Fat Protocols vs. Fat Applications

Translated by elcreto

Summary

- The Fat Protocol Thesis has emerged since the advent of blockchains, signaling a departure from Web 2.0, where value used to concentrate at the application layer.

- The thesis bases itself on the grounds that the protocol layers represent 70% of the total market cap of the crypto market and that the valuations of Aptos and Sui are high.

- Yet, increasingly, transaction fees are trending down, making it harder for protocols to funnel value. Moreover, some opponents argue that the less-than-expected network effect will further intensify the trend of values being increasingly captured at the application layer.

- The 180-day cumulative revenues back this argument as 7 out of 10 largest projects turned out to be applications.

- The discussion surrounding fat protocol versus fat applications warrants attention from both business and investment perspectives.

1. Fat Protocol: The Emergence of a Theory That Refutes the Way Web 2.0 Has Been

In the blockchain circle, there’s a topic that has never been short of disputes—the pros and cons surrounding fat protocols versus fat applications, first ignited in 2016 by Joel Monegro of Union Square Ventures.

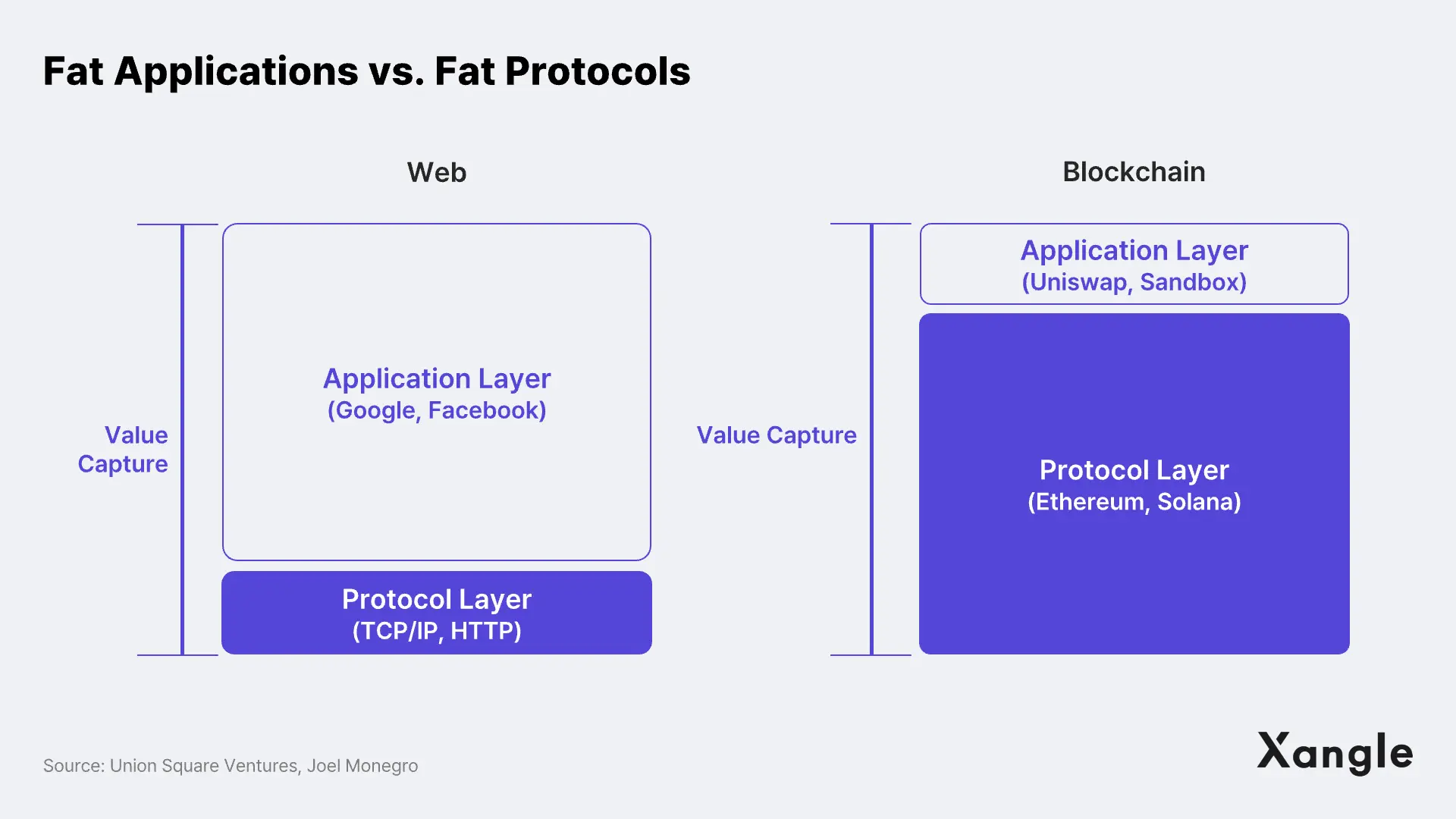

In the era of the Internet, dubbed as the age of Web 2.0, it seemed undeniable that the application layer—as best illustrated by the examples of Google and Facebook—generated most of the value. It drew a stark contrast to the protocol layer, such as TCP/IP and HTTP, whose contribution has been paramount to the world of the Internet but left without return. Put another way, the age of Web 2.0 has been the age of fat applications, in which value used to concentrate at the application layer.

The shift to fat protocols came with the dawn of the age of Web 3.0 built on blockchain networks, claiming that the value distribution is reversed. The Fat Protocol Thesis argues that the protocol layer (layer 1s) capture most of the value while the application layer (dapps) a fraction of it, shaping a stack of fat protocol and thin application.

Then in what way do blockchains generate value differently from Web 2.0? The two drivers of the shift Joel Monegro states are as follows:

1) Shared Data Layer → Increased Competition at the Application Layer

Blockchains are accessible for anyone. They are decentralized networks that lower the barrier for entry. This leads to a competitive and vibrant ecosystem, and fees charged by dapps will likely converge to zero, citing better user experience and service. Eventually, the amount of value captured in applications is bound to shrink.

2) Token Incentives → Accelerated Growth of Protocols

Monegro argues that tokens native to a blockchain protocol as well as shared data layers boost the use of the services on the blockchain. In the earlier stage, tokens primarily incentivize research and service development, attracting investors, developers, and early adopters. Popular services then bring more users to the protocol and eventually end up raising the price of tokens, creating positive network effects.

2. Market Cap: Protocols → Applications

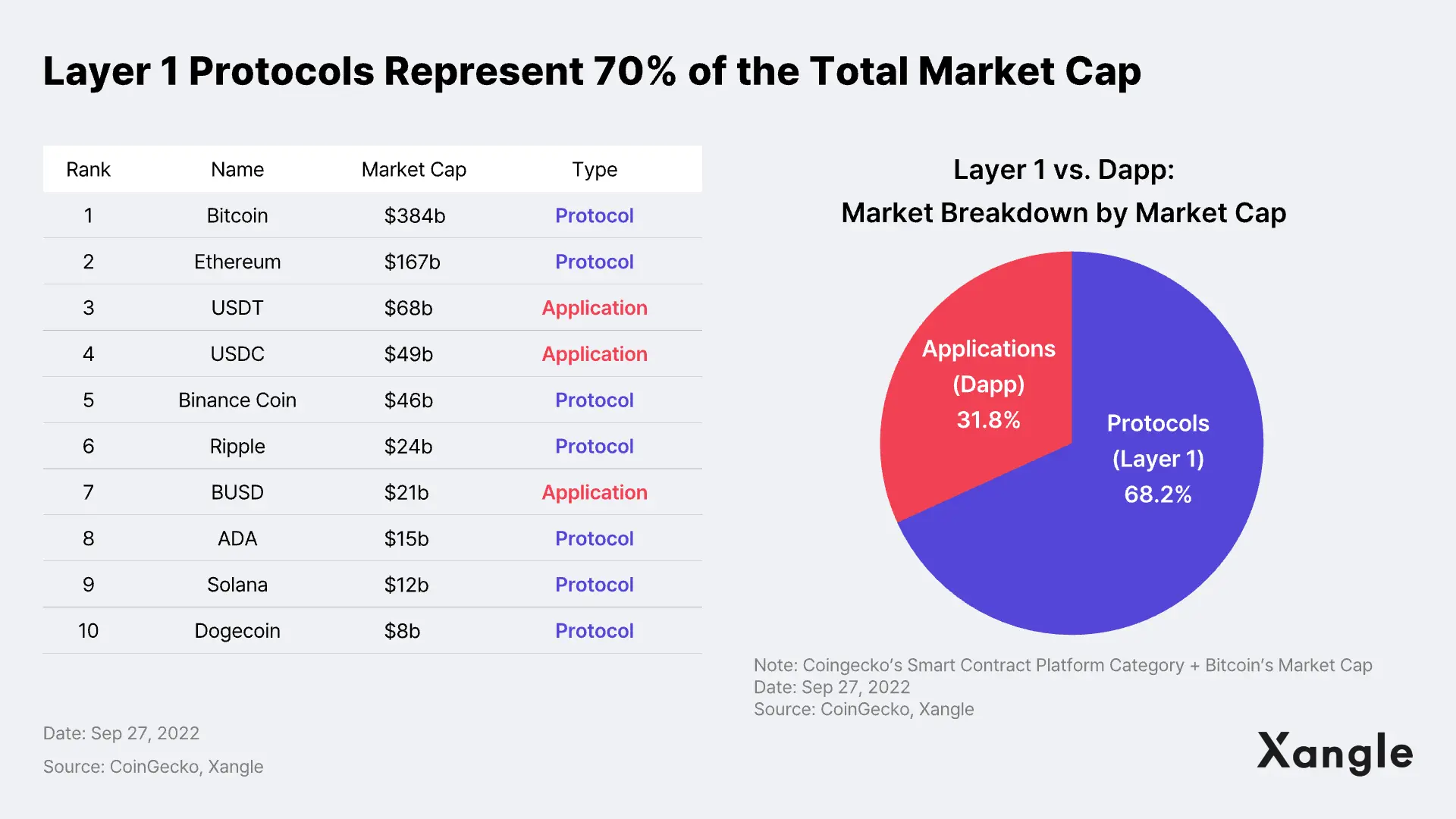

Six years on since the Fat Protocol Thesis was first introduced in 2016, the crypto industry is led by layer 1s, which are protocols. Except stablecoins, all the projects ranked in the top 10 by market cap are layer 1s. Indeed, the total market cap of layer 1 protocols—including Bitcoin and smart contract platforms—represents as much as 68% of the crypto market.

The high valuation of Aptos and Sui, the layer 1 blockchains built by former Meta developers, backs the Fat Protocol Thesis (For more details, check out Aptos vs. Sui Comparison: Similarities and Differences). The fact that the market and investors are assigning higher valuations to protocols than to applications suggests that they are seeing more value capture potential in protocols than in applications. Then how do protocols capture value?

3. Value Capture Process of Protocols

1) Transaction Fees

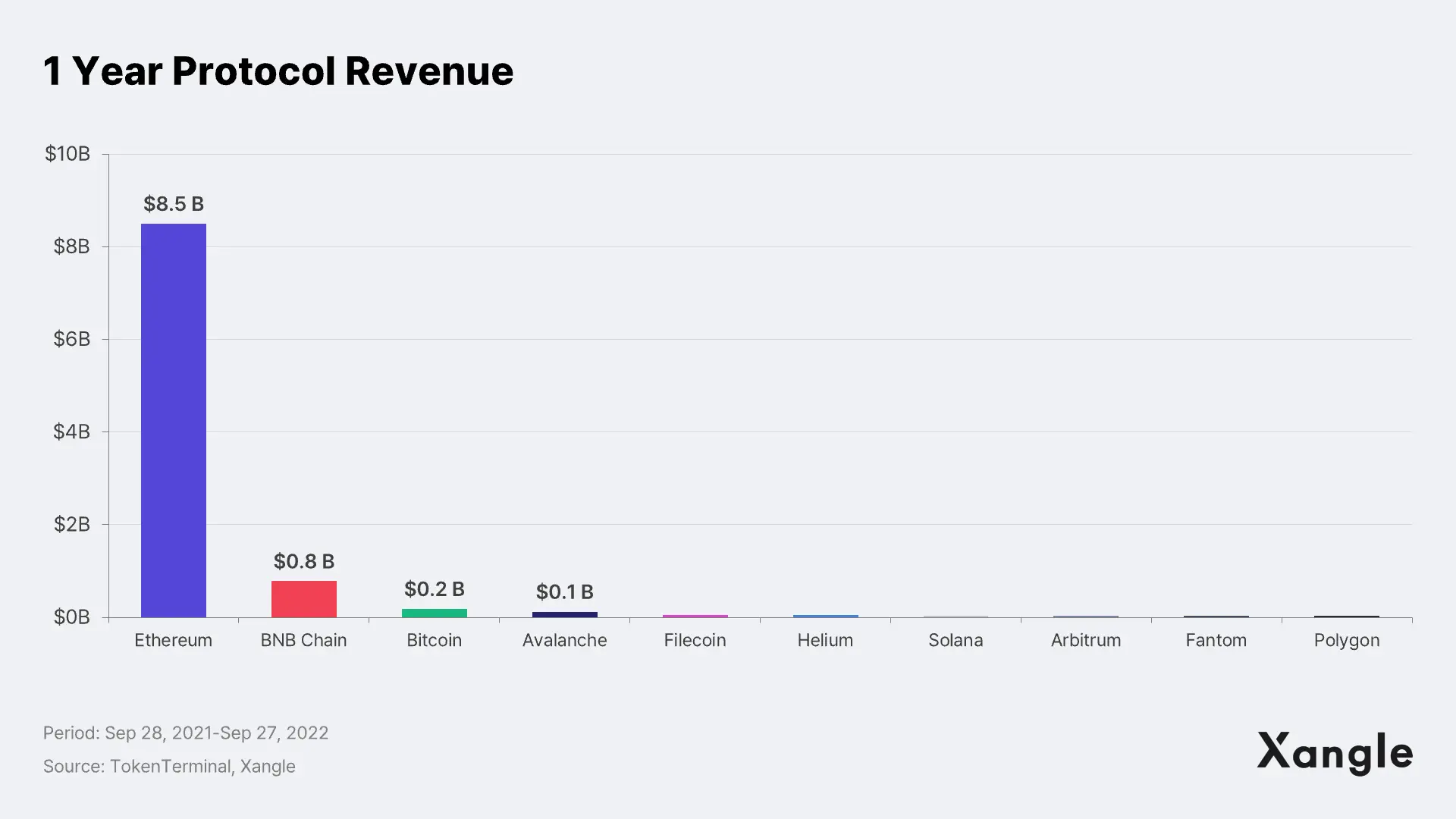

Most of the value captured by a protocol comes from transaction fees. Transaction costs are fees that blockchains charge users for certain activities on the chain. Transaction fees are then paid back to blockchain network and node operators, including validators. This way, protocols are virtually sharing their profits from fees with tokenholders, given that most layer 1s work under PoS consensus algorithms. In the case of Ethereum, the fee income for the past year reached a whopping $8.5B. The fees that used to be paid to miners before the Ethereum Merge are now paid to ETH stakers post-Merge. It is quite a clear-cut framework where users get to pay fees for using the blockchain protocol, and the fees charged on transactions on the chain are paid back to the tokenholders of the protocol.

2) Token Demand & Protocol Scalability Correlation

Other than transaction fees, token staking is another way of capturing values. Token staking is locking more than a certain amount of cryptocurrencies to help support the operation of a protocol (which is layer 1). Avalanche’s subnets, Polkadot’s parachain auctions are cases in point: users need to stake a certain amount of tokens to use Avalanche’s subnets, and Polkadot periodically launches parachain auctions to lease a parachain slot to the candidate with the highest bid. The architecture of both projects is designed to require more tokens to scale, which propels value accrual to the protocol layer. Since the first auction in Dec 2021, Polkadot has launched 28 parachain auctions so far, having 130M DOT (worth $827M) staked in the protocol.

Similarly, Cosmos, which supports app-specific blockchains, has just started to capture value with its native token ATOM. Addressing the long-held criticism of its tokenomics over ATOM’s inability to capture value, Cosmos released a roadmap along with the ATOM 2.0 Whitepaper on Sep 28. (For more details, check out ATOM 2.0 Whitepaper). According to the whitepaper, i) MEV revenues will flow back to the Cosmos treasury; ii) ATOM’s inflation rate will be brought down; and iii) ATOM and Cosmos appchain tokens will be mutually held—all in an effort to push up the value of ATOM. This draws a stark contrast to Web 2.0 protocols, which used to have no returns from applications.

The main points of the Fat Protocol Thesis discussed so far can be summarized as follows:

- Joel Monegro first proposed the Fat Protocol Thesis, arguing that, unlike Web 2.0, the Web 3.0 ecosystem would see value capture taking place in the protocol layer.

- By market cap, the value of protocols significantly dwarfs the value of applications, once again adding more legitimacy to the Fat Protocol Thesis.

- Transaction fees and token staking are the primary sources of value capture for protocols.

Obviously, there are opponents who refute the Fat Protocol Thesis and side with fat applications. The principal arguments of the Fat Application Thesis are: i) the poorer-than-expected network effect, ii) growing competition between protocols and not-so-profitable fees income, and iii) the rise of high-quality applications.

The gist of these arguments boils down to this: Web 3.0 will eventually move away from fat protocols and see value capture taking place in the application layer. Here’s a closer look at the theory.

4. The Fat Protocol Thesis Is Dead

Monegro came up with the idea of fat protocols, seeing protocols being disproportionately larger than applications. Back then, quality applications were virtually non-existent, not to mention DeFi, making it only natural that most of the value was captured in the protocol layer. This is best illustrated by projects, such as Litecoin and Stellar, which stirred up hype with narratives like “digital silver” and “cross-border payments platform.”

But the crypto market has gone through a series of transformations. First, there was a flood of next-gen smart contract platforms seeking to outperform Ethereum. Applications responded with the multi-chain strategy, which basically aims to support multiple blockchain protocols. Then there came tokenomics designed to capture value in application tokens, which indeed translated into sizable profits. This trend began to sap the legitimacy of the argument that the application layer captures little value in the Web 3.0 ecosystem.

1) Value Capture Becoming Harder for Layer 1 Protocols

As discussed earlier in this article, transaction fees are one of the primary sources of value capture for layer 1 protocols. But as was evident from the above chart, layer 1s’ fee revenue remains minuscule compared to its market cap. This is mostly attributable to low transaction fees. Protocols need to keep their gas fees at an appropriate level to secure enough value. These days, however, they are competing to keep their gas fees as low as possible in search of a larger user base. On Ethereum, the broad adoption of rollups and technological advancements will gradually translate into low gas fees. If the gas fee sinks too low, value capture becomes even harder for protocols—posing a dilemma for layer 1s.

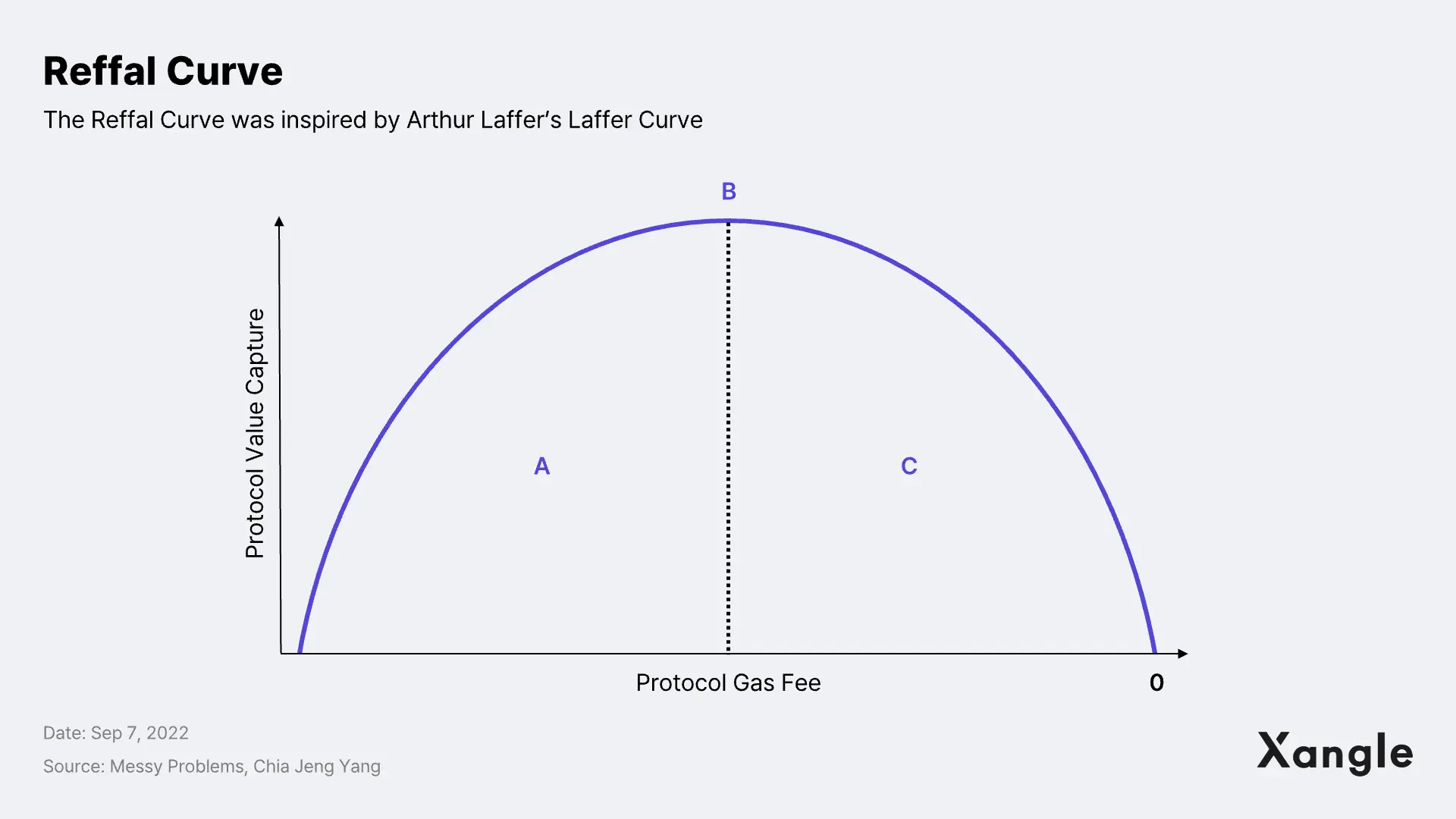

The Reffal Curve best describes this. Chia Jeng Yang describes the relation between protocol gas fees and value capture through this model citing economist Arthur Laffer, who proposed the Laffer Curve which is often brought up during discussions surrounding tax rates. Put simply, it claims that protocols can reap the most value at point B where the gas fee stands at a Goldilocks level.

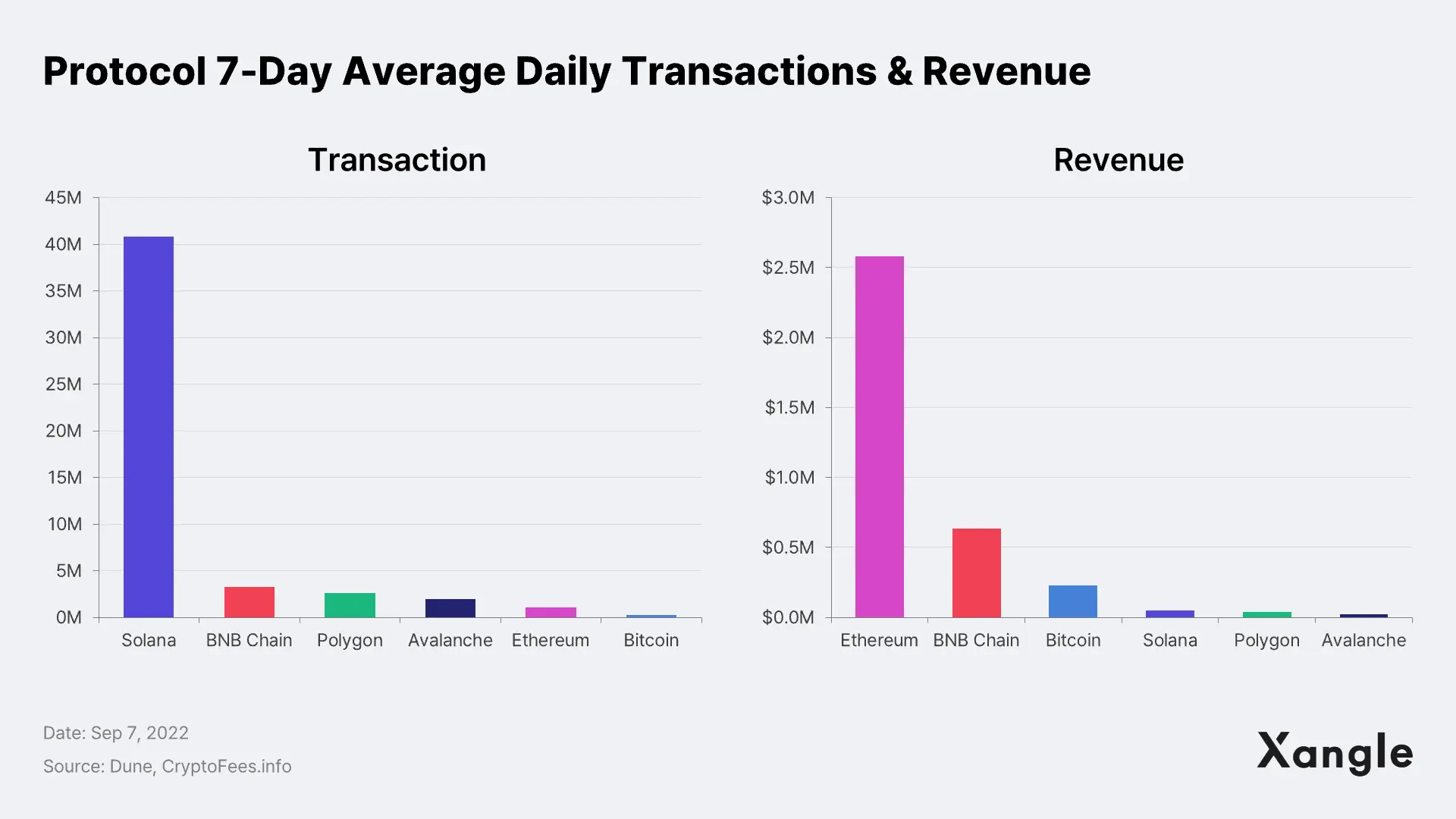

Comparing transactions and revenue between Ethereum and layer 1 protocols starkly illustrates the logic behind the Laffer Curve. On a daily basis, Ethereum raises an average of $2.6M in revenue while the number is $50,000 for Solana. Also on a daily basis, the 7-day average number of users on Ethereum is around 20,000, a ninth of Solana’s 180,000. This suggests that even with a radically larger user base and transaction volume, Solana’s revenue remains below 2% of Ethereum’s. This also goes the same for other protocols charging low fees—with revenues lagging far behind Ethereum despite a greater number of transactions.

Ethereum’s current gas fee may not be sustainable for the longer term. Yes, mass adoption of blockchain requires lower gas fees. But too low a gas fee may end up undermining the fees revenue, posing a risk to the sustainability of a protocol. Contraction of the fees revenue that incentivizes network participation may result in a decrease in the demand for validator nodes, jeopardizing the sustainability of the protocol. Protocols requiring high specification nodes, in particular, will find it even harder to secure validators once the rewards start to underperform.

2) Network Effect Lagging Behind Expectations

The multi-chain landscape has put applications at an advantage over protocols in terms of network effects. While the arrival of smart contract platforms, such as Solana, Avalanche, and Near Protocol, has fueled the competition between protocol layers, applications has fast expanded into other ecosystems by launching the same services on new protocols. Without cross-chain infrastructure like bridges, protocol layers are pretty much unable to bring users or liquidity from a disparate ecosystem—or even worse, a bridge could act against the interest of the protocol by posing material risks, just like the ones exposed in recent hacks.

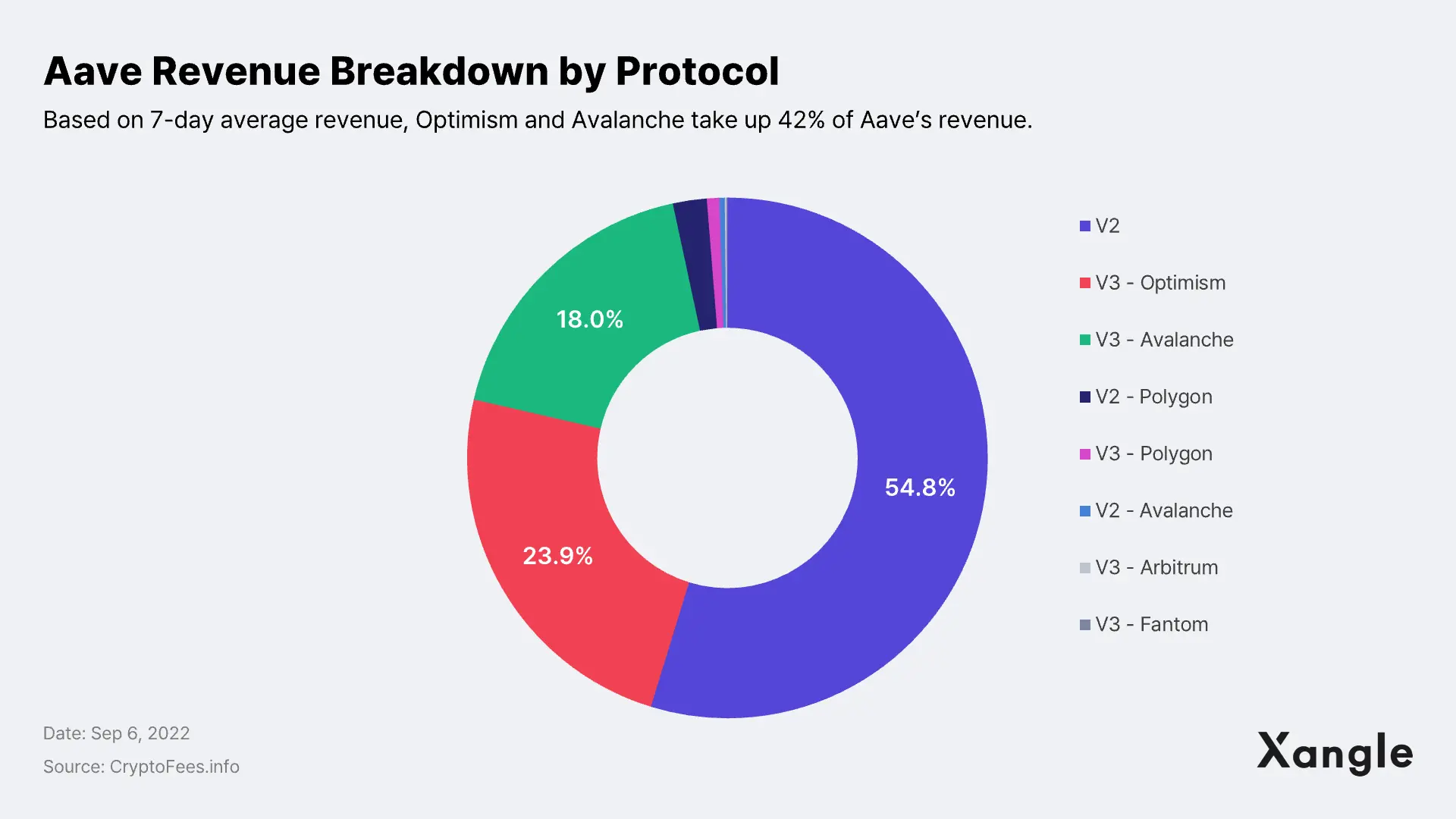

Looking at applications leveraging EVM compatibility to enter multiple protocols, many would feel that applications’ network effects make more sense. In Aave’s case, only 55% of the total revenue comes from Ethereum—with the rest being generated by highly EVM-compatible chains, such as Optimism and Avalanche. This pattern is found not just in Aave but in other applications as well, e.g., Uniswap, Curve, and SushiSwap.

Some are choosing to go even further, building appchains like dYdX, to achieve both scalability and value capture at once. Powered by the StarkEx engine, dYdX used to run an orderbook-style decentralized derivatives exchange, but has recently migrated to a Cosmos SDK-based appchain. Apparently, applications’ migration to other protocols is relatively easier whereas protocols will have to risk being kicked out of the roster once they fail to satisfy the demands of applications.

3) Applications Starting to Rake in Value

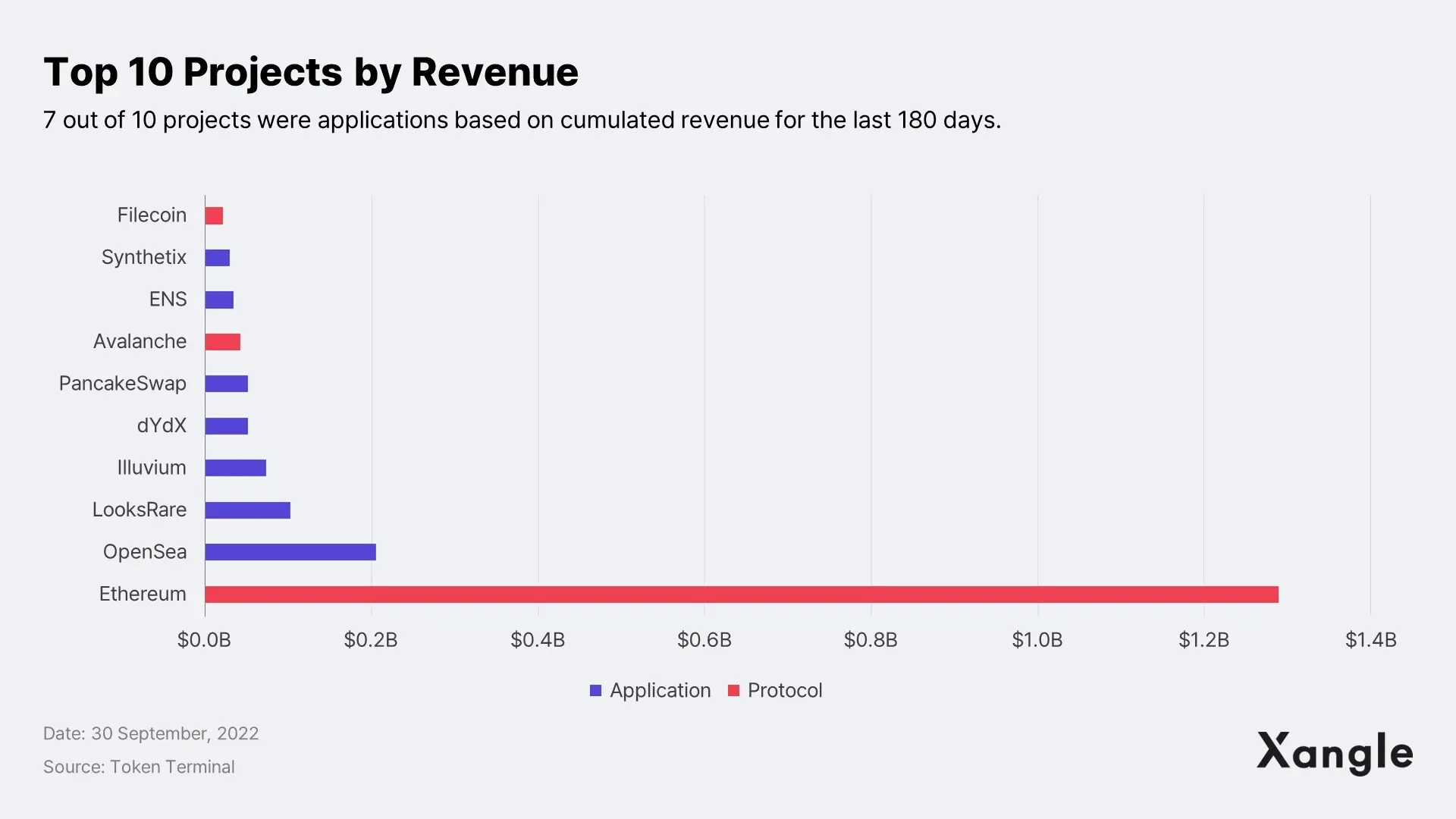

When protocols capture value by charging fees in exchange for blockchain infrastructure, applications can provide native services to drive revenue. As is obvious from the bar chart below listing the top 10 projects by revenue, competitive applications capture more value than protocols.

Based on the 180-day cumulative revenue as of Sep 30, 2022, seven of the top 10 biggest gainers are applications. Protocols may have to minimize or even eliminate gas fees to enable better user experience—and this may hold true for almost all protocols. Lower or zero fees will further erode the efficiency of value capture at the protocols layer, letting relatively more value concentrate at the application layer. Such diminishing gas fees and growing anticipation for killer dapps explain why fat applications are increasingly gaining ground.

5. Fat Protocol vs. Fat Application: A Topic Warranting Attention from Blockchain Business and Crypto Portfolio Perspectives

As discussed along with the Fat Protocol Thesis, the protocols layer still exhibits higher valuations. The mega success of Solana—a protocol often referred to as the alternative to Ethereum—touching a market cap of $100B after four years of launch, was particularly regarded as an epitome of layer 1’s potential. Avalanche, Cardano, and Polkadot also followed suit, valued at tens of billions of dollars. The question is: will value continue to concentrate at the protocol layer?

Although the topic has never been short of pros and cons, we have already learned from the developments that have unfolded throughout the history of Web 2.0 that a trend is constantly bucked—and this time, it may be in favor of fat applications. If applications do gain the upper hand and start capturing most of the value, just like they did in Web 2.0, considerations and approach will transform along—especially for blockchain businesses and crypto investors. For those who are mulling a blockchain business, launching the go-to multichain dapp or appchain may be a better option rather than building a layer 1 blockchain on their own. An application may be a better option for investors as well to potentially attract a larger user base and ultimately enable a better risk and return, given the intensifying competition in the layer 1 market.

The blockchain industry is still too nascent to predict the future landscape. The debate, however, is worth watching. In our next publication to follow up on the topic of fat protocols versus fat applications, we’ll discuss the requirements key to the success of an application and the ways to translate the success of an application into the growth of a protocol.

Other Related Research Articles

- What Constitutes a Mainnet? An In-Depth Look Inside the Building Blocks

- Aptos vs. Sui Comparison: Similarities and Differences

- Loot On StarkNet: ZK-Rollups Enter Blockchain Gaming

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Solana RWA: A Look at the Key Players](https://resource.xangle.io/files/content/F779A005246C0299246537AACB3A39F2_1782287059970.webp)