Uniswap’s Fee Switch and the Return of Fundamentals

Table of Contents

1. A Post-Regulatory Pivot: Why Uniswap’s Fee Switch Marks a Structural Breakpoint

2. The Cash-Flow Turn: Rebuilding $UNI as a Value-Accruing Asset

2-1. Aligning protocol revenue with token value via fees, sequencer revenue, and treasury assets

2-2. Internalizing MEV at the protocol layer with PFDA

3. Redefining DeFi Valuation: From PSR to PER and Beyond

4. Fundamentals Return: Cash Flow Overtakes Hype as the Core of Token Valuation

1. A Post-Regulatory Pivot: Why Uniswap’s Fee Switch Marks a Structural Breakpoint

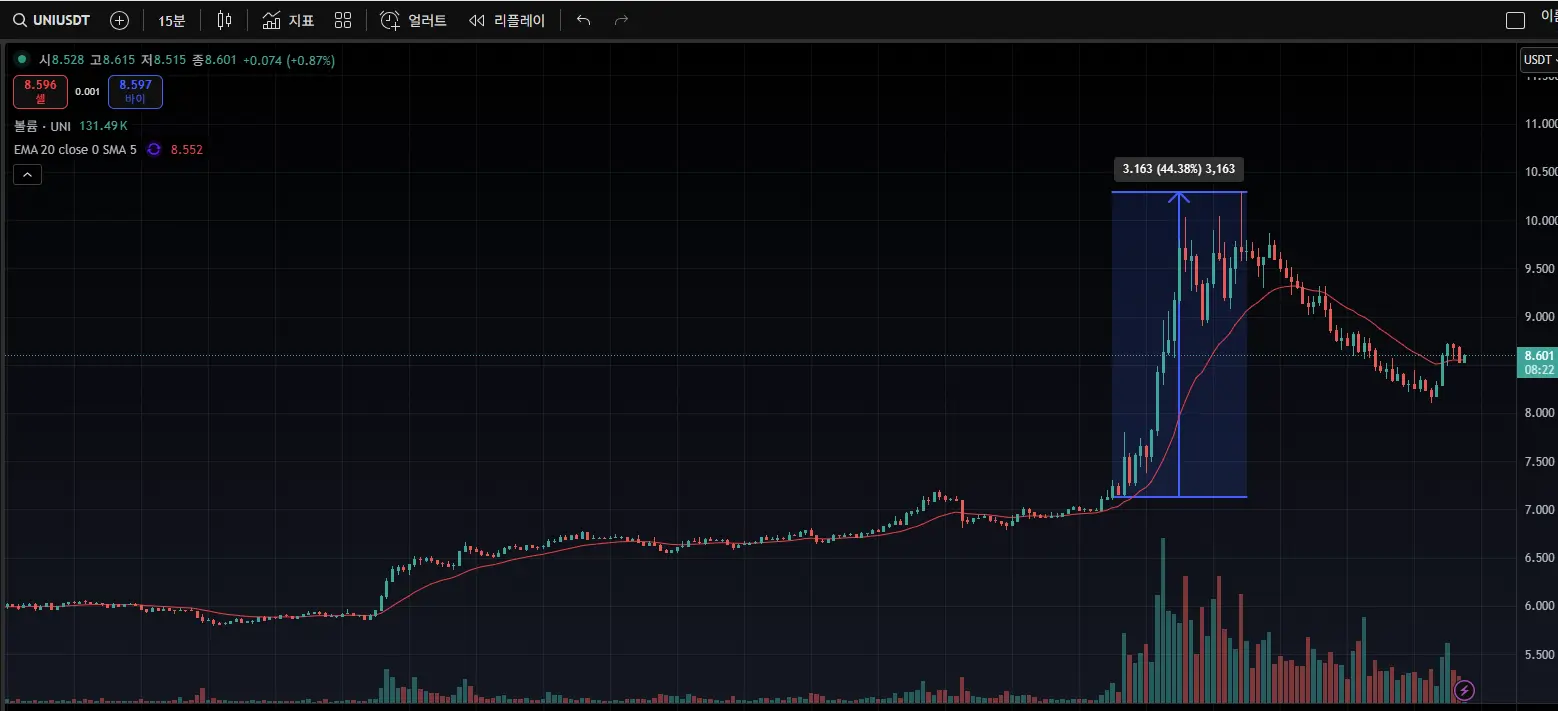

Uniswap founder Hayden Adams recently unveiled a governance proposal introducing a “Fee Switch” mechanism that would distribute a share of protocol fee revenue to token holders, immediately drawing strong market attention. The proposal represents more than a simple structural update. After years of operating under regulatory constraints, Uniswap is signaling a shift toward realigning protocol revenue with tokenholder value. The impact was immediate: $UNI rallied more than 40% following the announcement, reflecting the market’s sharp reaction.

Source: TradingView

Source: TradingView

Uniswap, the largest decentralized exchange (DEX) in the DeFi sector, has been a focal point of U.S. regulatory pressure since the SEC investigation in 2021 and the Wells Notice issued in 2024. Regulators questioned whether $UNI should be considered a security and whether Uniswap effectively functioned as an “unregistered securities exchange.” To avoid intensifying securities-related scrutiny, the protocol maintained a structure where no revenue was distributed to token holders. The result was a persistent disconnect: despite generating substantial and sustained fee revenue, that economic output could not be reflected in the token’s value.

The regulatory environment shifted dramatically at the end of 2024 with the launch of the Trump administration. Paul Atkins, known for his crypto-friendly stance, was appointed as SEC Chair, triggering a rapid move toward deregulatory policy. Atkins publicly stated, “Most crypto tokens are not securities, and we will draw a clear line,” signaling a strong intent to resolve the regulatory overhang that had weighed on the industry for years.

Against this backdrop of regulatory easing, Uniswap’s Fee Switch proposal is widely seen as a move into a new phase. Historically, 100% of trading fees were distributed to liquidity providers (LPs). With the Fee Switch activated, a portion of those fees will instead be directed toward the buyback and burn of $UNI. Considering that Uniswap has already processed more than $4 trillion in cumulative trading volume and generated approximately $2.7 billion in fees, the Fee Switch has the potential to recast $UNI from a pure governance token into an asset valued on actual cash flows.

The proposal represents more than a catalyst for short-term price appreciation. It marks a potential turning point for decentralized protocols broadly—signaling a shift back toward economically grounded models where revenue generation directly supports tokenholder value. As this approach aligns with a more permissive regulatory environment, the move could reshape valuation frameworks across the entire DeFi space. The following sections examine the core components of Uniswap’s Fee Switch and the broader implications this proposal may carry for the market.

2. The Cash-Flow Turn: Rebuilding $UNI as a Value-Accruing Asset

2-1. Aligning protocol revenue with token value via fees, sequencer revenue, and treasury assets

The proposal centers on establishing a self-reinforcing mechanism where revenue generated by the Uniswap protocol is systematically used to burn $UNI, ensuring that token value becomes directly tethered to protocol earnings. The burn budget is sourced from three streams: fee revenue, sequencer revenue, and treasury assets.

Swap fee revenue generated from Uniswap pools

The rollout begins on Ethereum mainnet, applying the Fee Switch to v2 pools and select v3 pools—segments that together account for roughly 80–95% of Uniswap’s total liquidity-driven revenue.

- Uniswap v2: The full 0.3% swap fee historically flowed to LPs. Under the Fee Switch, LPs retain 0.25% while the remaining 0.05% accrues to the protocol.

- Uniswap v3: Fee tiers differ across pools, so governance will determine the protocol’s share on a per-pool basis. Initial parameters allocate one-fourth of LP fees from low-fee pools (0.01%, 0.05%) and one-sixth from high-fee pools (0.3%, 1%) to the protocol.

Protocol revenue collected through this mechanism is automatically routed to TokenJar, an on-chain smart contract. Any withdrawal from TokenJar must pass through the Firepit contract, which burns $UNI. Greater trading activity therefore expands protocol revenue, and expanding revenue results in reduced circulating supply—a positive value-accrual loop embedded directly into protocol design.

Sequencer revenue from Unichain

The same burn path also applies to sequencer revenue originating from Unichain, Uniswap’s L2 network. Within only nine months of launch, Unichain has reached an annualized trading volume of roughly $100 billion and generated around $7.5 million in sequencer revenue. After deducting L1 data costs and the 15% fee owed to Optimism, all remaining net sequencer revenue is sent directly to the UNI burn contract.

Treasury-allocated $UNI for burns

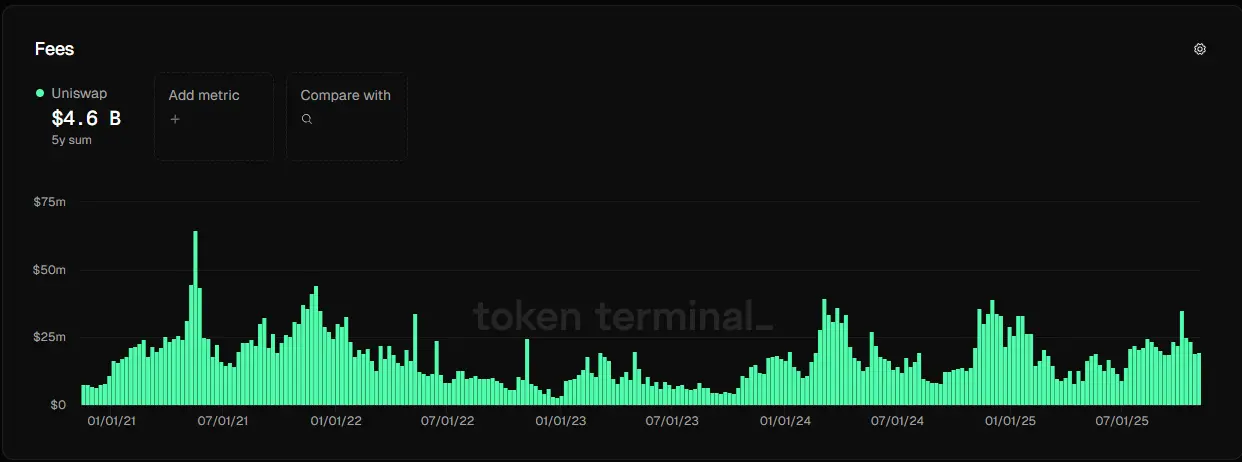

A final burn component comes from Uniswap’s own treasury. Despite generating over $4.6 billion in cumulative trading fees over the past five years, none of that value accrued to the token due to the Fee Switch’s long-standing inactivity. To partially reflect this unrealized value capture, the treasury will immediately burn approximately 100 million $UNI. The action is widely viewed as Uniswap’s explicit acknowledgement of its historical gap in value capture—and a clear commitment to tying token supply reduction and long-term value appreciation going forward.

Source: Token Terminal

Source: Token Terminal

2-2. Internalizing MEV at the protocol layer with PFDA

The proposal introduces PFDA (Protocol Fee Discount Auction), a new fee mechanism designed to bring MEV (Maximal Extractable Value) revenue—historically leaked to external actors—back into the Uniswap protocol and redirect it toward $UNI burns.

MEV refers to profit extracted by validators or searchers via transaction reordering, preferential inclusion, or pre-execution during block production. Historically, these proceeds accrued almost exclusively to validators and bot operators, offering no economic benefit to the protocol or its token holders. PFDA reshapes this dynamic by channeling MEV, which previously escaped the system, into a burn path that increases $UNI value.

The mechanism is intentionally straightforward. For a defined period, a specific wallet wins an auction that grants the right to execute swaps without paying protocol fees. The winning bidder pays for privileged access that enhances MEV or arbitrage profitability. The proceeds from that auction are then routed directly into the Firepit burn contract, reducing $UNI supply and reinforcing its value.

Under this model, MEV that once flowed to block producers instead terminates within the protocol itself, contributing directly to $UNI burns. The shift not only neutralizes part of the external MEV race but also establishes a new, protocol-native revenue stream. According to the governance proposal, PFDA is expected to increase LP earnings by roughly $0.06–$0.26 per $10,000 of trading volume. Given that current LP returns range from –$1 to $1 per $10,000 in volume, PFDA represents a meaningful structural improvement for both the protocol and its liquidity providers.

Beyond the burn mechanics, the proposal incorporates several additional changes: i) Converting v4 into an aggregator, ii) consolidating the Uniswap Foundation into Uniswap Labs, and iii) removing interface, wallet, and API fees. Readers seeking further details may refer to the official proposal linked here.

3. Redefining DeFi Valuation: From PSR to PER and Beyond

Until the Fee Switch, valuation of blockchain protocols largely relied on the PSR (Price to Sales Ratio). The metric, market capitalization divided by revenue, has been particularly effective for comparing relative valuations among projects operating within the same category. In DeFi, protocols generate substantial trading-fee revenue, yet that revenue often does not accrue directly to the token. PSR therefore provides a practical way to measure a protocol’s market value relative to its underlying economic footprint. Because many tokens undergo ongoing issuance, changes in circulating supply should be considered when interpreting PSR levels.

The table below compares the PSR of major DEXs and DeFi protocols, including Uniswap, offering a sense of which protocols appear relatively undervalued or overvalued.

Raydium posts the lowest PSR at roughly 0.25, while SushiSwap marks the highest at 13.05. Uniswap stands at 4.82, placing it on the higher end of the spectrum.

Once the Fee Switch is introduced, the PER (Price to Earnings Ratio) becomes applicable. PER—market capitalization divided by net income (revenue minus operating expenses)—is a widely used valuation metric that indicates how many multiples of profit the market assigns to a company or protocol.

Activation of the Fee Switch channels the portion of fee revenue remaining after LP rewards into token burns. Under that structure, LP payments can be treated as operating costs, while revenue allocated to $UNI burns can be considered net income, thus enabling a more grounded, economics-driven valuation approach.

PER calculations, however, require several assumptions at the current stage:

- For Uniswap, net income is assumed to equal 0.05% of total trading fees, as estimated by Token Terminal.

- For all other protocols, because Fee Switch–like mechanisms have not yet been introduced, protocol revenue as reported by Token Terminal is treated as net income.

Applying these assumptions yields a PER of approximately 96.36x for Uniswap—the highest in its peer group. The figure should not be interpreted solely as overvaluation; it also reflects Uniswap’s position as DeFi’s clear first mover and its reputation as one of the most stable and trusted protocols in the sector.

These values are preliminary reference points built on initial assumptions. As the Fee Switch is implemented and its economics take clearer shape, more precise and analytically robust valuation models are expected to develop. If similar mechanisms become common across the industry, traditional finance–style comparative analyses will become increasingly feasible and more informative.

4. Fundamentals Return: Cash Flow Overtakes Hype as the Core of Token Valuation

The significance of Uniswap’s Fee Switch extends far beyond the immediate price appreciation of $UNI. The shift has the potential to mark the beginning of a new valuation paradigm for the entire DeFi industry. Uniswap has long stood as the flagship protocol of Ethereum DeFi and, under the Biden administration, became a central example of intense SEC scrutiny. The fact that this same Uniswap is now activating protocol revenue and formally adopting a token value–accrual model sets a powerful precedent for other DeFi projects. Several tokens, such as $ENA, $AAVE, and $LIDO, are already being discussed as likely next adopters of similar mechanisms.

A fully active Fee Switch is expected to soften the long-standing challenge of “valuation opacity” that has characterized many DeFi tokens. Detailed standards, covering revenue recognition, cost attribution, and the entity responsible for valuation, will still require ongoing debate. Even so, the market is beginning to transition from narrative-driven pricing toward frameworks grounded in measurable revenue and actual cash flows.

Uniswap’s Fee Switch may serve as an inflection point that reallocates capital toward protocols capable of consistently generating revenue and translating that revenue into tangible token value. The shift is likely to strengthen investor demand for protocols with sustained usage, real economic activity, and proven product-market fit. An era is emerging in which fundamentals carry more weight than storytelling, and cash flows speak louder than hype.

The mechanism, however, is not a guaranteed path to structural success. Using a portion of protocol revenue for $UNI burns necessarily reduces rewards flowing to LPs. Lower LP profitability may push liquidity toward competing DEXs. Such outflows can widen slippage, impair price discovery, and ultimately reduce both trading volume and protocol revenue. Uniswap’s central challenge is therefore clear: it must strike a sustainable balance between token value accrual and LP incentives. How Uniswap navigates this trade-off—designing a revenue-sharing structure that enhances tokenholder value while retaining competitive liquidity—will be critical to the protocol’s long-term trajectory.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.