KRW Stablecoins: Beyond Legislation—Distribution and Usage

Introduction

1. Stablecoin Institutionalization Trends

2. Circulation and Connectivity as the Core: Why Orchestration Matters

3. Requirements for an Orchestration Layer

4. Kaia as the Orchestration Layer for Stablecoins

5. Conclusion

Introduction

Discussions around a KRW stablecoin are gaining momentum rapidly. Yet in Korea, the dominant questions remain narrowly focused: who will issue it, and under what reserve structure and supervisory framework. The issuing entity, reserve assets, regulatory authority, and institutional alignment are clearly important. However, these questions alone are not sufficient to explain where a KRW stablecoin’s real competitiveness will come from.

In global markets, the value of stablecoins is defined less by issuance itself and more by what follows: circulation, connectivity, and real usage. Even if issuance is permitted, a KRW stablecoin that remains confined to a supplementary domestic payment role offers limited incentive to replace existing financial infrastructure with a tokenized system. Its value as a new payment and settlement infrastructure emerges only when it expands into areas where traditional systems have been structurally inefficient; cross-border remittances, global payments, and on-chain FX. Jurisdictions that have already allowed issuance have moved into this phase. The competitiveness of a KRW stablecoin will be determined not at issuance, but in how effectively it achieves distribution and connectivity.

The core constraint lies in coordination. Expansion across multiple currencies and payment channels cannot be realized without a structure that can orchestrate them into a single flow. That structure is the orchestration layer. For a KRW stablecoin to function as real infrastructure, the requirements of this layer must be defined first. This report examines global and domestic regulatory trajectories, and outlines why Kaia is the most suitable orchestration layer for a KRW stablecoin, based on three key requirements and supporting empirical cases.

1. Stablecoin Institutionalization Trends

1-1. Major Jurisdictions Enter the Circulation Phase

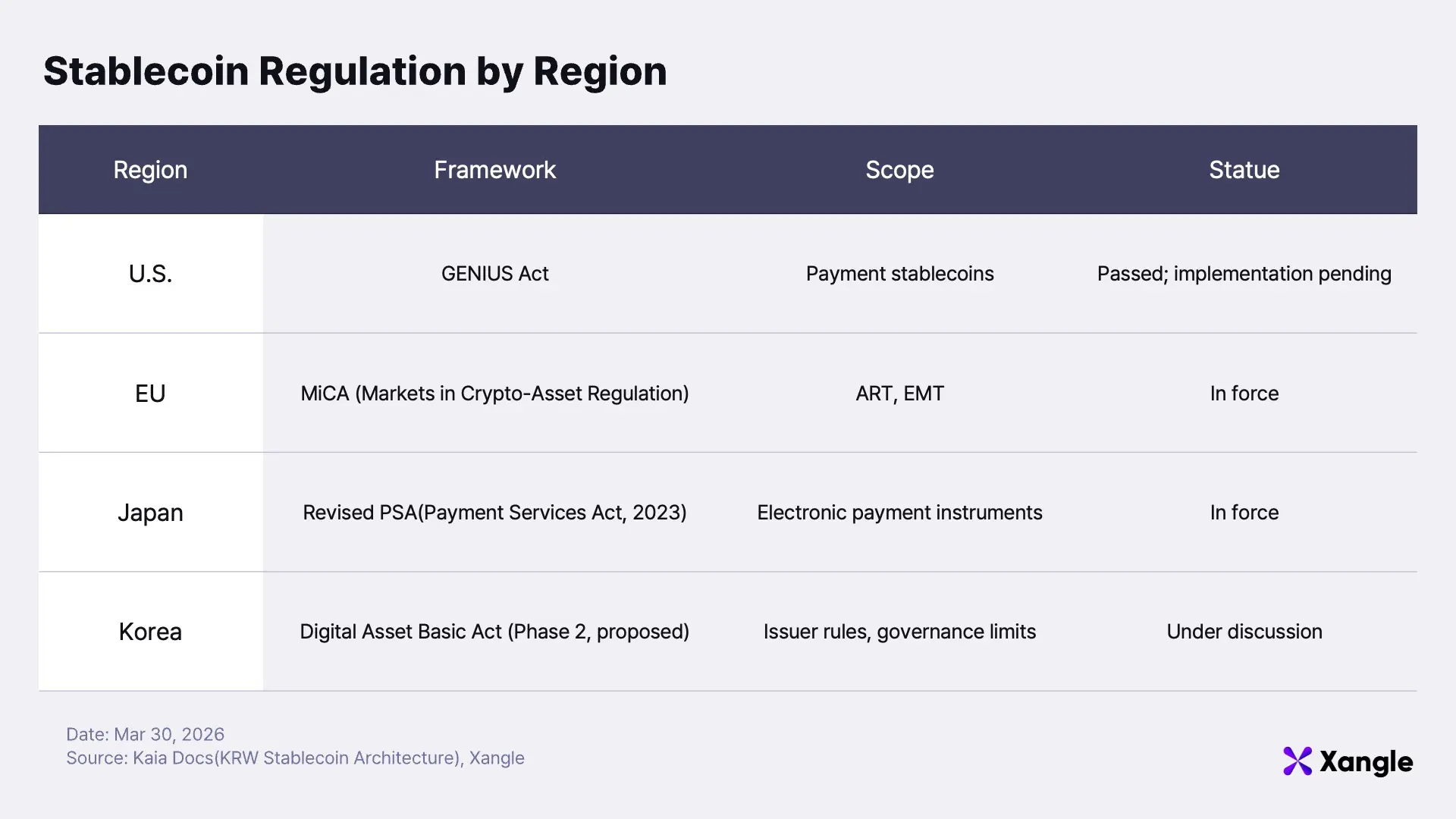

Until just a few years ago, how to approach stablecoins remained one of the more difficult questions for regulators to resolve. Allowing privately issued digital dollars or euros was not a trivial decision; it carried direct implications for the existing monetary order and financial system. The market, however, did not wait. Dollar-denominated stablecoins such as USDC and USDT expanded rapidly despite regulatory uncertainty, prompting authorities to shift toward bringing them within formal regulatory frameworks.

The United States provides the clearest articulation of this shift. The GENIUS Act establishes both the eligible issuers of stablecoins and the conditions under which issuance is permitted; its core focus lies in reserve asset composition and the criteria for licensing. The European Union, through MiCA (Markets in Crypto-Assets Regulation), has defined token categories and formalized issuance approval, reserve requirements, redemption rights, disclosure obligations, and supervisory frameworks. Japan has taken a more conservative approach, revising the PSA (Payment Services Act) to classify stablecoins as electronic payment instruments while restricting eligible issuers.

With regulatory direction becoming clearer, market adoption has accelerated. In the United States, USDC has begun integrating into card payment rails through settlement pilots with Visa and banks; card transactions can now be settled in dollar-denominated stablecoins behind the scenes. PayPal’s PYUSD is already being used for peer-to-peer transfers and online merchant payments. In Europe, EURC has been deployed in on-chain card settlement through partnerships with Wirex and Visa. In Japan, JPYC is circulating across multiple public chains and is expanding its use cases, including a planned integration with the LINE messenger.

A clear pattern emerges. Once issuance is permitted, the immediate focus shifts to designing circulation and connectivity. Issuance is not the end objective; integration into real payment, remittance, and settlement channels is. The key question is no longer whether stablecoins can be issued, but which ones can secure broader distribution channels and meaningful usage.

1-2. Korea: Regulatory Framework Still in Progress

In contrast, Korea remains at a stage where the institutional framework itself is not yet fully established. The Act on the Protection of Virtual Asset Users currently in force focuses on user asset protection and the prevention of unfair trading practices. It does not address who should issue a KRW stablecoin, how redemption should be structured, or how it should circulate. These issues are intended to be formally addressed in the proposed Digital Asset Basic Act, commonly referred to as the second-phase legislation. The bill outlines conditions such as minimum statutory capital requirements for issuers, full segregation of reserve assets at a ratio of at least 100%, and issuance authorization based on coordination among relevant authorities.

At the same time, the discussion has grown increasingly complex. As of March 2026, consultations are ongoing among the Digital Asset Task Force, financial authorities, and the Bank of Korea over issues such as the “51% bank ownership rule,” which would effectively position banks as the primary issuers, as well as restrictions on major shareholders of exchanges. The debate has moved beyond whether issuance should be permitted to how much authority should be granted, and to whom; negotiations remain ongoing.

Caution is clearly warranted. However, an exclusive focus on these issues risks sidelining a more fundamental question. Defining the issuing entity does not, in itself, ensure that a KRW stablecoin will see real usage. At a time when global markets are already experimenting with post-issuance circulation and usage, the discussion must expand beyond legal design; it should also address where and how a KRW stablecoin can be deployed in practice.

2. Circulation and Connectivity as the Core: Why Orchestration Matters

2-1. Beyond Domestic Payments: The Cross-Border Opportunity

A KRW stablecoin has the potential to improve the efficiency of existing infrastructure even in domestic payments and settlements. Connecting issuance, transfer, and settlement into a single on-chain flow reduces intermediary processes and simplifies settlement. Its full potential, however, becomes more evident when extended beyond domestic use into areas that require coordination across multiple currencies and payment channels, such as cross-border remittances, international payments and settlement, and on-chain FX. If a KRW stablecoin remains confined to a supplementary domestic payment role, the incentive to replace existing financial infrastructure with a tokenized system remains limited. From this perspective, the core of a KRW stablecoin lies not in issuance itself, but in its circulation and connectivity structure.

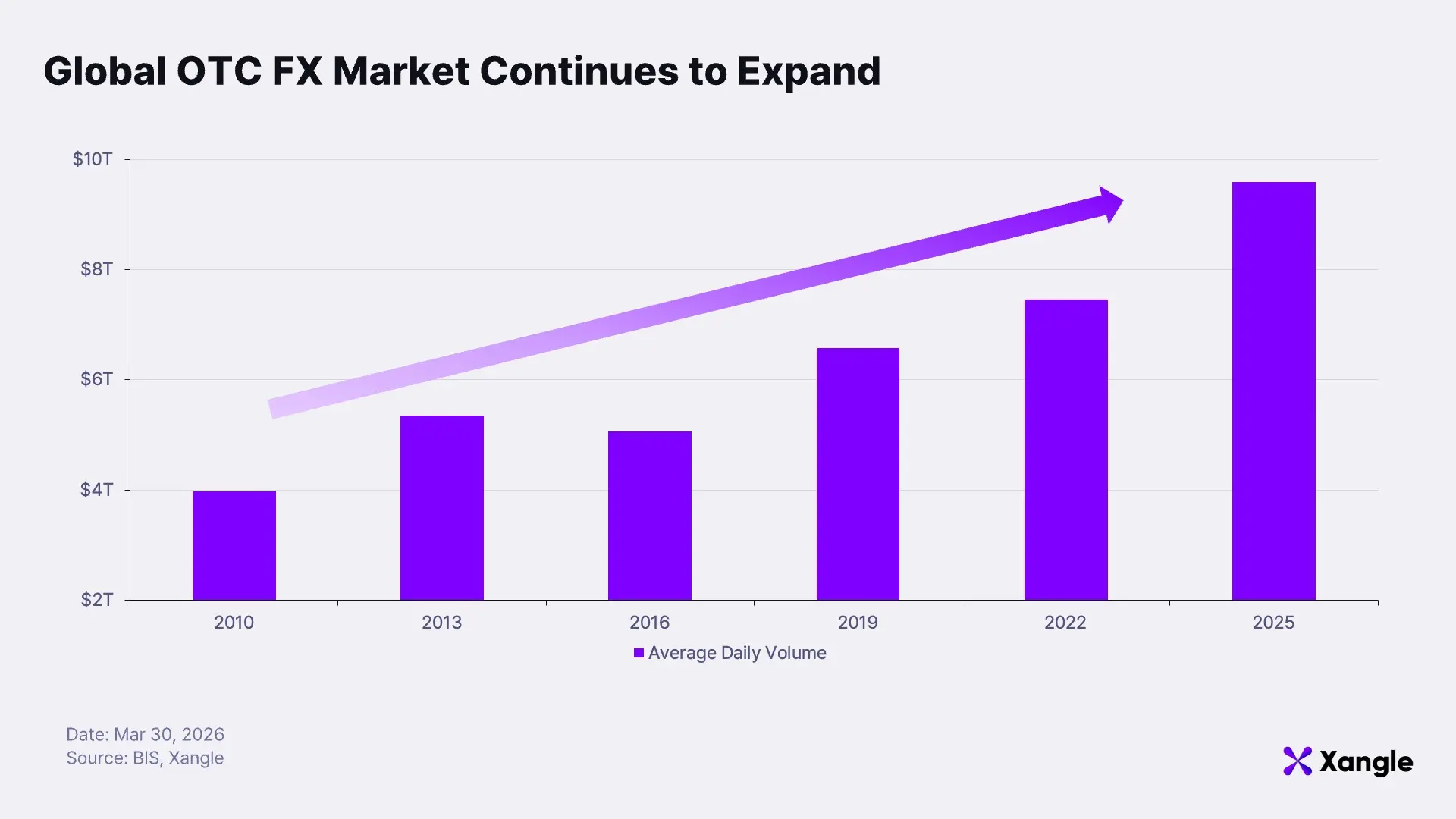

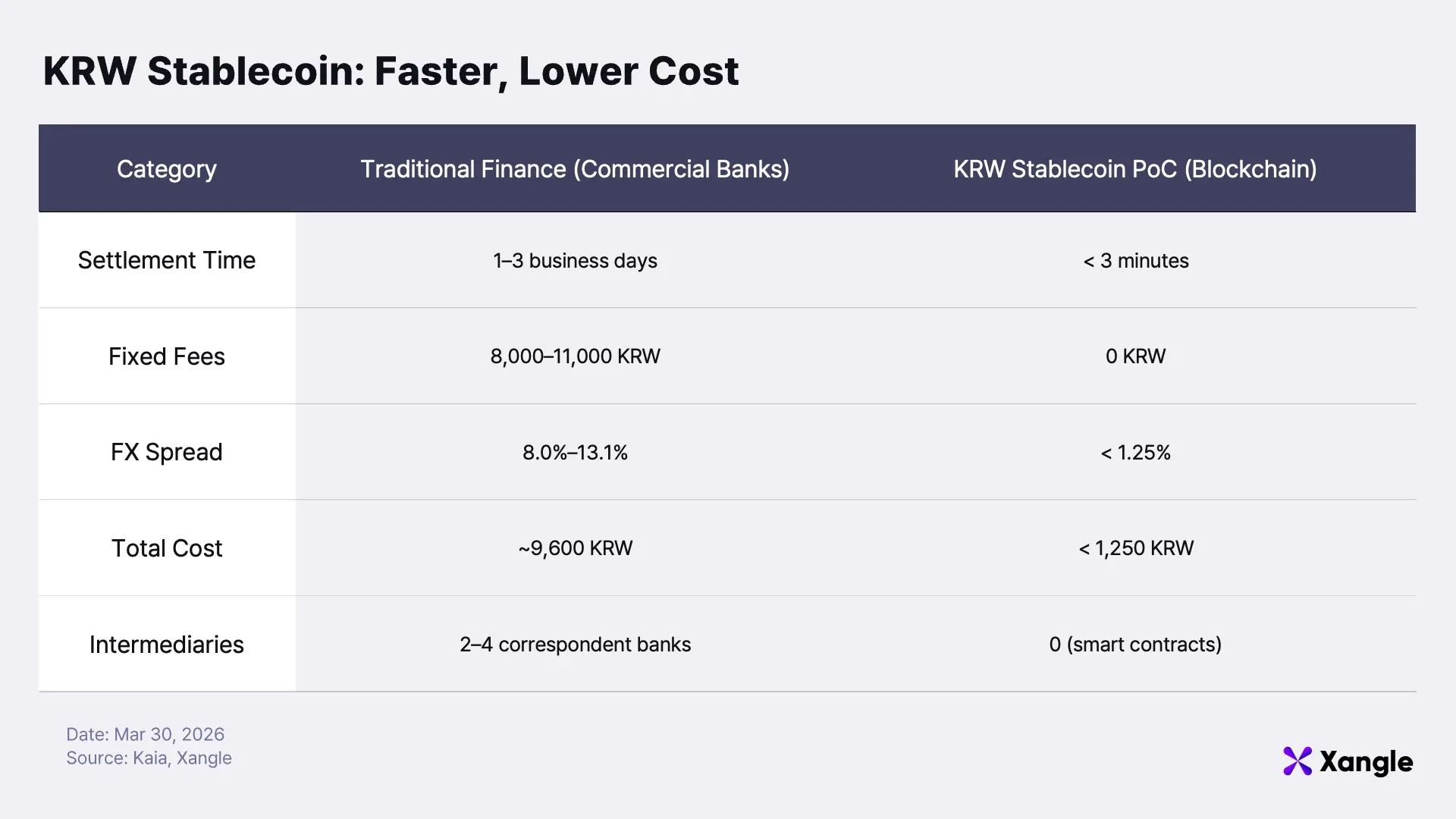

The clearest expression of this potential lies in domains where multiple currencies and payment channels intersect: cross-border remittances, international payments and settlement, and on-chain FX. According to the Bank for International Settlements (BIS), as of April 2025, the average daily trading volume of the global OTC FX (over-the-counter foreign exchange market) reached $9.6 trillion, with spot transactions alone accounting for approximately $3 trillion per day.

Despite its scale, the market remains structurally inefficient. Settlement still takes one to three business days due to reliance on intermediary institutions, while fees and FX spreads remain elevated. Transactions are executed in real time, yet the actual movement of funds is delayed by several days. If a KRW stablecoin can interoperate with other currency-denominated stablecoins—such as USD, EUR, and JPY—and integrate into this flow, it can unlock its role as a new payment and settlement infrastructure capable of meaningfully replacing existing systems.

2-2. Cross-Chain Orchestration

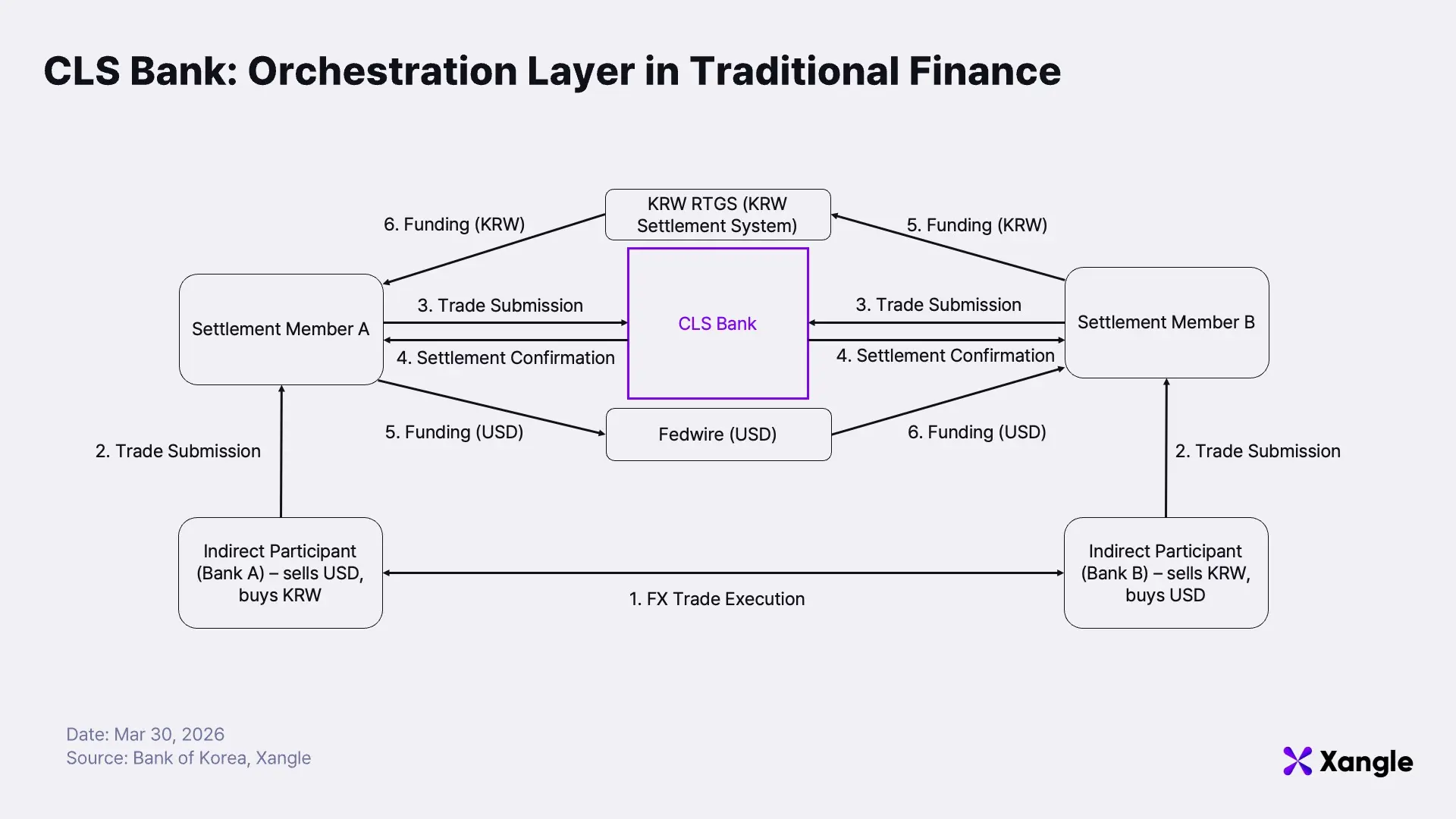

Once a KRW stablecoin begins to operate alongside dollar-, euro-, and yen-denominated stablecoins, the challenge extends beyond simple currency exchange. In traditional finance, this problem is addressed by CLS Bank. For example, when a Korean bank executes a transaction to sell KRW and buy USD, the absence of CLS would introduce settlement risk: KRW may be delivered while the counterparty fails to deliver USD. CLS eliminates this risk through a Payment versus Payment (PvP) mechanism, ensuring that both legs of the transaction settle simultaneously and preventing structurally asymmetric outcomes.

An equivalent problem exists in on-chain environments. When a KRW stablecoin and a USD stablecoin reside on different blockchains, a transaction may be finalized on one chain while failing on the other, creating an asymmetric state. Without a structure that can connect and settle such transactions within a unified flow, cross-border payments and exchanges cannot function as real infrastructure. This is the core rationale for an orchestration layer.

Global players are already moving to build or adopt this layer. Tether is extending Ethereum-based USDT liquidity across multiple chains through USDT0. Mastercard’s acquisition of BVNK reflects a similar direction. BVNK provides infrastructure that connects payments and settlement between fiat currencies and stablecoins; through this acquisition, Mastercard aims to directly bridge on-chain payments with existing payment rails. The approaches differ, but the underlying objective is consistent: enabling stablecoins to operate across multiple networks and payment infrastructures. Even if a KRW stablecoin initially launches within a single-currency framework, it must be designed with future interoperability in mind, allowing seamless integration with other currency-denominated stablecoins.

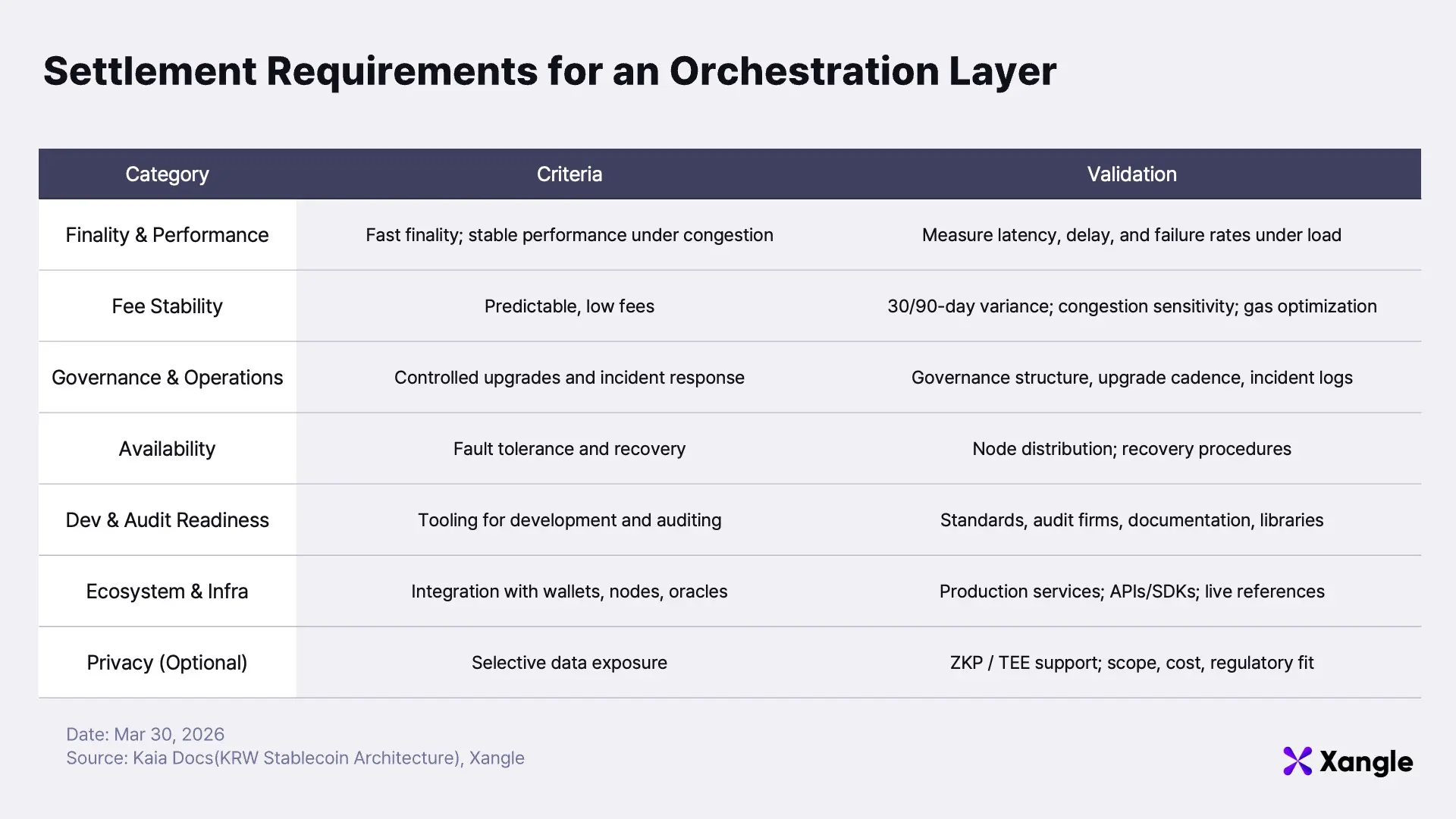

3. Requirements for an Orchestration Layer

For an orchestration layer to function as a real payment and settlement infrastructure, three conditions must be met. First, operational control must extend across the entire lifecycle of issuance and redemption. Second, it must provide settlement functionality that ensures finality and transactional trust. Third, it must support the expansion of circulation and connectivity across multiple currencies and channels. These conditions build sequentially: without control, settlement loses meaning; without reliable settlement, any expansion built on top cannot function.

3-1. Issuance–Redemption Integrity and Operational Control

Strict design of issuance and redemption is essential. The moment on-chain supply loses its 1:1 parity with reserve assets, instruments redeemable for KRW begin circulating beyond the reserve base. Such a breakdown can undermine monetary order and erode trust in payment systems. If improperly issued stablecoins become distributed across multiple blockchains, recovery and control become significantly more difficult. Issuance and redemption must therefore be governed within a single, unified process that includes KRW deposits, reserve verification, on-chain minting and burning, and record-keeping.

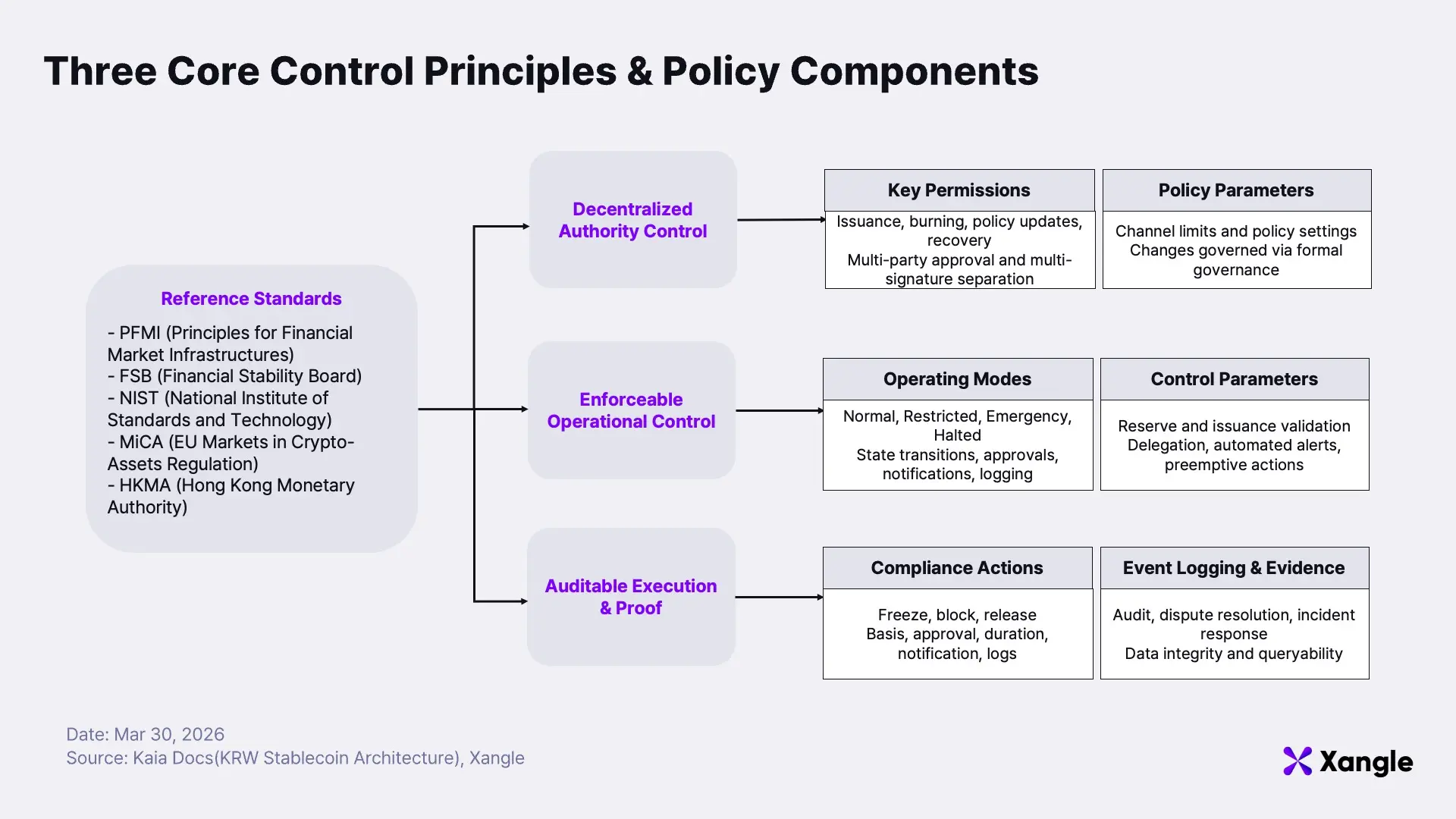

For this process to be trusted in practice, the operational control framework must be designed alongside it; three principles define this structure.

The first is the prevention of concentrated authority. If critical permissions—such as issuance, burning, and policy changes—can be exercised by a single individual or key, the entire system becomes vulnerable to compromise or operational error. These risks can be mitigated by separating authority under a multi-party approval structure based on multi-signature governance.

The second is enforceable control. A system that relies on subjective operator judgment for each abnormal event cannot guarantee timely or consistent responses. Defining four operational modes—normal, restricted, emergency, and halted—and pre-specifying the functional scope permitted under each state enables consistent and rule-based responses to abnormal conditions.

The third is auditable evidence. Beyond issuance and redemption records, decisions such as restrictions or policy changes must also be recorded together with the criteria and procedures under which they were executed. Without such records, identifying root causes and assigning accountability becomes difficult in the event of an incident, and external supervisory authorities cannot reliably verify whether controls are functioning as intended.

3-2. Settlement Design for Reliable Operations

Control alone is not sufficient for an orchestration layer. As outlined in Section 2, when a KRW stablecoin and a USD stablecoin are exchanged across different chains, an asymmetric outcome may arise—one side of the transaction completes while the other fails. Preventing this structurally requires clear finality of settlement, accurate and persistent transaction records, and post-execution verifiability of control actions. If settlement integrity is compromised, trust in all payments and transfers executed on top of the orchestration layer deteriorates accordingly.

Settlement must be designed under a different set of priorities than issuance–redemption control. In issuance and redemption, authority control and consistency are paramount. In payments and transfers, execution speed, fee predictability, and resilience under congestion become critical. If a retail payment takes tens of seconds, or if small-value transfers incur unpredictable fees, there is little justification for replacing existing infrastructure. For an orchestration layer to function as real payment infrastructure, control and performance must be integrated within a single system.

3-3. Scalability in Circulation and Connectivity

Issuance–redemption control and settlement functionality alone do not complete an orchestration layer. Real value emerges only when a KRW stablecoin connects across currencies and channels. Without such connectivity, even a system with robust control and stable settlement remains confined to domestic payment use. To operate in practice, the orchestration layer must satisfy three conditions that enable expansion in circulation and connectivity.

The first is on-chain FX and a liquidity hub. A transaction cannot execute if liquidity is unavailable at the point of conversion—whether exchanging KRW stablecoins into USD or JPY, or executing cross-border payments. Seamless multi-currency exchange and settlement require a structure that manages both liquidity and routing in tandem.

The second is external scalability through super apps and SDK/API integration. Infrastructure alone is insufficient if access is limited. Users must be able to manage multiple stablecoins within a single interface and execute FX, transfers, and payments seamlessly. At the same time, open APIs and SDKs must enable banks, fintechs, and platform operators to integrate these capabilities into their own services, allowing the KRW stablecoin to circulate beyond any single application.

The third is compliance integration. In a system where stablecoins from multiple jurisdictions are interconnected, regulatory requirements must operate within the transaction flow itself. Without embedded compliance, such as Travel Rule enforcement and KYC/AML, cross-border connectivity may be technically feasible but operationally constrained. Only when each jurisdiction’s regulatory framework is incorporated into the circulation structure can usage extend into real-world deployment.

4. Kaia as the Orchestration Layer for Stablecoins

As outlined above, an orchestration layer must satisfy three conditions to function as real payment and settlement infrastructure: issuance and operational control, reliable settlement, and scalable circulation and connectivity. Kaia is the orchestration layer that, in the context of a KRW stablecoin, meets these requirements in practice.

4-1. Why Kaia Fits the Orchestration Layer Model

Kaia is an EVM-based public blockchain formed through the merger of Kakao’s Klaytn and LINE’s Finschia. This origin defines its differentiation. KakaoTalk and LINE together serve more than 250 million users across Asia, creating a structure where blockchain infrastructure is embedded directly within existing user channels from the outset. Infrastructure is not built first in search of users; it is deployed on top of already established distribution channels.

Kaia is already progressing toward the issuance of stablecoins from other jurisdictions, particularly in the context of on-chain FX and liquidity hubs. In Japan, JPYC is exploring issuance on Kaia, while LINE NEXT is working with JPYC to integrate a yen-denominated stablecoin into the LINE messenger. As multiple currency-denominated stablecoins begin to accumulate on a single chain, a KRW stablecoin can integrate into this environment and naturally extend into FX and settlement with other stablecoins.

External scalability is anchored in operational experience. Kaia has already integrated and operated a digital asset wallet, KLIP, within KakaoTalk during the Klaytn era. This experience provides a practical foundation for designing user onboarding, wallet integration, and service operations when embedding a KRW stablecoin into messenger-based services. At the same time, Kaia’s EVM-compatible architecture supports SDKs and public RPC APIs, enabling banks, fintechs, and platform operators to integrate KRW stablecoin functionality into their own services. The advantage lies not in the messenger channel itself, but in the combination of proven in-platform blockchain integration and a technical stack that supports external expansion.

An orchestration layer must do more than process transactions quickly; it must also define transaction validity with clarity. As multiple currencies and settlement layers become interconnected, ambiguity in finality directly undermines system-wide trust. Kaia addresses this with a one-second block time and instant finality. Transactions that may take approximately 12 minutes to finalize on Ethereum reach finality within one second on Kaia, allowing for clearer criteria in determining which transactions should be preserved or reverted under abnormal conditions.

4-2. How Kaia Is Operationalizing a KRW Stablecoin

Suitability cannot be determined by structural conditions alone. It must be evaluated based on how a KRW stablecoin is handled in practice. Kaia is positioning itself not simply as an issuance layer, but as an orchestration layer that extends from issuance into real payments, settlement, and cross-border remittances.

A representative example is the pilot conducted in the first quarter of 2026. The initiative was carried out jointly by a major domestic commercial bank and K-STAR, with Kaia operating as the orchestration layer across the full lifecycle of KRW stablecoin usage. The scope extended beyond issuance to include transfers, offline payments, cross-border remittances, and settlement. In domestic offline payments, the focus was on reconstructing the existing PG-centered settlement structure; in cross-border remittances, on redesigning the intermediary model built around correspondent banking. Whitelisting and KYC/AML-based controls were also embedded directly into the operating structure.

The pilot validated an end-to-end on-chain flow for both domestic payments and cross-border remittances. In domestic payments, KRW stablecoins were transferred from users to merchant wallets and settled back into KRW. In cross-border remittances, KRW stablecoins were exchanged into USDT on-chain and delivered to recipient accounts via local partners. Whitelisting and KYC/AML controls were applied under conditions closely resembling real transaction environments. The pilot therefore moved beyond issuance and transfer, demonstrating that KRW-denominated value could be extended into real payment and cross-border remittance use cases within a domestically designed framework.

The pilot was structured as PoC Phase 0—the initial validation stage—and subsequent phases toward commercialization are already in progress. On the settlement side, validation is expanding to larger transaction volumes and real payment data to test processing stability. At the same time, regulatory messaging and compliance frameworks required for a KRW stablecoin are being integrated more deeply into smart contract architecture. Preparations for cross-border payments are also advancing. Rather than relying on intermediary assets such as USDT, the next phase focuses on onboarding local stablecoins across Asian markets and establishing inter-currency liquidity pools. This effort is being aligned with each jurisdiction’s legislative timeline. The scope is no longer limited to issuance and transfer; it is evolving toward a multi-currency payment and settlement framework for KRW stablecoins across Asia.

5. Conclusion

For a KRW stablecoin, legislation is only the starting point. Competitiveness is determined by what happens after issuance—circulation and real usage. If it remains a supplementary domestic payment instrument, there is limited reason to replace existing financial infrastructure with a tokenized system. Its value increases when it expands into areas where traditional systems have been structurally inefficient: cross-border payments and settlement, multi-currency connectivity, and on-chain FX. The key question is not issuance itself, but how the stablecoin is designed to be used and connected from the outset.

Kaia becomes relevant here. As a Korea-based blockchain, it has worked closely with major domestic commercial banks and enterprises to design and validate the full lifecycle of a KRW stablecoin, from issuance through circulation to real usage. This positions Kaia not simply as an issuance platform, but as an orchestration layer capable of building and operating real-world usage structures alongside financial institutions. As the discussion shifts from whether issuance should be permitted to how usage can be implemented, Kaia is already offering a concrete answer.

Regulatory frameworks are still evolving, and the structure of a KRW stablecoin requires further refinement. That does not necessarily represent a disadvantage. Other jurisdictions have already moved ahead with issuance, circulation, and usage, providing both reference points and lessons. Korea can use these precedents to design a more refined post-issuance model, one that more effectively connects circulation to real-world adoption. In this setting, Kaia has the potential to act as a distribution channel anchored in Asia-based messenger platforms, extending reach after issuance and supporting broader adoption. It stands out as an orchestration layer capable of translating KRW stablecoin circulation into practical usage.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article was written at the request of Kaia. All content in this article was written independently by the author(s), and neither CrossAngle nor Kaia had any editorial control or influence over the content. The author(s) may hold the cryptocurrencies mentioned in this article at the time of writing.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Solana RWA: A Look at the Key Players](https://resource.xangle.io/files/content/F779A005246C0299246537AACB3A39F2_1782287059970.webp)