Pendle Finance: Innovating the DeFi Landscape

Translated by Lyne Choi

Table of Contents

1. Introduction: Pendle Finance Positioned to Capture High Yield as LSD War Heats Up

2. Yield Tokenization of Pendle Finance

3. Enhancing Efficiency with the Pendle V2 Update

3-1. Pendle V2 AMM

3-2. vePENDLE Tokenomics

4. Overcoming the Challenges of Yield Trading

5. Closing Thoughts: Pendle Finance Can Enhance DeFi Market Efficiency, but Adoption May Be Limited

5-1. Addressing the Limitations of Existing Protocols via Diversified Asset Offerings

5-2. The Need for Robust Risk Management Products for Building a Sustainable Structure

1. Introduction: Pendle Finance Positioned to Capture High Yield as LSD War Heats Up

In 1Q 2023, LSD services such as Lido, Rocket Pool, and Frax Finance garnered significant market attention ahead of the Ethereum Shanghai update scheduled for April. Liquid Staking Derivatives (LSDs) are services that facilitate the securitization of native assets on Proof-of-Stake-based blockchain networks (refer to the Xangle Original article, “Liquid Staking Competition Set to Heat Up After Shanghai Update”).

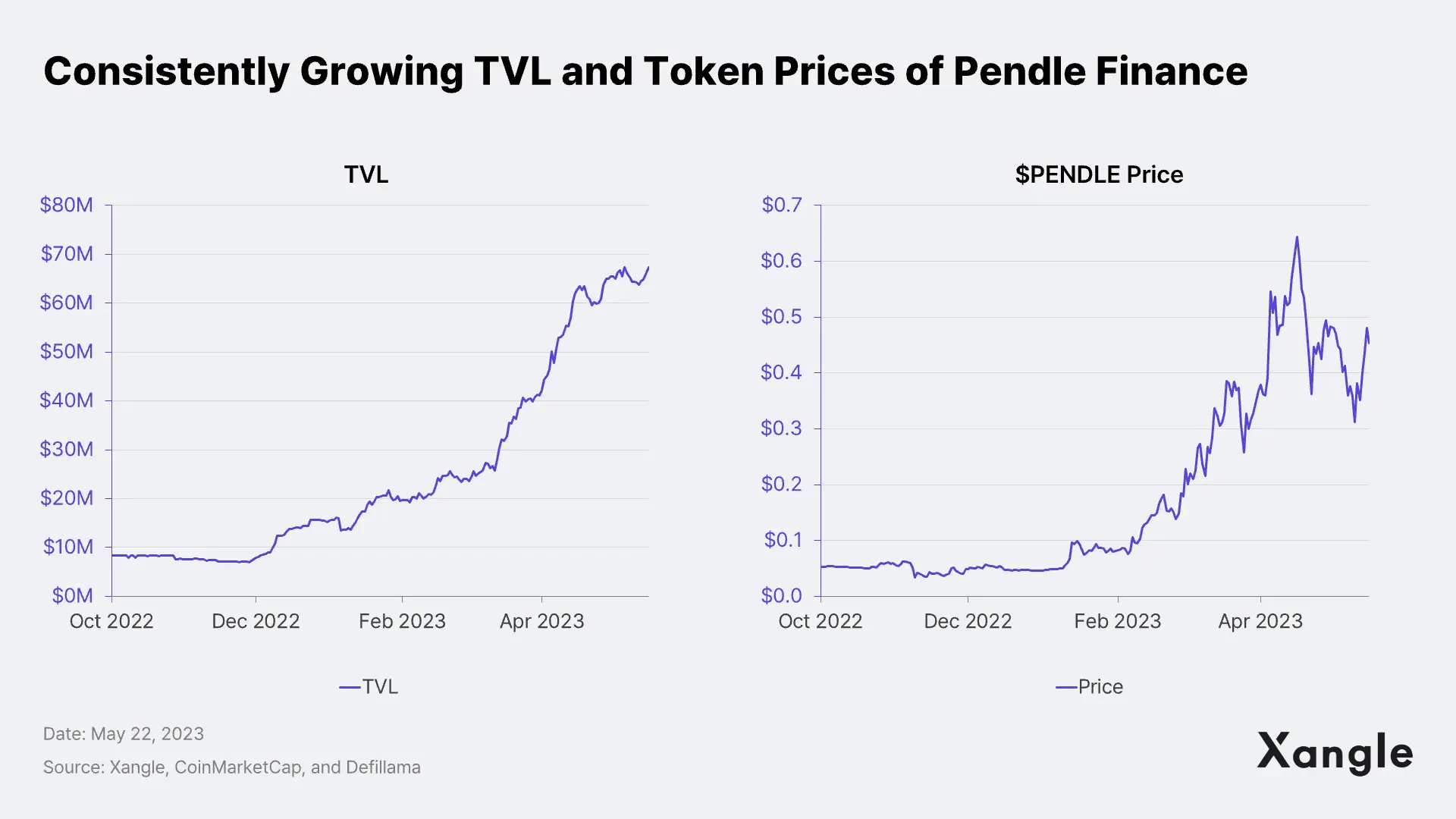

Within the framework of the LSD narrative, several DeFi projects utilizing LSD assets have captured market attention, and Pendle Finance is among them. On Nov 29, 2022, Pendle Finance launched Pendle V2 and witnessed consistent capital inflows up until mid-April. Since the V2 launch, the project has achieved a Total Value Locked (TVL) of approximately $67M, with the token price performing exceptionally well, rising over 1,000%. Also known as LSD-FI, Pendle Finance has been able to capitalize on the LSD narrative and experience significant growth. Now, let's delve into the services it offers.

2. Yield Tokenization of Pendle Finance

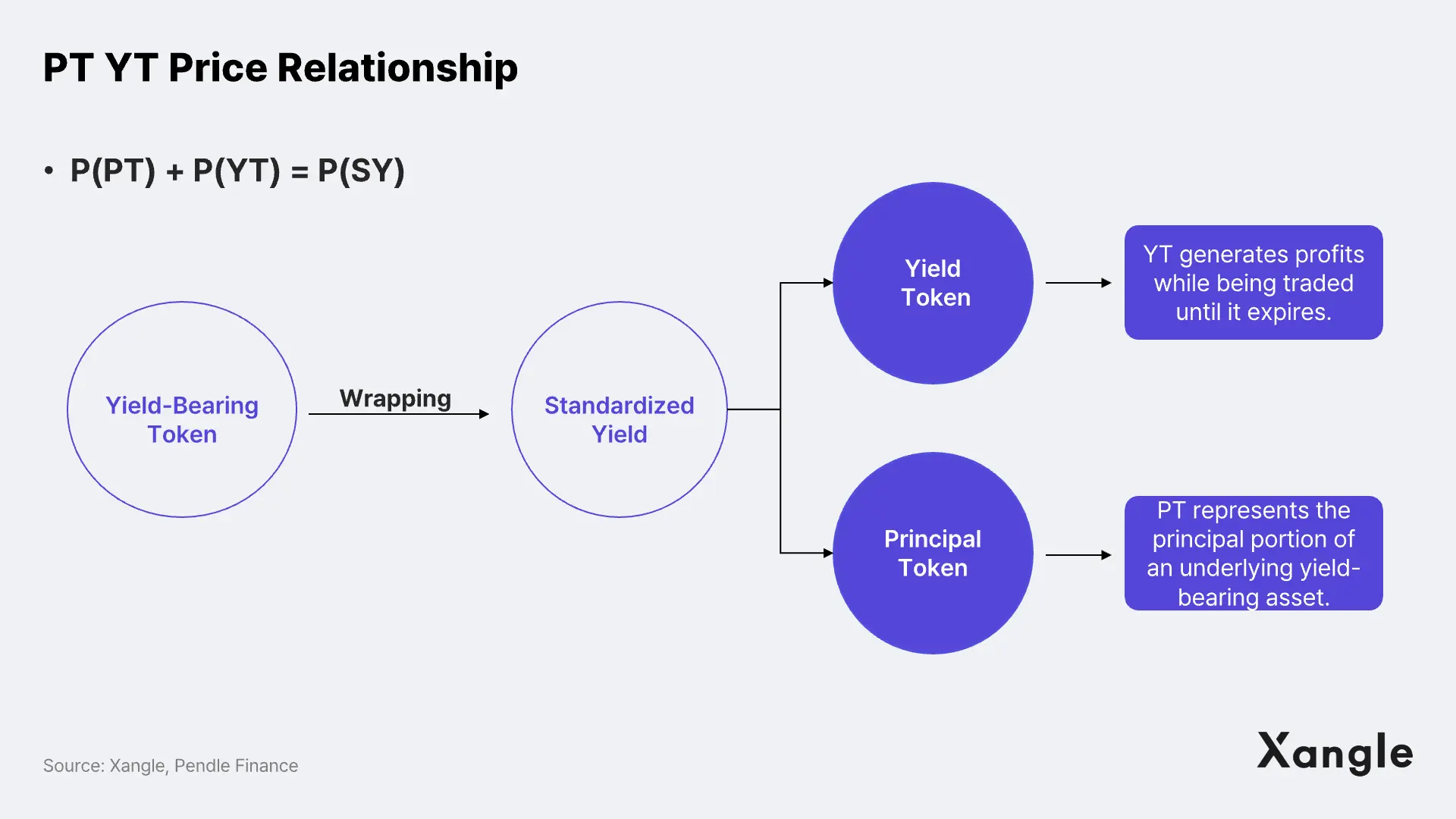

Pendle Finance is a unique form of DeFi protocol that tokenizes yields separated from LSD tokens (which provide staking rewards) or Yield-Bearing Tokens (YBTokens) and supports trading of those yield tokens.

To separate yield from YBTokens, which were generated using different mechanisms, Pendle wraps YBTokens into Standardized Yield (SY). YBTokens like stETH, FRXETH, and GLP generate yield through different protocols and structures. This poses a challenge of manually integrating YBTokens when they are utilized on a protocol other than their native one. To address this issue, Pendle Finance proposes SY as a standard (EIP-5115), which bundles YBTokens with diverse mechanisms into a unified interface.

By employing the wrapped SY, Pendle Finance can issue two types of tokens: Principal Tokens (PT) and Yield Tokens (YT). PT represents the principal amount of the YBToken and grants the right to redeem an equivalent number of YBTokens upon maturity. On the other hand, YT represents the interest accrued on YBTokens from the present time until maturity. This structure resembles a strip bond that separates the bond's principal and interest, making it more appealing for investment. In this context, PT can be likened to a zero-coupon bond, while YT corresponds to the interest portion detached from the bond.

Given that PT represents the detachment of interest from an interest-generating asset, its price is always equivalent to the price of SY minus the price of YT. This relationship leads to the following price equation.

As an illustration, let's consider the scenario where you stake 100 DAI in Compound for three months. After the three-month period, you would receive 1 DAI and 0.5 COMP as interest. Using Pendle Finance, user has the option to wrap the initially staked 100 cDAI of YBTokens in SY, allowing them to mint 100 PT cDAI and 100 YT cDAI, respectively. In this case, PT holders have the right to redeem their 100 PT cDAI tokens upon expiration, receiving 100 DAI in return. On the other hand, YT holders will receive 1 DAI and 0.5 COMP in interest until the maturity of the tokens. Suppose the price of 1 PT cDAI is $0.95 at the time of minting. Consequently, the price of 1 YT cDAI would be $0.05.

3. Enhancing Efficiency with the Pendle V2 Update

Pendle Finance has been facilitating the trading of PT and YT tokens through its automated market maker (AMM). To further enhance trading efficiency and bolster the protocol's value, Pendle V2 was introduced in November. This update encompassed two key aspects: 1) enhancements to the Pendle V2 AMM and 2) improvements to tokenomics through the introduction of the ve(3, 3) model. Let's delve into the components of the Pendle V2 update that contributed to the growth of Pendle Finance.

3-1. Pendle V2 AMM

1. Improved Capital Efficiency with 1 Pool, 2 Markets

In the earlier version, Pendle V1, separate pools (SY-PT Pool and SY-YT Pool) were required for trading PT and YT tokens. Consequently, despite issuing PT and YT assets through SY, Pendle V1 encountered liquidity fragmentation, as liquidity had to be provided to both pools individually to facilitate the trading of the two assets. To address this issue, Pendle V2 AMM leverages flash swaps, ensuring that only one pool of SY-PT pairs is necessary for trading both PT and YT tokens.

This enhancement allows liquidity providers to consolidate previously fragmented liquidity into a single pool, where they can provide liquidity while earning fees from two markets: PT and YT. Furthermore, the high correlation between the assets deposited in the pool helps minimize impermanent losses. Similar to how the price of a zero-coupon bond approaches its face value as it nears maturity, the price of PT also converges to the price of SY as it approaches maturity. Consequently, even if temporary losses are incurred due to fluctuations in the price of PT, holding it until maturity and allowing the price to converge to the price of SY will eliminate those impermanent losses.

Additionally, traders dealing with PT and YT will benefit from lower swap costs and increased liquidity. In the following example, the purchase of YT is executed from a single pool, specifically the SY-PT Pool.

Buying YT-aUSDC

- Buyer sends aUSDC into the swap contract (auto-routed from any major token)

- Contract borrows more aUSDC from the pool

- Mint PT-aUSDC and YT-aUSDC from all of the aUSDC

- Send the YTs to the buyer

- The PTs are sold for aUSDC to repay the loan from step 2

Concentrated Liquidity with Low Interest Volatility

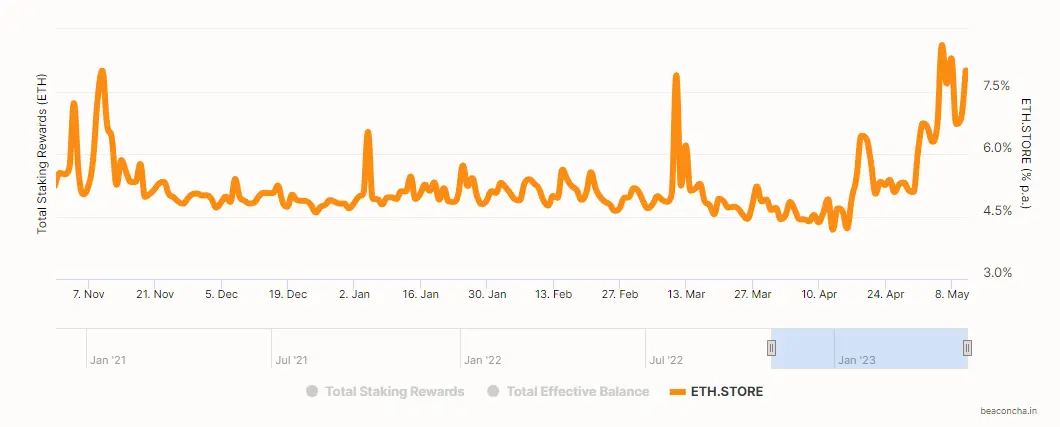

In general, the interest volatility of YBTokens tends to have a narrower range compared to the price volatility of YBTokens. This makes it relatively easier to predict the upper and lower bounds of the interest rates. For instance, Ethereum staking yields have fluctuated within a range of approximately 4-9% over the past six months. By understanding the approximate interest volatility of an asset, liquidity can be concentrated within that range, enabling larger transactions with lower slippage.

Change in Ethereum staking reward rate over the last 6 months, Source: Beaconcha.in

3-2. vePENDLE Tokenomics

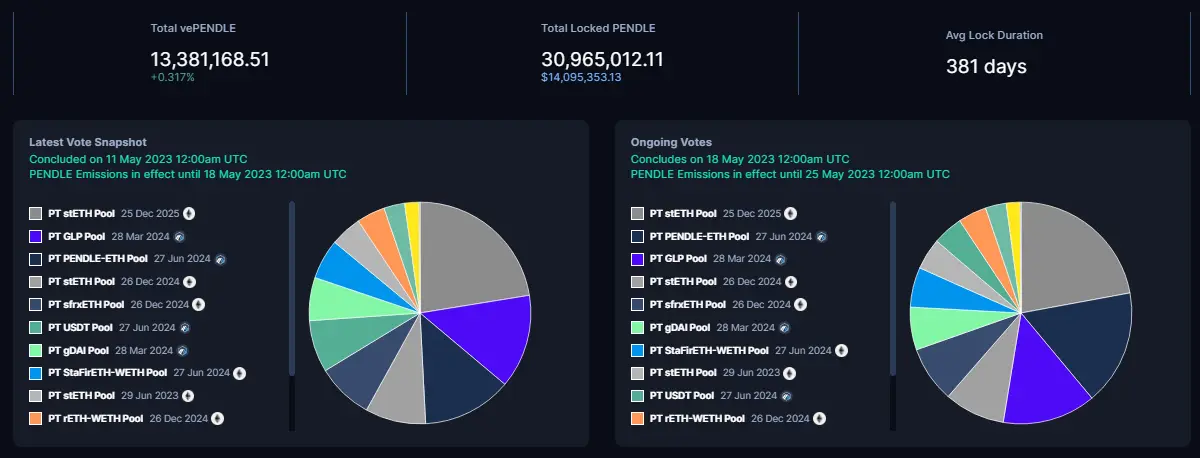

As part of the V2 update, Pendle Finance introduced the ve(3,3) model with $vePENDLE (Vote-escrowed PENDLE) tokens, which are utilized for governance voting. This model aims to reduce the supply of $PENDLE tokens, stabilize token prices, and improve the overall stability of the protocol. Users are rewarded with $vePENDLE tokens for locking up $PENDLE tokens on the platform. The staking period for the tokens can range from one week to two years, and the lockup period determines the size of the $vePENDLE reward. Holders of $vePENDLE tokens can participate in a weekly community vote to increase LP rewards for their preferred pools.

vePENDLE Vote Snapshot, Source: Pendle Finance

Users who hold $vePENDLE tokens can also benefit from a share of the platform's revenue, which is derived from the following sources:

- 3% fees from the yield accrued by YT, all directed to $vePENDLE.

- The yield from matured, unredeemed PTs will be collected by the protocol in stablecoins as its revenue stream.

- Swap fees of 10bps (on 1 year-to-maturity products) are dynamically adjusted over time, 80% belongs to $vePENDLE holders.

With this structure, Pendle Finance aims to mitigate token depreciation by incentivizing liquidity providers to lock their received $PENDLE rewards within the protocol. This way, they can earn additional rewards over time.

4. Overcoming the Challenges of Yield Trading

Addressing the complexities involved in yield trading is crucial for users looking to engage in PT and YT trading on Pendle Finance. In this section, we will explore the yield trading strategy on Pendle Finance using a few examples. Before delving into the trading strategy, it is important to understand the distinction between two key interest rates utilized by Pendle Finance: the Underlying APY (U-APY) and the Implied APY (I-APY). The U-APY represents the 7-day moving average of the YBToken underlying PT and YT. On the other hand, the I-APY reflects the market consensus on the future APY, which is determined based on the trading activities of market participants within Pendle's PT and YT markets. The variance between these two rates significantly influences an investor's investment approach and strategy.

When U-APY > I-APY

- Let's consider a scenario where SY-stETH has a U-APY of 5% and an I-APY of 4.5%. If an investor believes that the current market has undervalued the APY of stETH and expects the I-APY to rise to 5% in the future, they would perceive PT as currently overvalued and YT as undervalued. In this case, if the investor holds PT, it presents an opportunity to sell the overvalued PT and acquire more of the undervalued YT.

When U-APY < I-APY

- Conversely, let's suppose SY-stETH has a U-APY of 5% and an I-APY of 5.5%. The investor perceives that the APY of stETH is overvalued in the current market and believes that the appropriate I-APY should be 5.3%. In this situation, if the investor purchases PT with a 5.5% interest rate and holds it until maturity, they will receive a 5.5% interest rate, which is higher than the 5.3% interest rate they consider fair.

This investment approach, based on predicting I-APY, bears similarities to interest rate swaps in traditional markets. An interest rate swap involves a derivative contract where two parties agree to exchange interest payments at regular intervals until a predetermined future maturity date. While there are various types of interest rate swaps, the standard interest rate swap is the most common, where one party pays a fixed rate while the other pays a floating rate. Pendle's yield trading can be likened to a standard interest rate swap, where an investor receiving a fixed interest rate of 4.5% in the U-APY > I-APY example mentioned earlier enters into an interest rate swap with an investor anticipating rising interest rates by investing in a floating rate asset.

Successful yield trading necessitates accurate predictions of the appropriate I-APY level. This requires not only a strong comprehension of the DeFi ecosystem but also a basic understanding of interest rate swaps, which aim to convert a floating rate into a fixed rate based on interest rate forecasts in traditional markets. For the average retail investor, these prerequisites may serve as barriers to entry into Pendle Finance. Some retail investors might not be drawn to Pendle Finance due to the more sophisticated nature of yield trading and the availability of other intuitively comprehensible alternatives for speculating on the price movements of specific assets.

5. Closing Thoughts: Pendle Finance Can Enhance DeFi Market Efficiency, but Adoption May Be Limited

5-1. Addressing the Limitations of Existing Protocols via Diversified Asset Offerings

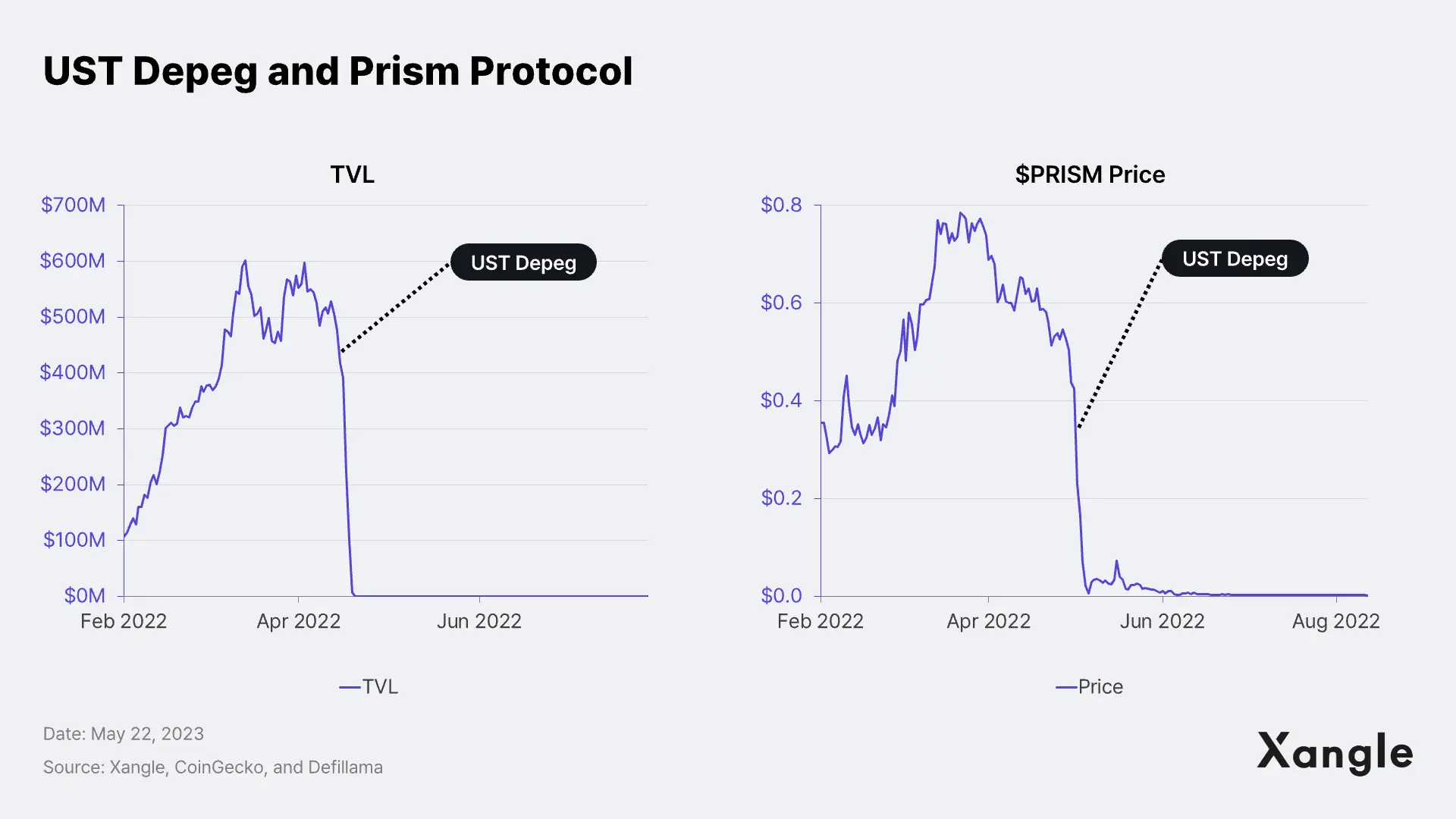

Pendle Finance introduces a unique concept of yield trading through yield tokenization. However, it is worth noting that Pendle Finance is not the first protocol to tokenize yields and enable trading based on yield-bearing assets. Prism Protocol was an earlier attempt at yield tokenization, specifically with the high-yielding asset $LUNA, which attracted a TVL of up to $600M within a short period. However, Prism Protocol's reliance on a single asset, $LUNA, proved detrimental when the UST de-pegging event resulted in $LUNA's decline, ultimately leading to the collapse of the protocol.

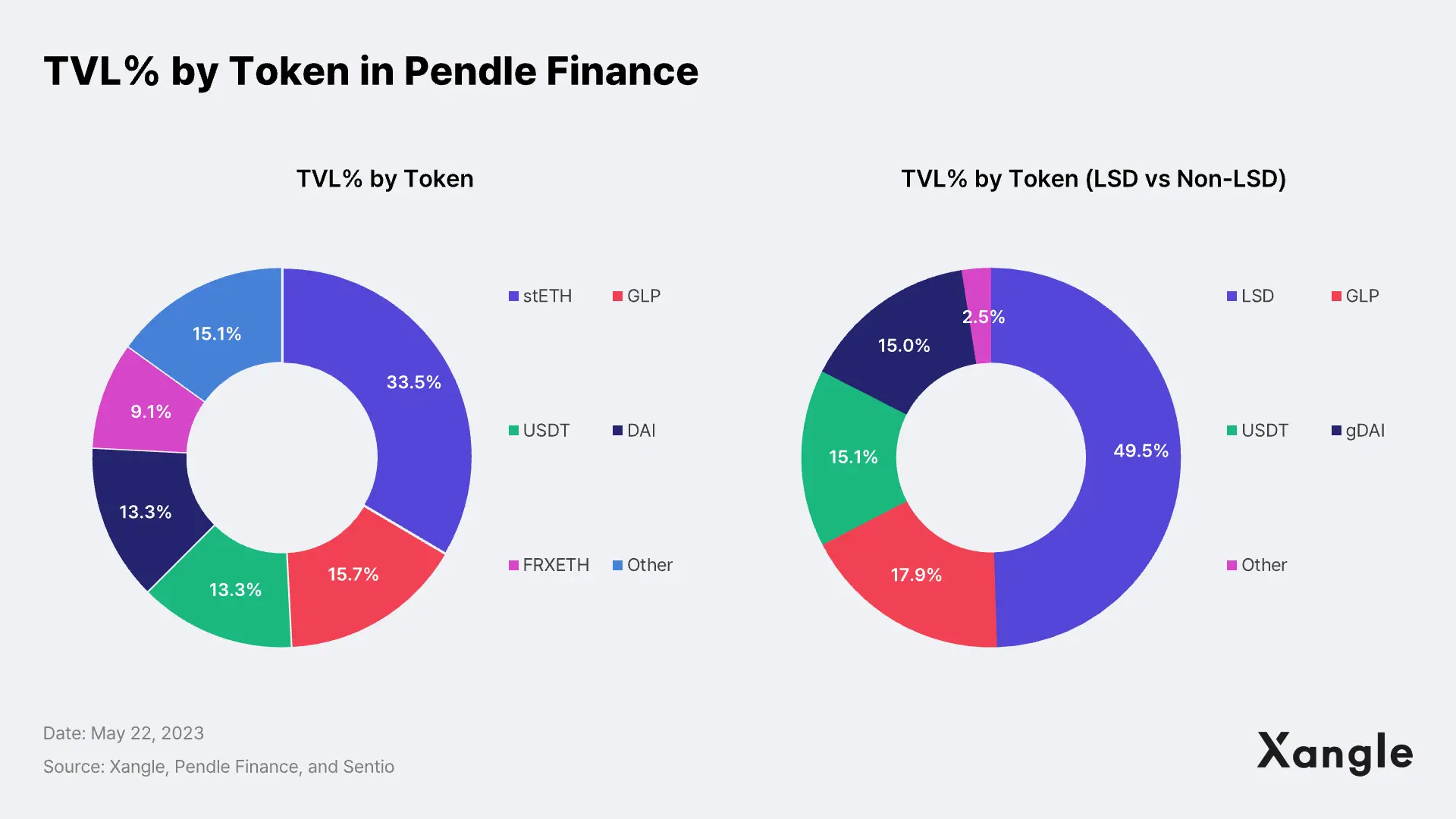

Reflecting on the case of Prism Protocol, which operated with a single yielding asset, $LUNA, Pendle Finance demonstrates a much more diverse and stable portfolio of yielding assets. The range of assets handled by Pendle Finance includes LSD tokens, which provide Ethereum staking rewards, as well as Real Elder assets like GLP and gDAI, distributing yields based on actual protocol revenue. These assets are expected to contribute to the provision of stable services in the future.

5-2. The Need for Robust Risk Management Products for Building a Sustainable Structure

Yet, there are doubts about whether Pendle's yield trading can generate consistent and steady demand. In the traditional market, interest rate swaps emerged in the 1970s to address the need of financial institutions to manage and hedge their interest rate risk, which has grown alongside increasing interest rate volatility. Interest rate swaps, typically traded over-the-counter (OTC), can be tailored to meet the specific requirements of buyers, effectively fulfilling the demand for risk management and experiencing substantial growth as a result. In essence, interest rate swaps can be seen as a response to the necessity of mitigating the risk associated with interest rate volatility, in addition to the inherent speculative nature of investing based on interest rate predictions.

As previously mentioned, yield trading bears similarities to the interest rate swap market. However, the effectiveness of yield trading in providing interest rate risk hedging to DeFi investors appears to be more limited compared to traditional markets. The high demand for interest rate swaps is mainly driven by their execution in the OTC market, where counterparties have the ability to define the terms and conditions of the transaction, making them more effective in managing risk than other hedging instruments within the OTC market. On the other hand, yield trading is expected to be considerably less effective in risk management as it relies on strategizing based on the fluctuation of I-APY within a confined pool (SY-PT). In other words, while the current yield trading may attract investors from an investment perspective through interest rate prediction, it is unlikely to generate significant demand from a risk management standpoint, which has been the primary driver of interest rate swap demand in the traditional market.

Pendle Finance has effectively secured yield-providing assets like LSD tokens for Ethereum staking rewards and GLP and gDAI for Real Yield, setting it apart from Prism Protocol's offering. However, for Pendle Finance to truly succeed in the DeFi ecosystem, it must expand its scope beyond mere long and short investments based on interest rate predictions. It needs to provide investors with the risk management advantages of traditional interest rate swaps. Failure to do so may hinder yield trading from gaining an advantage over other DeFi protocols, considering its inherent complexity. It remains intriguing to witness whether Pendle Finance can transcend traditional trading and deliver effective interest rate risk management benefits to its users.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.