A Check on Tether (USDT) and the Bank Run Risk

[Xangle Originals]

Written by RoHu

Translated by Rhea

A Check on Tether (USDT) and the Bank Run Risk

Summary

- The key risks with Tether’s stablecoin, USDT, are the possibility of devaluation of its collaterals and a potential bank run from sudden and massive repurchase requests.

- Due to continued allegations against its coin, Tether disclosed the breakdown of its collaterals last March, which showed that the bank run risk is limited.

- However, Tether still needs to overcome the challenges brought on by the suspicion claiming that it made structured products and derivatives with its assets, limiting their liquidity, and the lack of trust in the financial firm that performed the audit on data Tether disclosed.

- If the distrust in Tether were to continue regardless of its fundamentals, a run on the bank is a very real possibility in case of any market shock. More time is needed to conduct sufficient stress tests on Tether.

Since the collapse of Terra’s algorithmic stablecoin, UST, concerns are rising about yet another stablecoin, USDT. USDT, or Tether, is already experiencing difficulties recovering its peg to USD 1 (remaining at $0.999), with about $10 billion in repurchases incurred. Against this backdrop, this article seeks to explore the potential risks of this stablecoin, USDT, and Tether’s risks, such as bank-run events that may result in the depegging of USDT. This topic deserves a closer look since a potential fall of USDT, which is about six-fold larger than UST, would likely have an impact of a significant scale on the digital asset market overall.

What is This “USDT” Issued by Tether?

Tether, or USDT, is a stablecoin issued based on the collateral assets or reserves. In theory, USDT holds the same value as the U.S. dollar since every USDT minted is backed by a $1 worth of an asset. As Tether is held against a set of substantial collaterals, its stability is much stronger than UST, an algorithmic stablecoin.

However, Tether has not been able to shake away the continuous suspicion that suggests the value of the assets they hold will fall short of its supply due to various allegations against them. Such allegations include the claims that Tether holds bad debts, such as ones from China Evergrande Group, and that the disclosed books on its collaterals may have been tampered. As such, some investors are still skeptical of USDT. This means that USDT may very well depeg, regardless of Tether’s fundamentals. As of May 26, 2022, $1 USDT is still being traded below USD 1 at USD 0.9991.

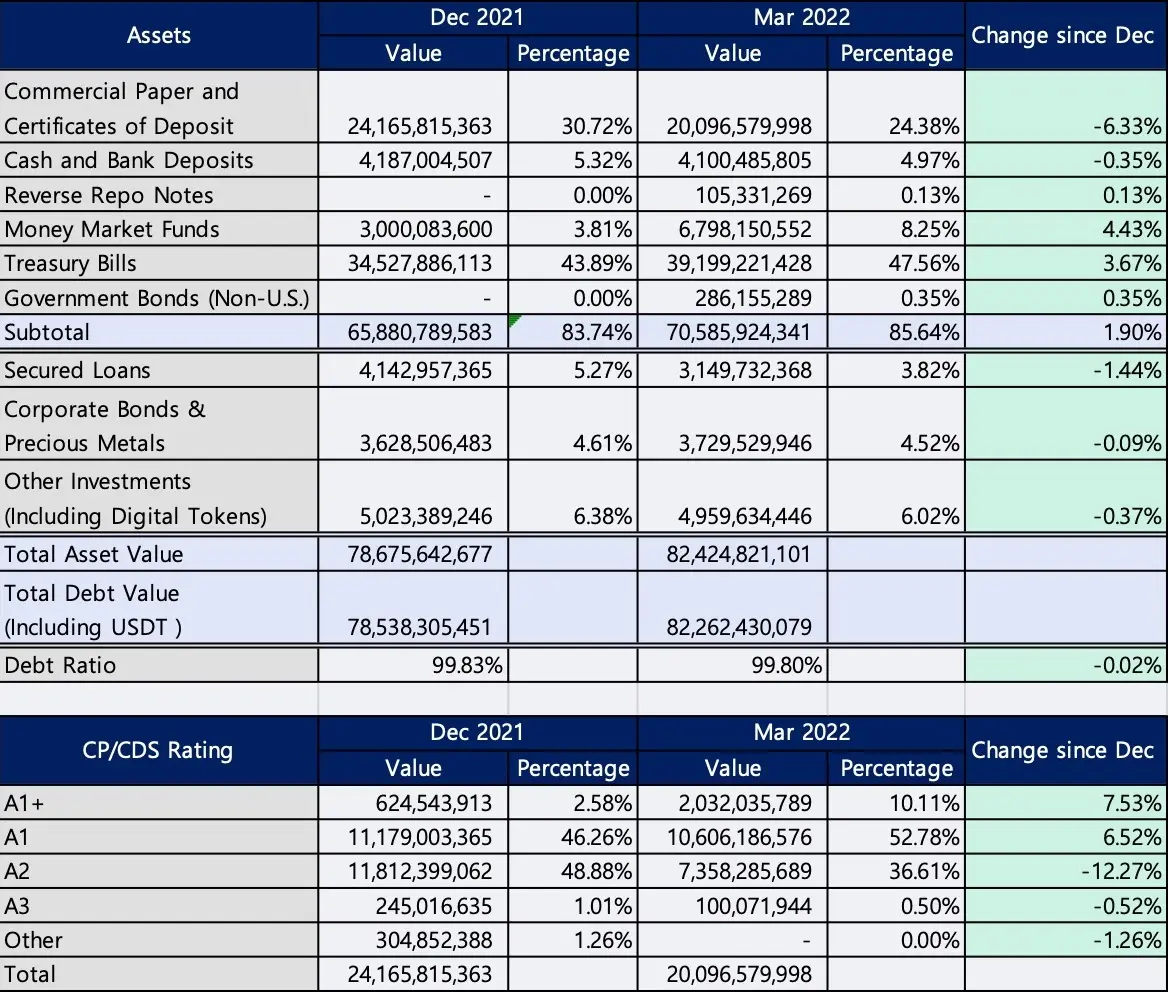

The list of Tether’s collateral assets disclosed as of March 2022 is as below:

What Are Tether’s Potential Risks?

1. Collateral Assets Risk: Risk of Collateral Devaluation

2. Lack of Information Transparency: Possibility of Data Disclosed by Tether Being Problematic (Auditor Credibility Issue)

3. Risk of Potential Bank Run: Possibility of a Bank Run Due to Lost Trust Regardless of Its Collaterals

First Risk: Collateral Assets Risk

1. Treasury Bills (Accounting for 47.56% With about $39.2 Billion) – Concerns Over Their Devaluation

Treasury bills are short-term U.S. treasury bonds with one-year or less maturity. T-bills are actively traded bonds with high market liquidity and a guarantee of interests received when carried to their maturity. These bonds are considered very secure collaterals as they have the top credit rating and practically no risk of default. The problem occurs when calls for repurchases are made before their maturity while the bonds’ value has decreased.

From January to July 2021, when the USDT market cap was rapidly expanding, the interest rate was around 0.07 – 0.12%. However, it surged to the current 2% since. Of course, with T-bills being short-term bonds maturing within one year, there is a good chance that Tether collected the principal and even profited from the interests. However, depending on at which point in time they decided to reinvest, there is a possibility that the par value of the bonds they hold may have dropped. It still would not be much of a problem if Tether held on to those bonds until maturity. However, if the demand for repurchase were to spike up along with the current rise in interest rate, there is a possibility that Tether would take a loss and sell the bonds. However, as the short-term bond market is very active in trading without significant price disturbances, the liquidity issue may be resolved through secured loans.

Treasury Bills’ Devaluation Estimated at $370 Million

Key Assumptions

- The average maturity for the treasury bills is assumed to be one year.

- A 1% devaluation is assumed for every 100bp increase in the interest rate.

- The interest rate is assumed to be 0.1% for January 2021 and 2% for May 2022.

- Assuming continuous roll-over, the devaluation ratio calculated with median value is as follows: (2%-0.1%)/2 = 0.95%

- The total loss from devaluation is as follows: $39 billion * 0.95% = $370 million

In other words, they could take a loss of about 460 billion if they respond to the immediate repurchase calls. While this amount may not seem sizable in terms of an absolute value compared to the total market cap, it could significantly impact Tether.

2. Commercial Paper and Certificates of Deposits (Accounting for 24.38% With about $20 Billion) – Increased Risk of Default

Tether had been rumored to hold commercial papers issued by the China Evergrande Group, which Tether dismissed at once. According to the information disclosed by Tether, most of the debts they hold are from companies with A to AA ratings and are considered to have a minimal likelihood of default as they are the most stable bonds after bonds with AAA ratings, such as the U.S. Treasuries or Apple bonds. However, no one can rule out the potential drop in the bonds’ par value due to the rising interest rate. Given the risk premiums and duration of the commercial papers, the loss resulting from them is estimated to be larger than the loss from the U.S. Treasuries.

3. Structured Derivatives – Unable to Estimate Their Liquidity and Risk Size

It would not be an issue if Tether simply held on to these bonds without liquidating them. However, if Tether were to liquidate its assets, structuring them into various derivatives, that would become a whole other story. The securitized assets go through a very complicated and multi-stepped liquidation process that involves various entities, making it potentially difficult to repurchase them in a pinch. This means that there is a high possibility that there are financial products issued and in circulation similar to the MBS products in the 2008 financial crisis. If an over-valued USDT is in circulation despite the drop in the securitized assets’ value due to the rise in interest rates, Tether would not be fully equipped to cover the large scale of repurchase requests if any were to occur.

4. Liquidity of Other Assets

Although most of Tether’s assets are in cash or cash equivalents, in extreme cases, its other assets may need to be sold off for cash as a last resort. Without knowing what these “other assets” are exactly comprised of, no one can be certain whether Tether has the ability to pool enough cash to prevent any potential massive and sudden bank run events.

Second Risk: Audits with Lack of Transparency

The second risk that resides with Tether is the lack of confidence in its accounting audits. Tether’s quarterly audit reports are drafted by an auditor firm named MHA Cayman. People raise questions about the integrity of their reports since, on top of the fact that they are located in the Cayman Islands, a tax haven, the firm supposedly consists of only three employees according to their LinkedIn page. Of course, this figure is only based on the number of LinkedIn subscribers working for MHA Cayman, and their own data shows that they have 11 to 50 employees, with their parent company, MHA MacIntyre Hudson, employing 777 people for their U.K. office as of 2021.

The real problem is that the mere fact that such suspicions exist can heighten investors’ anxiety in case of a black swan event, intensifying the possibility of a bank run. This will be further discussed in the next section of this article: the risk of a bank run.

Third Risk: Risk of Tether Bank Run from Lack of Trust

Bank runs are caused by the loss of collateral assets. That is technically correct. However, what is more important is the matter of the issuer’s credibility. All these allegations about Tether’s collaterals taking a hit or audit reports not being transparent come together to bring down people’s trust in Tether. If such a lack of trust were to cause a surge in debt repurchases, there is a chance that Tether will not be able to handle the large scale of repurchase calls even with the collateral it has secured, resulting in a run on the bank. Bank runs are highly contagious. If users who lost their faith were to take flight on an exodus, it would accelerate the bank run. As we saw in the case with UST, if the suspicion on Tether’s fundamentals continued and depegging worsened, the situation could quickly turn for the worse and trigger a run on the bank.

Such runs on the bank resulting from a collapse of trust are also an issue applicable to banks. In order to avoid such a situation, various parties involved in the Korean banking industry are taking measures to improve overall credibility, which include banks maintaining a set cash reserve ratio (the Korean government set a 7% reserve requirement), the government enforcing protection for depositor for deposits of KRW 50 million or less, and the Central Bank of Korea serving the role of the lender of the last resort.

Tether is currently assumed to have a cash reserve ratio of about 5% (in cash and bank deposits) for USDT, but no alternative means of prevention like institutionalized rules and regulations or the Depositor Protection Act of Korea.

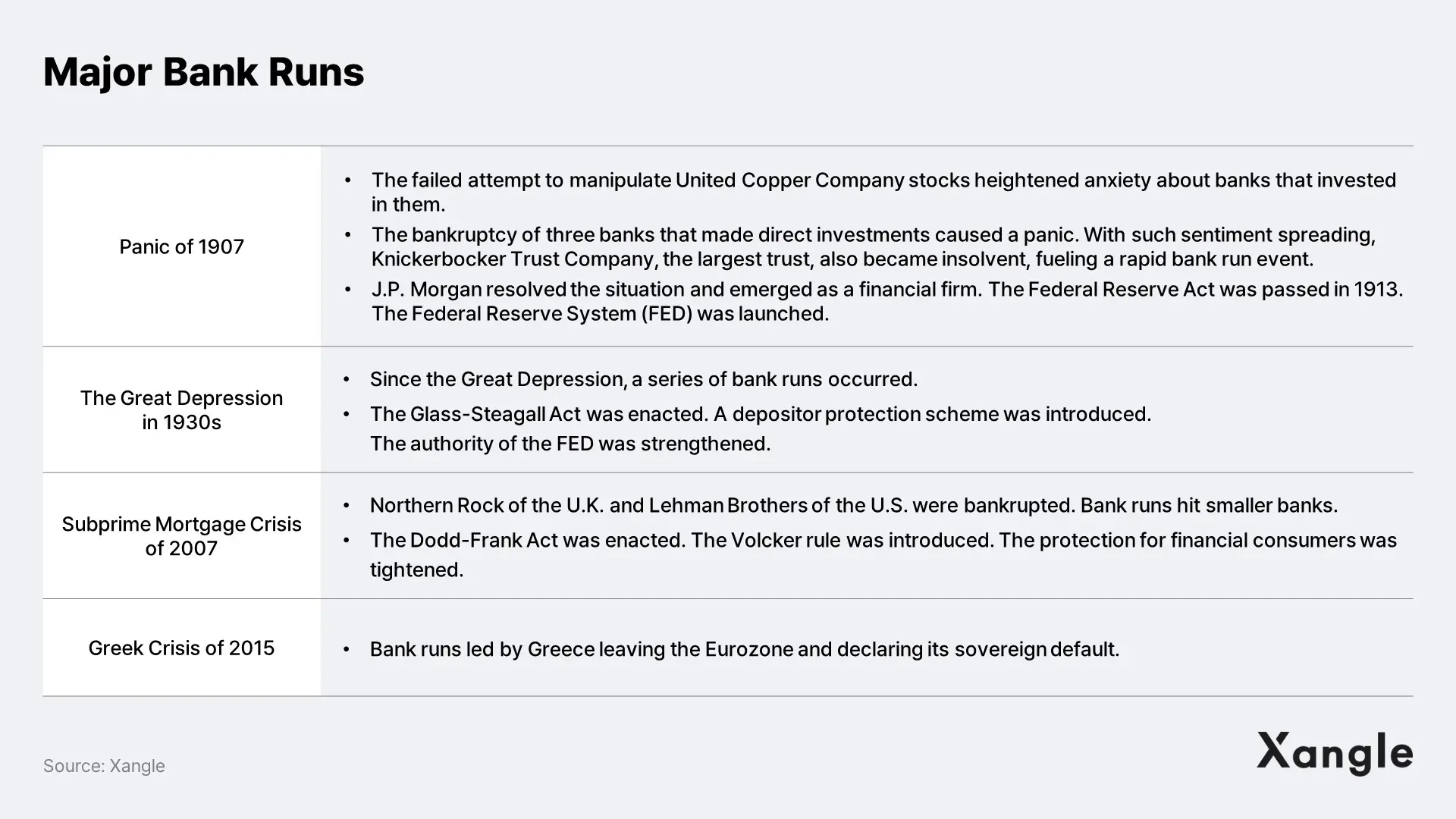

A Look on Tether Through the Lens of Past Bank Runs

By taking a closer look at the cases of banks that suffered bank runs in the past, we can get a rough idea about the degree of potential risks for stablecoins. Of course, the situation with the traditional banks is different from that of stablecoins, as the former can use loan leverages once their statutory cash reserve ratio (of 7% in Korea) is met, while the latter is required to secure close to 100% collateral. However, considering that their bank runs were initiated by the issue of trust and market sentiment, it is worth noting whether Tether is free from the same risk.

Historically, bank runs have been black swans: an event in the market that has a low likelihood of occurring, is impossible to predict, and yet has a tremendous impact when they do take place. Many of the bank runs were indeed triggered by macro events that could never have been predicted.

One may look this over as just a side note, thinking that the current situation is not as dire as something like the Great Depression and that bank runs would only occur in such extreme situations. However, we have already seen more money erased from the recent events than from the dot-com bubble, and the investment sentiment has also drastically declined. As for the crypto market, not only has the fall of the great UST-LUNA caused the people to shy away from investments, but people are also waiting to see how different governments would wield their power and announce the introduction of their crypto regulations. In such a situation, who is to say with certainty that Tether, who lacked public trust even before any of these challenges, will not be faced with a bank run?

Although bank runs are closer to something of a black swan event, the current sentiment of the crypto market and the impending blade of the regulation makes it probable for such a black swan scenario to take place where Tether has to battle the bank run. The companies that survived various crises, such as Brexit and the embezzlement scandals of some Korean companies, were able to save themselves from spiraling down to bank runs because they had gone through sufficient stress tests and secured the public trust. That is not the case with Tether. Not only did they not have enough time to be thoroughly tested for how they will perform under stress, but they also have to deal with external concerns eroding their reliability and further macro environment risks.

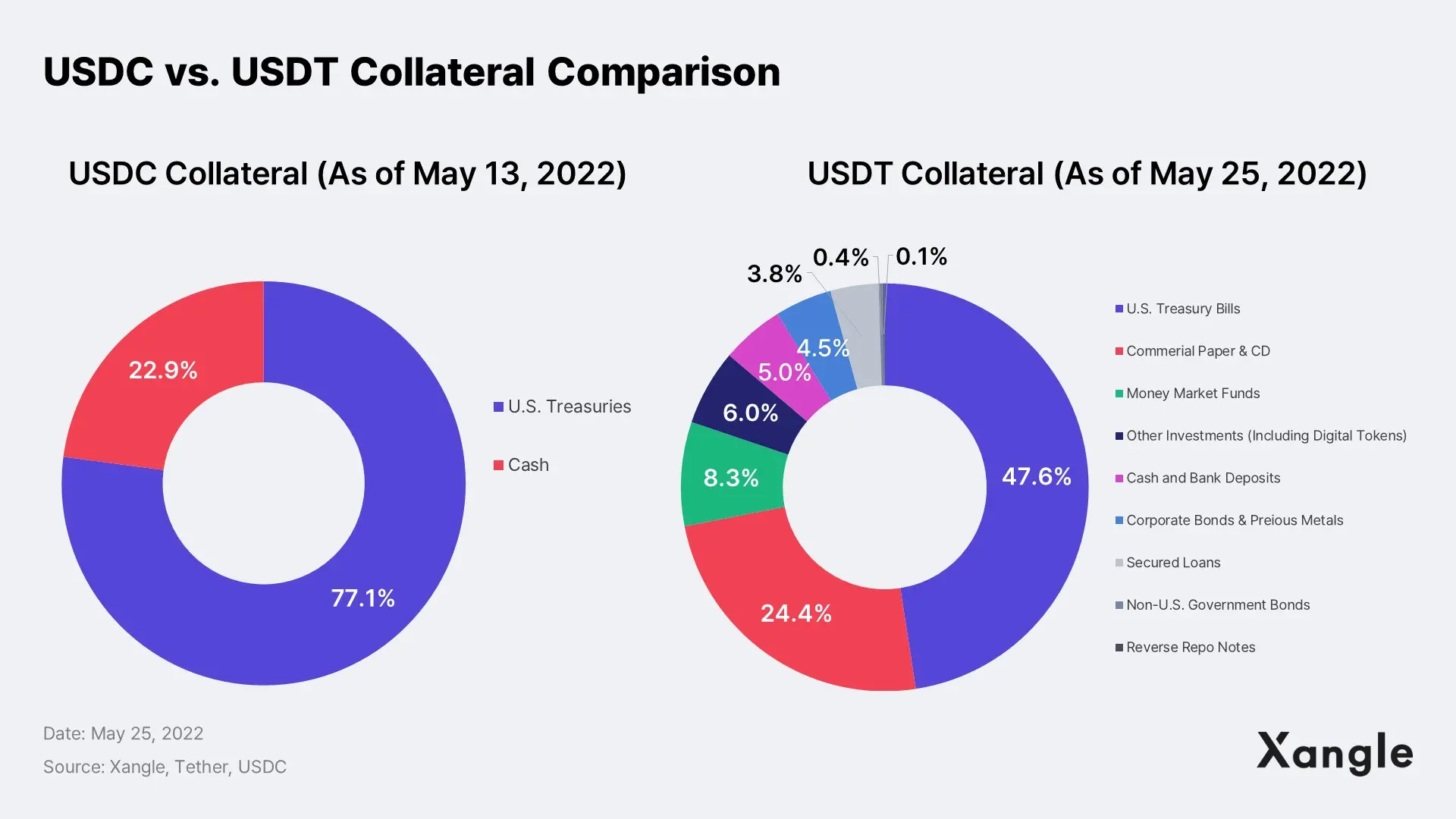

Difference Between USDC and USDT

How are other stablecoins performing in such turmoil? Let us explore one of the major stablecoins, USDC.

The USDC is issued by Circle, a company placed well within the American financial system and under the regulations of the Financial Crimes Enforcement Network (FinCEN) of the U.S. Department of Treasury. Circle has also mitigated its legal risks by acquiring licenses in each state it operates its business. Moreover, the collateral backing USDC is consisted of 77% in U.S. Treasuries and 23% in cash, offering overwhelmingly more stability than that of USDT. BUSD, a stablecoin traded on Binance, is also issued by a company under the New York state’s regulation, Paxos. It is also considered more stable than USDT with a collateral mix that only contains cash and U.S. Treasuries.

In Conclusion: On-going Stress Tests for Stablecoins and Other Crypto Assets

At the end of the day, what really matters is the “trust.” People are no longer worried about the bank run risks when it comes to the American banks and the Federal Reserve System because they have restored confidence in them after having endured a series of stress tests over a long period of time. The same goes for the banks in Korea. The depositors are not worried about bank runs even when faced with an event like the recently uncovered scandal of a KRW 60 billion embezzlement from Woori Bank because they have built a strong trust as they overcame various challenges and crises over the past few decades. Crypto assets such as USDT are similarly going through their own version of stress tests at the moment. Only after passing such a long-term test and proving themselves will they be able to claim their position as stablecoins fully acknowledged by investors.

Governments in different countries are speeding up their moves on their regulations for stablecoins, including the U.S. government, with a bill pending in Congress for better transparency and stability for stablecoins. From such a perspective, USDT is at a crossroads right now. If Tether’s USDT were to be brought into the fold of the existing and regulated system and transparently disclose its information, successfully passing the stress test, it would be able to take its roots as the key currency of the crypto market. Meanwhile, the U.S. federal government rejected Tether’s petition to refuse disclosure of information about its collaterals to protect its proprietary knowledge on capital efficiency. Although such disclosure may expose its position, data transparency must come first, nonetheless, for the purpose of protecting the investors. If the crypto market’s continued growth in the upward right direction is to be believed, it will serve as a greater benefit for Tether as well to secure its position in the crypto market as the key currency.

The solution for the bank runs witnessed in the panic of 1907 and the Great Depression of the 1930s was to inject financial bailouts and calm the depositors. Getting investors to rest assured and convincing them that the banks were safe was one of the pillars of the strategy to prevent further bank runs. It even involved the U.S. president holding sit-down talks and local churches reaching out to their communities. The current situation with Tether is not much different. If Tether is truly seeking capital efficiency through stable collaterals, as they claim, they must reassure panic-stricken individual investors by transparently disclosing their information and pass the stress test. Tether is urged to wipe out such risks from the crypto market promptly.

For More Readings Like This Article:

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.