Stable: Purpose-Built Infrastructure for USDT

Table of Contents

1. The Stablecoin Infrastructure Market Can’t Be Ignored

2. Stable: The Final Piece for USDT Mass Adoption

2-1. Stablecoin infrastructure must work for everyday payments

2-2. For mass adoption, assets must move freely and securely

2-3. Institutional liquidity requires privacy protection

3. Stable’s Opportunities and Growth Potential

3-1. USDT’s dominance and Stable as its direct beneficiary

3-2. The future of stablecoins and Stable’s role

4. Conclusion: Stable, the Inevitable Settlement Rail for the Stablecoin Era

1. The Stablecoin Infrastructure Market Can’t Be Ignored

The growth of the stablecoin market is now indisputable. Backed by U.S. Treasuries and pegged 1:1 to the dollar, stablecoins combine monetary stability with the flexibility of blockchain-native assets. This dual nature has accelerated adoption across Web3, where stablecoins are expanding into an ever-wider range of use cases. Their ability to enable fast, low-cost remittances and payments has also pushed them into the spotlight as a global settlement medium. As of September 12, 2025, stablecoin circulation surpassed $300 billion, nearly 50% higher than at the start of the year, while monthly trading volume exceeded $970 billion. Cumulatively, peer-to-peer (P2P) transfers alone have crossed $6 trillion, underscoring how firmly stablecoins are embedding themselves into the global payments and remittance stack.

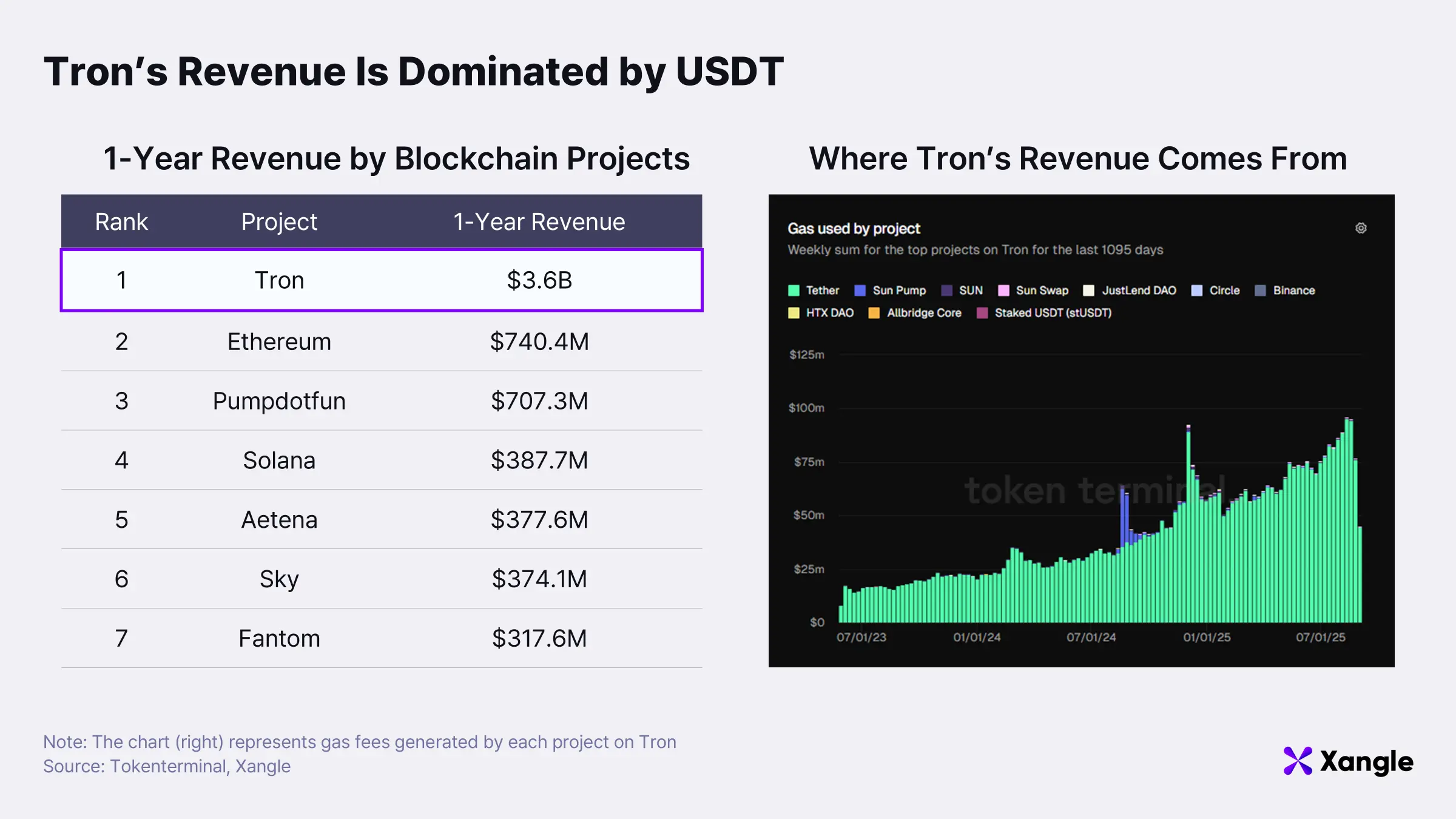

Rising demand has translated into massive revenues for issuers. In 2024, Tether posted $13 billion in net income, nearly matching Goldman Sachs’ $13.5 billion. But the upside is not confined to issuers. Blockchain infrastructure providers where stablecoins circulate are also emerging as major beneficiaries. Tron, for example, generated $3.6 billion in revenue over the past year, with an estimated 99% of all transactions tied to USDT activity. As USDT volumes climbed, fee revenues for the chains processing these transactions soared. This pattern is not unique to Tron, multiple Layer1s have seen fee growth on the back of rising USDT usage. In effect, the blockchain infrastructure layer where stablecoins are issued and transacted has become a direct derivative play on stablecoin adoption. If stablecoin growth accelerates further, infrastructure providers are positioned to become the second-largest profit centers in the value chain, right after issuers themselves.

It is against this backdrop that Stable emerged, a project built to directly target this vast market. As U.S. Treasury Secretary Scott Bessent has forecast, the stablecoin sector is on track for even steeper growth. With issuance expanding and usage deepening, the blockchain infrastructure layer, where transaction fees are recognized as revenue, will inevitably scale in tandem.

But growth in market size is only part of the story. There is also a structural opportunity. Most existing Layer-1 chains were never designed as infrastructure optimized for stablecoin payments. Even the most widely used EVM chains cap out at only a few thousand transactions per second (TPS), far below the throughput required for everyday payments. On Ethereum, fees often range from a few cents to several dollars, creating further limitations on real-world usability. For corporations and institutions, the lack of privacy on public blockchains poses an additional barrier, as key contract terms or investment positions risk being exposed. Stable sets out to address these gaps head-on—positioning itself as a dedicated, payments-focused stablecoin Layer-1.

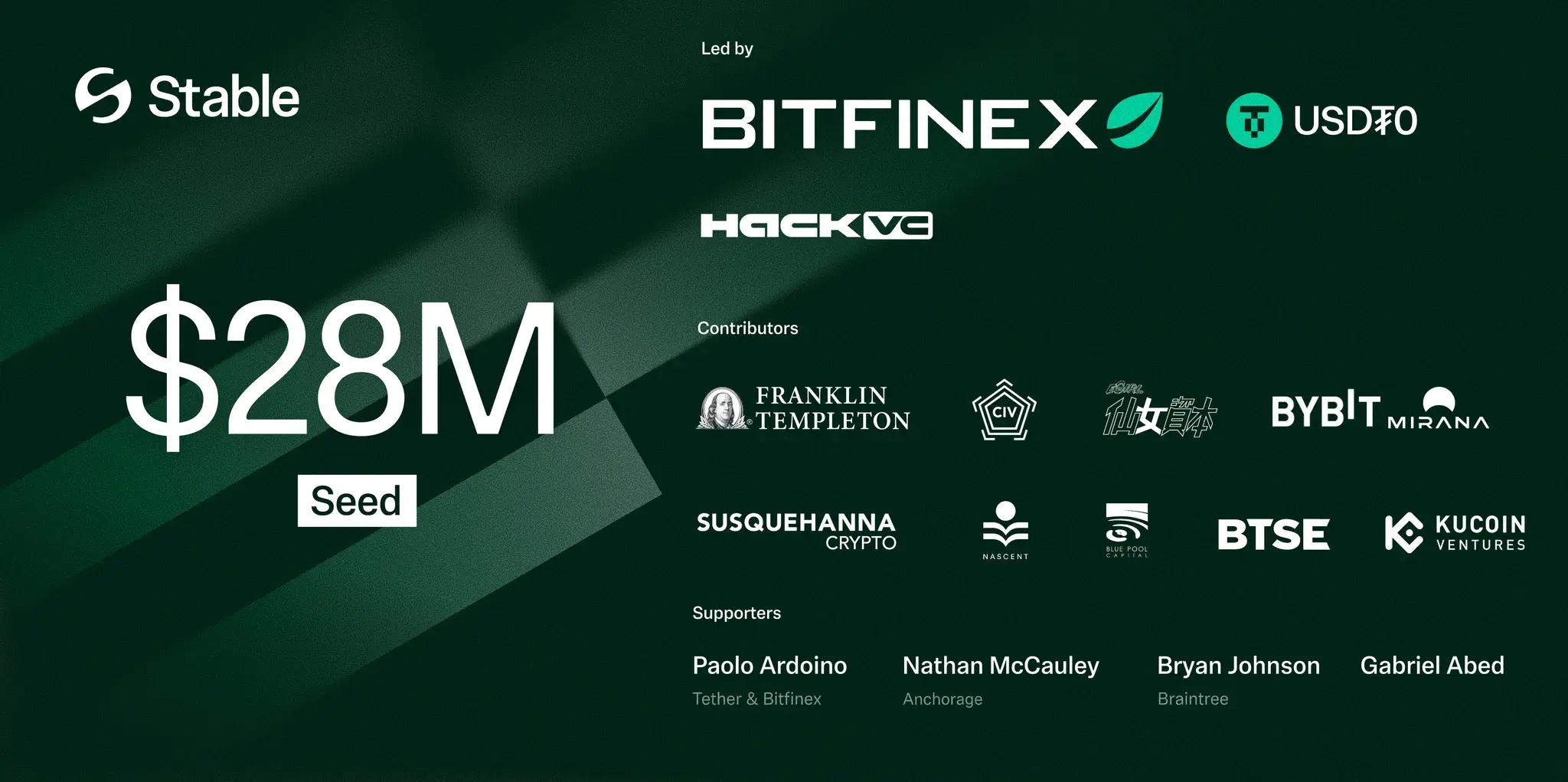

The project also comes with significant backing. Bitfinex, the exchange at the very root of Tether’s growth, has invested in Stable, while Tether CEO Paolo Ardoino serves as an advisor. This strongly signals direct support from the Tether team. With Tether’s entrenched network and its potential future use cases across payments, remittances, and beyond, Stable is expected to operate as a core infrastructure layer powering Tether’s next phase of expansion.

This report examines the background behind Stable’s launch, the pain points in existing infrastructure it aims to resolve, and the role it is positioned to play as stablecoins build out new markets across payments, remittances, and investment.

2. Stable: The Final Piece for USDT Mass Adoption

2-1. Stablecoin infrastructure must work for everyday payments

Global payment networks already operate on ultra-fast infrastructure. Visa handles around 24,000 transactions per second (TPS), Mastercard about 5,000 TPS, and while precise numbers are not publicly disclosed, banks are also believed to run core systems capable of processing several thousand TPS. This backbone allows global payments and remittance systems to settle massive transaction volumes without delay.

Blockchain infrastructure, however, remains far behind, or has yet to demonstrate real scalability. The Ethereum mainnet, which accounts for roughly 40% of USDT issuance, processes just 15–20 TPS in practice. Solana, often highlighted as “fast,” was architected for a theoretical 65,000 TPS, but in reality averages closer to 1,000 TPS, with peaks of 4,709 TPS. On multiple occasions, such as NFT minting surges or heavy bot traffic, the network has stalled entirely or experienced severe slowdowns. For stablecoins to evolve into true global settlement rails, blockchains must achieve performance closer to traditional payment networks while maintaining stability under stress.

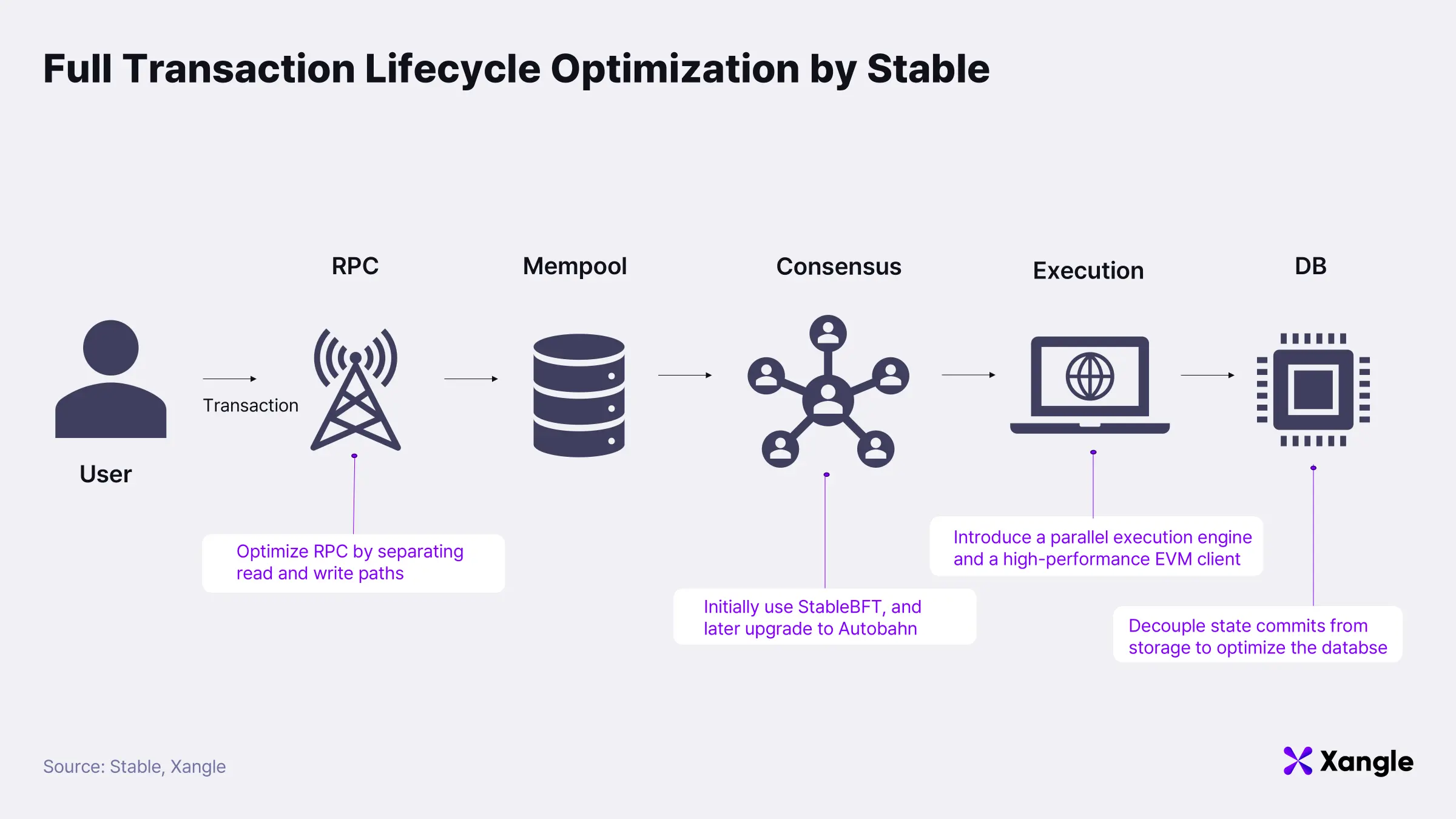

If these fundamental constraints remain unresolved, stablecoins will struggle to establish themselves as core infrastructure for global payments and remittances. This is the exact gap Stable is designed to fill. Purpose-built for payments and remittances, Stable is building a proprietary stack grounded in performance, scalability, and reliability. The entire transaction lifecycle has been re-engineered to eliminate bottlenecks, targeting both high throughput and low latency while ensuring seamless, USDT-native operations across the network.

Concretely, when a user submits a transaction, it is first delivered to the network via the RPC interface, stored in the mempool, then added to a block through consensus. Afterward, it is executed in the state machine and finally committed to the database (DB) before the user receives a finalized result. If a bottleneck occurs at any stage in this pipeline, overall system performance deteriorates. Stable addresses this by optimizing every step—RPC → mempool → consensus → execution → DB—ensuring ultra-low latency and high-speed payments. The specific improvements at each stage are described below.

Consensus

Stable employs StableBFT, a CometBFT-based Proof-of-Stake consensus protocol designed for instant finality without forks, ensuring the network remains secure even if some validators fail or act maliciously. In financial infrastructure such as remittances and payments, where immediate settlement is critical, this design choice is particularly relevant.

Even at the current stage, the system already provides high throughput and stability, but Stable plans further upgrades. Upcoming improvements include separating transaction propagation from consensus propagation and enabling transactions to be delivered directly to proposers, reducing latency. The roadmap also envisions a transition to DAG-based “Autobahn consensus”, where multiple proposers can submit blocks simultaneously. This approach would maximize throughput and allow the network to recover quickly from disruptions.

Execution

Stable introduces Stable EVM, fully compatible with Ethereum but enhanced for performance. Users can continue using familiar tools like Metamask, while precompiles give smart contracts safe access to core chain functions such as token transfers and staking. Looking ahead, Stable plans to roll out StableVM++, combining a high-performance EVM with a parallel execution engine (Block-STM). Block-STM executes multiple transactions concurrently and reprocesses only conflicting segments, a design expected to significantly boost scalability.

Database

Disk I/O has long been the biggest bottleneck in blockchain performance. In conventional systems, after transaction execution, state changes must be committed and written to disk before the next block can be processed—introducing delays. Stable addresses this by decoupling state commitment from storage. Once a new state is committed, the next block can execute immediately, while data persistence occurs asynchronously in the background. Stable also implements a dual-tier data structure: MemDB stores frequently accessed “hot” data in memory, while VersionDB manages older “cold” history on disk. This architecture enables fast reads for live data while maintaining secure archival storage for historical records.

RPC

Consensus speed alone doesn’t guarantee performance; the RPC layer is the main gateway for wallets and dApps to interact with the chain. Traditional RPCs share heavy resources with consensus and execution, making them prone to slowdowns under load. Stable introduces a split-path architecture, separating read and write requests, and deploys lightweight dedicated RPC nodes to eliminate unnecessary contention. This architecture substantially reduces query latency. Future upgrades will integrate EVM view-optimized nodes and a native indexer, enabling dApps to fetch on-chain data faster and more directly.

Stable is not chasing headline TPS metrics. By optimizing the entire pipeline, the network achieves both high throughput and instant finality. This level of stability and scalability, still unproven in most existing blockchains, lays a credible foundation for a USDT-centered global payments and remittance network.

2-2. For mass adoption, assets must move freely and securely

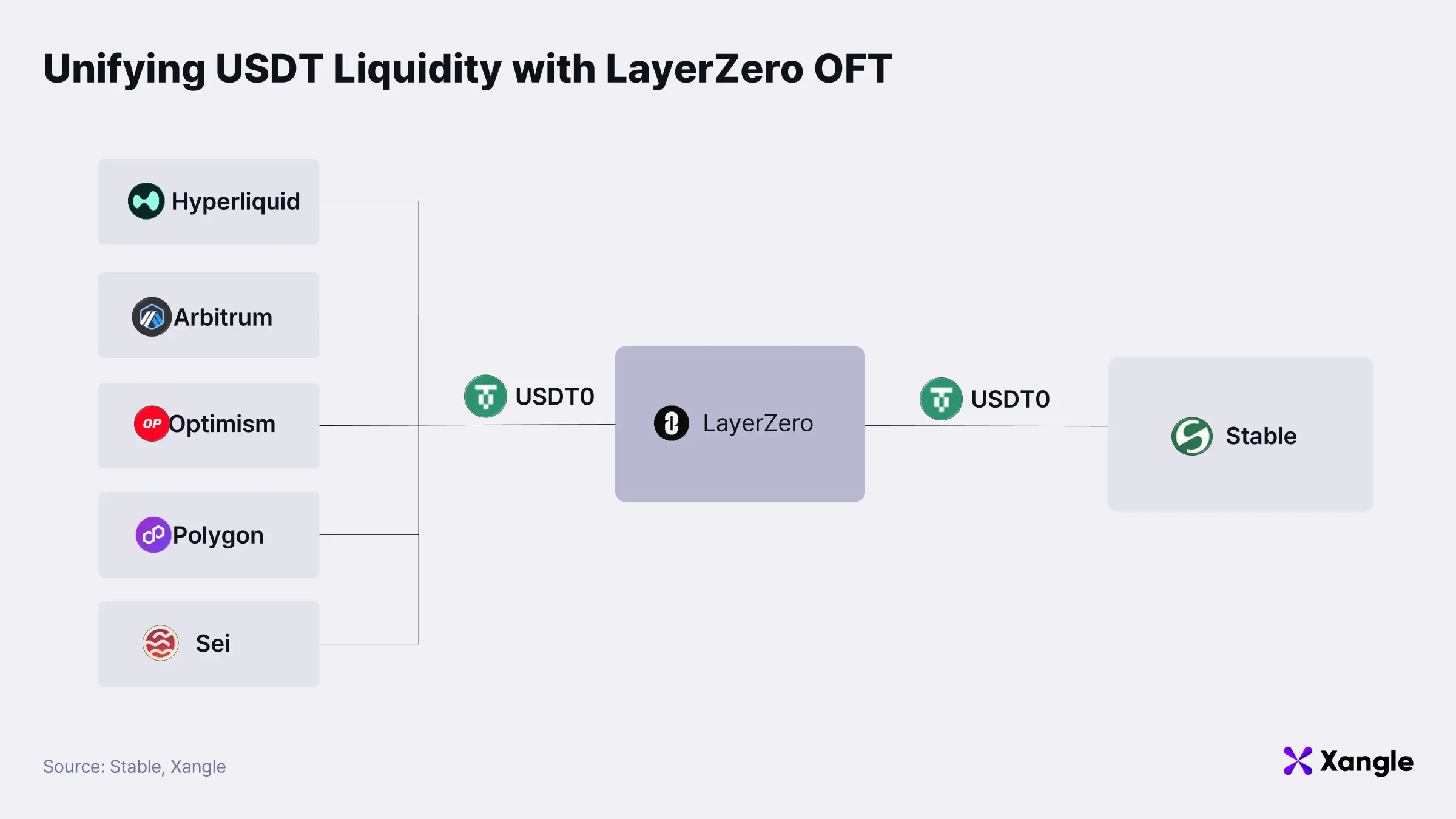

Even with scalable payment chains, stablecoins face a structural barrier of fragmented liquidity in becoming true global settlement rails. Today, USDT is issued across multiple networks—Ethereum, Tron, Arbitrum, and others. Because cross-chain transfers rely on bridges, liquidity is scattered. This fragmentation leads to chain-specific price discrepancies, slippage, transfer delays, and high bridge fees; all of which erode user experience and capital efficiency. On top of that, recurring bridge exploits remain a serious roadblock.

Stable tackles this by consolidating USDT liquidity into a single infrastructure. It introduces USDT0, an omnichain token based on LayerZero’s OFT (Omnichain Fungible Token) standard, enabling frictionless transfers across major networks like Ethereum, Arbitrum, and Avalanche, without wrapping or creating separate liquidity pools. This design unifies fragmented liquidity, ensuring deep USDT liquidity from day one, faster transfers, and drastically reduced slippage and bridge costs.

Currently, most USDT liquidity is concentrated on Tron, which also enjoys strong network effects. This makes USDT0 integration a decisive factor for Stable’s success. If Stable can effectively aggregate fragmented liquidity through USDT0, it could replicate Tron’s network effect quickly—while offering superior performance and usability to capture a larger share of the USDT market.

Another major barrier to stablecoin adoption as a global payments medium is the gas fee model. On most blockchains, native tokens (ETH, TRX, AVAX, etc.) are required to pay fees. For enterprises and institutions, this is a major friction point: to send a payment, they must hold native gas tokens; without them, the transaction cannot proceed. This forces a cumbersome process of depositing funds on an exchange, purchasing gas tokens, and transferring them into a wallet—an unacceptable UX hurdle for payment infrastructure.

Stable eliminates this problem by making USDT itself the gas token. Within the chain, gasUSDT is used for protocol-level fees, while USDT0 is used for dApp and DeFi interactions, but users never need to distinguish between them. Thanks to account abstraction, simply holding USDT0 in a wallet is enough; it is automatically converted into gasUSDT when fees are required. Going further, Stable leverages EIP-7702 and account abstraction to ensure that simple transfers incur zero gas fees altogether.

In essence, Stable creates an environment where “all you need is USDT”—covering everything from transaction fees to remittances. This simultaneously resolves the two fundamental barriers of liquidity fragmentation and gas inefficiency, paving the way for institutions to realistically adopt blockchain-based payments and settlements.

For readers interested in the technical details of account abstraction (EIP-4337) and EIP-7702, please refer to the official specifications.

2-3. Institutional liquidity requires privacy protection

Stablecoins offer clear advantages: 24/7 availability, fewer intermediaries, and significant gains in speed and efficiency for global remittances. Yet their full transparency of transaction data creates a critical barrier for institutional adoption. For corporations and financial institutions, payment sizes and remittance flows are highly sensitive competitive information that cannot be exposed publicly. Privacy is therefore essential for onboarding institutions.

Stable plans to address this via zero-knowledge (ZK)-based confidential transfers. In this model, sender and recipient addresses remain visible on-chain, but the transaction amount is concealed, accessible only to the counterparties and authorized auditors. This approach allows institutions to safeguard sensitive payment data while still satisfying regulatory audit requirements.

Equally critical for institutions is stability. Retail users may prioritize speed or low fees, but institutions move transactions in the hundreds of millions or even billions of dollars. For them, chain and token reliability and sustainability are non-negotiable. Current USDT infrastructure, however, is fragmented across Ethereum, Tron, Arbitrum, and other chains, making it difficult to verify or guarantee the stability of each network. Moreover, most general-purpose chains focus on growing their ecosystems rather than optimizing for stablecoin settlement, leaving them less responsive to institutional needs. By contrast, Stable is purpose-built for institutions, offering infrastructure tightly integrated with USDT. This specialization enables it to deliver a higher level of reliability than generic chains and positions it as the trusted settlement rail that enterprises demand.

In addition, Stable allocates dedicated blockspace to guarantee predictable speed and costs, and introduces bulk aggregation of large USDT transfers to remove potential bottlenecks—delivering the level of reliability institutions require.

Ultimately, Stable unites privacy and stability in a trust-first infrastructure purpose-built for institutions—setting it apart from generic blockchains. This dual focus makes it far more likely that enterprises will adopt Stable as their preferred settlement rail in the global payments ecosystem.

3. Stable’s Opportunities and Growth Potential

3-1. USDT’s dominance and Stable as its direct beneficiary

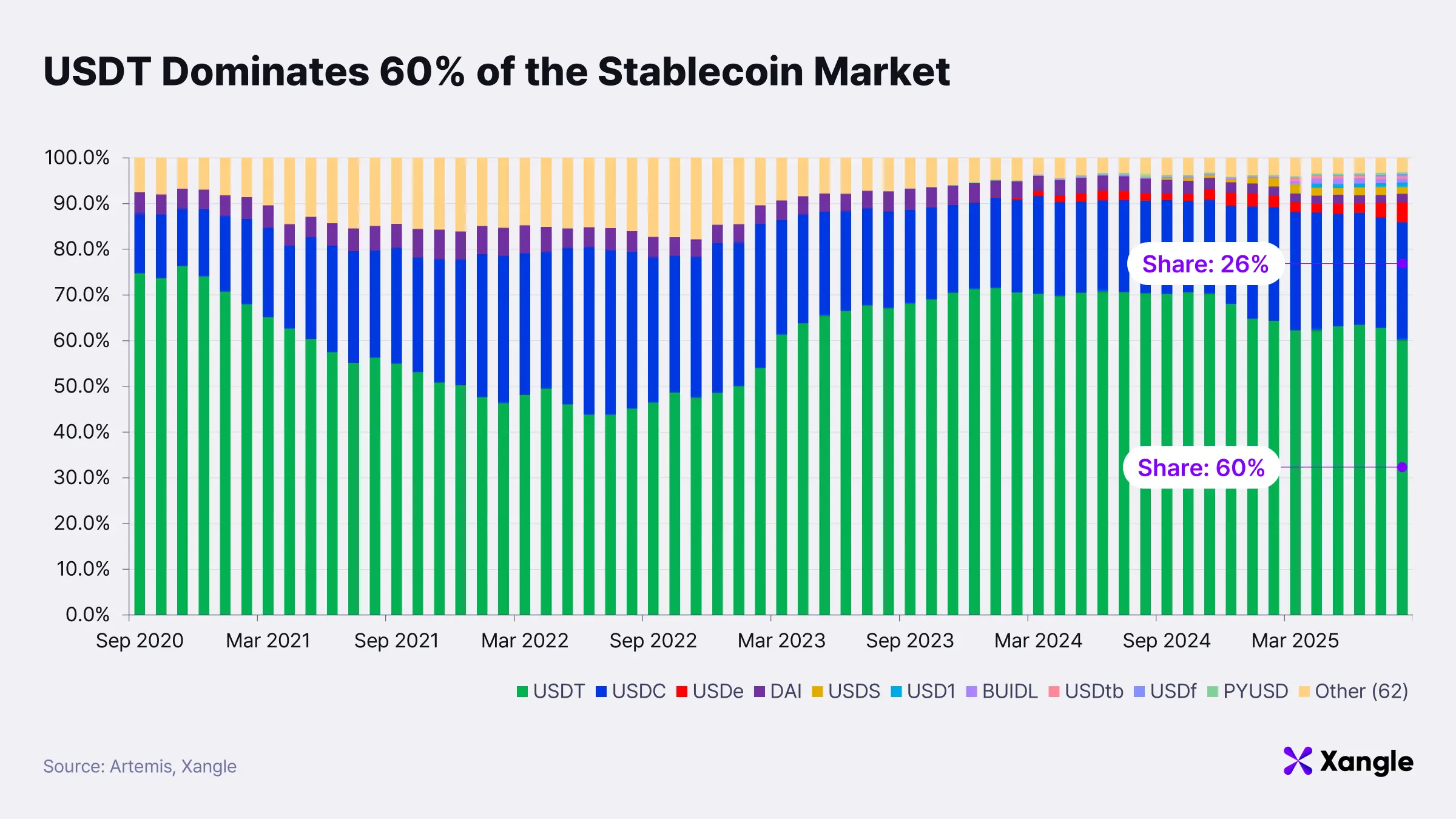

USDT continues to dominate the stablecoin market. As of August 2025, it accounts for around 60% of total supply, leaving USDC and other competitors far behind. Its influence has extended well beyond global exchanges and DeFi into payment and remittance networks across emerging markets. On centralized exchanges (CEXs), USDT has become the default base currency and leading trading pair, while most derivatives markets also rely on USDT as the margin asset. Years of accumulated liquidity and entrenched trading habits have hardened into powerful network effects, making it nearly impossible for any new stablecoin to dislodge USDT in the short term.

These network effects are especially visible in emerging-market adoption. In Argentina, more than 70% of all crypto transactions are conducted in USDT, far above the global average of 44.7%. Amid hyperinflation and currency instability, citizens effectively treat USDT as money; using it for savings, daily payments, and trade remittances. Turkey shows a similar dynamic: stablecoin purchases amount to 3.7% of GDP, with an estimated $63.1 billion in annual transaction volume. Beyond these, countries such as Brazil and Bolivia are rapidly expanding real-world USDT use through QR code payments, ATM cash-outs, and merchant acceptance, further entrenching USDT as part of local financial infrastructure.

Since 2024, new stablecoins such as USDe, USD1, USDS, and PYUSD have entered the market, yet USDT has maintained its dominance, underscoring its resilience against fresh competition.

This is where Stable’s opportunity comes into focus. With USDT’s network effects continuing to strengthen, its share of the market is likely to expand even further. The direct beneficiary of this growth could be Stable, which delivers infrastructure purpose-built for payments and remittances. Institutions require predictable speed and reliability for large-scale settlements, while retail users look for low costs and simple UX in everyday transfers. Stable positions itself as the first USDT-native Layer-1 capable of meeting both demands. This positioning enables Stable to grow alongside USDT adoption. Put simply, the more USDT solidifies its role as the global payment currency, the stronger the case becomes for Stable as its dedicated settlement rail.

3-2. The future of stablecoins and Stable’s role

Stablecoin adoption is accelerating. As of August 2025, total circulation has surpassed $280 billion, more than doubling in just a few years. Monthly transaction volume exceeded $970 billion, with roughly 99% of that activity concentrated among institutional investors and whale accounts. Peer-to-peer (P2P) transfers alone have accumulated over $6 trillion, underscoring that stablecoins are already functioning as a practical medium for payments and remittances on a global scale.

Yet this growth represents only the beginning. According to McKinsey, the daily volume of payments and remittances settled in stablecoins still accounts for less than 1% of global money flows. Despite their proven importance in crypto markets, stablecoins remain underutilized relative to the broader financial system. U.S. Treasury Secretary Scott Bessent even projected that stablecoin market capitalization could surpass $2 trillion in the long run; over seven times larger than in September 2025.

Mainstream adoption will transform stablecoin use far beyond today’s model. Currently, users often need to remit funds, transfer to an exchange, liquidate tokens, and then cash out. In the future, stablecoins held in wallets will be usable directly for online shopping, subscription services, and trade payments—bypassing unnecessary steps. Corporations will handle payroll and supply chain settlements in stablecoins, while individuals will spend them just as easily as local currency. Even Web2 payment giants are seeking footholds in this market. Stripe is building its own blockchain infrastructure, whereas Visa is focusing on expanding stablecoin settlement support across existing blockchains.

This is the inflection point where Stable identifies its opportunity: to deliver infrastructure purpose-built for payments and remittances, positioning itself to capture this explosive growth. By integrating a native gas model, ultra-low-cost and ultra-fast consensus, privacy features, and dedicated blockspace, Stable offers both institutions and retail users the reliability and efficiency they demand. Once stablecoin payments crystallize as a new standard in global finance, Stable is uniquely positioned to become the infrastructure layer that absorbs this demand most directly.

That vision is already starting to materialize. On September 22, Stable announced a strategic investment from PayPal Ventures, the global digital payments leader. As part of this partnership, PayPal USD (PYUSD) will be deployed on Stablechain, significantly extending stablecoin utility into mainstream contexts. By aligning with one of the world’s most trusted payment brands, Stable can greatly expand its reach. With PayPal’s massive global user base, this collaboration could prove a defining turning point in establishing Stable as core payment infrastructure at a global scale.

4. Conclusion: Stable, the Inevitable Settlement Rail for the Stablecoin Era

Tron has already demonstrated the scale of stablecoin infrastructure as a business model, proving just how critical it is to secure the rails that USDT depends on.

The challenge, however, is that despite the significance and potential of stablecoins, most existing Layer1s fail to meet the specialized requirements of payments: performance, gas UX, privacy, and institutional readiness. Stable positions itself as the USDT-native settlement rail designed to fill this gap. Its OFT-based liquidity unification (USDT0), USDT gas model, fully optimized transaction pipeline, ZK-based confidential transfers, and reserved blockspace collectively target the predictability, confidentiality, and operational simplicity that institutions demand. The key variables ahead are how much adoption Stable can drive across both institutions and retail users, and how much of Tron’s current role it can realistically displace.

Another reason Stable warrants close attention is that the stablecoin market is still in its formative stage. As stablecoins capture a greater share of global payments and remittances, their impact could drive system-wide transformation across the financial sector. It is not difficult to imagine a future where nearly every payment and remittance is executed via stablecoins—with Stable providing the underlying infrastructure. In such a scenario, Stable would no longer be just another blockchain, but the core layer redefining the paradigm of global payments and remittances.

That said, it is still too early to assign definitive value to Stable. The project must first prove it can consolidate USDT liquidity scattered across multiple chains—including Tron—and meet the real-world demands of both institutional and retail users. Yet Stable’s positioning and potential are clear. As the chain most deeply integrated with USDT, Stable is uniquely placed to capture USDT’s growth trajectory directly, making it the most credible candidate to emerge as next-generation infrastructure for the coming era of stablecoin payments.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article was written at the request of Stable. All content in this article was written independently by the author(s), and neither CrossAngle nor Stable had any editorial control or influence over the content. The author(s) may hold the cryptocurrencies mentioned in this article at the time of writing.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Solana RWA: A Look at the Key Players](https://resource.xangle.io/files/content/F779A005246C0299246537AACB3A39F2_1782287059970.webp)