FTX Crash: What is in the Crypto Bill Backed by FTX’s Founder?

Translated by LC

Table of Contents

1. Introduction

2. What is the DCCPA Bill?

3. Issues

4. SBF's Suggestions

5. CZ's Position

6. The Core Principle of Crypto Regulation

6-1. A Comprehensive Crypto Taxonomy Integrating TradFi and Crypto Assets

6-2. Clear Distinction and Understanding of TradFi and DeFi

6-3. Mandatory Disclosure of Crypto Assets

7. Closing Thoughts

1. Introduction

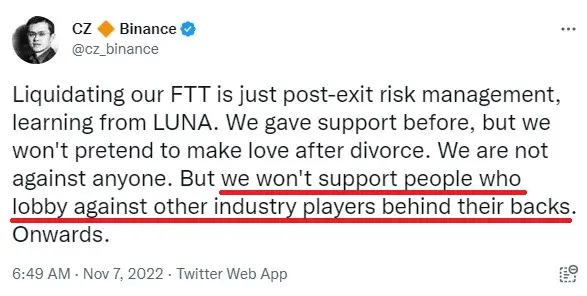

FTX suffered the cryptocurrency equivalent of a bank run that ended up causing price falls in the overall crypto market. The drama started when Binance CEO Changpeng Zhao (CZ) said he would liquidate all of Binance’s FTT tokens (the native token of FTX), $500M equivalent in cash (for complementary reading, refer to “related articles” at the end of this article). In a tweet, CZ explained the FTT liquidation was “just post-exit risk management,” adding, “we won’t support people who lobby against other industry players behind their backs.” CZ’s tweet seemed aimed at FTX CEO Sam Bankman-Fried (SBF). What were SBF’s lobbying efforts targeting, and what is the direction of cryptocurrency regulation? To answer these questions, we need to take a look at the Digital Commodities Consumer Protection Act (DCCPA) bill, a.k.a. “DeFi Killer” bill.

The DCCPA bill was officially introduced to the U.S. Congress in Aug 2022 to amend the Commodity Exchange Act (CEA) to grant the Commodity Futures Trading Commission (CFTC) exclusive jurisdiction over digital commodity markets. The DCCPA bill is understood to have been in favor of CeFi over DeFi, and SBF aggravated the controversy surrounding the bill by being a vocal proponent of it.

At this point, we can only speculate as to why CZ, who leads the largest CeFi company globally, was complaining about SBF’s lobbying tactics. Nonetheless, it became apparent that the FTX crisis will further accelerate the introduction of cryptocurrency regulations to protect investors. Taking advantage of the absence of regulations, many crypto asset operators have been negligent, and the damage to investors has grown out of control. On this account, transparent and strong regulatory guardrails are needed for the crypto industry. Furthermore, the crypto community collectively has a role in seeking a constructive middle ground rather than just emphasizing its value of operating with no central authorities involved. In this regard, the Xangle research team would like to propose three key principles regulators should consider when introducing cryptocurrency regulations.

2. What is the DCCPA Bill?

On Aug 3, 2022, Senate Agriculture Committee Chairwoman Debbie Stabenow and John Boozman, the top Republican on the committee, introduced a bipartisan bill aimed at regulating crypto assets. The DCCPA is narrower than the Responsible Financial Innovation Act (RFIA), proposed by Senators Cynthia Lummis and Kirsten Gillibrand, as it is more focused on crypto spot markets were Bitcoin, Ethereum, and other cryptocurrencies and digital assets trade.

The Senate’s attempt to amend the CEA through the DCCPA is intended to strengthen supervisory authority while minimizing controversy over the legal interpretation by clearly defining digital commodities and entities that facilitate trading in digital commodities over which the CFTC has jurisdiction. In Sep 2022, the CFTC issued an order settling charges against bZeroX and penalizing the protocol for illegally operating an organization that offered leveraged and margin trading of digital assets and simultaneously filed suit against Ooki DAO for violating the same laws. The CFTC alleged that bZeroX offered margined and leveraged digital asset trading on unregistered exchanges. The case indicates that CFTC already has legal grounds to penalize and monitor illegal activities of digital asset platforms without the DCCPA. If the DCCPA passes into law, it will grant the CFTC an extension of regulatory powers over the sector.

The DCCPA is currently undergoing a mark-up based on hearings by the Senate’s Committee on Agriculture, Nutrition, and Forestry and the Senate’s Committee on Banking, Housing, and Urban Affairs. The latest draft copy of the DCCPA bill was made public by Gabriel Shapiro, general counsel of Delphi Labs. The regulatory requirements outlined in the draft bill are the following:

- The Commodity Exchange Act is amended to provide the CFTC jurisdiction with respect to, any account, agreement, contract, or transaction involving a digital commodity trade.

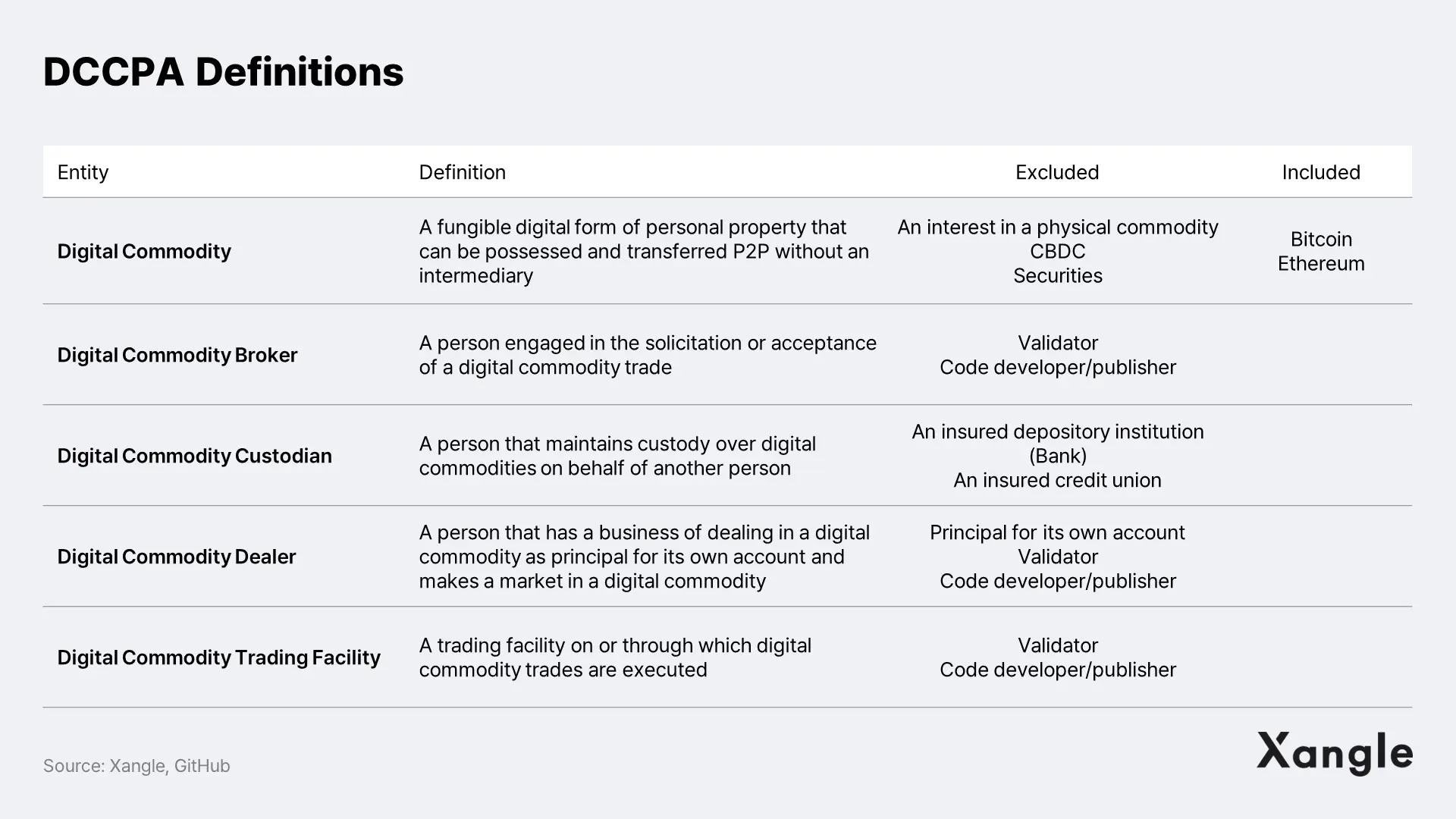

- The term “digital commodity” means a fungible digital form of personal property that can be possessed and transferred person-to-person without necessary reliance on an intermediary.

- The term “digital commodity” includes property commonly known as cryptocurrency, such as Bitcoin and Ether.

- The term “digital commodity platform” means a person that is a digital commodity broker, custodian, dealer, and trading facility and shall comply with CFTC’s registration requirements.

- The term “digital commodity trading facility” means a trading facility on or through which digital commodity trades are executed.

- The term “digital commodity trading facility” does not include a person solely because that person validates digital commodity transactions or develops or publishes software.

- The digital commodity platform shall disclose to the CFTC information concerning price, trading volume, and other trading data on digital commodities.

- The CFTC shall make, promulgate, and enforce such rules governing margined or leveraged trading.

- After the listing of a contract for a digital commodity has taken effect, the CFTC may require the delisting of the contract or disapprove the listing.

- With respect to a digital commodity that purports to have a fixed value, meaning stablecoins, the CFTC may disapprove the issuer of the digital commodity, the collateral or reserves backing the digital commodity, and the terms by which the issuer will redeem the digital commodity.

- The CFTC shall assess and collect fees on digital commodity platforms.

The draft version of the DCCPA bill is drawing heavy criticism from crypto communities. Let's look at some of the debated issues in the bill.

3. Issues

Firstly, the definition of "digital commodities" is still unclear. Not only that – no specific guidelines were presented to classify them as "digital commodities." Although Bitcoin and Ethereum are classified as "digital commodities," even that has not been agreed upon between SEC and CFTC.

While the SEC claims that the Howey test can determine if a cryptocurrency is a security, it has never disclosed a list of security tokens that passed the test, and SEC's lawsuit against Ripple Labs, which could provide a clue, has been ongoing for nearly two years. Shapeshift CEO Erik Voorhees responded to SEC's lawsuit with cynicism, saying, "the SEC enforces where it thinks it can easily win, and absolves itself of any proactive definitions, relying on an 80-year old rule about Florida orange groves to govern a global multi-trillion dollar industry of diverse and evolving digital assets" – a quote of which demonstrates the side effects of imposing regulations of traditional finance to rather technically complex digital assets. It has been well over 10 years since the Bitcoin genesis block was created; however, the reality is that neither the SEC, SFTC, nor the court has been able to present a clear digital asset classification system.

However, a comprehensive crypto taxonomy shall be established to integrate traditional finance and crypto assets before introducing regulations. Without clear classification frameworks, it is difficult to determine which agency has the authority to supervise which virtual assets, let alone the detailed rules.

Secondly, a DEX is highly likely to be included in the category of "digital commodity trading facility," – which is broadly defined as "a trading facility on or through which digital commodity trades are executed," but the term does not explain the distinction between CEX (involves a central authority or third party) and DEX (depends on smart contract technology to exchange assets). As a result, DEXs are likely to be subject to numerous compliance obligations, starting with CFTC registration requirements.

Under the Bank Secrecy Act (BSA), the Commodity Futures Trading Commission (CFTC) requires financial institutions to implement reasonable customer identification procedures (CIP) for verifying the identity of any person seeking to open an account, meaning DEXs registered with the CFTC must perform KYC due diligence on its users. In other words, financial authorities will have control over individual access to financial services, which goes against DeFi's core philosophy of improving access to various financial services. It also hinders the development of the DeFi ecosystem in practical terms. Furthermore, acquiring and operating the CFTC's license incurs considerable costs (for audits and operating the internal compliance team), posing a significant burden for projects that large funds do not back. Not only that, the CFTC registration process takes several months prior to launching a project, which greatly undermines the timeliness and competitiveness of the product.

Thirdly, the DCCPA authorizes the CFTC to impose arbitrary fees on platforms to carry out licensing and oversight activities. The problem is that it is highly likely that the project will not be able to afford to pay additional fees because compliance costs have already been incurred, and in that case, these fees will inevitably be passed on to end users. Most of DeFi's advantage is attributable to not having a central authority or a third party, but the such advantage will no longer be applicable. // forces projects to sacrifice decentralization // DEXs aim to complete transactions more quickly and cheaply than their centralized counterparts. They do this by cutting out the intermediary entities that take a cut of transaction fees on CEXs.

Most concerning of all is the lawmakers' lack of understanding of blockchain technology, as seen in some of the definitions of the "digital commodity trading facility." For example, the bill describes that "a digital commodity trading facility shall make public timely information on price, trading volume, and other trading data on digital commodities to the extent prescribed by the Commission," however, all DEX interactions happen on-chain and are transparently kept and disclosed on a ledger. The bill also states that "a digital commodity platform shall hold customer property in a manner that minimizes the risk of loss of, or unreasonable delay in access to, the customer property," but this is only applicable to CEXs that involve central authorities or intermediaries in operation, not to DEXs on which users retain full control of their wallets. Against this backdrop, the bill is sparking intense debate as it is written by lawmakers with a lack of awareness of blockchain technology and aims to apply a regulatory framework similar to traditional finance.

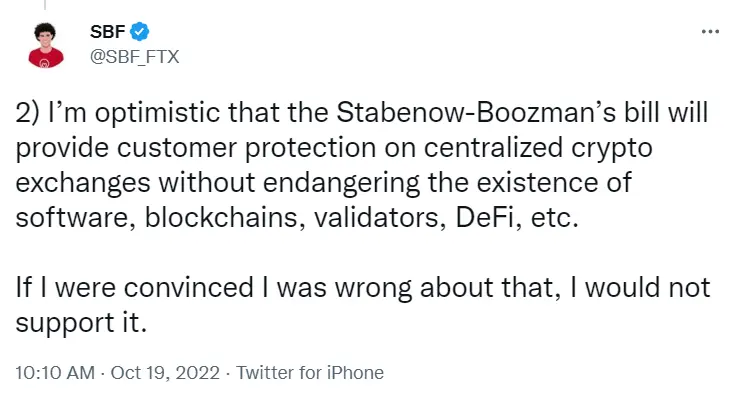

Nevertheless, SBF was a vocal supporter of the DCCPA bill and had been lobbying federal lawmakers to pass crypto-friendly regulations. SBF then went on to propose the Possible Digital Asset Industry Standards to “create clarity and protect customers,” but the response to the proposal has been significantly negative as it reads like a very traditional finance regulatory structure which could be interpreted as a ban on DeFi.

4. SBF's Suggestions

The DeFi/crypto investigative journalism rekt.news wrote, “SBF and Alameda have had deep enough pockets to bleed many protocols dry through DeFi’s wild west period, and now they want to stifle innovation for the rest of us,” criticizing SBF’s proposal strongly. SBF’s proposal was widely panned on social media, including an opposing statement posted by ShapeShift CEO Erik Voorhees. Let’s break down SBF’s proposals, especially the highly debated ones: “Sanctions, allowlists, and blocklists” and “DeFi.”

First, SBF proposes that while the Office of Foreign Asset Control (OFAC) maintains on-chain sanctions lists, there should be an on-chain list of the sanctioned addresses that include not only the blocklists but also the entire list of addresses that transferred funds to or accepted funds from the sanctioned addresses.

OFAC is a department within the U.S. Treasury, and they maintain a very specific blacklist of “sanctioned entities,” such as terrorists and narcotics traffickers. OFAC has the authority to enforce economic sanctions to prevent financial transactions in which U.S. persons may not engage unless authorized by OFAC. Under OFAC’s sanction program, essentially all interactions with comprehensively sanctioned countries, such as Cuba and Iran. In this context, SBF proposing to “respect OFAC’s sanctions lists” and delegating the authority to OFAC to maintain the on-chain blacklist is an act against those who advocate for an open and free economy and discrimination against millions of those who are financially underprivileged.

In Aug 2022, the OFAC sanctioned the Ethereum mixer Tornado Cash, adding it to the Specially Designated Nationals (SDN) List, pointing to Tornado's role in laundering millions worth of cryptocurrency stolen by the North Korea-affiliated hacking organization Lazarus Group. The fact that they prohibit certain protocols just because some malicious users' wallet addresses and transactions have occurred and that these sanctions activities can be used for political purposes has created strong hostility toward OFAC. Even if OFAC's blacklist becomes a reality, it is unclear whether it will technically enforce applicable sanctions. Still, it cannot be denied that when combined with the DCCPA bill, which seeks to bring several DeFi protocols under the CFTC's jurisdiction, it is a fairly threatening proposal for the DeFi ecosystem.

Second, SBF advocates that individuals that host centralized GUIs (Graphic User Interface), which allow one to access DeFi protocols, should be "licensed."

- You don't need a financial license to upload the DeFi application code to the blockchain.

- Validators should remain permissionless and free.

- However, the following activities would potentially require licenses: i) Those who actively provide a front-end GUI that encourages and facilitates US retail investors to trade on decentralized protocols, and ii) those who are actively marketing DeFi products to retail investors.

The front-end GUI refers to a window for accessing DeFi applications such as Uniswap (app.uniswap.org) and Curve Finance (curve.fi), and SBF is fact suggesting that virtually all DeFi applications should obtain licenses to operate. If such a proposal is implemented, only the individuals who can query codes directly on the blockchain (those with programming knowledge) without the help of a GUI will be free to use DeFi applications, while the rest will have to use DeFi services through GUIs registered and licensed with the financial authorities. If regulations require KYC to use such interfaces, this will result in breaking away from DeFi's value of free access to financial services and reverting control over financial activities to centralized authorities. The imposed fees by CFTC will also add a burden on users.

According to SBF, the front-end GUIs are hosted through centralized cloud services (e.g., AWS, Azure), and service fees are also paid through a centralized payment system, indicating that DeFi applications are already under the jurisdiction of regulators. He believes a reasonable compromise is necessary to ensure the freedom of validators and code developers, which he values most.

SBF's proposal cannot be regarded as mere personal thoughts of a stubborn businessman because his words and actions carry weight in Capitol Hill. SBF is a major political donor – he spent over $40M supporting political figures, including Senator Kirsten Gilibrand, who introduced the Responsible Financial Innovation Act (RFIA), and Debbi Stabenow, who introduced DCCPA. It is no coincidence that both Senators introduced bills in favor of FTX and CEX.

5. CZ's Position

There are several reasons why CZ criticized SBF’s lobbying activities.

First, CZ has no connections in Washington, as he is based in China and Canada. SBF, on the other hand, has been actively engaged in lobbying in U.S. policy circles, maintaining close ties with politicians who are key players in enacting crypto-related bills. CZ must have been concerned that the bill would work in favor of FTX and be unfavorable to rival CEXs such as Binance, as SBF had built exclusive ties with the U.S. policymakers.

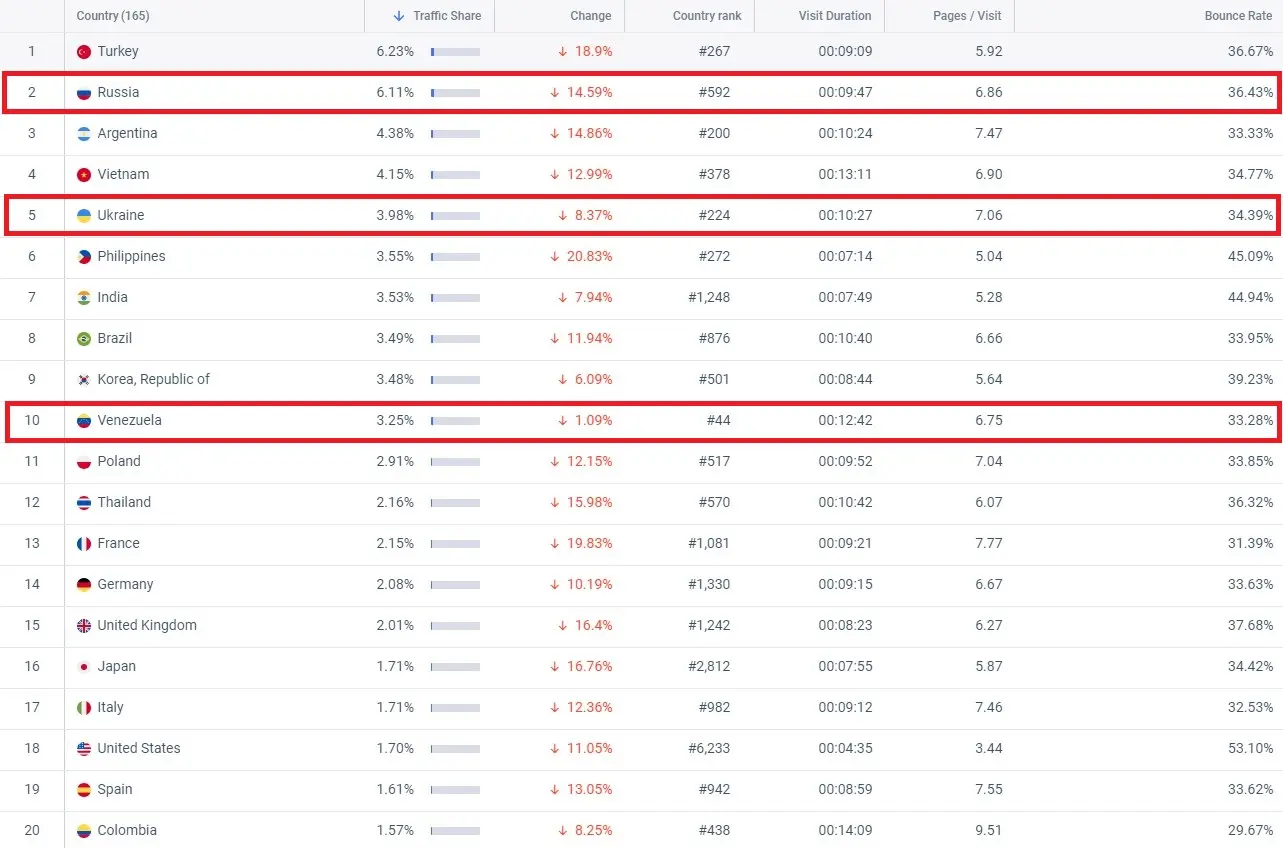

CZ’s concerns are backed by the fact that SBF supports OFAC’s sanctions lists. Based on the number of visitors to the Binance website, Russia, Ukraine (Crimea, Donetsk, Luhansk), and Venezuela rank 2nd, 5th, and 10th, respectively, but they are all on OFAC’s sanctions lists. In other words, Binance will instantly lose over 10% of its total traffic if OFAC manages the blacklist, potentially causing Binance to lose its market share as it has a large user base in emerging countries that conflict with the U.S., such as Turkey.

Source: similarweb

Second, Binance operates a mainnet called the Binance Smart Chain (BSC). CZ predicts that the crypto exchange market will move from CEX to DEX within the next few years and dreams of BSC taking over the hegemony of the DEX market (see related Xangle Research articles for more information). There is no doubt that CZ was not happy with SBF openly supporting the DCCPA bill, which contains provisions against DeFi, especially DEXs.

6. The Core Principle of Crypto Regulation

The ideological conflict and lack of regulation surrounding the DCCPA bill eventually resulted in the downfall of FTX. Now that FTX is in ruins, policymakers are tasked with introducing a stricter bill. Introducing a crypto bill has become inevitable. While insisting on a very traditional finance regulatory structure would be problematic, blindly pushing the principle of decentralization and non-intervention is not helpful in establishing the proper regulation. In this context, here are three key principles essential for the introduction of crypto regulations:

- A comprehensive crypto taxonomy integrating TradFi and crypto assets

- Clear distinction and understanding of TradFi and DeFi

- Mandatory disclosure of crypto assets

6-1. A Comprehensive Crypto Taxonomy Integrating TradFi and Crypto Assets

A detailed taxonomy that classifies crypto assets necessitates an international standard. The taxonomy of crypto assets found in pending bills is currently different by country – which significantly reduces the predictability of regulation from the perspective of ecosystem participants, including issuers/distributors, exchange platforms, and investors. To minimize confusion, a standardized taxonomy should be in place internationally, even if details of crypto regulations for each category may vary from country to country.

For example, suppose that crypto assets X are classified differently as stablecoins in Country A and commodities in Country B. Suppose Country A requires a regular audit of collateral assets while Country B does not. In that case, there will be no incentive for the issuer/distributor to comply with the audit and other strict regulations to list X in Country A. For this reason, projects will only list their assets with fewer regulatory requirements, as complying with regulations that differ by country is time-consuming and costly. Ultimately, the advantage of crypto assets that can be exchanged freely across borders will be virtually invalid.

Regulators also need reliable and consistent access to crypto assets that are distributed without borders to analyze market risks related to crypto assets and protect investors. Without a standardized international taxonomy, collecting data will be challenging.

Meanwhile, TradFi is already executing various global taxonomies. More than 150 countries classify financial assets according to the International Financial Reporting Standards (IFRS), and many exchanges around the world use the Global Industry Classification Standard (GICS) or ICB (Industry Classification Benchmark) to classify the sectors of listed companies. Establishing a unified taxonomy, the lowest common denominator of regulation, is a way to increase regulation's predictability and facilitate cross-border cooperation.

The crypto asset taxonomy should be set based on an applicable framework (i.e., the Howey Test for determining whether a certain asset can be classified as a security) at a practical level that takes into account the technical characteristics of the blockchain and should be mutually exclusive with no overlapping assets for each classification. A list of crypto assets by classification should also be presented by each regulator or by the Standard Setting Bodies (SSB).

Taxonomy for crypto assets should:

- Be based on a framework that can be applied at the practical level

- Be mutually exclusive with no overlapping assets for each classification

- Present a list of crypto assets with clear classification by global standard-setting institutions

6-2. Clear Distinction and Understanding of TradFi and DeFi

To establish a global taxonomy, TradFi and Defi must be distinguished.

A research report released by the European Commission (EC) at the end of Oct 2022 points out that TradFi regulation and supervision cannot be onboarded in the DeFi ecosystem. The report also states that policy enforcement is restricted to the set of entities that are legally subjected to the authority of standard public institutions; however, it is difficult to distinguish the legal entity in DeFi as it relies on publicly distributed ledgers and smart contracts to provide services without requiring the presence of intermediary agents. For this reason, DeFi protocols do not bear means of enforcement from standard policy frameworks. Above all, the report says that the benefits of service users and the technical feasibility of regulation should be fully considered before making premature and inadequate attempts to regulate DeFi.

Against this background, the EC introduced a proposal for a regulation on Markets in Crypto-Assets (MiCa) to establish a legal framework through which rules will apply to areas closely related to the TradFi system, with the stablecoin measure coming in first. MiCA is being viewed positively in terms of its depths of technical understanding and feasibility. Inadequate attempts to regulate DeFi based on TradFi’s regulatory framework will bring side effects, and the DCCPA bill is an example. All things considered, regulations should be enforced in applicable areas only after thorough investigation and research have been conducted.

6-3. Mandatory Disclosure of Crypto Assets

Investor protection necessitates proper management and supervision, but it must be transparency-based, not permission-based. In other words, while developers can develop/deploy various financial services without permission from regulators and individuals can exercise their rights to engage in financial activities freely, projects are obligated to disclose specific information on crypto assets to allow investors to make the right decisions.

Specifically, projects should disclose the following information in real-time via public platforms:

- Whitepaper

- Smart contract audit report

- Tokenomics

- Token distribution/circulating supply

Publicly traded companies issue regular reports with financial statements in a certain format to help investors understand the company’s financial status and make the right investment decisions. Crypto projects, too, should release whitepapers, smart contract audit reports, and tokenomics in a unified format on a public platform for better readability to aid investors.

The white paper/tokenomics should be updated at the time of the initial listing or roadmap change, and smart contract audit results should be updated at the time of the initial listing or code change. As for token distribution/circulating supply, the related on-chain data should be monitored in real-time. Authorities should apply effective supervision and oversight to crypto-asset activities and markets to ensure transparency and prevent malicious activities, but with minimal intervention.

7. Closing Thoughts

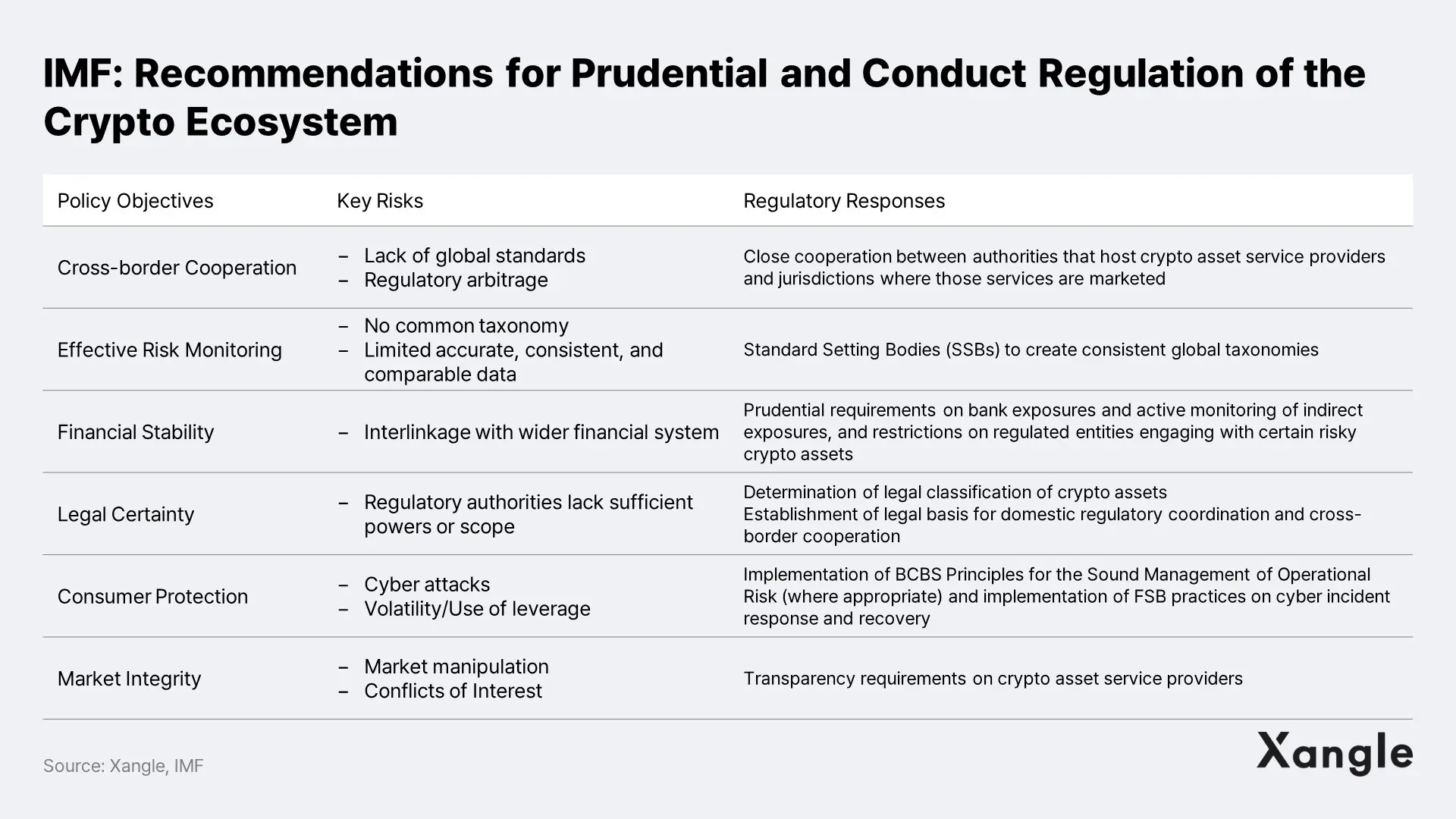

- A comprehensive crypto taxonomy integrating TradFi and crypto assets: Cross-border Cooperation & Effective Risk Monitoring

- Clear distinction and understanding of TradFi and DeFi: Financial Stability & Legal Certainty

- Mandatory disclosure of crypto assets: Consumer Protection & Market Integrity

In Sep 2022, the IMF proposed six elements to achieve a consistent global regulatory framework under the "Recommendations for Prudential and Conduct Regulation of the Crypto Ecosystem." If the three core principles outlined above are abided by, a comprehensive and constructive regulatory framework will certainly be achieved.

As an English proverb says, "more haste, less speed." With the fall of the FTX, there are growing voices to introduce regulations fast, but a hastily drafted bill will not prevent another FTX crisis. Policymakers and the crypto community should put their heads together to understand each other's positions and slowly but surely work on the challenges to adopt effective crypto regulation.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.