FRAX's Innovative Stablecoin Protocol: What Will It Change?

[Xangle Originals]

By Do Dive

Translated by elcreto

Summary

- Existing stablecoin models have a trade-off between capital efficiency and price stability.

- Adopting a fractional algorithmic stablecoin system, FRAX emerged as a reasonable compromise of existing models.

- Its TVL and price indicators are suggesting that Frax Finance’s model is rapidly gaining market recognition.

Types of Existing Stablecoins and the Trade-Offs

Stablecoins in the crypto market can be broadly divided into asset-backed stablecoins and algorithmic stablecoins (Although various models have emerged recently, only the basic models will be covered this time). Each stablecoin model has its own pros and cons, and there has been an ongoing discussion in the market about which is better. In particular, each model entails a trade-off between price stability (or reliability) and capital efficiency (or scalability).

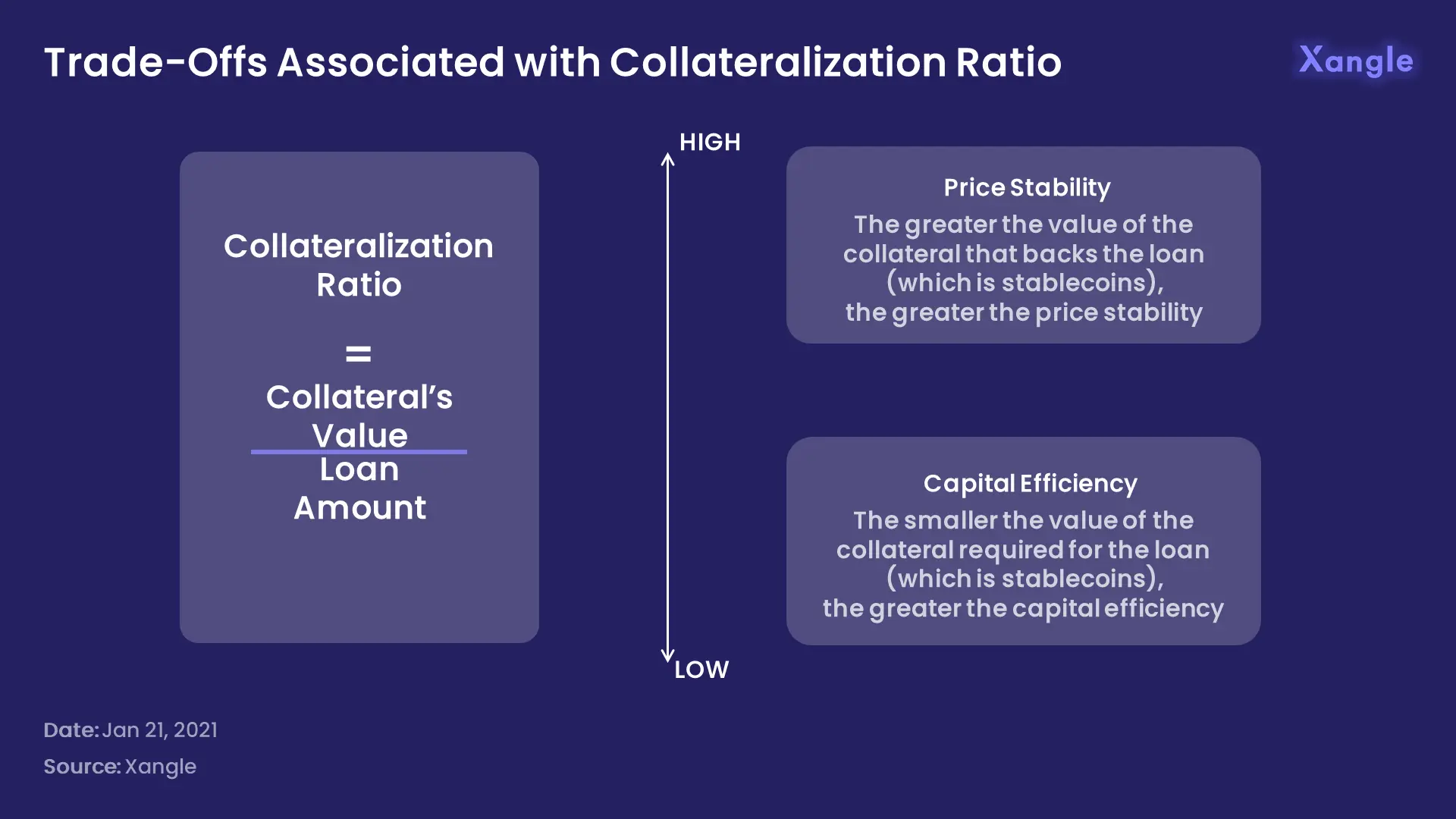

In the crypto market, stablecoins are issued in exchange for a pledged asset of a certain value, so it is necessary to understand the collateralization ratio. The collateralization ratio is the ratio of the value of the collateral to the amount of the collateralized debt. It indicates the amount of the collateral required to issue the stablecoin. If the collateralization ratio is 100%, you have to pledge an asset worth 1 dollar to issue 1 dollar worth of the stablecoin. Likewise, if the collateralization ratio goes down to 80%, 0.8 dollars is required to issue 1 dollar worth of the stablecoin.

As the collateralization ratio goes up, the size of the pledged asset that backs the value of the stablecoin gets bigger, thereby securing consumer confidence and price stability. There is a limit though. Stablecoin issuance’s dependence on the value of the collateral limits its scalability and dampens its capital efficiency, reducing its control to have the supply more in line with an increase in demand. Conversely, if the collateralization ratio goes down, capital efficiency is achieved at the expense of price stability.

Asset-Backed Stablecoin

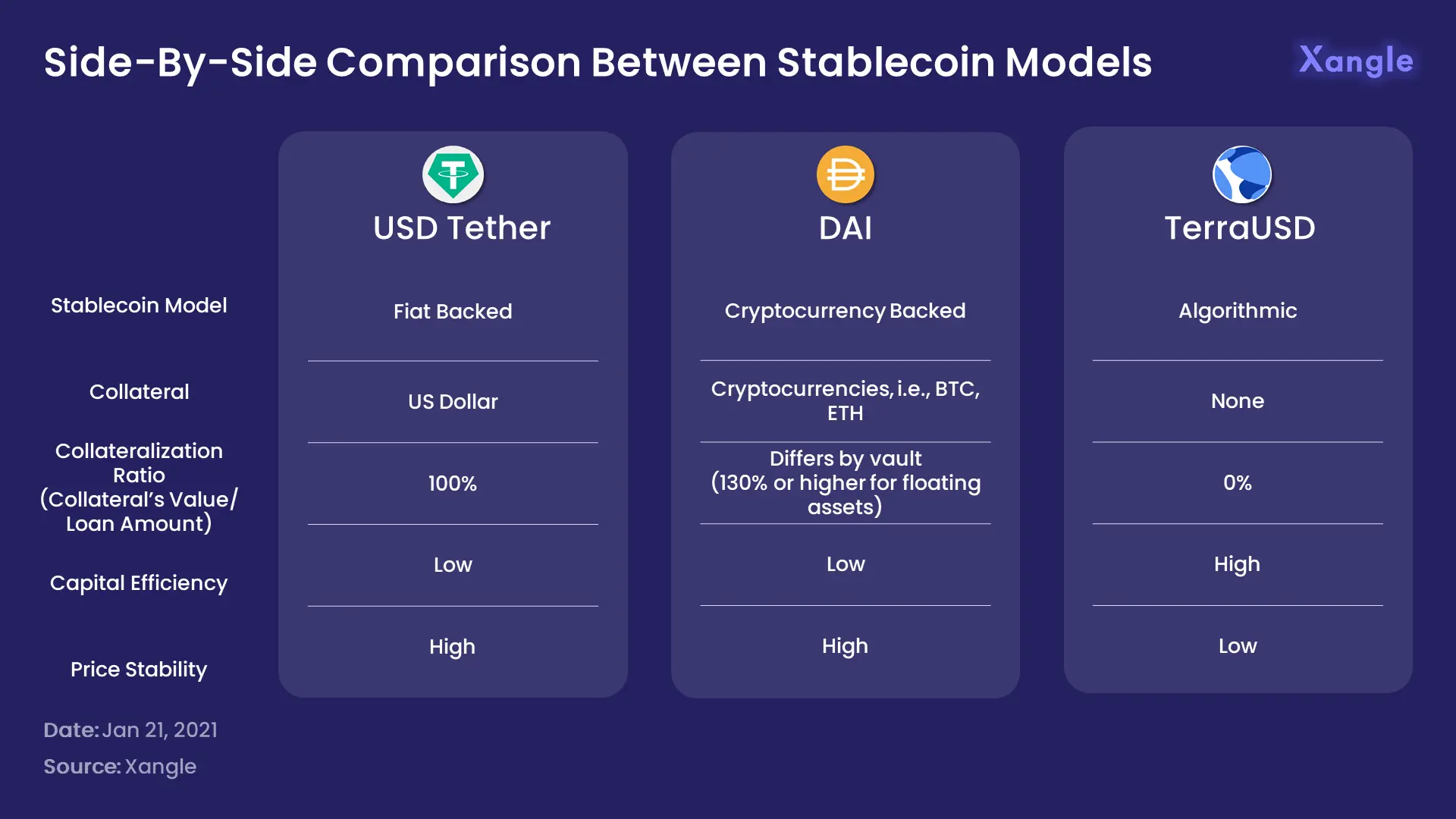

Asset-backed stablecoins can be largely divided into fiat-backed and cryptocurrency-backed stablecoins. Both types have in common that the stablecoins are issued upon receiving collateral that has a value equal to or greater than the value of the stablecoin. USDT and MakerDAO’s DAI respectively are representative of the fiat-backed and cryptocurrency-backed stablecoins.

USDT (USD Tether), a Fiat-Backed Stablecoin

USDT is a stablecoin issued by Tether. 1 USDT is pegged to the value of 1 USD and when a user deposits U.S. dollars into Tether, it issues USDT equivalent to the amount deposited. In other words, It has a mechanism where the collateralization ratio—the value of assets pledged as collateral divided by the value of issued stablecoins—is always maintained at 100% upon issuance of stablecoins.

And because Tether maintains the 1-to-1 ratio for USDT to USD, there is a window for arbitrage, which allows for stability in the price of USDT when its price becomes volatile. For example, if the price of USDT falls below 1 USD in the market, market participants can buy USDT in the market, exchange it for a fiat currency with Tether, and profit from the differences. Conversely, if the market price of USDT climbs above 1 USD, the user can profit from having USDT issued by Tether and sold in the market.

DAI, a Cryptocurrency-Backed Stablecoin

DAI is a stablecoin soft pegged to the USD, issued by MakerDAO, a decentralized loan platform. DAI is a cryptocurrency-backed stablecoin and MakerDAO users can deposit cryptocurrencies, such as ETH and WBTC, in the vault and issue DAI under a requirement of minimum collateralization ratio.

As the price of collateral constantly changes, stablecoins tries to secure price stability by automatically liquidating the collateral and returning the difference to the user when the collateralization ratio falls below the minimum collateralization ratio due to a price drop. It also promotes price stability in the same way as USDT, keeping the window open for an arbitrage opportunity.

Sub-conclusion 1: Price Stability at the Expense of Capital Efficiency

The asset-based model adopted by USDT and DAI achieves price stability and reserve adequacy by holding collateral equal to or greater than the value of the issued stablecoin. But there is a catch that deters its capital efficiency: the excessive collateral that is required to be maintained to have a stablecoin issued. In addition to the aforementioned assets, various other assets belong to either of the following two stablecoin models.

- Fiat-backed stablecoins: USDT, USDC, TUSD, GUSD, PAX, etc.

- Cryptocurrency-backed stablecoins: DAI, sUSD, RSV, VAI, etc.

Algorithmic Stablecoin

Algorithmic stablecoin is a model that attempts to achieve stability of the target price by using an algorithm—instead of collateral—to adjust the supply and demand of stablecoins. A successful algorithmic stablecoin model is the UST (TerraUSD) issued by the Terra network, which will be discussed more in detail in the following paragraph.

UST (TerraUSD)

UST is an algorithmic stablecoin developed by the Terra Network, a Layer 1 protocol. Specifically, anyone can swap UST for LUNA at the exchange rate of 1 UST for $1 worth of LUNA, the native staking and governance token of Terra. If UST hovers above or below the target price of 1 USD, there is always an arbitrage opportunity of LUNA-UST swap, which ensures price stability. During this process, LUNA is burnt when UST is minted and when UST is redeemed, LUNA is newly minted, algorithmically achieving price stability of non-volatile asset UST by adjusting the supply and demand of volatile asset LUNA.

Sub-conclusion 2: Capital Efficiency That Comes at the Price of Price Stability

The merit of algorithmic stablecoin models, such as UST, is the capital efficiency since the issuance does not impose a requirement of collateral. In the early stage of the launch of a stablecoin, however, it is difficult to secure utilities—the so-called bootstrapping, possibly exposing it to price volatility during the period. Moreover, the price can move even more radically due to the absence of collateral, again dampening its price stability. Apart from UST, there are other stablecoins as well that adopt an algorithm-based model.

- Algorithmic Stablecoins: UST, ESD, FEI, etc.

FRAX as a Compromise: Can It Write a New Chapter?

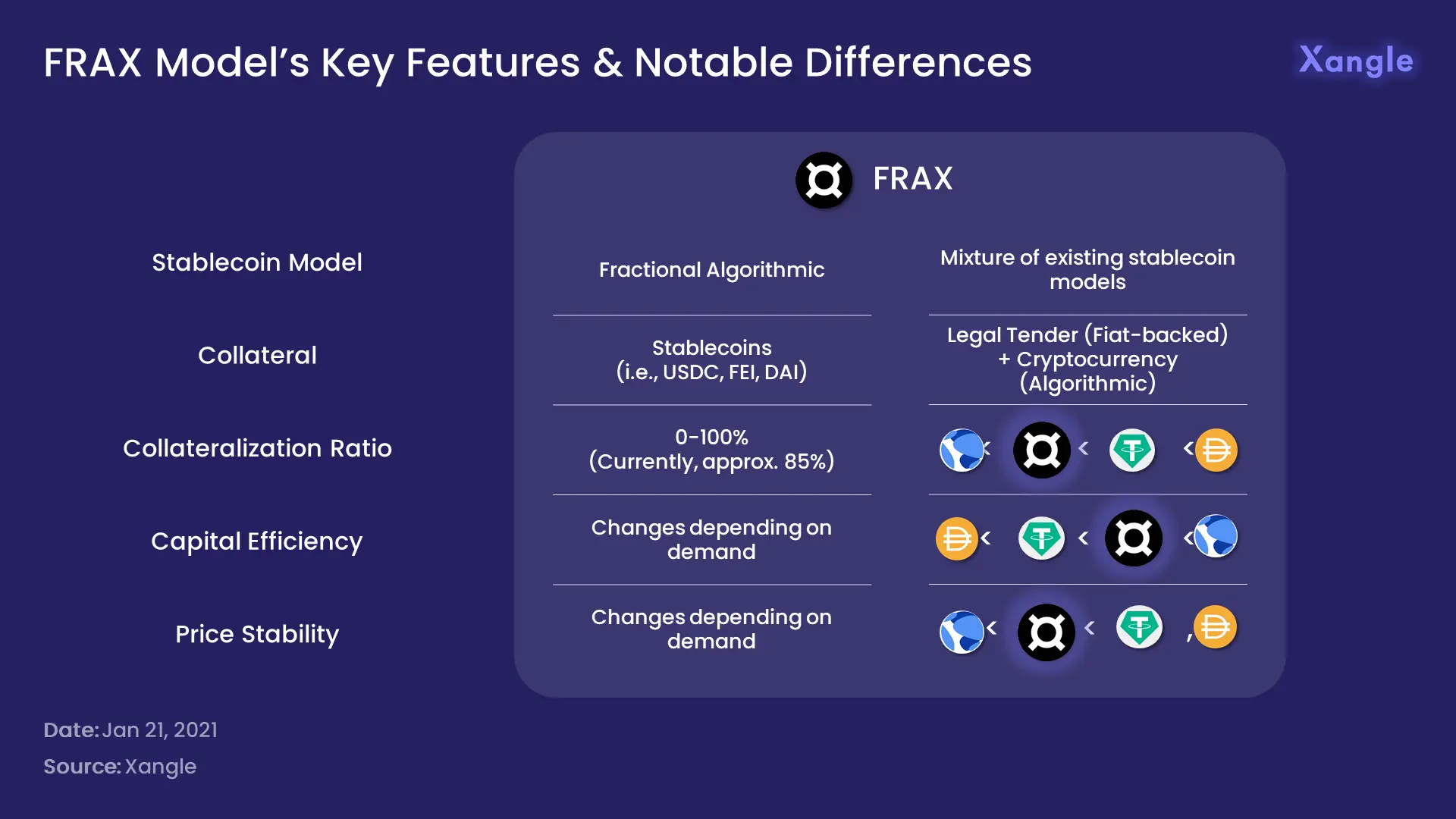

A Fixed-price, Cryptocurrency-Backed, Algorithmic Stablecoin

Frax Finance's stablecoin, FRAX, has adopted a so-called fractional algorithmic stablecoin system, that is, it is a partially algorithmic stablecoin. FRAX's price stabilization mechanism employs both asset-based and algorithmic models.

Initially, FRAX is issued at a 1:1 ratio using several stablecoins, including USDC, as collateral. In other words, it starts with an asset-backed stablecoin model with a 100% collateralization ratio, which is very much similar to USDT’s fiat-backed stablecoin model. Then, the Frax protocol tracks FRAX’s market price hourly, adjusting the collateralization ratio by 0.25%. If the price of FRAX is above $1, the market demand is judged to be high so the collateralization ratio is lowered. And if the price of FRAX is below $1, the market demand is judged to be low and the collateralization ratio is raised.

If the initial collateralization ratio set at 100% declines, the algorithm that burns an equivalent amount of governance token is put in place. This lowers the amount of stablecoins required to issue FRAX and instead, burns FXS (Frax Share), the governance token of Frax Finance. On the other hand, if FRAX is redeemed, collateral, such as USDC, is returned as per the collateralization ratio, and FXS is newly created according to the ratio that is left after the return of the collateral.

FRAX as a Reasonable Compromise

FRAX may look like a simple mixture of existing stablecoin models, but it is deemed a reasonable model in that it algorithmically maximizes capital efficiency upon expansion of demand while achieving price stability and reliability of the stablecoin by raising the collateralization ratio when there is a contraction in demand. As the collateralization ratio is adjusted on an hourly basis, arbitrage opportunities, such as Mint/Redeem and Buyback/ Recollateralization, are also open to prevent a radical price movement within a session, further stabilizing the price.

As was previously discussed in The Great Curve War, FRAX has grown rapidly by demonstrating a TVL growth of nearly $2 billion within a short period of time, ranking 20th in Defillama’s DeFi dApp TVL ranking. The collateralization ratio of Frax Finance, which has maintained a collateralization ratio of between 85-90% since its launch, currently stands at 84.25% as of Jan 20. As Frax Finance’s governance token FRAX is burnt upon issuance of FRAX according to a specific ratio, such decreasing supply has prompted the price of FXS to shoot up 7-fold in a short period of time (from $5.7 on Oct 20, 2021 to $41 on Jan 12, 2022).

It appears that FRAX's innovative model is gradually gaining market recognition as a reasonable compromise between an algorithmic stablecoin model with a zero-percent collateralization ratio, a fiat-backed stablecoin model with a 100-percent collateralization ratio, and a cryptocurrency-backed stablecoin model with a 130-percent-or-higher collateralization ratio. The complex and meticulous protocol designed by Frax Finance is one of the essential drivers of such steady growth. In my next article, I’ll take a look at Frax Finance’s protocol design.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.