The Past, Present, and Future of dYdX: Will Tokenomics Sway the Rise and Fall of dYdX?

Translated by LC

Table of Contents

1. Introduction

2. DYDX vs. GMX: On-Chain Activity

3. Will Tokenomics Sway the Rise and Fall of dYdX?

4. dYdX Leaves Ethereum to Build a Standalone Cosmos Appchain

5. Potential Risks of Migration to Cosmos Appchain

6. The Emergence of New Competitors: KUJIRA and Sei Network

7. Closing Thoughts: What Does the Future Hold for dYdX Post Migration?

1. Introduction

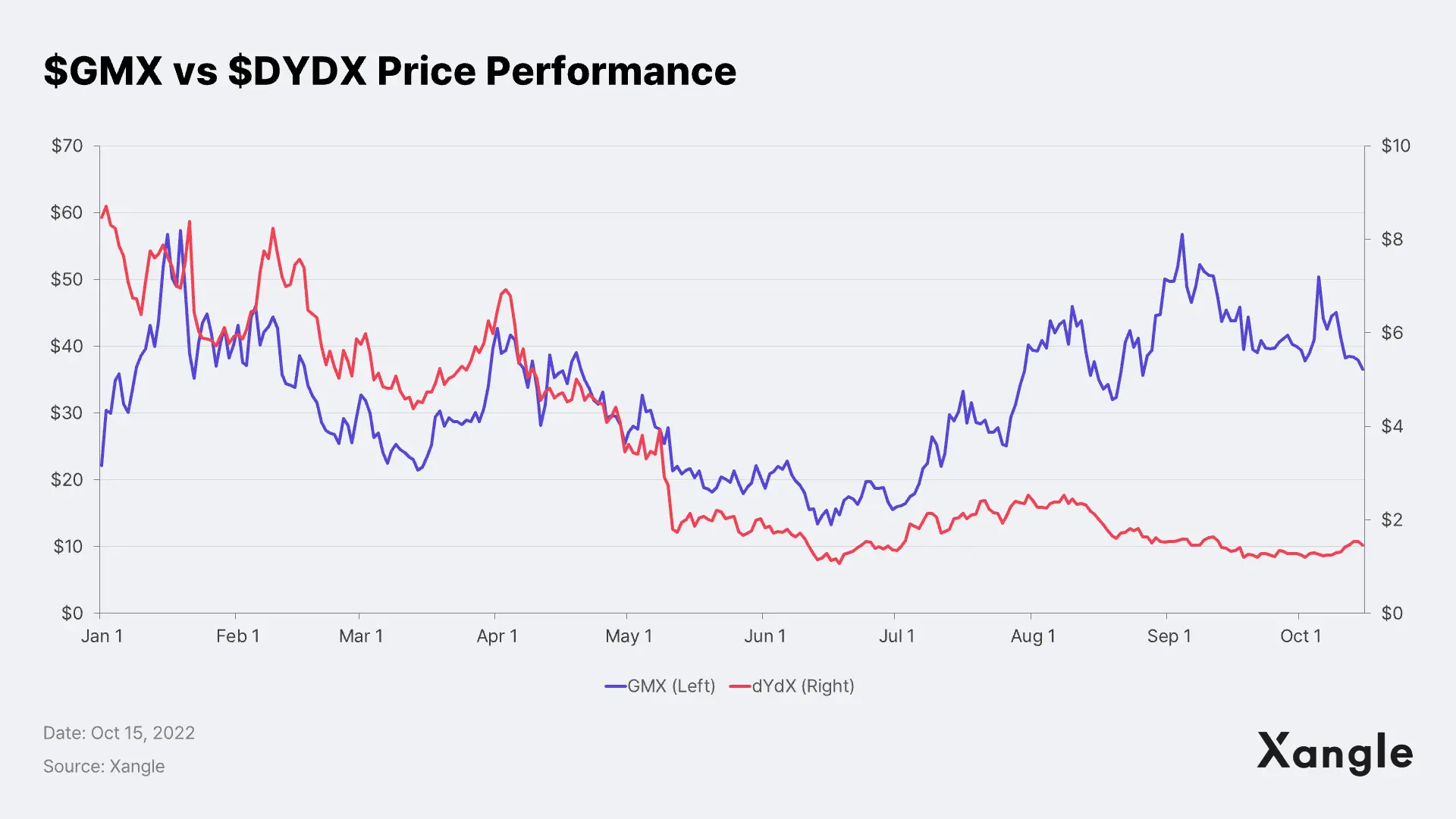

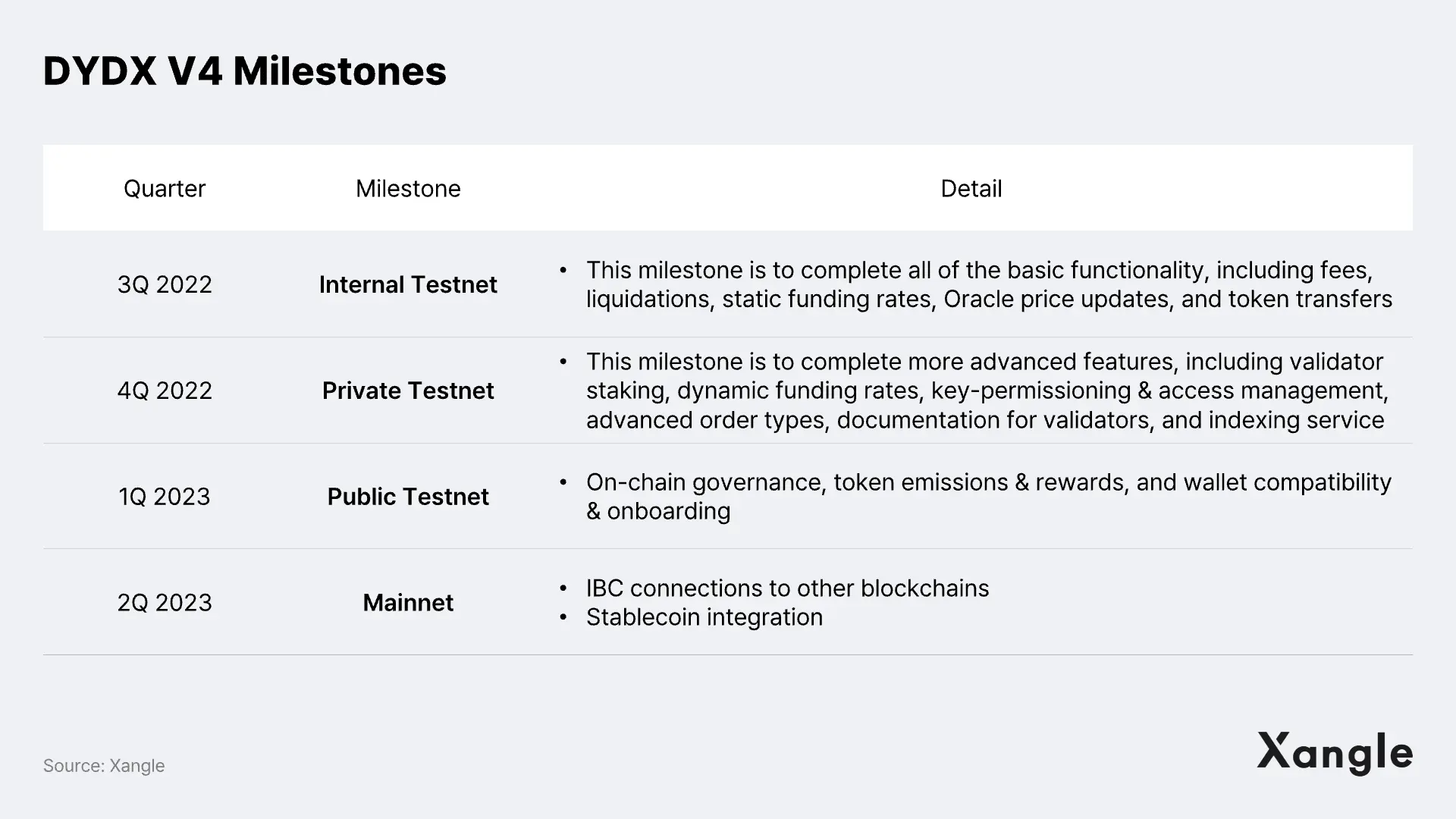

While the recent $GMX performance is notable, the $DYDX price still shows no sign of rebounding. What is the problem with dYdX, and can the Cosmos appchain, which is scheduled to be released in the 2Q 2023, become a game changer (refer to the DYDX roadmap below)? Before investing in the derivative futures DEX market, let's dive into the past, present, and future of one of the top decentralized crypto derivatives exchanges, dYdX.

2. DYDX vs. GMX: On-Chain Activity

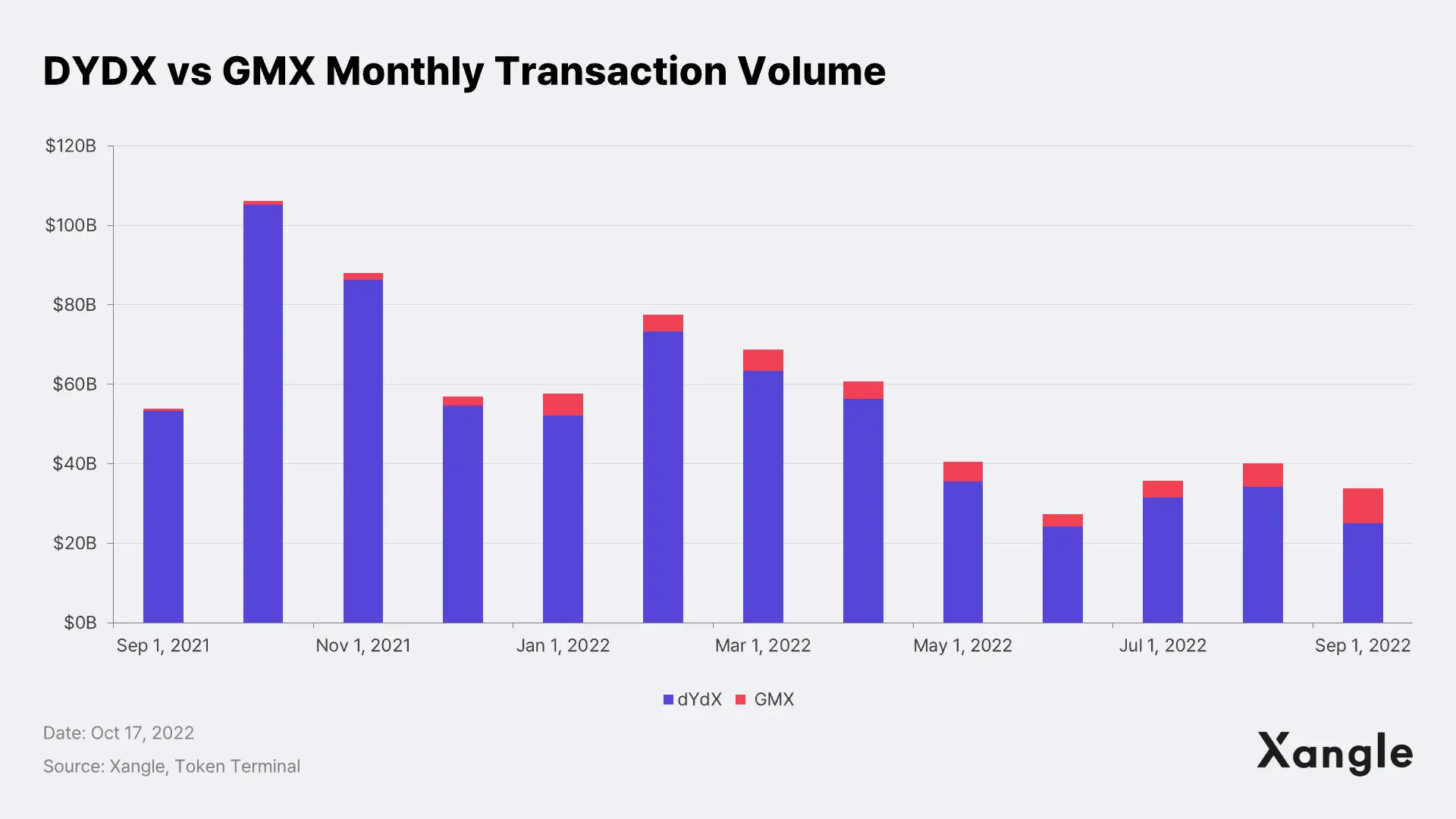

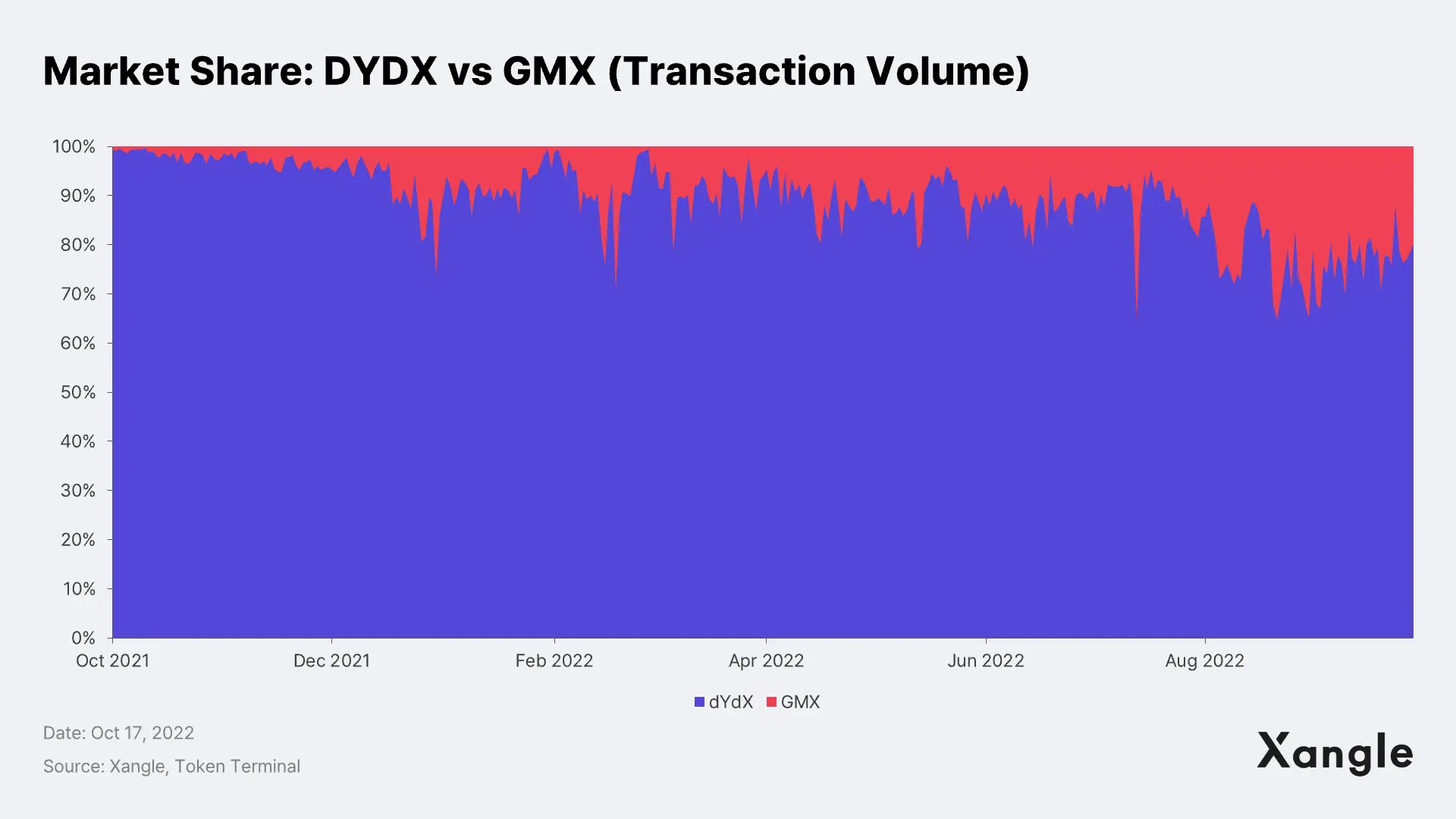

Before taking a deeper dive into dYdX, let’s get into the distinction between GMX and dYdX, the top two crypto perpetual protocols, in terms of on-chain activities, including i) transaction volume, ii) open interest, and iii) the number of users.

2.1 Transaction Volume

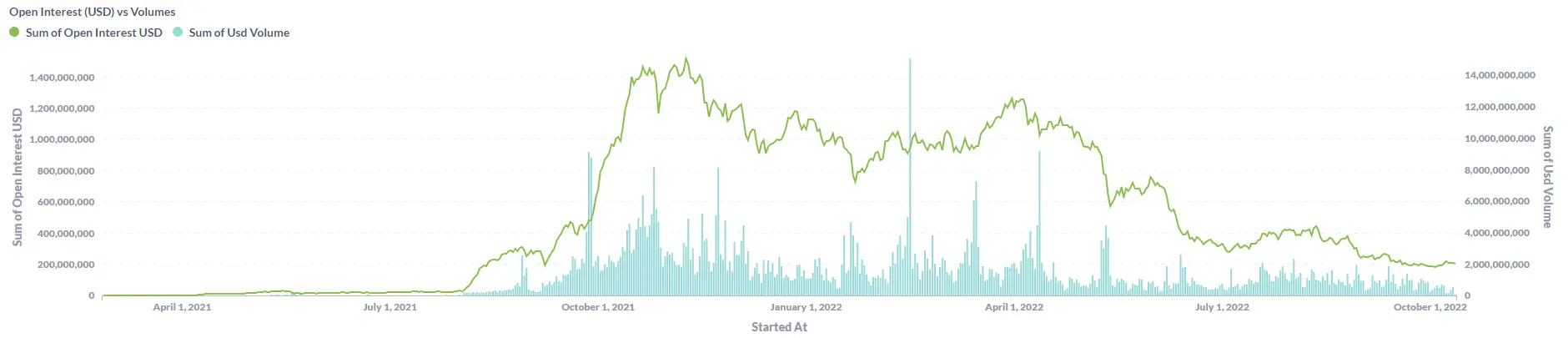

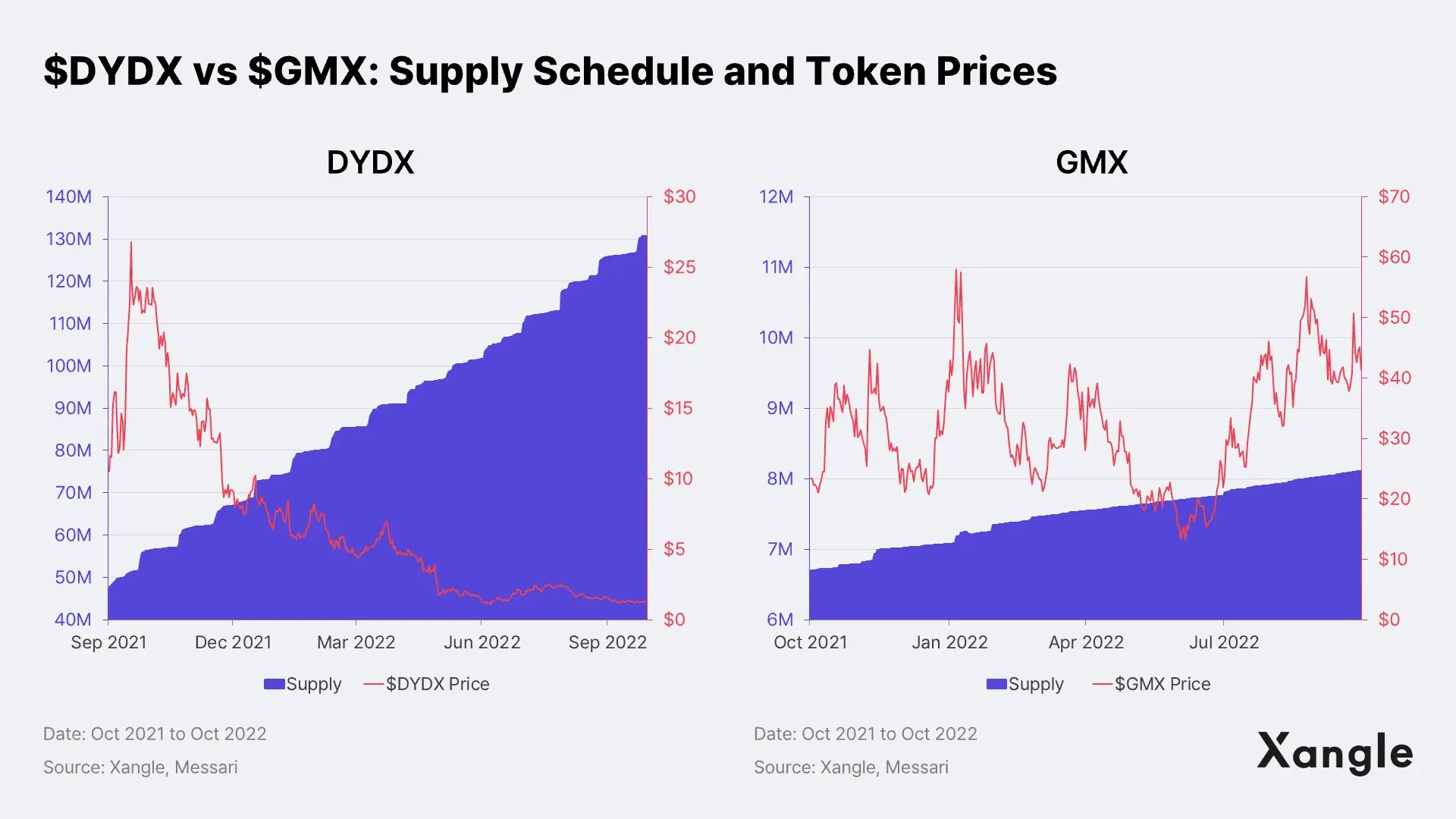

As of the end of 2021, dYdX trading volume has continued to decline, while GMX trading volume has been steadily increasing. dYdX has been sluggish, falling from $105B in October last year to $25B (YoY -76%) in September 2022, while GMX rose from $960M in October 2021 to $8.7B (YoY +806%) in September 2022, showing remarkable growth (GMX trading also includes swap transactions, but margin trading accounts for more than 90%. As a result, dYdX's market share has decreased from +99% to 80%.).

2.2 Open Interest

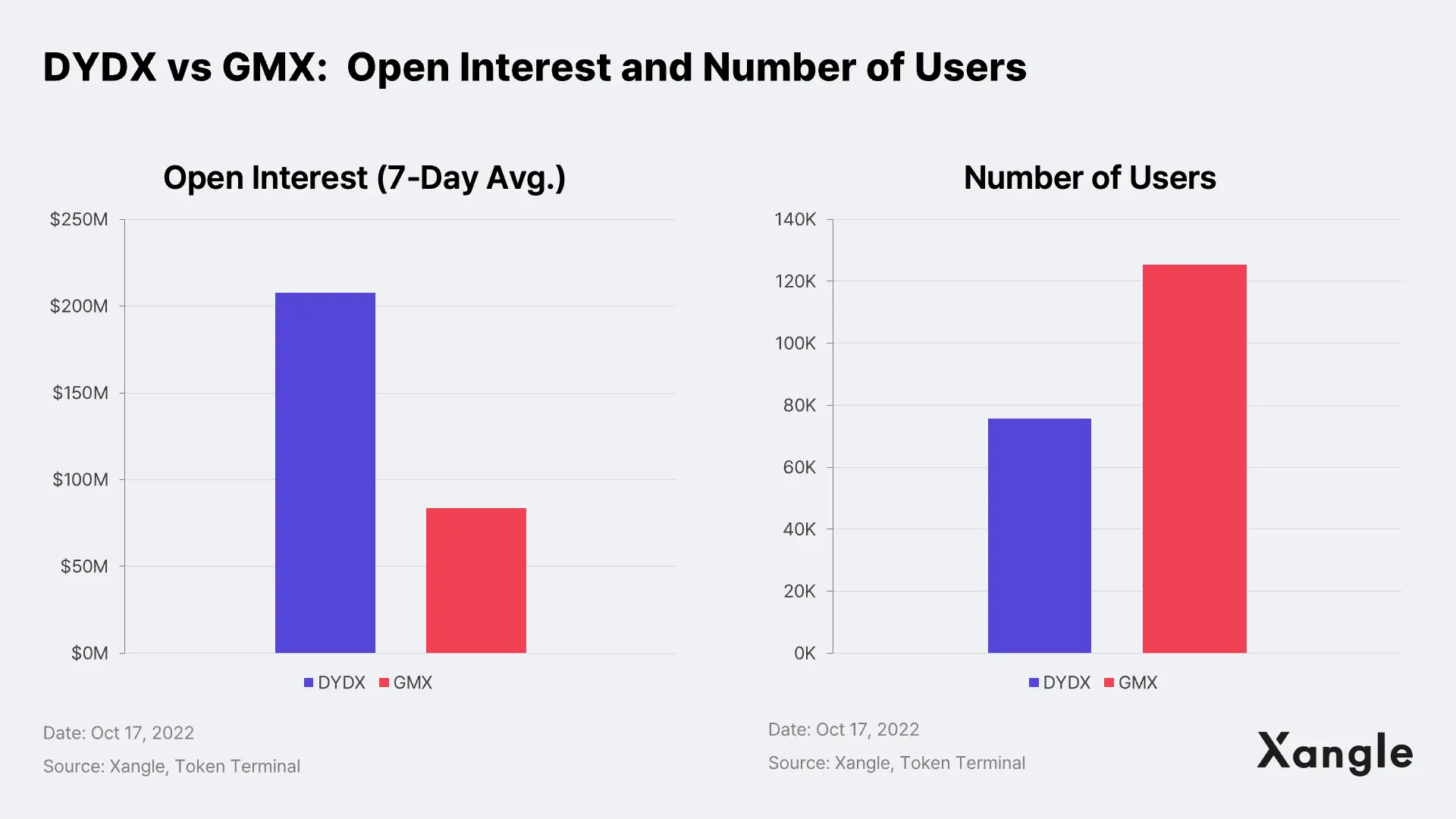

dYdX’s daily open interest had reached $1.4B in 4Q 2021, but it now has bottomed to about $200M as of writing. GMX’s 7-day average open interest is roughly $84M, about a 21% increase MoM.

2.3 Number of Users

dYdX and GMX are trusted by over 75,000 and 125,000 users, respectively. Of the total GMX users, 56,000 (roughly 45%) use the margin trading service. GMX has a slightly higher number of users based on the trading volume than dYdX, meaning that small holders trade more via GMX.

3. Will Tokenomics Sway the Rise and Fall of dYdX?

In the early days, dYdX had i) abundant liquidity through collaboration with various MM (market makers) such as Amber Group and Sixtant, ii) fast transaction speed and low slippage by leveraging hybrid orderbook (off-chain orderbook, on-chain settlement), and iii) dominated the market with aggressive trading rewards. Above all, dYdX’s trading reward strategy has contributed the most to its short-term success and, at the same time, the main culprit for the current sluggish performance. In other words, users who were initially drawn to the platform to earn $DYDX rewards are leaving as investing in $DYDX has become less profitable due to the continued drop in token prices. Then why is the $DYDX price not recovering?

3.1 High Inflation

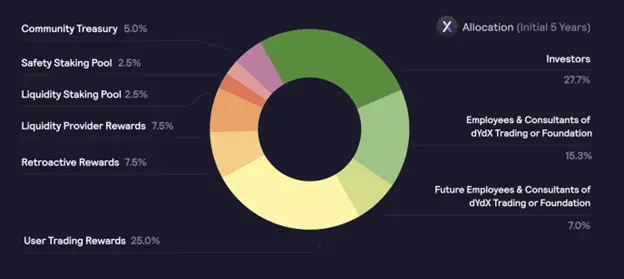

dYdX offers 25% of total token issuance to users over 60 epochs as a reward for trading (trading reward was reduced by 25% as the DIP-16 agenda passed on Oct 7, 2022), and this benefit allowed users to onboard quickly while causing high inflation at the same time. Unlike GMX, which has maintained token inflation at 21% over the past year, the $DYDX inflation rate has reached a whopping 176%. At present, roughly 130M $DYDX is in circulation, only 13% of the total issuance. Moreover, the average annual inflation rate is expected to reach 66% over the next four years, indicating that the overhang risk is expected to remain high in the future. Meanwhile, investors will need to pay particular attention to extreme price volatility in Feb 2023, during which the tokens allocated to founders, teams, and investors will be unlocked, starting with $1.5B $DYDX.

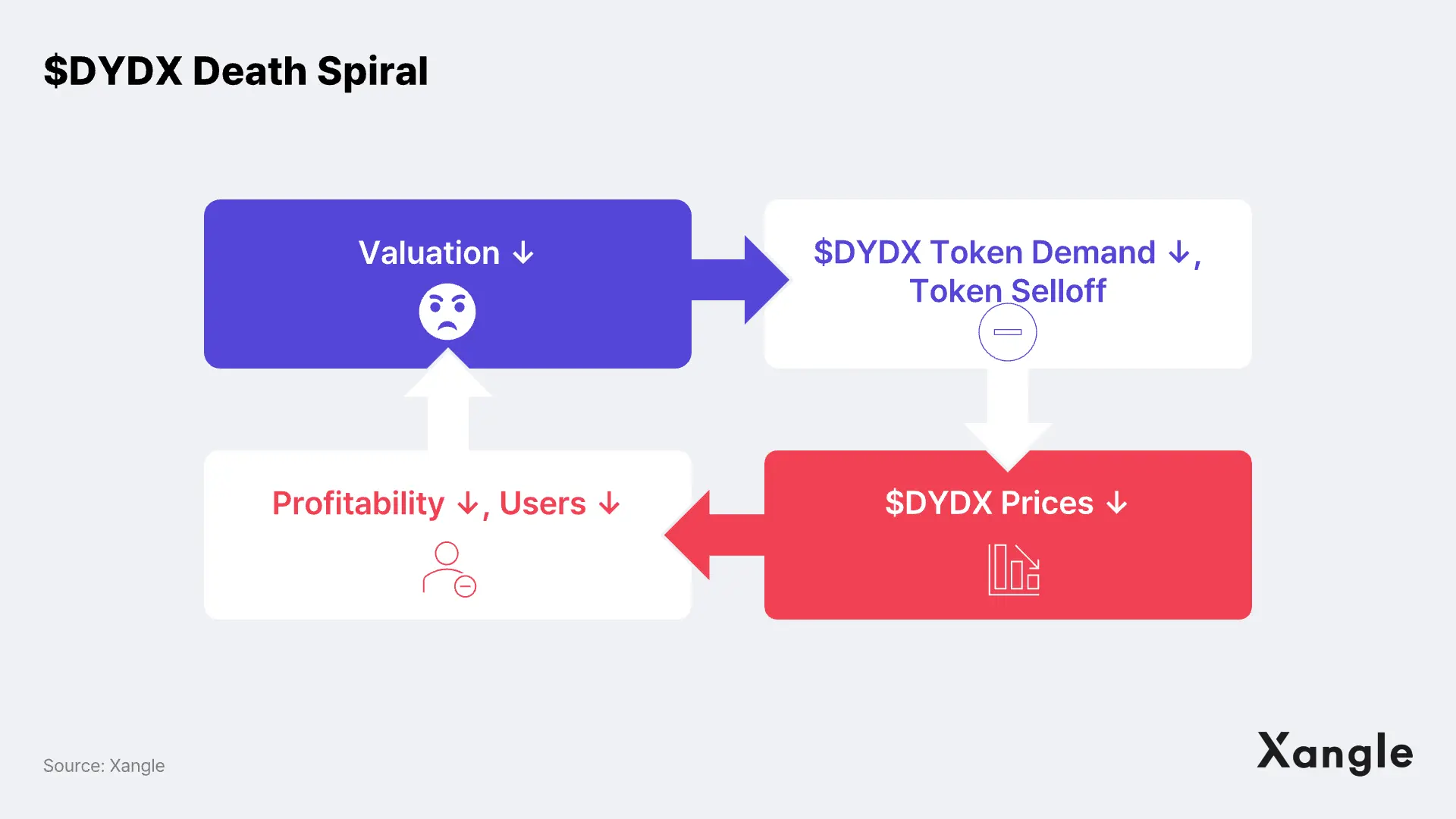

3.2 Lack of Token Utility Spurring Selling Pressure of $DYDX

If DYDX had distributed a portion of its revenue to token holders like GMX, the selling pressure would have been lower than it is now. Since $DYDX is just a governance token, and the only one other benefit to holding the token is to enjoy some trading fee discount when using dYdX, individual investors and traders have little incentive to hold/buy $DYDX, leading to a similar death spiral phenomenon to P2E games experienced earlier in 2022 (see figure below).

3.3 dYdX Announces to Move Away from Ethereum, Prompting Concerns about Its Future

Although Ethereum is far less scalable compared to other L1 blockchains, Ethereum-based dApps are reluctant to leave Ethereum because the Ethereum ecosystem is i) the most active in terms of the number of users, TVL, revenue, number of developers, and number of dApps, and ii) the most secure blockchain. For this reason, when dYdX announced that it was leaving Ethereum to build its own L1, investors likely took the news as a bad sign. Then why is dYdX pivoting to Cosmos?

4. dYdX Leaves Ethereum for Its Own Cosmos Appchain

Before explaining why dYdX decided to build a standalone appchain, I would like to briefly touch on what an appchain is and its offerings to understand the reason behind dYdX’s migration to Cosmos.

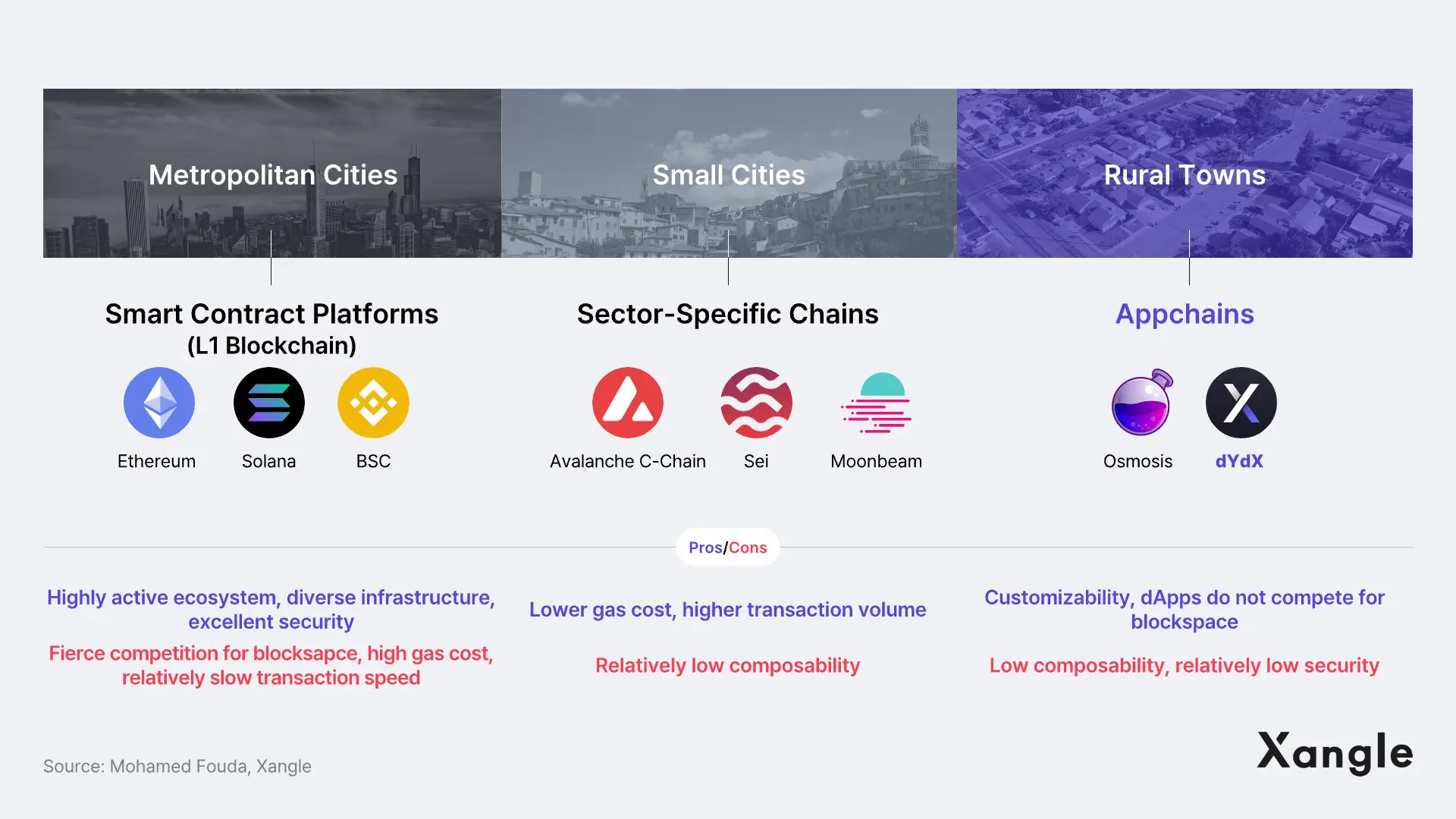

4.1 What is an Appchain?

An application-specific blockchain, or appchain, is a blockchain that is exclusively designed to operate one specific application or function. An appchain dedicates its blockspace to a specific application and boasts excellent performance as it offers full customizability from designing a consensus algorithm to deciding the number of validators to security structure. Currently, numerous projects are using appchains, and the major L1 projects that support appchains are Polkadot (Parachain), Cosmos (Zones), Avalanche (Subnet), and Polygon (Supernet). While an appchain can be accessed and used by anyone, it differs from a public blockchain as an appchain is dedicated to a specific blockchain.

The notion of L1 chains as cities is useful to understand how they differ from appchains. According to Mohamed Fouda, L1 chains act like metropolitan cities where everyone, from users to developers, wants a piece of it as they have a diverse infrastructure that can support a wide range of businesses (dApps). These big cities are populous, wealthy, and protected by solid walls, making them harder to attack. At the same time, it is overpopulated and highly congested, and prices (gas costs) are generally high.

On the other hand, appchains are a network of rural towns dedicated to a single business/service. Each town can create its own rules and policies, making it less crowded and cheaper. The town’s single business is used by everyone in the town, meaning that customers may even come to this town for this specific business if it is unique enough. These small towns sometimes visit each other to use different services, but it may not be an easy journey to pay a visit to these towns since they may not be well-connected to the external world. If you are unlucky, you could be attacked on the way back.

Then there are sector-specific chains, which lie in between the two aforementioned models. Sector-specific chains only support some businesses, e.g., DeFi or gaming. Though more secure than appchains, they are less popular than L1 chains.

4.2 Advantages of Appchains

Appchains offer developers the following benefits:

- Performance: Because dApps compete with each other for blockspace on the same network, it is often the case that one popular dApp consumes a disproportionate amount of resources, which increases transaction costs and latency for users of other dApps. Unlike L1s, appchains offer projects the ability to keep transaction costs and latency low, which results in better UX for end users. Appchain’s unique features may benefit projects building dApps that require high throughput (e.g., games or order book exchanges). Gaming applications are the best example of this category. The majority of interactive games require extremely high throughput to support users’ game interactions, and these transactions should be free because no one would pay gas fees for every action when playing games. For these reasons, Axie Infinity launched a dedicated appchain on the Ronin sidechain.

- Customizability: Another great advantage of an appchain is that it allows developers to continue optimizing their applications for their end users. Larger applications will want to make certain design choice trade-offs, such as throughput, finality, security level, composability, and privacy, amongst others. With appchains, developers are guaranteed the freedom to customize their requirements. The projects running appchains can even select the network participants themselves. For example, validators of a project using zero-knowledge proofs can have high-performance hardware requirements such as running an SGX or FPGAs. For Web2 companies that require whitelist or KYC’s validators, appchains could offer a way to adopt Web3 without going fully permissionless.

- Value capture: An application is able to capture MEV by running its own sequencers or validators, which can create opportunities for new crypto native business models. For example, dYdX validators, who will likely be market makers, can offer no fees for users but could slightly adjust the execution prices.

- Accrue more value to tokens: With similar qualities to L1 native tokens, appchain tokens can accrue more value from being used as staking tokens or gas tokens. I will explain this in more detail in the following section

4.3 Issues with Appchains

Despite the several advantages, some risks need to be taken into consideration.

- Security: In appchains, the security largely depends on the adoption of the application and the price of the application’s native token (except for parachains). If the application adoption is weak and the token price is low, the network security becomes weak, enabling malicious parties to acquire enough stake to attack the network at a low cost. For this reason, projects that operate appchains require validators to stake the native token and operate sophisticated infrastructure with high uptime to participate in the network. The validator rewards dependence on the token price adds pressure on application developers to use high token inflation.

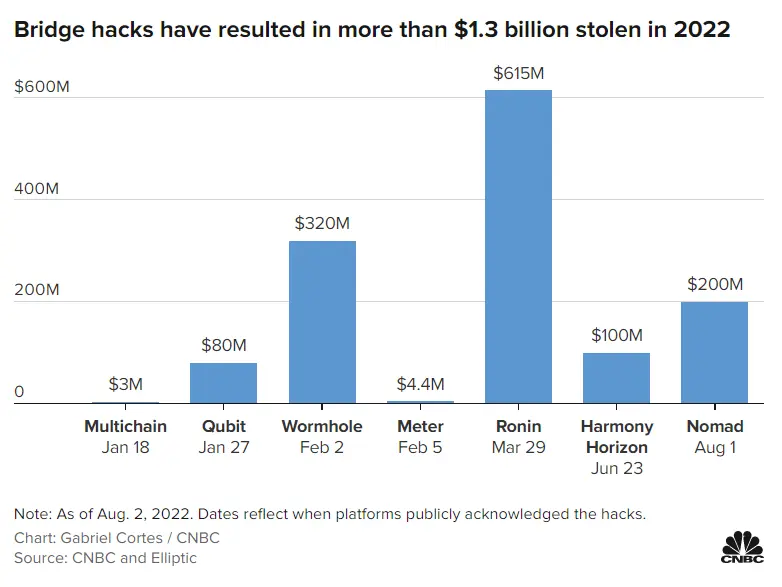

- Bridged assets: An appchain is a single mainnet that requires bridging several assets to leverage liquidity. However, bridging assets i) carries the risk of exploitation, ii) degrades the user experience, and iii) may lead to fragmented liquidity. Meanwhile, the recent bridge exploit incidents that drained several millions from Binance, Nomad Bridge, and Wormhole once again highlight crypto bridges’ vulnerabilities, indicating that it remains to be seen whether appchains can remain safe from attacks.

- Cost: Launching an appchain comes at a high price. Building an appchain will require increased costs and a long list of additional infrastructure, including RPC nodes, archival nodes, block explorer, and network monitoring services. Moreover, maintaining a chain requires significant planning and communication with the validators to arrange network upgrades or respond to bugs and network downtime. Many startups hence cannot afford the costs associated with building an appchain in the early stage.

- Composability: One of the main advantages of building L1 blockchains is atomic composability, meaning dApps can build on each other, and users can seamlessly interact with multiple protocols in the same transaction. For example, DEX routers can route a single trade through different AMMs to achieve the best pricing and flash loans, where a transaction can borrow from a lending protocol and execute a trade or an arbitrage on AMMs. On the contrary, appschains lack this atomic composability because each dApp is isolated from the rest, and interactions between dApps require cross-chain messaging protocol.

4.4 Why is dYdX Deploying its V4 on Cosmos Appchain?

Being one of the top exchanges in terms of volume, sizable engineering team, and know-how, building on appchains itself would not be a challenge for dYdX. That said, we will look into i) why dYdX has opted to deploy appchains in Cosmos and ii) the future outlook of dYdX after moving to Cosmos. Considering the problems dYdX had in the past, dYdX’s future vision, and the advantages/disadvantages of an appchain, here is why the move is set to develop appchains.

A) Achieving Full Decentralization

The dYdX foundation has long been emphasizing its aim to develop and grow the protocol ecosystem to turn it into an entirely decentralized exchange. dYdX’s rationale for the move to appchains is the following:

- Centralization concerns: dYdX is currently using up with StarkWare to record transactions on Ethereum. StarkEx is an L2 SaaS (Software as a Service) developed by StarkWare. StarkEx, a comprehensive STARK proof solution, creates source codes, generates zero-knowledge proof, and executes transaction settlement upon receiving service fees from projects. Though highly useful, StarkEx is i) not an open-source code and ii) the sequencer, which creates the validity proof, is centralized. For these reasons, StarkEx is perhaps not the right tool for dYdX to achieve full decentralization. DYdX likely had no choice but to use StarkEx as an alternative solution in the beginning, but now that it has a lot to offer its users, it is likely that the platform is developing an open-source chain to break away from the centralized solution. This is because switching to a public chain would allow the validator nodes, not StarkWare, to handle consensus, settlement, and computation.

- Decentralization of orderbook matching: dYdX currently keeps its orderbook off-chain while matching the orders on-chain, but with the development of a dedicated blockchain, validator nodes will run the orderbook. Hence in dYdX V4, each validator will run an in-memory orderbook, with state root values being updated in real-time by the network and the resulting trades being subsequently committed on-chain.

B) Potentially Avoiding Regulations on Security Tokens

Achieving full decentralization may be one of many reasons for launching its own chain. Perhaps dYdX is trying to mitigate its regulatory risk of being categorized as a security token by launching appchains to secure a large number of validators and building a decentralized service not run by dYdX Trading Inc. Its announcement that the profit (transaction fee) would be given out not in the form of dividends but as rewards for PoS staking could also be understood in the same context. However, one concern is that the scalability decreases as the number of validator nodes increases. This is because as the number of validator nodes increases, the time it takes for transaction consensus becomes longer.

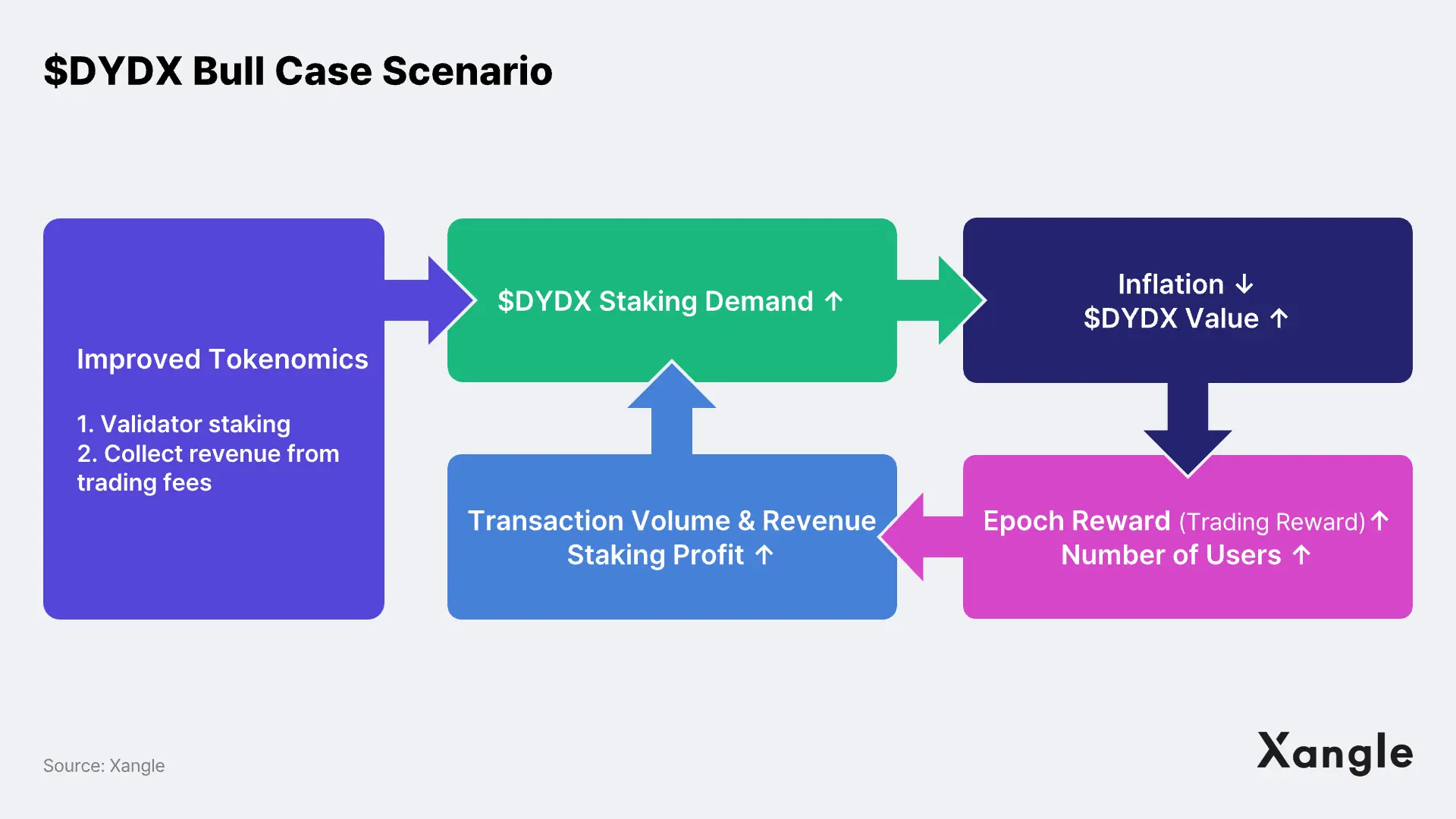

C) Token Value Accrual

As explained earlier, there are two major reasons why the token price remains sluggish despite dYdX being one of the perpetual derivatives giants: i) Low token utility and ii) high inflation. However, by having an independent chain, dYdX will have its L1 native token, which will, in turn, accrue the following value to its token.

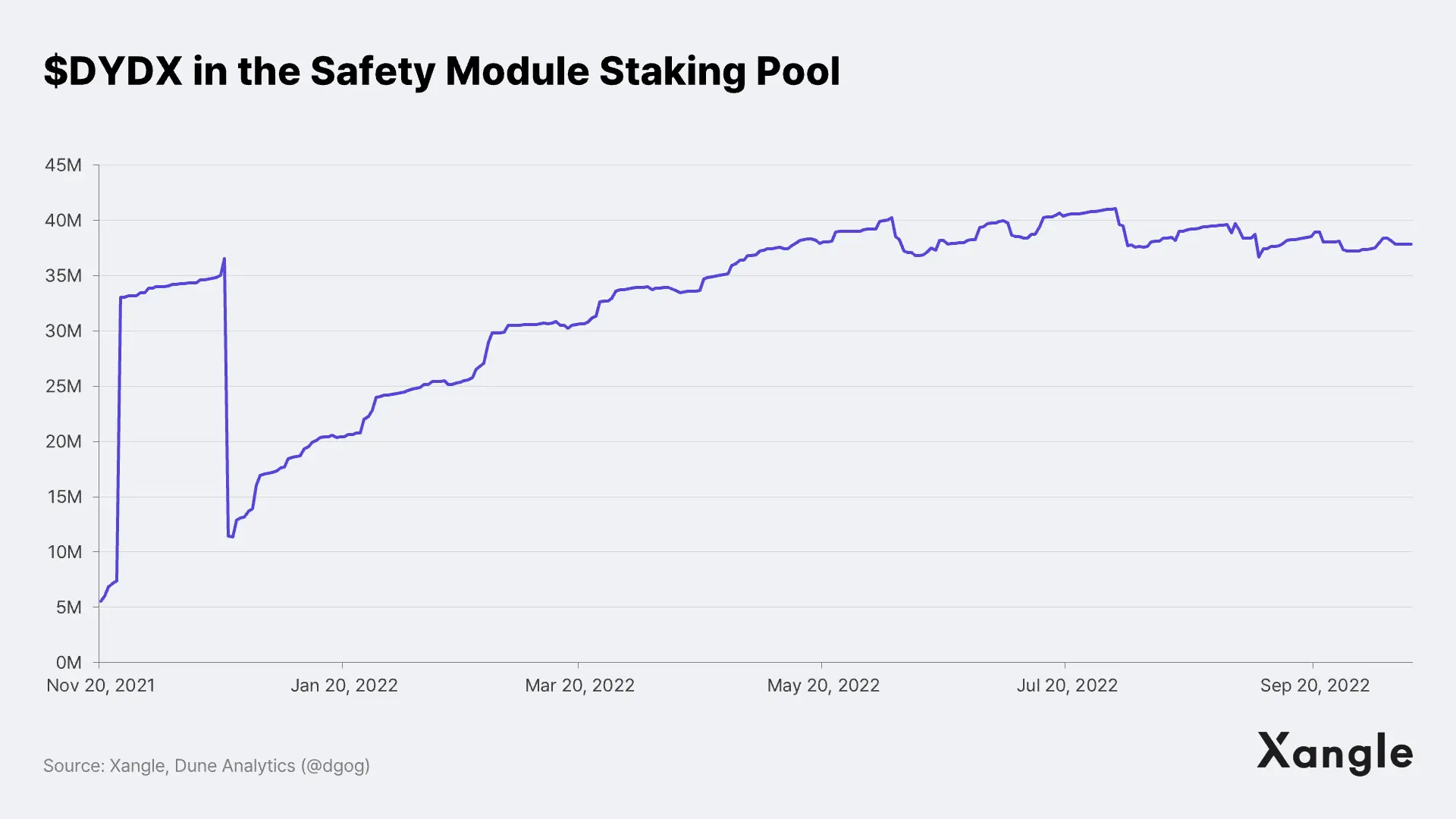

- Staking: As is the case for any PoS chains, a token owner must stake $DYDX to become a dYdX appchain validator. Currently, the only available method to stake $DYDX is to use the Safety Module Staking Pool, which will be used in the case of insolvency or other issues with the protocol. As of Oct 15, the $stkDYDX stored in the staking pool is about 37.7M. It is equivalent to about 28% of the circulating supply. Following the move to appchains, validator staking will increase dramatically, which is expected to offset, to some extent, the overhang risk caused by high inflation of $DYDX.

- Fee structure: In V3, all revenue collected on the trading fees went to dYdX Trading Inc., but following the launch of appchains dedicated to dYdX, fees will accrue to validators. It is highly likely that a percentage-based trading fee structure will be applied. If the protocol allows indirect staking, it will be a clear incentive for holders to hold $DYDX. As no fees will be incurred when trading on the dYdX appchain, validator nodes can obtain i) block creation rewards and ii) transaction fees.

However, one concern is that the inflation rate is still high even after switching to an appchain (66% on average for the past four years). Trading rewards will be paid out steadily and the token supply held by founders, teams, and investors will begin to be unlocked from 2023 onward. Another downside of the standalone appchain is that dYdX validators will be paid in $DYDX for block creation reward, which creates a security cost as some form of token emission to validators is required, possibly increasing the inflation rate. Moreover, if the number of users using the platform decreases and causes the transaction fee to decline, the block reward could further increase to prevent validators from leaving.

D) Building Additional Features

dYdX has an ambitious goal to eventually become one of the largest crypto exchanges, meaning they will not settle for just offering perpetual futures. dYdX plans to add other trading products, such as spot, margin, and additional synthetic products. To that end, dYdX should move away from third-party infrastructure and migrate to a mainnet optimized for DeFi trading since StarkEx is an application specific ZK rollup through which only specific transaction types selected in advance can generate STARK proof (in the case of dYdX, perpetual futures transactions). In this context, the dYdX appchain can be seen as a cornerstone to open the way to build additional features, bringing i) great network activity, ii) revenue capture, and iii) increased utility to $DYDX.

E) Creating Good Quality Products is What Matters

Many people in the crypto industry say dYdX should remain with Ethereum, a blockchain with the biggest ecosystem, to achieve continued growth. However, dYdX CEO Antonio Juliano and key executives have repeatedly emphasized that dYdX's overriding goal is to create outstanding products that provide an optimal user experience. In their view, the factor that determines the success of a dApp is not the underlying blockchain but the quality of the product, and if a good product is created, users will naturally follow. From this point of view, Cosmos is a reasonable option as the platform provides a flexible development environment, has experience producing major L1s such as Osmosis and Terra, and has an active ecosystem. Furthermore, as laid out in the Cosmos Hub (Atom 2.0) white paper, Cosmos plans to make substantial improvements leveraging interchain security and liquid staking.

Sidenote: Enabling Increased Scalability Many Not Have Been the Motivation for dYdX’s Flight to Cosmos

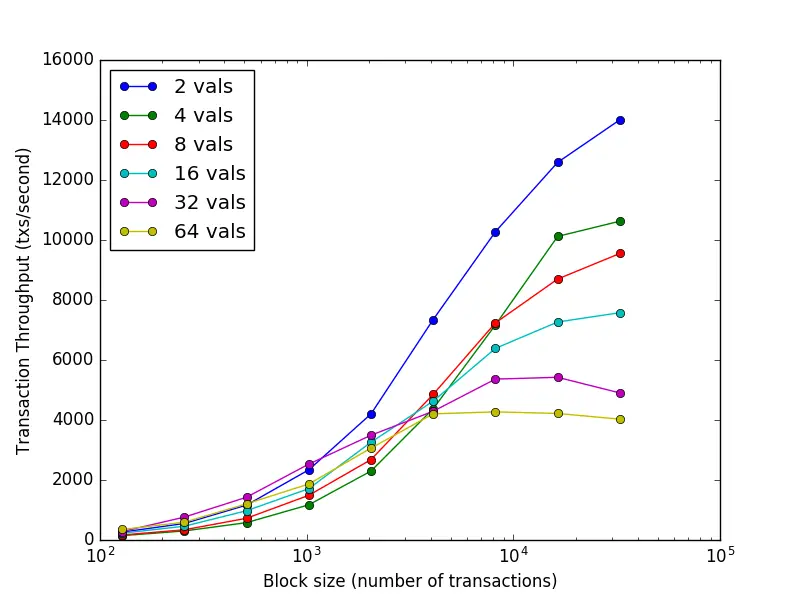

For dYdX, scalability improvement may not have been the main motivation for building its appchain. The existing dYdX product processes about 10 trades per second and 1,000 order places/cancellations per second, which can be handled with StarkEx's throughput (9,000 TPS). Furthermore, there is no guarantee that the dYdX appchain will outperform StarkEx. Based on the Tendermint Core Consensus Engine, the theoretical maximum TPS is 10,000, but according to Paradigm Research, the throughput drops significantly to 4,000 TPS when 64 validator nodes participate in the consensus algorithm. As the number of validator nodes increases, the time it takes to reach a transaction agreement will inevitably increase, so it remains to be seen how dYdX will improve the scalability problem.

5. Potential Risks Post Migration to Appchain

While there are benefits to Cosmos migration, it carries potential risks. Below is the summary of the aforementioned risk factors:

- Network security: There are potential security risks from building its own validator set. By switching from StarkEx to appchains, dYdX will no longer be able to use the validator nodes of Ethereum, a network with the highest security among existing blockchains. In case of a breach of the dApp, the token value will plummet, and the low market value of tokens may raise the security risks of the chain. However, it seems that some of the risks can be offset when implementing the interchain security mentioned in the Cosmos Hub white paper (for complementary reading: “ATOM 2.0 Whitepaper: Newly Refined Vision to Enable ATOM to Become Cosmos’ Reserve Currency”).

- Token inflation: As described above, as a risk associated with network security, most projects running an appchain require high uptime from validator nodes in order not to be exposed to hacking, and in return, nodes expect high rewards. As such, appchains incur huge economic costs in the process of bootstrapping nodes, which leads to high token inflation. dYdX’s current token inflation is high as it is, so in case of inflation rises even higher, it would be challenging for the token price to bounce back.

- Bridge hack: After migration, Except for the Cosmos chains that can communicate via IBC, dYdX is required to bridge assets between dYdX <-> Ethereum (or other L1 blockchains) post migration to Cosmos. However, the recent bridge exploit incidents that drained several millions from Binance, Nomad Bridge, and Wormhole once again highlight crypto bridges’ vulnerabilities. According to Chainanalysis, the total damage caused by the bridge hack in 2022 is close to $1.4B.

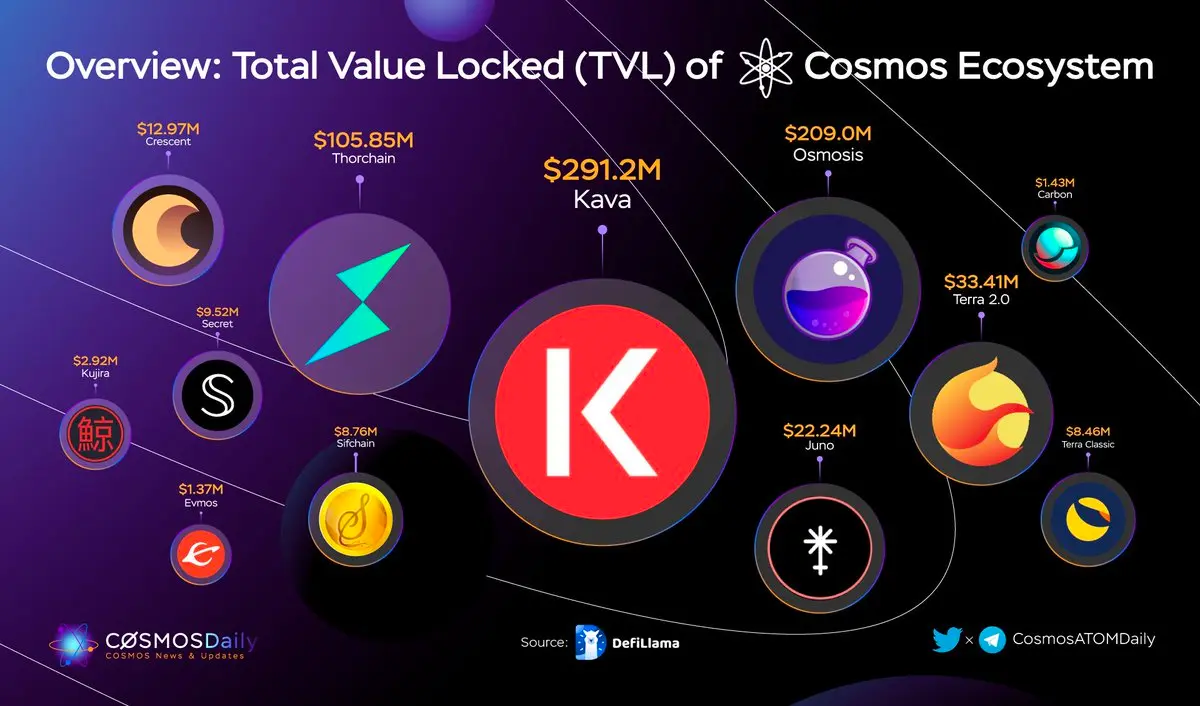

- Liquidity: Pivoting to Cosmos poses another risk related to liquidity, as dYdX will not be able to leverage the vast network of assets in the Ethereum ecosystem. As of Oct 15, 2022, Ethereum's total TVL is close to $30B, while Cosmos' TVL is less than $1B in total, raising concerns about whether Cosmos could offer a sufficient level of liquidity. Compared to the stablecoin market cap, the gap becomes even wider. A total of $89B of stablecoins are circulating in Ethereum, while Cosmos does not exceed $500M even with all Tendermint-based chains combined. On a positive note, Circle has announced its plans to provide USDC to Cosmosin in early 2023.

- Oracle: The Cosmos ecosystem lacks reliable oracles such as Chainlink. Although Cosmos has Band Protocol and UMEE, it is difficult to determine what level of technology and stability the oracles have at this point.

- Governance: A decentralized structure can lead to various problems, such as complicating the decision-making process or significantly slowing development. As dYdX is trying to be a fully decentralized protocol governed by its holders, the governance structure will play a crucial role in determining the future of dYdX.

6. The Emergence of New Competitors: KUJIRA and Sei Network

Competition is expected to intensify further among the derivatives trading exchanges. Let’s look at some of the competitors in the Cosmos ecosystem that are coming into the scene.

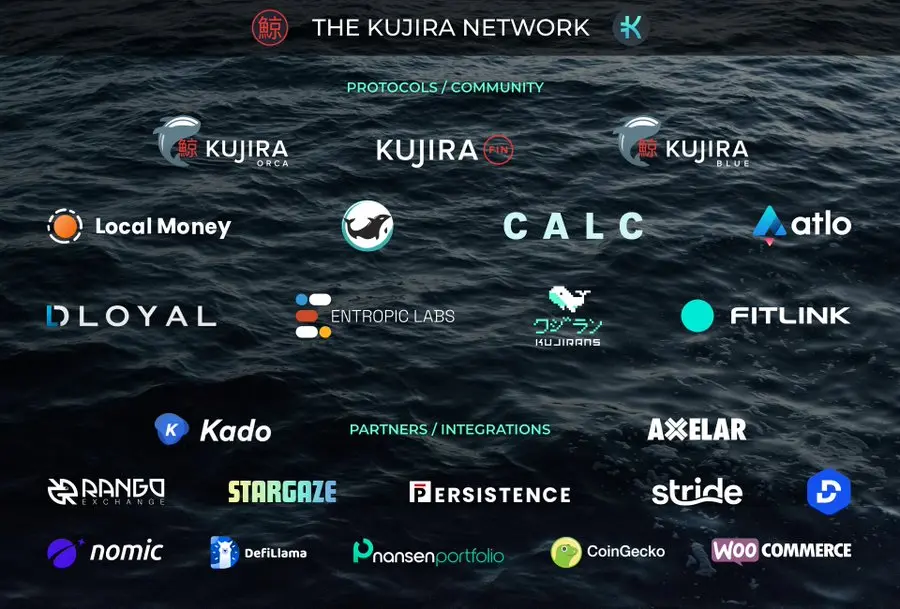

KUJIRA

Kujira is a semi-permissioned sovereign Cosmos Layer 1 platform that launched its mainnet in Jun 2022. Kujira is drawing investor attention with fast development speed and great UI/UX. The word Kujira means “whale” in Japanese. The platform chose the name with a vision to help every user to become a crypto whale. The Kujira project has multiple whale-themed dApps other than L1:

- FIN: FIN is an on-chain orderbook style token exchange that plans to launch margin trading on FIN.

- ORCA: ORCA is a public marketplace for liquidated collateral. It allows everyday users to participate in liquidations by selling these liquidated assets from the lowest to highest discount, evenly between everyone bidding at the same discounted rate. ORCA was popular among those looking to get their $LUNA.

- Blue: BLUE is the Kujira Dashboard featuring Govern, Swap, Stake, IBC/Bridge, and Mint (USK).

Sei Network

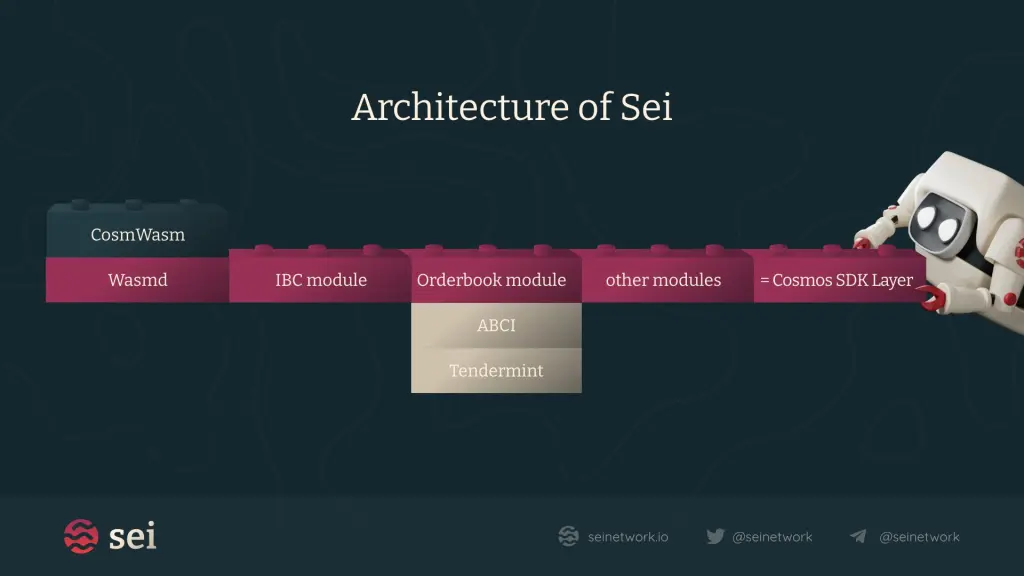

Sei Network is the first orderbook-specific L1 blockchain built using the Cosmos SDK. This features a built-in CLOB (Central Limit Order Book) module, which aims to become the L1 for DeFi applications without implementing AMMs. Others tried this before SEI; for example, Serum (built on Solana) attempted to introduce on-chain CLOBs. Unlike dYdX, Sei is a 100% on-chain orderbook infrastructure. Sei plans to enable new types of financial projects, from live sports and betting to complex options and futures. Sei also offers the following features:

- Permissioned blockchain: Sei is a permissioned blockchain, meaning that developers need to submit a proposal and see it passed via governance before deploying a smart contract.

- Scalability: Sei’s maximum TPS is 22,000 with a 600 ms transactional finality, a highly scalable network. However, whether Sei can deliver these numbers remains to be seen.

- Frontrunning protection: Sei prevents MEV by implementing Frequent Batch Auctioning.

7. Closing Thoughts: What Does the Future Hold for dYdX Post Migration?

Although dYdX has shown remarkable growth starting in 2H 2021, it has been on the decline after gradually losing its market share to GMX in less than a year. The macro-environment could have affected Crypto’s downturn; however, I believe the problem lies in tokenomics. In this context, here is why the move is set to develop appchains: i) Achieve full decentralization and avoid regulations on security tokens, ii) bring greater utility to DYDX token, and iii) accrue additional value to DYDX token through token utility improvement and service expansion. Leaving Ethereum means that dYdX would have to take the aforementioned risks, but I believe staying in the Ethereum ecosystem poses higher risks considering that GMX is taking away dYdX’s market share. If dYdX could dramatically improve its tokenomics by moving to a native chain on the Cosmos ecosystem, I envisage a bigger future for dYdX, perhaps playing a primary role in leading the “Cosmos Summer,” just as STEPN amassed millions in profit and led the Solana boom when the move-to-earn application was first launched.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.