Anchor's Yield Reserve is Not Looking Well: Projections and Current Trends

[Xangle Originals]

Written by Moon Bit, Bonk

The Current State

Terra’s sustainability has been questioned since its inception. Its algorithmic stablecoin, UST, maintains its peg through arbitrage trades made between LUNA and UST. Some critics believe that the relationship between LUNA and UST can trigger a death spiral; a perpetual downward spiral that will ultimately result in the failure of the pair. Indeed, UST showed some signs of instability in times of crisis, yet was able to maintain its peg.

Stability and growth are fundamentally driven by demand for the stablecoin. Whether it be arbitrage, lending, or yield farming, demand for UST is required for the LUNA-UST pair to maintain a healthy relationship. Higher UST demand leads to more LUNA burns, decreasing the supply of LUNA to push its prices higher and creating more demand for LUNA as the token’s price increases according to UST demand.

But what if UST demand drops? And what if that demand is totally dependent on one protocol in the Terra ecosystem? Yes, it is time to talk about Anchor Protocol.

Savings on Steroids

As of writing this article, Anchor provides a whopping 19.4% APY for providing UST. There is no threshold where the annual yield declines, there is no minimum amount to deposit, and there is no lockup period. Not only that, all the yield is provided in UST, a stablecoin. So, basically, the user can use Anchor as a savings account with a super high interest rate.

In the age of negative interest rates, Anchor’s rates are more than attractive; it would be stupid not to save on Anchor. And here comes the $450 million dollar question: how do they pay for all the interest?

How Does It Add Up?

Currently, there are two main revenue streams: lending and staking. Users can lend UST from the protocol for providing collateral in bLUNA, bETH, wasAVAX, and bATOM. The protocol will stake the collateralized assets to accrue staking rewards. The annual borrowing rate currently stands at 13.29%.

When there are enough lenders and collateralized assets under management, Anchor can take profits, but this has not been the case ever since its launch. Currently, Anchor’s Yield Reserve heavily subsidizes the losses.

As the protocol gained popularity due to its high yield, the reserve neared depletion earlier this year. On the 18th of February, the Anchor UST Yield Reserve was injected with approximately $450M by the Luna Foundation Guard. According to an analysis by Hashed, it claims that the reserve will last for at least 45 weeks until the protocol turns profitable.

On the 7th of April, the Yield Reserve decreased to $331M, initially from $505M. For 48 days, the Yield Reserve saw outflows of an average of $3.625 million per day. Extrapolating the current trend, the reserve is projected to deplete in 91 days. That is 13 weeks, which is merely a third of the projected timeframe. This obviously raises questions in terms of the sustainability of the protocol.

At Xangle, we compared the projection with the current trend. We collected the data for key metrics after the Yield Reserve injection to compare them with the base projection model proposed by Hashed. Keep in mind that the data is only an aggregate of very short-term data (48 days).

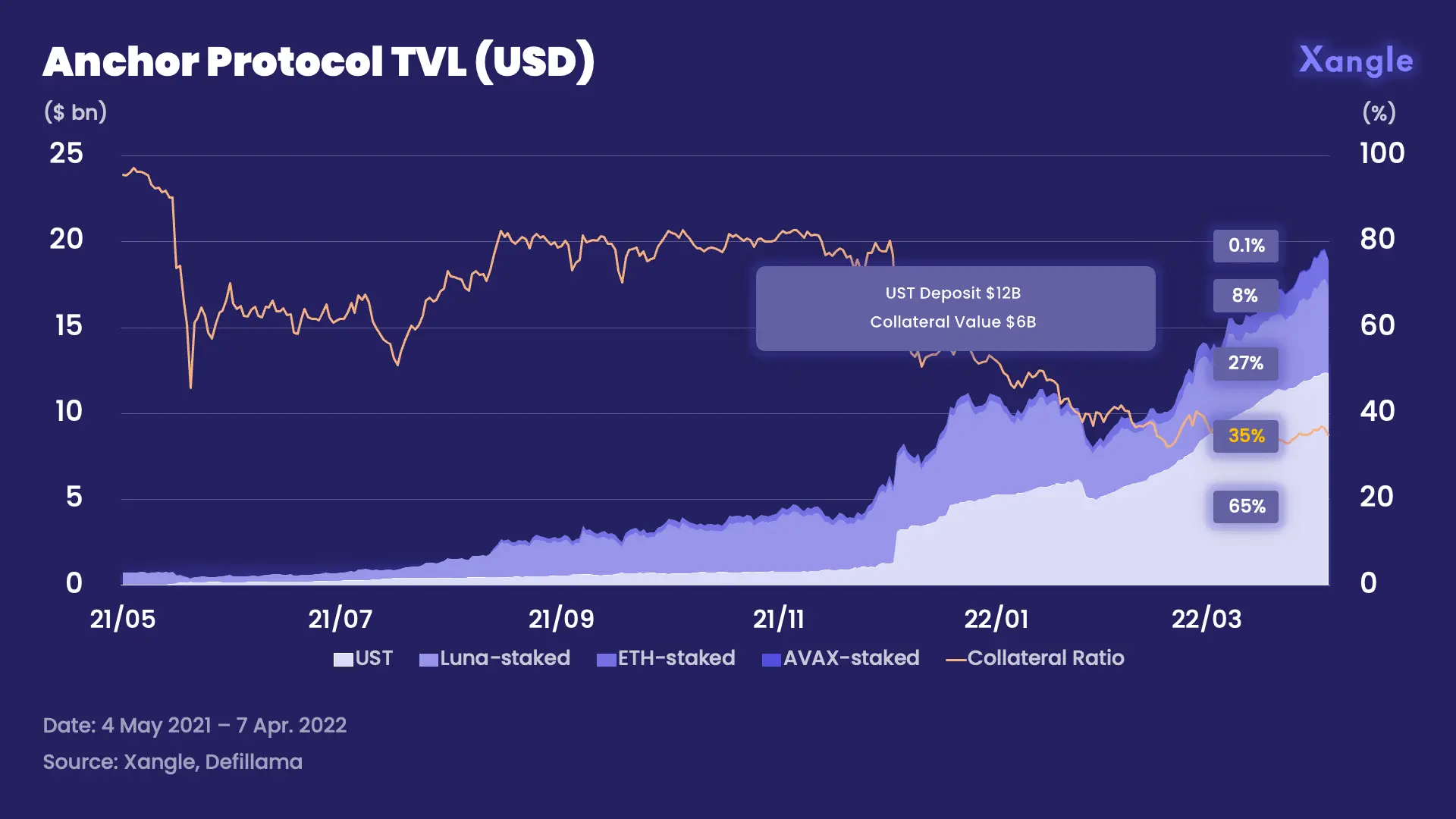

TVL & Reserve

First, let’s take a look at the macro:

- On the 7th of April, Anchor Protocol’s TVL recorded $19 billion.

- The UST locked on Anchor is approximately $12 billion, accounting for 65% of the TVL.

- The ratio of collateralized assets (bLUNA, bETH, wasAVAX, bATOM) to UST locked on anchor is falling.

- A lower collateral ratio implies lower cash inflows. More assets are being introduced to Anchor to increase the collateral ratio and ramp up stake revenue.

In short, Anchor is looking at a downward trend in its collateralized assets in terms of value. But one must consider that the value of assets goes through price fluctuations and thus cannot be a clear indicator when tracking the growth of collateralized assets on the protocol. Yet, it is still important as a point of reference pertaining to the loan-to-value ratio; a lower asset value leads to decreased lending volume, resulting in diminished cash inflows.

Furthermore, ongoing macro trends are not favorable to Anchor. As geopolitical issues like the Russia-Ukraine war and lockdowns in China are causing supply chain bottlenecks and adding pressure to inflationary forces, central banks are commencing rate hikes. The UST peg to the dollar becomes much more vulnerable during bear markets as the demand for risk assets like LUNA shrinks.

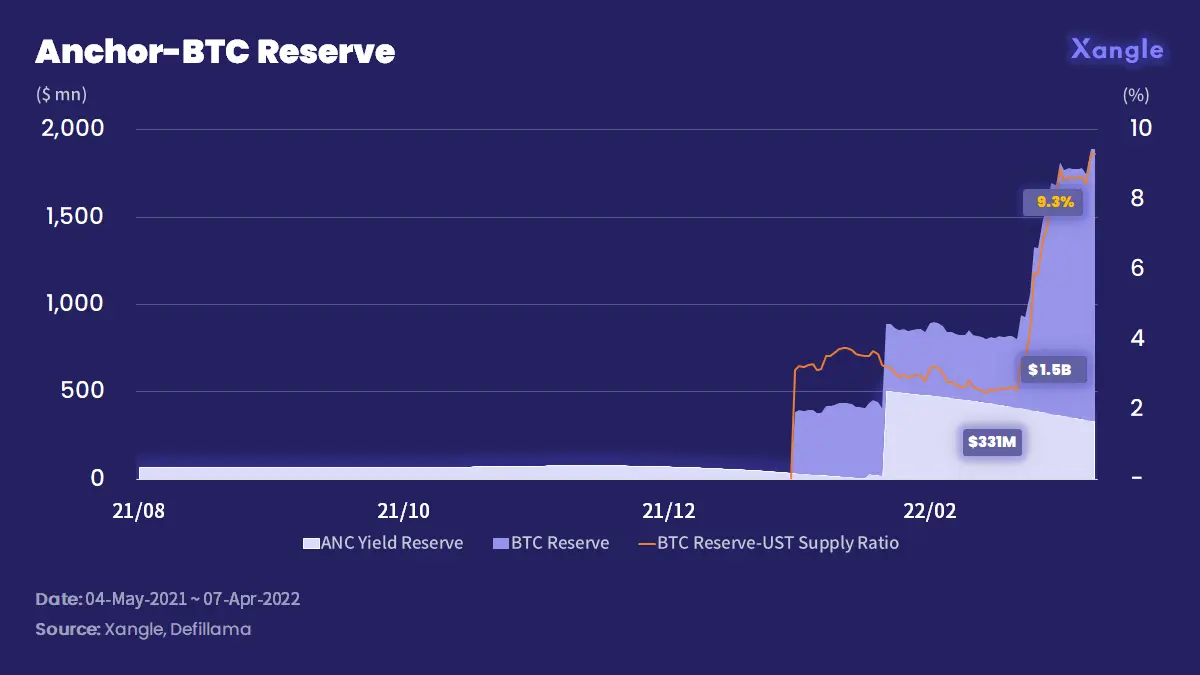

Right on time, the Luna Foundation Guard (LFG) introduced the BTC Reserve as a safeguard to maintain the UST peg during volatile market situations.

- Though the BTC reserve has no direct impact on the cashflow of Anchor, it will absorb the volatility when UST drops below $0.98.

- The BTC Reserve has grown to 9.3% of the UST market cap and is planning to expand the reserve up to 10 billion dollars.

Projections vs. Current Trends

Cash Outflows

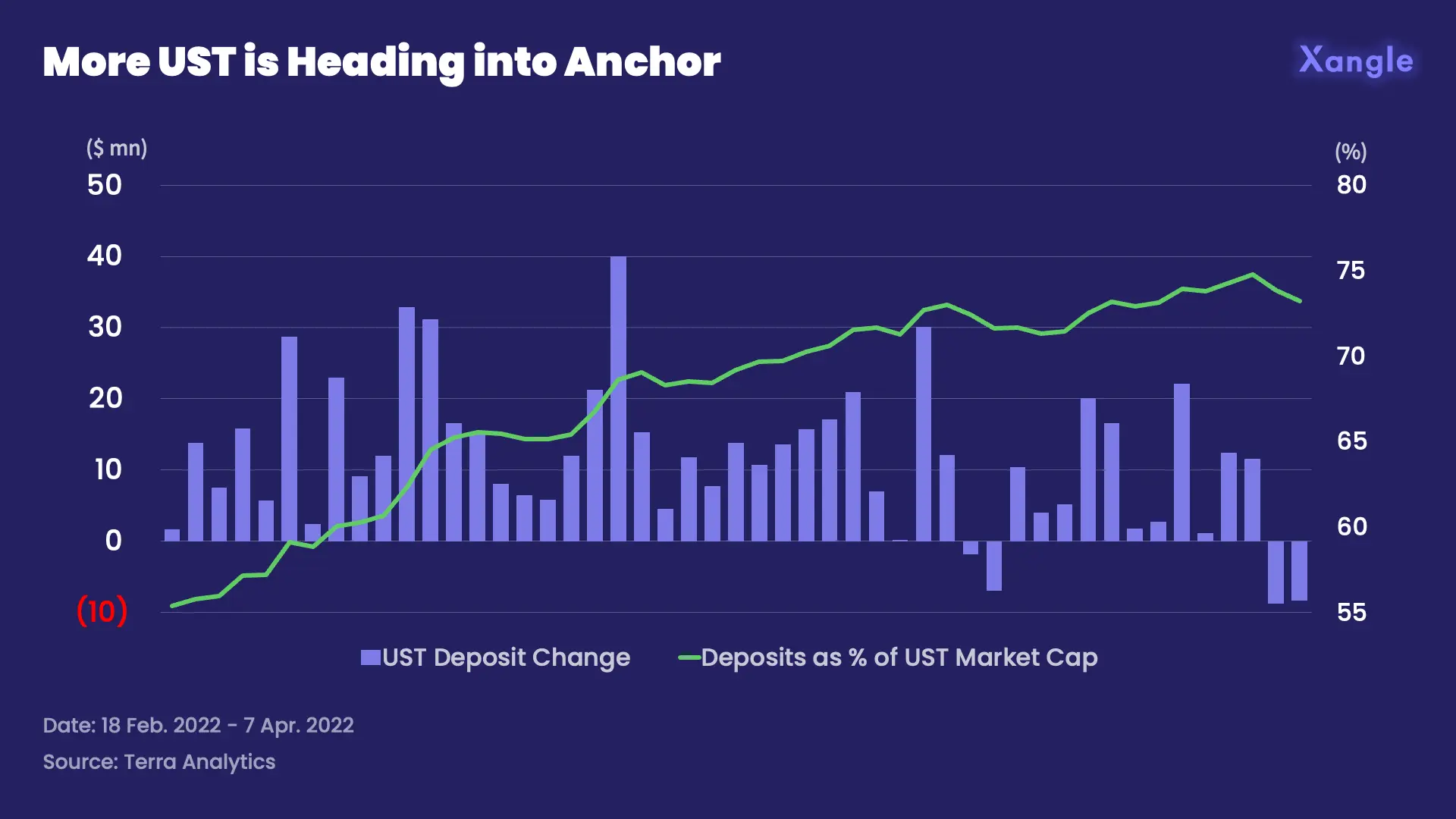

Seven weeks after the injection, UST and deposits on anchor grew significantly above the projection model while the yield on deposits maintained similar levels.

- The current trajectory is showing significant growth of UST and UST deposits on Anchor.

- Though the average of UST deposits on anchor is sitting at 67%, the rate of UST deposits on anchor is increasing, which is alarming.

- Only 48 days ago, nearly 20% of the UST market cap moved to Anchor. Will this rate decrease? Maybe when semi-dynamic yield rates are applied.

- On a side note, the compound weekly growth rate (CWGR) for UST deposits on Anchor during the 48-day period was 9.6%, making it 4.4% higher than the UST market cap CWGR.

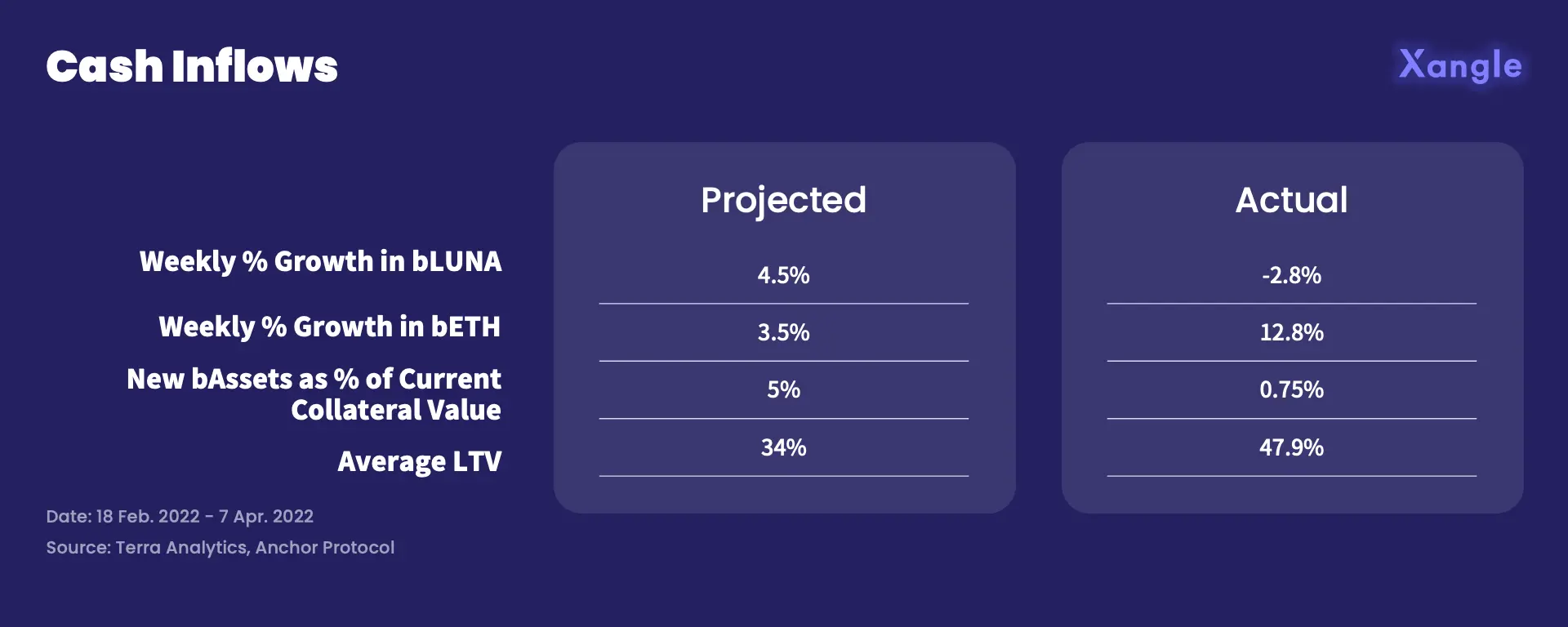

Cash Inflows

Now let’s take a look at the cash inflows. The two key metrics to follow are collateral and borrowing. Collateral is provided in the form of bAssets, which include bLUNA, bETH, wasAVAX, and bATOM.

- bLUNA recorded negative growth while bETH overperformed.

- Currently, new assets such as wasAVAX and bATOM are underperforming, but the two assets were only recently introduced; it is too early to judge if the growth of the two assets will stay stagnant, not to mention that other assets will be introduced in the future.

- When we calculated the compound daily growth rate of wasAVAX during a period of 16 days, it showed a daily growth of 3.5%.

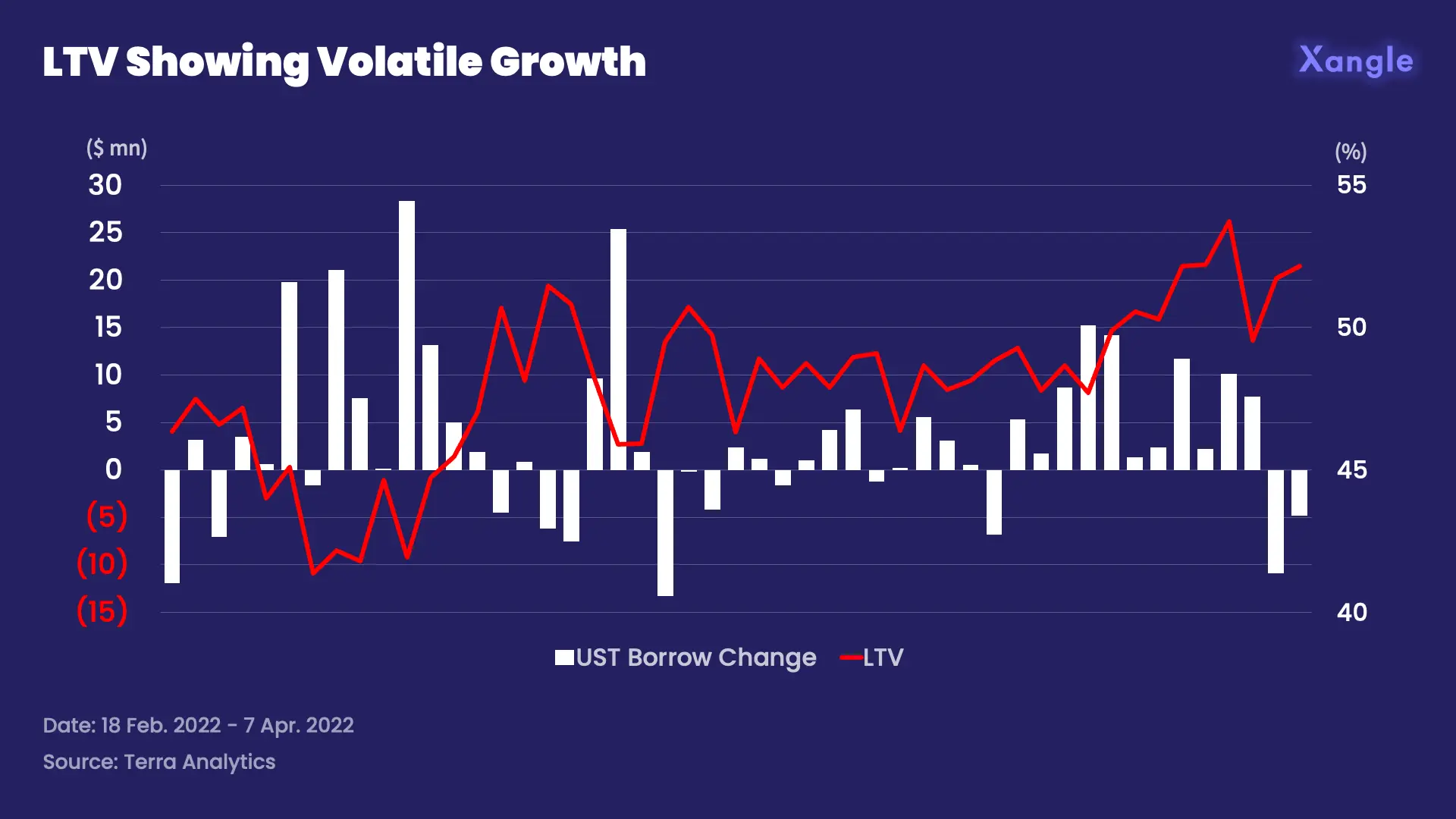

- LTV is fluctuating on a daily basis, but the overall trend seems positive.

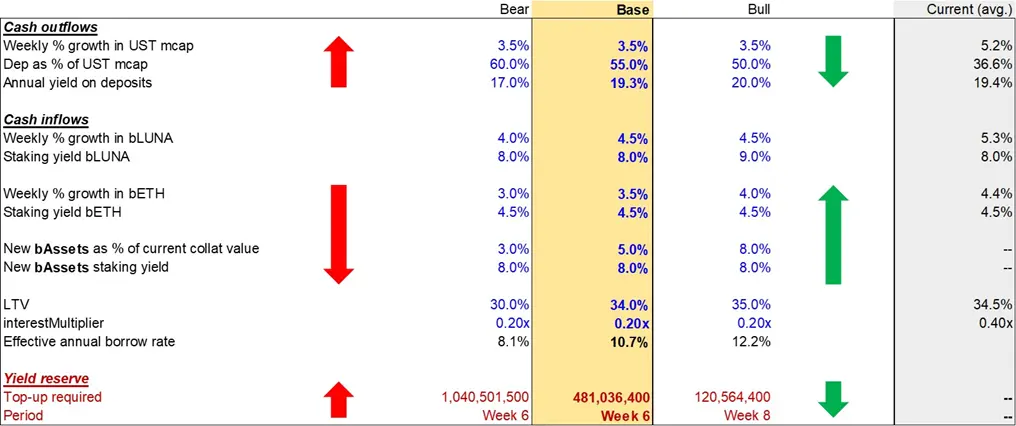

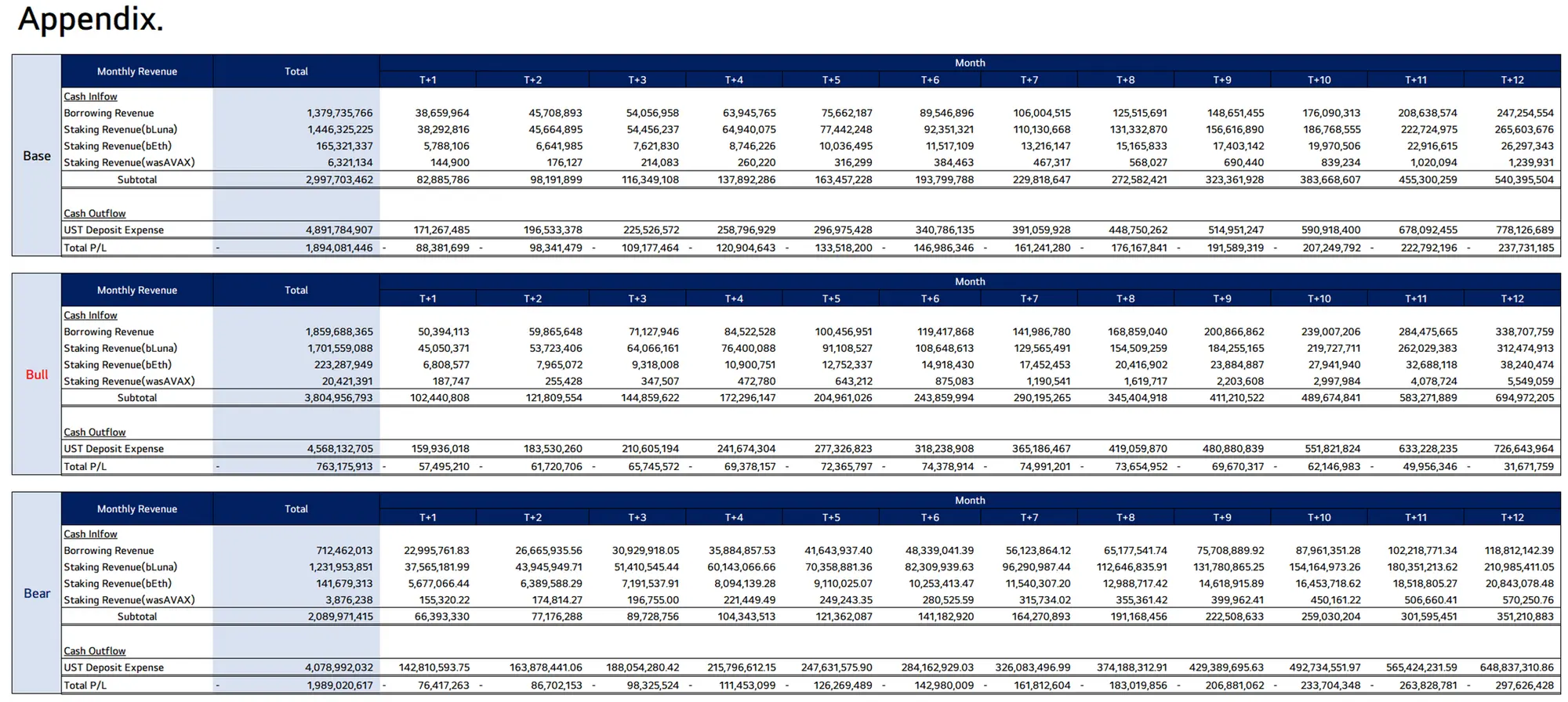

Projection Models

Based on a 12-month cashflow analysis of three scenarios, the Yield Reserve is expected to be depleted in no more than five months.

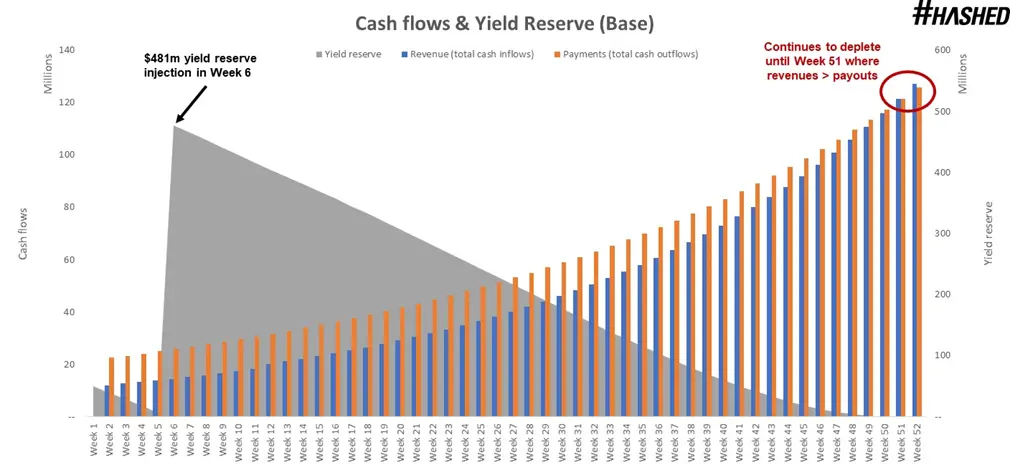

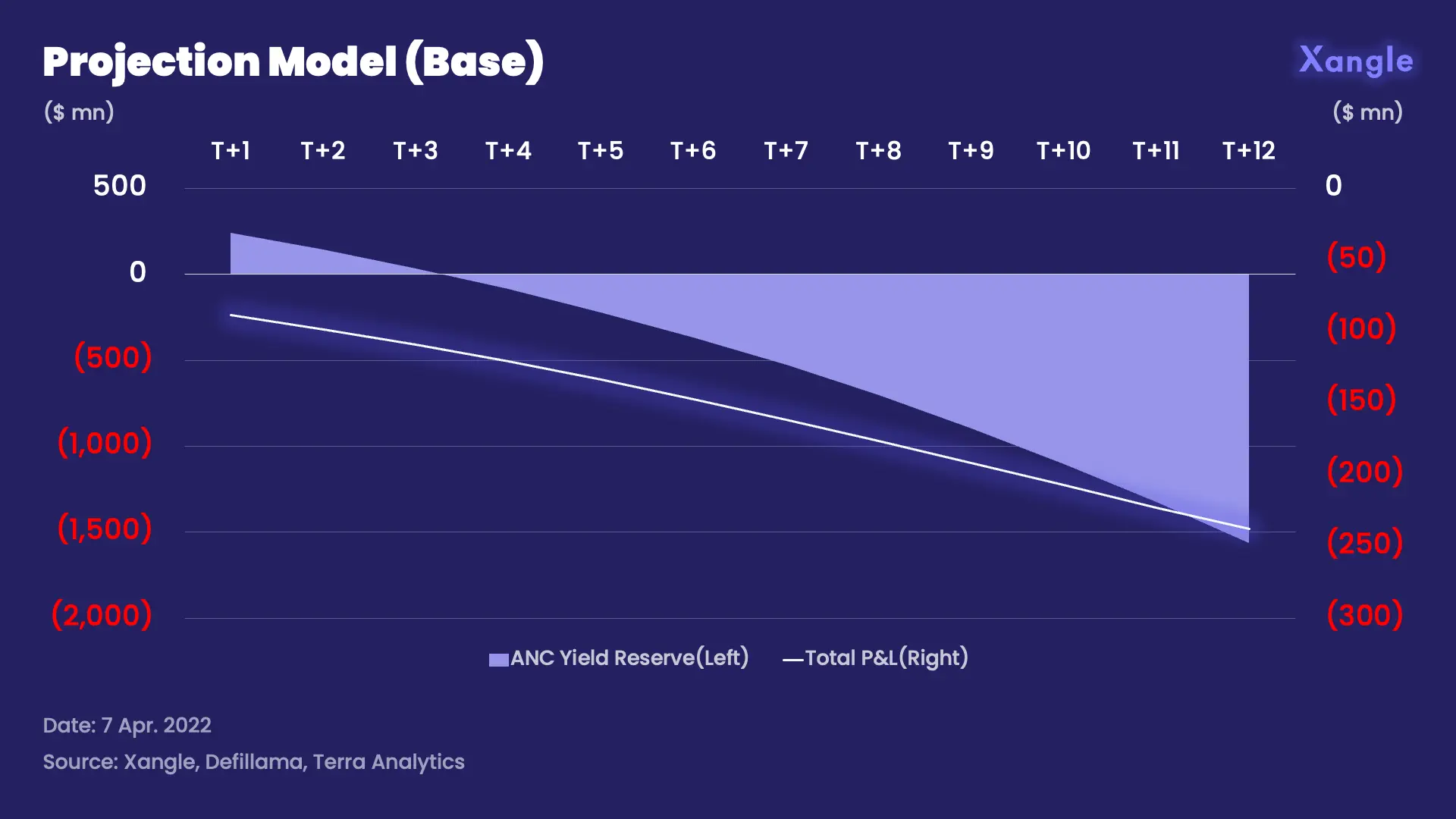

Projection Model (Base)

- According to our base projection model, the Yield Reserve will be depleted in three months.

- Under base model conditions, cash outflows will slowly increase.

- When a dynamic earning rate is applied, deposit yields must go down to 15% APY to turn a profit.

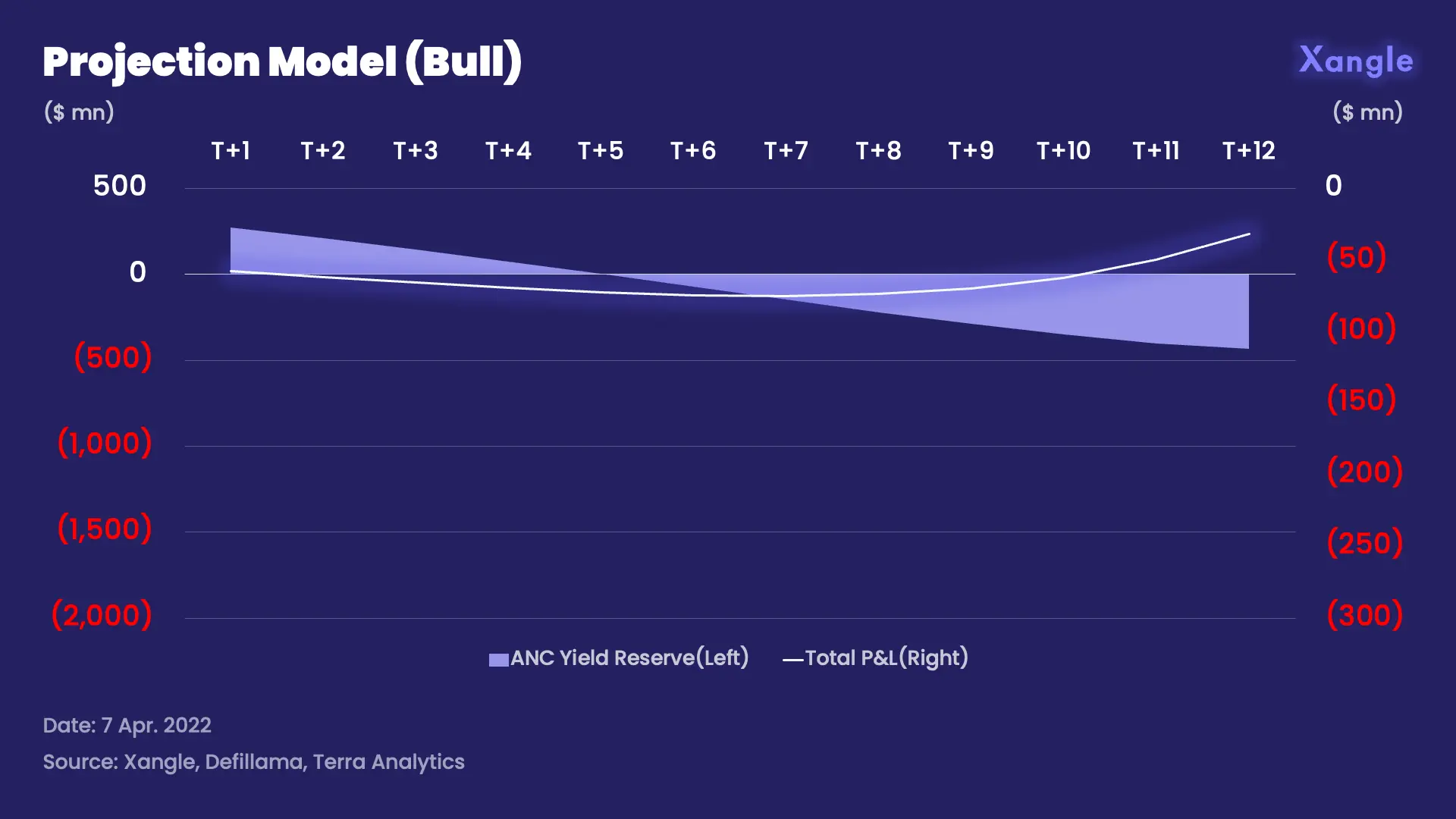

Projection Model (Bull)

- Though the Yield Reserve will be depleted in 5 months, cash flow will eventually turn profitable after a year.

- The bull projection model assumes that 50% of the UST market cap will be deposited on Anchor. Currently, the average of UST deposits on Anchor is 67% after the top-up.

- A bull case will not be achievable unless the UST deposits on Anchor are dramatically reduced.

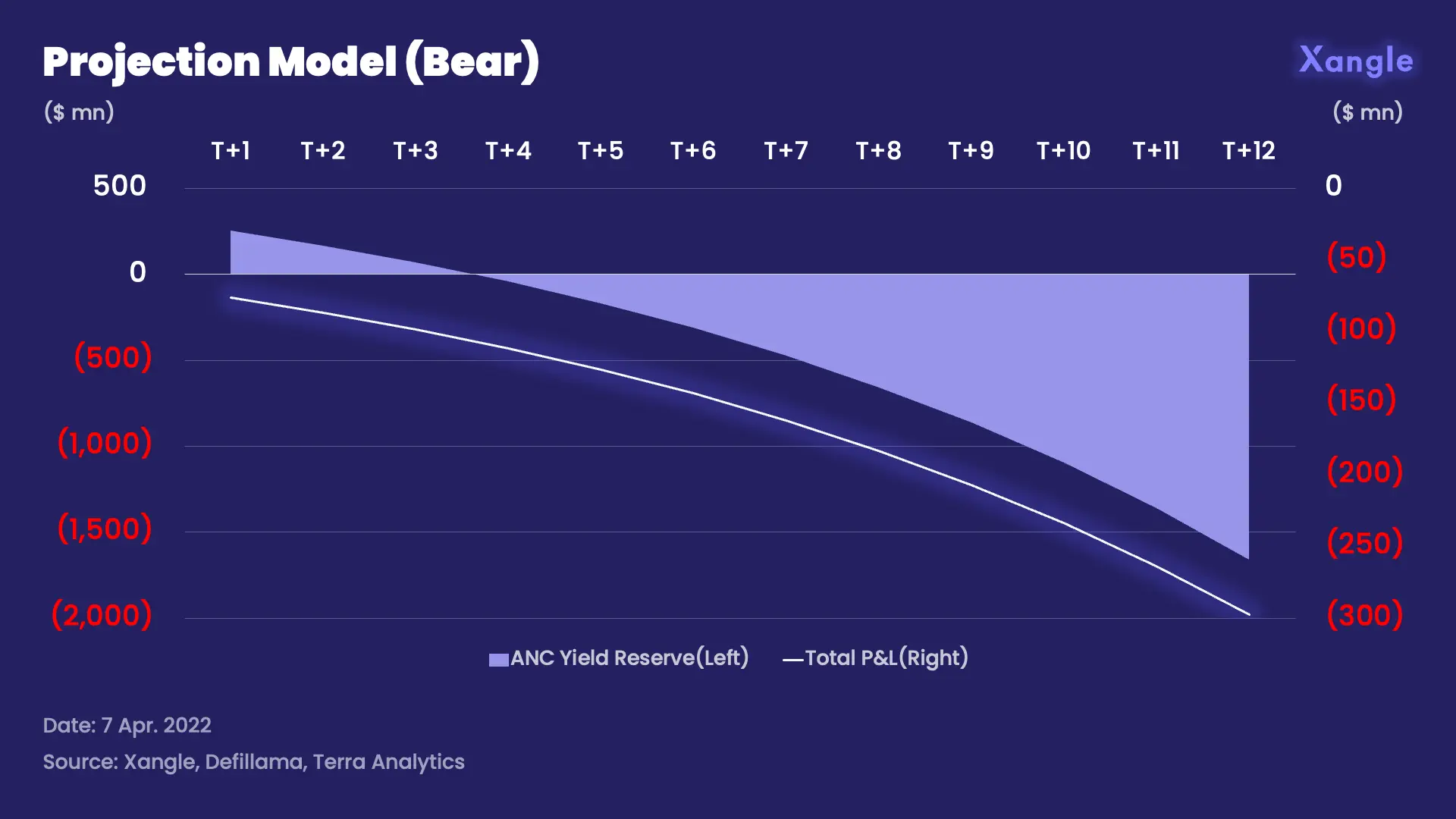

Projection Model (Bear)

- According to the bear projection model, the Yield Reserve is scheduled to deplete in 3 months.

- In such circumstances, UST Deposit Yields fall to 16.5%.

End Notes

UST as an algorithmic stablecoin has shown unprecedented growth. At its core, Anchor Protocol is bleeding to maintain its high yield. Without demand outside Anchor, the current trend where UST is concentrated on Anchor will exacerbate its imbalance in cashflows.

To address the cashflow imbalance, Anchor is adding more collateralized assets like bATOM and wasAVAX while increasing the LTV for bLUNA and bETH for additional leverage. UST demand is being further pushed by liquidity pools like the 4pool on Curve Finance and asset purchases on BTC and AVAX. At the moment, it seems like the underlying strategy is to infiltrate the Bitcoin, Cosmos, and Avalanche network to create a flywheel effect, where UST stands as the de facto leader of decentralized stablecoins.

However, it is inevitable to lower the UST Deposit Yield as it is not sustainable at current rates. When yield rates are adjusted, maintaining a competitive advantage over other protocols will be the first challenge, as UST deposits and collateral assets might leave the protocol for higher yields. Therefore, Terra falls into the conundrum between economies of scale and profits. Is it high yield or trust?

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle Valuation Series] ④ Lending Protocol](https://resource.xangle.io/content/thumbnails/711/content_711_thumbnail_adb18197.webp)