Will Terra’s Anchor Protocol Continue to Cruise Ahead Despite the Yield Reserve Issue?

[Xangle Digest]

By Moon Bit

Translated by elcreto

Summary

- As Anchor Protocol’s TVL grows over time, questions have been raised over Anchor Protocol’s yield reserve and whether it can maintain its current 19% APY.

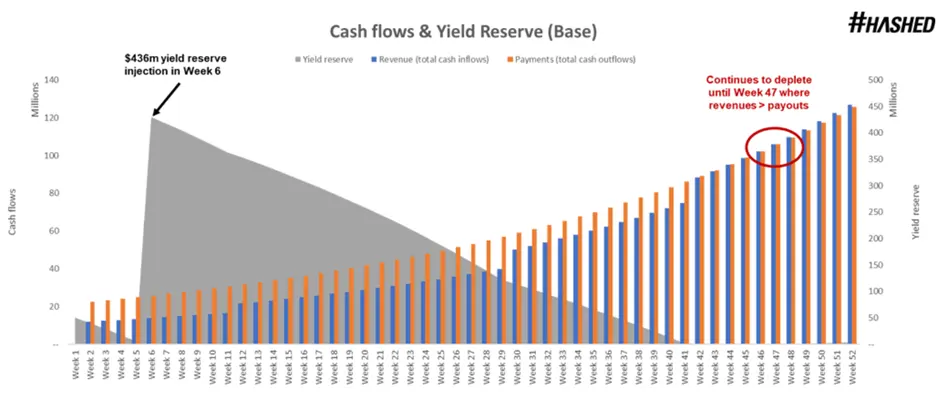

- As such, LFG (Luna Foundation Guard) stepped in and topped up Anchor Protocol’s yield reserve with UST worth US$500M on Feb 18.

- Moing forward, it may be less burdened by the yield payout if the market outperforms the forecast, but if the market condition worsens, its yield reserve again will stir up questions.

LFG Troubleshooting the Issue

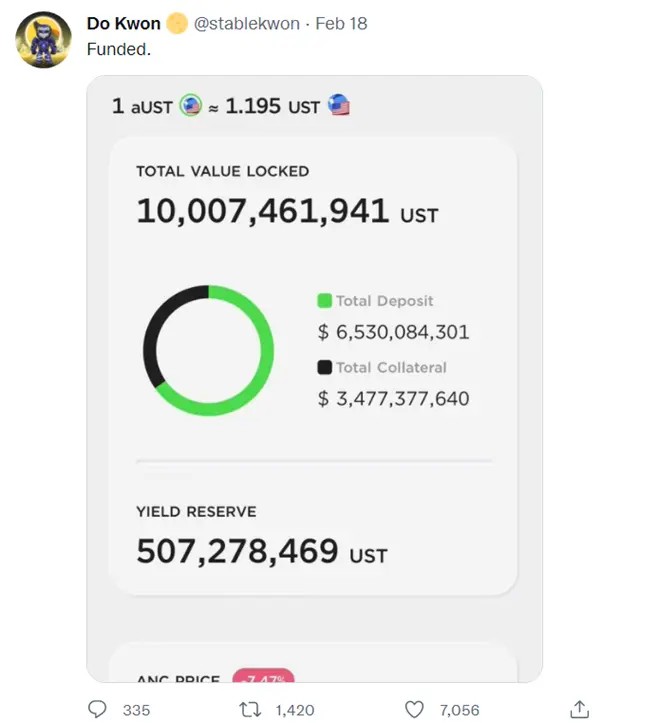

On Feb 18, Terra’s CEO Do Kwon announced via Twitter the injection of US$450M worth of UST in Anchor’s yield reserve. Following the Feb 8 announcement that the Luna Foundation Guard (LFG) would pay US$450M to cover Anchor’s yield reserve, the LFG swapped 9.5M LUNA to UST and completed the yield reserve on Feb 18.

Anchor Protocol's Yield Reserve: What Causes the Concern?

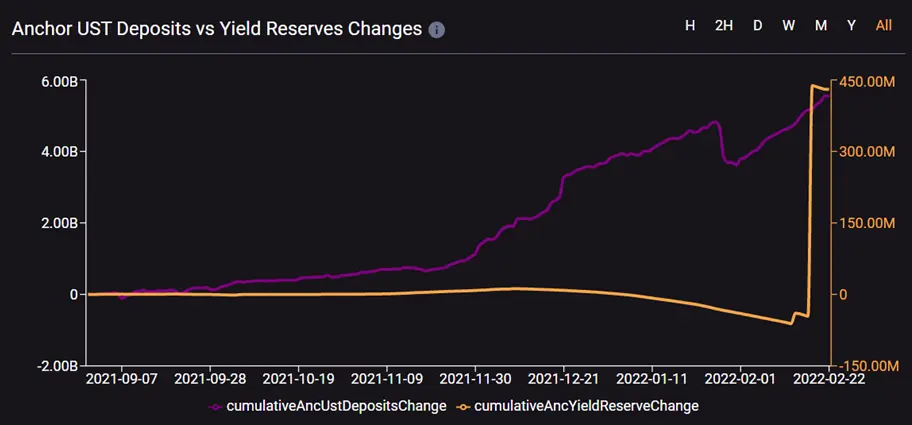

Anchor Protocol's yield reserve has constantly been an issue. Terra's anchor protocol pays an APY of 19-20% for the deposited UST (Terra USD). Since Nov 2021 when the crypto market started to wobble, liquidity in the market flowed into stablecoin deposits, which had been demonstrating a steadily high APY even in the bearish market.

As a result, Anchor Protocol’s TVL has shot up, sparking concerns that the yield reserve may not be sufficient enough to offset the yield payout. The source of financing the yield payout for Anchor Protocol has been revenue from lending and staking the collateral, such as bLUNA and bEth. Considering that the high-yield stablecoin deposits have been the primary driver of growth for Terra and that Anchor Protocol takes up a large proportion of TVL within the Terra blockchain (55% as of Feb 22) while having many dApps on it, Terra may be exposed to greater volatility whenever Anchor fluctuates.

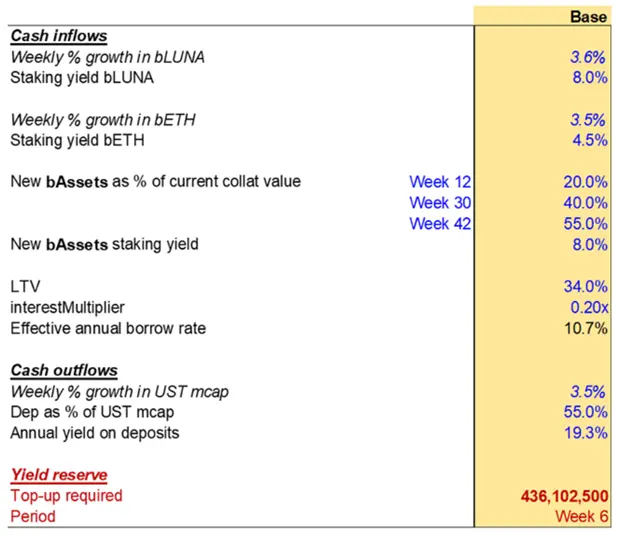

As questions have been raised over Anchor’s future cash flow, Hashed, a key investor for Terra, initiated an analysis and proposed a yield reserve of $450M. The analysis in the improvement plan predicts that Anchor will break even roughly around 40 weeks after the replenishment of funds, given the adoption of Anchor's V2 model and the addition of new collateral, such as bSOL. If the market conditions turn out better than expected, the burden of yield payout will be alleviated while conversely, the burden may escalate even further than the estimate if the market trends down, tossing it back to the same question.

A Fine Line to Walk to Break Even

If the crypto market remains bearish, funds floating in the market will be out in search of stable options. Given that one of such options is high-yield stablecoin deposits, the amount of yields Anchor Protocol has to pay out is bound to increase.

Although, of course, lowering the APY or adjusting the loan interest rate may alleviate the yield payment burden, such actions may end up damaging LUNA’s price as well as Terra’s revenue and TVL and even the ecosystem itself, given UST’s minting volume, LUNA’s value and the dynamic of the Terra ecosystem. Conversely, if the volume of minted UST grows but the demand is biased towards UST deposits in Anchor Protocol, the yield payment burden will likely escalate even further. In other words, Terra has to navigate such tradeoffs and continue to expand the ecosystem and replenish the funds until Terra’s sales exceed yields payable on UST deposits.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.