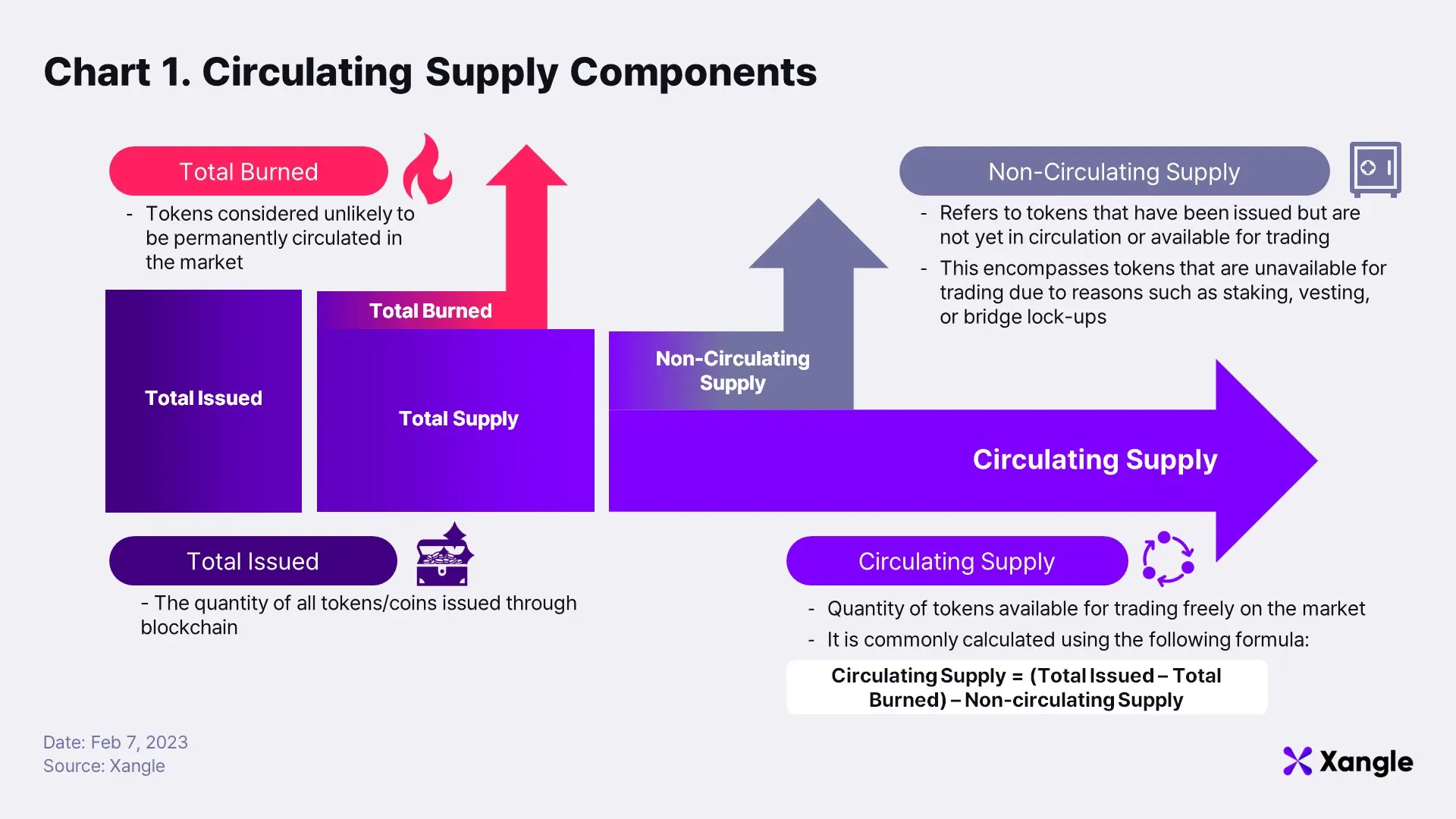

Before we delve into everything, let's explore how the "circulating supply" is understood in the stock market and the cryptocurrency market. “Circulating supply” in the stock market refers to the free float of shares. Free float represents the total issued shares minus the amount not traded in the market, signifying the number of shares freely traded among investors within the circulation market. In the stock market, the free float ratio is commonly used as a substitute for free float divided by the total issued shares as a percentage rather than an absolute number. Similarly, in the cryptocurrency market, "circulating supply" refers to the amount of supply minus tokens/coins not circulating in the market out of the total issued tokens/coins, due to reasons such as staking or vesting, representing the quantity of tokens/coins freely traded in the market “Circulating supply” in both markets essentially refers to the volume available for trading among investors. It refers to the marginal amount that investors can buy and sell in order to shape the price through supply and demand. However, there are some technical peculiarities unique to the cryptocurrency market. For instance, tokens/coins issued in the cryptocurrency market can be autonomously burned by holders (assuming burn function is implemented within the token contract), and tokens/coins with an inflationary structure from validator rewards may experience fluctuations in total issuance depending on the speed of block generation. Therefore, accurately tracking circulating supply in the cryptocurrency market requires meticulous real-time tracking of a token’s total issued and burned amount based on on-chain data (Chart 1).

3. Significance of Free Float Ratio

3-1. Guide for investors

In the stock market, the free float ratio serves as an investment guide for liquidity and price efficiency. Assuming equal stock prices, a higher free float ratio allows more investors to participate in trading stocks, naturally leading to increased trading volume. Through active trading by numerous investors, stock prices reflect various information, enhancing price efficiency. Conversely, it’s hard to say that the price of stocks where the free float is limited and controlled by a few shareholders objectively reflects the company’s market value. Furthermore, stocks with a low free float ratio are more likely to have low trading volumes, which can lead to wider bid-ask spreads and slippage losses during the trading process. Hence, lower free float ratios not only hinder objective reflection of market value but also pose greater difficulties for investors to trade. Therefore, under identical conditions, stocks with higher free float ratios are generally considered more suitable for investment compared to those with lower ratios.

3-2. Key element in index calculation

The free float ratio is also a key indicator for calculating the indices underlying passive financial products. Major global indices such as the S&P 500 in the United States and the KOSPI 200 in South Korea calculate the weight of constituent stocks based on free float market capitalization, of which free float market capitalization of individual stocks is calculated by multiplying stock prices by free float shares. The index calculates the weight of stocks and index value based on the free float ratio to reflect the number of shares that are currently in circulation to indicate market conditions more accurately. The Korea Exchange (KRX), which calculates South Korea's representative stock indices such as the KOSPI 200 and the KOSDAQ 150, excludes stocks with a free float ratio of less than 10% from consideration for index inclusion. This decision is based on the judgment that stocks with significantly low free float ratios, despite having a large market capitalization, do not effectively contribute to market movements. Ultimately, the calculation serves to improve the ease of investment and marketability of passive financial products based on indices. Passive financial products such as index funds and Exchange-Traded Funds (ETFs), considered significant players in the stock market, replicate the performance of specific indices by trading the stock baskets constituting the index. Therefore, the influence of the free float ratio on the allocation of fund capital to each stock, thereby affecting the market, is substantial.

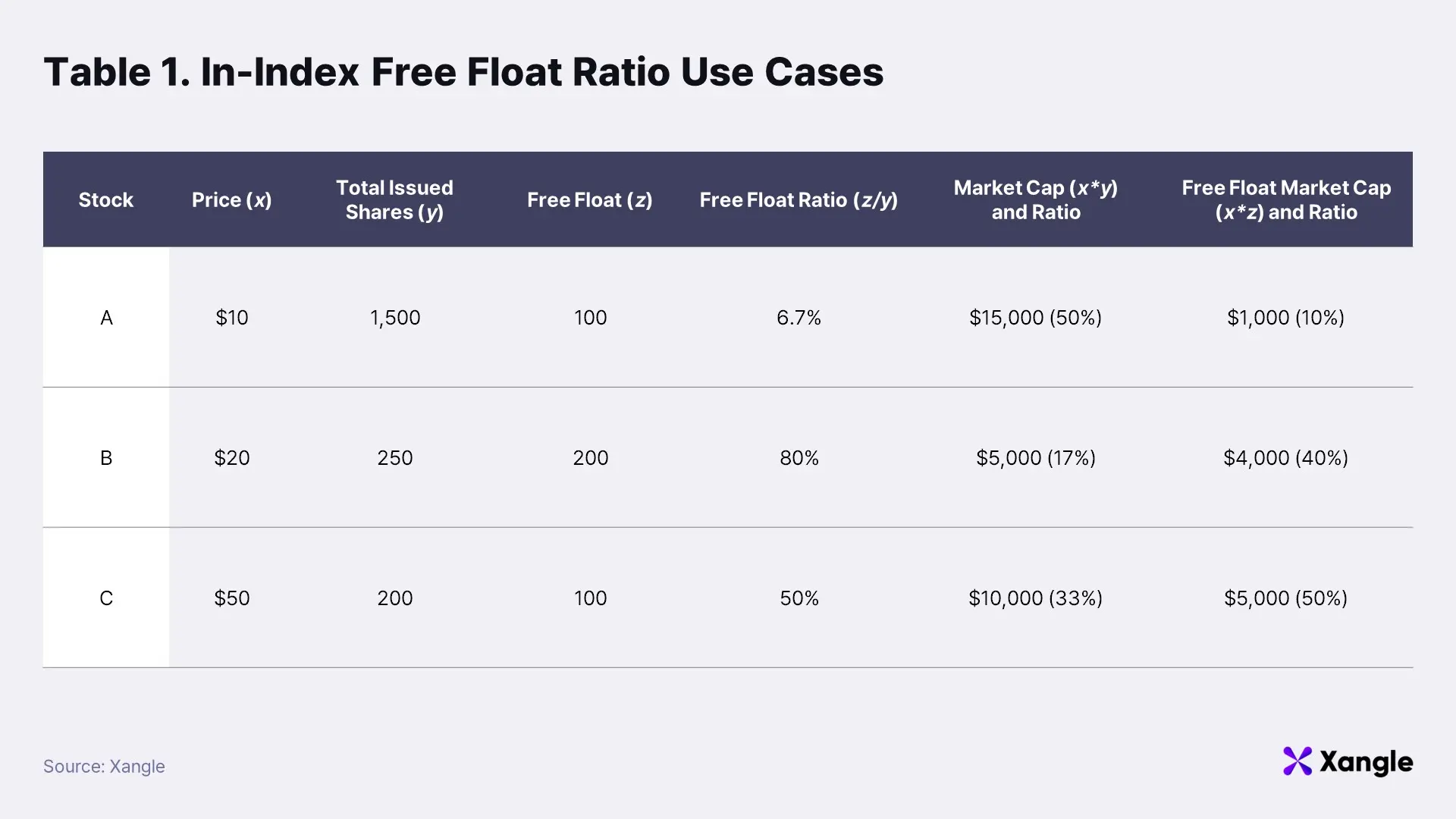

To illustrate, let's consider an index composed of three stocks, A, B, and C (Table 1). If the index is calculated based on total issued shares rather than free float shares, the weight of stock A jumps from 10% to 50%. Consequently, a fund tracking this index needs to allocate half of its AUM to buying stock A. As ETFs and passive financial product managing organizations are obligated to hold the underlying assets of the index they track, funds will be funneled into the stock in proportion to its weight in the index. This reveals that if the free float ratio of stock A is 6.7%, it implies that the volume actually traded in the market is less than a tenth of the total issued shares, indicating insufficient liquidity to accommodate large-scale buy orders from fund managers. If an index is constructed based on simple market capitalization, it becomes difficult for managers to hold stocks in proportion to the actual composition of the index, resulting in a discrepancy between the fund's net asset value (NAV) and the performance of the underlying index. This tracking error not only makes normal fund management difficult, but also reduces investors' confidence in the fund and the underlying index. Furthermore, if an index is calculated based on market capitalization instead of free float market capitalization, large passive fund managers may cause price distortion in the process of buying and selling disproportionately large quantities of stocks compared to the available circulating shares in the market. As passive funds grow in size, their flows are increasingly driven by indices, which means that the free float ratio is increasingly influential on stock prices. Let's take a look at how the free float ratio is managed in the stock market.

4. Management Methods of Free Float Ratio

4-1. Standardizing free float ratio

The concept of free float ratio is standardized in the stock market. In the United States, the Securities and Exchange Commission (SEC) played a crucial role establishing the concept of the free float ratio as an industry standard. By requiring detailed disclosure of ownership structure for all listed companies, it laid regulatory groundwork to calculate the free float ratio based on a mutually agreeable figure. Additionally, as many investors began to utilize the free float ratio to assess the liquidity and marketability of listed companies, gradually establishing standardization and market practices for the free float ratio. In South Korea, the KRX played an important role in standardizing the concept of free float ratio. The KRX defines free float shares as total issued shares minus illiquid shares. Illiquid shares refer to those restricted from trading or are not in circulation, including shares held by major shareholders, related parties, government-funded institutions, as well as treasury shares, company shares, protected shares, and overseas DR shares. As will be discussed later, the KRX, like the SEC, KRX mandates the disclosure of information regarding the ownership structure of different securities and conducts regular reviews of both primary and secondary markets.

4-2. Methods to calculate and disclose free float ratio

Although centralized financial institutions such as the SEC in the United States and KRX in South Korea set standards for free float ratio, its actual calculation and disclosure are usually done by the index producers. As mentioned earlier, free float ratio is a key indicator for calculating index, so it is usually published regularly, usually in time for index rebalancing. Also, each organization specifies the calculation method to quantify the ratio, which may vary slightly from one index to another due to different reference dates, calculation methods, and so on. In South Korea, the KRX (KRX is both an exchange and an index producer, and in this context, an index producer) officially releases the data on the business day following the June and December index change dates every year. In addition, the KRX has a policy of only changing free float ratio if the change rate is 5% or more, and maintaining the existing ratio if it is less than that. In the case of S&P Dow Jones Indices, the leading U.S. index producer, the ratio is reviewed quarterly and announced on the March, June, September, and December change dates (before the market opens on the Monday after the third Friday). In the case of S&P DJI, an exception is made for changes in the free float ratio of 5% or more to be reflected immediately under the Accelerated Implementation Rule.

4-3. Monitoring shareholder composition

The exchange of shares, which is the basis for calculating free float ratio, and the shareholder composition are managed in a unified database through the securities depository settlement system in each country. A securities depository settlement system is one in which investors, financial investment companies, etc. open accounts with a centralized securities depository settlement company, deposit the securities they own, and process payments for sales, purchases, etc. between accounts without physically moving the securities. Korea Securities Depository of South Korea and Depository Trust & Clearing Corporation in the United States, the Depository Trust & Clearing Corporation serve as the central securities depository in each country. Since stock purchases and sales are also carried out through securities firms, the shareholder composition of listed companies is jointly managed in multiple databases in real time. In addition, investors are notified through the shareholding disclosure system when there is a significant movement in volume that could affect the stock price. The shareholding disclosure system refers to a system that requires companies listed on the securities market to report any changes such as the number of shares owned by the largest shareholders of the company without delay to the KRX. It is based on the "Financial Investment Services and Capital Markets Act" and the "Market Listing Regulations" of the KRX, so it is legally binding, and sanctions are imposed on listed companies if they miss reports or violate deadlines. Technically, this is an obligation to report the holding status and changes within five business days when a company holds more than 5% of a stock, or when the holding percentage changes by 1% or more, or when there is a change in important matters such as the purpose of holding, and the information is publicly disclosed to all investors through the electronic disclosure system (DART). In the U.S., the SEC's Form 4/13F and Schedule 13D/13G serve the same purpose. As mentioned above, the ownership status of shares is updated in real time on a common database, and as listed companies are required to stick to the disclosure obligation rule, free float ratio is rather both timely and transparent in the stock market.

4-4. Other management mechanisms

Factors that affect free float ratio, such as the form of issuance and the composition of shareholders, are not solely managed in the issuance market. In South Korea, they are being reviewed from the secondary market, where shares are first listed. The Korea Exchange assesses the listing structure, distinguishing between rights offerings and rights sales. In a rights sale, the exchange conducts a comprehensive evaluation of the objectives, purposes, and scale of the proposed sale. The Exchange conducts the examination, prioritizing the protection of small investors. Since rights sale could occur as an exit strategy when there is a financial investor as a shareholder, the Exchange checks whether there are any issues related to the protection of small investors due to contracts between the financial investor and the largest shareholder or related parties. Furthermore, the Exchange also specifies the diversification requirements. The diversification requirement is determined by the public share ratio or equity capital of the listing applicant, which can be summarized as 1) a certain public share ratio or number of public shares and 2) higher equity capital requiring a higher share diversification. The number of minority shareholders and their shareholdings are monitored from the listing stage to ensure that the company has adequate share diversification and liquidity. Furthermore, the KRX has a delisting condition for failing to meet the share diversification standard, so managing share diversification requirements extends beyond listing. If the ratio of common shareholders falls below 10%, the stock is designated as a managed stock, and if it is determined that it has not improved within a given time, it can be delisted.

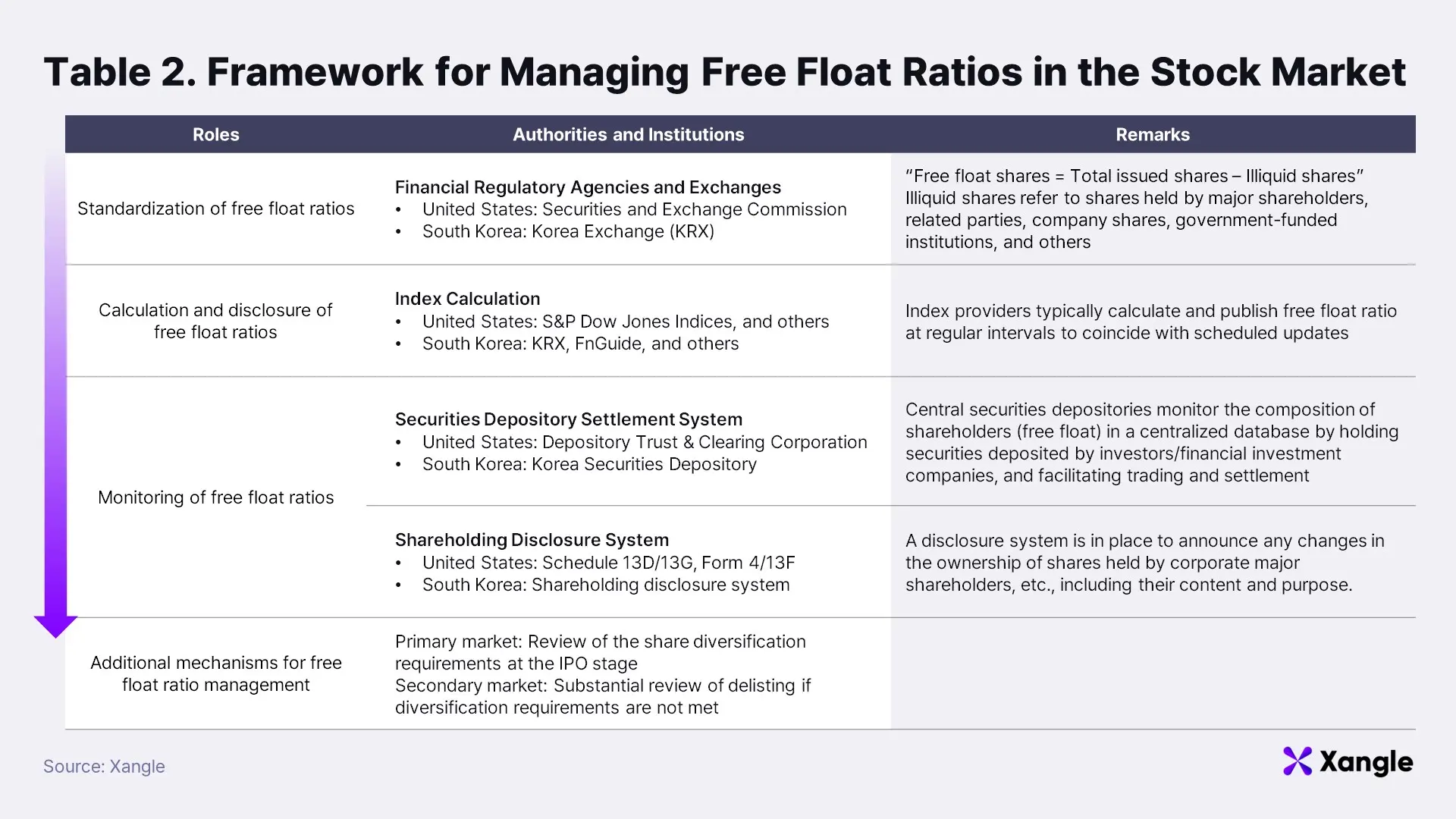

Let's summarize the management framework for free float ratios within the stock market (Table 2):

- First off, we need clear definitions and standards for free float ratios.

- Different index providers autonomously calculate and disclose free float ratios according to these standards.

- The securities transaction data forming the basis for free float ratio calculations is managed in a centralized database under the securities settlement system.

- Major shareholding changes are disclosed through the shareholding disclosure system.

- Furthermore, various regulations exist for managing free float ratios within the issuance and distribution markets for investor protection.

5. The Escalating Significance of Circulating Supply Management in the Cryptocurrency Market

Previously, we emphasized that in traditional markets, free float ratios serve as indicators of liquidity and price efficiency, guiding investment decisions and index calculations. In the crypto space, circulating supply is paramount as it acts as a compass for investments. It's anticipated that circulating supply will emerge as a pivotal indicator for future cryptocurrency indices and passive markets, even though its full activation is yet to be realized.

The significance of circulating supply in the cryptocurrency market as a guiding metric for investments vastly greater than its counterpart in traditional stock markets. Unlike stocks, the crypto space lacks tokens with sustainable revenue models and established valuation methodologies with long-term validation. With no standardized criteria for evaluation, token prices are predominantly dictated by market demand and supply dynamics, underscoring the pivotal importance of circulating supply metrics, particularly given the scarcity of mechanisms to regulate token supply.

Issuing tokens via smart contracts is easily accessible to anyone, with issuers having complete control over the token supply. Moreover, the global landscape is populated with numerous exchanges, each with its own listing criteria. Typically, the assessment of circulating volumes is confined to the circulation plan outlined in the project's whitepaper. However, even after listing, there's often no effective mechanism to prevent many projects from releasing tokens that exceed their initial distribution plans. As underscored in the "[Circulating Supply Series #2] Addressing Ongoing Circulating Supply Controversies," several projects falter in adhering to disclosed distribution plans or fail to promptly disclose them, perpetuating suspicions of excessive release of tokens. To preempt such incidents, the implementation of precise circulating supply calculation standards and a robust, auditable disclosure framework is imperative.

Moreover, circulating supply in the cryptocurrency market stands as a pivotal metric for index calculations. With distinctions drawn between market capitalization and fully diluted valuation, where circulating supply serves as the defining factor, it's apparent that various indices within the cryptocurrency space must derive from liquidity market capitalization.

It's inevitable that passive investment strategies will gather momentum in the cryptocurrency market. As financial markets mature, they tend to become more efficient, favoring passive strategies that track beta (indices) rather than actively seeking alpha. Moreover, the demand for passive financial products is anticipated to surge due to their various benefits, such as lower fees, transparency, and risk diversification. Notably, in equity markets, passive funds already constitute nearly 50% of the total fund market.

Though the cryptocurrency market is still in its infancy, the dominance of passive investment strategies is premature. Regulatory and technological barriers must be overcome before indices can seamlessly integrate with investable financial products, given the complexity of token issuance across multiple mainnets and the fragmented nature of exchanges. Nonetheless, numerous global and domestic institutions, including Xangle, are actively computing indices. Index fund tokens like Total Crypto Market Cap Token (TCAP) and DeFi Pulse Index Token (DPI) consistently attract Total Value Locked (TVL), indicating a growing interest in passive investments within the cryptocurrency space. Consequently, the importance of free float ratios within the domain of indices is expected to expand accordingly.

6. Suggestions for Managing Circulating Supply

With the recent greenlighting of Bitcoin spot ETFs paving the way, the cryptocurrency market is steadily edging towards mainstream adoption, amplifying the clamor for robust risk management practices. To solidify crypto assets as a credible asset class, immune to such concerns and embraced by investors, a sophisticated circulating supply management framework is imperative. Hence, we present circulating supply management proposals drawing insights from the stock market's free float ratio management, as previously examined.

6-1. Standardization of circulating supply metrics

First and foremost, establishing universally accepted circulating supply metrics is paramount. This initiative ensures the following: 1) Exchanges can transparently elucidate their listing/delisting decisions regarding tokens amid circulating supply controversies. 2) Token projects overseeing issuance and circulation can devise management strategies for wallets holding tokens. 3) Investors can gain deeper insights into the supply-demand dynamics of their token holdings. Without clear metrics, persistent queries such as "Why was Token A delisted while Token B remains listed?" will continue to echo throughout the community.

The foundational framework will resemble that of the stock market. Similar to how the total number of shares outstanding is deducted from the number of illiquid shares to determine floating shares, the total token supply is deducted from the number of tokens burned to ascertain the circulating supply. This definition is already mutually acknowledged by CoinMarketCap, Token Unlocks, and others. Nonetheless, the most intricate hurdle lies in delineating the "illiquid token supply" category.

The decentralized nature of blockchain technology means that tokens aren't issued and distributed using a standardized approach, making it challenging to establish clear boundaries. Take, for instance, locked-up token supplies — some projects structure their smart contracts to automatically transfer tokens to investors' wallets upon unlocking, while others employ legal agreements for locking. In the former scenario, aggregating on-chain data allows for considering it as circulating supply since the locked tokens will be released from the project's wallet to investors' wallets upon unlocking. However, in the latter case, determining it as circulating supply solely based on on-chain data is impractical as investors can receive locked tokens from the project's wallet at any time.

Ultimately, achieving a universally accepted definition is paramount for market participants. Once consensus is reached, projects can align their token distribution strategies accordingly to meet listing requirements. For instance, suppose there's a consensus in the market that tokens staked by PoS chain validators are deemed non-circulating, while rewards are considered circulating, and they should be kept separate within a wallet address. Projects currently distributing rewards to staking addresses would need to adjust their tokenomics to separate these categories, either through smart contract code adjustments or operational policy changes, to secure exchange listings.

To accommodate a wide array of projects, it's imperative to explore various scenarios comprehensively. Therefore, collaborative efforts involving entities like DAXA, the Financial Supervisory Service, and other infrastructure providers related to circulating supply are essential. These collaborations can facilitate the sharing of examples and the building of consensus, ensuring a robust framework for defining circulating volumes in the crypto market.

6-2. Calculation and disclosure of circulating supply

Several data providers, including Xangle, Token Unlocks, Token Terminal, among others, are already engaged in the crucial task of calculating and disclosing circulating supply, guided by clear objectives. In this pursuit, two fundamental principles stand out: 1) Directness and 2) reliability and real-time availability of data. Directness underscores the frequency and depth of communication with token issuers. While whitepapers typically outline circulating supply plans, the ever-evolving nature of projects often necessitates revisions due to roadmap adjustments, token/mainnet migrations, or security incidents like hacks. Ensuring clear communication and swift disclosure of any alterations is paramount to maintain investor confidence and market transparency. Furthermore, many projects manage token circulation across distinct wallets for investment, marketing, and ecosystem activities. Collaborating closely with projects allows data providers to capture these nuances comprehensively, enhancing investor understanding and trust.

The reliability and real-time aspect of data pertain to the accuracy of circulating supply metrics derived from on-chain sources. To ensure timely data, access to the latest block data from the token issuance network is crucial. Additionally, establishing mechanisms for cross-verification among multiple network nodes enhances data integrity. Moreover, accurate calculation of non-circulating supply requires projects to disclose addresses of reserve wallets they oversee. Hence, the reliability and real-time nature of circulating supply data are intricately intertwined with the directness of communication and collaboration between data providers and project teams.

6-3. On-chain circulating supply monitoring

The assessment of token holder dynamics and transactional histories rests on the decentralized, publicly accessible data stored through blockchain technology. Monitoring on-chain circulating supply isn't about disputing data access rights; rather, it's about the timely aggregation and presentation of information in investor-friendly formats.

For example, our Live Watch service leverages wallet addresses directly provided by projects to calculate on-chain circulating supply. This data is then compared with projected circulation amounts, offering a clear visual representation. Furthermore, established blockchain data providers like Etherscan furnish insights into the holdings and distribution proportions of the top 1,000 holders across ERC networks. Lately, prominent on-chain analytics platforms such as CryptoQuant and DeFiLlama have expanded their offerings to include data relevant to circulating supply. This growing involvement of data institutions underscores the criticality of transparent token circulation management. With more institutions monitoring on-chain circulating supply, investors gain additional access points to information, contributing to a reduction in information asymmetry.

6-4. Additional mechanisms for circulating supply management

While defining and transparently managing circulating supply is crucial, there's also anticipation for exchanges to establish listing and delisting standards based on this metric. Exchanges are poised to construct data pipelines, either directly from projects or through third-party data providers, to receive essential data and enforce compliance with circulating supply plans. This enforcement should encourage projects to disclose relevant information accordingly. Despite the growing sophistication of the crypto market, many investors still rely solely on exchange listings as a signal for investment, often overlooking critical factors. Therefore, it's imperative for exchanges to proactively integrate circulation-related criteria into their listing and delisting procedures, thereby easing the burden on investors.

Furthermore, the roles of institutions providing supplementary information for circulating supply calculations, such as smart contract audits, AML compliance, and forensic analysis, are anticipated to gain increased significance in the crypto space.

7. Final Thoughts

The crypto asset market is still in its nascent stage, yet it's attracting significant investment despite its immaturity. This underscores the urgent need for multi-faceted regulatory interventions to safeguard investors. Crafting and implementing regulations based on a profound comprehension of the entirely novel technology of blockchain poses an understandably formidable challenge. Nevertheless, it's crucial to recognize that we're not entirely devoid of precedents. Insights gleaned from the myriad regulations that have evolved over centuries in traditional financial markets can offer valuable guidance. Specifically, the management systems for free float ratios in stock markets serve as promising examples, particularly in the context of circulating supply. With these insights as our foundation, we anticipate progressing towards a systematic management framework, beginning with the standardization of circulating supply criteria. As information asymmetry diminishes, more investors will likely flock to the market, amplifying the call for a structured approach to circulating supply management. This, in turn, will bolster the regulatory framework in a reinforcing cycle, cementing a more resilient ecosystem.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.