[Xangle Valuation Series] ④ Lending Protocol

[Xangle Originals]

Written by Jehn, Crypto_Gang, CHOBiden

Translated by elcreto

The 4th edition of Xangle's valuation series is Lending Protocol.

In the crypto market, a lending protocol serves the role of the existing banks while a DEX serves as a securities exchange or an investment brokerage in the traditional context. High-profile lending protocols have generated meaningful revenue since the end of 2019 and are the drivers behind the DeFi Summer in 2020. Lending protocols are earning profits from the spread between the interest rates on crypto deposits and loans and are regularly engaging in investor relations reporting project’s achievements, making data available for valuation. In this article, we will discuss the business model of lending protocols, go over the indicators necessary to value each protocol, and estimate the value of the widely-used protocols like MakerDAO, Aave, and Compound.

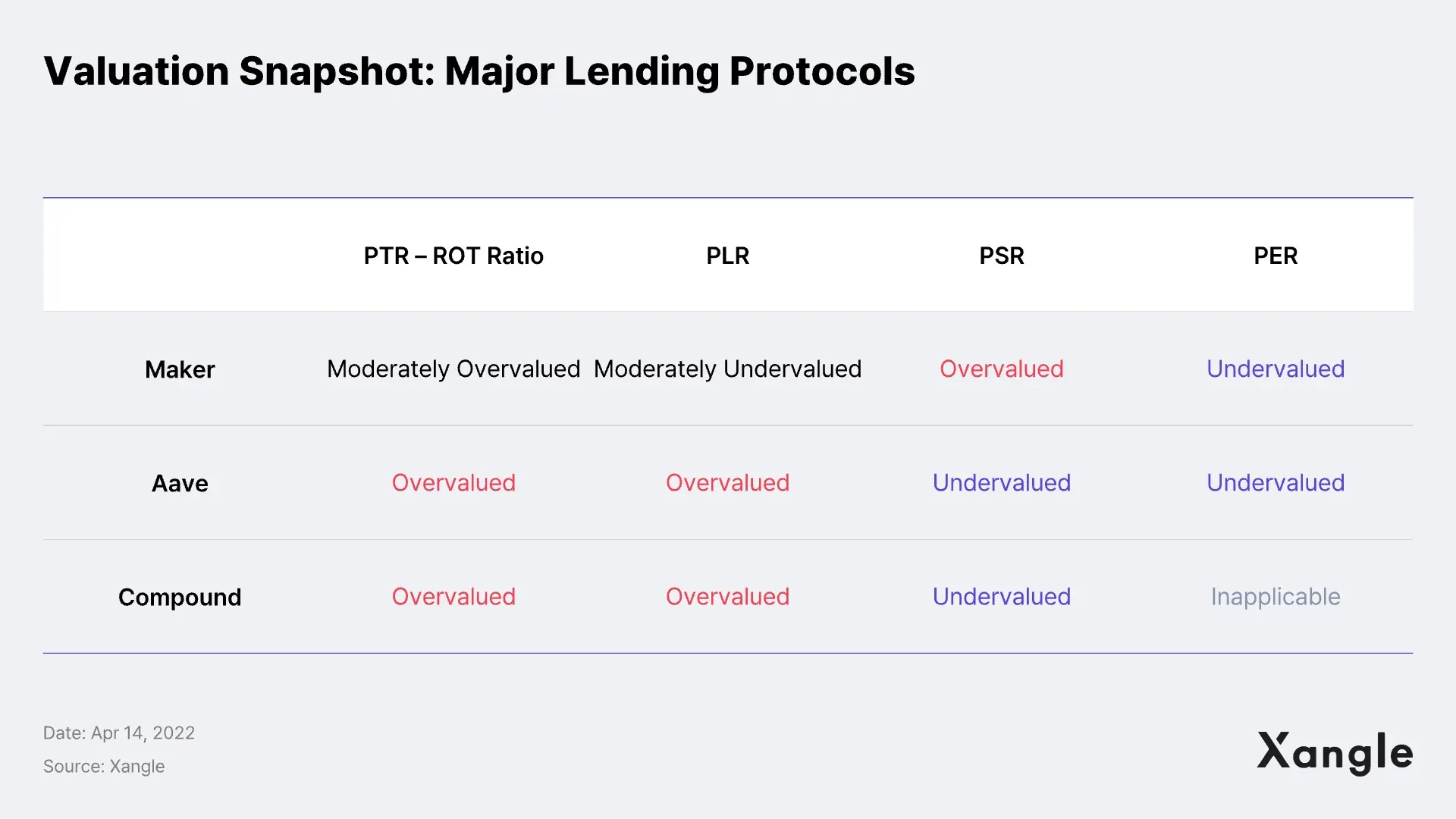

Determining the key indicators to be used during the valuation process is critical in finding the right valuation model. In this valuation series, we set TVL, loan size, revenue, and earnings as the valuation criteria. In our findings, our TVL-based PTR (Price-to-TVL Ratio) and ROT (Return-on-TVL) evaluation indicated an overvaluation of lending protocols while our loan volume-based PLR (Price-to-Loan Ratio) evaluation indicated that Maker is somewhat undervalued and Aave and Compound are overvalued. Meanwhile, PSR (Price-to-Sales Ratio), a sales-based assessment, indicated that Maker is overvalued and Aave and Compound are undervalued, compared to their peer group, including online banking. Lastly, PER (Price-to-Earnings Ratio), an earnings-based assessment, suggested that both Maker and Aave are undervalued while Compound’s net deficit made PER inapplicable.

We will now move on to discuss the methodologies adopted herein and the interpretation of the results more in detail.

1. Lending Protocol

1) State of the Market

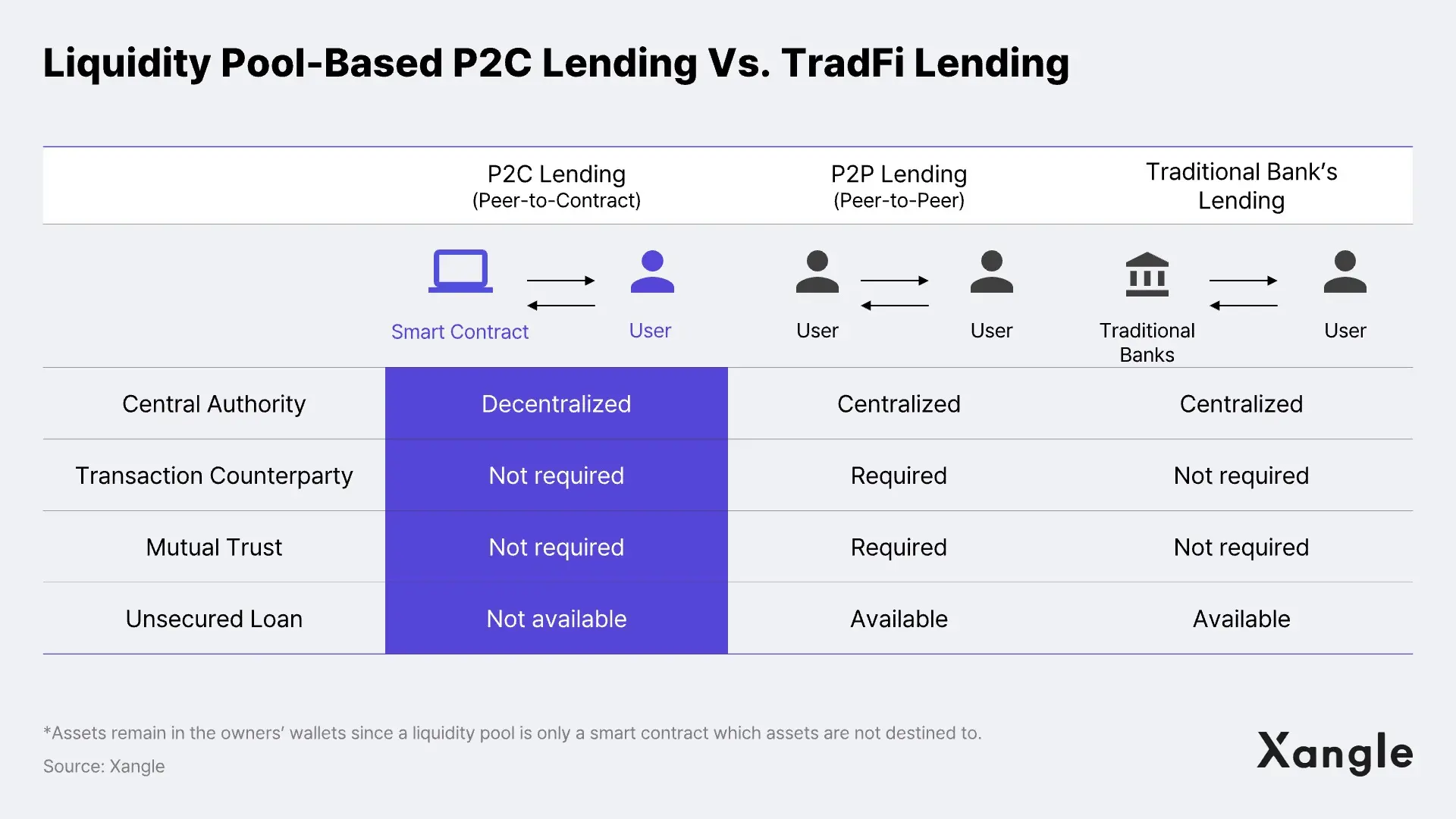

Lending protocol (Lending) is a protocol that performs similarly to a bank, providing deposit and lending services without an intermediary. Yet, lending in the crypto market is provided primarily based on collateral because credit in this market is hard to define and evaluate.

Few years ago, P2P (Peer-to-Peer) microlending drew much attention, connecting each lender and borrower. Its streamlined brokerage process enabled i) higher interest rates than banks and ii) an easier access to the service for borrowers. Decentralized lending protocols do not provide direct matching services between lenders and borrowers. Instead, all parties interact with smart contracts, without the need for any intermediaries, and users are rewarded proportionally to their contribution. In this sense, P2P microlending can be classified as Web 2.0 service and lending as Web 3.0 service. For the glossary of common terms for lending protocol, please refer to “[3] DeFi Terminology – Lending Service.”

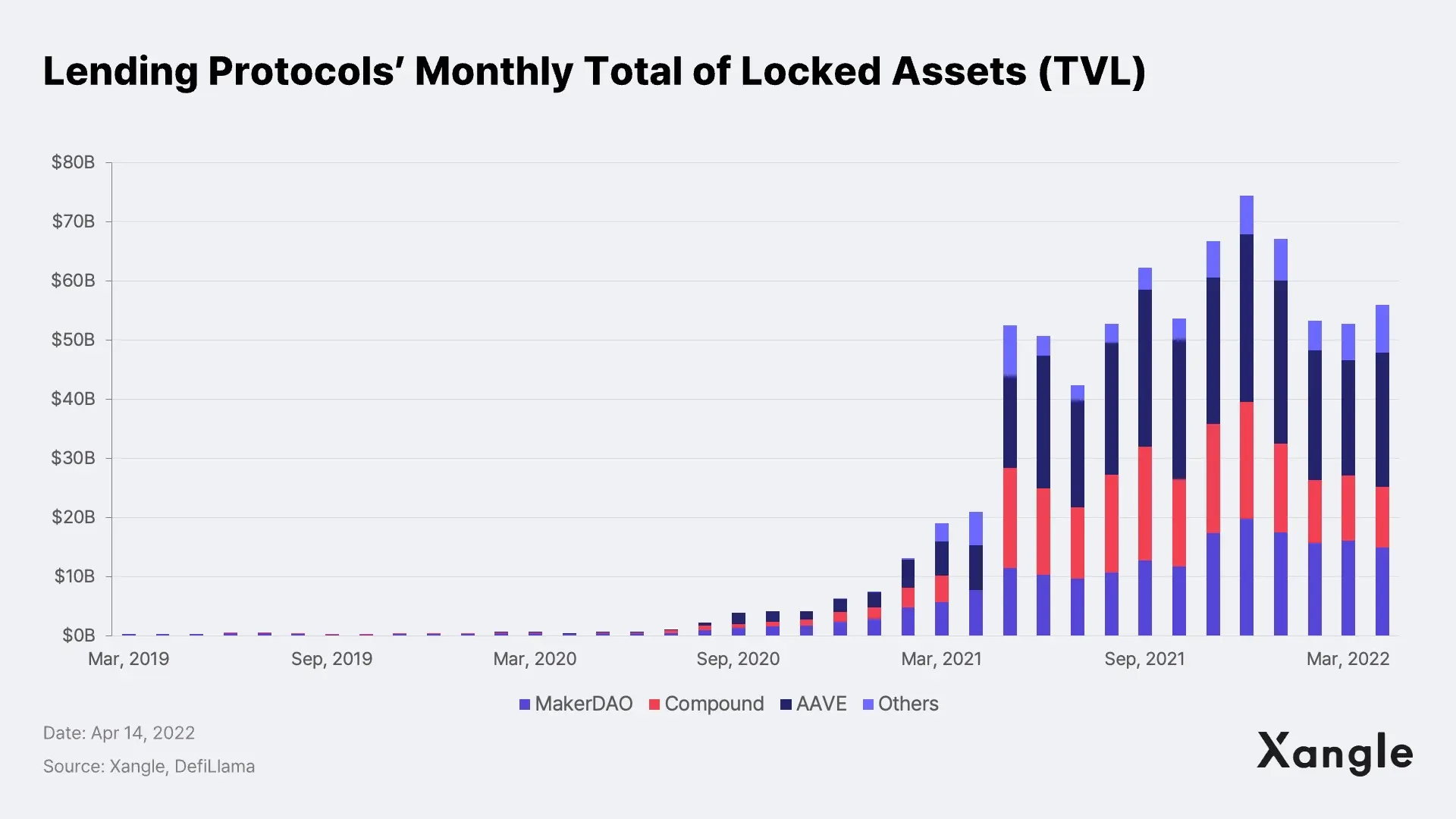

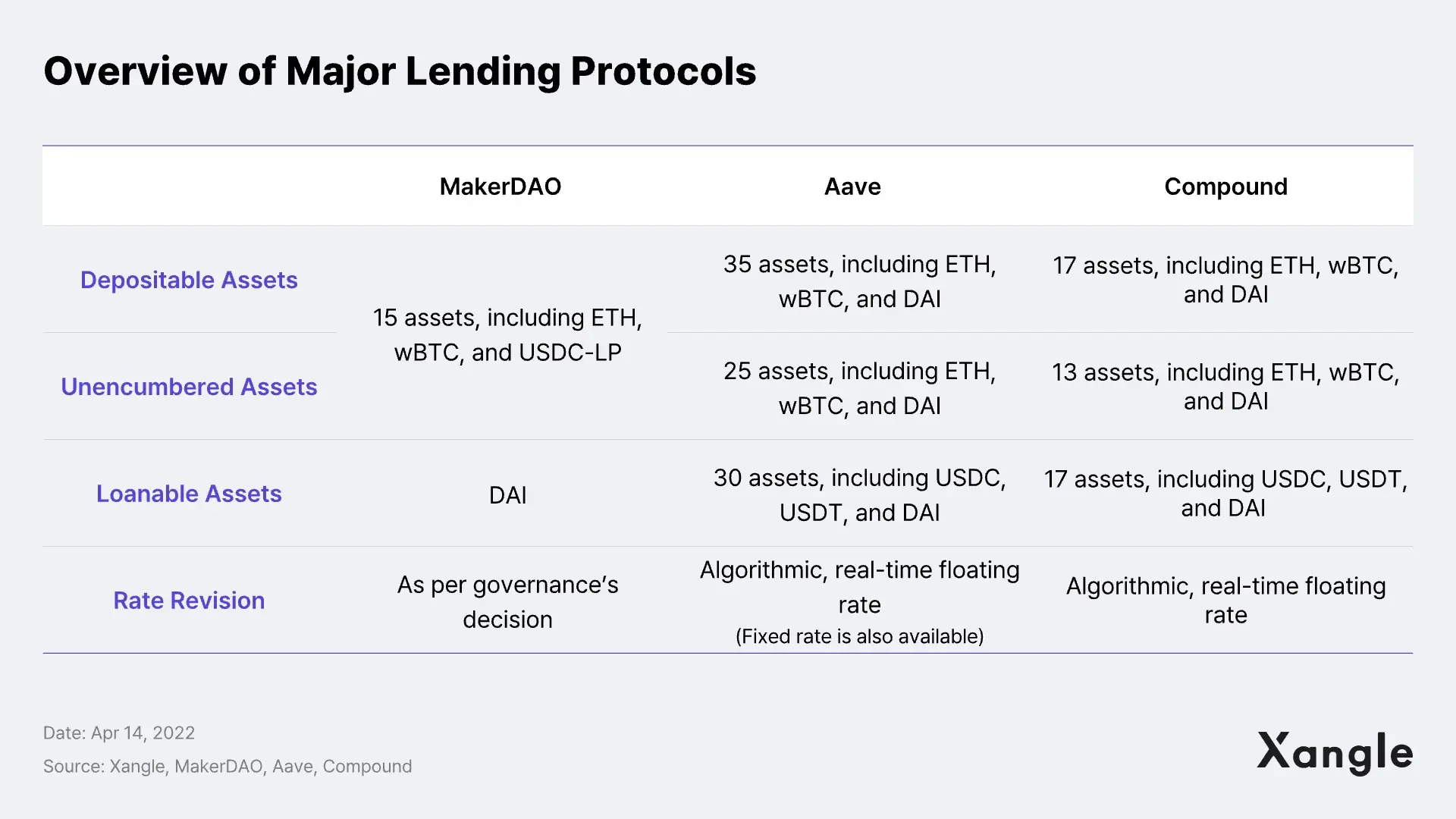

The lending sector was first to take root in the crypto industry, creating a hype in the market from 2020 to 2021. As of end-2021, the amount of assets deposited in major lending protocols was $74B, a 11.9-fold increase from 2020. To compare projects with the same duration of operation, we chose the top three protocols that were put in service in 2021—MakerDAO, Aave, and Compound. More details about each lending protocol can be found in the XCR report at the link below.

MakerDAO-XCR (Link) | Aave-XCR (Link) | Compound-XCR (Link)

2) The 2021 Key Indicators for Lending Protocol

In the context of traditional industries, banks' financials tend to differ from manufacturers' and so do the key performance indicators, as banks generate financial revenue from financial assets. As such, we saw revenue, earnings, asset, equity, and interest income as the markers that allow us to estimate the value of each lending protocol.

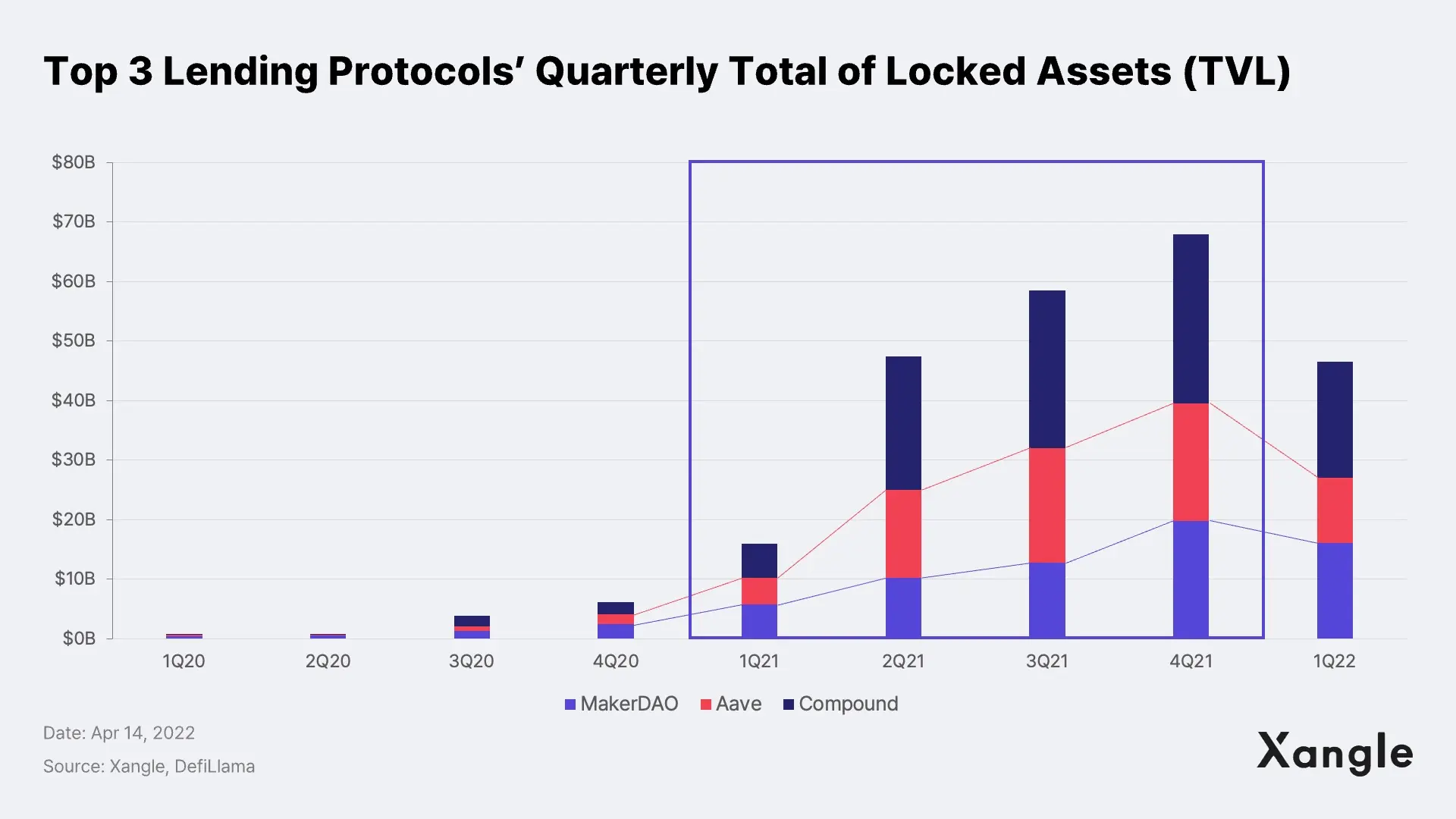

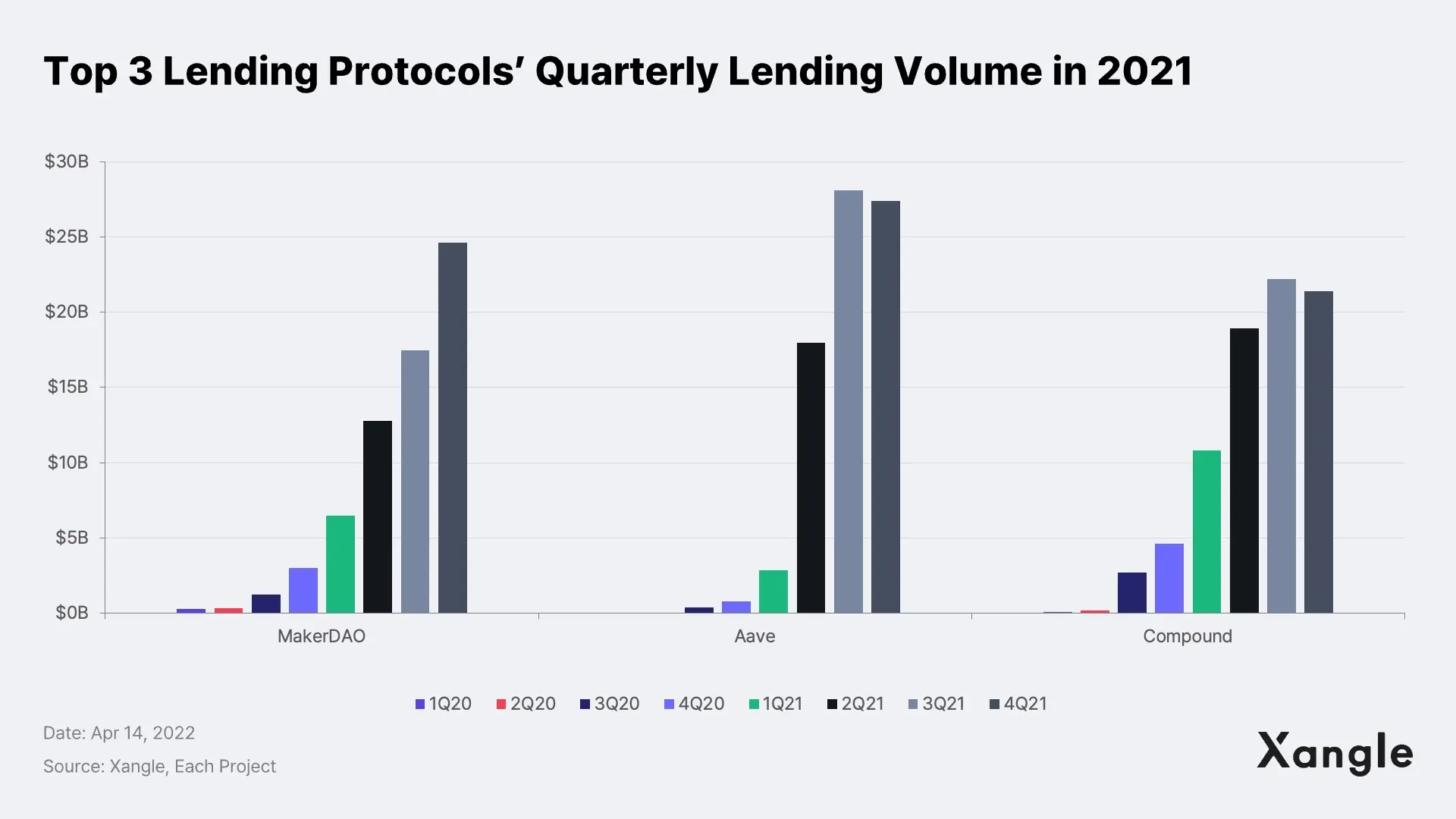

To start with, we saw Total Value Locked (TVL), the value of all crypto assets deposited in the protocol, as assets for traditional banks. In 2021, the YoY TVL growth rate of Maker DAO, which has been the No.1 lending protocol, stopped at 8.2x, lagging behind the growth rate of its peers, while Aave and Compound spearheaded the growth of the market, growing 12x and 13.5x respectively.

Lending, on the other hand, is the source of revenue and increase in assets for banks, garnering capital. Major protocols had seen double-digit growth that continued from the previous year up until 3Q 2021, outperforming the single-digit growth of KakaoBank, South Korea’s best known digital bank. Except for MakerDAO for which stablecoin DAI shored up its performance, the market has been bearish since 4Q 2021 and remains so in 2022 with Aave and Compound’s lending also dipping from the previous quarter.

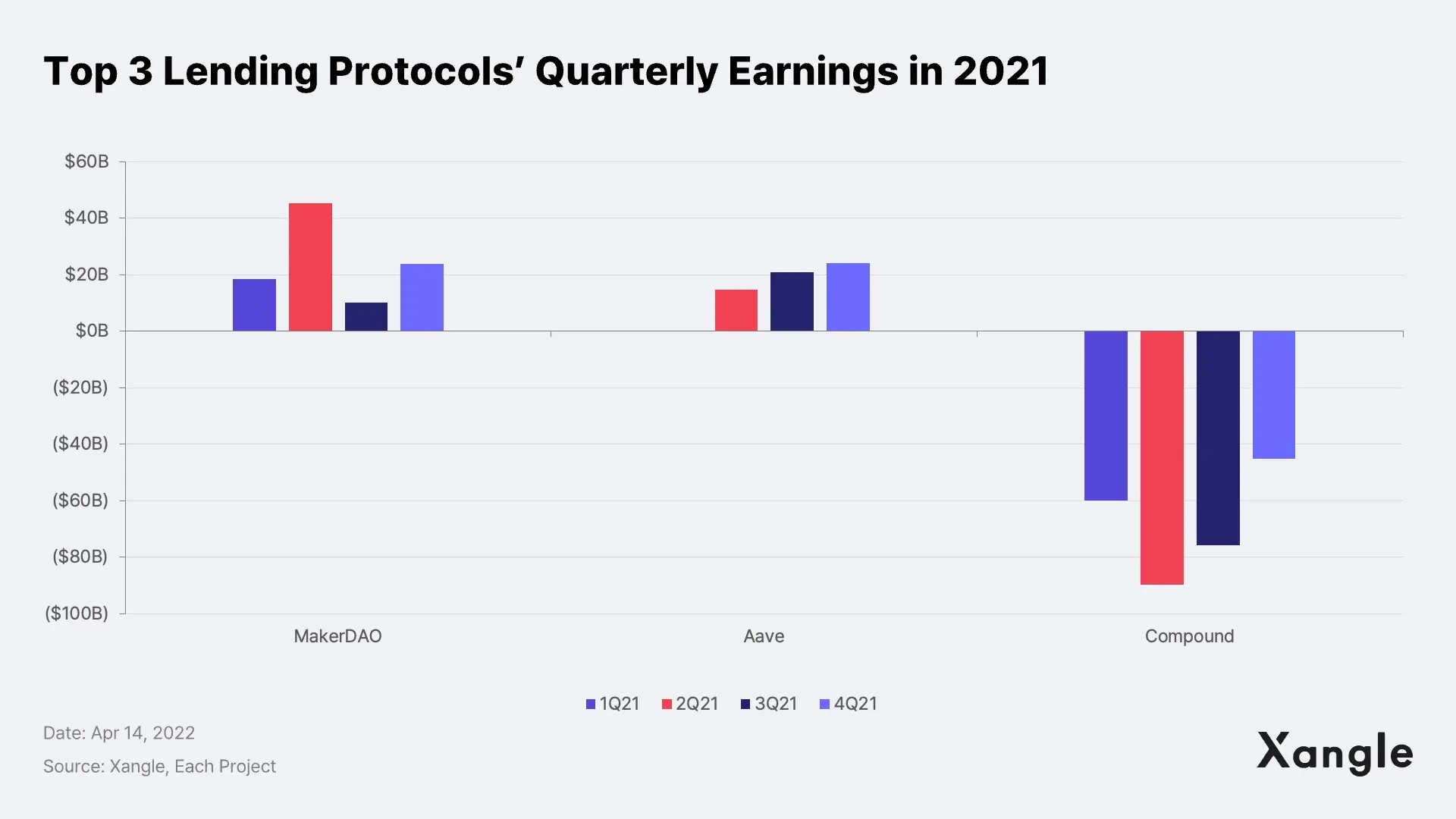

Each lending protocol differs in structure and has different revenue streams. Overall, lending protocol’s income does not seem on par with their volume growth, such as TVL and lending. In 2021, the top three lending protocols combined recorded a negative income, which was primarily driven by Compound’s shift in focus where the protocol started to offer its governance token COMP to reward contribution to multiply its user base and locked-up assets, risking a dent in profitability.

Yet, it is too premature to have a grim outlook for the lending sector simply because their net income is in the red. It was not until 3 years ago that the DeFi industry and one of its key sectors, lending service, drew attention, and more importantly, lending did achieve a significant volume growth last year. Using the indicators discussed above, we will now start calibrating the value of each protocol.

2. Asset-Based Assessment: PTR & ROT Using TVL

TVL (Total Value Locked) is the sum of all crypto assets deposited in a DeFi protocol. For lending protocols, TVL represents all assets under the management of the protocol and is used as an intuitive indication of the value of the protocol. DeFiLlama, for instance, adds up assets deposited in the protocol as well as i) native governance tokens staked, ii) LP tokens locked, and iii) assets pledged as collateral.

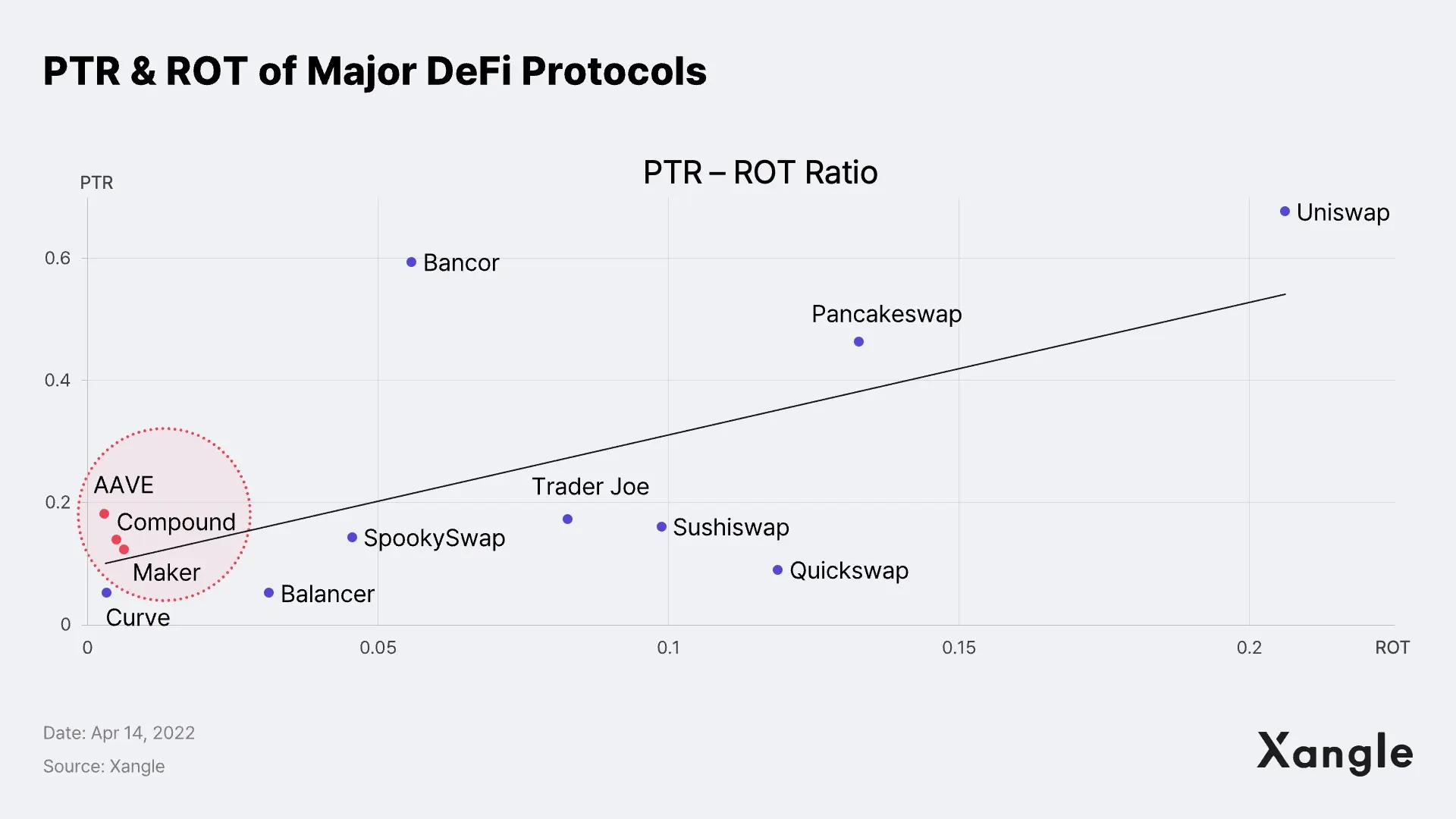

The PTR and ROT of the three lending protocols as of today are as follows, suggesting that MakerDAO has the highest PTR and the lowest ROT and is relatively undervalued compared to Aave.

The ratios also suggest that most popular lending protocols are relatively overvalued compared to DEXs, implying that lending protocols’ market cap tends to be higher than DEXs’ despite the protocols’ significantly low asset turnover.

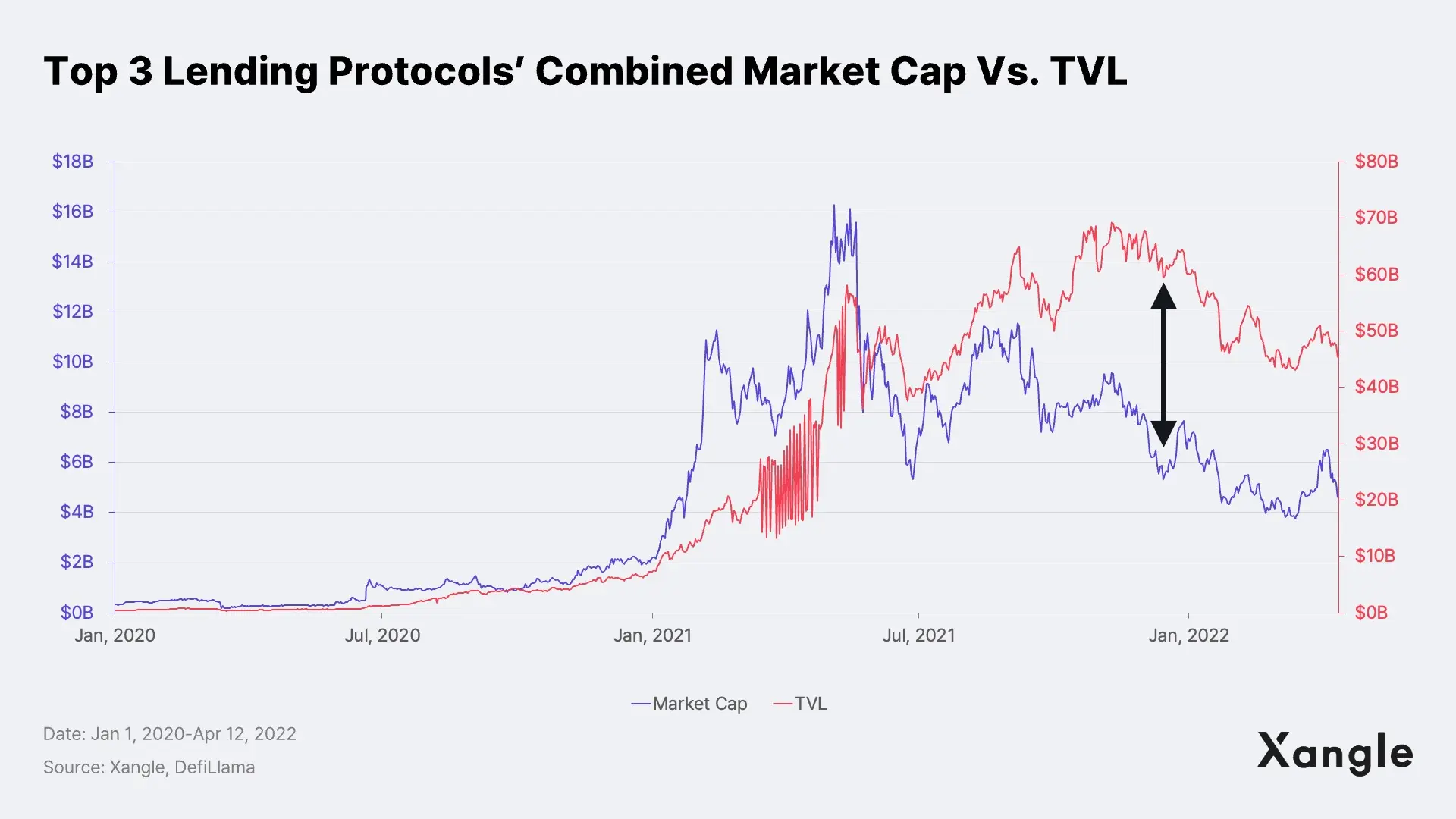

The combined market cap and trend of TVL of the leading lending protocols since 2020 indicated that their TVL has lately been relatively discounted when applied to valuation. Unlike during the DeFi summer in 2020 when lending protocols’ market cap and TVL were on a similar trajectory, a noticeable gap began to show from 2H 2021 and onwards, repeating a cycle of ups and downs.

It seems that the gap can be explained by the burden of yields and possible dilution of token value from such yield payment.In the business model of lending protocols, the larger the assets deposited, the bigger the burden of yields payable to the depositors. Unlike Maker, which issues DAI in exchange for collateral and thus, is free of the burden of yields, Aave and Compound are bound to pay out yields.

Moreover, if the protocol distributes native governance tokens as yield, tokens will be newly minted or unlocked from the reserve, multiplying the supply and diluting the value of the tokens. The market began to lose its luster from 2H 2021 and onwards, creating an incentive for the investors to lock their assets in in hope of earning yields rather than take out loans. Although there was little impact on the TVL, this was considered a risk that may hurt the protocols’ revenue and profit margin.

Apparently, the TVL-based valuation has failed to act as a proper indication of the value of the lending protocol. Therefore, we sought to base our assessment on indicators that are more directly linked to revenue and profitability.

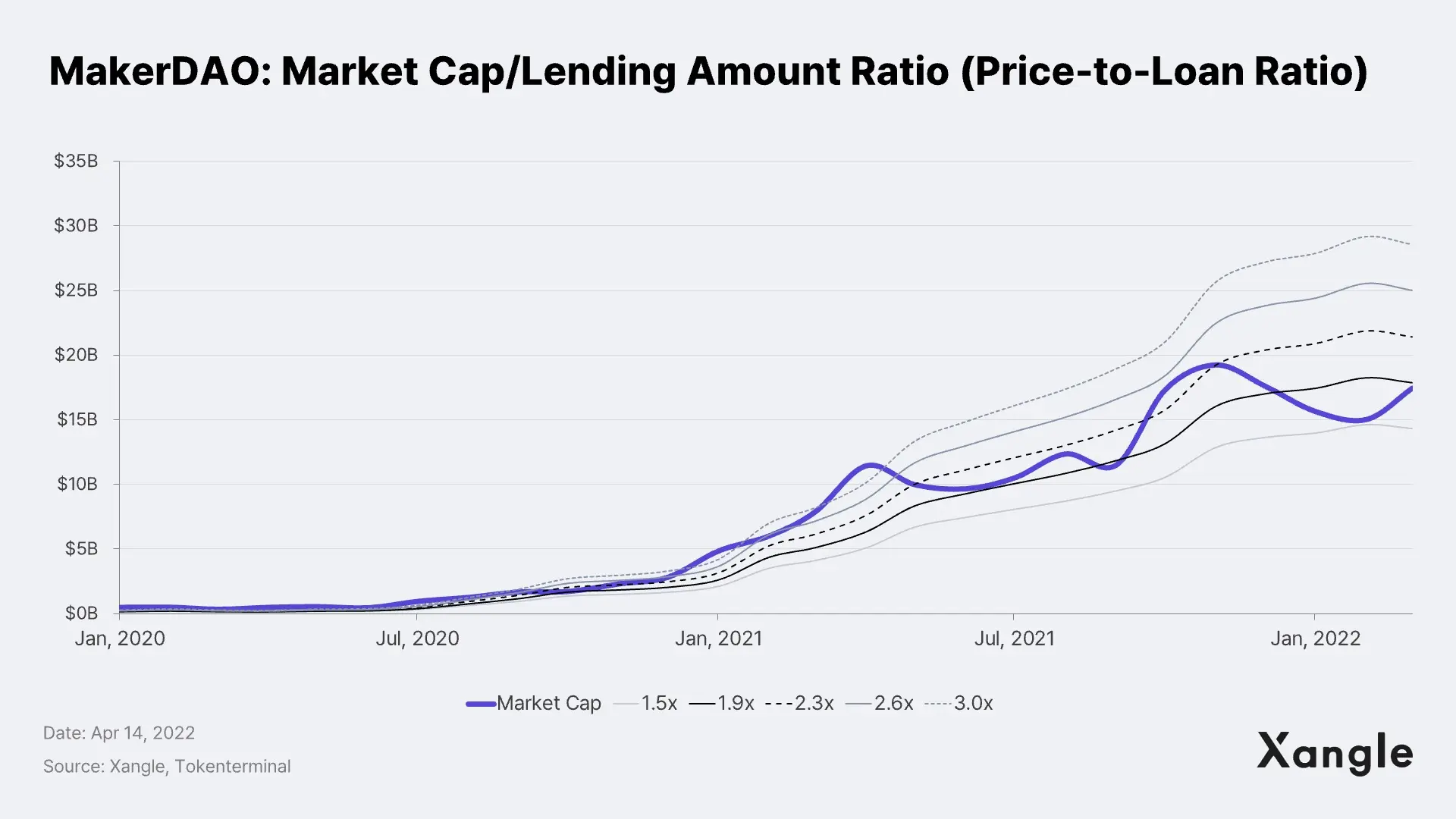

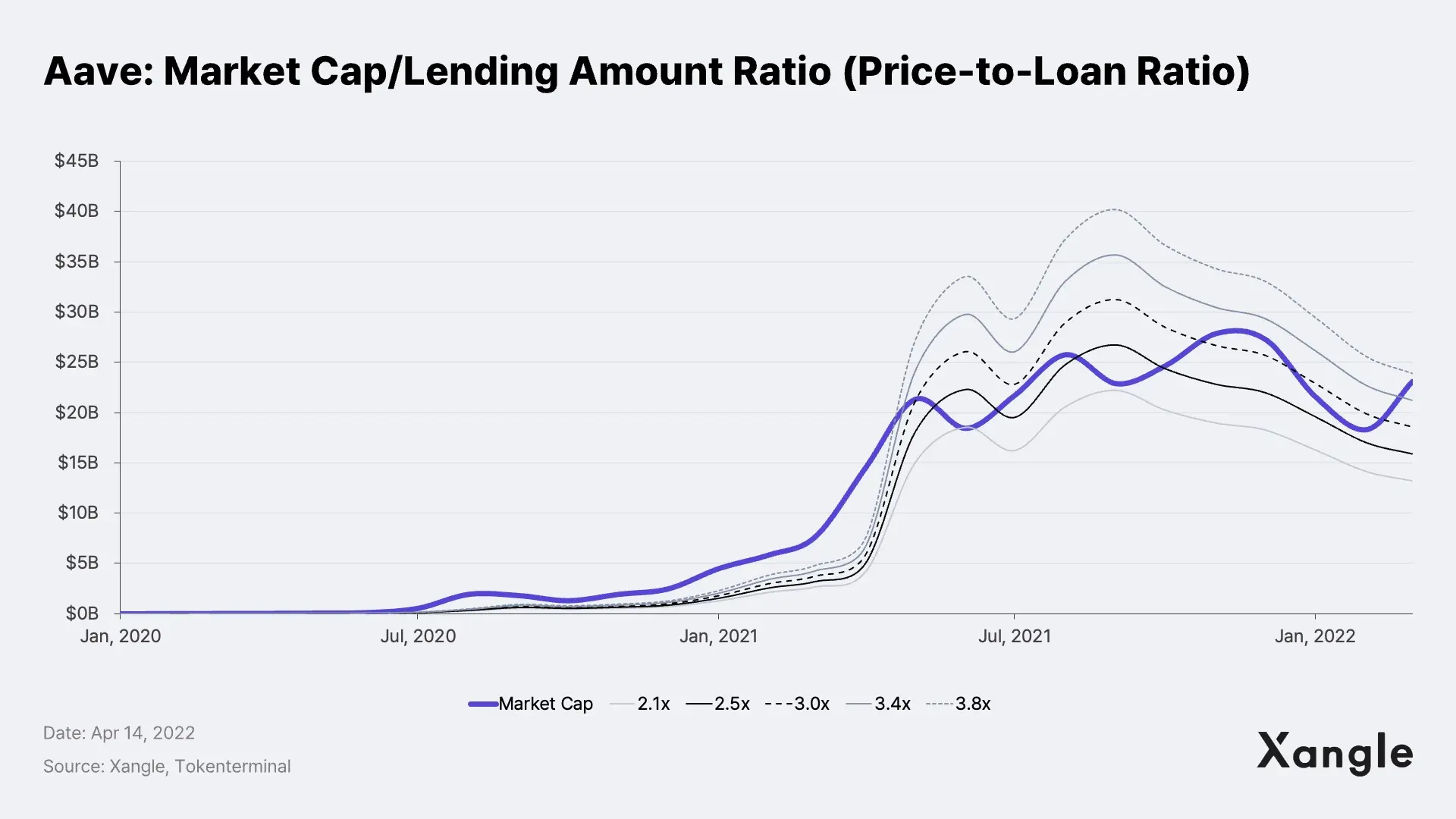

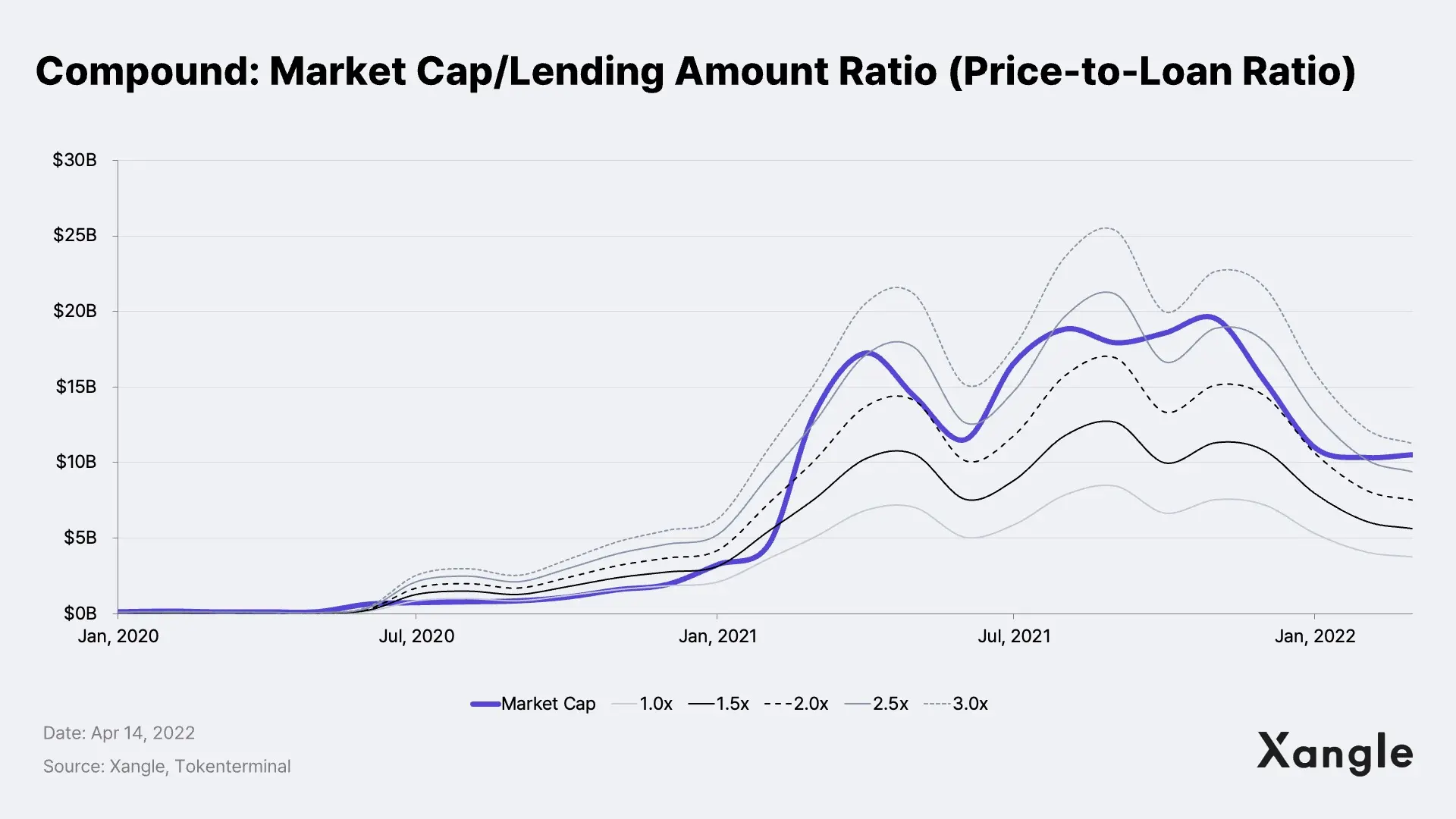

3. Net Asset-Based Assessment: PLR Using Loans Made

In the crypto industry where financial disclosure is not mandatory, lending protocols have made their business results public and engaged in investor relations much more actively than other projects. Yet, as there were few financial statements available, we valued each protocol regarding loan as net asset. Crypto lending requires a high collateralization ratio, and any borrower’s failure in maintaining the ratio or repaying the debt automatically prompts smart contract to liquidate the borrower’s asset.

Loans may require a collateral to cover more than 200% of the loan amount and some of the protocols, including MakerDAO, receive only certain types of assets as collateral. The amount of loans made to borrowers may be a more conservative approach than the net asset value but, as liabilities are left out from our consideration, we applied the amount as it is. The following is a band chart of PLR, which compares market cap with loans made to borrowers.

As of Mar 2022, the PLRs of MakerDAO, Aave, and Compound stand at 1.8x, 3.7x, and 2.8x. Even a comparison between lending protocols suggests that MakerDAO is relatively undervalued than Aave and Compound.

In retrospect, MakerDAO had slid to 1.9x during a market correction in 2021, after which it started to rebound. Currently, MakerDAO’s PLR hovers around 1.8x, which we view as fairly valued or slightly undervalued. As of Mar 2022, Aave trades at a historic high of 3.7x suggesting the highest overvaluation, while Compound also at a higher-than-usual multiple. In Aave’s case, however, the March 2022 release of V3 and its impact might not have been fully reflected in the ratio, which leaves a margin for interpretation.

Looking at the trend of the lending volume in Apr 2022, MakerDAO is the only lending protocol that staged a turnaround from the previous quarter with Aave and Compound remaining on a losing streak. Moreover, any short-term improvement in revenue or profit margin is not in sight yet, making it even harder to justify their multiples of price/loan ratios.

In the meantime, net asset value can be assumed as the treasury of each protocol. Indeed, treasury of a protocol actually provides funds for the operating expenses and is a staple in most of the IR reports, suggesting that it reflects business and financial performance of a project. As of Apr 13, 2022, market capitalizations of MakerDAO, Aave, and Compound respectively are 5.0x, 7.6x, and 2.8x the treasury. Yet, treasury comprises governance tokens and tends to suggest a short-term financial stability rather than the overall value of a project as it is “a set value” that aims to keep a certain amount of tokens apart from the circulating supply.

4. Earnings-Based Assessment: PSR & PER Using Revenue Structure

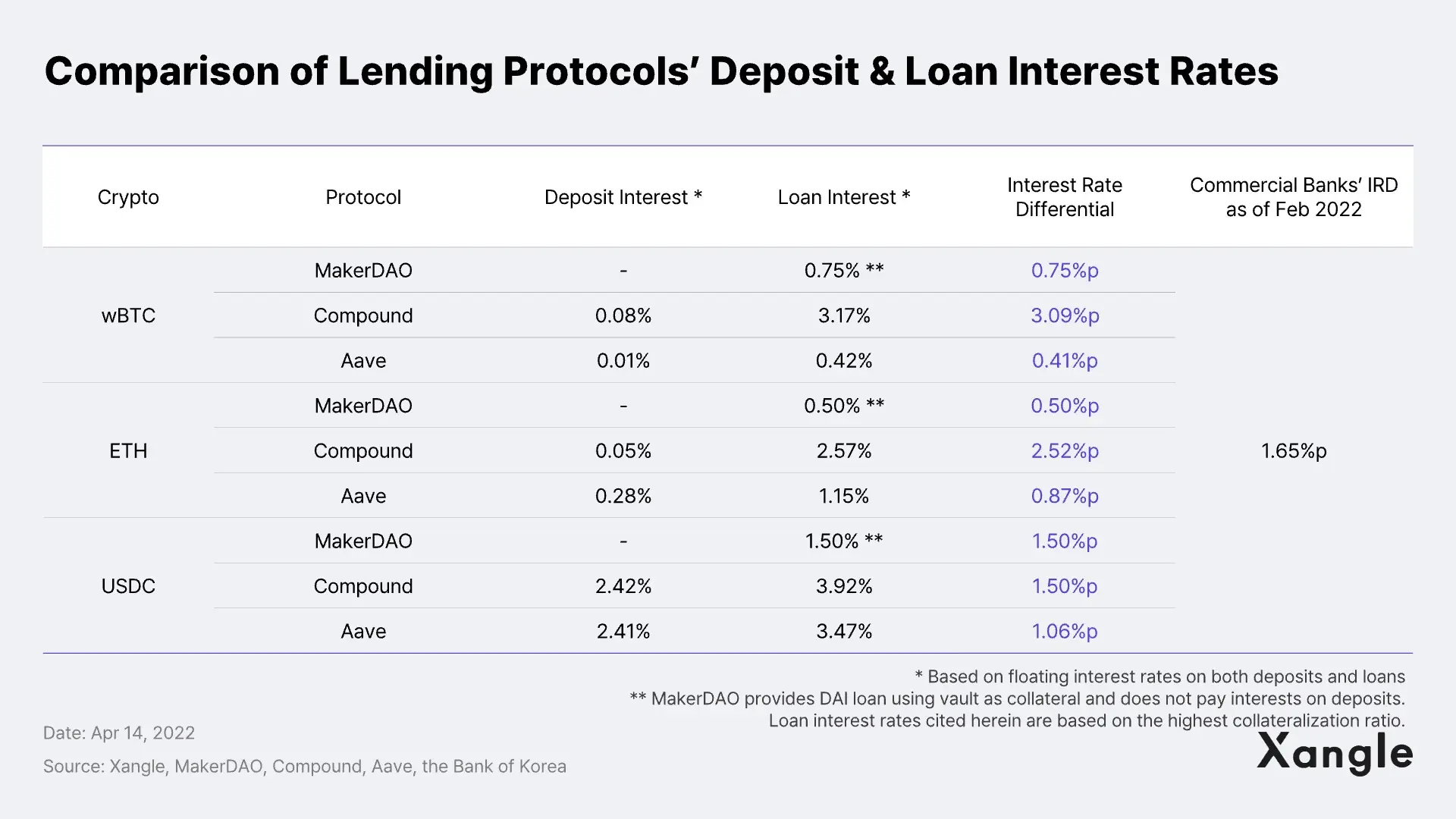

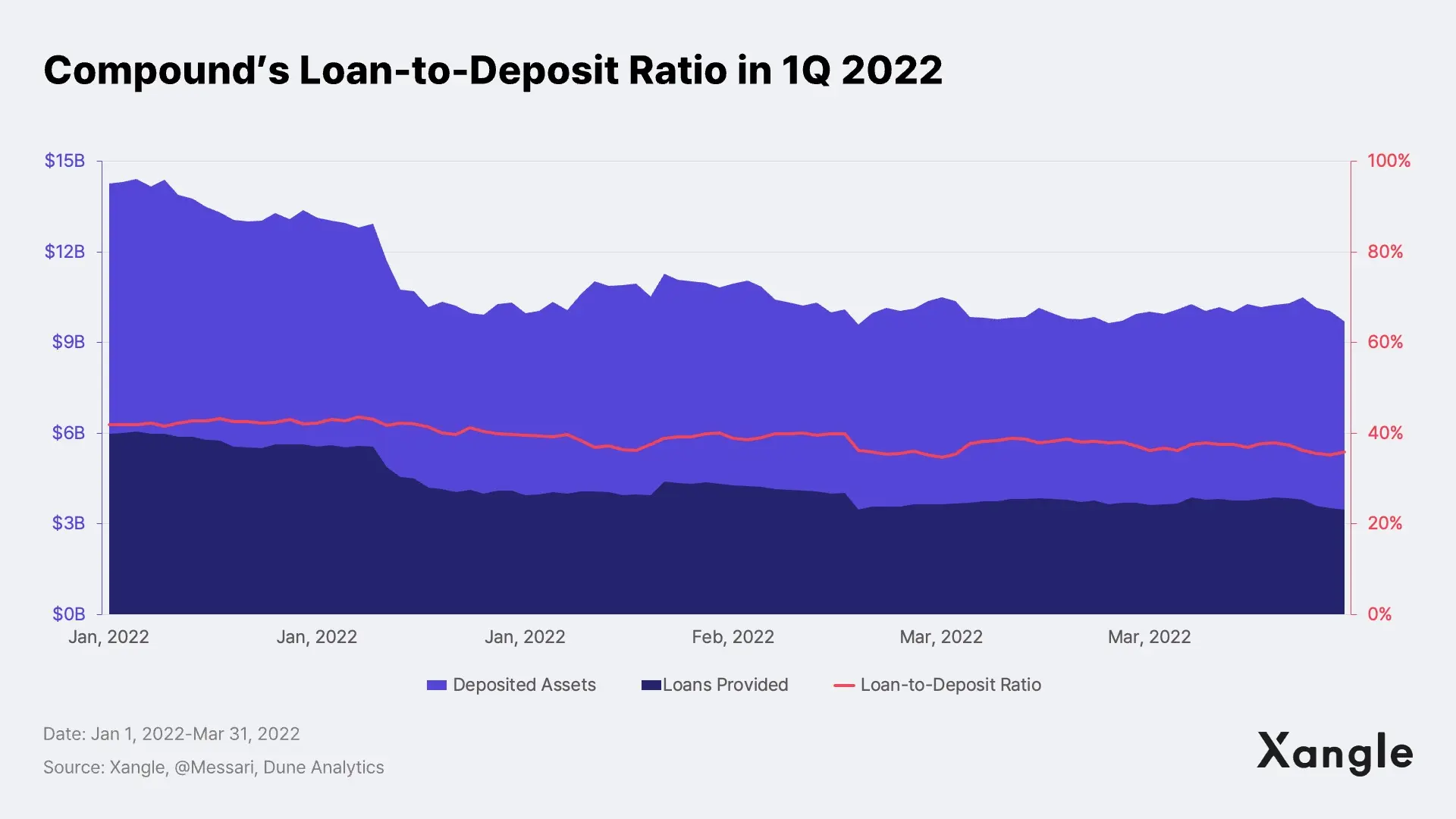

1) Loan-to-Deposit Margin (LDM) of Lending Protocols

Loan-to-Deposit Margin (LDM) represent the difference between interest earned on assets and interest paid on liabilities and is one of the metrics that measures profitability of a lender, or more specifically a bank. Despite many differences, lending protocols and banks’ loan business do look alike in that they both pay interest to depositors and collect interest from borrowers. The following are the key assets and interest rate on deposits and loans of each lending protocol (with key assets being selected based on market cap).

Interestingly, unlike Aave’s low LDM, Compound’s LDM is even higher than that of commercial banks. This is because lending protocol’s interest rate is adjusted by supply and demand in an algorithmic or decentralized governance process, making their highly demanded deposit cheaper while loans more expensive. As of 1Q 2022, Compound’s loan-to-deposit ratio is 39.2%, which is a stark contrast to the 80% level of commercial banks. Now, we’ll move on to discuss why Compound’s high IRD does not necessarily mean a high profitability.

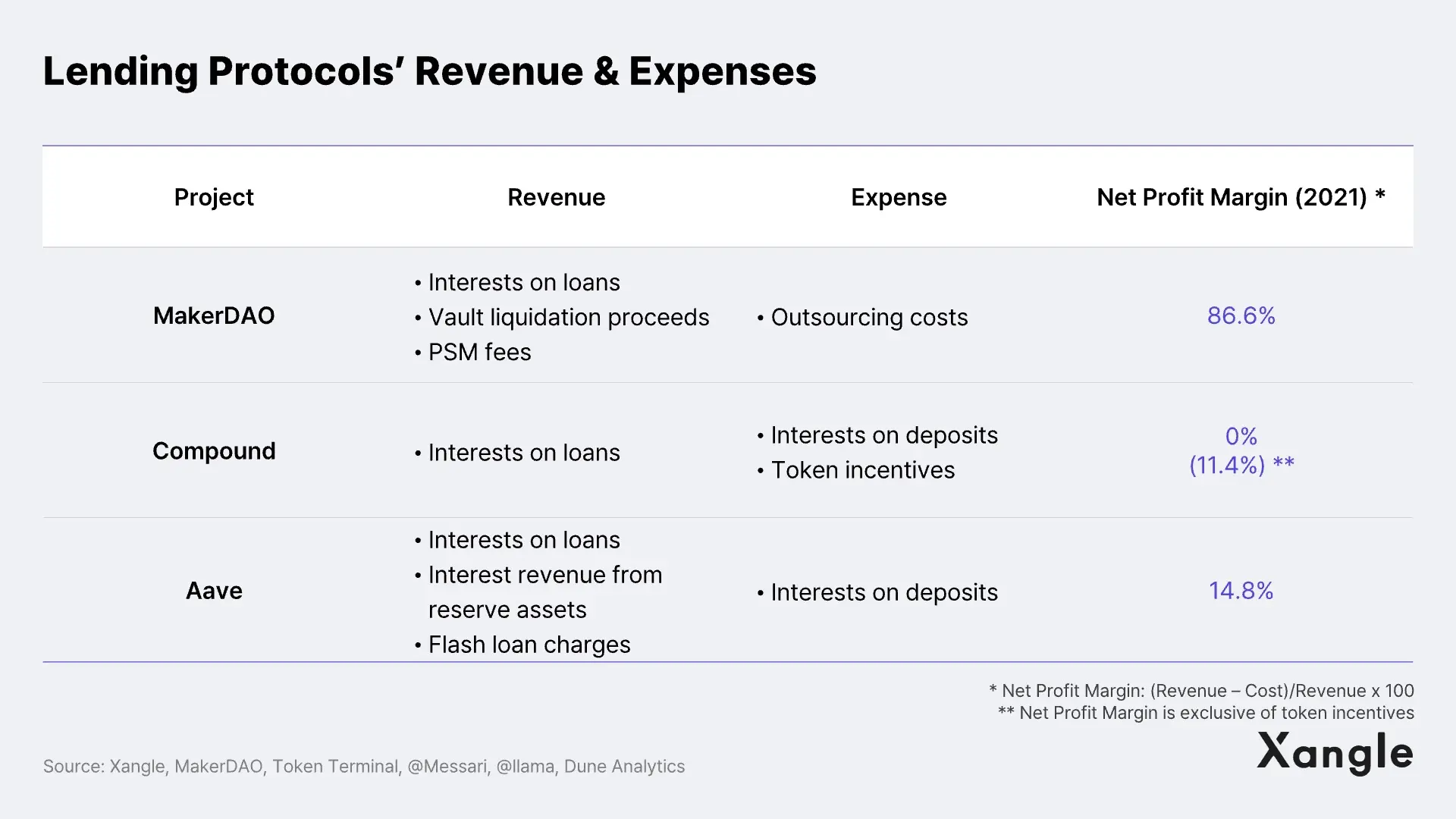

2) Lending Protocol’s Revenue and Costs

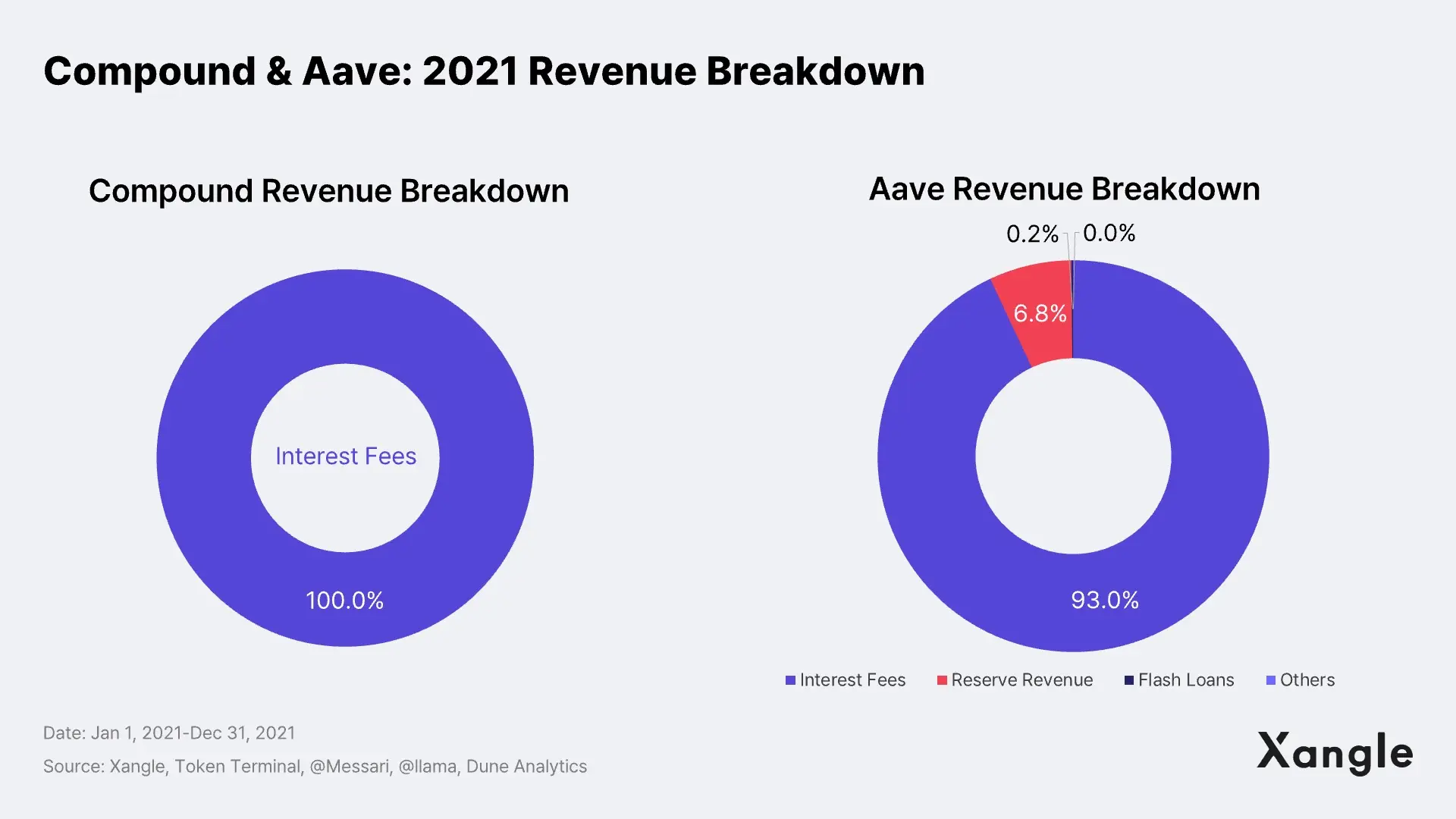

Before verifying if IRD is a proper indication of profitability, one should be aware of the revenue structure unique to lending protocols. For Compound, which generates revenue only from its loans, the loan interest can be viewed as revenue while deposit interest as cost. Even for Aave, which has multiple other sources of revenue such as management of reserve assets and flash loans, the primary source of revenue that takes up 92% is the interest from the loans. The way the lending protocols generate revenue warrants the view that it is similar to how banks earn the income from the difference between interest received and paid.

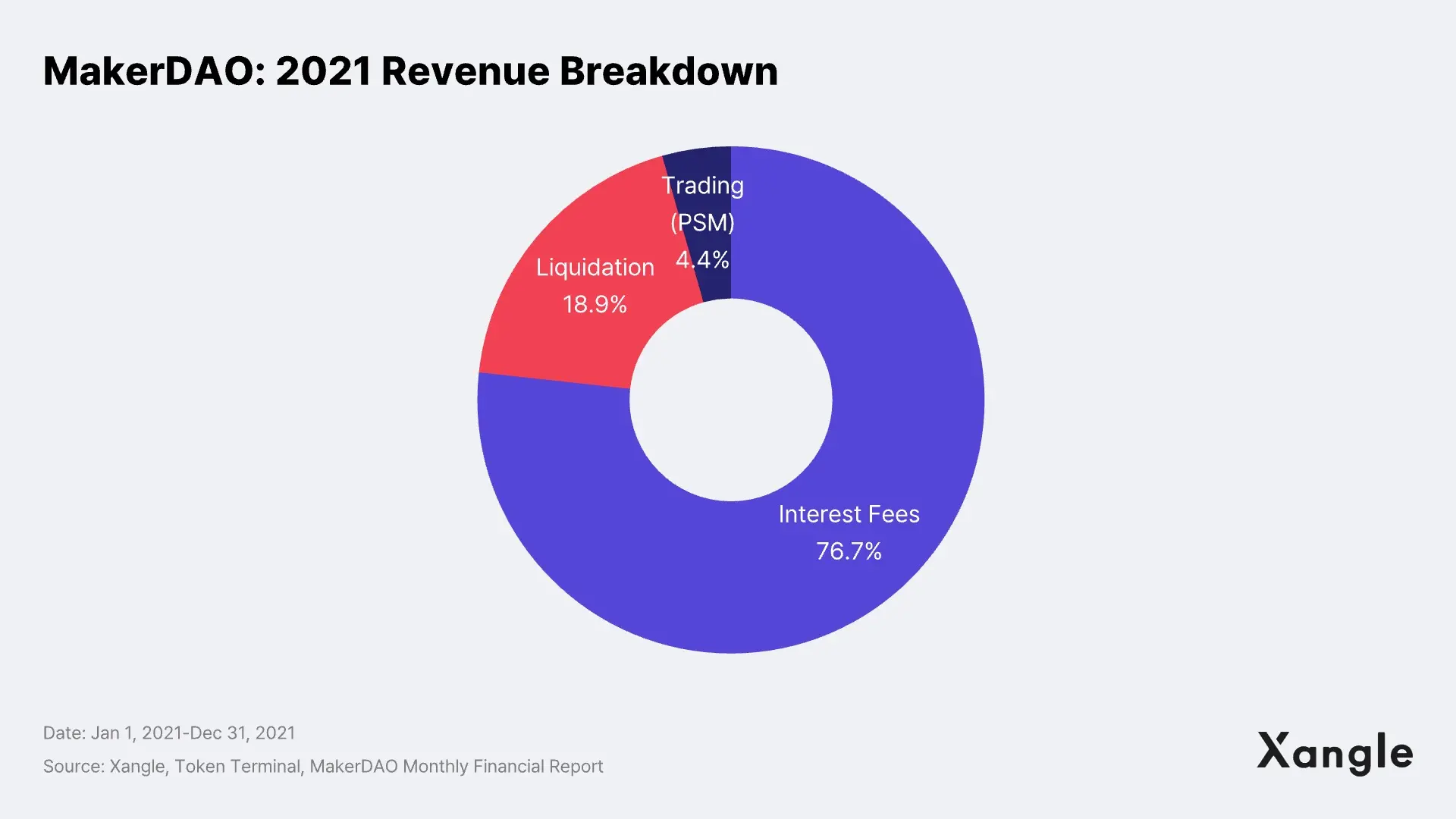

Maker DAO, which issues stablecoin DAI as collateral, is an exception. While most of MakerDAO’s revenue arises from the interest on loans, 23% of the revenue comes from other sources. Trading and liquidation are the non-lending businesses: the former is the transaction fees of PSM (Peg Stability Module) that aims to maintain DAI’s $1 peg and the latter is the liquidation penalty that arises from liquidation of collateral. The following shows how MakerDAO’s revenue streams are different from that of Compound or Aave.

Unlike other lending protocols, MakerDAO provides loans after a borrower sends assets to the vault and DAI is issued. While it collects loan interests (which are vault fees), it does not have to pay out interests, making the cost the protocol incurs very low. As such, MakerDAO’s net profit margin is a whopping 86%, which is significantly higher than its peers’ 10%. It is more reasonable to see Compound’s net profit margin of 11.4% as 0% because Compound offers COMP to incentivize users to attract more traffic. The overall amount of COMP offered as an incentive to depositors and borrowers throughout 2021 was $310M.

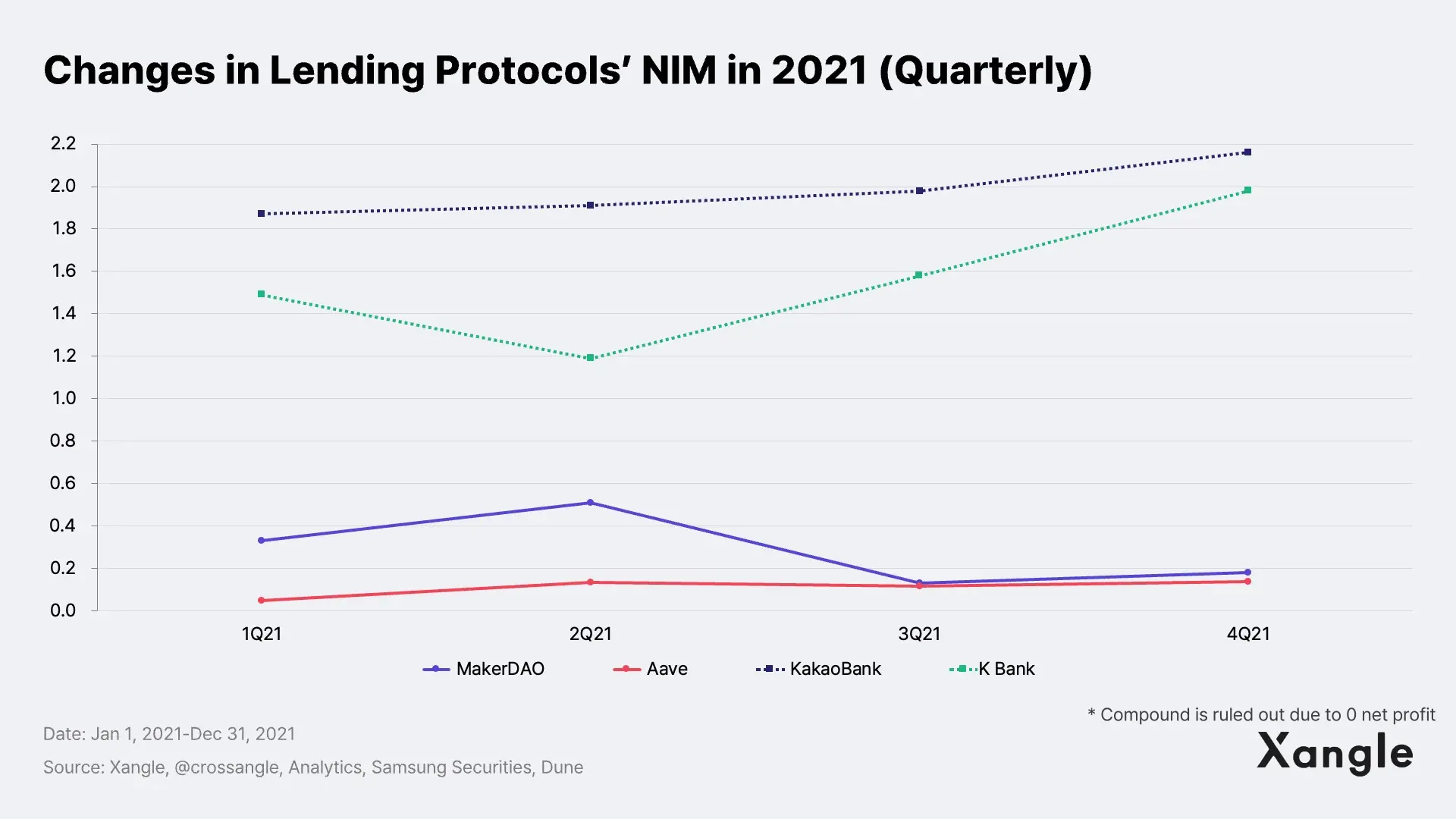

3) NIM Comparison of Lending Protocols

Net Interest Margin (hereinafter, NIM) seems to be a useful indicator to look at to see how much income is generated per unit of asset. NIM is developed to complement IRD and is calculated by dividing LDM by AUM. Once applied to the lending protocols, NIM will allow us to discuss not only the IRD but also the income from the assets under their management. We saw deposited assets as AUM and applied the aforementioned revenue and cost.

MakerDAO and Aave’s NIM for 2021 was 0.28 and 0.11 respectively, showing a notable gap with the NIM of around 2 of the digital banks in South Korea. Still, it may be inappropriate to apply NIM to lending protocols the way NIM is applied to for-profit businesses as they do not solicit loans like financial institutions. Using algorithm, they simply provide matching between potential borrowers and lenders. Further, while their low NIM may indicate that they are failing to earn enough income from the assets under their management, it may also mean that the deposits in the lending protocols are relatively profitable. All this is possible because the protocols are decentralized and not for-profit.

4) Lending Protocol’s PSR & PER Comparison

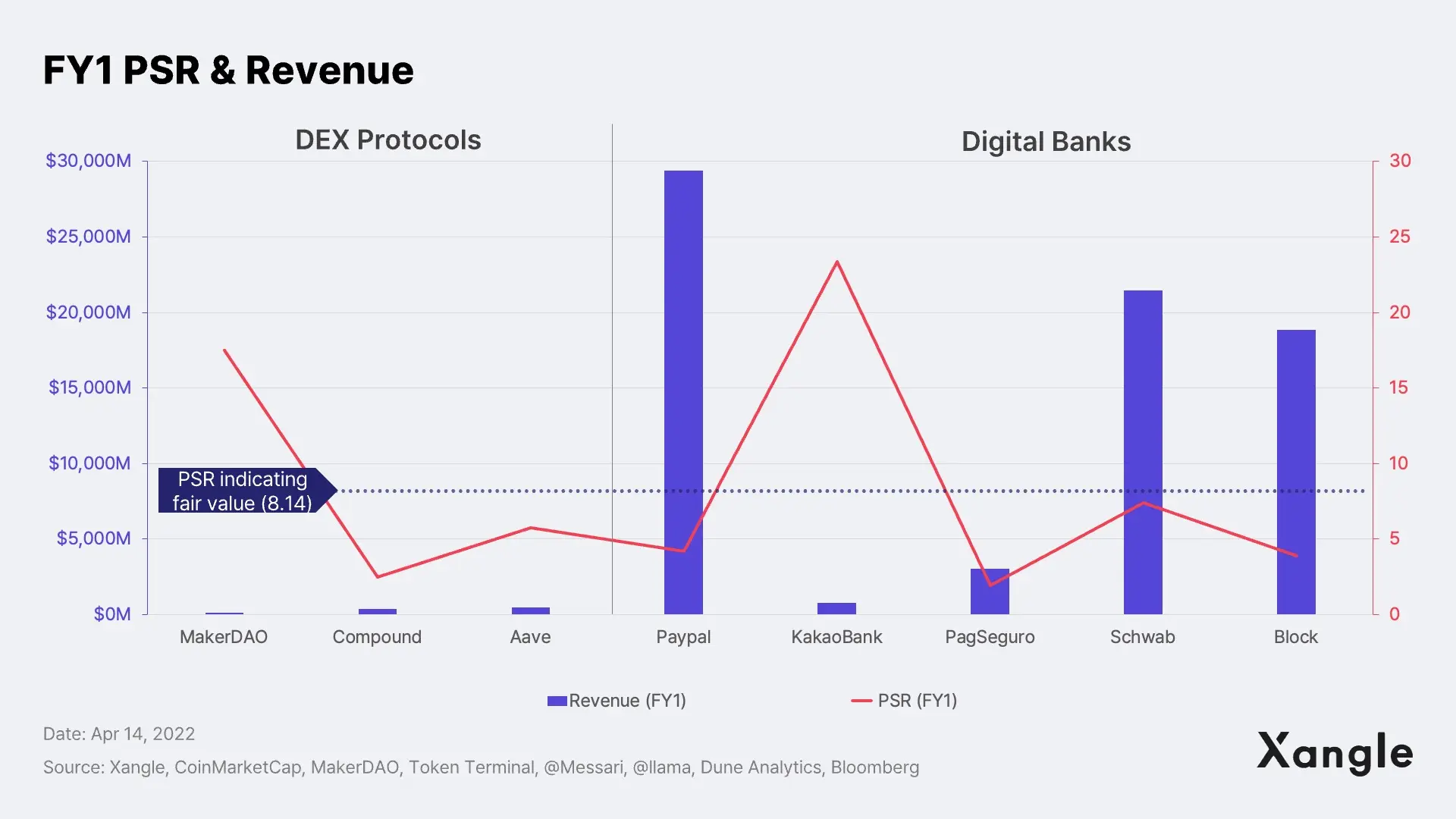

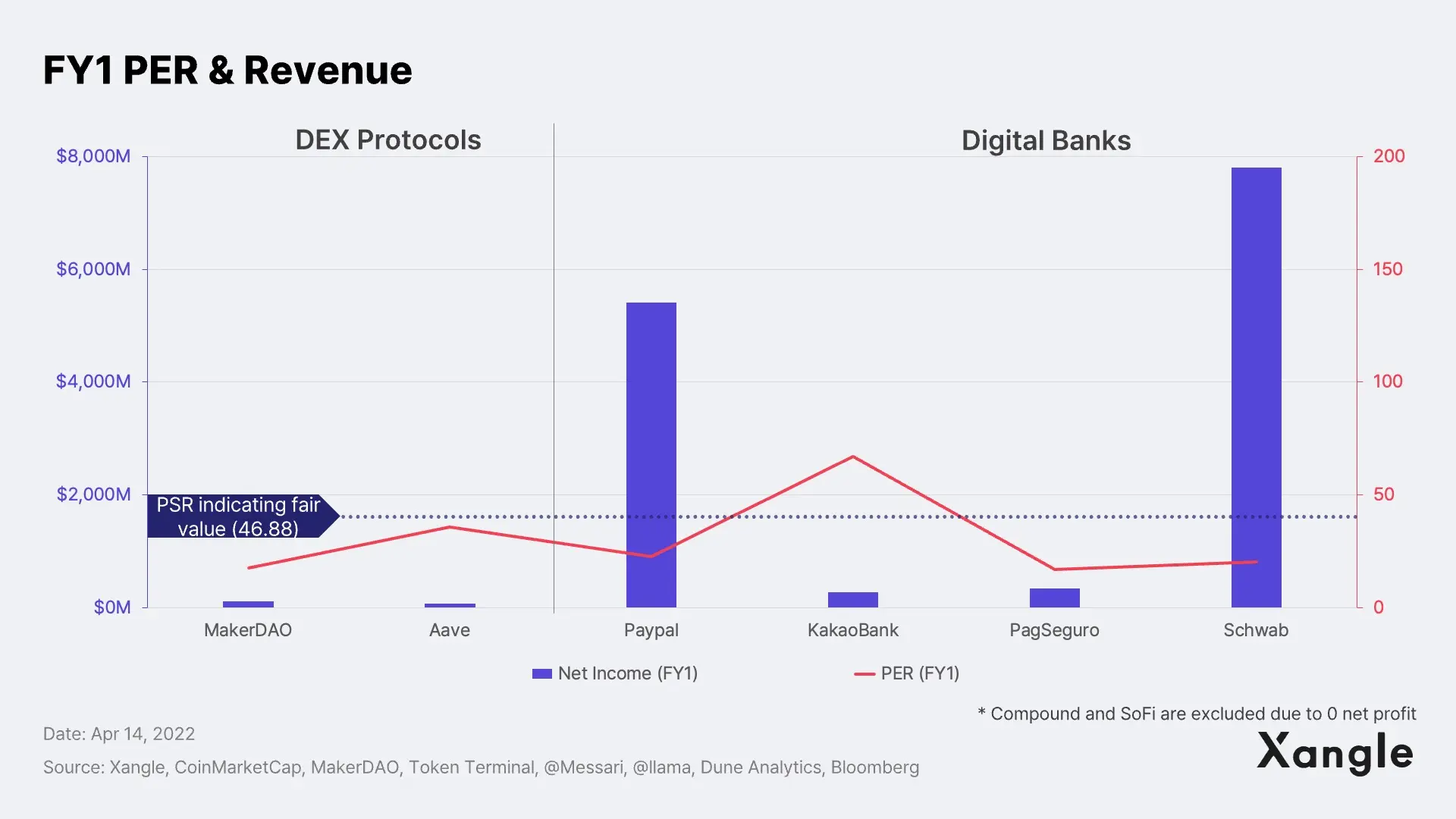

But are lending protocols really overvalued despite low profitability? We tried to find the most straightforward answer to this question with PSR and PER. Like we have already covered in our [Xangle Valuation Series] DEX (Link), a valuation based on PSR or PER aims to determine if the protocols are overvalued or undervalued relative to their revenue, net income, and market cap. In other words, PSR and PER are the ratios that can present us with the multiples the protocols are receiving in the market, compared to their revenue and net income.

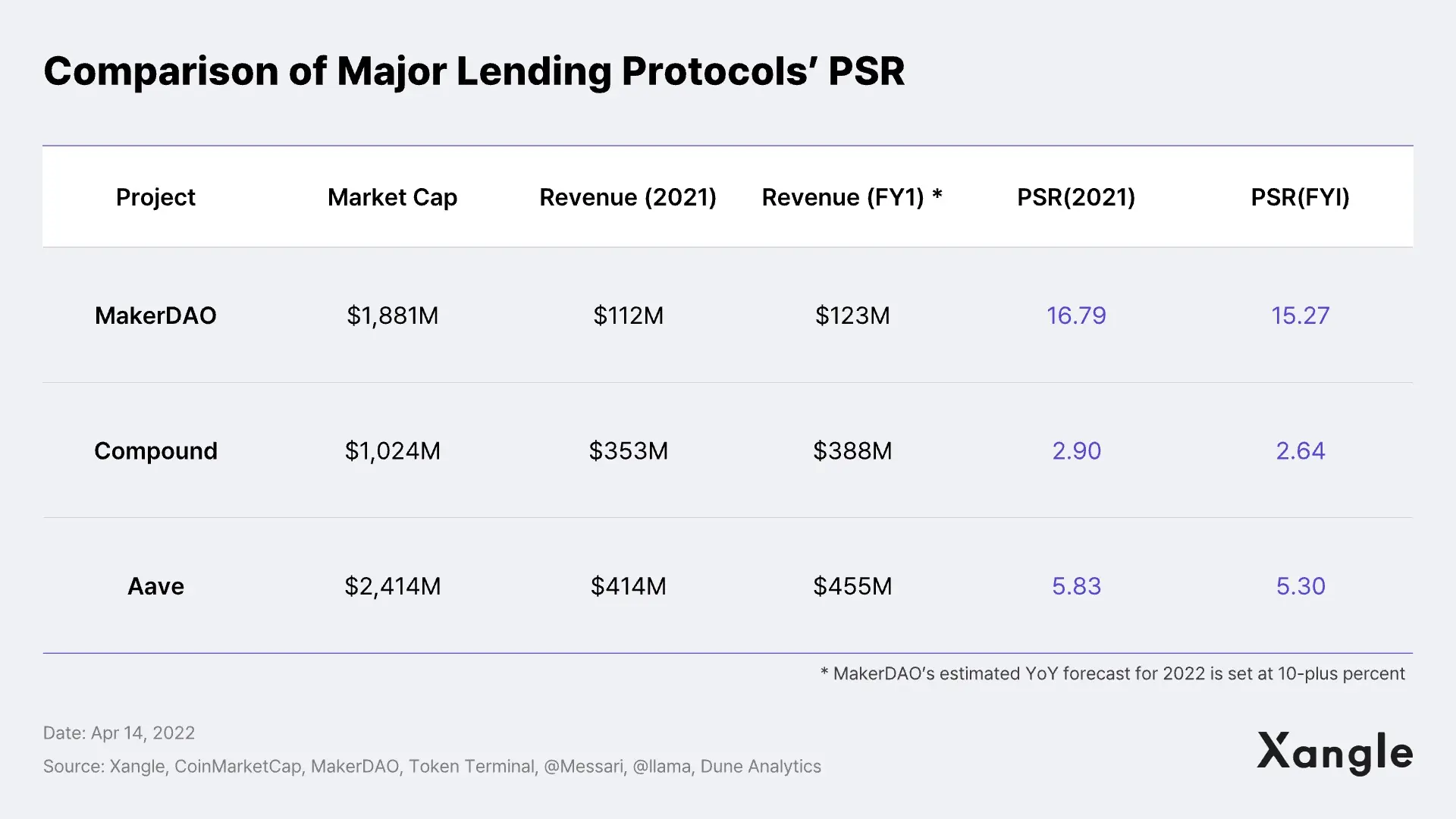

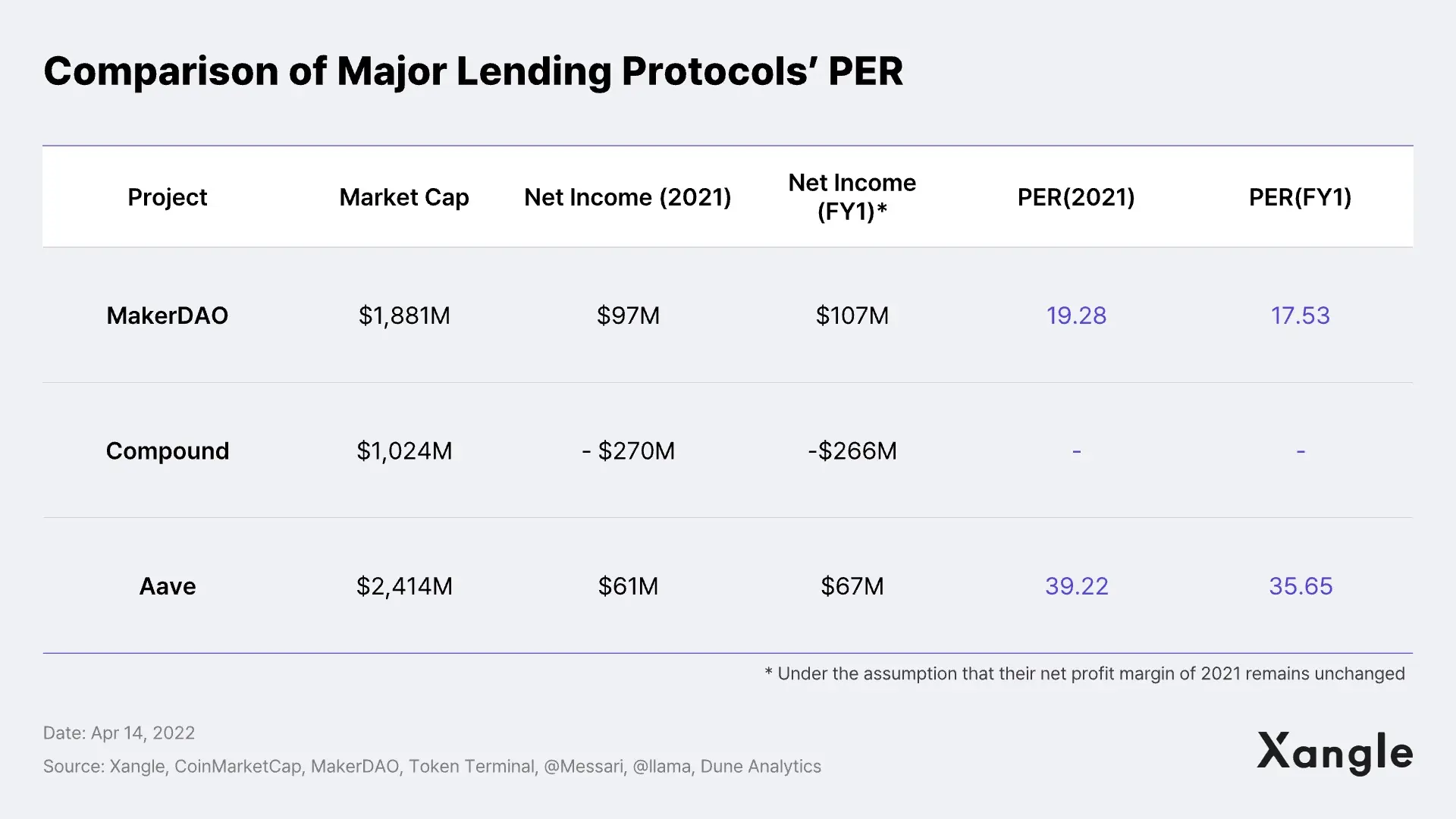

To calculate their PSR and PER, we set a market cap based on the circulating supply as the variable given that token distribution and a subsequent increase in circulating supply dilute protocol’s value. We retrieved the revenue and cost data for 2021 from Token Terminal and monthly financial reports of each protocol. This is because Token Terminal counts only the loan interests as revenue and deposit interests as cost, which can create a gap with the market. The YoY growth estimate for 2022 (FY1) is set at 10%, adopting MakerDAO’s announcement.

According to the PSR results for the major lending protocols, Compound came in at 2.90 while MakerDAO at 16.79. Although this may be seen as an indication that MakerDAO is substantially overvalued compared to Compound, it should be reminded that MakerDAO keeps registering a net profit margin of higher than 80%.

Contrary to PSR, the PER results seem to suggest that the most undervalued lending protocol is MakerDAO, considering its net profit. While PER was unavailable for Compound, which failed to register a net profit due to token incentives, Aave recorded a high PER, seemingly reflecting expectations over the recent V3 launch and subsequent partnerships with financial institutions and multichain expansion. Then, what would be their fair value?

5) Fair Value Based on PSR & PER

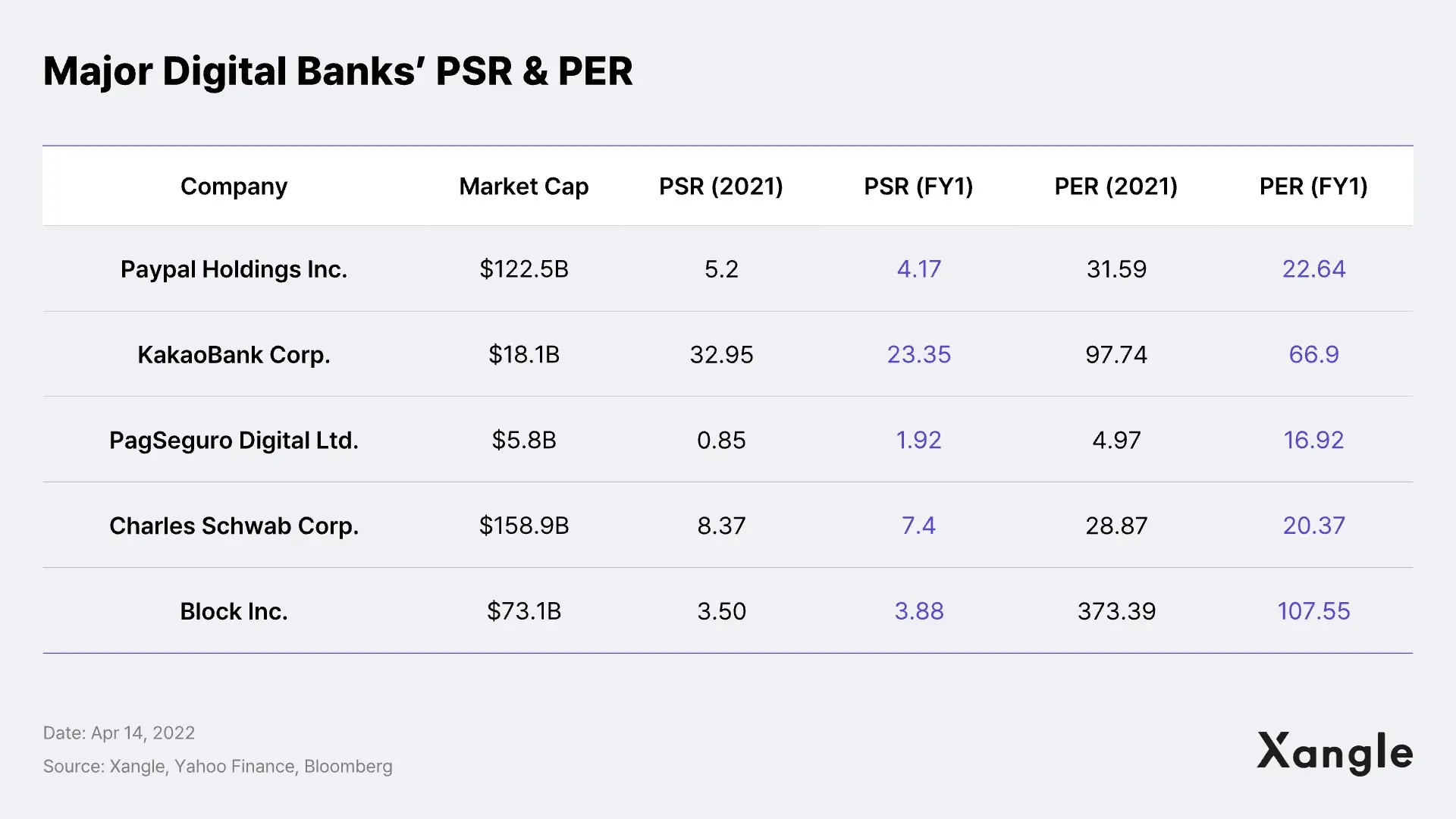

Selecting a peer group to determine overvaluation or undervaluation using PSR and PER. In the sense that the top three lending protocols provide loans leveraging deposited assets, their business model is the most similar to that of a digital bank among the traditional banking business models. The PSR and PER of the digital bank chosen as the peer group are as follows:

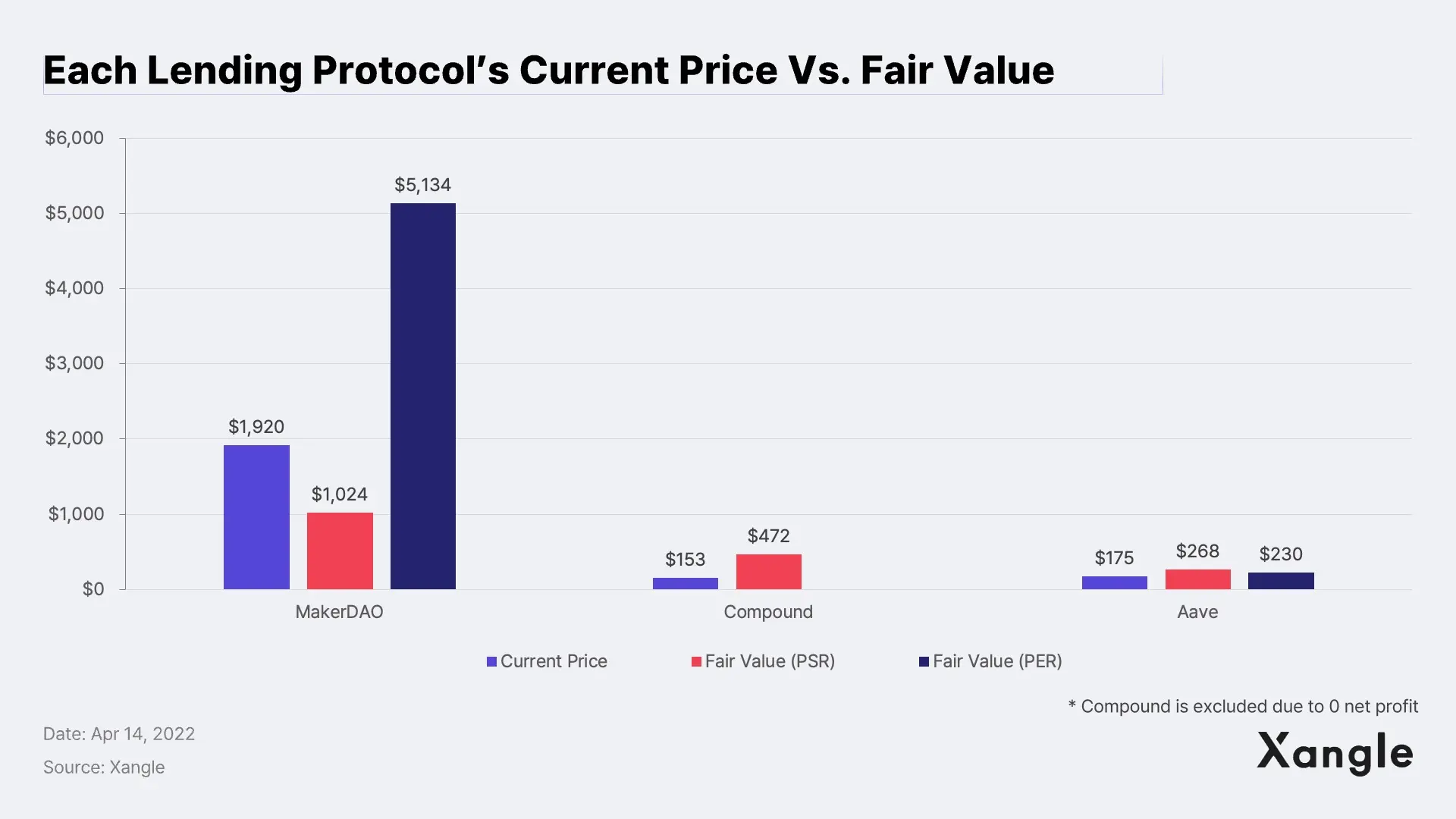

The peer group’s average PSR and PER were 8.14 and 46.88 respectively. Here, we will adopt these ratios as the fair value and see if each lending protocol is fairly valued. Compared to its competitors, MakerDAO is moderately overvalued based on PSR but undervalued based on PER as its high earnings ratio warrants 2.7x the current value. PSR and PER of Aave, on the other hand, indicate that the protocol is currently undervalued and that its price may potentially rise 1.5x and 1.3x. Compound, on the other hand, had a potential to jump 3-fold but failed to achieve a net profit, making PER unavailable. Yet, DeFi protocols are P2C lending platforms and there are significant differences between their business models and banks’ business models. The business models differ even among the lending protocols, and the estimated fair values should only be used as reference.

5. Platform-Based Assessment: Estimating Network’s Value Based on Number of Users

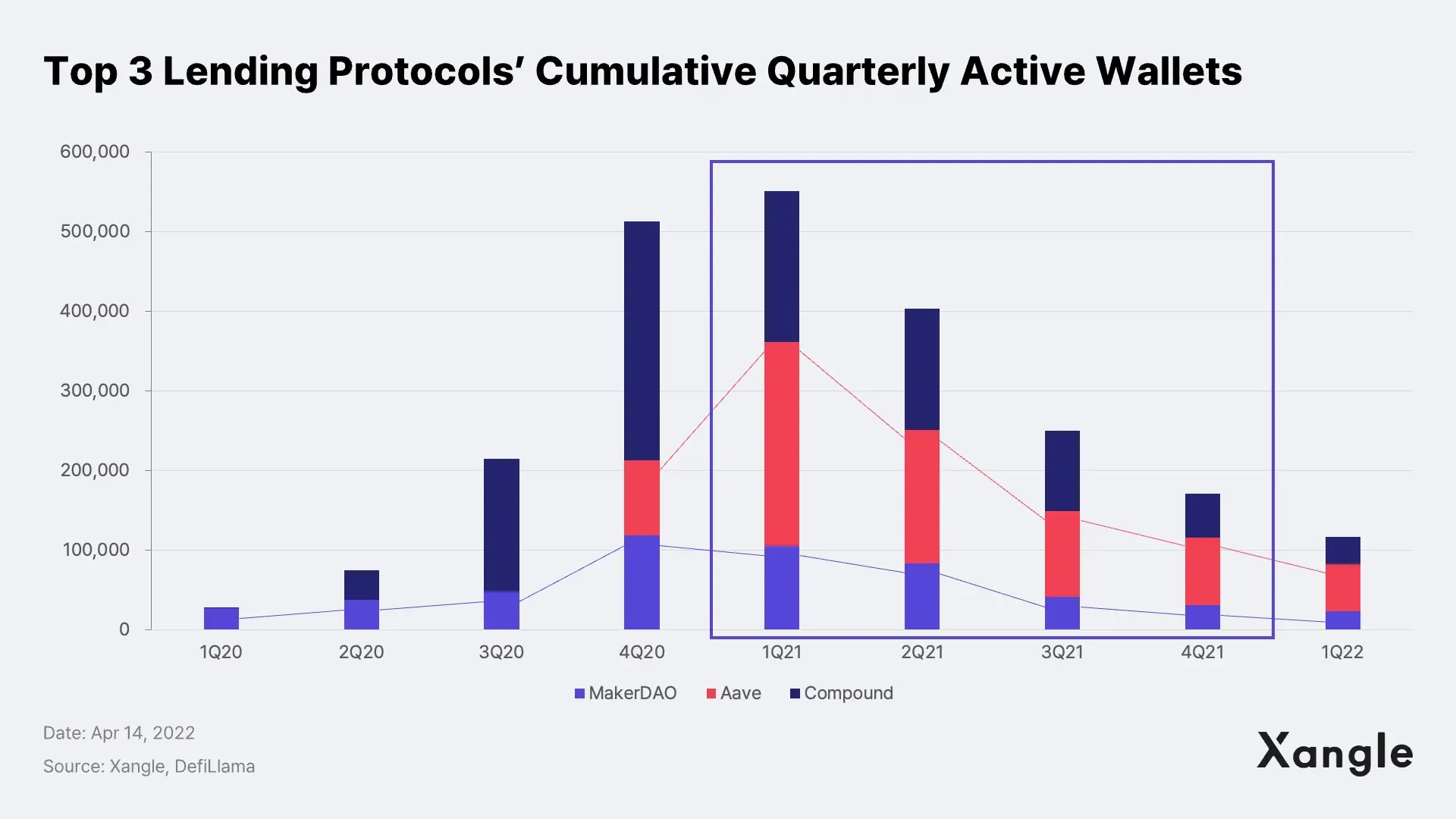

If lending protocols are considered basic DeFi platforms, the number of active users is applicable to valuation of lending protocols in the same way the number of monthly visitors to the platform (MAU) are reflected in the valuation of digital banks. In the context of blockchain, the number of active wallets, rather than simply the number of visitors, is more likely to give a more accurate snapshot of the usage level of a protocol.

Major lending protocols’ cumulative active users are continuously on the decline after it peaked in 1Q 2021. When this is combined with other factors, including TVL, lending volume, and earnings, it suggests that the growth of the protocols seems to have been primarily driven by a rise in the price of deposited assets or by the so-called whales, rather than the health and organic growth of the protocols. As such, it is considered that securing a larger group of B2C consumers and enhanced profitability will be the key to higher multiples for lending protocols.

6. Lending Protocol: Full of Potential Despite a Few Shortcomings

We have analyzed the lending sector in the crypto market from various angles and found that this sector seems to be relatively overvalued than the DEX sector. The drivers behind such overvaluation of the top three lending protocols are believed to be: i) a constant demand for a DeFi protocol that has time-tested stability, bucking market fluctuations; ii) a strong demand for the tokens as governance tokens as engagement in governance is exceptionally high in those projects. For this valuation, we decided not to include the high-performing Benqi, Maple Finance, and Solend given their short presence in the market.

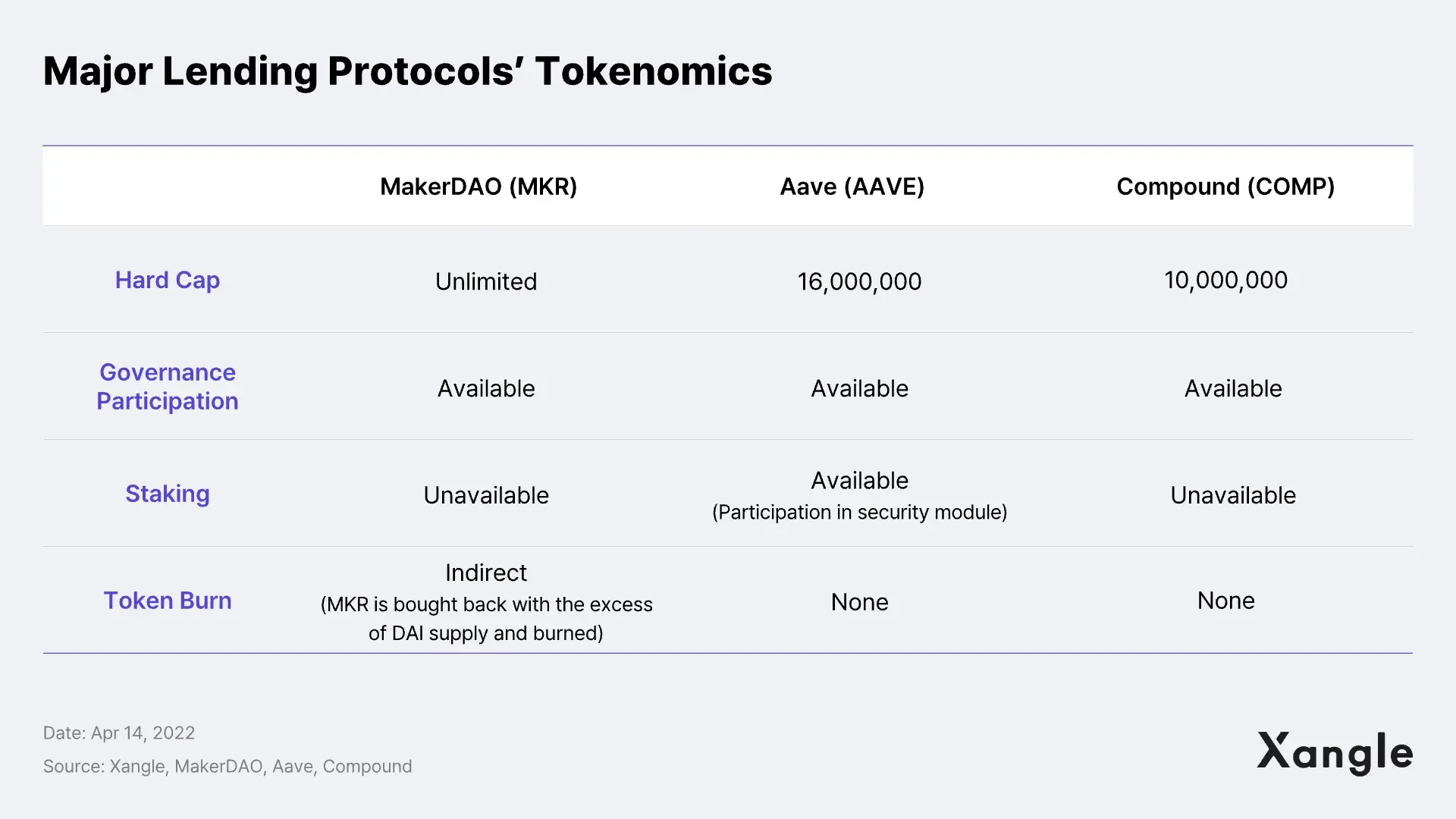

Token economics is another essential variable in valuation. In this valuation, we ruled out Discounted Cash Flow (DCF) and Residual Income Model (RIM) based on our judgement that both models are not applicable given the tokenomics of the protocols. Instead, we worked primarily on NIM and PER to compare net income against revenue. Unlike DEXs where a percentage of transaction fees is paid as yield, the top three lending protocols do not share the profits but rather keep them in their treasury, making a cash flow-based valuation inappropriate. The initiatives of token utility improvement discussed in MakerDAO and Aave's governance forum, therefore, bodes well for the lending protocols.

In “[Xangle Valuation Series] ④ Lending Protocol,” we tried to set forth valuation metrics, focusing on the key indicators that investors should be mindful of. Now that we have key performance indicators available for estimating the fair value of a protocol, we would expect crypto to become more widely adopted as a means of investment rather than speculation.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.