[Xangle Valuation Series] ② Ethereum and Layer 1

[Xangle Originals]

By Jehn, Ponyo, Crypto_Gang. CHObiden, TraceØ, Do Dive

Translated by elcreto

Determining the Value of Digital Assets in an Era When Crypto Became Much More than Just Bitcoin

by Jehn

Back in 2017, when the crypto craze had swept the whole country, even the least interested seemed aware of Bitcoin. The prices of most cryptocurrencies, however, started to halve from the beginning of the following year, putting a damper on the fervency. The crypto market was seemingly fizzling out like a short-lived meme. Yet again, contrary to what it looked like, the crypto ecosystem has stealthily but massively sprawled into many applications, including DeFi, NFT and P2E.

The Crypto market’s evolution and sprawling ecosystem since 2021 are marked by the following monumental changes: i) ‘revenue numbers’ began to arise from the ecosystem of each protocol with Ethereum being at the forefront and ii) the advent of layer-1 blockchains was followed by the development of layer-2 solutions, intensifying competition between protocols. All these point to the ample demand for the blockchain network and now is a good time to ponder how to better assess the value of each protocol.

Bitcoin, the so-called ‘digital gold,’ was followed by more scalable Ethereum where smart contracts run and layer-1 coins emerged with unique features even more versatile than Bitcoin. Disparate from the traditional assets, cryptocurrencies were shoved into a brand new asset class called “crypto,” leaving valuation methodologies to a constant discussion. In this context, let’s go over the perspectives and criteria that can constitute the valuation methodology for layer-1 coins, the building blocks of Web 3.0.

The Nature of Ethereum and Other Layer-1 Coins as Assets

The reasons Ethereum and other layer-1 coins exist and carry value vary, depending on the structure and nature of each network. Among them, this article will primarily focus on Ethereum in exploring various valuation methodologies and identifying a layer-1 coin to which each methodology can be applied.

Ethereum is the oldest layer-1 coin that has the largest ecosystem, occupying the second largest market capitalization (about 18% dominance) after Bitcoin. In the DeFi market, it not only represents more than 50% of the assets locked but is a test-bed for new applications, such as NFT and P2E. Moreover, since the consensus algorithm is increasingly transitioning from PoW (Proof of Work) to PoS (Proof of Stake), Ethereum is evolving again to feature even more diverse attributes of assets and, therefore, considered a fair representation of most layer-1 coins.

We based our estimation of the value of Ethereum on the following three definitions:

- Store of value

- Capital required to run the Web 3.0 network

- Securities of a technology company with strong growth potential

1. A Store of Value Equivalent to, or Replacing Bitcoin

Ethereum is the second oldest blockchain platform after Bitcoin with an unrivaled ecosystem. It has added scalability to Bitcoin, evolving to become the world’s leading computational platform. ETH, the digital currency native to Ethereum, is used as collateral not only on its own network, but also on other layer-1 networks. ETH is also the second most popular cryptocurrency after Bitcoin among investors in the traditional financial market, increasingly gaining grounds as a store of value.

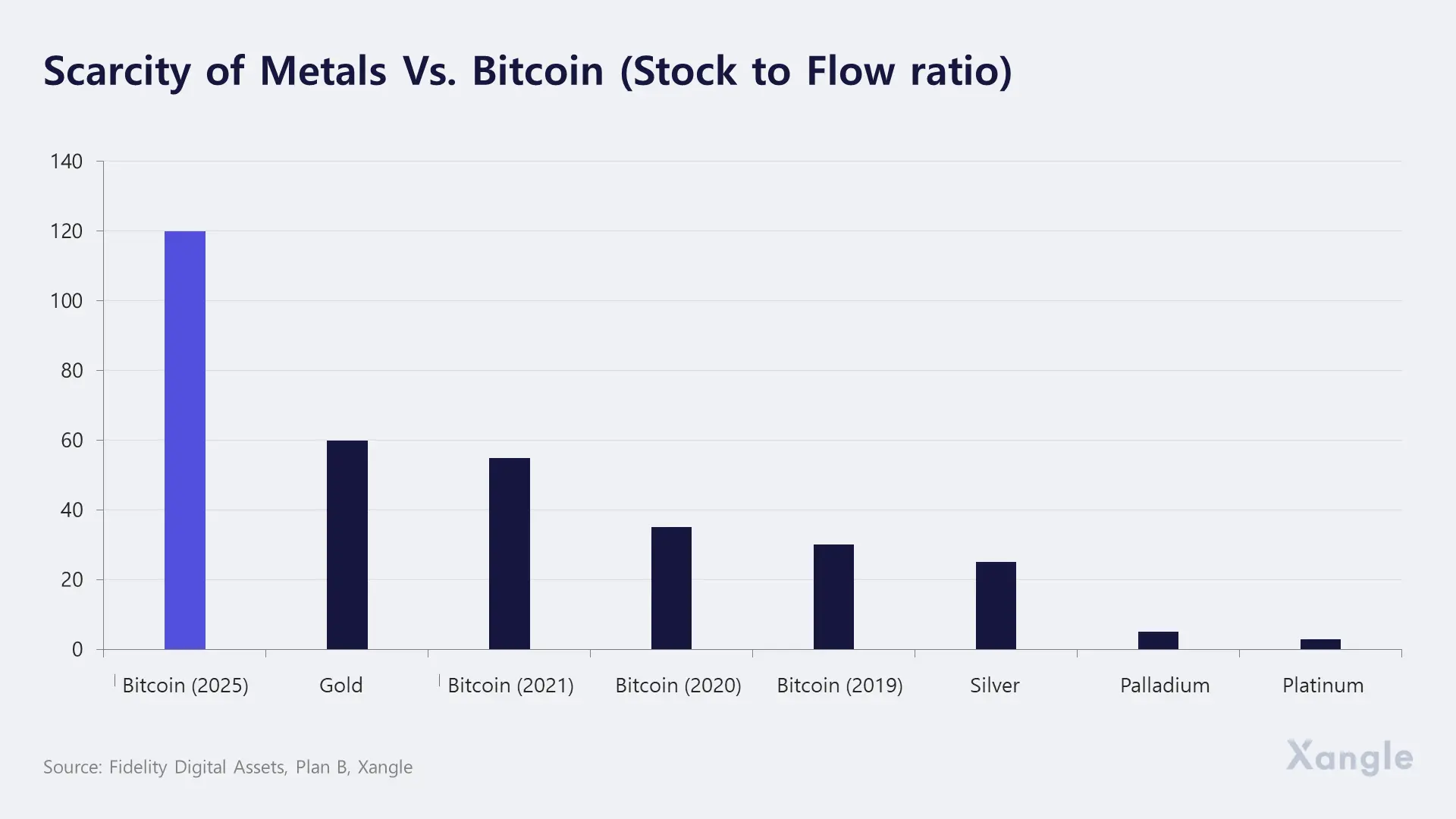

The Digital Silver

Bitcoin’s i) scarcity and ii) immutability have earned it the title 'digital gold.' The most widely known model for predicting the price of digital gold is PlanB's stock-to-flow (S2F) model.

Crypto analyst PlanB once said that the S2F model did not go well with Ethereum because the supply of Ethereum had not been fixed, and its value was determined by usability instead of scarcity. Considering that Ethereum has been spending part of its network fees to burn ETH since EIP-1559 was introduced in Aug last year, and assuming that a significant amount of tokens has been staked in the network since it switched to the Proof-of-Stake (PoS) consensus model, the circulating supply of ETH may shrink, possibly making the cryptocurrency scarce to some degree. In this sense, Ethereum can be viewed as 'digital silver' given 1) its scarcity and 2) wider application in the platform than Bitcoin. Just like the silver market, Ethereum has a smaller market and higher volatility compared to Bitcoin. As of Mar 19, 2022, Ethereum’s market cap ($0.35T) is about 25% of that of silver ($1.4T), seemingly suggesting an upside potential of quadruple growth.

Ethereum from a Portfolio Perspective

Bitcoin has been criticized for the large amount of electricity consumed for the PoW mining mechanism and subsequent environmental consequences. With the growing trend of higher ethical standards for corporate activities and broader attention to ESG (Environmental, Social, and Governance) management, some are entertaining the possibility that Ethereum, which has switched to PoS, may partially replace Bitcoin in the portfolios.

Assuming that global institutional investors include Bitcoin in their portfolio and allocate 0.5% of their global AUM (Assets Under Management) to Bitcoin, the tentative value of Bitcoin could reach as high as $130,000. If Ethereum manages to replace Bitcoin and rises from 45% to 60% of Bitcoin’s market cap, the value of Ethereum in the future will exceed $12,000, quadrupling its value—just like in the previous scenario.

2. Raw Material or Currency: Capital Required to Run the Web 3.0 Network

Paying network fees is a common utility for all layer-1 coins. Layer-1 coins serve as raw materials for the network as a smart contract needs to reward miners or validators on the blockchain.

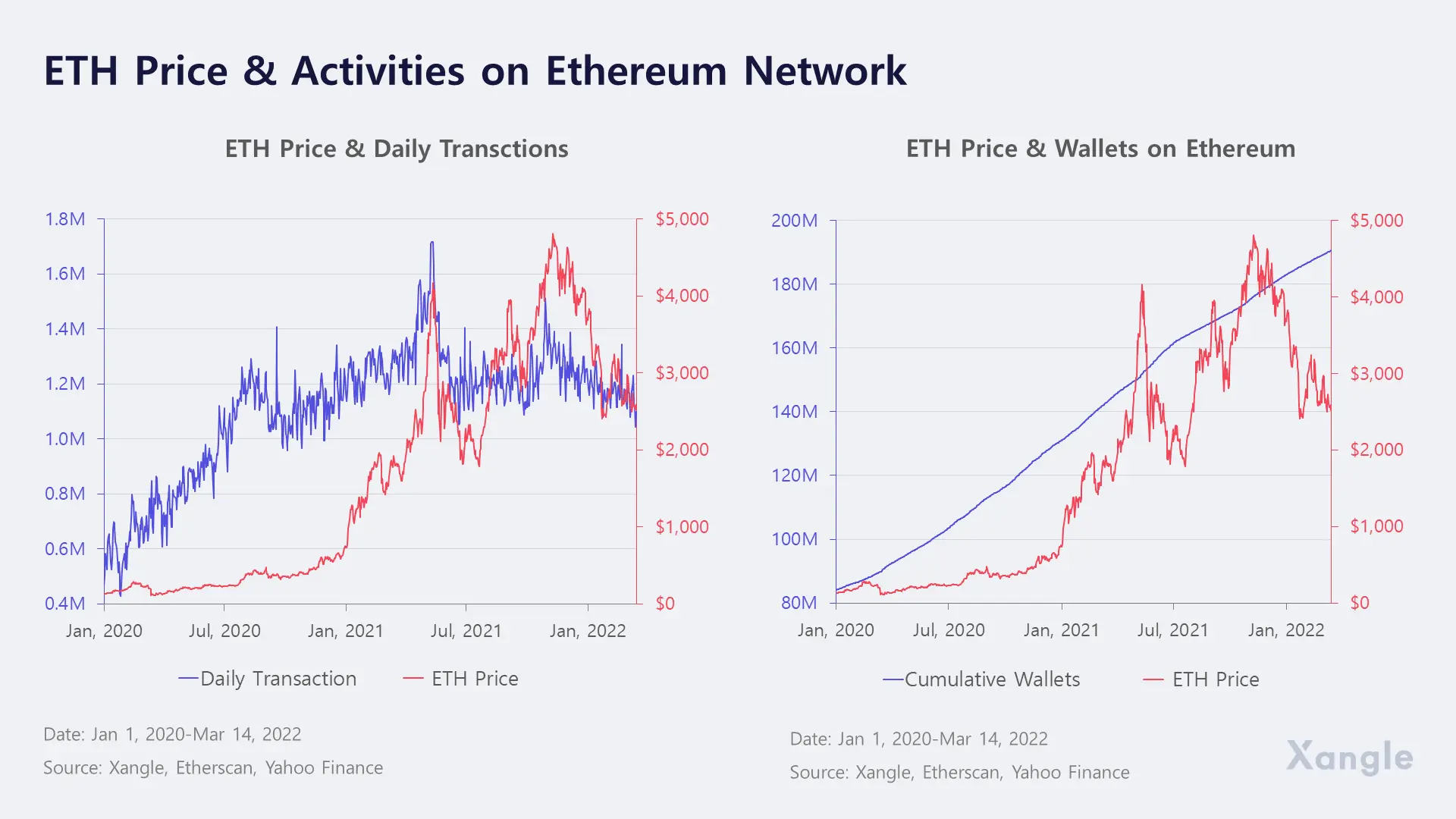

The term ‘gas fee’ on Ethereum, which is actually a network fee, illustrates that native coins are used as raw materials for the network operation. As such, we saw supply and demand for the network as the drivers of the value of the raw material for the network—ETH.

When compared side by side, there is a strong positive correlation between price and on-chain usage indicators, which directly affect the network’s economy. Already, various valuation models are being discussed to estimate the fair value of native cryptocurrencies.

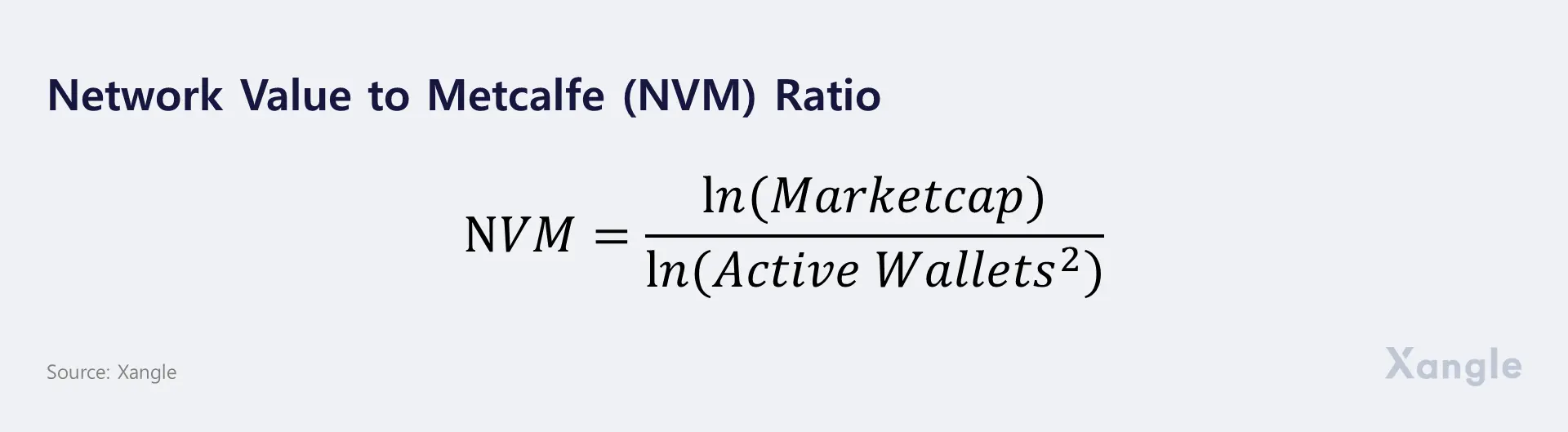

Network Value-to-Metcalfe Ratio

by Ponyo

NVM (Network Value to Metcalfe) ratio is based on Metcalfe's law, which states that a network's value is proportional to the square of the number of participants in the network. The concept—which was initially an attempt to quantify the network effect—became widely known after the law was proven in academic circles to be applicable to Internet networks like Tencent and Facebook.

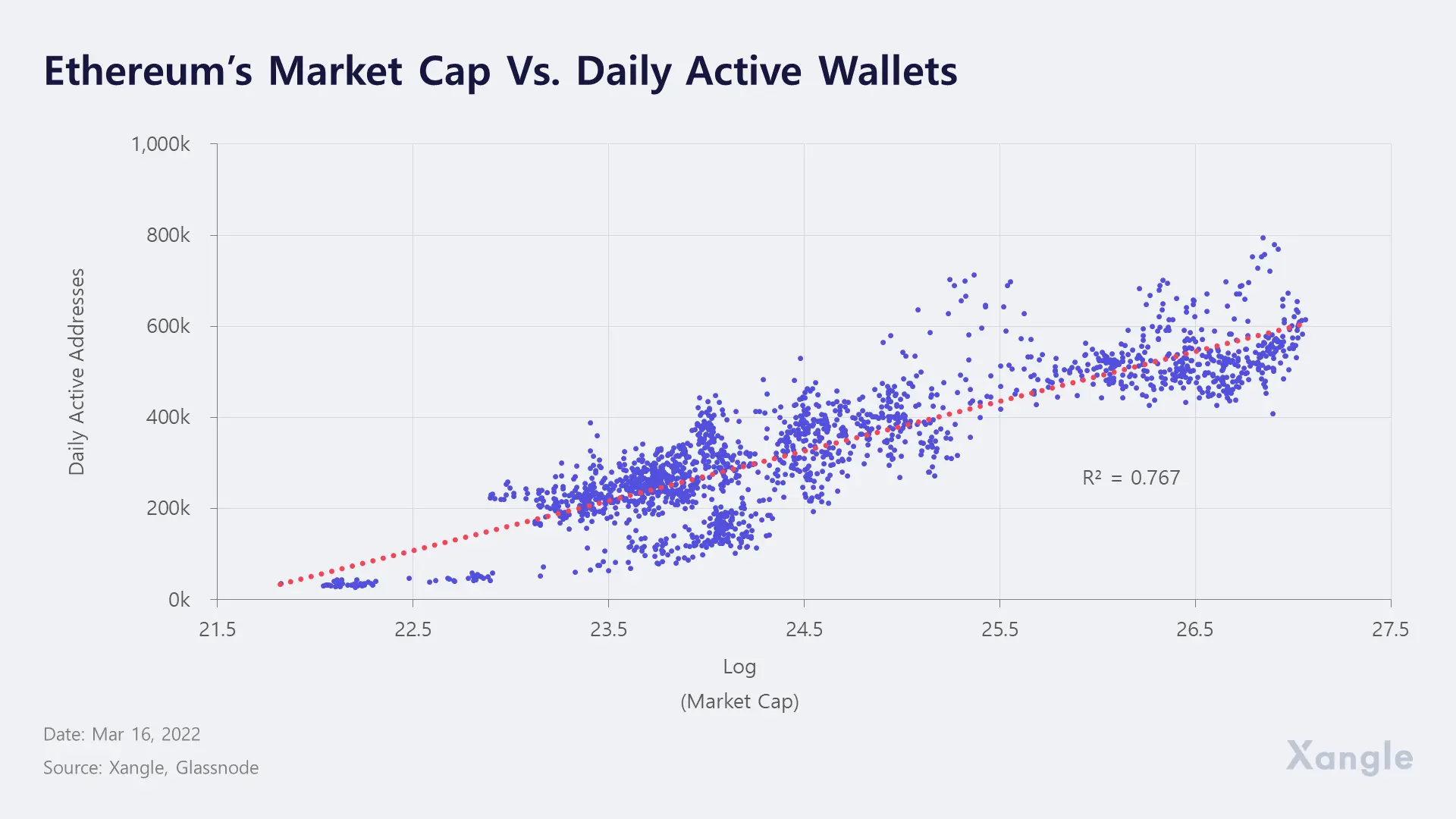

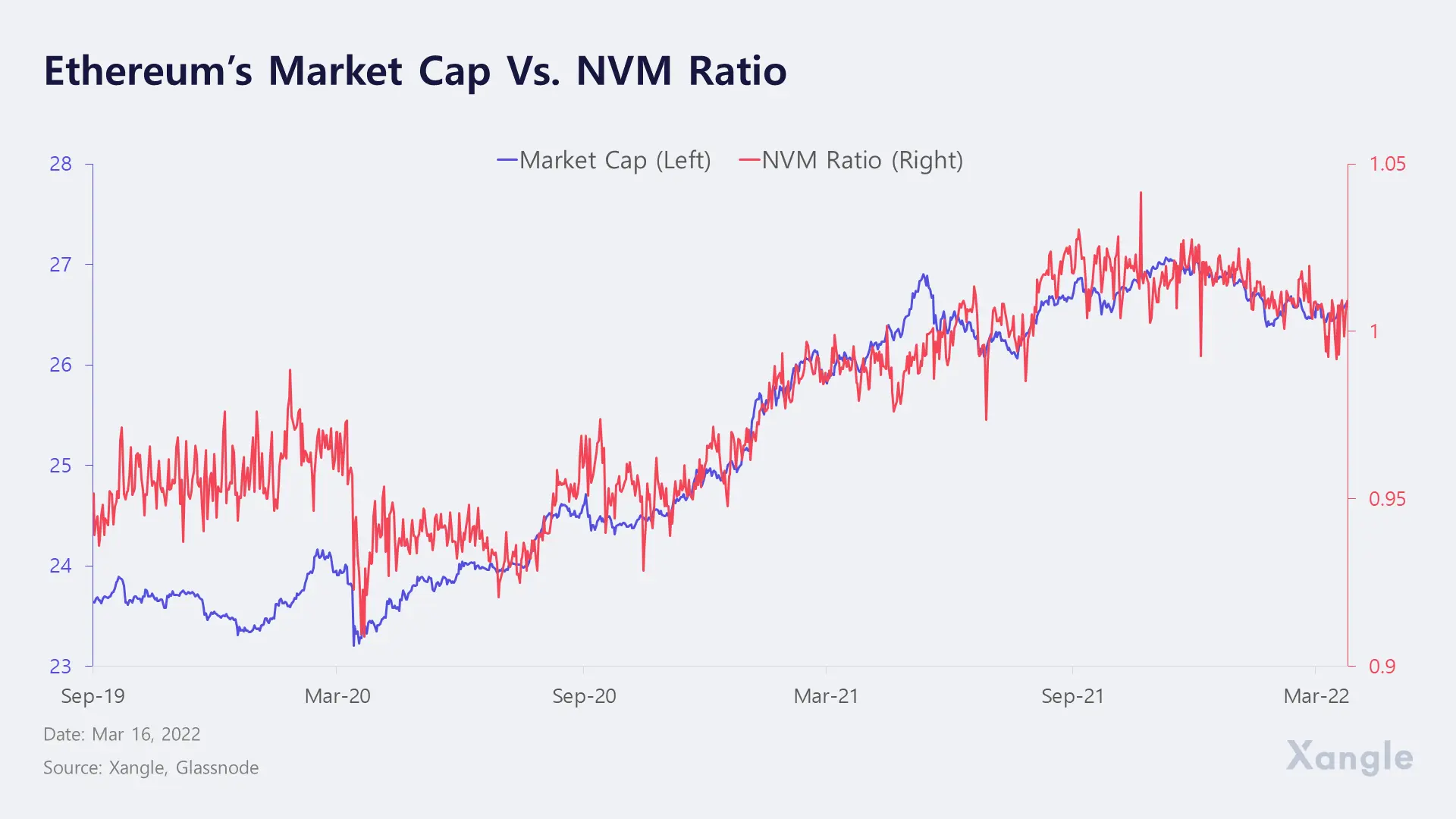

The NVM model sees the L1 blockchain as a network and estimates its value based on the number of active wallets, which is the number of participants. Considering that the correlation between Ethereum's market cap and the number of daily active wallets has been meaningfully strong over the past five years, NVM is considered a valid valuation methodology (See figure below).

The formula to find the NVM ratio is as follows:

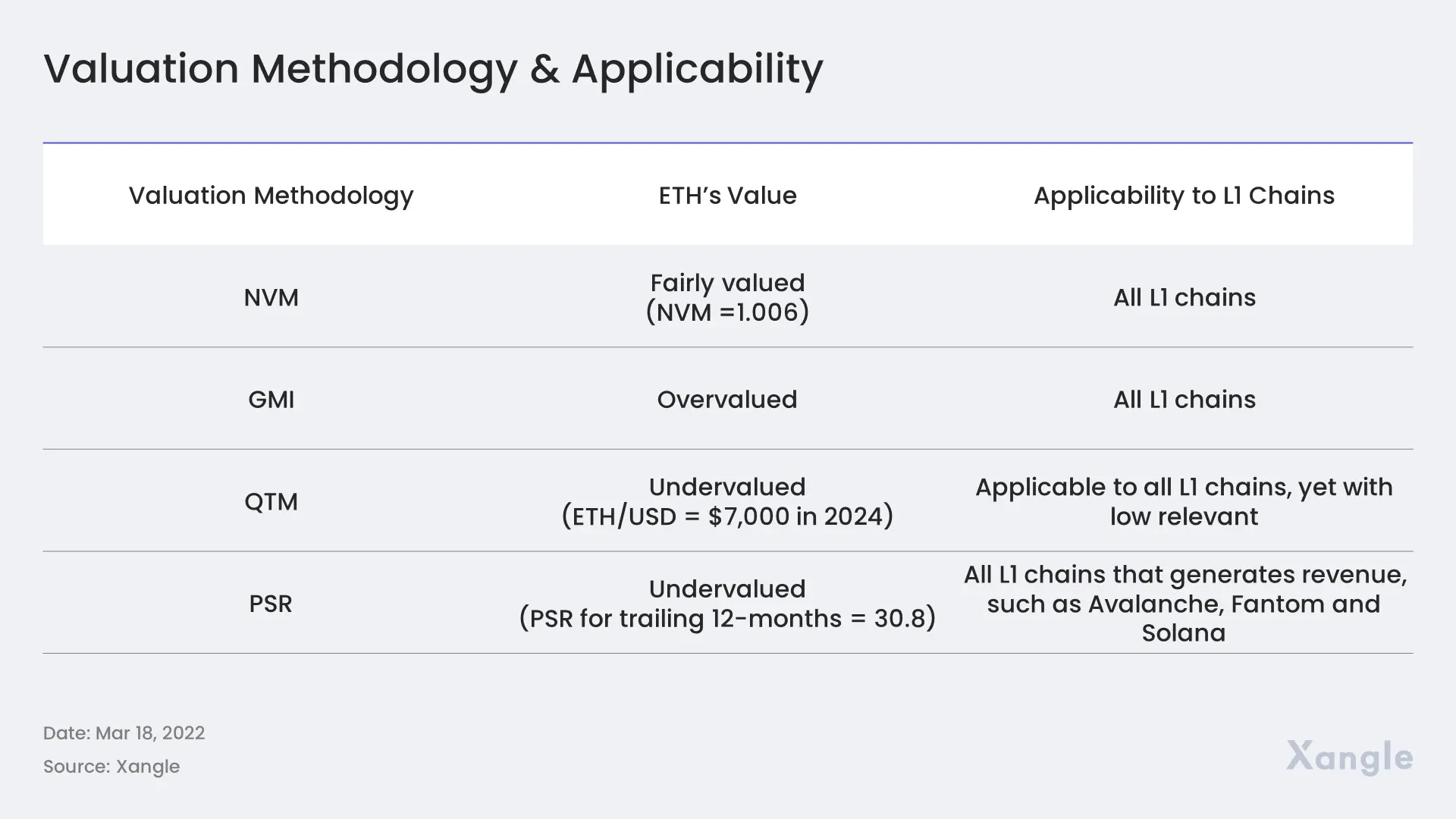

Theoretically, since the NVM ratio is obtained by dividing the network’s market cap by the network’s value defined by Metcalfe, 1 may be considered the basis to determine whether the L1 is overvalued or undervalued (higher than 1 = overvalued, 1 or lower = undervalued).

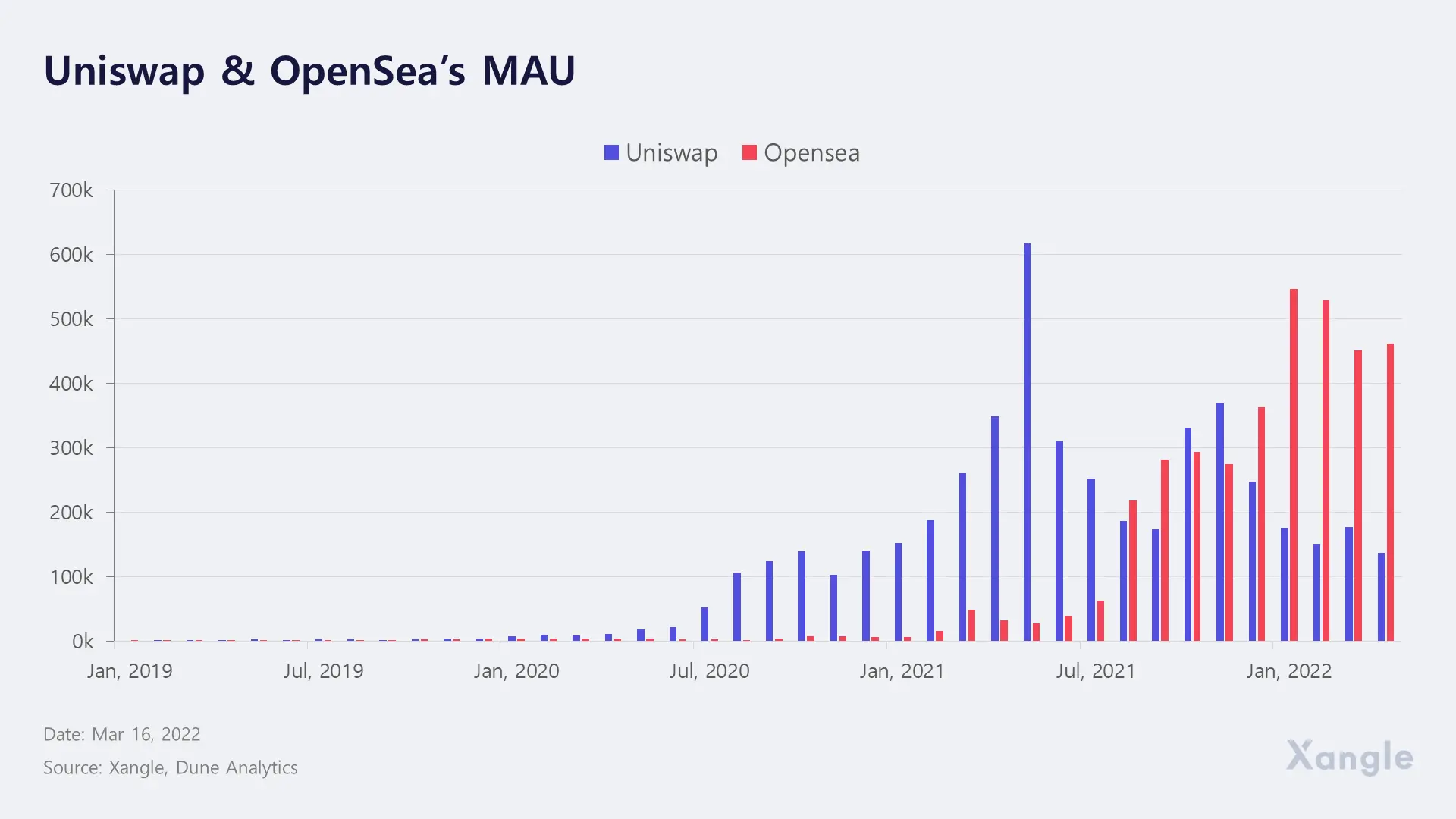

Starting in the summer of 2020, Ethereum’s NVM ratio started to rise, moving in tandem with its market cap. It is considered to be the result of a surge in active wallets upon the ‘DeFi summer’ and subsequent NFT craze. During that same period, the largest decentralized exchange Uniswap and NFT marketplace OpenSea saw a steep rise in the number of users. As of Mar 16, 2022, Ethereum’s NVM ratio stands at around 1.006, indicating that its market cap faithfully reflects the value of the network.

Again, such way of valuation became applicable to Ethereum because proof of the network’s value continued to rise as the network’s actual use cases and applications grew. Just like Facebook and Tencent, the network effect does also take place in the blockchain as a blockchain is a decentralized database managed by a peer-to-peer network.

The biggest advantage of the NVM ratio is its broad application to all L1 blockchains, such as BSC, Solana, Avalanche, and Phantom, not to mention Ethereum. Yet, the following should be considered before applying it: i) applying the ratio may be inappropriate for other L1 networks than Ethereum given that, unlike their high rate of growth, their ecosystems have just been activated only recently and that they do not have enough scales and ii) the calculation result may be inaccurate in some cases because the ratio uses the number of daily active wallets, which is highly volatile. Therefore, the outcome may be improved by incorporating 7-day, 30-day, or 1-year average daily active wallets as a variable in an attempt to partially offset the volatility.

GMI (Global Macro Investor) Network Value Model

by Crypto_Gang

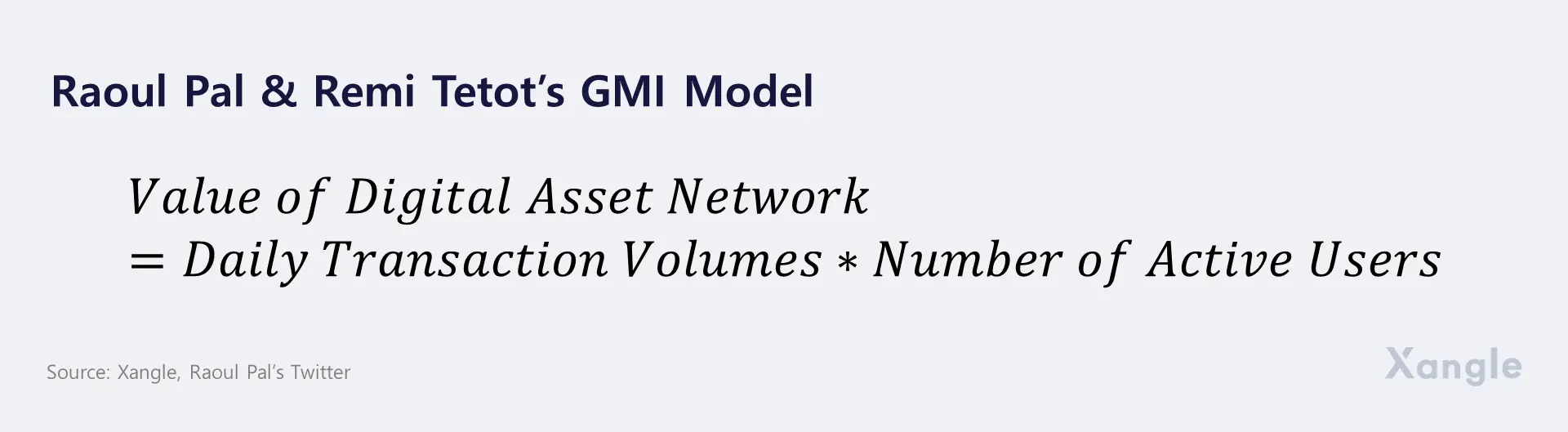

Some have proposed a new methodology to measure the value of a network, suggesting that Metcalfe’s law, although prominent, is difficult to apply in practice. Recently, Raoul Pal, the CEO of Real Vision and Global Macro Investor (GMI), and his founding partner Remi Tetot unveiled in their tweet their own valuation model, the GMI Model.

In their model, the value of a digital asset network is measured by multiplying the daily trading volume by the number of active users. They claim that their model can approximate the network value.

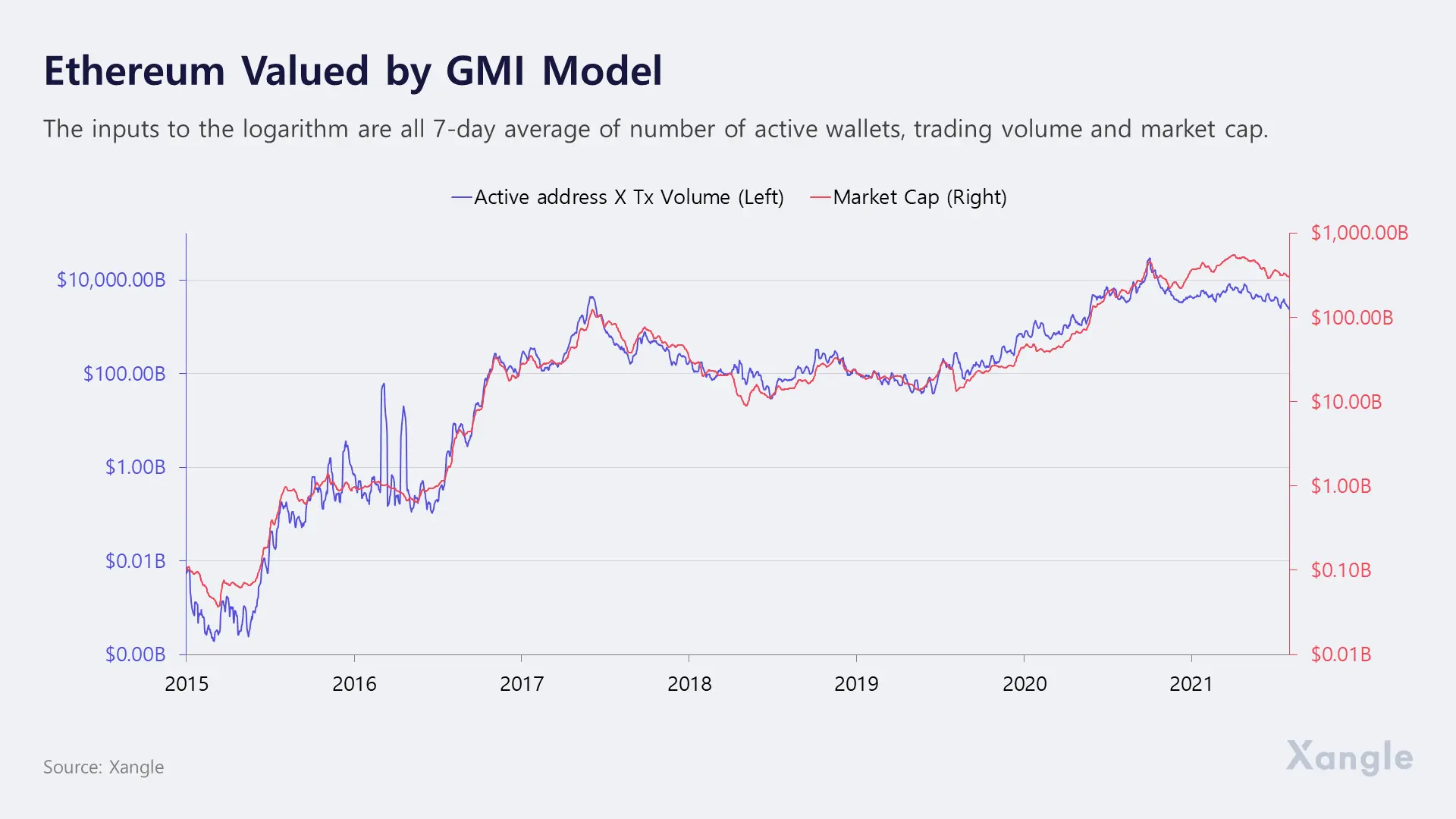

Although the specifics of the model’s methodology have yet to be disclosed, the result calculated based on GMI's model appears to be convincing to some extent. The graph Raoul Pal presented on Twitter shows a strong correlation between the market cap and network value.

A chart drawn up based on the GMI Model exhibited a strong coupling between Ethereum’s market cap and network value until 2020. Since 2021, however, they started to decouple as Ethereum’s market cap has been valued at a higher price than its network value, implying that the model would deem Ethereum as overvalued.

Yet, the GMI Model seems to require further verification. While it estimates the value of a network using the numbers of on-chain transactions and active users, it—just like the NVM ratio—lacks more specific assumptions that would reflect distinctive attributes of each ecosystem. For example, Raoul Pal has not yet specified how he would assess the value of Ethereum when the Layer 2 solution is considered. Therefore, making GMI’s model more sophisticated requires consideration of how to reflect the distinctive characteristics of each Layer-1 coin.

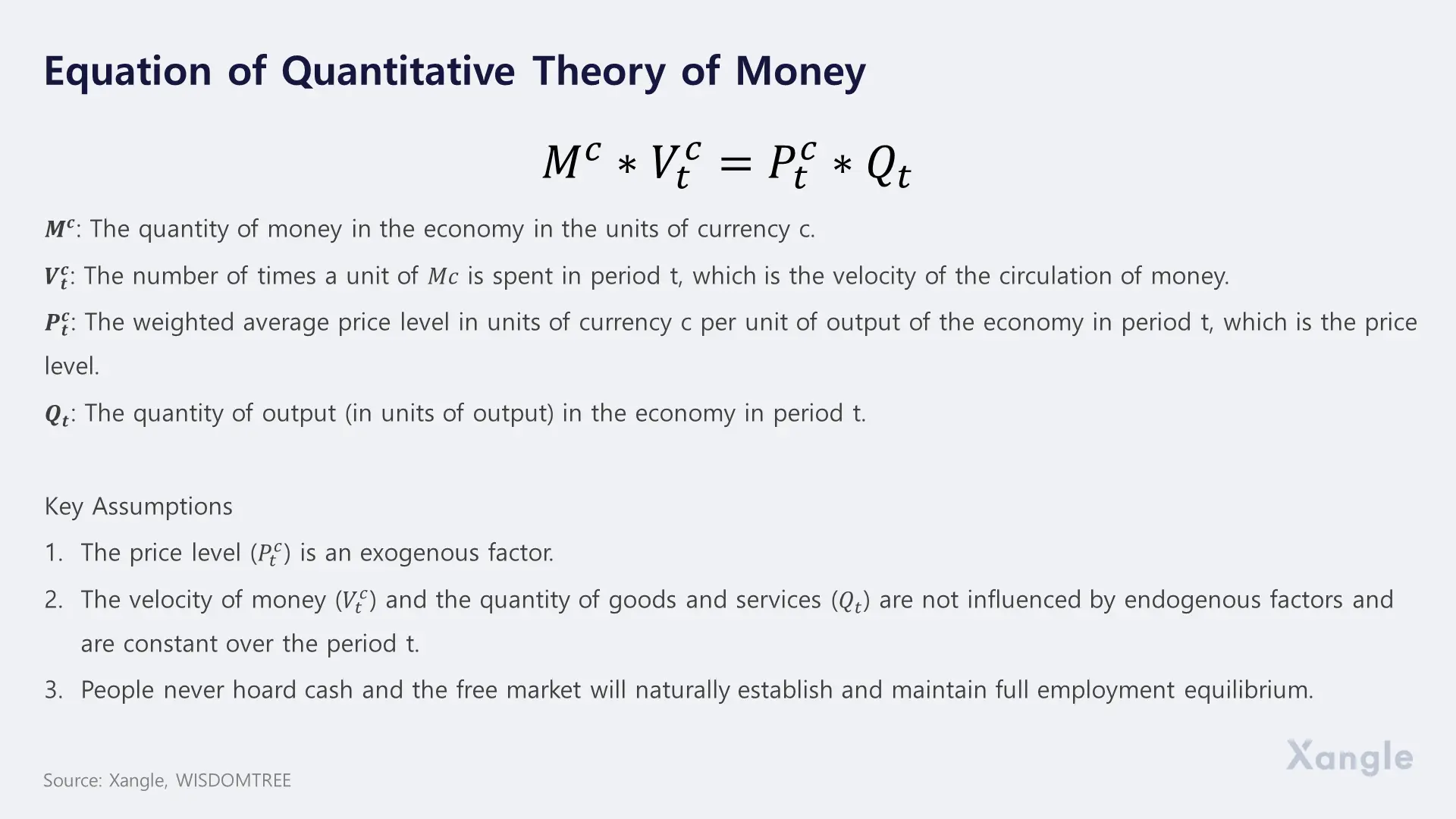

QTM (Quantitative Theory of Money)

by CHOBiden

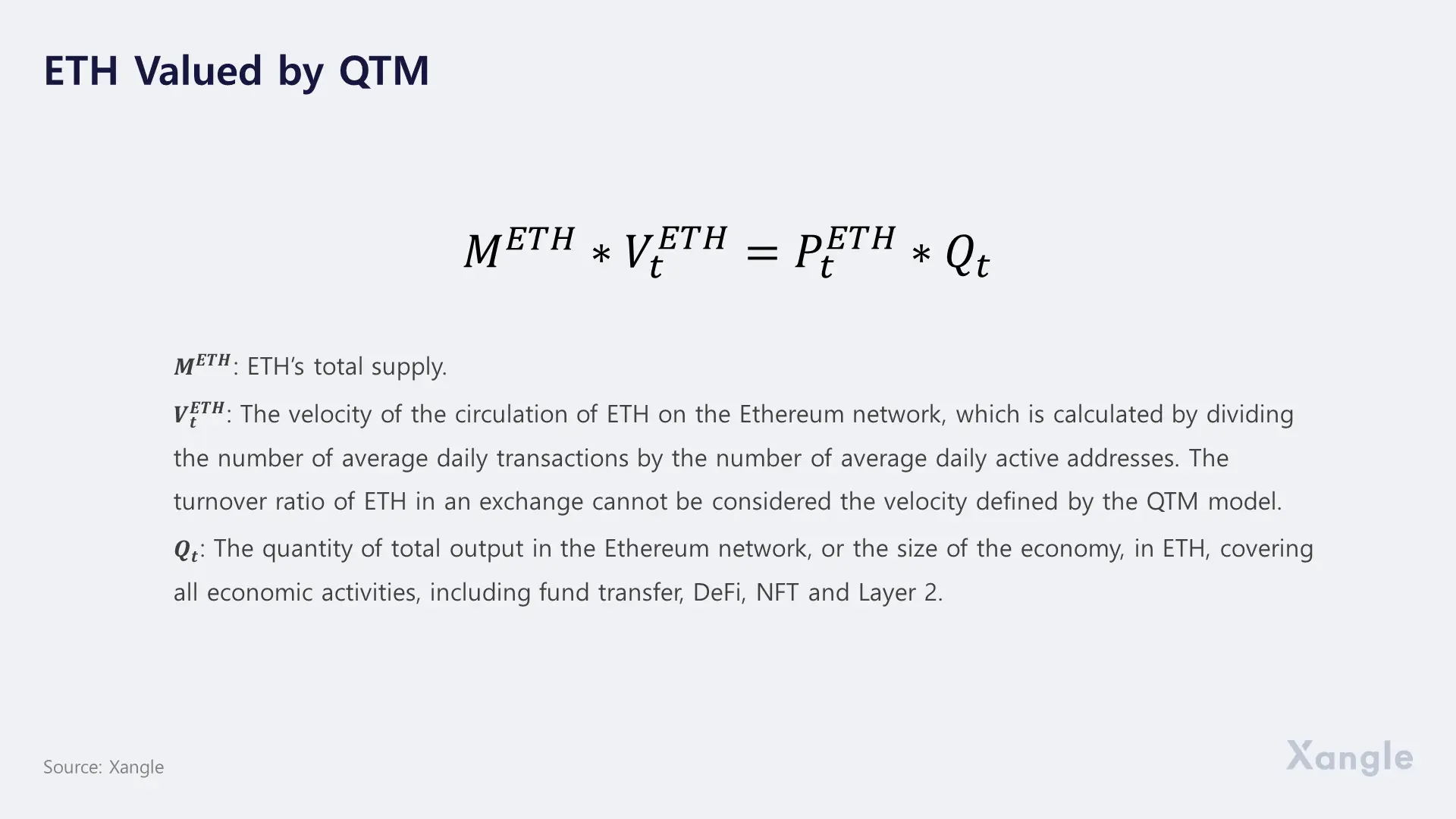

While Layer-1 coins may be likened to raw material, given that they are used to pay for the network fee, they may also be viewed as the key currency for transactions in the network. Despite the rapid surge in the trading volume of stablecoins, ETH is still the most widely used currency for Ethereum-based DEXs, lending and NFTs. If a Layer 1 mainnet is a city or a country, Layer 1 coins are money or a medium of exchange, allowing for application of the Quantitative Theory of Money (QTM).

The QTM is a macroeconomic model that has been developed by Irving Fisher, Milton Friedman and other prominent economists. It describes the relationship between the total economic output and the value of money in circulation. The Quantity Theory of Money equation is as follows with ETH being the variable:

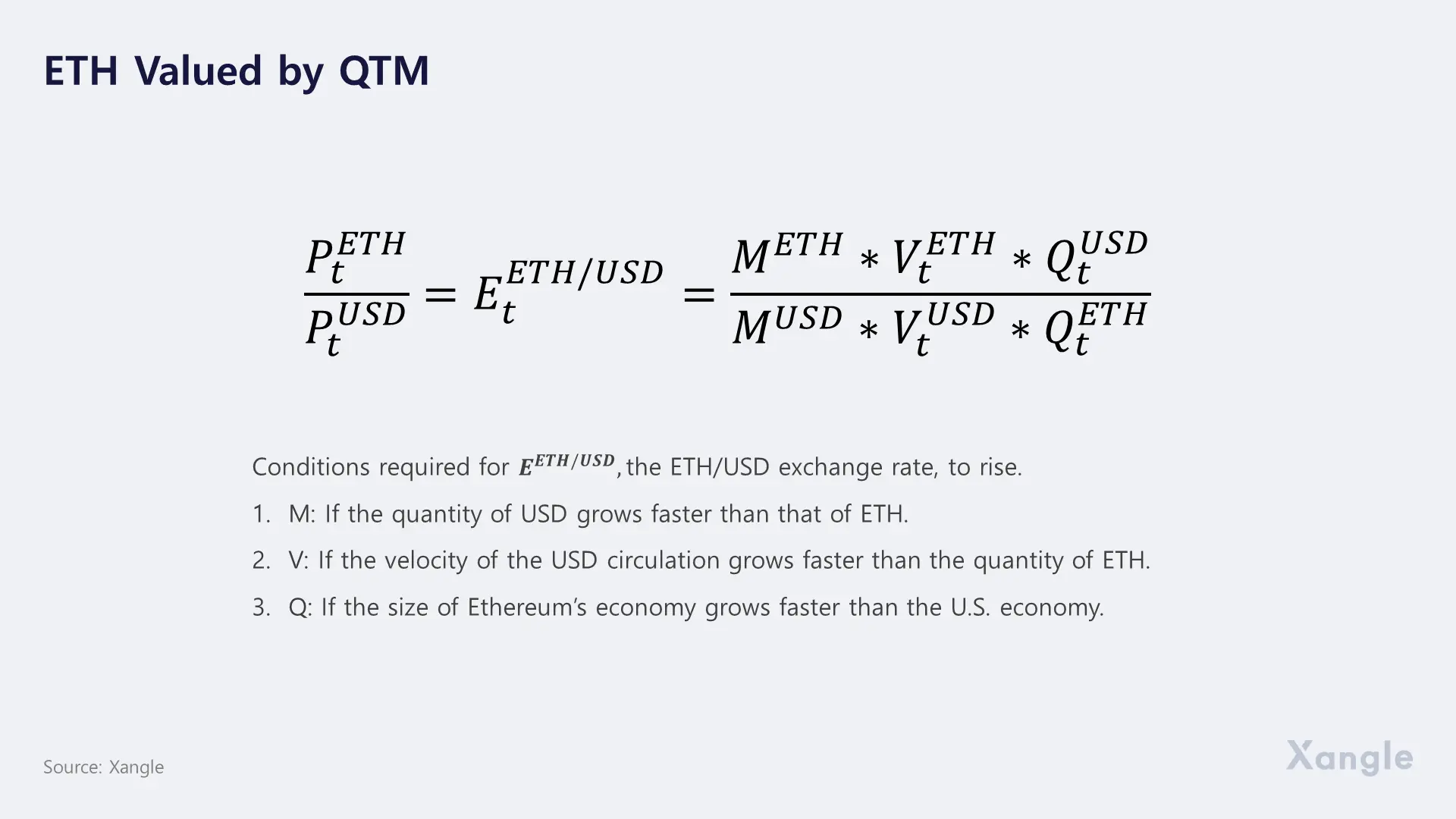

One thing to be mindful of when applying this model is that P in this equation represents the price level rather than the price of ETH and that the same model should be applied to the USD to find the ETH/USD exchange rate. Yet, again, the current ETH/USD exchange rate as of 2022 that is calculated by the formula is not the dollar-based price of ETH since P is a comparison between price levels.

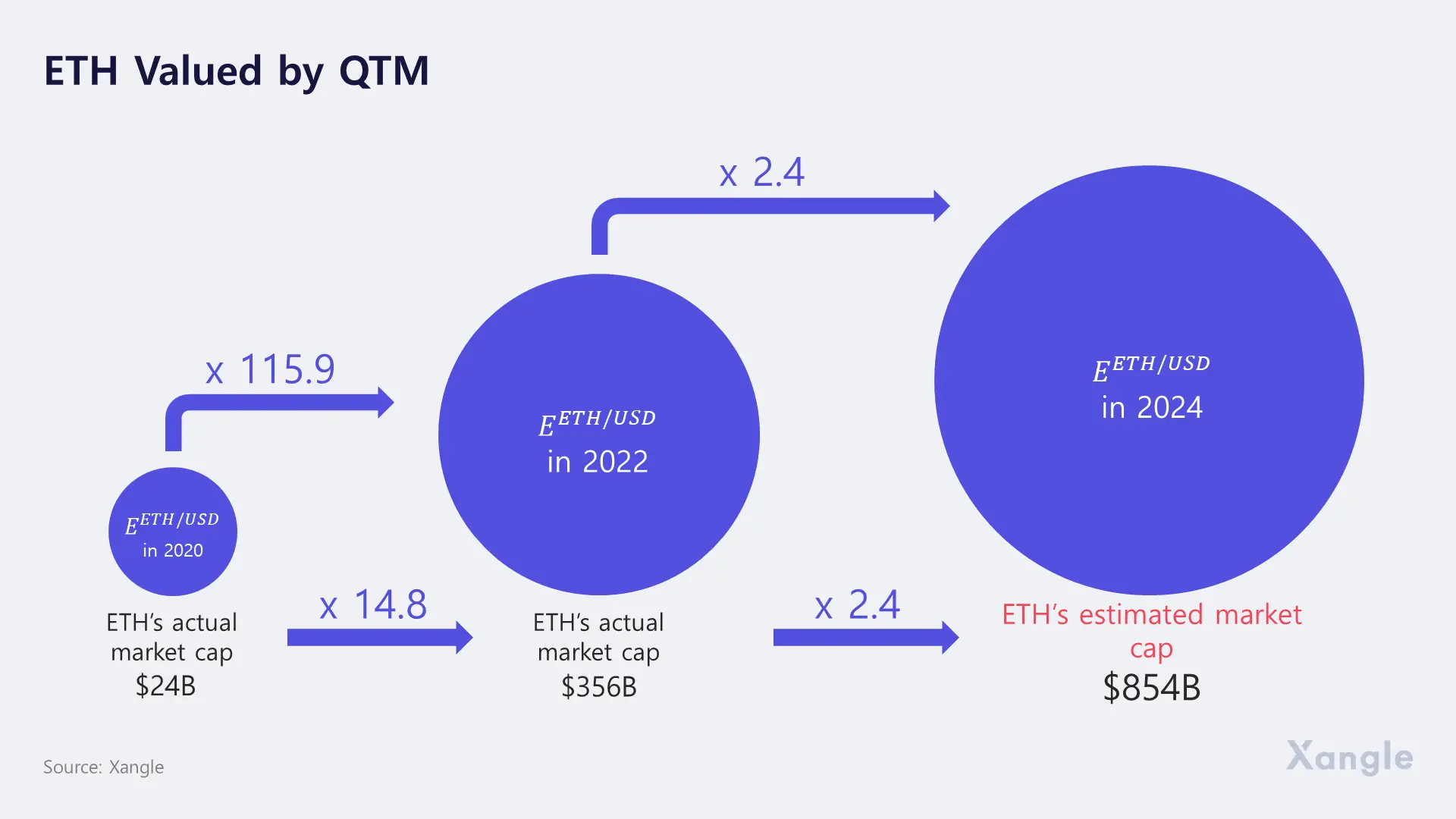

We compared the 2020 and 2022 ETH/USD exchange rates that the QTM model turned in to examine the validity of the outcome and also the upside potential of ETH for 2024. We set the annual growth rate of the money supply of ETH by 2024 at 4% and the annual growth rate of the economy at 60%, referring to ResearchandMarkets.

According to the QTM model, the ETH/USD exchange rate turned out to have jumped 115.9 times in 2022 compared to 2020, while Ethereum’s market cap grew by 14.8 times in those years. Despite the possibility of the recent macroeconomic volatility that might have caused the undervaluation, if the possible undervaluation is ruled out, the market capitalization of ETH in 2024 is estimated at $854B (approx. $7,000 per 1 ETH) under a conservative assumption.

Although the exact size of an economy and speed of money circulation cannot be measured and the quantity theory of money is essentially not designed to measure the value of a currency, there is no denying that the attempt to view a new type of asset called ETH as an independent national currency of a country called Ethereum was meaningful in itself. While the QTM may also be applied to other Layer 1 blockchains like Avalanche, Fantom and Solana, a meaningful result is deemed unlikely given that the blockchains have actually been put to use for less than a year.

3. Securities of Technology Companies with High-Growth Potential: Stocks or Interest-Bearing Assets

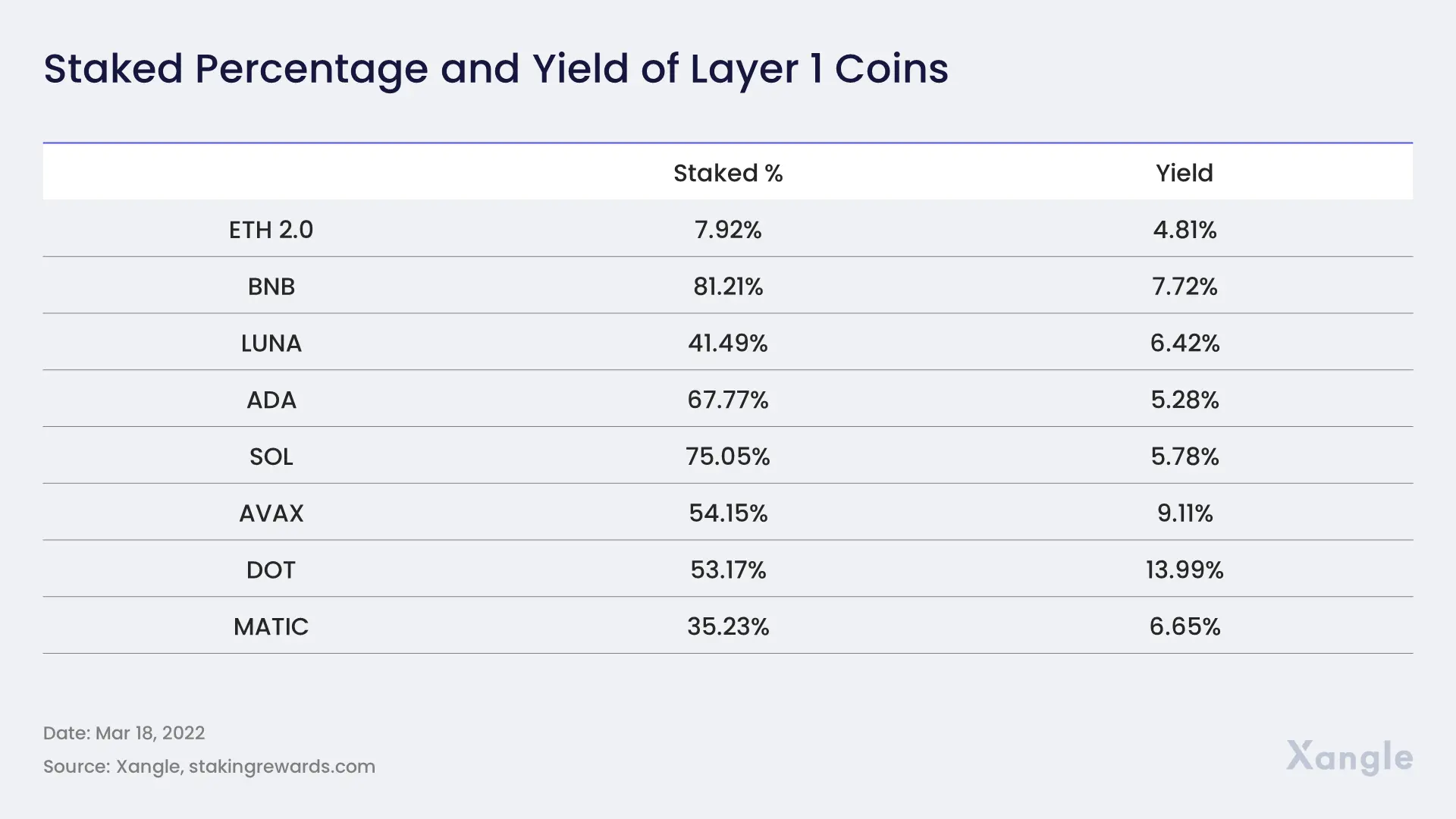

Ethereum, as well as most Layer 1 coins, ran an Initial Coin Offering (ICO) at the beginning of their project. An ICO is the equivalent of an IPO in the stock market, raising funds to run the project. Although there is an ongoing debate over whether or not cryptocurrencies can be legally classified as securities, they are, in a sense, stocks or interest-bearing assets in that: crypto holders can claim part of the ownership of the protocol according to their stake; the profits that arise from the protocol are distributed through dividend payout or token burn; and staking is rewarded with yields on the PoS-based layers.

Ethereum, in particular, was able to generate steady revenue from the protocol, and the network has grown to a meaningful level since the summer of 2020 in which the network took off. According to Token Terminal, the cumulative revenue of the Ethereum protocol over the past year is about $10.8B. Considering that the protocol generates revenue, the following valuation approach is also applicable.

Price-to-Sales Ratio (PSR)

by. TraceØ

In the stock market, the Price/Sales Ratio (PSR) is commonly used to appraise potential high-growth companies. It is an indicator obtained by dividing the current stock price by the sales per share. The PSR is primarily applicable to investment decisions that put more weight on the growth potential of a company. Coupang, for example, was listed on the Nasdaq last year but had been failing to turn a profit despite such a rapid sales growth.

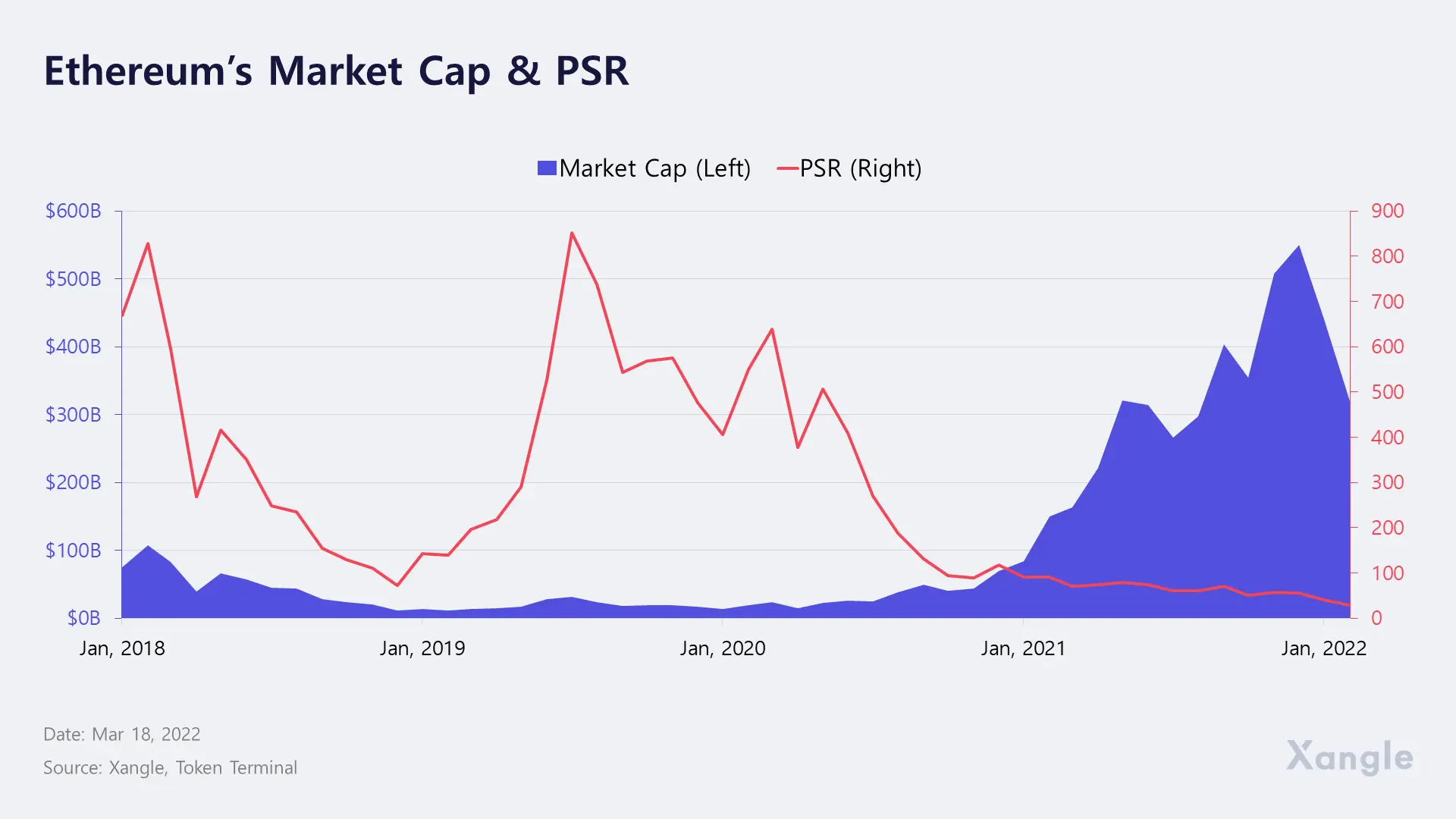

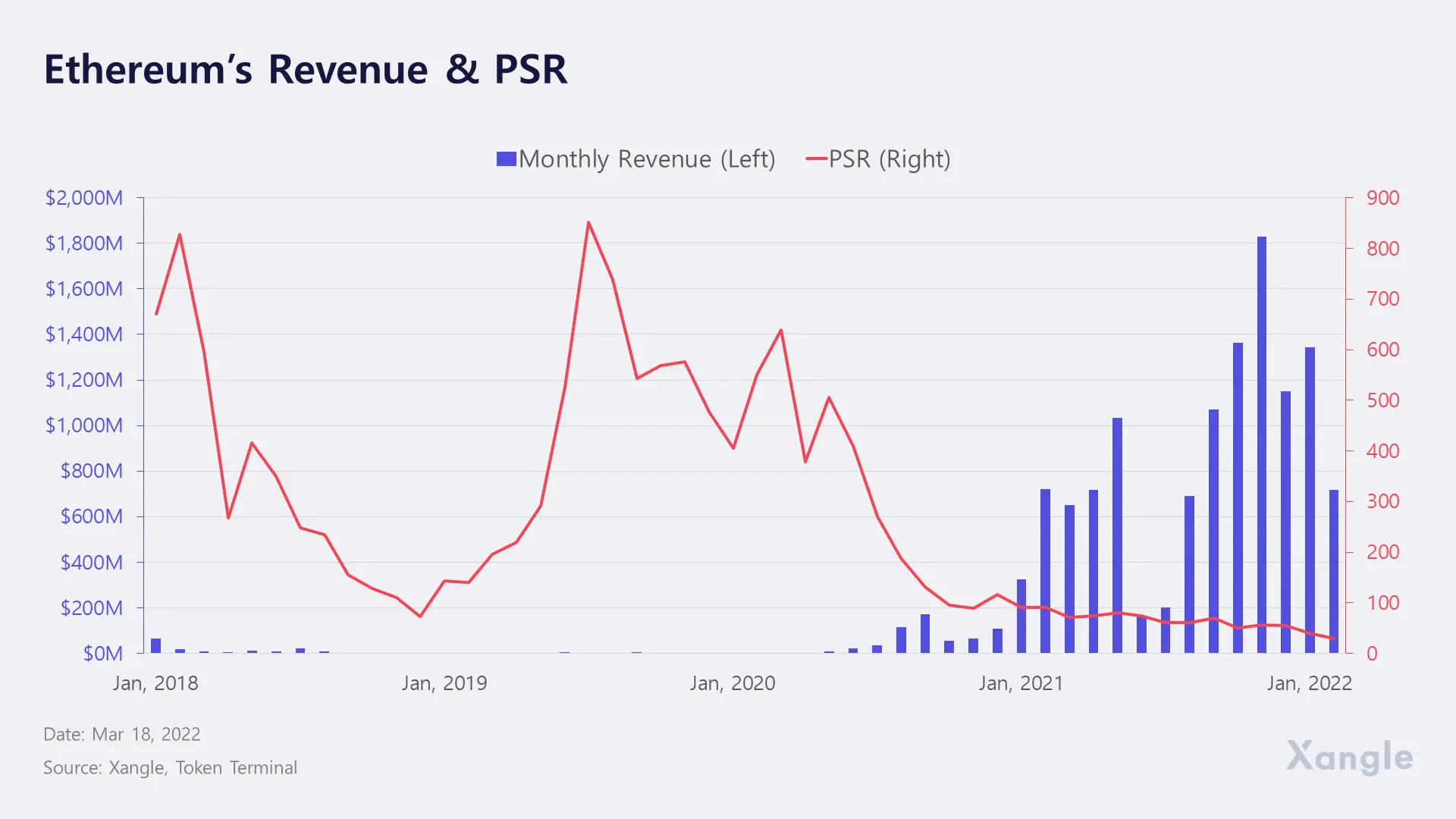

The same logic was deemed applicable to the Ethereum network as its revenue has grown exponentially year after year since its launch. Unlike in the past when the PSR indicated that the network was overpriced, the ratio has become relatively deflated since 2020 with the boom in the ecosystem that led to a radical spike in revenue. Since Ethereum does not have a hard cap on ETH supply and the circulating supply constantly changes, we based the PSR chart not on 1 ETH but rather on Ethereum’s market capitalization and total sales.

Looking at the band of the ratios (trailing 12 months) since 2020, when sizable revenue started to arise, ETH used to trade at around 75x until 2021 but started to trade at around 45x-60x after the NFT craze had led to a spike in sales in 2Q and 3Q 2021. Already, the market slowdown and rapid advances in Layer 2 have significantly lowered the gas fee and the enhanced scalability will further boost the on-chain usage of the network, allowing the PSR to potentially stand at 45x. As such, the current PSR of 30x is deemed somewhat underpriced than what the ratio could potentially reach.

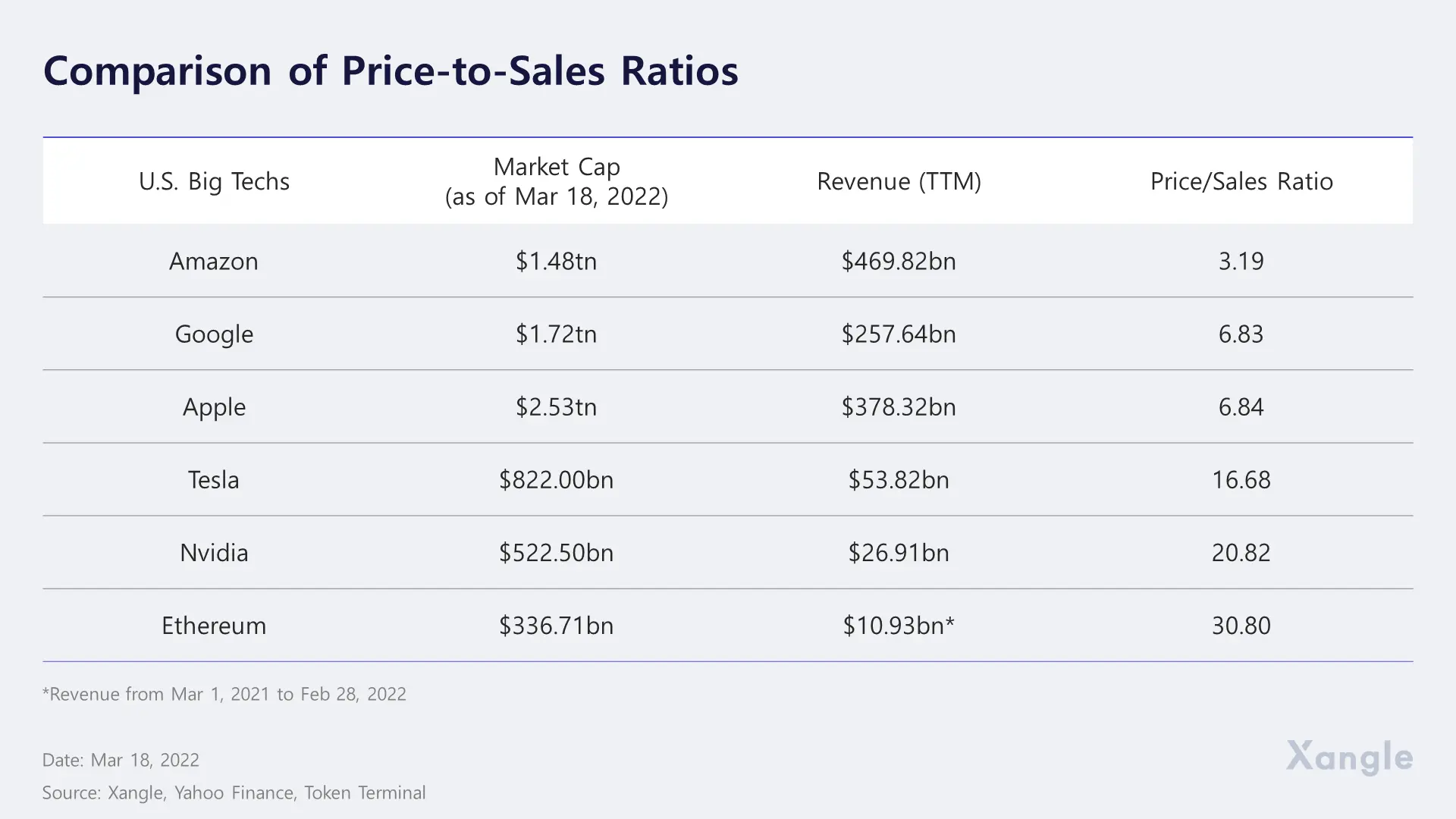

For comparison, the price/sales ratios of U.S. big techs are as follows. This may make Ethereum’s PSR look relatively higher, but Ethereum’s accelerating revenue growth somewhat warrants putting an extra premium on the network.

The Proof-of-Stake (PoS) blockchains, on the other hand, consume less energy during a consensus process and thus are expected to lower the cost of running the nodes. Considering that blockchain projects are run in a decentralized manner, their net profit margin is expected to be higher than that of traditional industries. A net profit margin of 80% may be a somewhat radical assumption, but if so, Ethereum’s current price-to-earnings ratio is approximately 37. On the other hand, the price-to-sales ratio or price-to-earnings ratio were not considered an appropriate indicator to gauge the value of most of the Layer 1 coins except Ethereum since their sales have not reached a meaningful scale.

Interest-Bearing Assets Under PoS Consensus

by Jehn

Ethereum is migrating from the Proof-of-Work (PoW) to Proof-of-Stake (PoS) consensus mechanism, and already, most of the Layer 1 coins have adopted the PoS algorithm. On the PoS chain, holders can earn yield by staking the Layer 1 coins on the network, but the differences with bonds are yields that keep changing according to the staking ratio or changes in policy and an absence of maturity.

Grayscale, the world's largest digital asset manager, defined crypto assets that provide yield and utility within the network as interest-bearing assets and saw them as a completely new asset class having the characteristics that have never existed.

Conclusion: Valuation Model Evolves along with the Market

by Jehn, Do Dive

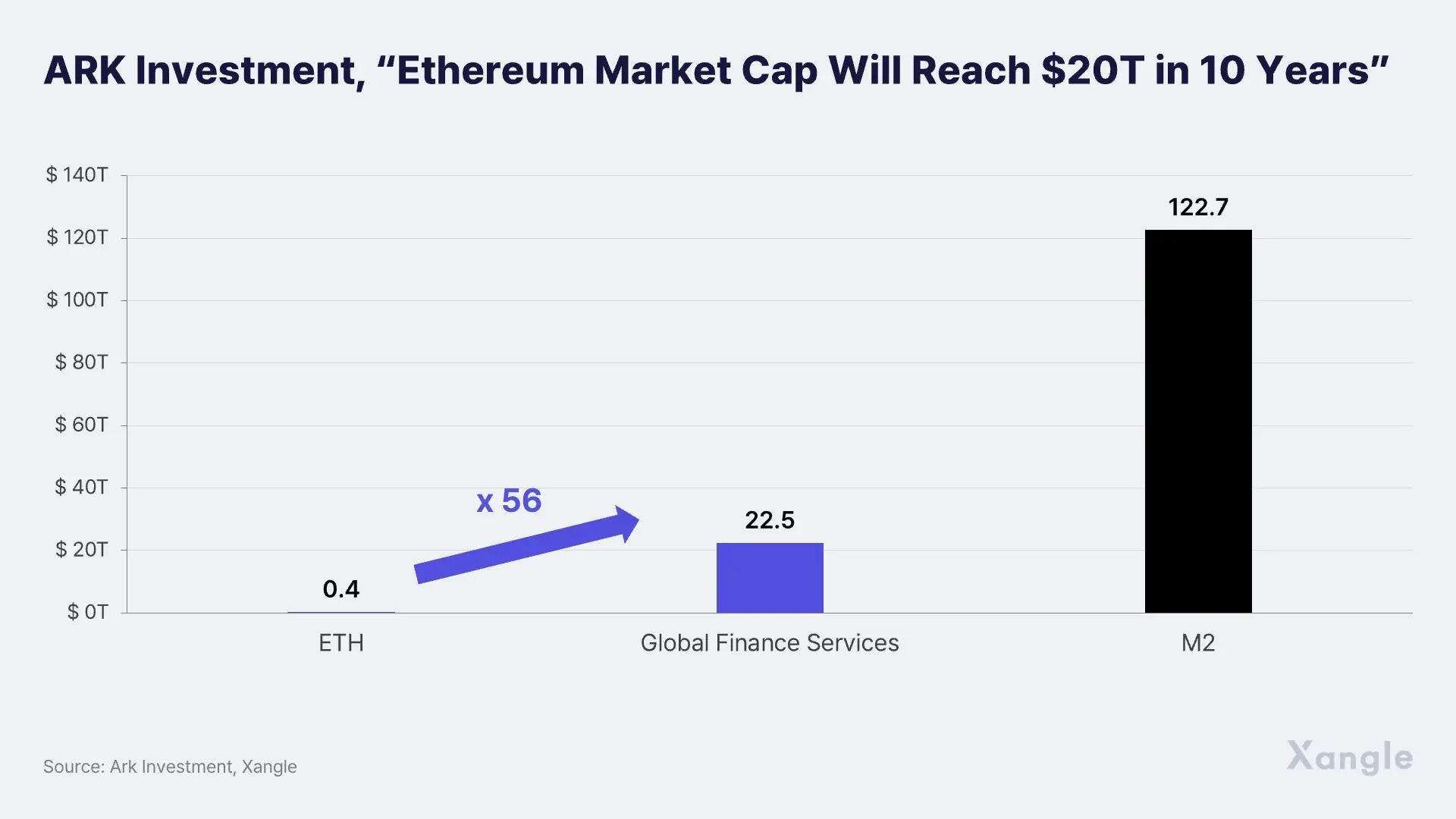

ARK Investment predicted that, in 10 years’ time, the Ethereum network would likely become the epicenter that will start replacing most of the traditional financial services, adding that the network’s market capitalization may also hit $20T if it partially replaces the global M2 money supply, considering that ETH is the most preferred collateral in the decentralized finance and NFT ecosystem.

Increasingly, expectations are running high as to how the Ethereum and other Layer 1 blockchain ecosystems will change our lives. As part of the Xangle Valuation Series, we valued Ethereum in this article and our assessment suggested that Ethereum is currently fairly valued or slightly overvalued as a network, but is undervalued as a store of value like money or securities.

The fact that the results differ depending on the valuation methodologies illustrates that Ethereum has the characteristics of many different asset classes, and that there is no valuation model that is able to provide a sufficient and clear explanation as of yet. In particular, the network’s expansion after the introduction of the Layer 2 or sidechain as well as the deflationary nature of the staking and burn mechanism were left out from the valuation models. Since EIP (Ethereum Improvement Proposal) 1559 went live in Aug 2021, part of the network fees have been spent on burning ETH, and a cumulative $5B worth of ETH has been burned so far. Considering that ETH is an asset that deflates in value as much as the network grows and that the staked amount will likely lead to a reduced circulating supply after the transition to the PoS, there seems to be no doubt that the per-unit value of ETH has upside potential.

Likewise, it is somewhat regrettable that the tokenomics of other Layer-1 coins was not sufficiently reflected in the valuation either. The extraordinary growth of the crypto market will only further propel the need to find the fair value of a cryptocurrency, which will then be continuously followed by subsequent fresh attempts. We hope this article served as an opportunity to reflect on how Ethereum and other Layer 1 coins are defined and where we see their values come from.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Solana RWA: A Look at the Key Players](https://resource.xangle.io/files/content/F779A005246C0299246537AACB3A39F2_1782287059970.webp)