이선영

Research Analyst/

XangleTranslated by Rhea

1. Index-Based Financial Products in a Leading Position within the Global Stock Market

1-1. What is an Index?

1-2. The Index-Following Passive Fund Market on the Rise

1-3. Low Fees and High Liquidity Leading to Massive Expansion of the ETF Market

2. Why Crypto Index Market is Destined to Grow

2-1. A Need for Benchmark in the Crypto Asset Market as with the Stock Market

2-2. A Need for A Basket Investment with Relatively Low Volatility

2-3. Crypto Index-Based Products Expected to Show a Rapid Growth Once Brought into Regulated System

3. Major Crypto Index Players

3-1. Traditional Index Powerhouses Seeking to Be the First Mover in Benchmark Indices

3-2. Blockchain Projects Attracting Investors with Theme-Based Indices

3-3. Oracle Projects Essential in Launching Crypto Indices

4. Current Regulations on Crypto Indices

4-1. The U.S. Taking a Pause after Launching Bitcoin Futures ETF

4-2. Too Early to Discuss the Korean Market

5. In Conclusion

“The best way to own common stock is through an index fund […]. A low-cost index fund is the most sensible equity investment for the great majority of investors.” – Warren Buffett

An index refers to the stock price index, which shows the changes in the price of stocks. As indices quantify the performances of specific asset groups in a standardized manner, representative indices such as the S&P 500 in the United States and KOSPI 200 in South Korea are used as indicators for the economic flow of specific nations or industries.

The type of funds designed and operated to follow such indices are called index funds. These index funds opt for the strategy of following more stable “market returns” rather than taking on an aggressive management strategy seeking to gain excess earnings. VFIAX (Vanguard 500 Index Fund Admiral Shares) and FXAIX (Fidelity 500 Index Fund) are a few examples of more widely-known index funds tracking the S&P 500.

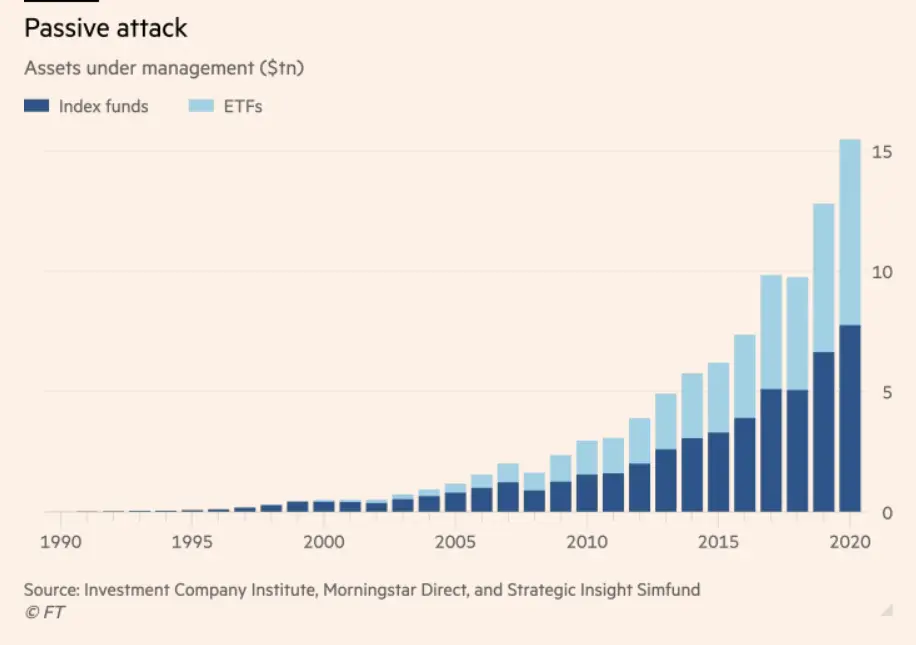

The size of the passive fund market is growing rapidly, with the number of assets in the global passive investment industry exceeding USD 15 trillion in 2019. Passive funds refer to the funds managed to seek the same returns as the benchmark index they follow. Included are index funds and ETFs (Exchange Traded Funds), which list indices on exchanges to allow for real-time trades in the same easy way that regular securities can.

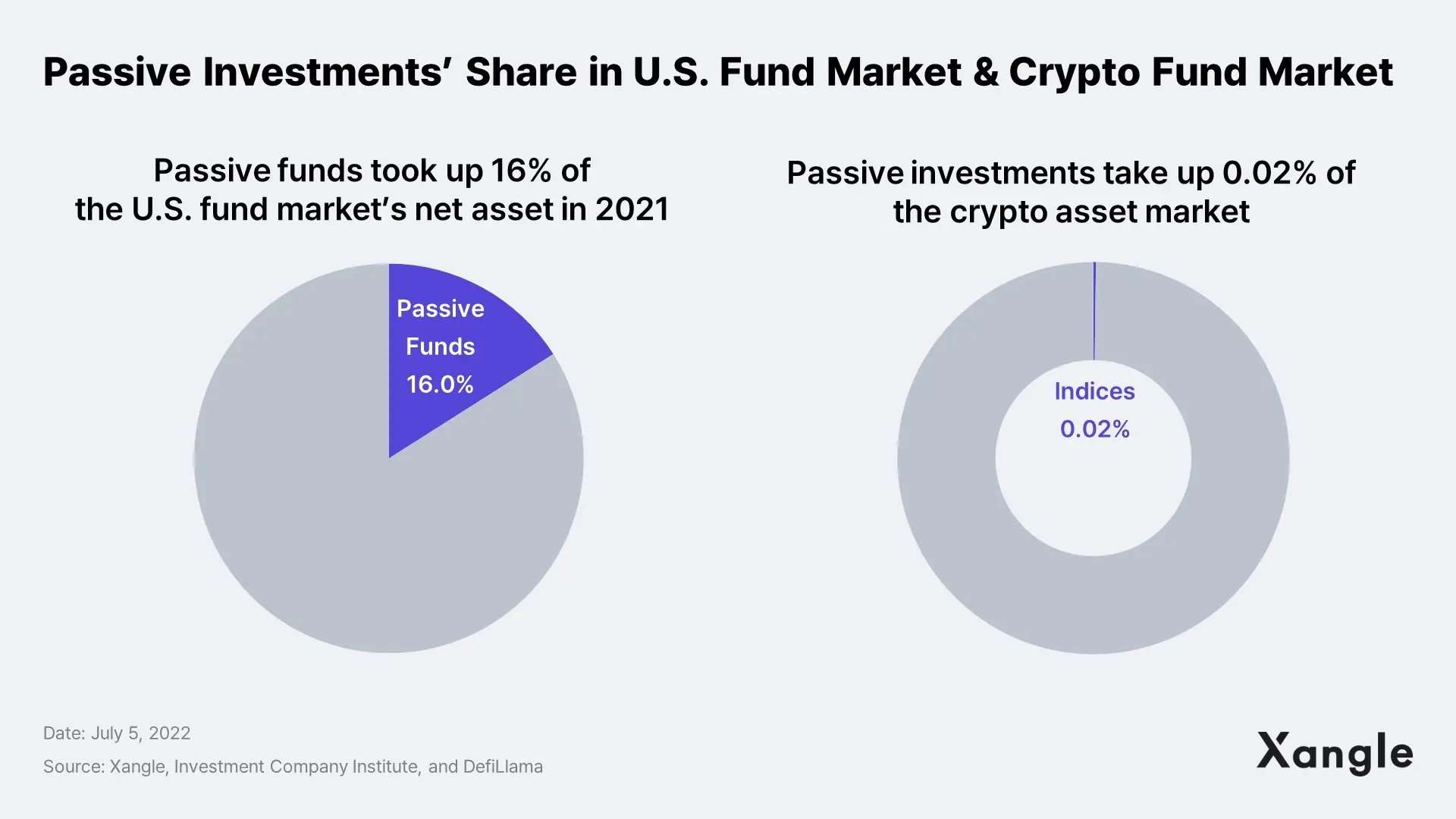

As of the end of 2021, passive funds overtook active funds, showing remarkable growth in their share in the U.S. stock market’s market cap from 8% in 2011 to 16% in 2021.

The three reasons below were behind such a growth spurt in the passive fund market.

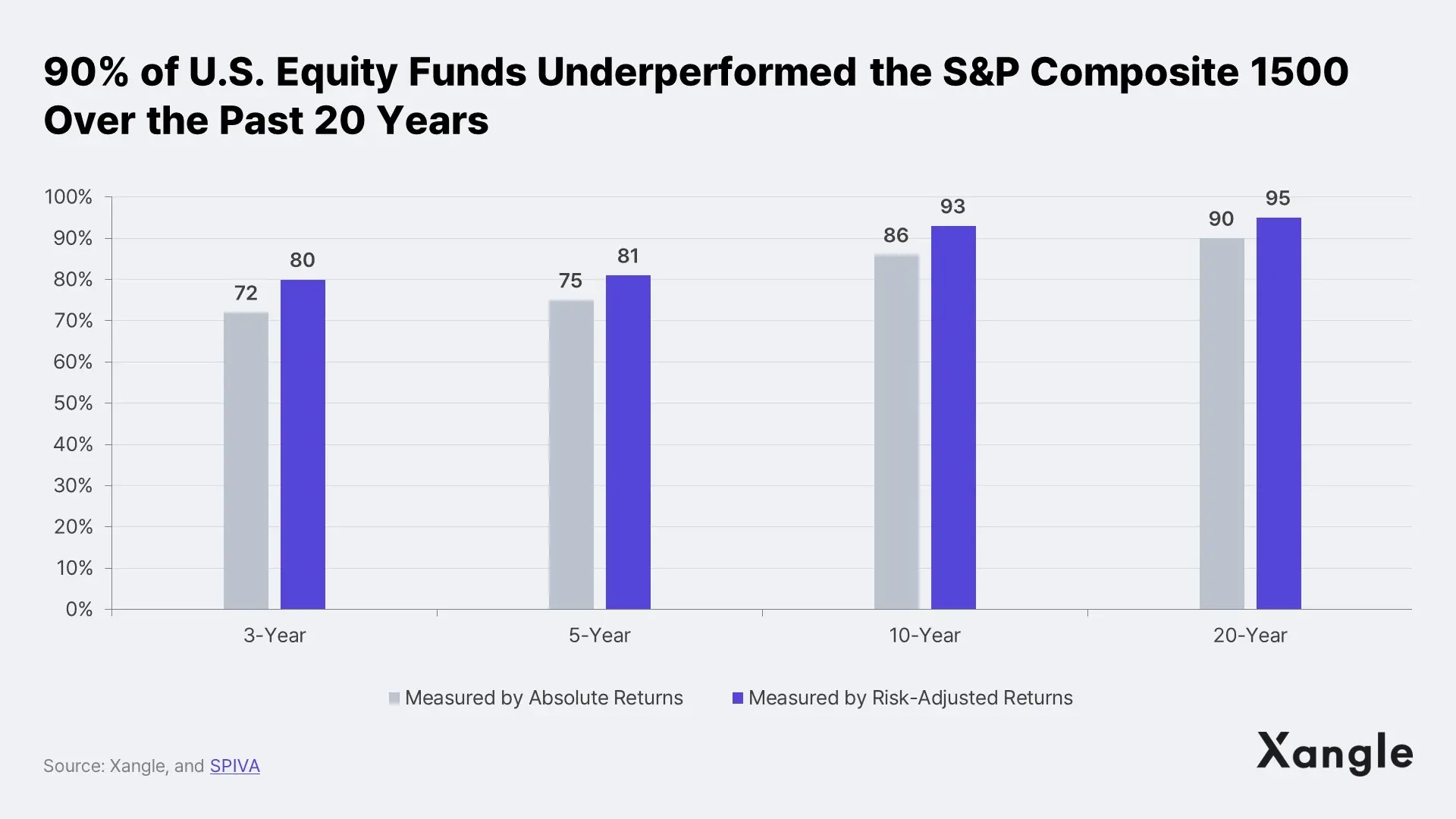

The first one of these factors seems to have had the biggest impact on the growth of the passive fund market, as evidenced by the fact that 90% of the equity funds for the past two decades performed below the S&P 500 Index.

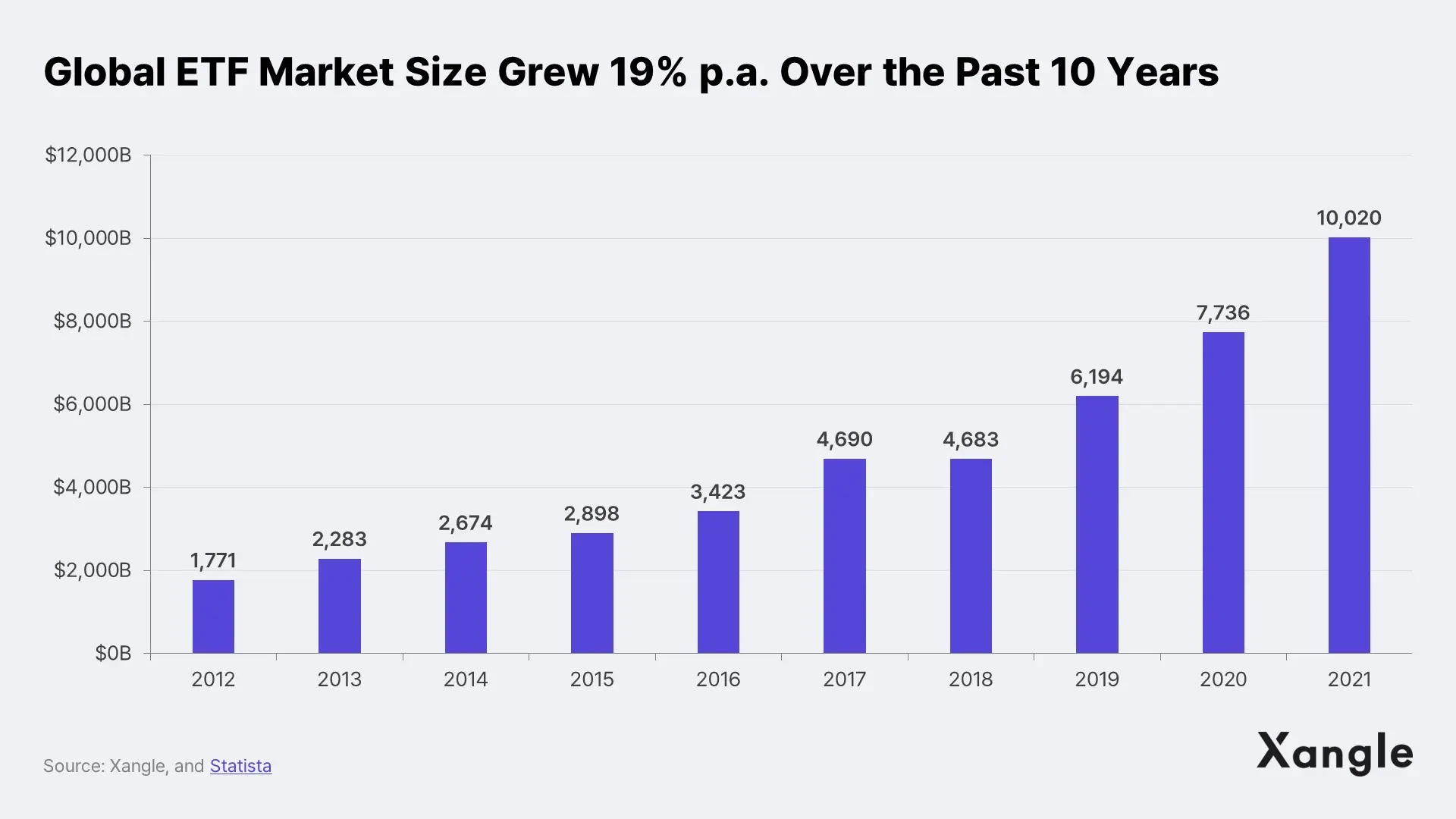

In particular, the ETF market expanded massively, thanks to the fact that these funds are listed on the exchanges and can be bought and sold in the market in the same manner as individual stock items. The global ETF market grew 19% per annum over the past decade, forming a market of USD 10 trillion as of 2021.

One of the most significant advantages of the ETF is its low cost. ETF’s fee is very low at around 0.2-0.4% when regular equity funds take 1-2% as rewards. The longer the investment period gets, the greater the impact the fund’s management cost has on its yield. At precisely such a point, ETF’s low fee can be a tremendous competitive edge.

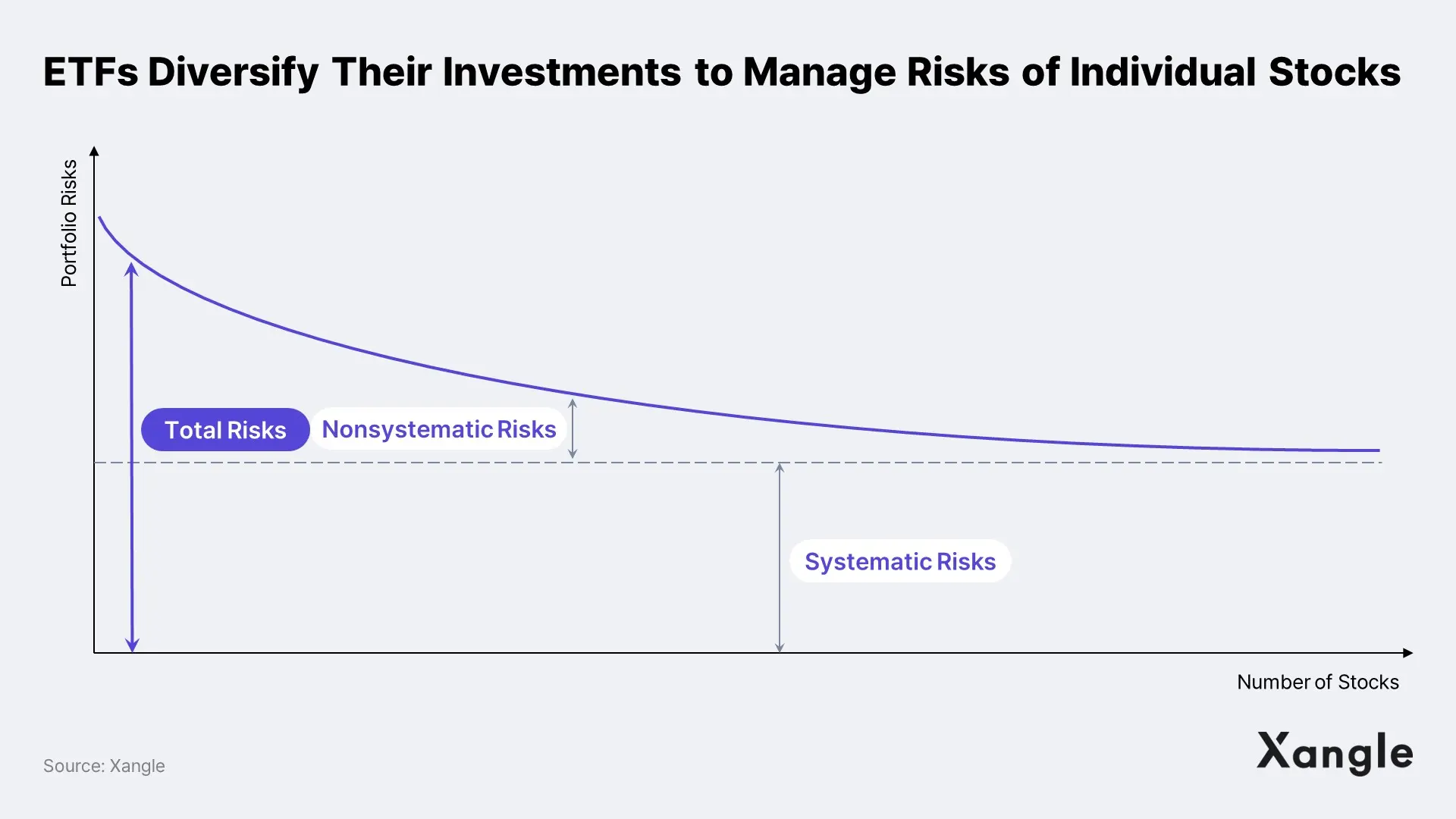

Moreover, ETFs only take on the market (index) risk, which is more systematic and less risky than the risks regular active funds generally bear. This translates into a minimal risk compared to investing in all of those companies individually. Such is achieved as the funds increase the number of stocks in their portfolios and offset and cancel out any dispersible risks each of the companies intrinsically holds.

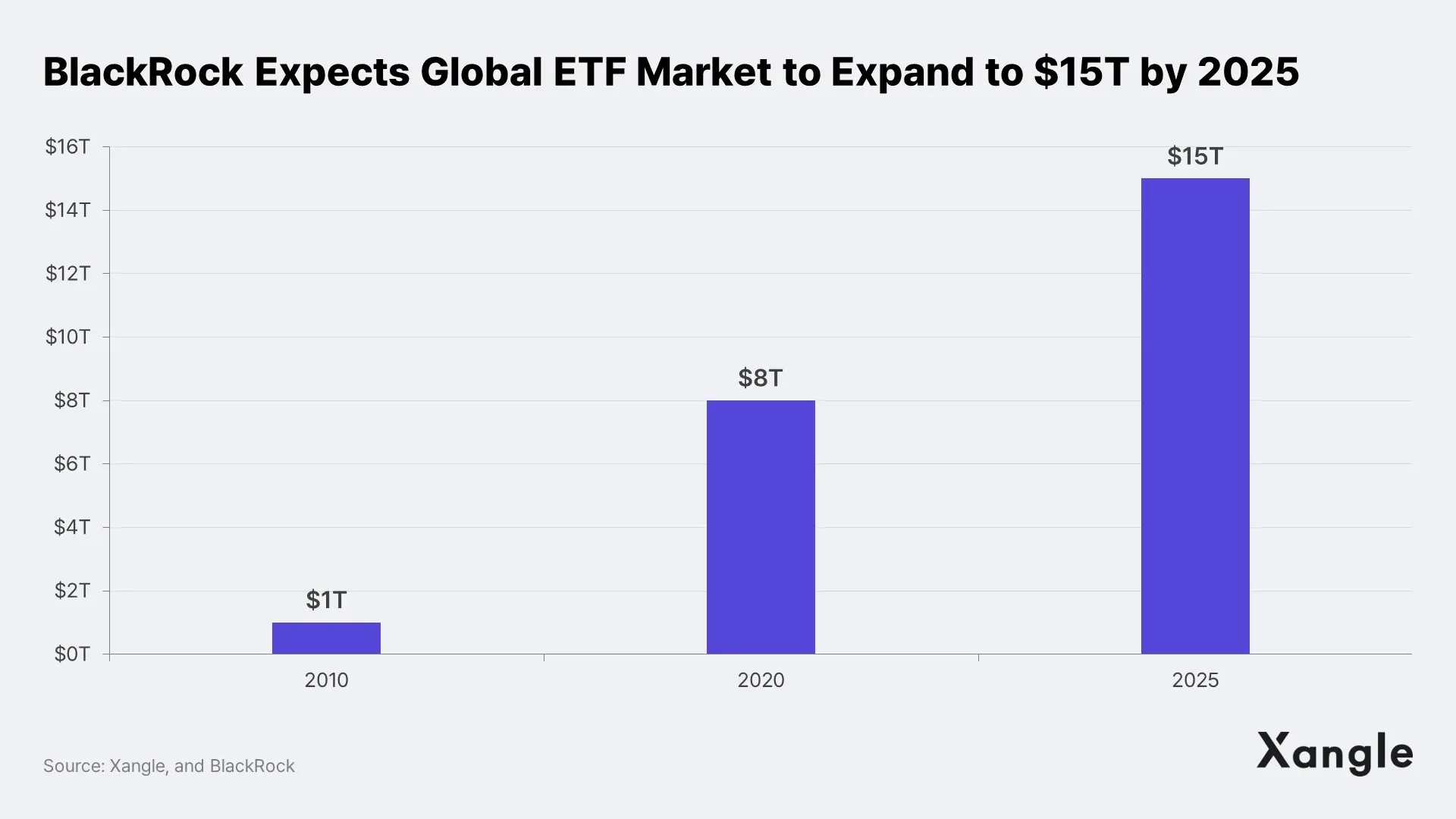

It looks like the ETF market will continue its growth in the future. BlackRock, the number one ETF trader in the United States, taking up about 34% of the U.S. market share (as of April 2022), estimated that the global ETF market will grow to reach USD 15 trillion by 2025. The passive funds market, including the ETFs, is also expected to continue its steady expansion.

Benchmark is an indicator that sets standards for evaluating investment performances. As such, it is vital to set an appropriate benchmark when investing. Previously, Bitcoin was used as the benchmark for crypto assets. However, as Bitcoin’s market dominance continues its steady fall, there is a need for a benchmark index that can also reflect the market performance of other altcoins.

<Source: Messari>

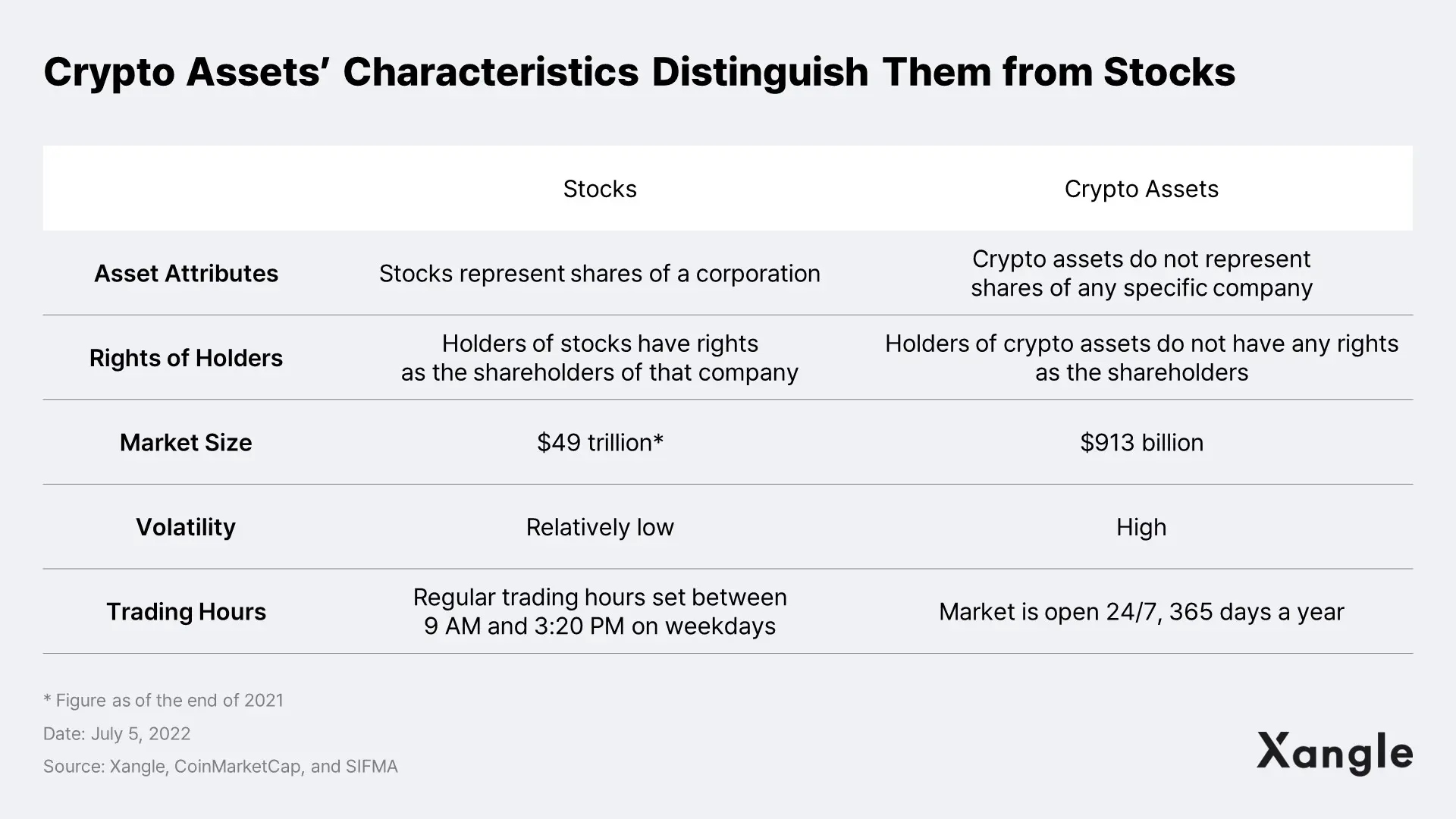

Furthermore, an appropriate benchmark will be able to provide novel and convenient investment opportunities for the investors seeking to allocate a portion of their portfolio to the overall crypto asset market. One thing to keep in mind is that the market is heavily disproportionate, with the market cap of Bitcoin and Ethereum combined taking up over 70% of the market. As such, the investors are in need of a benchmark index that has been appropriately designed to reflect the growth of the crypto asset market.

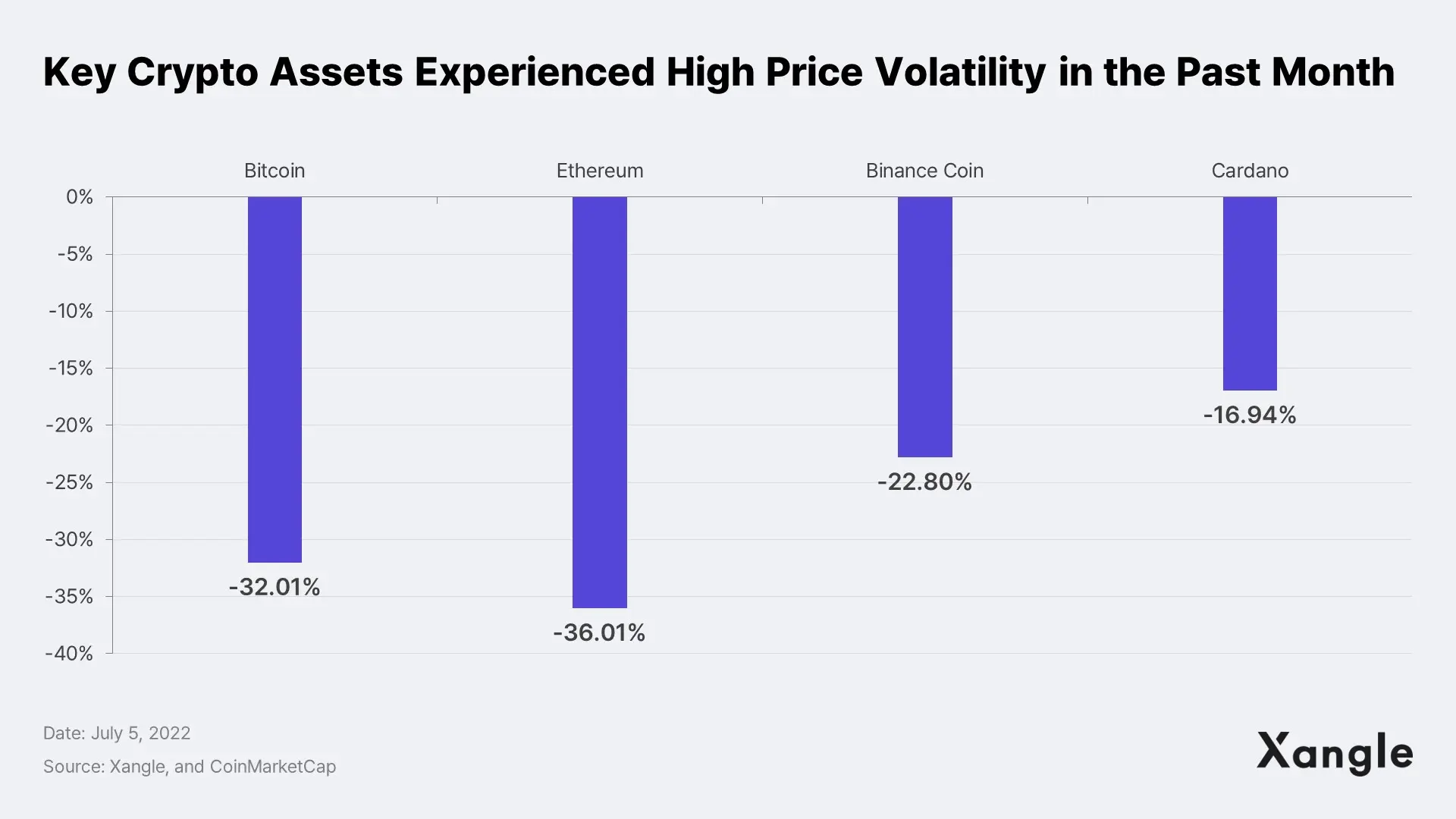

According to CoinMarketCap, the top 10 crypto assets in the market experienced high price volatility with over a 20% drop month-on-month. The price volatility of the crypto asset market is rather sizable since there is no artificial intervention such as government involvement to ease the volatility nor any means to measure the assets’ value. High price volatility is both an opportunity and a risk. There is a need for investment assets with relatively low volatility for investors who are sensitive to risks.

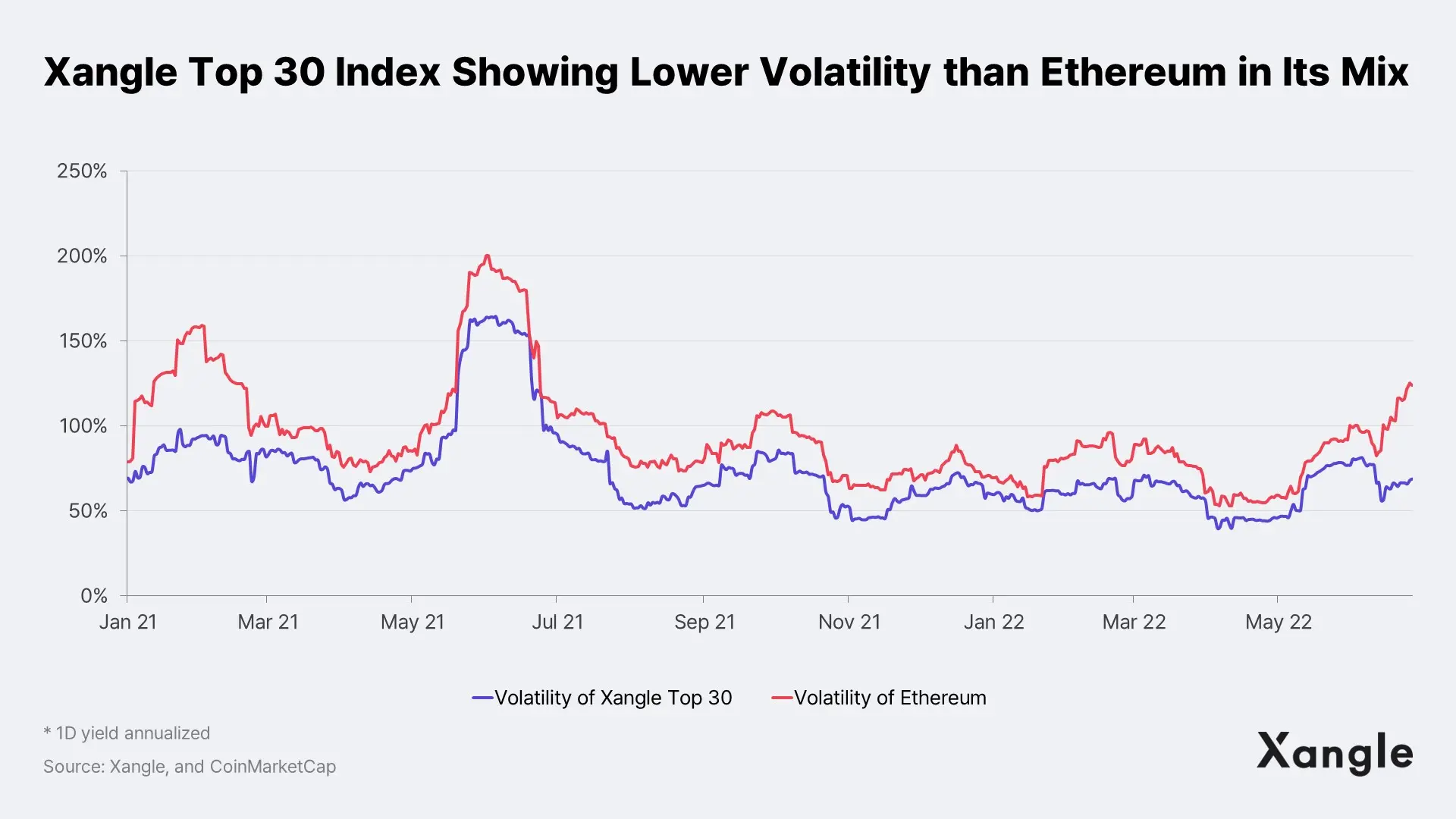

In such a situation, an index can be a good alternative. As shown in the graph below, the volatility of a crypto index is lower than that of the individual assets comprising that index. The Xangle Top 30, Xangle’s benchmark index that tracks the market cap of the top 30 assets, has shown lower volatility than Ethereum in all the different time periods from 2021 and onward.

With the total market cap of the overall crypto asset market estimated at USD 894 billion (as of June 29, 2022; source: CoinMarketCap) and crypto assets gaining more and more recognition, institutional investors are showing a growing interest in taking on crypto assets into their portfolio. However, the current environment does not allow institutional investors to buy crypto assets in baskets, only offering limited access to position themselves in Bitcoins, even which is further limited to futures ETFs.

If crypto assets were to be brought in as one of the recognized asset groups in the system in the future, it is expected that they will be managed in a similar manner as the stock market practice. If so, index-based products are expected to be actively launched, and the size of the passive fund market, including ETFs like the stock market, will also expand. Although the market cap of the crypto asset ETFs remains at a mere 0.3% now, it is expected to outpace the growth of the crypto asset market with 1) the influx of institutional investors upon deregulations and 2) active investment into DeFi indices.

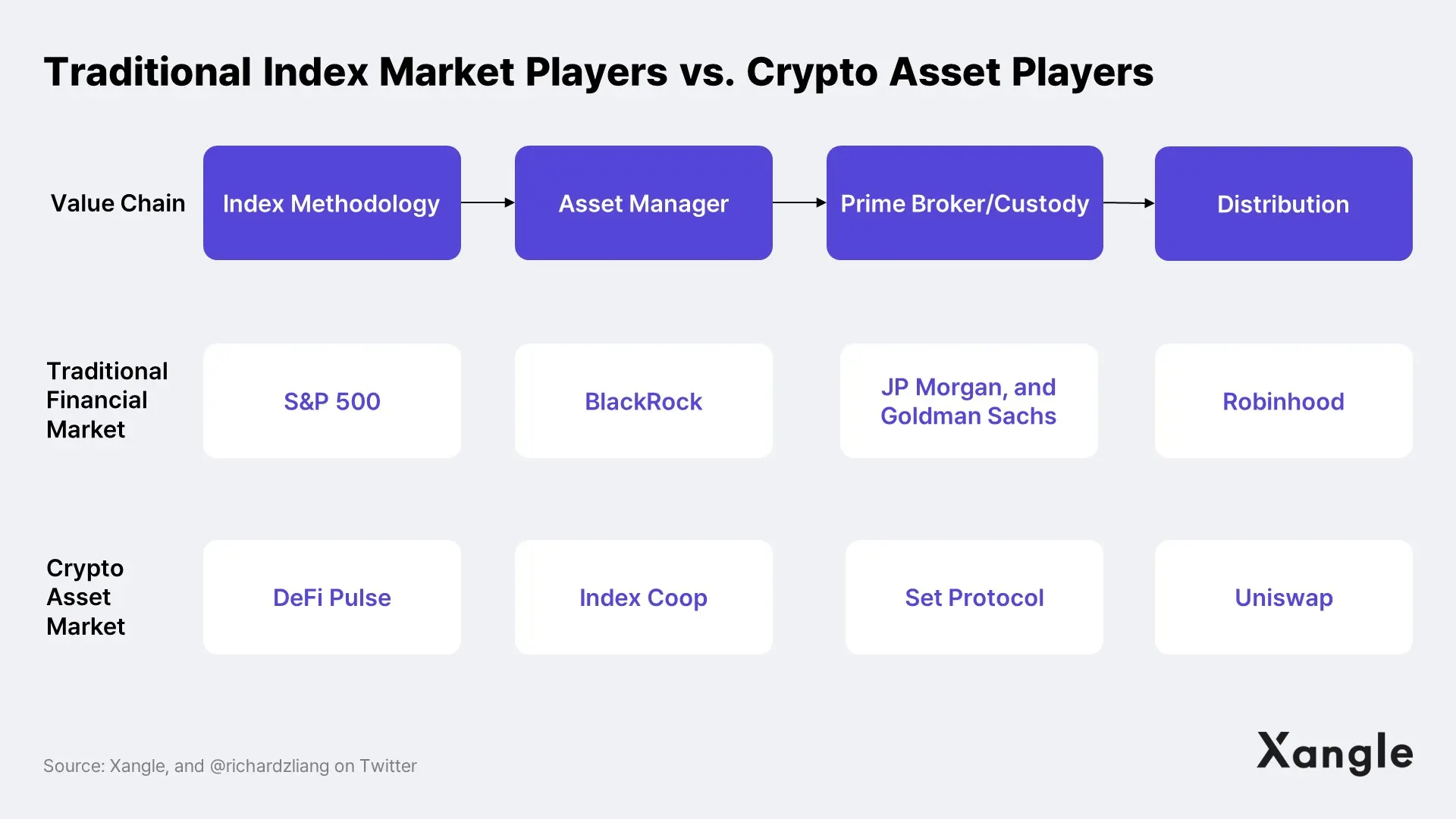

Having confirmed the potential for the rapid growth of the crypto asset index market, traditional index traders and blockchain projects are both launching different crypto index products.

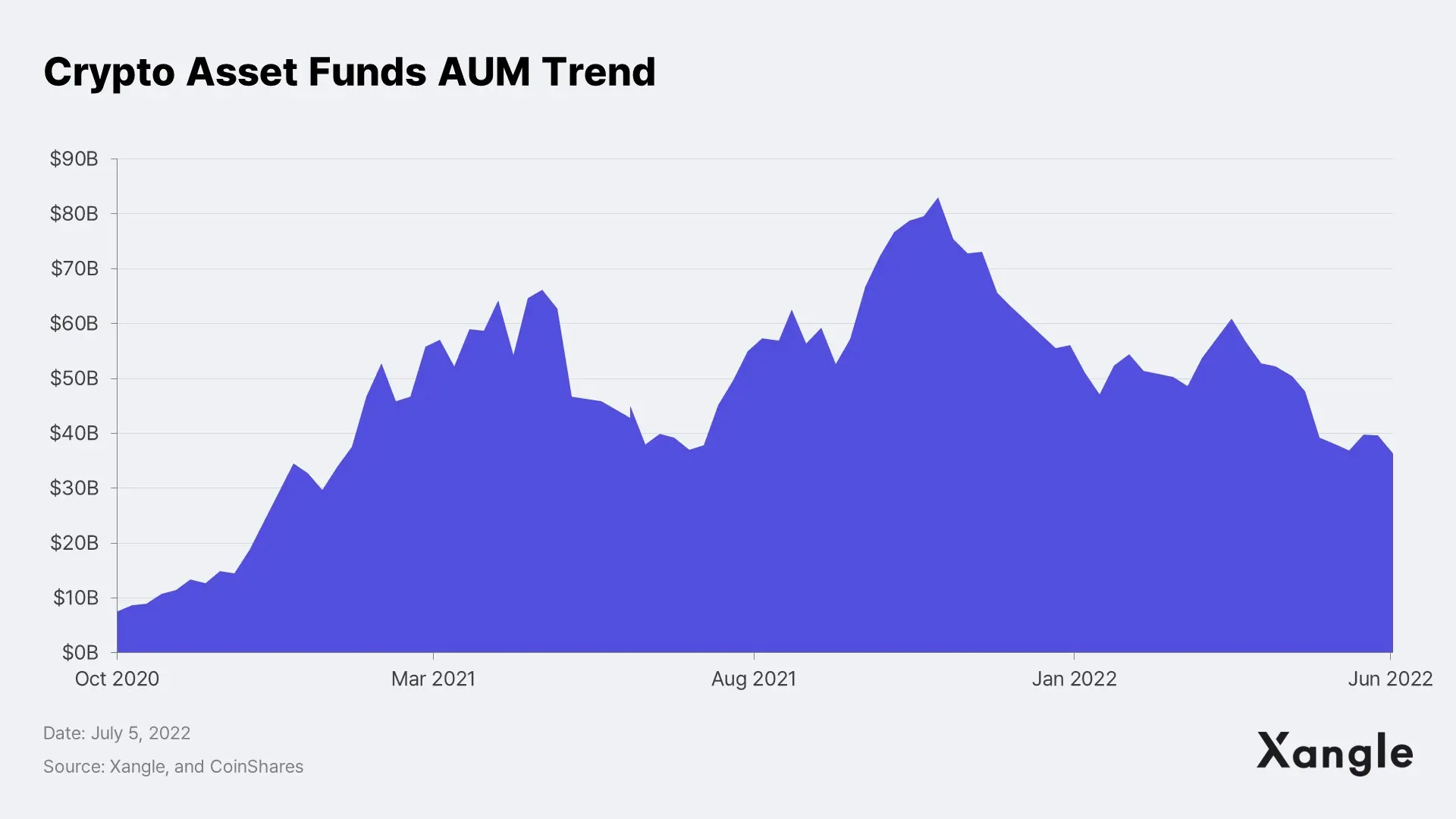

Following the changes in the market participants’ attitude toward digital assets and the growing interest by investors, traditional index players are also joining in to launch their own crypto indices. In particular, as the size of the crypto asset fund expands markedly, with its peak point reaching USD 80 billion, the interest in the index business is also heightened.

Index players took their first steps by creating the lead benchmark indices used in the crypto asset market and are now working on laying the foundation to make a new money pipeline in the new market.

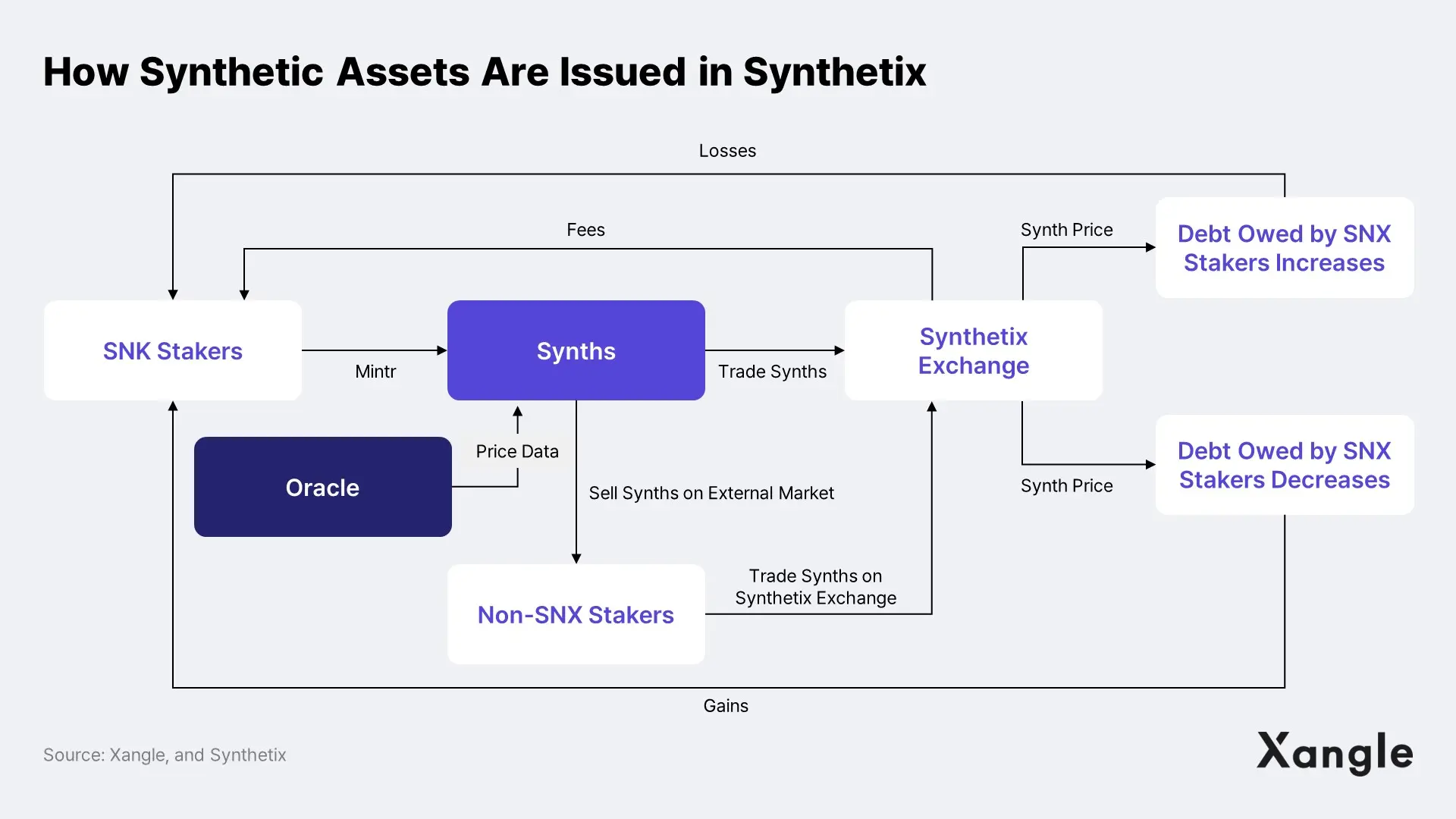

Unlike the traditional index players seeking to take an early position for the benchmark index, blockchain projects are launching products based on themed indices with a high investment attractiveness. Synthetix, a synthetic asset protocol, launched a DeFi-related index (which has been stopped for now), and Index Coop launched theme-based indices related to DeFi, metaverse, and Web3.

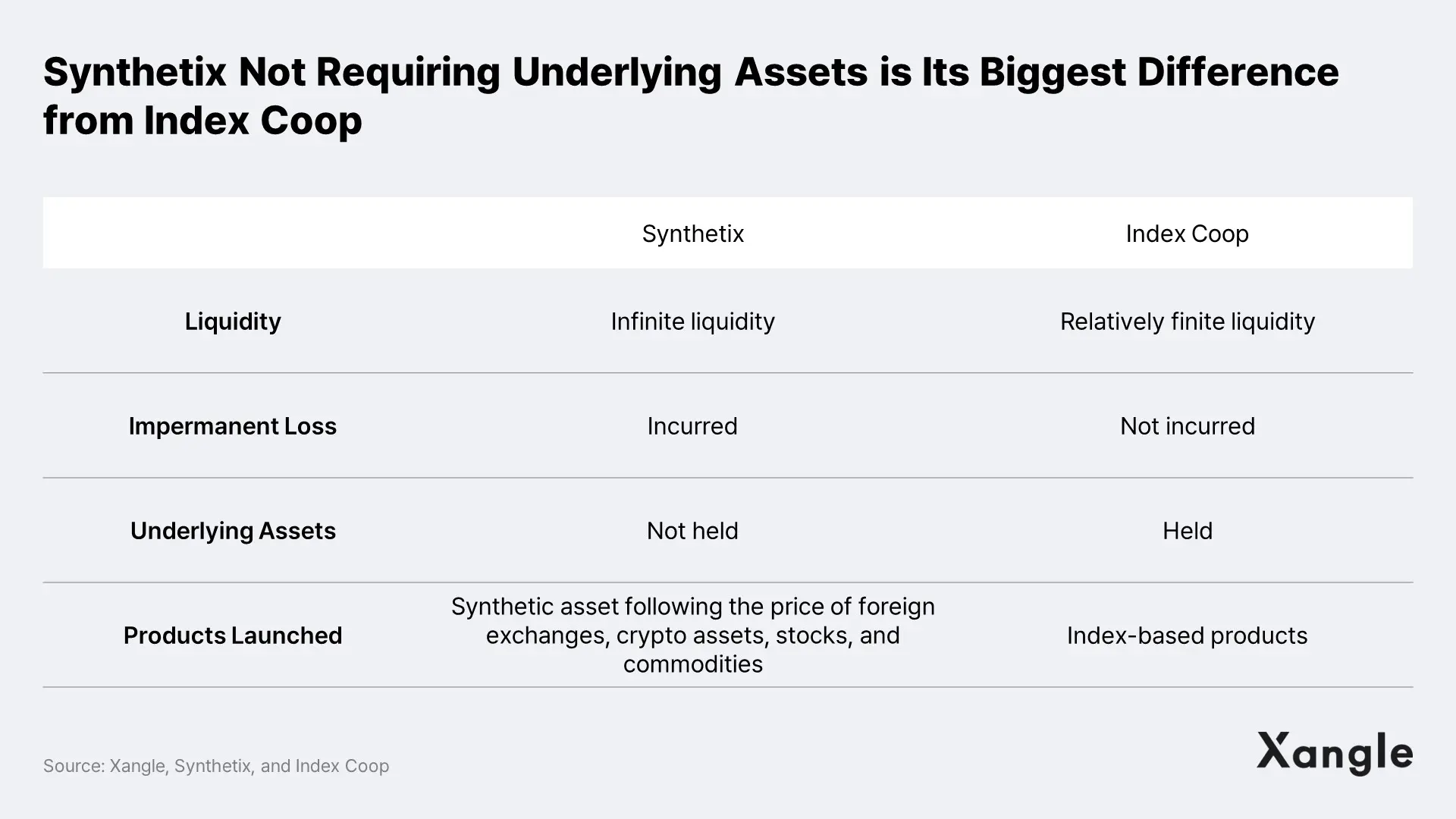

The biggest difference between Synthetix and Index Coop is that the synthetic assets in Synthetix can be issued without being required to hold any underlying assets.

Synthetix is a “decentralized” platform that issues Ethereum-based synthetic assets. Synthetic assets refer to products that provide returns by making investments in only tracking the prices of assets without requiring the asset holder to purchase the actual stocks of the underlying assets. In the traditional financial system, the investors had to use different platforms for investing in different types of products such as stocks, foreign exchanges, commodities, cryptocurrency, and indices. However, with Synthetix, the investors are able to trade all of these products in one place.

On Synthetix, SNX tokens can be put up as collateral to issue Synths. This provides nearly infinite liquidity and does not incur any slippage – the inability to execute an order at the desired price – which has been pointed out as the weakness of the traditional financial market.

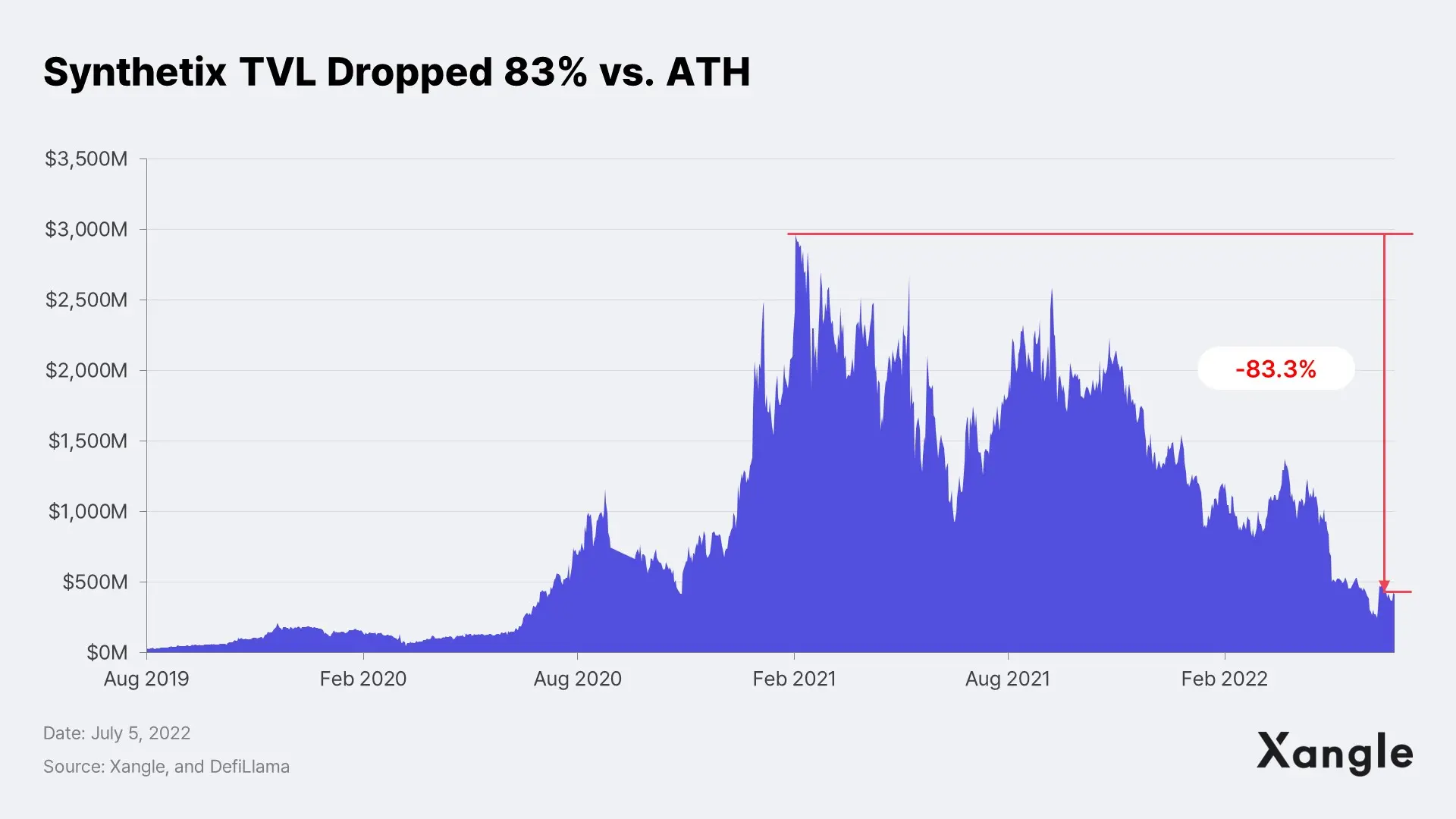

Based on the competitive edge it bears from having such convenience and the high SNX token collateralization ratio required to issue Synths, Synthetix’s TVL has grown rapidly since its launch in 2019. Moreover, Synthetix enjoyed the limelight until H1 2021 by providing over 40 synthetic assets, including sJPY, sOIL, sTSLA, and sCOIN, recording a high TVL of USD 2 billion at one time.

However, when the United States Securities and Exchange Commission (SEC) mentioned potential regulations on security tokens, Uniswap delisted over 100 security tokens from its interface, which included many of the synthetic assets from Synthetix. Shortly after Uniswap’s delisting, Synthetix also passed a governance proposal to stop all the support for synthetic assets involving stock and commodities, with their low liquidity as the reason.

Currently, the only synthetic assets available are on foreign exchanges and crypto assets; however, they lack the appeal to attract investors compared to synthetic assets based on commodities or stocks because they cannot be exchanged for their underlying assets. After Synthetix stopped supporting these massive amounts of synthetic assets, its TVL dropped sharply.

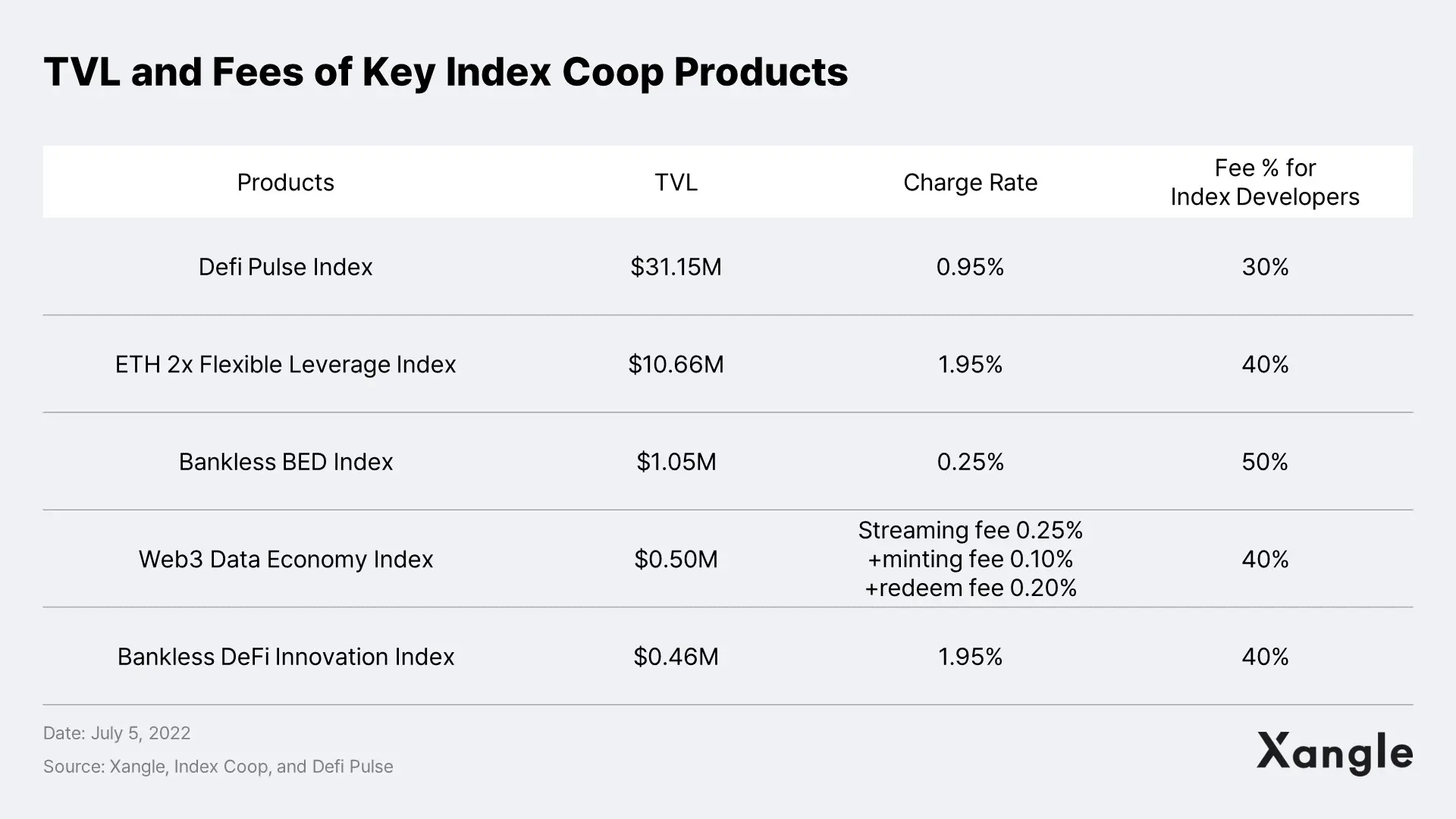

Index Coop is a representative crypto index project where crypto asset indices are formed and operated by decentralized organizations that hold INDEX tokens, such as DeFi Pulse, a DeFi data player, and Set Labs, a team of engineers.

Unlike the traditional index players targeting benchmark indices, Index Coop is launching other indices, such as theme-based indices, sector-based indices, and leveraged indices, and helping investors to gain easy market exposures from these themes and sectors.

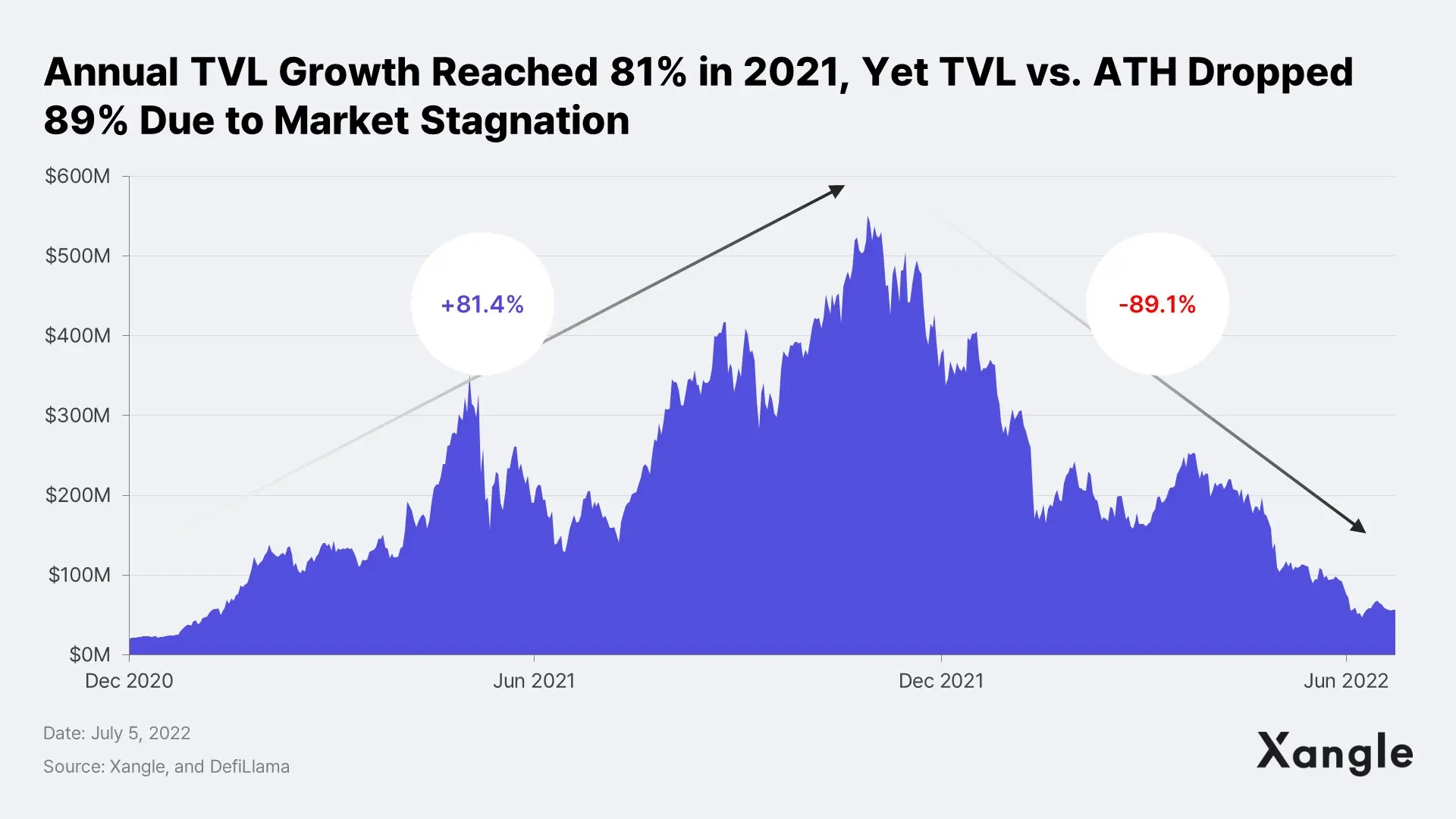

Having launched indices in various themes, Index Coop enjoyed a huge TVL growth and even received about USD 10 million in investment from the widely-recognized venture capitals such as Galaxy Digital and Sequoia Capital over the past year. However, with the underlying asset prices falling in this stagnant market, AUM has also taken a nosedive.

Index Coop is currently issuing key index tokens in collaboration with Set Protocol. Investors can issue the index tokens themselves via Index Coop or purchase them through DEXs.

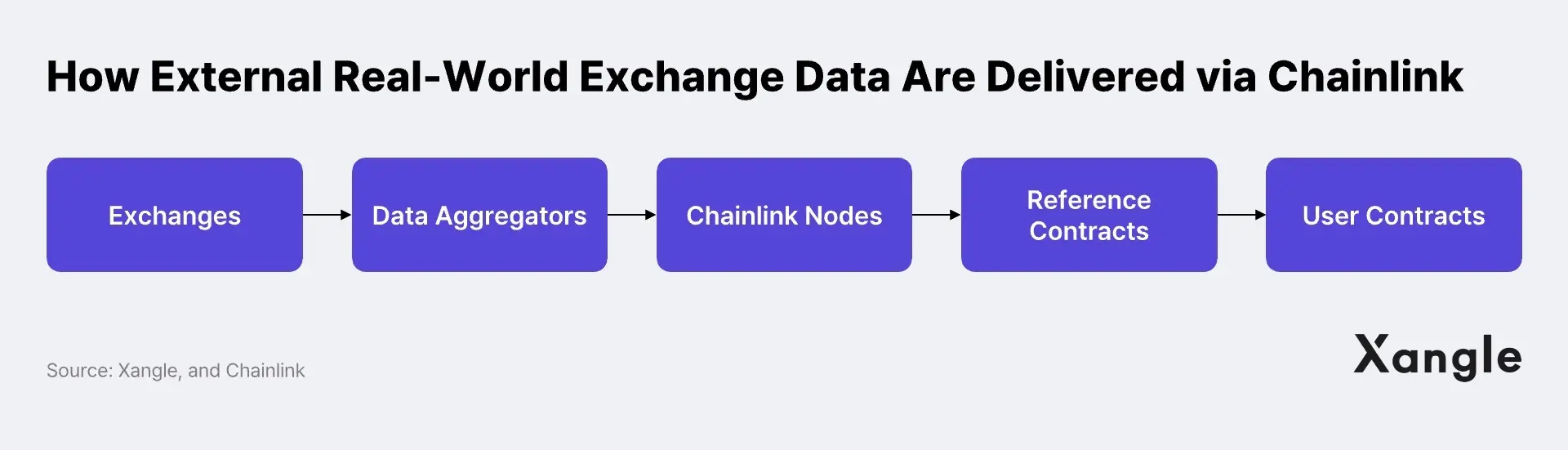

Blockchain projects use oracles such as the Chainlink and custody projects such as the Set Protocol when launching crypto-based indices. Oracles are projects that bring real-world data onto blockchains. DeFi projects mainly use Chainlink’s price data oracles when calculating their indices, and Chainlink’s oracles are structured as below.

Chainlink verifies off-chain data by 1) aggregating external real-world exchange data required for the DeFi applications, 2) aggregating data obtained from independent Chainlink nodes, and 3) organizing such data gathered in an off-chain oracle report to enable usage by smart contracts.

As explored earlier, there is currently no regulation on launching crypto indices, and even the traditional players are entering the market by launching their own crypto indices. However, ETFs are fund products and are regulated as such. Such a roadblock is clearly illustrated in how there is no ETF based on crypto assets in the U. S. as of yet due to the issue with the SEC approval.

On the other hand, Canada and Europe have recognized crypto assets as financial assets and enabled investors to make their investments under the safety of government regulations, making way for Bitcoin-based spot ETFs being launched.

In the United States, with the first ever Bitcoin futures ETF launched last October, the door was opened to invest in Bitcoins within the regulated system, and a foundation was set up to expand the investor base. Although the Bitcoin futures ETFs have structural limitations, such as the price gap with the spot and the burden of the roll-over (extension after maturity) cost, they are deemed to have served as a momentum that increased access for individual and institutional investors to invest in Bitcoin, as well as market transparency.

Moreover, given how the fees charged for Bitcoin investment trusts offered by Grayscale in U.S. and Bitcoin ETFs in Europe and Canada are around 2%, the Bitcoin futures ETFs are deemed to have successfully maintained their low cost, which is the advantage of ETFs.

It is a whole different story for the spot Bitcoin ETFs, which will have the biggest impact on the institutional investment capital and the crypto assets’ adoption into the system. The approval for their circulation still has not been obtained since the application seeking approval from the U.S. SEC was rejected last November. The SEC’s concerns about launching spot Bitcoin ETFs are as follows:

The approval request for Grayscale’s Bitcoin EFT was recently rejected because “[Grayscale’s] application failed to answer the SEC’s questions about preventing market manipulation, as well as other concerns.” Anticipation for the spot ETF approval grew further as the SEC passed the Bitcoin futures ETF by Teucrium, an ETF-focused fund manager, under the Securities Act of 1933 and the Securities Exchange Act of 1934, rather than the Investment Company Act of 1940. However, such anticipation has not borne any fruit so far.

In the Korean market, entities such as Xangle, the crypto exchanges, and Wavebridge have launched crypto indices. Among these, Xangle launched the Xangle Crypto Top 30, which can be construed as a benchmark index for the crypto asset market, and three other theme-based indices, Xangle DeFi, Xangle NFT, and Xangle Korean Crypto.

However, the index-based ETFs cannot be launched for now because the relevant laws still have not been established yet. Since ETFs are financial products, they can be traded only after getting the stamp of approval from the Korean Exchange’s listing eligibility review, much like any other regular securities. At the moment, it is hard to tell whether Bitcoin ETF products will be able to obtain such confirmation from the Korean Exchange.

On the other hand, Wavebridge, a Korean startup, is seeking to operate its crypto index business by establishing an asset management company in the home of Exchange Traded Funds (ETFs), the United States. Wavebridge plans to obtain the U.S. SEC approval to establish and incorporate an asset manager and list four to five ETFs in the U.S. stock market within the year.

Having witnessed the rapid growth of the crypto asset market, traditional index players and blockchain projects are both seeking to make an early move into the market and take an advantageous position by launching benchmark indices and theme-based indices, respectively. However, many obstacles remain for the crypto index market to be actively take-off since index financial products need government-level decisions to be launched, as illustrated in the U.S. SEC’s recent rejection of Grayscale’s spot Bitcoin ETF application.

However, since many companies have already started waging full-fledged entry into the crypto asset market, crypto asset-related regulations are expected to follow the practice of the market in the end. Unlike the stock market, the crypto index market is a very small market that currently takes up only 0.02% of the crypto asset market. However, in the future, when the crypto indices are brought into the scope of crypto asset regulations, and demand for passive investment grows further, it will be recognized as another form of many investment behaviors. Anticipations are riding high for the strong growth of the crypto index market.