Kaia: Building Asia’s On-Chain Capital Market With RWAs

1. The Structural Gap in On-Chain Capital Markets

2. Kaia’s TradFi-Native Approach to RWA Design

3. How Yield-8 Deploys Capital Into Real-World Assets

4. Conclusion: RWAs as the Entry Point to On-Chain Capital Markets

1. The Structural Gap in On-Chain Capital Markets

In recent years, the concept of “on-chain capital markets” has sat at the center of discussions around DeFi and RWAs. The narrative is straightforward: rebuilding traditional finance’s capital formation, asset management, and settlement functions on blockchain rails. For that narrative to become an actual market structure, three pillars are required: investable assets, a capital circulation layer that puts those assets to work, and users who actually use them. Assets are the market’s raw material; circulation is the engine that keeps capital moving; users are the destination where that capital ultimately lands. A market only functions when all three pillars are aligned.

Over the past few years, DeFi has rapidly built out the circulation layer among the three. Lending, deposits, liquidity provision, and leverage strategies have, for the most part, already been implemented on-chain. The asset pillar, however, remained empty for a long time. Most assets brought on-chain were crypto-native, and yields were generated from endogenous loops within the chain. The same structural limitation repeated itself: when liquidity entered the system, yields held up; when liquidity left, those yields faded with it.

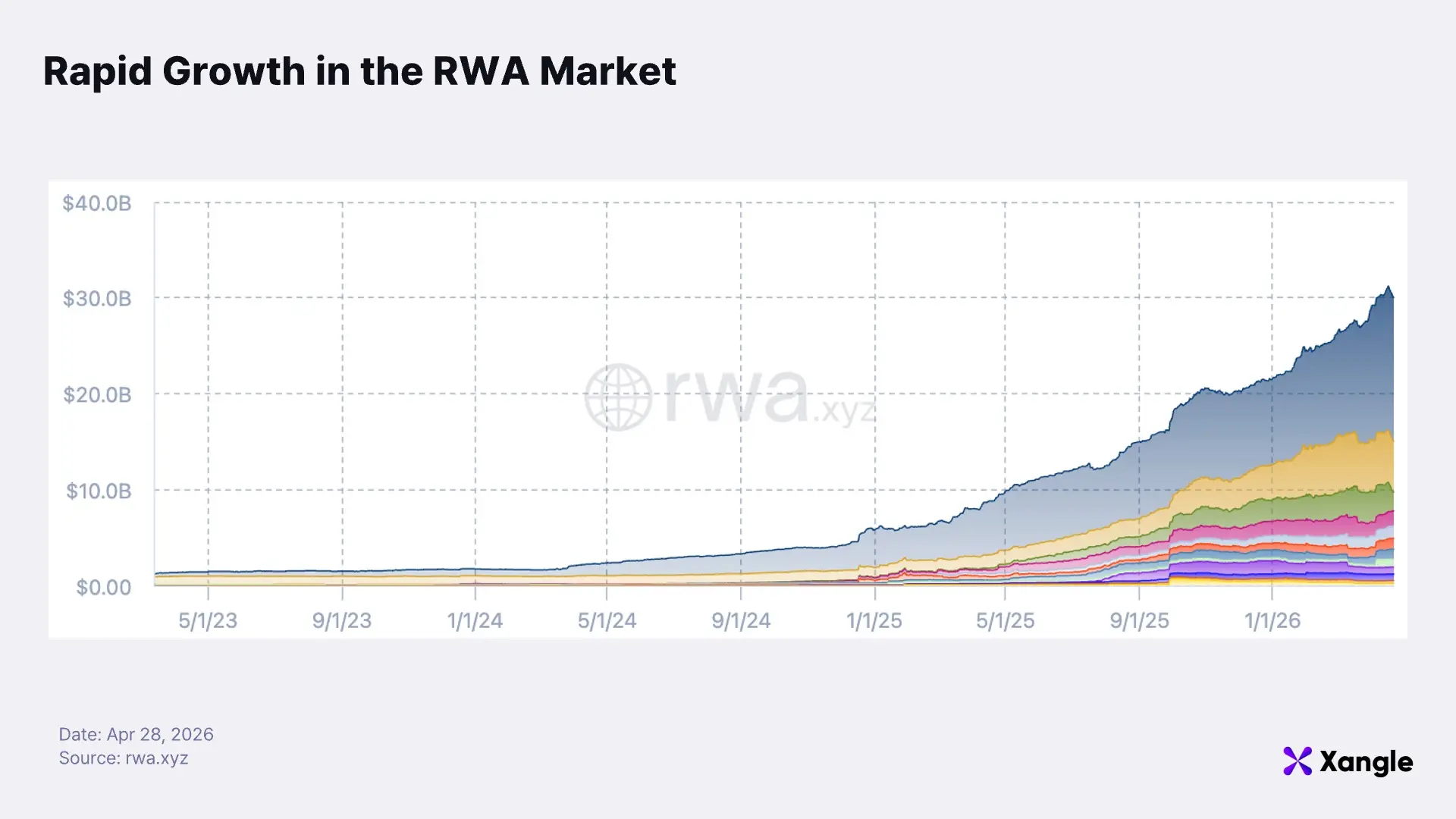

Against that backdrop, RWAs—real-world assets—came into focus. The approach is to tokenize real-world assets such as U.S. Treasuries, private credit, and real estate, then bring them on-chain. The assets reside on-chain, but the source of yield comes from the real economy outside the chain. In other words, the real asset pillar that DeFi’s circulation layer had long been waiting for is beginning to take shape. Market size has grown rapidly as well, with the RWA market surpassing $30 billion. Another notable development is that major traditional financial institutions such as BlackRock and Franklin Templeton have begun launching RWA products directly. RWAs have moved beyond the proof-of-concept stage; they have become a market where capital is actually flowing in.

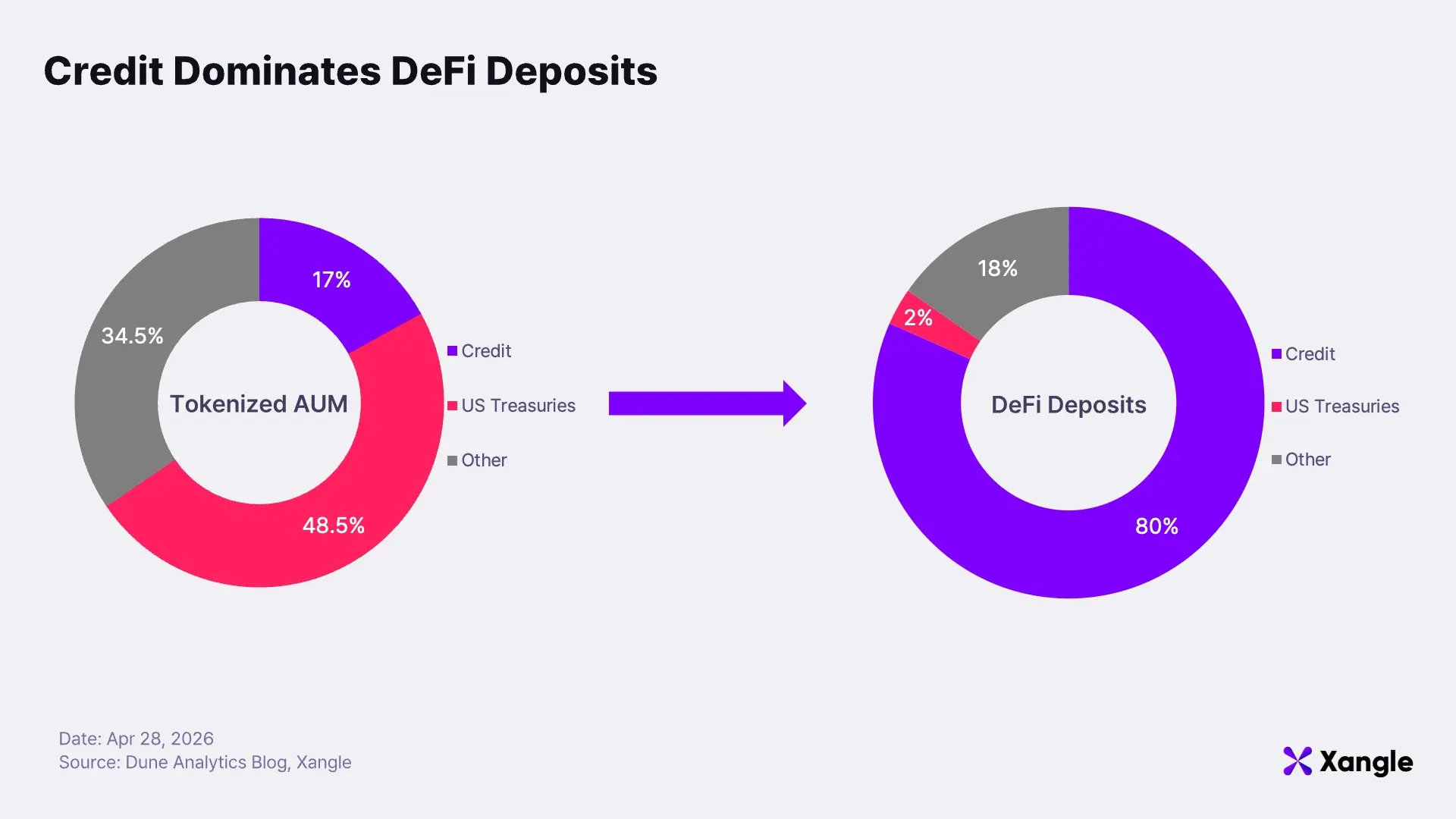

For all that growth, however, the underlying composition remains heavily skewed. The overall RWA market continues to expand, but assets actually used in DeFi as collateral, for leverage, or within yield structures amount to roughly $2.7 billion—only about 9% of the total is being meaningfully put to work on-chain. Composition matters even more. Looking only at tokenized assets overall, U.S. Treasuries account for roughly half of the market and represent the largest share, while private credit accounts for just 17%. Yet the picture flips entirely when looking at the assets actually used in DeFi. Among RWA assets used in DeFi, private credit accounts for 80%, while U.S. Treasuries account for only 2%. Despite the headline size of the RWA market, private credit is what is actually shaping on-chain capital markets.

The divergence points to where on-chain capital markets are headed. Low-yielding assets such as Treasuries may be tokenized, but they do not generate enough return to support the yield economics of DeFi’s leverage and collateral structures. Private credit, by contrast, offers higher yields and remains an area with significant liquidity constraints even in traditional finance. When combined with on-chain collateral, leverage, and distribution structures, it can unlock tangible value. Private credit, in that sense, is the asset class that can play a functional role in on-chain capital markets.

Yet the private credit segment has its own gap. Most private credit used in DeFi today consists of assets distributed through U.S.- and Europe-based platforms such as Maple Finance, while RWA products tied to Asia’s real economy remain scarce. The rails for bringing those assets on-chain have not yet been built. Demand for DeFi-compatible RWAs is clear, and Asia has a broad financing gap that private credit could fill; the connective layer between the two, however, remains underbuilt. For Asia’s on-chain capital market to take shape, the asset pillar must be filled first.

2. Kaia’s TradFi-Native Approach to RWA Design

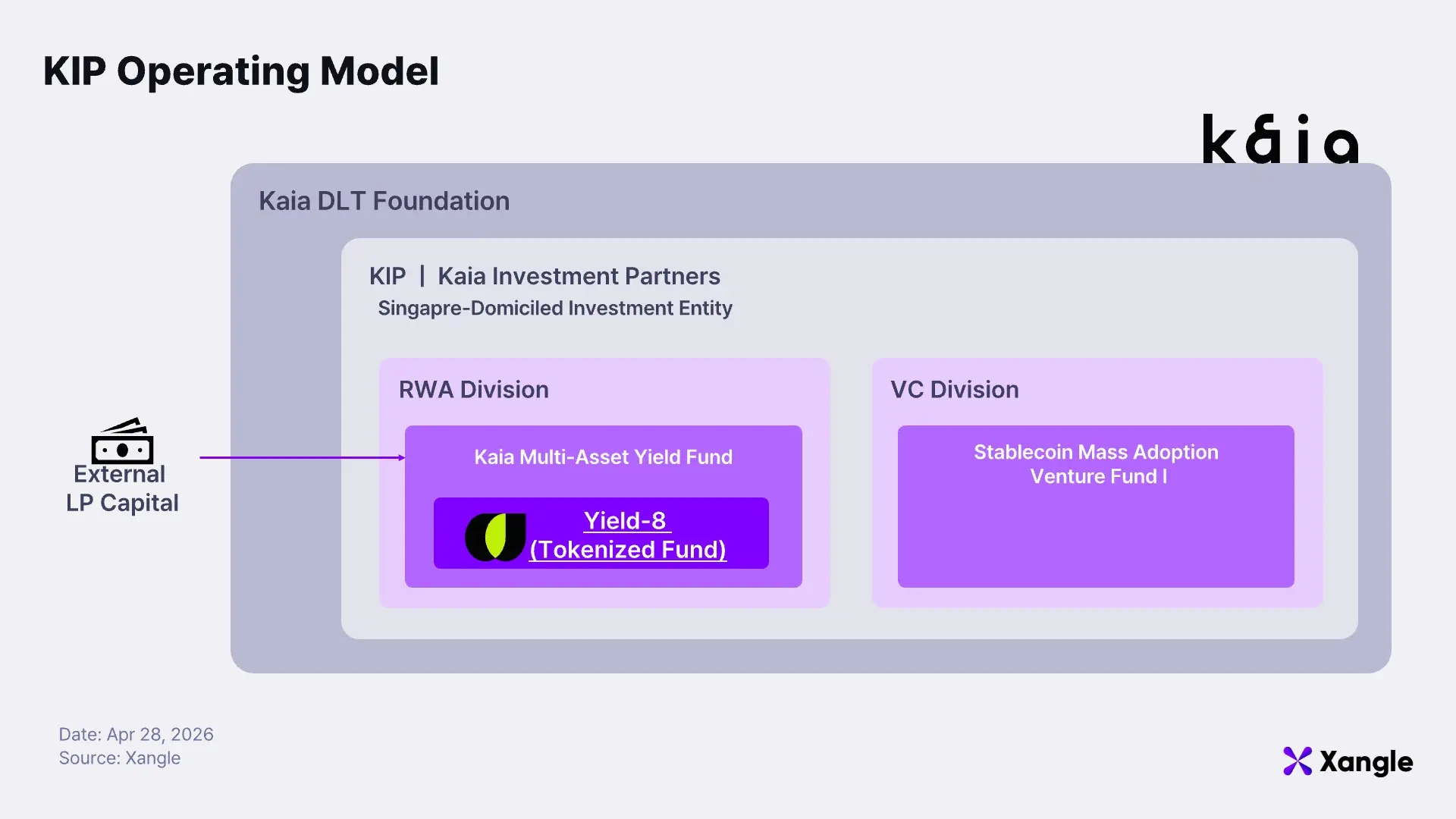

Kaia offers one of the clearest examples of how this gap can be addressed. Kaia’s ambition is to build Asia’s on-chain capital market, and RWAs are the mechanism for filling the asset pillar in that buildout. As discussed above, on-chain capital markets require three pillars—assets, circulation, and users—to work in tandem. Kaia already has access to a user base anchored by KakaoTalk and LINE, Asia’s largest messenger platforms, and it is also building out DeFi protocols on its chain. One pillar remains: assets. For Kaia’s envisioned capital market to become an actual structure, assets that generate yield from the real economy outside the chain must come on-chain. KIP, or Kaia Investment Partners, is the vehicle Kaia established to build that asset pillar.

2-1. KIP: Applying the TradFi Asset Management Playbook to RWAs

Layer 1 blockchains have generally followed a similar playbook in scaling their ecosystems: allocate native tokens for developer grants, use liquidity incentives to attract deposits, and bring in users with marketing rewards. The model worked for early-stage expansion, but its limitations were clear. Ecosystem growth depended heavily on token prices and foundation treasuries; structural access for external capital remained limited. Once the market cycle turned, foundations inevitably had less room to deploy capital.

Kaia chose a different path for RWAs. Rather than expanding its ecosystem around token incentives, Kaia is bringing the asset management structure of traditional finance on-chain. The sequence is as follows: 1) establish an investment entity that can accept external capital within Singapore’s regulatory framework; 2) structure yield-bearing assets tied to Asia’s real economy into fund products; and 3) tokenize those products into instruments that can circulate on-chain.

The flow—sourcing assets, packaging them into funds, and offering them to investors—resembles the operating model of a traditional asset manager. The difference is where the final product circulates: on blockchain rails. KIP sits at the center of that structure. Kaia established KIP as a separate investment entity in Singapore. KIP is a wholly owned subsidiary of the Kaia DLT Foundation, but its role differs from the foundation’s existing operating model. Rather than expanding the ecosystem by relying on the foundation treasury, KIP is built to receive external LP capital—capital from limited partners—and manage it within a separate investment structure.

The legal structure was also designed around external capital formation. KIP operates under Singapore’s VCC, or Variable Capital Company, structure. The VCC is a legal form widely used in global fund management; the accounting, audit, and due diligence systems required for raising external capital and operating funds are already institutionalized within that framework. In other words, before issuing RWA products, Kaia first built the legal and operational foundation needed to house them.

KIP is divided into two divisions. The VC division invests in the infrastructure needed to expand the stablecoin ecosystem. Its focus areas include payment infrastructure, on/off-ramp infrastructure, yield protocols, and compliance solutions—the foundational components required for stablecoins to circulate in practice. The RWA division structures Asian real-world assets into fund products and tokenizes them into products that can be issued repeatedly. One division builds the distribution infrastructure; the other supplies the assets to be brought on-chain.

Most importantly, KIP has already moved beyond planning and into execution. It is in discussions with major financial institutions in Hong Kong on the tokenization of floating-rate notes, while also actively building additional pipelines, including RWA tokenization collaboration models with Korean financial institutions. For KIP’s envisioned issuance cycle to work in practice, however, it must prove more than a one-off asset tokenization. The full flow must be validated: the product reaches users, generates yield, and capital is recovered. Yield-8 is the first attempt to prove that cycle.

2-2. Yield-8: Kaia’s First Tokenized RWA Fund

Yield-8 is a tokenized fund issued against the value of the Kaia Multi-Asset Yield Fund, a private fund managed by KIP’s RWA division. Its structure brings multiple yield-bearing assets together into a single fund and distributes that exposure in tokenized form. By holding Yield-8 tokens, users gain exposure to the returns generated by the fund’s full underlying asset portfolio.

Yield-8 targets the private credit market. It seeks an annual yield of more than 8%, with a particular focus on assets tied to Asia’s real economy. Private credit is currently the segment where RWA demand in DeFi is most concentrated, yet Asia-based products remain largely absent. Demand for DeFi-compatible RWAs is clear; Asian assets capable of absorbing that demand, however, have not been sufficiently tokenized. Yield-8 is designed to target that gap.

The key point is accessibility. Private credit has traditionally been difficult to access unless one is a large institution or professional investor, precisely because its yields are attractive. Product sizes are large, distribution takes place over the counter, and disclosure standards differ by asset manager—all of which create high barriers to entry for ordinary investors. Yield-8 lowers those barriers by bundling such assets into a single fund, tokenizing the fund, and distributing it on-chain. In effect, it opens access to a market that had previously been restricted.

Access alone, however, is not enough. When private credit comes on-chain, the biggest risk is not yield but opacity. Token issuance itself is not technically difficult. If it remains unclear which real assets the token is linked to, who manages those assets, and how they are legally protected, the token becomes little more than an instrument that trades on price without real backing from the underlying assets. For users to deposit and use it as collateral in DeFi, the market must be able to verify that the token is backed by real assets—and that those assets remain protected even in cases of default or dispute.

Yield-8 addresses that issue by stacking two verification frameworks: one from traditional finance, and one from on-chain infrastructure. The underlying fund is a formally registered private fund in Singapore and follows traditional financial standards for fund administration, accounting audits, and anti-money laundering controls. The tokenization layer built on top of it is executed within a separate regulatory sandbox; external security audits are applied to both the smart contracts and the bridge. Since the two verification systems are delegated to specialized parties in their respective domains and operate independently, Yield-8 sits at the intersection of TradFi and on-chain finance.

Further improvements are also planned on the transparency front. Kaia and KIP are preparing a transparency dashboard that will allow users to check the fund’s mark-to-market valuation, portfolio weights, and real-time APR directly on-chain. The core concept is “Always-On NAV.” Many existing RWA products have been tokenized without providing sufficient visibility into how the underlying assets are managed; Kaia and KIP aim to address that limitation by disclosing operational data on-chain. The dashboard is scheduled to launch in the first half of 2026.

3. How Yield-8 Deploys Capital Into Real-World Assets

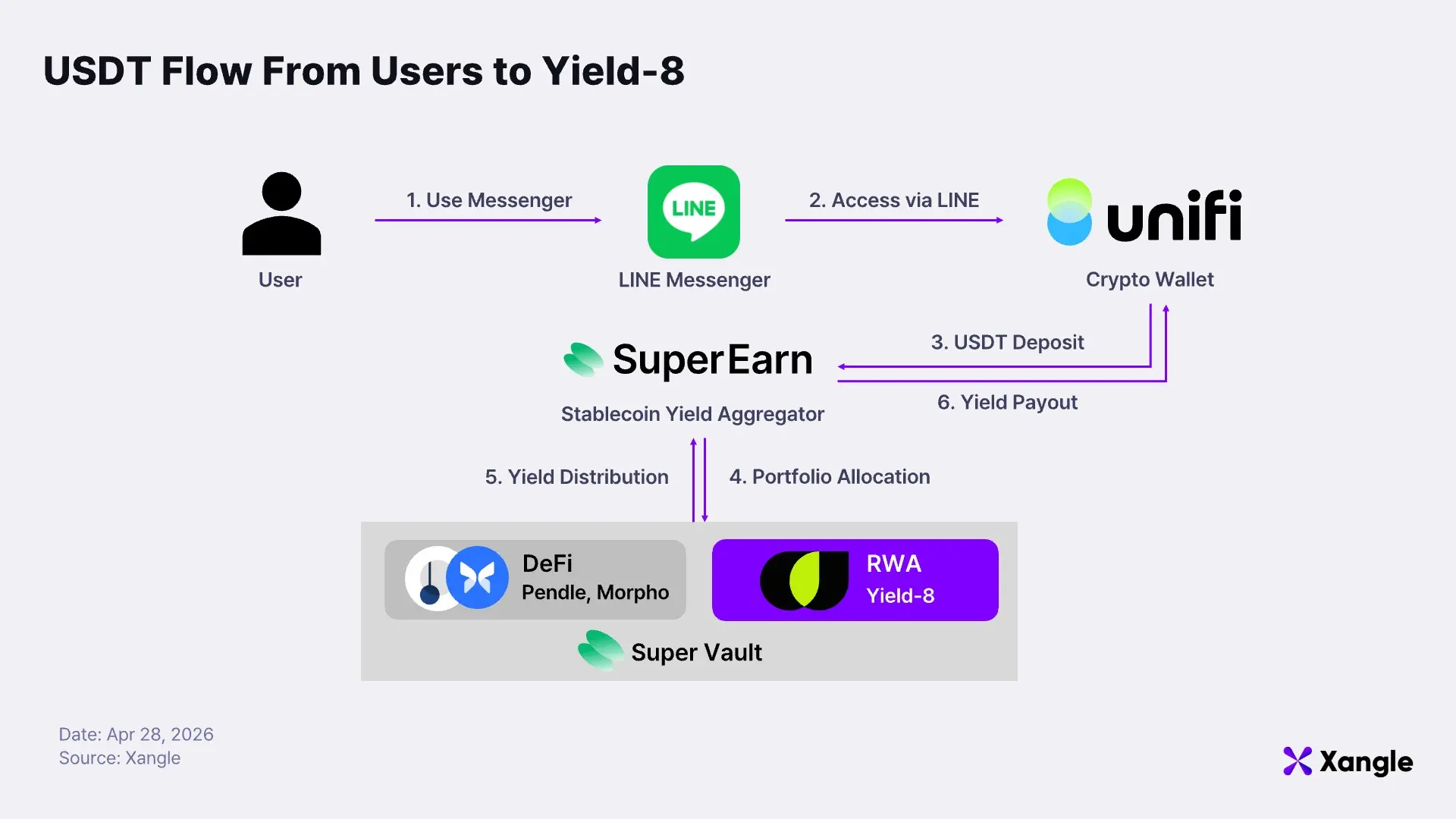

Before examining which assets Yield-8 invests in, it is worth first looking at how the product reaches users. User capital reaches Yield-8 through several interface layers.

From the user’s perspective, the experience is a single user-facing interaction: depositing USDT inside a messenger app and receiving yield. Behind the scenes, however, four interfaces are connected and operate together. The important layer here is SuperEarn. SuperEarn provides Super Vault, a service that combines and manages multiple on-chain stablecoin yield sources. Yield-8 is included as part of the Super Vault portfolio, so a portion of the USDT deposited by users is exposed to the returns generated by Yield-8’s RWA strategy after passing through SuperEarn’s risk management and asset allocation process.

Which RWA assets, then, does Yield-8 invest in Yield-8 currently allocates capital to three RWA assets. Galactica represents the largest allocation at 35%, followed by YieldCore and Forest Jalan at 25% each. The remaining 15% is held in USDT to support user redemptions and maintain liquidity. All three assets fall under the broader category of Asian private credit, but each operates in a different market.

3-1. Galactica: Tokenized Ship Financing in Indonesia

Indonesia is an archipelago made up of thousands of islands, which makes ships a critical part of its logistics infrastructure. Maritime transport accounts for an overwhelmingly large share of not only imports and exports, but also domestic freight movements. The problem is that ship financing has not kept pace with that demand. Ships are high-value assets that can cost from several billion to tens of billions of won, making it difficult for shipowners to purchase them with equity capital alone. The standard structure is typically an LTV-based model: bank loans finance 50–60% of the vessel’s value, while the remainder is covered by equity or other funding sources. In Korea, Japan, and the United States, this lending structure is well developed, allowing shipowners to raise capital relatively easily. Indonesia is different. The local fleet is largely centered on small coastal transport vessels, which makes standardized valuation difficult; credit information on shipowners is also limited, leaving traditional banks reluctant to underwrite the segment aggressively. Clear financing demand exists, yet the funding rails capable of absorbing that demand have remained weak. Galactica starts from this demand-supply mismatch—and aims to resolve it through tokenization.

Galactica is structured as a joint venture between Kaia and Indonesian shipping company PT Pelayaran Korindo. PT Pelayaran Korindo is a major shipping company with roughly 50 years of operating history, bringing both in-house fleet operating experience and a local shipping network. The division of roles is clear: Kaia handles token issuance and external capital connectivity, while Korindo is responsible for actual vessel operations and local execution.

Galactica has completed two funding rounds so far, both of which were successfully raised. The first issuance, Pegasus 1, was deployed into short-term bridge financing for MT Danaputri 1, a $25 million LNG vessel. The second issuance, Pegasus 2, was a $1.5 million deal used to support fleet operation expansion for an Indonesian shipping company. Both issuances were conducted through InvestaX, a licensed platform operating under the supervision of the Monetary Authority of Singapore, or MAS, and were therefore executed within a formal regulatory framework. In other words, Galactica is not a one-off pilot; it is validating market demand while refining its issuance structure into a repeatable model.

Galactica’s significance goes beyond a simple shipping investment. Its return base comes from cash flows generated by long-term, fixed-rate lease contracts, making it a stable asset that is separated from crypto market volatility. Physical vessels also serve as collateral, giving it relatively high collateral quality even among private credit products. Most importantly, Galactica is directly connected to the real logistics flows of Indonesia’s regional economy. Among Kaia’s RWA assets, it is the clearest expression of Kaia’s narrative: bringing Asia’s real economy on-chain.

3-2. YieldCore: Short-Term Financing for South Korean Gas Stations

YieldCore targets the specific funding structure of South Korea’s gas station market. Gas stations typically operate by receiving fuel from refineries first, selling that fuel, and settling payment afterward. A time lag therefore exists between inventory procurement and the collection of sales proceeds. Under normal conditions, gas stations can bridge that gap without much strain using their own capital and predictable sales volumes. When oil prices surge or fuel sell-through slows, however, the situation changes. Inventory remains on hand, but payment settlement dates stay fixed; temporary funding shortfalls can emerge as a result. Gas stations consistently generate short-term financing demand to bridge these gaps, yet the segment has been difficult for traditional banks to underwrite as a dedicated lending market: revenue turns over quickly relative to asset size, and collateral valuation can be complex.

The demand has become even more visible as risks around the Strait of Hormuz have recently increased. South Korea relies on the Middle East for roughly 70% of its crude oil imports, and more than 95% of those imports pass through the Strait of Hormuz. Instability in the Middle East raises crude procurement costs, which can translate into higher gasoline and diesel prices. When prices rise, consumers cut back on refueling volumes, and gas station inventory sells through more slowly. Sales proceeds are collected later, but payments to refineries must still be made on the agreed settlement dates. The gap creates short-term working capital demand for gas stations. YieldCore supplies the short-term capital needed to fill it.

YieldCore tokenizes short-term gas station loan assets and converts them into a structure that external investors can participate in. Investor capital is deployed first to settle the payables that gas stations owe to refineries, and the gas stations repay principal and interest within three months. The resulting loan receivables are incorporated into the Yield-8 fund in tokenized form, allowing users to gain indirect exposure to the returns from these loans through Yield-8. Repayment stability is secured through a dual-collateral structure: the primary collateral is the gas station’s future sales, while real estate is added as secondary collateral. A Korean securities firm also participates through a trust structure, managing the flow of funds. The first issuance was $500,000 in size; a $900,000 issuance is currently underway, with the structure gradually scaling.

YieldCore’s significance lies in converting an off-chain asset, short-term financing for gas stations, into part of an on-chain yield product accessible to general users. Previously, the loan receivables were handled only between financial institutions and gas stations. Once incorporated into the Yield-8 portfolio, however, general users can gain indirect exposure to their returns. YieldCore is therefore an example of bringing cash flows from Korean commercial finance into an on-chain yield structure.

3-3. Forest Jalan: MSME Working Capital and Earned Wage Access in Indonesia

Forest Jalan targets two markets in Indonesia: working capital financing for MSMEs and EWA, or Earned Wage Access, for workers. It provides merchants with working capital that is repaid based on daily sales, while giving workers early access to wages they have already earned. In particular, EWA is not a loan. It is a non-debt product that allows workers to receive an already accrued wage claim ahead of the normal payday, making it structurally distinct from microloans.

In an economy like Indonesia, where self-employment and informal labor account for a large share of the workforce, funding demand across both segments is widespread. Yet despite clear demand, the existing financial system has not supplied this capital effectively. The problem lies in the absence of credit underwriting data. Many small merchants in Indonesia do not have organized financial statements or tax records, and many workers lack sufficient banking histories. Traditional bank underwriting models had no way to assess their creditworthiness, which meant that lending often could not take place at all. Informal short-term lending markets filled the gap, but excessive fees and interest rates repeatedly became a problem. Wage advance services also existed, but on an effective interest rate basis, they often imposed a significant burden on borrowers.

Forest Jalan addresses this problem with AI-based credit assessment built on platform data. By partnering with Grab and job platform JOOB, it gains access to a pool of roughly 28,000 businesses and about 850,000 workers. Based on merchant payment volumes, hiring activity, and labor data, Forest Jalan assesses merchant creditworthiness as well as workers’ employment and income continuity. The starting point for underwriting is directly observable first-party data, such as payment gateway transactions, wage payment records, and hiring activity. Forest Jalan then layers AI-based assessment on top of that data to infer signals that individual data points alone cannot capture, including revenue stability and continuity of employment and income. As transactions accumulate, assessment accuracy becomes increasingly refined. Forest Jalan’s core competitive strength lies in expanding both the breadth of observable data and the depth of its inference model.

Once underwritten, the assets are tokenized and incorporated into the Yield-8 fund, allowing users to gain indirect exposure to their returns through Yield-8. Merchant working capital is recovered through an automatic repayment structure based on daily sales, while Earned Wage Access operates by allowing workers to receive a portion of wages they have already earned in advance. Although the data is limited to the pilot period, Forest Jalan recorded a 0.2% default rate on MSME working capital and a 0% non-recovery rate for Earned Wage Access. The results suggest that platform data-based underwriting can function as an alternative credit signal.

The logic connecting these three assets becomes clear here. Galactica, YieldCore, and Forest Jalan differ by industry and geography, but they are all based on credit demand in Asia that traditional finance has not sufficiently served. Ship financing, short-term gas station financing, and microfinance may appear to be separate markets, but they share the same underlying structure: recurring cash flows generated from the real economy and credit premiums that the formal financial system has not fully priced. Yield-8 bundles these assets into a single portfolio and converts them into an on-chain yield product accessible to general users.

Yield-8 is not the end state, but the starting point. It is the first product in Kaia’s Onchain Yield ETF series. The portfolio is expected to expand to more than 10 assets going forward, and the next product is targeting launch in Q2 2026. Under this structure, Kaia aims to continuously turn cash flows from Asia’s real economy into on-chain assets and build a capital market that issues, manages, and distributes them.

4. Conclusion: RWAs as the Entry Point to On-Chain Capital Markets

Kaia’s RWA structure is clearly distinct from a one-off pilot. By establishing KIP as a standalone investment entity under Singapore’s VCC framework, Kaia created a pathway for external capital to enter the ecosystem. It then layered Yield-8, its first product, on top of that structure, building an issuance framework that can be verified across both traditional finance and on-chain infrastructure. Rather than designing a single isolated project, Kaia has built an operating model premised on continuous issuance within a unified system.

The significance of Kaia’s RWA approach lies in the fact that the gaps identified at the beginning of this report are now being addressed in practice. The biggest limitations of the existing RWA market were twofold: assets were heavily concentrated in U.S. Treasuries, and even when tokenized, many of those assets were not meaningfully used in DeFi. Kaia targets both gaps at the same time. It has tokenized Asia-based real-economy assets across shipping, gas stations, and microfinance within the private credit segment, while also connecting those tokens to a distribution path where they can generate real yield through SuperEarn.

While other RWA projects compete over liquid, easy-to-tokenize assets, Kaia is moving into areas that traditional finance has either failed to reach or failed to serve sufficiently. Rather than treating tokenization itself as the end goal, Kaia uses on-chain capital markets to address inefficiencies in the real economy. In that sense, its approach is closer to the core purpose of on-chain capital markets. The model is backed by strengths that are unique to Kaia. An Asia-wide messenger user base of 250 million people can function as a practical distribution channel for RWAs, while Kaia is also pushing forward with the onboarding of Asian local-currency stablecoins such as JPYC and Korean won stablecoins. RWA is the starting point. From there, Kaia’s broader vision is to build an on-chain capital market where asset issuance, distribution, and payment infrastructure are integrated within a single ecosystem.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article was written at the request of Kaia. All content in this article was written independently by the author(s), and neither CrossAngle nor Kaia had any editorial control or influence over the content. The author(s) may hold the cryptocurrencies mentioned in this article at the time of writing.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.