A Complete Summary of Stablecoins: Who Will Claim the Throne?

[Xangle Originals]

Written by CHOBiden (Apr 29, 2022)

Translated by Rhea

Table of Contents

1. Introduction

1-1. Competition for Stablecoins is Heating Up

1-2. What Makes Stablecoins So Important?

2. Different Types of Stablecoins

2-1. Fiat-Collateralized Stablecoins

2-2. Crypto Asset-Collateralized Stablecoins

2-3. Algorithmic Stablecoins

2-4. Fractional Stablecoins

3. Discussion on the Hot Potato: Algo Stablecoins

3-1. Are Algo Stablecoin Currencies?

3-2. Challenges Algorithm Stablecoins Seek to Address

3-3. Challenges Algorithm Stablecoins Must Resolve

4. CBDC and Regulations on Stablecoins

4-1. Current Policies in Different Countries

4-2. Potential CBDC Implications for Stablecoins

5. Conclusions

5-1. New Experiments

5-2. What Should Be the Next Steps for Stablecoins?

1. Introduction

The hottest keyword in the crypto scene in the first quarter of this year was “Stablecoins,” without question. As the market overall takes on a trend more focused on risk avoidance, stablecoin farming with high yield and guaranteed principles was in high demand. It was also such high yields from farming stablecoins, UST and USDN, that were behind the rapid climb of LUNA and WAVES even during the bear market. Moreover, in April, NEAR and TRON announced the launch of their own stablecoins, USN and USDD, respectively, fueling the stablecoin competition even further. This trend is the exact opposite of the direction taken by the last year’s bull market, where stablecoin farming was only used as a mere means of leverage and drove market participants to take even more interest in stablecoins.

1-1. Competition for Stablecoins is Heating Up

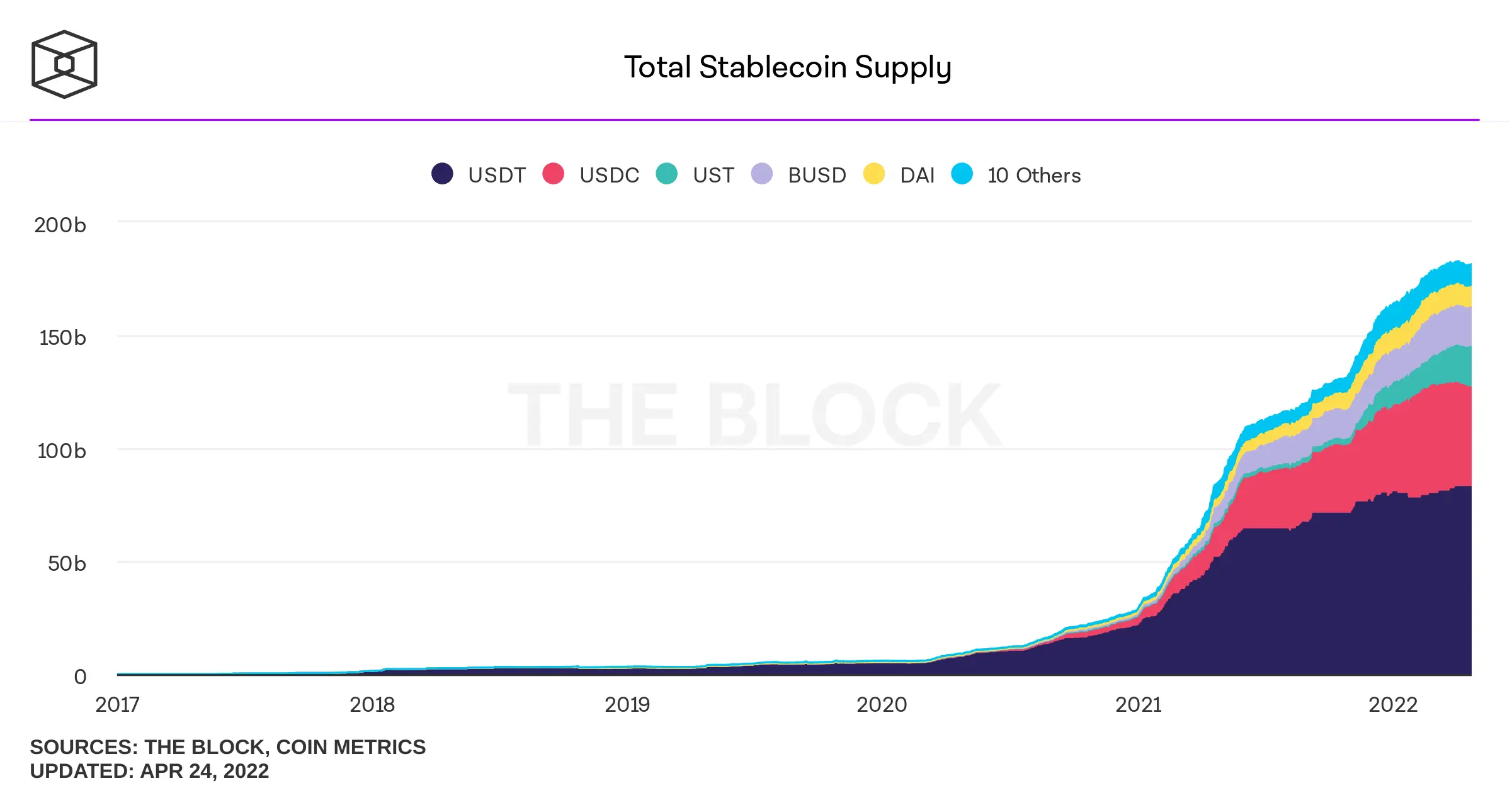

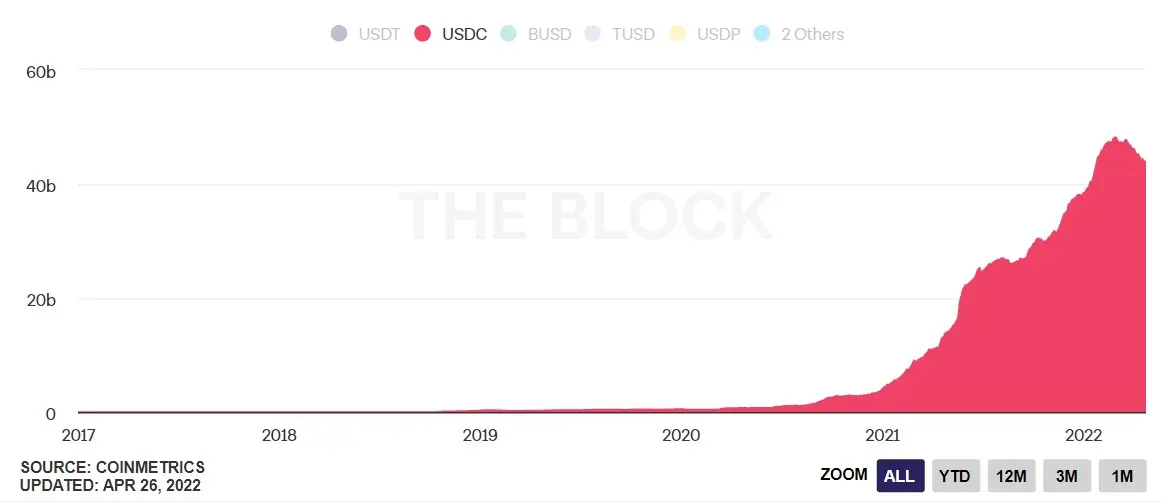

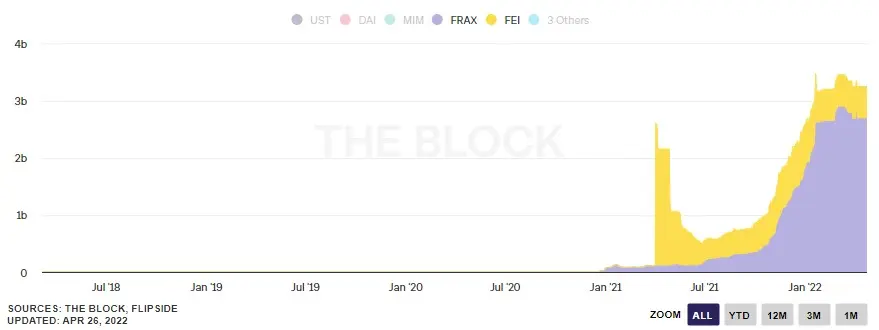

The total volume of stablecoins issued and in circulation has grown over 2,900% since January 2020, reaching $181 billion today. Numerous stablecoins tested their luck in this sea of opportunities presented during such a rapid expansion, but many of such projects dissipated as they failed in their early stages. The fact that only 8 stablecoins* have successfully secured their position with over $1 billion in supply out of a total of 96 stablecoins listed on CoinMarketCap only goes to show just how fierce the competition is. As different stablecoins take their shots at climbing up the throne to rule over the stablecoin market, the issuers of stablecoins backed by fiat currency are striving to comply with the regulations, and projects issuing stablecoins on blockchains are putting their every effort into securing their stability and utility.

* USDT, USDC, UST, BUSD, DAI, FRAX, MIM, and TUSD

1-2. What Makes Stablecoins So Important?

So, how important a role does stablecoins play in the blockchain economy that it is getting just about everyone rush to get their piece of this cut-throat battle for the throne of this market? The biggest reason would be the high demand for crypto assets with their value fixed or “pegged” to the value of fiat currencies. With the blockchain-related industry growing explosively and bringing in large scales of capital infusion, a growing number of non-expert users are starting to participate in the blockchain economy. Unlike the blockchain users in the early days who stood against the traditional currency policies and financial system both in principle and practice, these new entrants show a strong preference for stable crypto assets with fixed value over those with severe volatility. It is in the same context that institutions are attracted to this market as well. Institutional investors managing massive capital also have a high demand for stablecoins that maintain the same value as fiat currencies. The fact that such stablecoins have secured their places at the very top in terms of market capitalization and transaction volume on their respective mainnets, despite all the numerous criticism against the U.S. currency policy, clearly shows that stablecoins take up a significant share of the blockchain economy.

Another reason is accessibility. While there may be various reasons behind the high demand for USD, including to use as a defense mechanism against depreciation of own local currency and for international remittance, actually going about using USD outside of the U.S. territory in the real world is very complicated. Even after going through all the hoops and hurdles of the various regulations on foreign exchange transactions in different countries, users have to deal with banks charging expensive fees for their currency exchange and money transfer services, making it expensive both in terms of time and cost. Stablecoins based on blockchain, on the other hand, enable any users worldwide with internet access to use USD in a very simple and inexpensive manner.

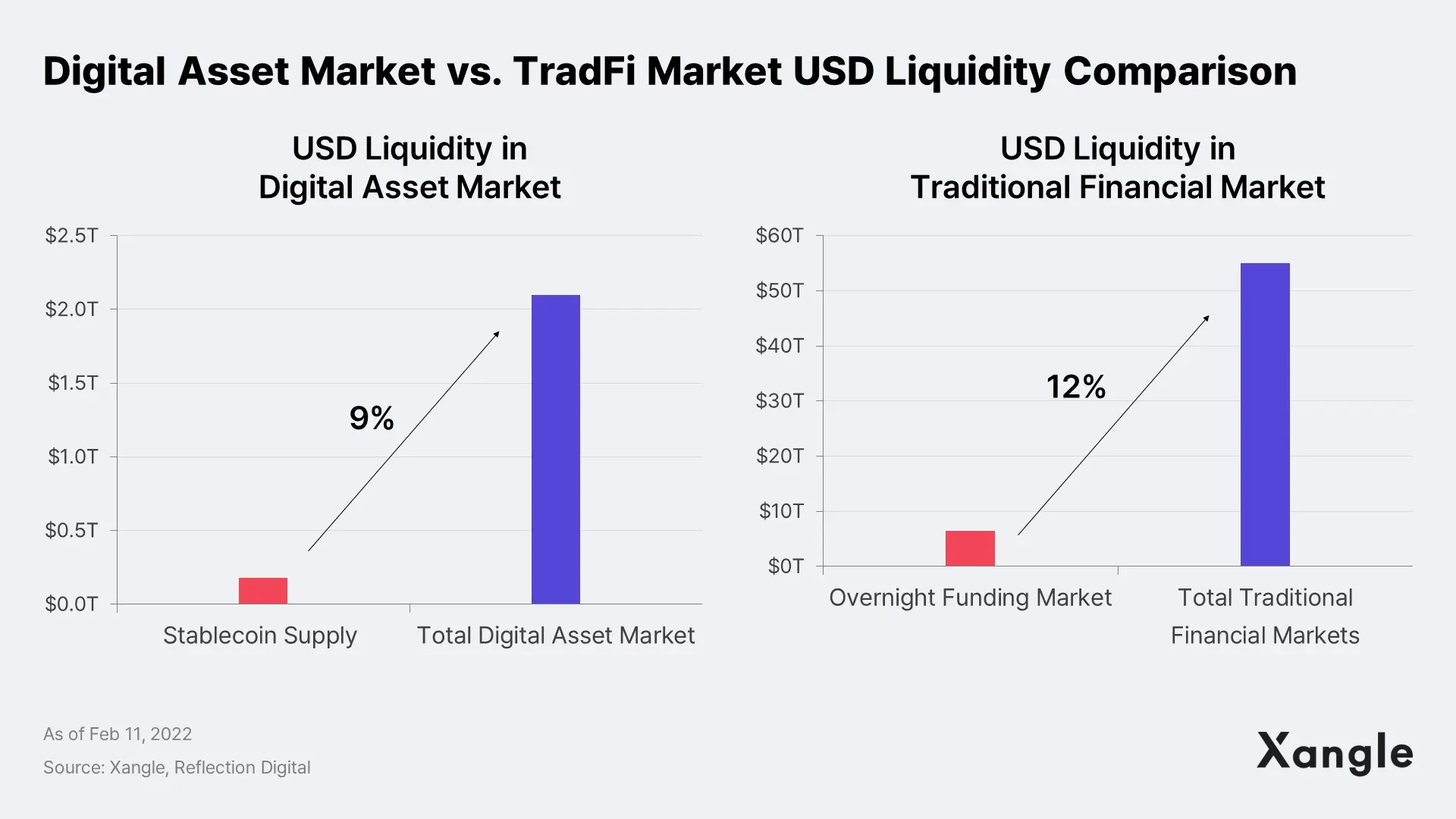

However, the supply of stablecoins is yet to catch up with such high market demands. According to Reflection Digital, as of February 2022, the circulating supply of stablecoins is about 9% of the total digital asset market, with 25% less liquidity compared to the traditional financial market’s dollar liquidity of 12%. This figure may not seem like much of a difference at a glance. However, it implies that the additional stablecoin supply required would extend to $300 billion, which is over 160% of the current supply, even with a conservative forecast of a two-fold growth for the digital asset market assumed for the next ten years. Shortage of stablecoin supply would cause an imbalance of supply and demand and leads to capital inefficiency in the blockchain economy, resulting in a funding cost increase. This is why an increase in stablecoin supply must be accompanied to reach an efficient blockchain economy.

2. Different Types of Stablecoins

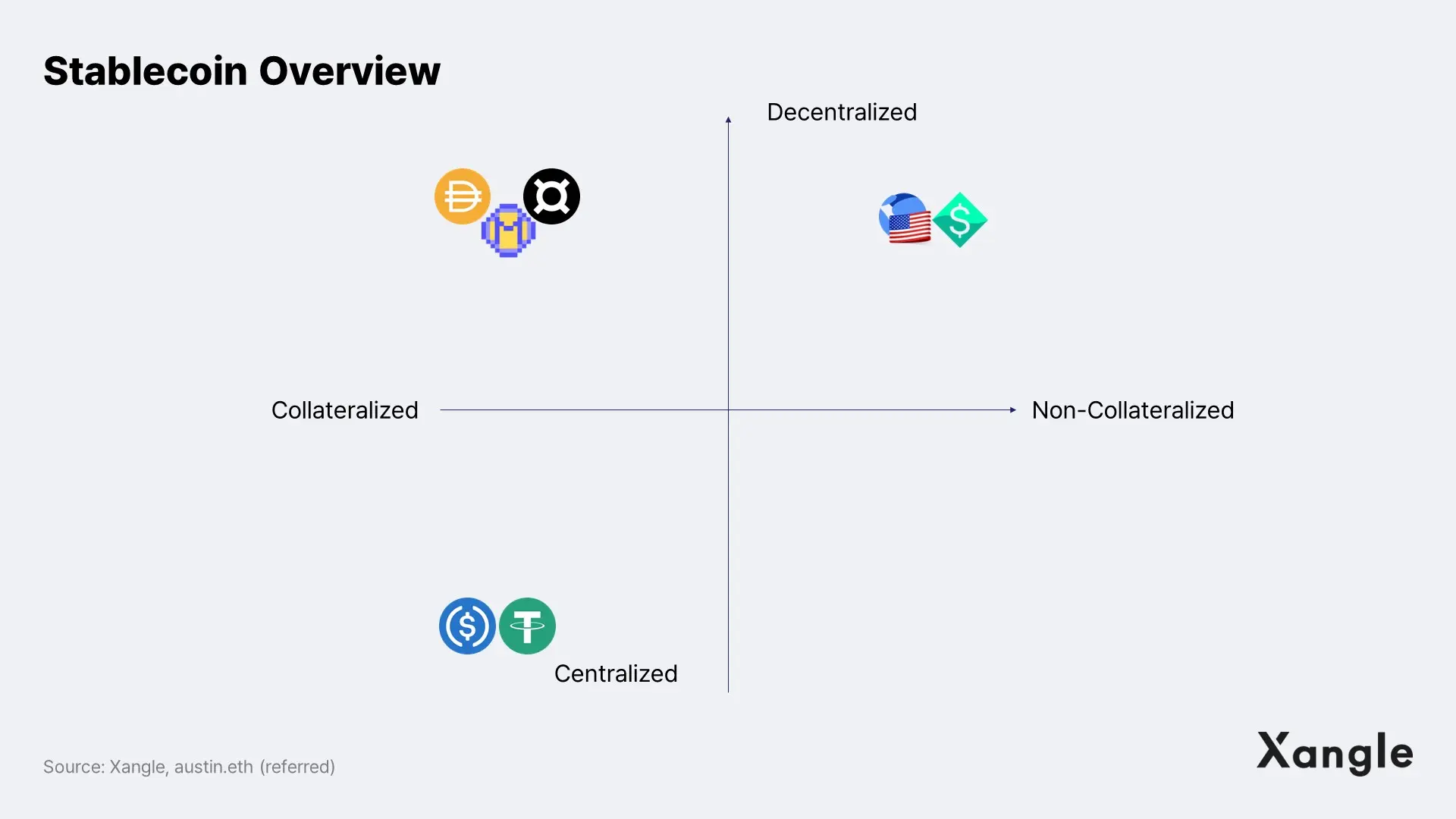

As discussed earlier, the stablecoins sector takes up an important position in the blockchain economy and shows a high potential for rapid growth. However, not all stablecoins follow the same mechanism. Because each stablecoin project uses different approaches to attain efficiency within the limitations of the “stablecoin trilemma,” a wide range and different types of stablecoin projects exist. The stablecoin trilemma is a theory put forth by Multicoin Capital with inspiration from the economic concept of the “impossible trinity (or trilemma),” which explains that there can be no stablecoin that would satisfy all three pillars as below:

- Price Stable

Maintains the same value as fiat currency - Decentralized

Free from controls by any centralized entity - Capital Efficient

Uses capital efficiently

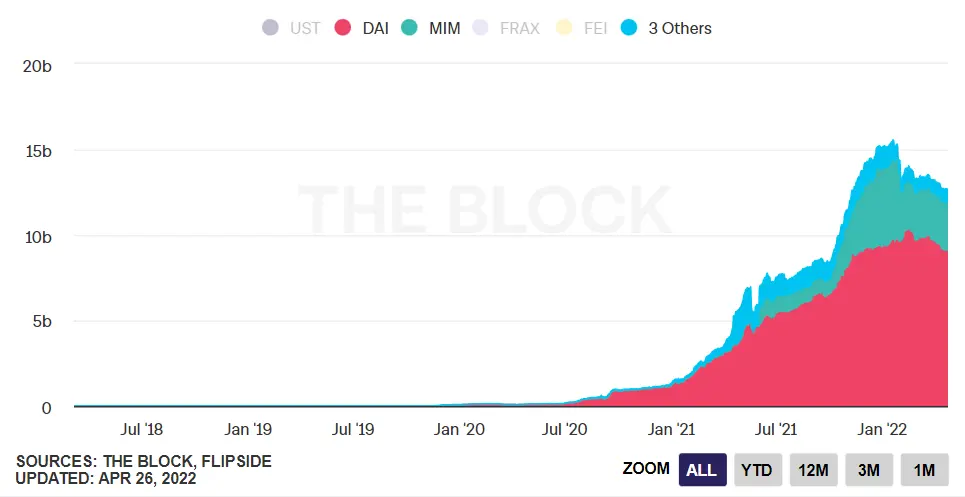

For instance, the fiat-collateralized stablecoins such as USDT and USDC satisfy the stability and capital efficiency needs. But they also come with a risk of centralization as they are under the control of the authorities issuing the fiat money. On the other hand, the crypto-collateralized stablecoins, including DAI and MIM, fulfill the aspects of decentralization and stability. However, this is at the expense of capital efficiency due to their high collateralization ratio. Algorithmic stablecoins like UST and USDN satisfy the aspects of decentralization and capital efficiency. But the risk of stability coexists since there is no collateral. Each of these categories can be explored in further detail with examples of a few representative cases as shown below:

2-1. Fiat-Collateralized Stablecoins

Fiat-collateralized stablecoins, or fiat stablecoins, refer to the stablecoins whose value is backed by cash and cash equivalents in custody under the traditional banking system. The most representative examples are USDT, USDC, and BUSD. Other than USDT issued outside the U.S. jurisdiction, USDC and BUSD are issued only with cash and the U.S. Treasuries as their collateral and under strict regulations by the U.S. government. Some people question the fiat stablecoins for being subject to censorship by centralized entities and having a single point of vulnerability. However, the fiat-backed stablecoins are most likely to function as the state-approved stablecoin in the future and currently take up about 80% of the total stablecoin supply. Because they are also the only type of stablecoins that can be directly exchanged with the physical U.S. dollars today, the rise and fall of their supply volume are sometimes used as a metric to check the digital asset market’s liquidity inflow and outflow.

2-2. Crypto Asset-Collateralized Stablecoins

Crypto asset-backed stablecoins, or crypto-collateralized stablecoins, refer to stablecoins backed by a single or multiple crypto assets as their collateral. The most well-known examples are DAI, MIM, and LUSD, which are secured loan stablecoins, and sUSD, ibEUR, and agEUR, which are synthetic asset* stablecoins. They only differ in whether they take the form of lending. Other than that, they are the same in that they require a high collateralization ratio that exceeds 100% due to crypto assets’ volatility and are liquidated if their collateralization ratio is not met. Despite the inconvenience of not being able to exchange crypto-collateralized stablecoins with physical U.S. dollars directly, they have their own set of advantages in that their stability is secured with high collateralization ratio and are decentralized and protected against censorship.

One might be inclined to think that crypto-collateralized stablecoins are more efficient and suitable to the ideology of decentralization than fiat stablecoins. However, they also come with pain points of their own. Their most significant issue is their inherent limitation that arises from the fact that these stablecoins take the form of loans, and the low capital efficiency from the over-collateralization which stems from that process. For example, in order to issue $100 worth of DAI, over $170 ETH is required, which results in capital inefficiency, having to hold over $170 in collateral to put just $100 in circulation. It is very ironic, especially if you think back to how one of the major reasons decentralized finance gained its spotlight in the first place was the capital cost saved from eliminating the intermediary. Moreover, there is the issue of difficulty in scaling up since the issuance of such coins is always accompanied by the risk of liquidation.

* Synthetic assets refer to assets following the value of other specific assets. Synthetics only follow their price and cannot gain the rights embedded in the underlying assets.

2-3. Algorithmic Stablecoins

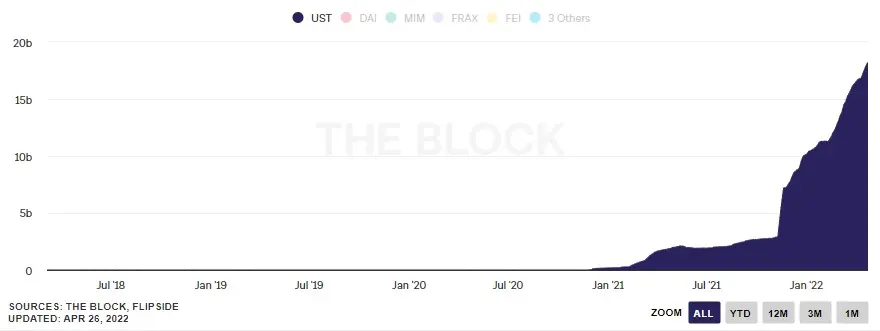

Algorithmic stablecoins, or algo stablecoins, refer to stablecoins that maintain their pegs to 1 USD only by adjusting their circulating supply volume and arbitrage trading algorithm. Since algo stablecoins have been at the height of everyone’s interest lately, this article will address the topic in further detail later. For now, the discussion will cover one of the representative cases, UST, to understand how their value is maintained without any collateral.

UST

UST is an algorithmic stablecoin issued on Terra mainnet, designed to be exchanged at any given time with $1 worth of LUNA, Terra mainnet’s key currency. In other words, it is programmed to maintain its $1 peg through arbitrage trading with LUNA whenever the price of UST deviates from $1. For example, when UST’s value is at $1.01, LUNA holders can burn $1 worth of LUNA and mint 1 UST to gain a profit of $0.01, and such pressure to sell will ensure that the price of 1 UST returns to $1. Conversely, when the UST price drops to $0.99, UST holders can burn 1 UST and mint $1 worth of LUNA to gain a profit of $0.01. Such arbitrage trading will continue until UST returns to its $1 peg. In summary, through the process of arbitrage trading between UST, which has a fixed value, and LUNA, which has a floating value, the supply and demand of issuing volume for both tokens are balanced, allowing UST to maintain its $1 peg.

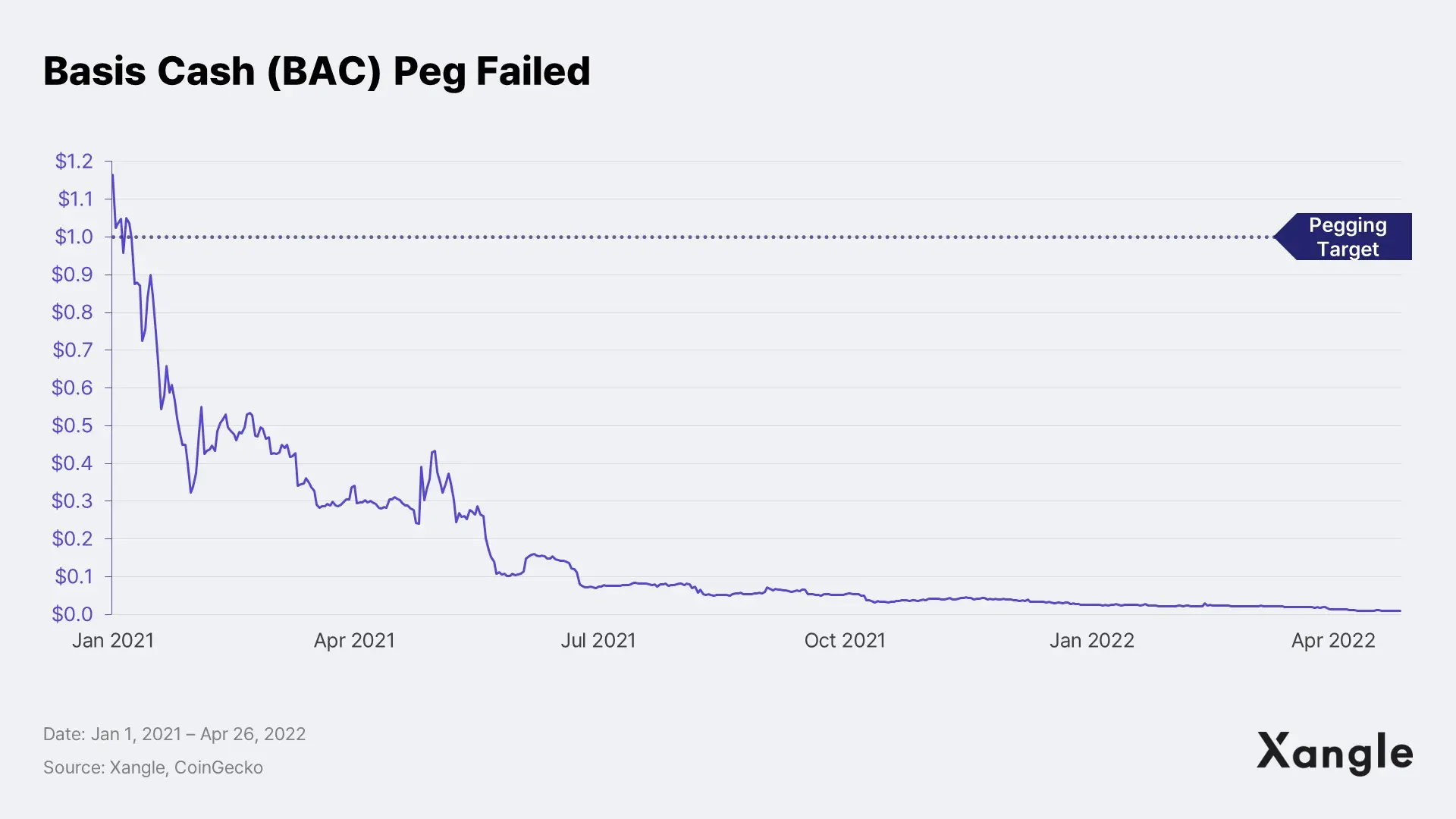

Since algo stablecoins are minted without any collateral, they can be supplied according to the market demand and have the advantage of strong capital efficiency and scalability (for adoption). However, numerous projects that tested the water with this model failed because of how challenging it is to secure initial liquidity and application. For example, Basis Cash (BAC) which was initiated from an idea that raised a considerable investment of $133 million from Bain Capital, Google, and a16z tried to maintain its $1 peg using the arbitrage trading with the bonds called the “Basis Bonds.” However, it ended in a failure as the price rapidly soared to over $400 upon launch and completely depegged. They were not successful in securing a sufficient scale of liquidity to absorb the market’s supply and demand in their early stage, and the fact that the application of the BAC stablecoins was limited to trading was as critical an issue as the failure of the design itself. The biggest risk algo stablecoins inherently carry, their stability, will be discussed in further detail in the later section.

2-4. Fractional Stablecoins

Fractional stablecoins, or mixed model stablecoins, use a mixture of tokenomics taken from crypto-collateralized stablecoins and algorithmic stablecoins. The collateralization ratio for their value is kept under 100%, and an algorithm backs the rest to maintain the peg. While usually categorized together with other algorithmic stablecoins, factional stablecoins differ in that they need to reach a specific level of collateralization in order to be able to issue any tokens. For example, LFG (Luna Foundation Guard) building up their Bitcoin reserve may look like they are taking the turn toward becoming a more mixed model of stablecoins. However, UST is not considered a fractional stablecoin since its minting is carried out only by burning LUNA and is not collateralized by any other assets. Their Bitcoin reserve is only used for non-LUNA arbitrage trading options and not as collateral for issuing UST.

The structure of fractional stablecoins varies from project to project. This article will discuss the following representative projects as examples: FRAX, FEI, and the recently launched USN.

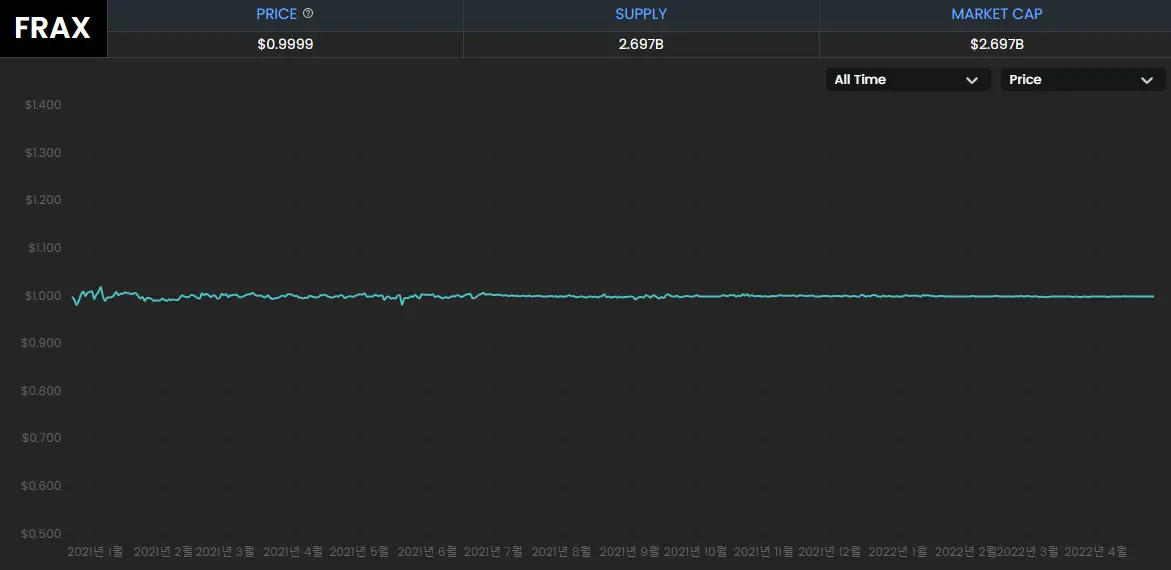

FRAX

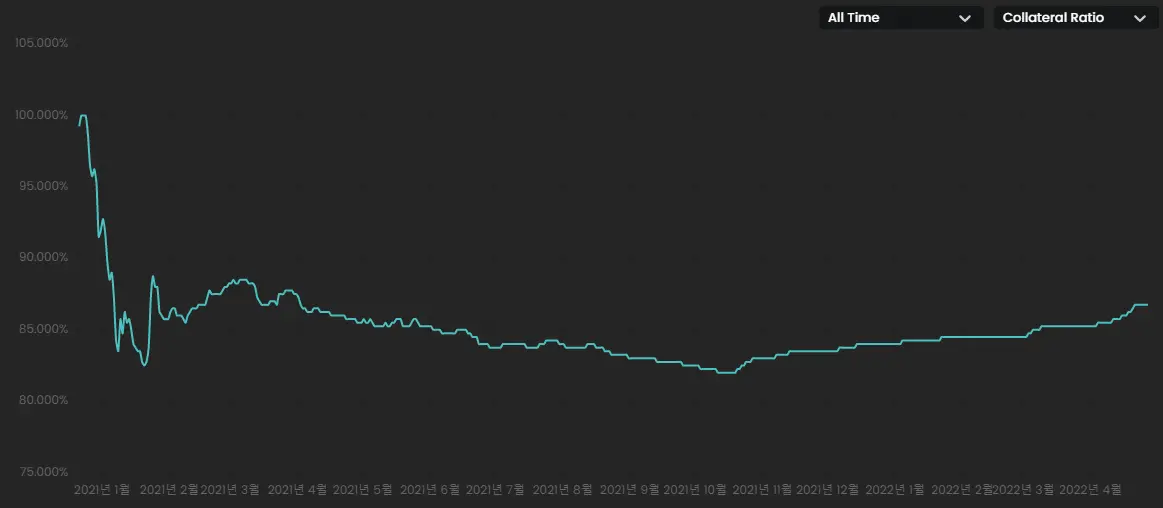

FRAX is a fractional algorithmic stablecoin based on USDC and its governance token, FXS. The project opted to mint FRAX with 100% collateralized in USDC at genesis and adjust the collateral ratio once every hour. If the price of FRAX rises above $1 with high market demand, the collateral ratio is lowered. If, conversely, the price of FRAX falls below $1 due to low market demand, the protocol increases the collateral ratio. For example, if the current collateral ratio is 85%, each FRAX can be minted with 0.85 USDC and $0.15 of FXS as collateral. In order to prevent the gap between each collateral ratio adjustment from growing too large, the protocol maximized capital efficiency and price stability using the mechanisms of buyback and recollateralization and the Algorithmic Market Operations Controller (AMO).* About one year and a half into its launch, FRAX is showing a strong performance by maintaining stable pegging to $1, having secured both stability and capital efficiency.

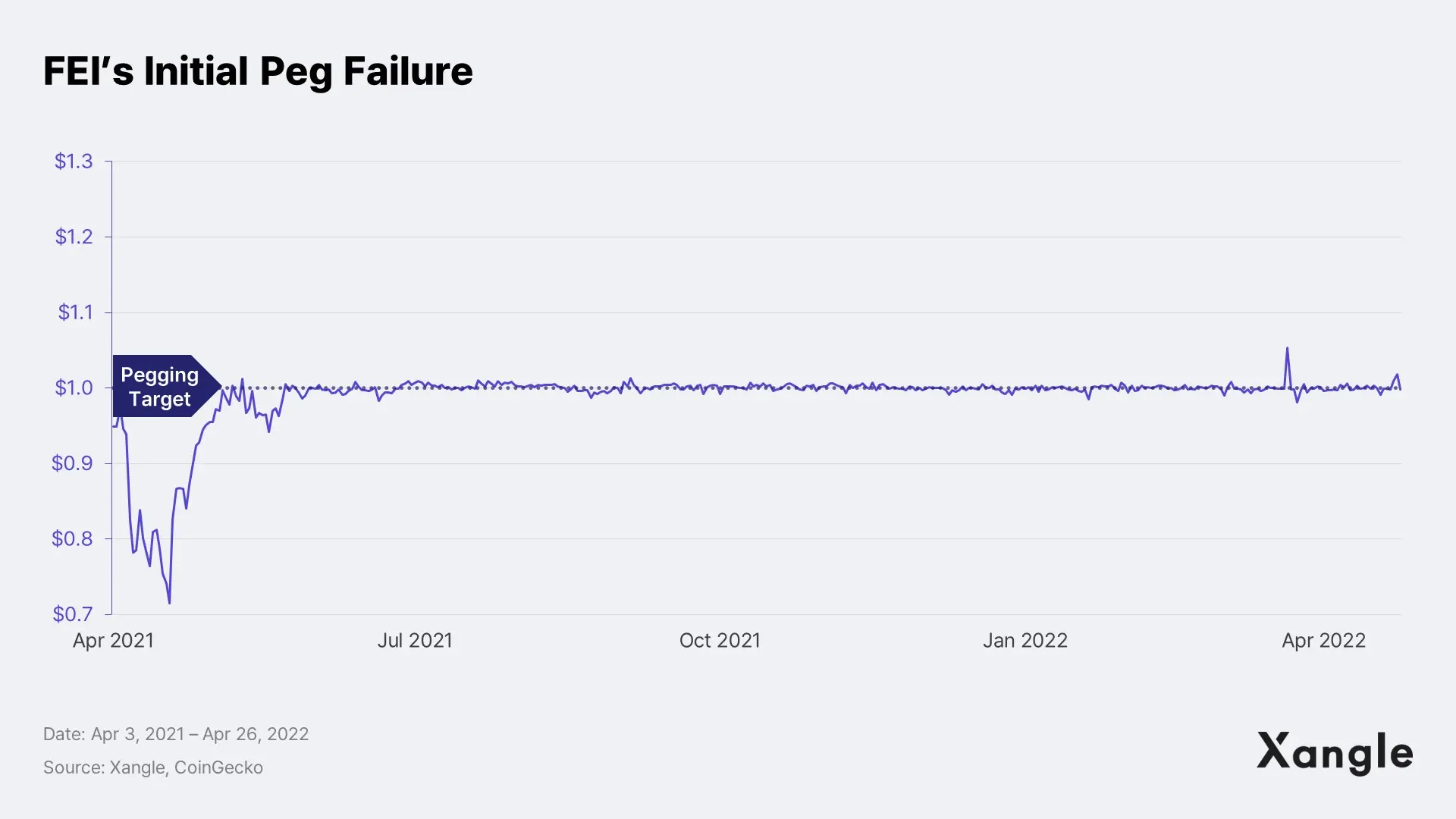

FEI

FEI is a stablecoin issued by Fei Protocol which founded the concept of “PCV” (Protocol Controlled Value). Although it is a fractional stablecoin much like FRAX, the big difference is that it aims to keep not less but a 100% or more collateral ratio. This model achieves relatively high capital efficiency compared to other crypto-backed stablecoins while securing more stability by maintaining a 100% or more collateral ratio. FEI’s treasury assets are purchased in their entirety by the protocol and used only for the below applications:

- Provided as liquidity for decentralized exchanges as collateral for stablecoin transactions

- FEI buys them back as treasury assets and burns them to maintain pegging

- Generates interest earnings with treasury assets and achieves excess gains

However, they experienced a serious failure to peg immediately upon their launch as a result of introducing the bonding curve* mechanism to bootstrap their initial treasury assets. At that time, Fei Protocol was set to sell FEI at a discounted price of below $1, but the higher-than-expected demand from participants drove up the price of FEI to the extent that they had to pay extra to purchase FEI. In response to this, the protocol minted more FEI than planned, causing participants who took a loss from such measures to dump their tokens in bulk and FEI losing its peg.

* The bonding curve is one of the methods to bootstrap initial liquidity where the price of the token is decided as per the curve of a preset function. The price drops when the demand is low, and the price rises when the demand is high. The price only moves in accordance with the curve of the function.

Fortunately, FEI overcame its initial volatility and has been maintaining its $1 peg since June 2021, with its policy changed to enable users to redeem FEI with treasury assets after the launch of v2 in December. The turbulent launch of FEI is a great example of how difficult it is to secure the initial liquidity for stablecoins, as well as what important role collaterals play as FEI returned to its peg despite their failed launch. Compared to FRAX, which kept its collateral ratio as low as 85% without any issues in its initial stage, FEI does fall a bit short. However, given that 75% of their collateral is in ETH, FEI can be considered to have secured more stable capital efficiency than other existing crypto-backed stablecoins.

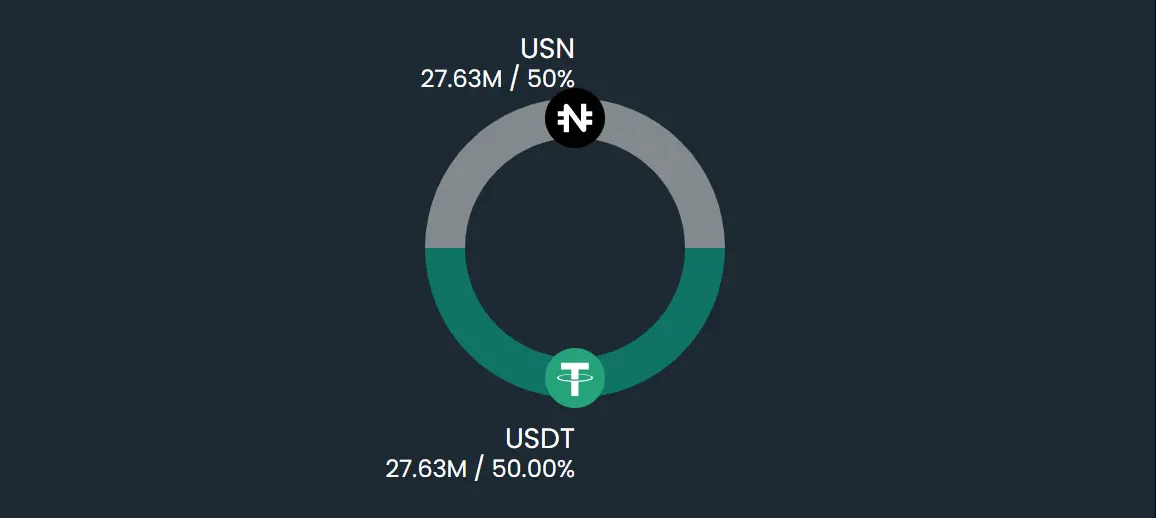

USN

USN, a stablecoin recently launched by NEAR protocol, also takes on the form of fractional stablecoin. While USN provides arbitrage trading opportunities with $1 NEAR, much like UST, the difference is that it is only issued with 100% collateral in NEAR and USDT reserves. Decentral Bank minting USN seeks to maintain the collateral ratio of 100% or above in order to ensure that they can buy back all the USN in circulation at any given time and continue to adjust the NEAR and USDT ratio within the reserve. Their need to maintain the collateral ratio at or above 100% makes them resemble FEI more than FRAX, raising questions as to whether they will be able to make a fast growth. However, it is definitely a positive sign that they now have secured their own alternative means to provide dollar liquidity to the NEAR ecosystem, which had been solely dependent on the Ethereum bridge for infusion of stablecoins.

3. Discussion on the Hot Potato: Algo Stablecoins

3-1. Are Algo Stablecoin Currencies?

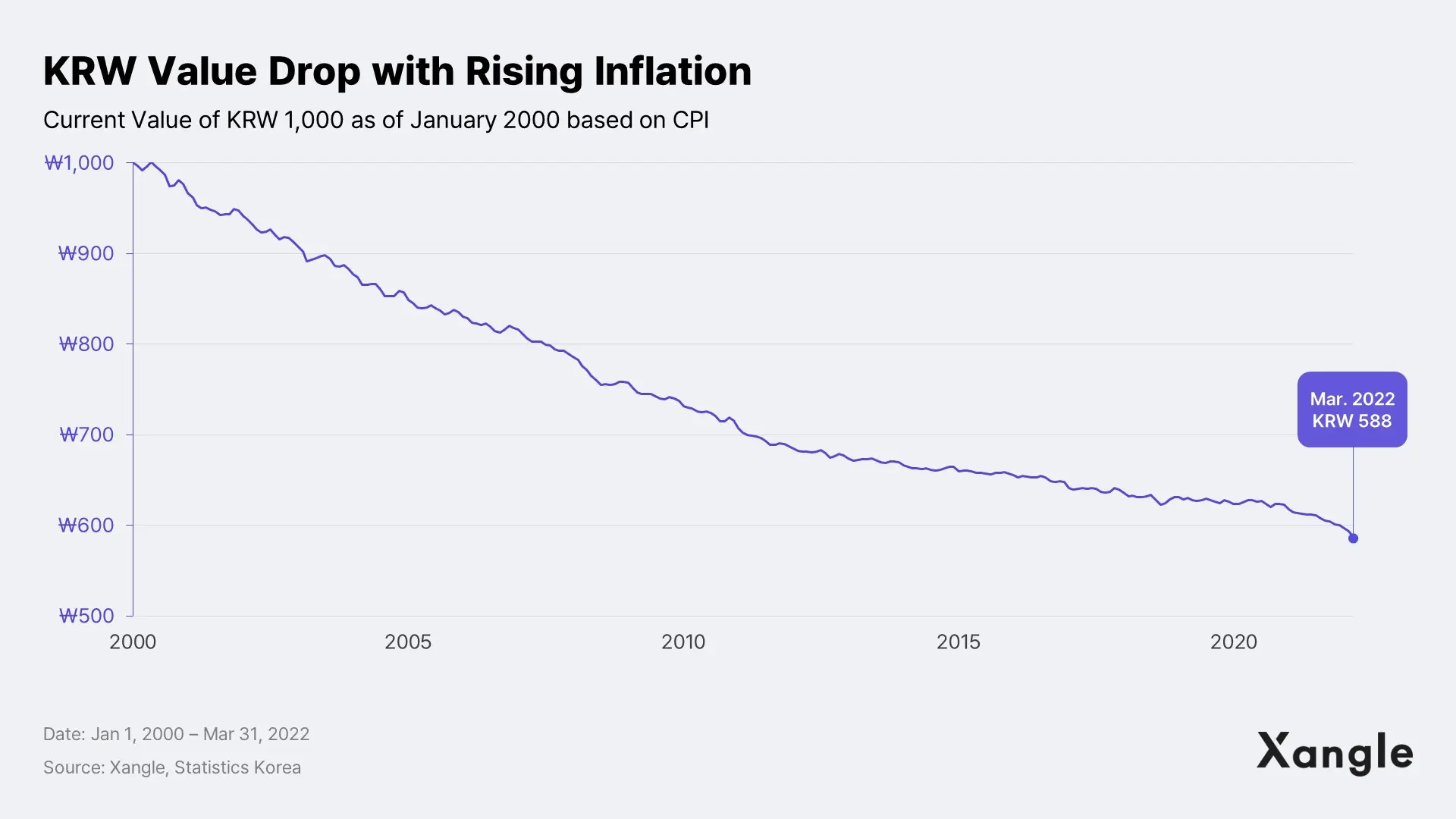

The discussion on algorithmic stablecoins, which hold no intrinsic value, is heating up even hotter with people butting heads as some criticize them as a complete fraud and others defend them as a breakthrough innovation. From the perspective of the algo stablecoin supporters, the fiat currency itself is not much different from the algorithmic stablecoins. The difference is that the fiat money is used based on trust that the government ensures its value, unlike algo stablecoins which maintain their value to $1 following the market principle. In the fifty years since the gold standard was abandoned in 1971, people have grown to use their fiat money, believing, without any doubt, that it holds its face value. For example, people would pay KRW 10,000 to a restaurant for their lunch, and such payment would be accepted because the restaurant owner believes that the KRW 10,000 note indeed is worth that much value. But is the government guarantee really an absolute? The examples we can find in history like Denarius of the Roman Empire, and Papiermark of the Weimar Republic support the claim that government-issued currency does not last forever and is determined by the market in the end. We do not even have to travel that far to such extreme examples. Just look at the Korean won and its value: you can see that what used to be KRW 1,000 in the year 2000 only holds a value of KRW 588 today due to rising inflation.

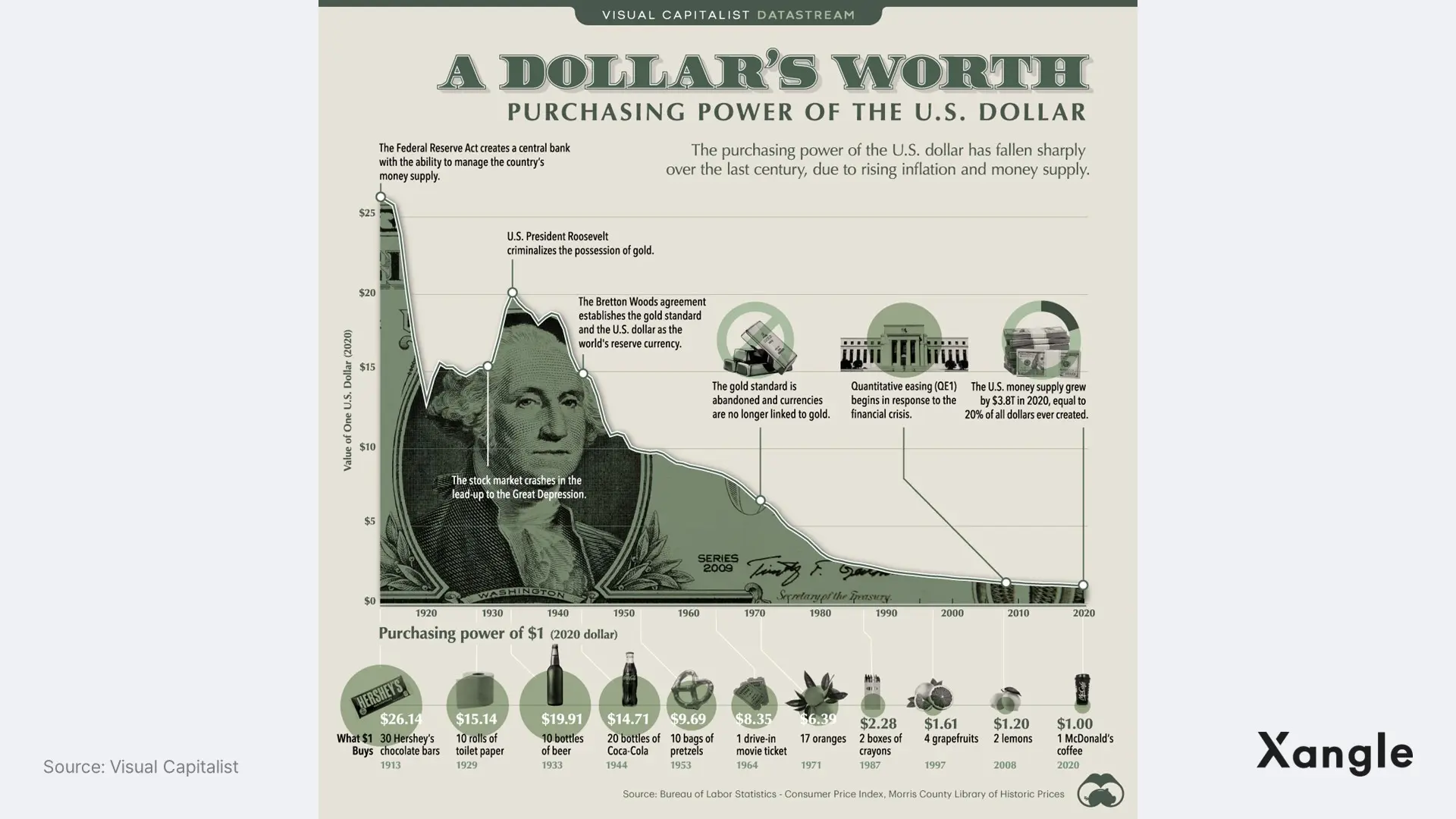

Article 48 of the Bank of Korea Act states that “The Bank of Korea notes issued by the Bank of Korea shall pass as legal tender current freely for all transactions.” However, such currency that can be passed for all transactions in Korea without any limitation has been continuing to lose its real value. This problem is not limited to Korean won either. The purchasing power of the U.S. dollar also dropped over 95% in the past 100 years due to rapid increase in its circulating volume. In this era of quantitative easing with the real value of fiat currency continues to fall, the argument criticizing the algorithmic stablecoins’ lack of intrinsic value may even be called illogical.

On the other hand, those against the algorithmic stablecoins point out that their $1 peg is nothing more than an illusion as algo stablecoins themselves are not currencies in essence, regardless of how the argument about the real value of fiat money turns out. Then, let us explore the three functions of money to find out the essential meaning of currency.

- Unit of Account

The measure of the value of goods and services - Medium of Exchange

Medium to exchange goods and services - Store of Value

Means to store economic value

Fiat money and algorithmic stablecoins both fulfill their roles as units of account and medium of exchange. What is controversial is whether algo stablecoins can serve as means to store value. Supporters of the algo stablecoins may claim that the fiat money also loses its purchasing power and, therefore, is not a means to store value. However, since algorithmic stablecoins do not have any assets held as collateral to ensure the intrinsic value, it is hard to say that they are means to store value. This is because algorithmic stablecoins are more of a synthetic asset following the value of $1 as set by the U.S. government than a currency that carries any intrinsic value of its own. In other words, whether the algorithmic stablecoins are a fraud depends on whether they are acknowledged as currency. For algorithmic stablecoins to go beyond being a mere synthetic asset and become a real currency in their own right, challenges as below need to be solved:

3-2. Challenges Algorithm Stablecoins Seek to Address

Despite many criticisms against algorithmic stablecoins, they have a clear and definite set of problems they seek to resolve, which are as below:

Supplying Dollar Liquidity that Meets Market Demand

As discussed earlier in the section “1-2. What Makes Stablecoins So Important?”, stablecoin supply volume is still relatively small compared to the total digital asset market. While the demand for stablecoins with a fixed value keeps increasing day by day as the bearish market continues and blockchain economy participants increase, it is difficult to issue the volume matching the actual market demand as stablecoins require collaterals. A low supply of stablecoins causes higher demand than supply, leading to capital inefficiency in the blockchain economy and, therefore, an increase in capital cost. Out of the need to achieve such an efficient blockchain economy, algorithmic stablecoins with flexible minting volume and capital efficiency were born.

Decentralization of Stablecoins

Stablecoins under the control of centralized authorities may be suspended from usage at any given time due to censorship. In fact, it is very much possible for the issuing authority of USDT and USDC to halt transactions or seize tokens from specific wallets. Also, there exists a single point of vulnerability where all the tokens issued by an issuer are put at risk in case an issuer of a stablecoin is attacked and breached. Although decentralized stablecoins backed by crypto assets as their collaterals, such as DAI and MIM, emerged to overcome such challenges, they are also still exposed to the risk of centralization as a significant portion of their collateral is also in USDC. Ironically, centralized stablecoins are widely used in the blockchain economy, where the users strive for a decentralized ecosystem. This is the reason Terra argues that “a decentralized blockchain economy requires a decentralized currency.”

3-3. Challenges Algorithm Stablecoins Must Resolve

However, even with these various advantages they offer, it is still hard to call algorithmic stablecoins a currency in its essence. The challenges algo stablecoins need to resolve are as follows:

Absence of Utility

Today, exchanging an algorithmic stablecoin for physical currency requires transactions with fiat-backed stablecoins such as USDT or USDC. Moreover, the range of their usage in exchanging goods and services in the real economy is also very limited. All in all, it is very difficult to use algo stablecoins like any other currency in the real world. It would be more plausible to consider algorithmic stablecoins as synthetic assets following $1 rather than a currency, with the scope of their main utility limited to arbitrage trading and interest farming. In this sense, the launch of the highly anticipated 4pool, a curve pool for UST-FRAX-USDT-USDC, is only a means to make it more convenient to make the exchange with fiat-backed stablecoins rather than adding more utility. Each of the protocols is also aware of such limitations. Frax Finance is planning to launch FraxSwap, their decentralized exchange using FRAX as the key currency, and FraxLend, their lending protocol. Fei Protocol is seeking to increase the scale of FEI loans based on its merger with Rari Capital, a lending protocol. While UST’s case is better off than others since it has established itself as the dominating stablecoin in the Cosmos ecosystem and transaction in UST is supported by large exchanges including Binance, the fact that over 60% of their supply still sits as a deposit in Anchor protocol is a potential risk.

Regulatory Uncertainty

Although it has been pointed out that algorithmic stablecoins must be utilized for the decentralization of stablecoins, we cannot leave out the possibility that a tight regulatory hold may be put in place. For example, what would happen if the U.S. government were to decide to designate USDC as a government-approved stablecoin minting authority and prohibit the exchange of USDC with other stablecoins? You may think that a DeFi protocol that is decentralized cannot be regulated by a government. However, if you recall how over 100 synthetic assets were delisted by Uniswap after the SEC chair stated that synthetic assets show the characteristics of securities last June, we cannot rule out the potential for tightening of such censorship once the regulations are actually put in place. Also, though very slight, the possibility does exist that Circle, the USDC issuer, may blacklist smart contracts and wallets providing liquidity as a pair with USDC. If such regulations were to come in effect, given that most of the algo stablecoins are currently highly dependent on Curve Finance and Uniswap V3 Stableswap for exchange to fiat-backed stablecoins, algorithmic stablecoins’ market share is likely to show a drastic decline.

4. CBDC and Regulations on Stablecoins

4-1. Current Policies in Different Countries

Will government-led CBDC (Central Bank Digital Currency) and private-led stablecoins co-exist in the battle to seize the digital currency dominance? The status of CBDC adoption and regulations will first need to be explored before getting further into this discussion.

The United States

While there has not been any bipartisan agreement reached in the U.S., which will hold direct sway over the most widely used dollar stablecoins, the Biden administration is making clear their intentions to bring crypto-assets into their existing regulatory regime over a series of steps.

- They emphasized the need for oversight, although they do not have any plans to ban stablecoins.

- They want stablecoin issuers to be insured to become depository institutions for physical dollars.

- They called for legislation stating open standards on compliance with restrictions on commercial entity affiliation and promotion of interoperability. In other words, they want a rule under a standardized regulation where stablecoins can be circulated.

- Stablecoin issuers need to comply with rules and regulations under existing regulatory authorities such as SEC until any specific legislation is established.

According to what the U.S. government has announced so far, it seems that they are leaning toward bringing in private stablecoins into the existing financial system rather than issuing CBDC themselves. Even if the U.S. were to issue CBDC, they would likely opt for the wholesale model with the money flowing from government to institutions, then onto the individuals, over a direct distribution from the government to individuals.

China

On the other hand, the Chinese government, which sent a shockwave through the market by prohibiting all and any crypto assets trading last year, is blatantly expressing its intentions to issue CBDC exclusively and to further control individuals based on such issuance. Chinese CBDC wallet holder count is already exceeding 130 million; the government has strong capabilities as well as willpower; and the Chinese domestic market is sizable. All of these come together as a perfect recipe to make China one of the very few countries that could successfully issue a centralized CBDC. Even with China being positioned as the factory to the entire world since the ‘90s, the Chinese government has been active in its effort to keep big American internet players from entering its market. The closed internet policy of the Chinese Communist Party, dubbed “Internet Sovereignty,” has a clear direction: The nation’s stability and unity are more important than the freedom of individuals. By issuing CBDC, the Chinese government seeks to achieve the goals below:

- Strengthen the government’s control by eliminating key crypto assets, the global competitor

- Take back control of capital flow from big tech players such as Alibaba and Tencent

- Break away from the U.S.-led international financial system

India

India has been at the forefront of the government-led digital payment race for the past decade, though much of the Korean public might not be aware. With the real-time mobile banking transfer enabled via an open standard called UPI (Universal Payment Interface) and the government restricting the market share held by big institutions, India has become the best practice case in digital payment regulation for the emerging economy. However, such remarkable achievements by the Indian government are put to the test due to the sudden and rapid rise of crypto assets and stablecoins. Unlike China, whose concern centers around weakened control over the individuals, India’s biggest concern is the usage of stablecoins potentially leading to the dollarization of the Indian economy and weakening of the Indian rupee. If privately issued stablecoins were to penetrate the market, it is evident that the government-led currency policy would have less influence over the economy overall. However, the issuance of CBDC is not something that can be easily decided given the impact it wields over the economy overall. It is precisely for this reason that the Indian government keeps making sharp turns left and right when it comes to its position on the topic of crypto assets.

European Union (EU)

The European countries will be regulating crypto assets in their jurisdiction on a state level until the MiCA (Markets in Crypto-Assets) regulation, a proposal to regulate crypto assets on an EU level, comes into force in 2024. Although the proposal the EU seeks to introduce is on the firmer side, including a mandatory prior asset of 2 – 3% to be secured and the crypto assets exceeding a certain level being required to comply with the regulations, the overall direction it takes is not negative. Regarding CBDC, the ECB (European Central Bank) continues to mention its drive toward the digital Euro but is maintaining a very cautious stance on its potential effects and risks. EU would have to take a more cautious approach to the matters concerning CBDC issuance since they are already using a unified currency without fiscal integration.

4-2. Potential CBDC Implications for Stablecoins

With most of the stablecoins in the market following the U.S. dollar, whether the U.S. government will impose any regulations is the most important factor in all this. Considering that the U.S. is leaning toward opting for private stablecoins issued under the government regulation, there is a good possibility that the stablecoins like USDC and BUSD that actively comply with the current regulations will survive. The recent news about the big financial players, including BlackRock and Fidelity, having made a $400 million funding for Circle, the issuer of USDC is putting more weight behind the speculation that the government will support private institutions issuing stablecoins. However, a few select stablecoins being officially approved to mint does not necessarily mean that there will be no regulatory implications for crypto-backed or algorithmic stablecoins as well. We will have to wait and see how things turn out on this front.

On the other hand, before long, all the emerging economies will find themselves stuck in a dilemma between CBDC issuance and stablecoin regulations as their sovereignty of currency hangs in the balance. However, if the current trend were to continue, it is not very likely that major countries will put a blanket ban on all crypto assets like China, but highly likely that the CBDCs will be issued based on private blockchains operated by a small number of nodes. Therefore, emerging economies’ issuance of their own CBDC is expected to have a very limited impact on dollar stablecoins traded on public blockchains.

5. Conclusions

5-1. New Experiments

Before this article comes to its closure, let us briefly introduce a few groups of stablecoins not addressed in the section “2. Different Types of Stablecoins” but are worth noting.

Forex Stablecoins: Synthetix, FixedForex, Angle, and Terra

Forex or foreign exchange stablecoins refer to stablecoins pegged to a fiat currency other than the U.S. dollar. They are issued on different protocols as below:

- Synthetix (e.g., sAUD, sGBP, sCHF) – Read more

They may issue stablecoin synthetic assets backed by their native token, SNX, and require a high collateral ratio of 400% or more. - FixedForex (e.g., ibEUR, ibJPY, ibKRW) – Read more

A synthetic asset issued against collateral much like Synthetix. However, by utilizing the lending protocol, IronBank, various collateral assets can be used, and the collateral ratio differs by collateral assets. The collateral ratio of each collateral asset is determined by an algorithm based on the said asset’s historical volatility. - Angle (agEUR) – Read more

Currently, only agEUR can be issued with ETH and USD stablecoins backing as collateral. Its main difference from the two protocols mentioned above is that the volatility is eased via entities called Hedging Agents and SLP (Standard Liquidity Providers), ensuring the collateral ratio does not exceed 100%. - Terra (e.g., KRT, SDT, THT) – Read more

Same as UST, these stablecoins can be issued in various currencies, such as Korean won, Singapore dollar, and Thai Baht, by burning LUNA, traded for arbitrage, and also be used to pay Terra blockchain transaction fees.

Stablecoin Backed by a Delta-Neutral Position: UXD – Read more

UXD, a Solana-based stablecoin, is issued with a delta-neutral position of a decentralized exchange for futures. For example, a user deposits $1 worth of SOL to UXD protocol and receives 1 UXD. Then, the protocol takes a short position in the decentralized futures exchange like the Mango Markets with that $1 SOL as the collateral. By taking long spot and short future, the protocol creates a position that will back $1 SOL for 1 UXD no matter how the price of SOL changes. In theory, this will solve the trilemma of stablecoins, ensuring that it is decentralized, capital efficient, and stable. However, it is not without limitations:

- Size of Decentralized Futures Market

As of March 2022, the total open interest of Solana-based futures DEX is about $30 million, which would place a ceiling on the total UXD supply. - Funding Rate Risk

A funding rate refers to a type of payment imposed on certain positions to minimize the difference between the future and spot prices. In general, the funding rates are positive (imposed on long positions). However, in case of funding rates turn negative, UXD protocol holding a short position will have to pay the funding, leading to a shortage of collateral.

Credit-based Stablecoin: BEAN – Read more

BEAN, claiming to be a credit-based decentralized stablecoin, maintains its $1 peg with no collateral but only the “Silo,” or the liquidity provider, and “Pods,” which hold attributes of debts. When the price of Beans drops below $1, the protocol sells Pods with which Beans can be bought at a discounted price and buys back the Beans with assets received to be burned to restore the pegging. Conversely, when the price of Beans rises above $1, new Beans are minted and distributed to the Silo members and Pod owners in a 50:50 ratio. The unique feature of this mechanism is that it pays rewards for liquidity provision and redeems debts only by the increase of supply, unlike other protocols that pay interests or redeem debts with the flow of time. Although the protocol recently experienced a painful event where its governance was robbed of all the assets in deposit with them by a flash-loan exploit, this was not a failure on the part of BEAN’s pegging mechanism itself. After a long discussion within DAO, they have decided to reboot the protocol in early May. It is definitely worth keeping an eye on whether they will be able to rise from the ashes.

Inflation-Pegged Stablecoin: FPI and VOLT

An inflation-pegged or inflation-resistant stablecoin is a relatively new concept that came about in response to heightened concerns about inflation, and refers to a stablecoin that follows the U.S. Consumer Price Index (CPI) rather than $1. Stablecoins are issued in different protocols as below:

- FPI – Read more

FPI*, an inflation-pegged stablecoin on Frax Finance, is issued based on FRAX, and its pegging target is adjusted every month according to the Chainlink’s CPI oracle. Much like FRAX, FPI maintains its peg in the form of a fractional stablecoin, and the increase in price as per the inflation is collateralized with the protocol’s yield. If the protocol’s yield falls short of the inflation, the new FPIS, the governance token, will be minted and sold into the market to maintain the collateral ratio. - VOLT – Read more

VOLT, an inflation-pegged stablecoin issued by Fei Protocol, also uses Chainlink’s CPI oracle to reset the pegging target every month but with the following difference. For one thing, unlike FPI minted against FRAX as the main collateral, VOLT does not use FEI as the main collateral for issuance. Secondly, while FPI aims to maintain partial collateralization and keep the collateral ratio under 100%, VOLT aims to maintain over-collateralization and keep its collateral ratio at or over 100%

5-2. What Should Be the Next Steps for Stablecoins?

This article explored a wide range of different types of stablecoins, from fiat-backed to inflation-resistant stablecoins. Who can tell which one of these will take the throne of stablecoins? One thing is for sure: A decentralized economy requires decentralized currency. As of right now, no one knows whether the answer for that prayer would be an algorithmic stablecoin, a fractional stablecoin, or even a brand-new type of stablecoin yet to come. However, everyone would agree that the crypto world needs a decentralized key currency with low volatility in its value.

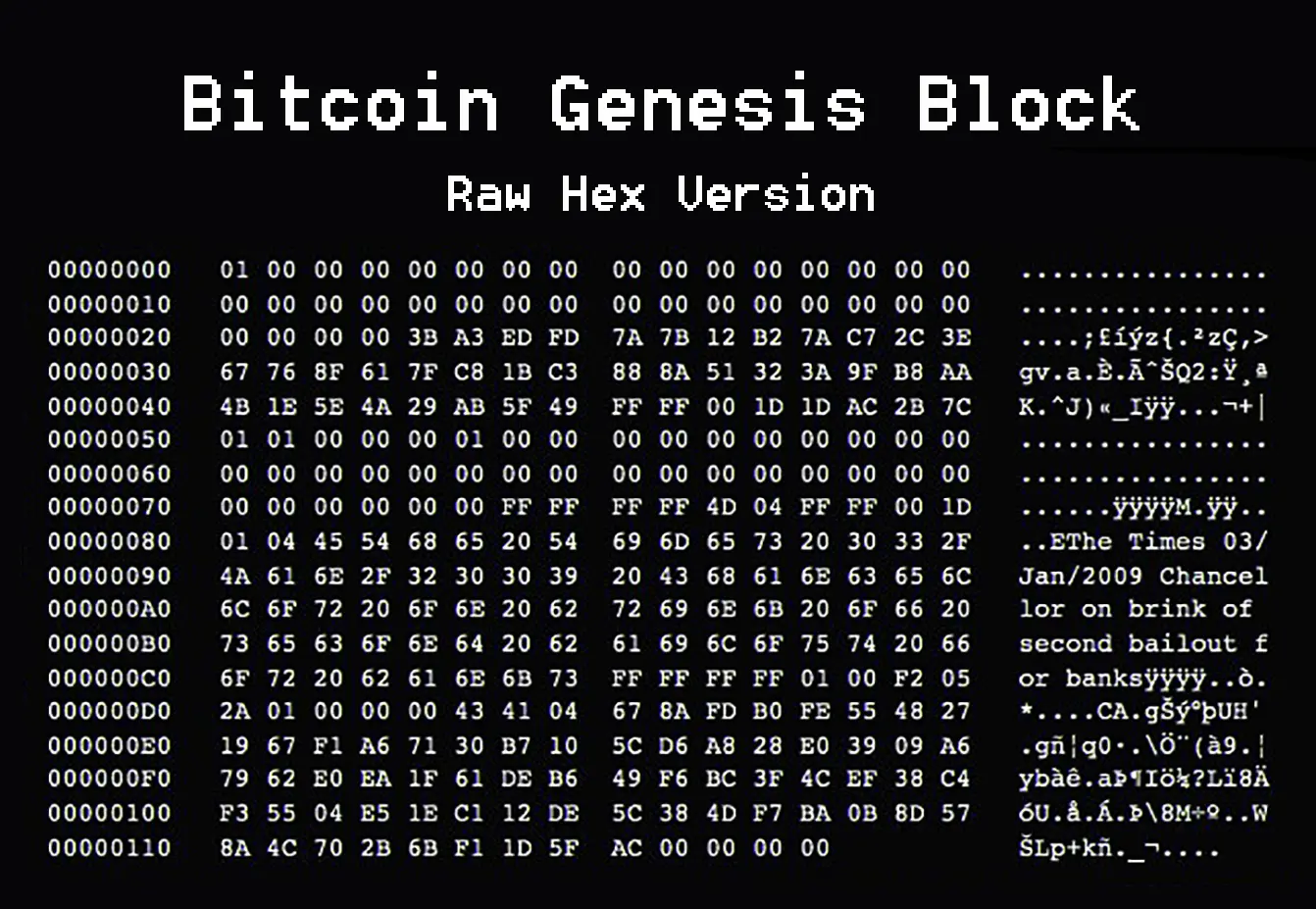

In January 2009, Satoshi Nakamoto wrote into the Bitcoin’s genesis block a headline from a British newspaper, The Times, which reads, “Chancellor on Brink of Second Bailout for Banks.” The historical and the very first block of Bitcoin is engraved with Satoshi’s antipathy and mockery of the existing financial system. Bitcoin, which laid the foundation for the blockchain economy, and even the decentralized finance (DeFi), made its start based on the resistance against the existing financial system and the currency policy. However, the fiat-backed stablecoins taking up over 80% of the market share today are not only issued by the centralized authority under government control but are also effectively entirely under the influence of the U.S. currency policy since they follow the value of the U.S. dollar. It is difficult to imagine USDC, fully supported and trusted by the market, would ever step down from the throne of dollar stablecoins. However, the dollar stablecoins might not be the only ones with a legitimate claim to this throne. Since people continue to pursue various innovative experiments such as inflation-pegged stablecoins, we can hold on to the ideological dream and look forward to one day welcoming the coronation of an independent key currency that is enabled solely on the blockchain.

[References]

Stablecoins in Unstable Times, Reflection Digital

Algorithm Stablecoin – The Holy Grail of next generation DeFi, HashKey Capital

What Keeps Stablecoins Stable, Richard K. Lyons & Ganesh Viswanath-Natraj

An Overview of Stablecoins, Multicoin Capital

Solving the Stablecoin Trilemma, Multicoin Capital

Stablecoins Are in a War for Dominance and It’s Getting Ugly, Vice

Beanstalk vs. Every Other Stablecoin

How Stablecoins Can Help Crypto Investors, and Why the U.S. Government Has Taken Notice, NextAdvisor

Inflation-Resistant Stablecoins: CPI coins, FPI & Volt, The Mothership

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.