Tether, The Undisputed Leader of Stablecoins

Table of Contents

1. The GENIUS Act: Stablecoins Enter the Regulatory Mainstream

2. The Stablecoin Market Today

3. Tether: the No.1 Stablecoin in the Market

4. Tether’s Path to Regulatory Trust

5. Closing Thoughts: Defending the Throne

1. The GENIUS Act: Stablecoins Enter the Regulatory Mainstream

Source: Reuters, Trump signing the GENIUS Act

Source: Reuters, Trump signing the GENIUS Act

In July 2025, the United States enacted the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act), establishing the first comprehensive federal framework for stablecoins. The Act closes long-standing regulatory gaps by clearly defining payment stablecoins, while reinforcing consumer protection, anti-money laundering standards, and system stability. It will take effect on the earlier of (i) 18 months from its enactment date, July 18, 2025, or (ii) 120 days after implementing regulations are published by the primary federal supervisory agencies for payment stablecoins (e.g., the Federal Reserve, FDIC, NCUA, OCC). Full implementation is therefore expected sometime in 2026.

The passage of the GENIUS Act marks a watershed moment: the first time stablecoins have been explicitly recognized in U.S. federal law, signaling their official integration into the financial mainstream. Its influence will extend beyond the U.S. As countries such as South Korea have yet to establish dedicated stablecoin laws, the GENIUS Act is poised to serve as a global reference point, shaping the foundation for international standards. For private issuers such as Tether and Circle, the Act presents both risk and opportunity. Strict reserve requirements and mandatory audits will be unavoidable for legal operation in the U.S., but compliance could unlock far larger opportunities, extending stablecoins from Web3-native use cases into traditional finance and even everyday consumer payments. The payoff is not just market legitimacy but potentially an expanded total addressable market and stronger dominance.

With the GENIUS Act, stablecoins have entered the regulatory mainstream. The question now is: which issuer can prove itself worthy of that position? At the center of this debate stands Tether, holding over 60% of global market share and determined to defend its dominance amid shifting rules. This report examines the current state of the stablecoin market, Tether’s positioning and regulatory strategy, its role in Korea, and its future roadmap.

2. The Stablecoin Market Today

A stablecoin is a digital token pegged 1:1 to fiat currencies such as the U.S. dollar. For example, Tether’s USDT is designed to maintain 1 USDT = 1 USD with minimal price volatility. To sustain the peg, issuers hold reserves equivalent to the circulating supply—typically in cash, bank deposits, short-term U.S. Treasuries and repos, and government-backed money market funds—and operate redemption mechanisms that allow holders to exchange tokens for fiat on a 1:1 basis. This ensures stability of value. Yet if most people trade crypto to profit from volatility, why does a non-volatile asset like stablecoins command so much attention and such a large market cap?

The answer is that stablecoins function less as “investment assets” and more as financial infrastructure for the digital economy. They serve as the base currency (trading pair) for crypto purchases and sales, and are widely used for transfers across exchanges, enterprises, and even national borders. On both centralized and decentralized exchanges, a significant share of spot volume is denominated in USDT or USDC pairs, positioning stablecoins as the primary gateway to market liquidity. DeFi has further expanded their utility. Stablecoins are used as collateral, for deposits, and in liquidity provision, creating opportunities to capture yields often higher than traditional bank deposits. This role as programmable, yield-bearing infrastructure has fueled persistent demand growth for stablecoins, reinforcing their position at the core of both CeFi and DeFi ecosystems.

2-1. A Market Cap Larger Than National Currencies

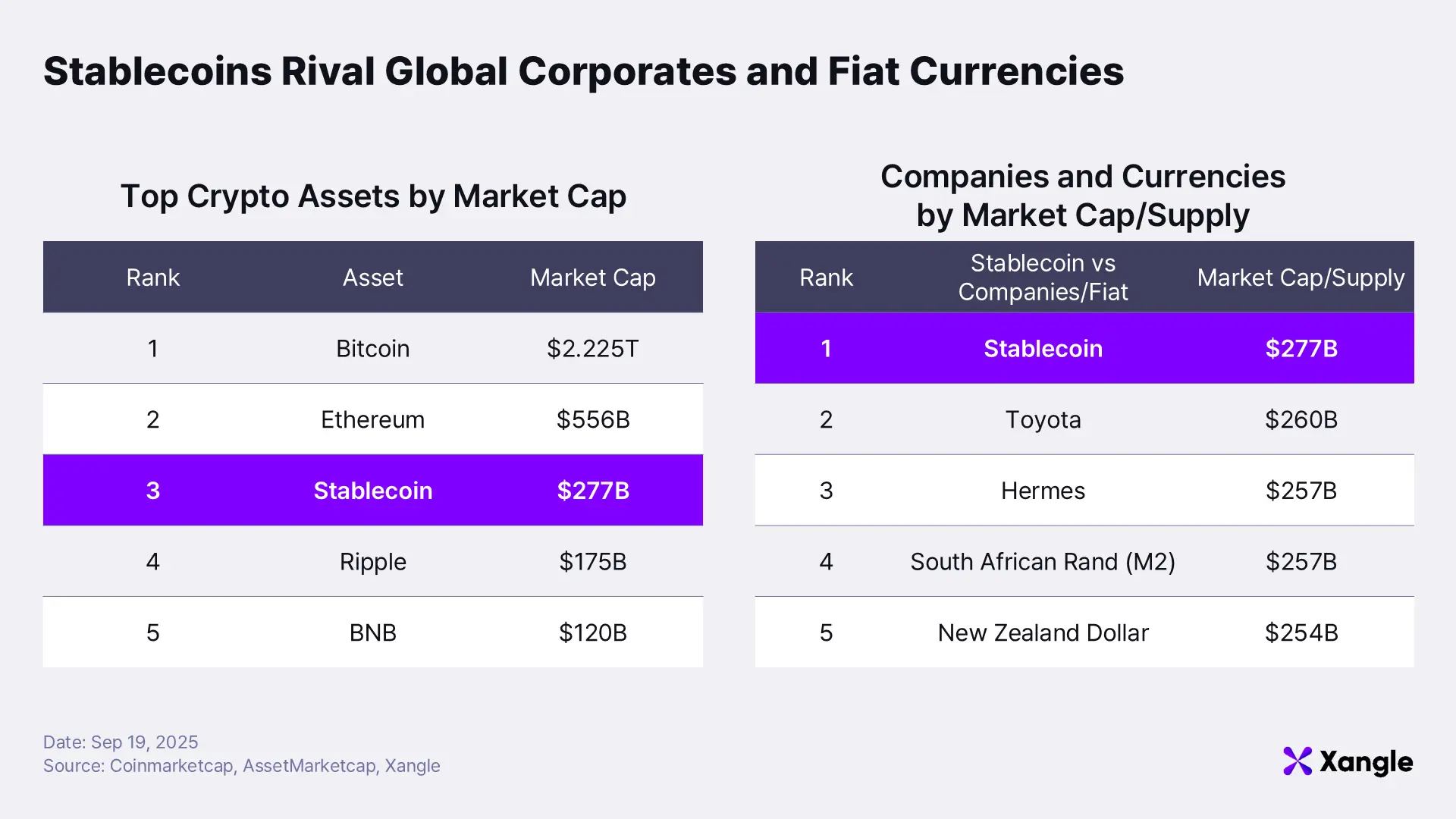

The total market capitalization of stablecoins currently stands at $277B, ranking third after Bitcoin ($2.225T) and Ethereum ($556B). This figure is more than 50% larger than the market cap of Ripple ($175B), which is the third-largest non-stablecoin crypto asset, underscoring the enormous demand for stablecoins. To put the size into perspective, the market capitalization of stablecoins surpasses that of global corporations such as Toyota Motor Group and Hermès, and even exceeds the M2 money supply of national currencies like the South African rand and the New Zealand dollar.

The growth trajectory of stablecoin market capitalization makes this rapid expansion even clearer. In early 2024, the total market cap was around $130B; in just 21 months, it has more than doubled to $277B. If this pace continues, the influence of stablecoins is likely to expand at an even more explosive rate. Given that their scale already rivals that of national currencies and their growth rate remains steep, the societal and policy implications of stablecoins can no longer be treated as peripheral issues.

2-2. On-Chain Data Validating Stablecoin Adoption

Source: Visa Onchain Analytics

Source: Visa Onchain Analytics

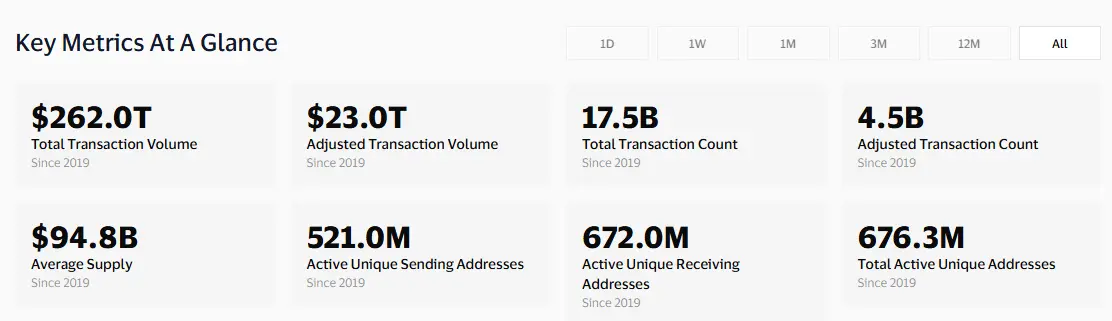

Beyond market capitalization, on-chain data also illustrates how widely stablecoins are being used. From 2019 to the present, the number of wallets that have sent or received stablecoins at least once has reached 676 million, with cumulative transaction volume of $262T (*adjusted: $23T) and a total of 17.5 billion transactions (*adjusted: 4.5 billion). While these figures may be somewhat inflated due to individuals creating multiple wallets and the inclusion of contract addresses, even if we conservatively assume one-tenth of the figure—67.6 million unique users—that would still exceed the population of South Korea.

*Adjusted transactions: data excluding bot activity, high-frequency trading (HFT), and internal circulation.

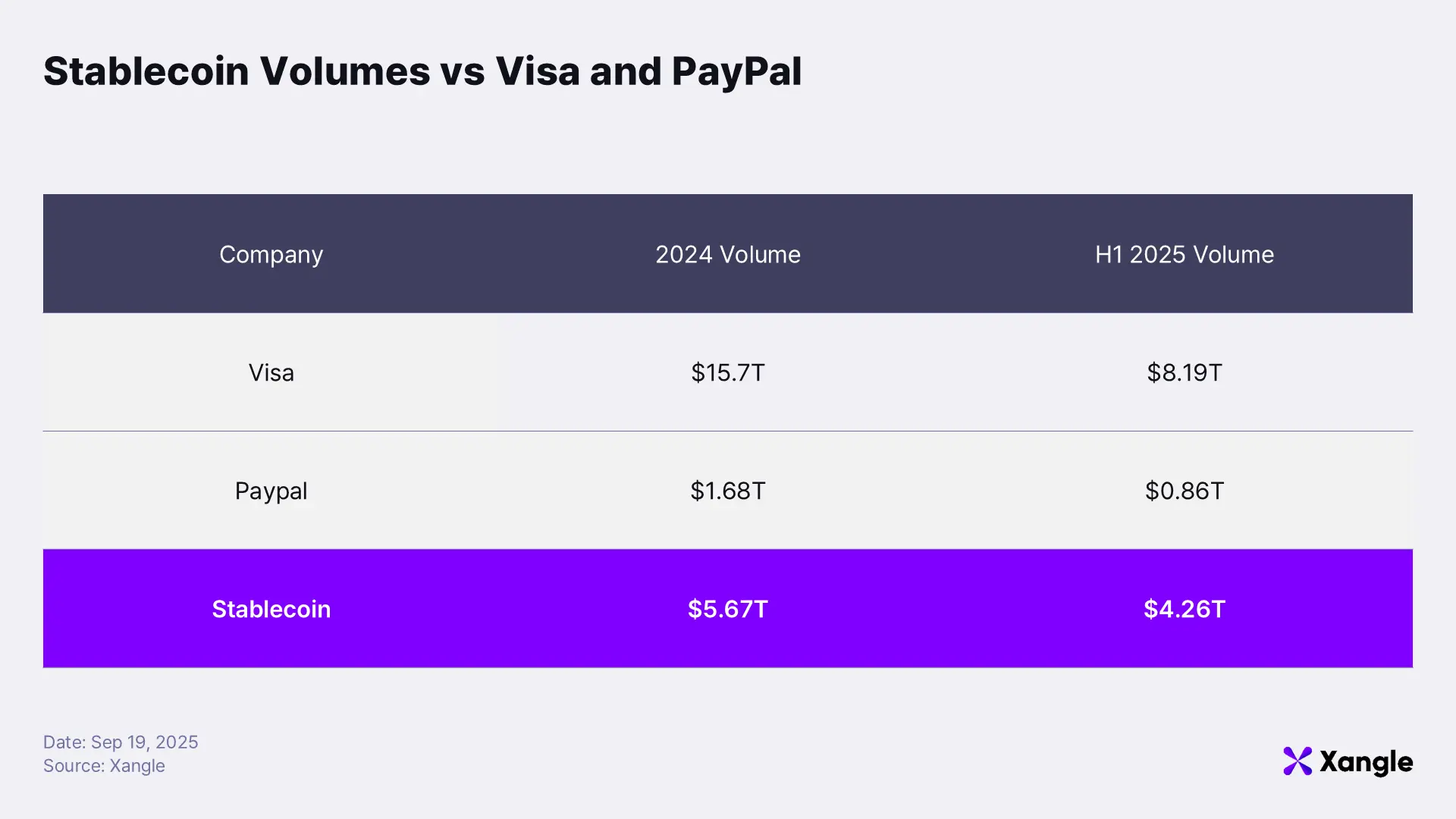

When compared with traditional payment giants, the scale of stablecoin transaction volume becomes even more striking. In 2024, Visa and PayPal recorded transaction volumes of $15.7T and $1.68T respectively, while stablecoins reached $5.67T—less than Visa but more than triple PayPal. By the first half of 2025, Visa and PayPal processed $8.19T and $0.86T respectively, while stablecoins processed $4.26T—about five times PayPal and nearly half of Visa. This demonstrates the pace at which stablecoins are becoming competitive with legacy payment systems.

Source: Stablecoin Playbook - Rui Shang

Source: Stablecoin Playbook - Rui Shang

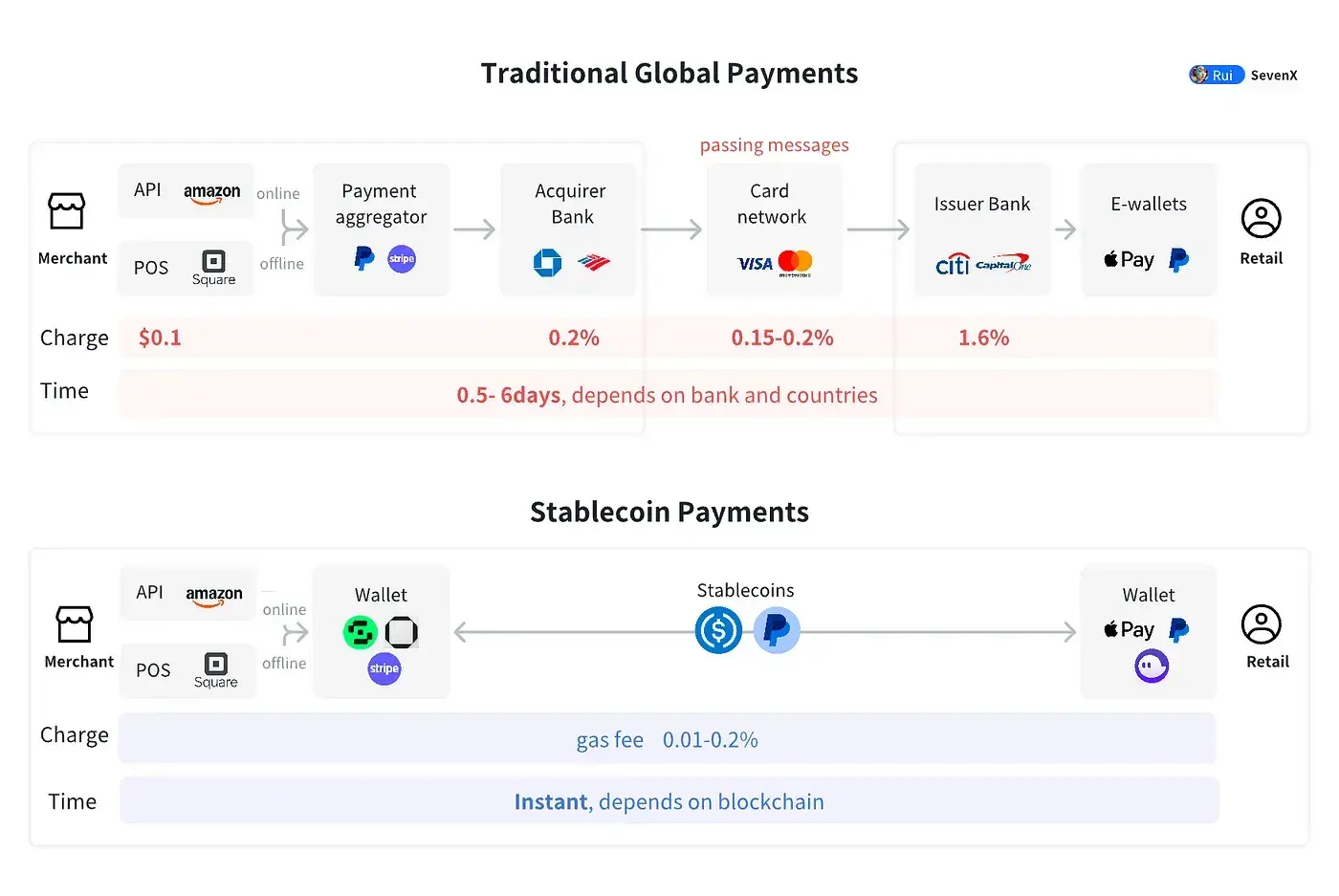

The explosive growth in stablecoin market capitalization and transaction volume is primarily attributable to their superior speed and lower cost compared to traditional fiat-based financial systems. Legacy global payment networks involve multiple intermediaries—payment processors, acquiring banks, card networks, and issuing banks—each adding fees of 0.1% to 1.6%. Final settlement typically takes at least half a day and up to six days. In contrast, stablecoin transactions eliminate most intermediaries, requiring only blockchain gas fees of about 0.01% to 0.2%, with settlement effectively occurring in real time, depending on blockchain confirmation speeds.

Smart contracts further enable trustless transactions without human intervention, supporting payments and transfers 24/7/365. Beyond that, programmable payment logic allows conditional disbursements, escrow, and automatic split settlements—capabilities traditional payment infrastructure cannot provide.

In short, stablecoins are not merely “digital versions of fiat currency.” They fundamentally disrupt payment cost structures, elevate settlement speeds to near real-time, and introduce programmable, automated functionalities that legacy finance has never been able to offer.

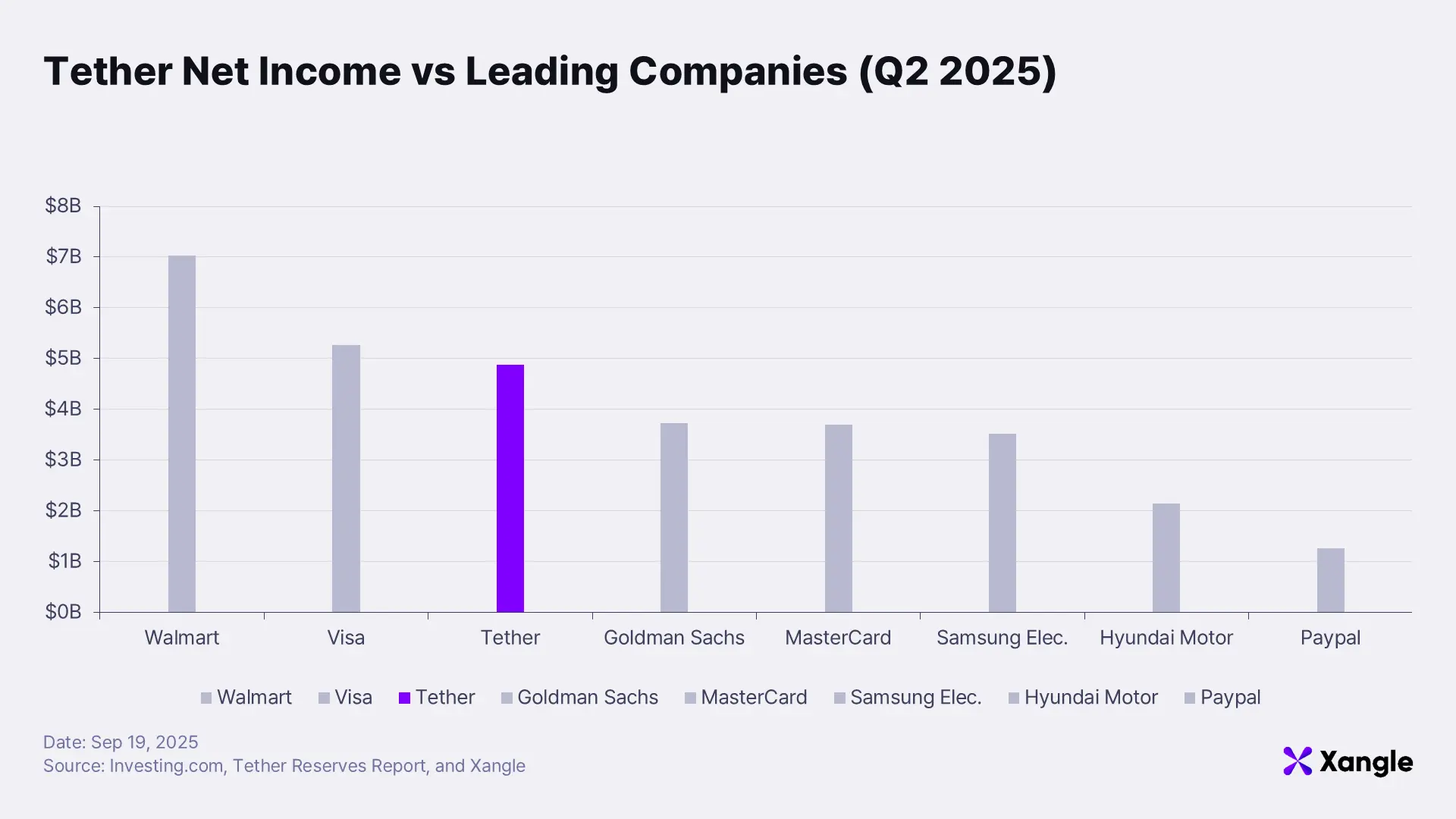

Moreover, the revenues of stablecoin issuers like Tether and Circle have grown comparable to, and in some cases surpass, those of traditional financial giants. In Q2 2025, Tether reported net income of approximately $4.9B—rivaling or even exceeding global payment companies such as Visa and Mastercard, as well as leading investment banks like Goldman Sachs. Notably, this figure also surpasses the net income of major South Korean corporates like Samsung Electronics and Hyundai Motor. In just 11 years since its founding, Tether has outpaced household-name conglomerates, underscoring the speed of its ascent. This trajectory signals that stablecoins are no longer just fintech startups but are positioning themselves as competitors and alternative infrastructure within mainstream finance—one of the key reasons why traditional incumbents are paying close attention and seeking to enter the stablecoin business themselves.

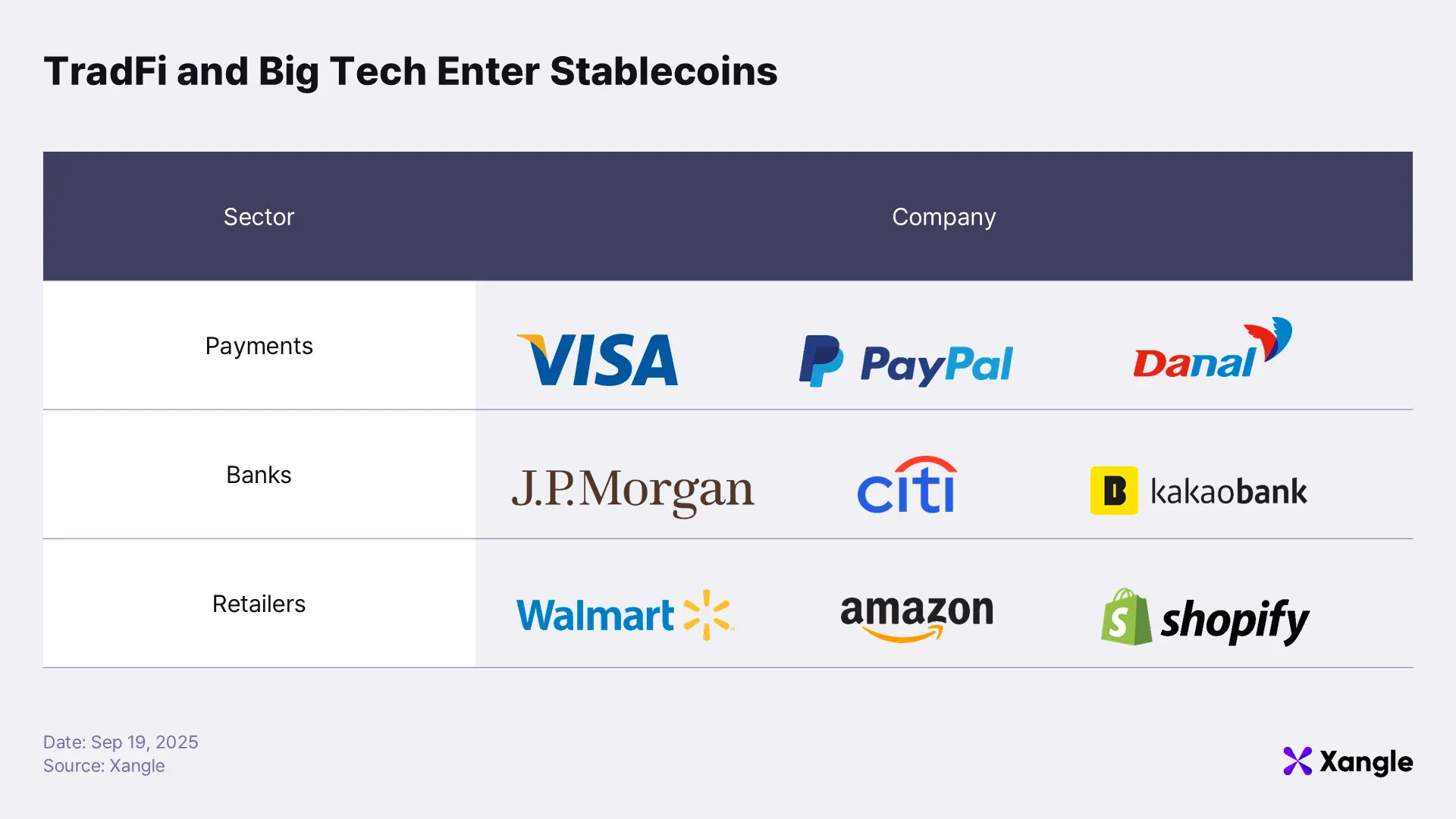

2-3. Corporate Strategies Around Stablecoins

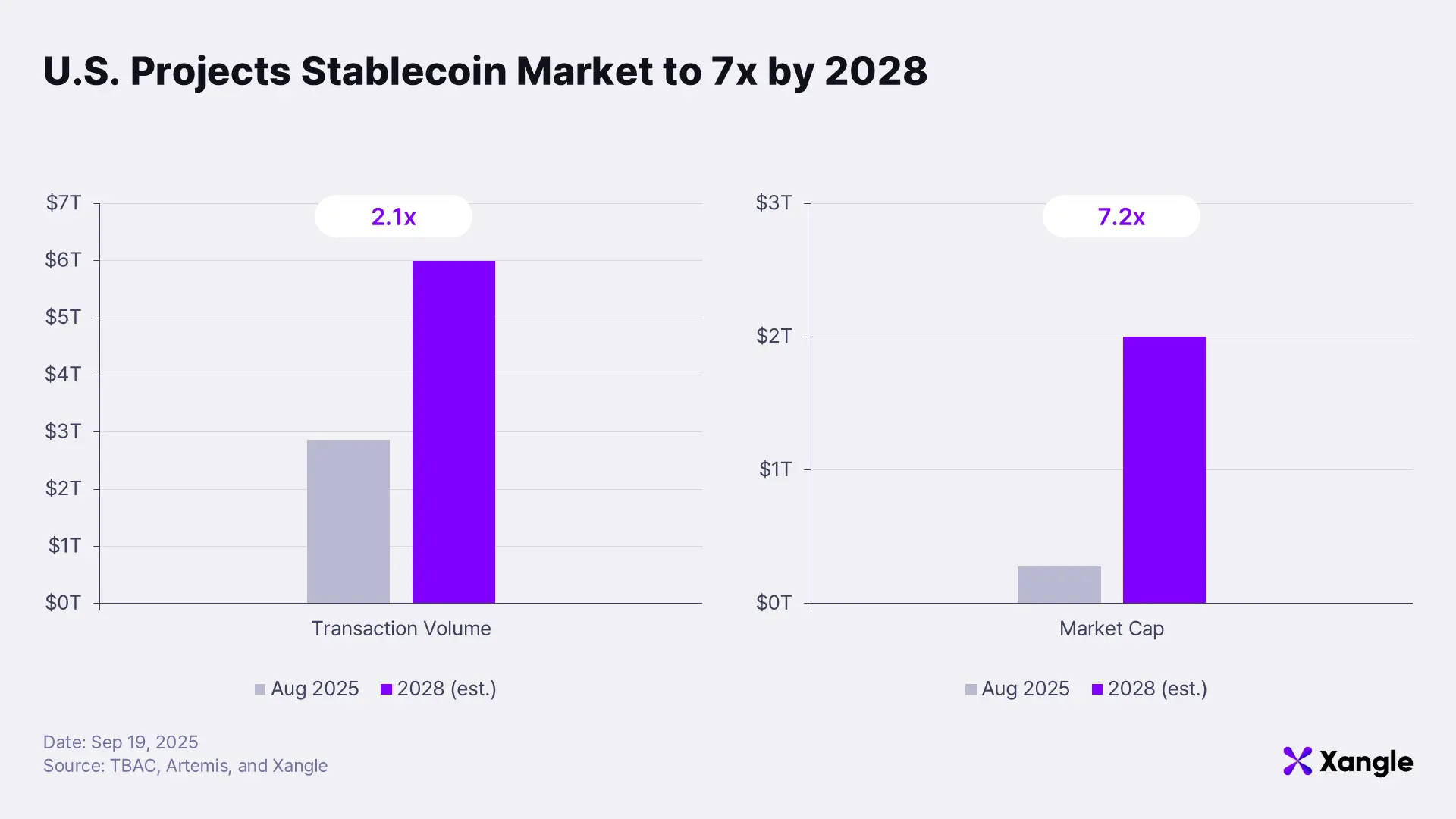

The rise of stablecoins is no longer confined to the crypto industry. Global payment networks, banks, and retailers are now moving in—clear evidence of how seriously corporates value the category’s potential. According to the U.S. Treasury Borrowing Advisory Committee (TBAC), the stablecoin market is expected to grow more than sevenfold from its current ~$200B, while adjacent verticals such as payments, cards, wallets, and custody are already expanding at pace.

We’ve already noted the profitability of the stablecoin business, but it’s equally important to examine how different types of corporates are positioning themselves and what strategic lenses they apply to the market. Recent moves by global enterprises show distinct motivations: payment networks aim to cut fees and secure first-mover advantage in new settlement rails; banks focus on defending legacy FX/remittance revenues while adopting stablecoins as modern liquidity-management tools; and retailers pursue margin gains through fee reduction and seek to lock in customers by monetizing transaction data.

Payment Companies

Among corporates, payment firms have been the quickest to move. Leading examples include global giants Visa and PayPal, as well as Korea’s Danal. For traditional payment processors, the rise of stablecoins is both an existential threat and a new opportunity. Their core revenue model, card transaction fees, faces direct disruption, as stablecoins operate on fee structures far below the traditional 1–2% card model. This is a technological shift significant enough to reshape the entire payments industry, forcing incumbents to fundamentally recalibrate their strategies. At the same time, incumbents’ existing global networks and vast customer touchpoints give them a strong foundation to emerge as leaders in the next generation of payment infrastructure.

Visa began piloting stablecoin settlements as early as 2021, cutting pre-funding timelines in half and reducing FX costs. By 2023, it expanded its pilot to major global acquirers such as Worldpay and Nuvei, marking the start of commercial deployment. PayPal launched its own stablecoin, PYUSD, in 2023, initially applying it to U.S. remittances and payment services before expanding into its broader ecosystem, including Venmo. PayPal has prioritized improving user experience in micro-remittances and e-commerce through fee savings and instant settlement, while positioning PYUSD as a long-term entry point into the global cross-border payments market. In Korea, Danal has been the most aggressive mover. As the country’s only crypto-based payment gateway, Danal commercialized real-world stablecoin payments through its subsidiary PayProtocol’s “Paycoin Mastercard.” It is also expanding internationally through partnerships with Alchemy Pay in Vietnam and the Philippines, while exploring integration with Ripple’s RLUSD and developing unified remittance/payment systems on Avalanche and Ripplenetworks. These efforts aim to create a ready-to-deploy framework for immediate commercialization once local regulation is in place.

Banks

Global banks have also been among the earliest movers in experimenting with stablecoin infrastructure. JPMorgan has operated JPM Coin on its proprietary blockchain Kinexys since the early 2020s, enabling real-time USD and EUR settlement for corporate clients. This model bypasses correspondent banks and the legacy SWIFT network, compressing settlement times from days to minutes. Citi has advanced along similar lines with Citi Token Services, allowing institutional clients to execute blockchain-based cross-border payments and cash management, actively positioning stablecoins as a lever for institutional efficiency. In Korea, KakaoBank has taken a central role in Kakao Group’s dedicated stablecoin task force (TF). The CEOs of Kakao, KakaoPay, and KakaoBank meet weekly to design an integrated business model spanning platform, payments, and banking, with plans to onboard Kakao Games and Kakao Pay Securities as the initiative scales into a group-wide project. Kakao has identified a KRW-backed stablecoin as a future growth engine, leveraging its ability to combine platform reach, payments infrastructure, and banking services to establish early market leadership.

Retailers

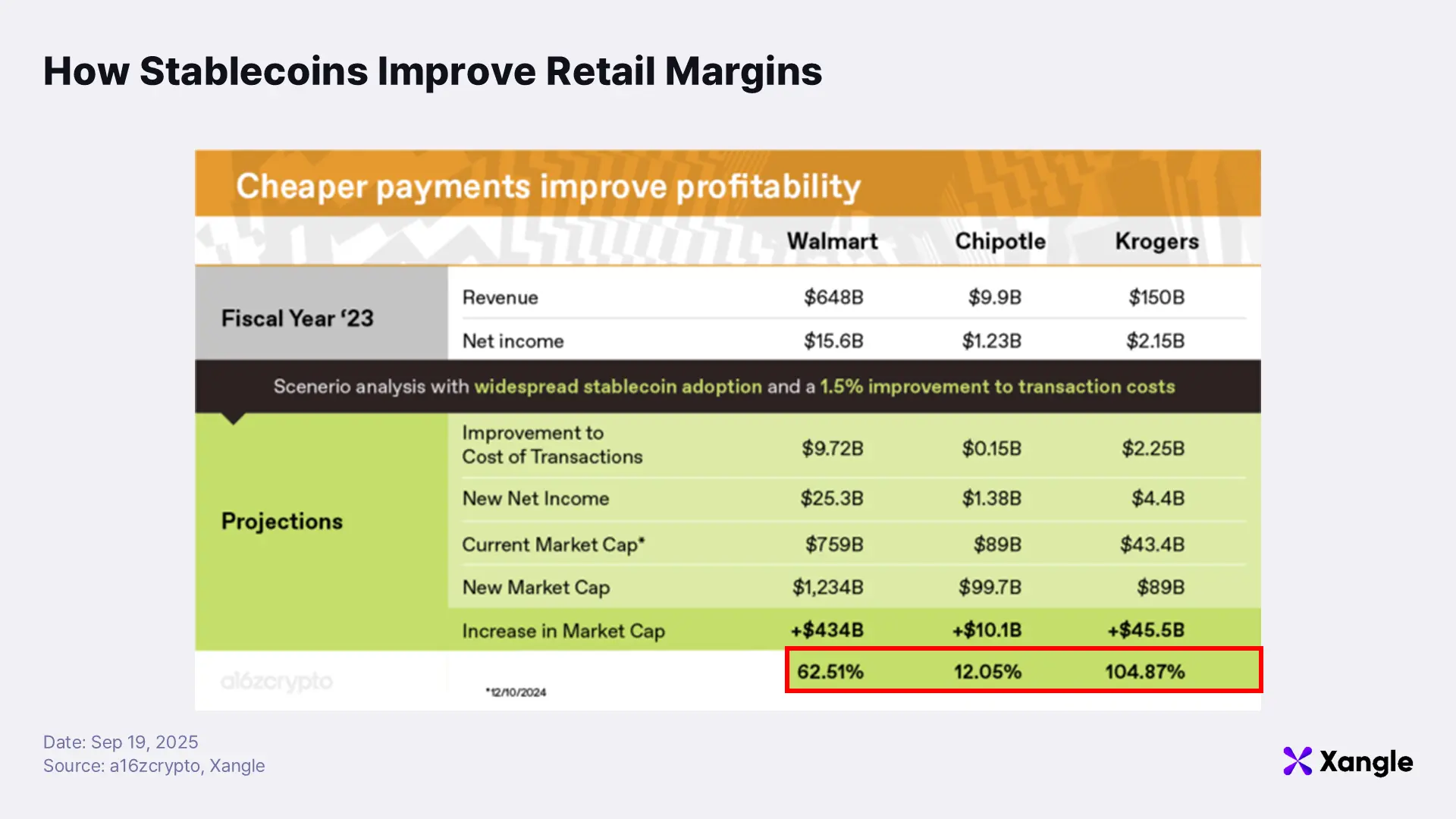

Retailers are also moving quickly into the stablecoin space. Walmart and Amazon are exploring in-house stablecoin issuance as a way to reduce card fees and improve margins, while Shopify has enabled its retailers to accept payments in USDC and other stablecoins. For low-margin retail sectors, the impact is significant: according to a16z, Walmart could increase net profit by 60%+ solely from fee savings, while supermarket chains such as Kroger could see profitability nearly double.

Stablecoins’ global interoperability adds another powerful use case in international commerce. Global retailers like Amazon can bypass local payment networks and FX conversions, offering faster and cheaper cross-border transactions. Every transaction is also recorded on-chain, enhancing transparency, while automated settlement simplifies reconciliation and improves supply-chain efficiency. Thanks to these advantages, leading retail enterprises increasingly see stablecoins not merely as a payment method, but as strategic infrastructure to overhaul cost structures and support global expansion.

That said, direct issuance requires caution. The global stablecoin market is already dominated by Tether (USDT) and Circle (USDC) in a duopoly reinforced by strong network effects and economies of scale. Liquidity is highly concentrated around the incumbents, making it structurally difficult for newcomers to compete. Even PayPal, despite its global brand recognition, has seen its stablecoin PYUSD stall at around $1B in circulation, falling short of becoming a universal settlement rail. With regulatory thresholds rising under the U.S. GENIUS Act, Europe’s MiCA, and other regimes, barriers to entry are becoming even higher. In this environment, partnering with incumbents like Tether or Circle may be a more effective strategy for corporates to secure distribution, settlement efficiency, and compliance than issuing their own tokens. Still, niche or ecosystem-specific stablecoins could continue to serve as replacements for loyalty points or closed-loop payment instruments within dedicated verticals.

3. Tether: the No.1 Stablecoin in the Market

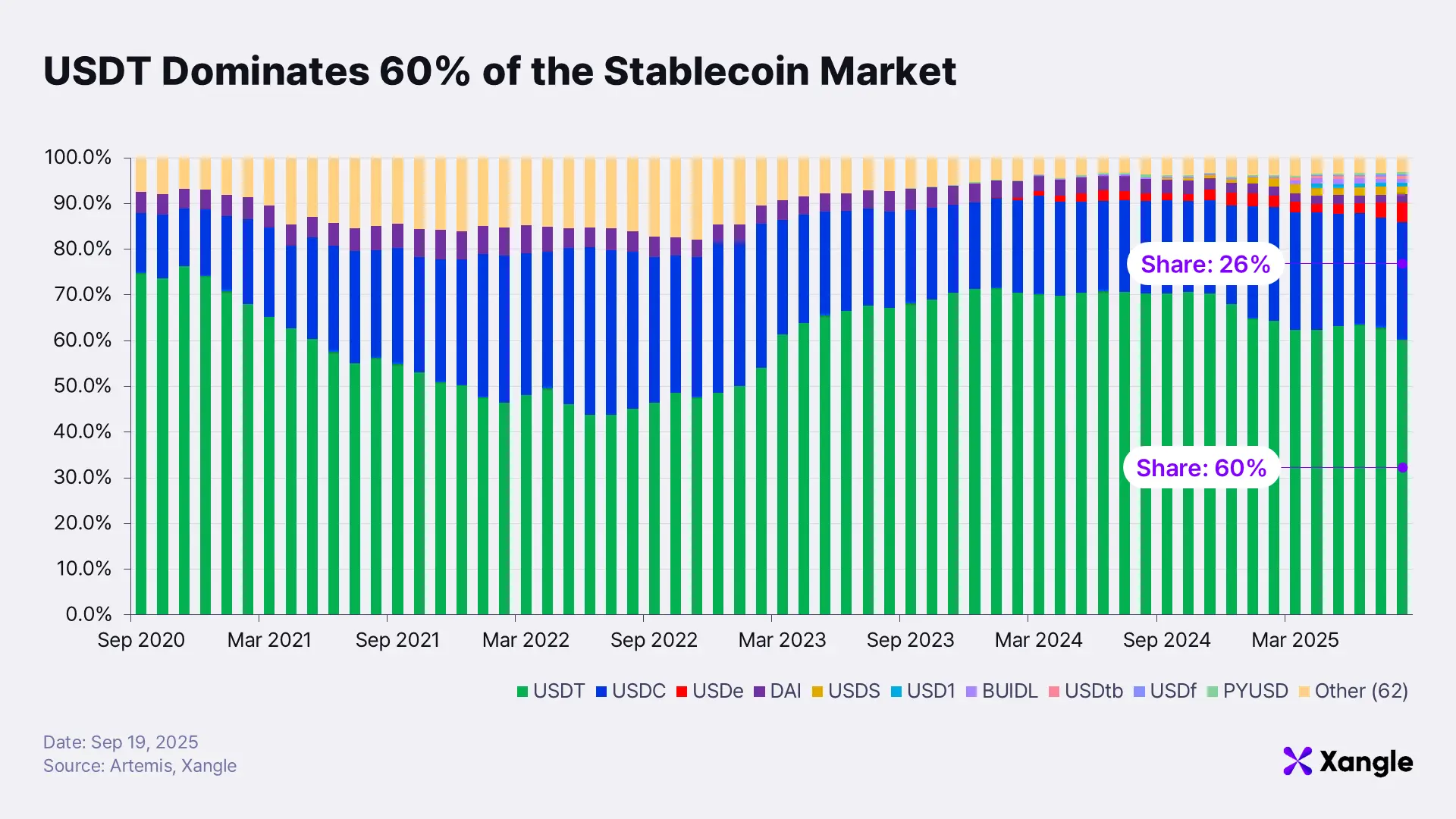

As of August 2025, Tether controls roughly 60% of the global stablecoin market, maintaining a commanding lead as the sector’s top player. While Circle’s USDC has emerged as the primary challenger, Tether still holds a decisive edge in both total circulation and actual usage. The key questions, then, are how Tether built this dominance and how the market evaluates its position today. The following section traces Tether’s growth path and business structure to better understand its market leadership.

3-1. Exchange Driven Network Effects

Tether launched in 2014 under the name Realcoin, later rebranding to Tether. In 2015, its USDT token was listed on Bitfinex, a crypto exchange under the same parent company (iFinex), which allowed it to quickly amass initial liquidity. At the time, most exchanges struggled to secure banking relationships, making fiat on/off-ramps difficult. For users, fiat deposits and withdrawals on exchanges were cumbersome. Only a handful of exchanges, including Bitfinex, Coinbase, Kraken, and Bithumb, offered limited fiat support. Platforms like Binance, which launched without fiat on-ramps, required users to first buy BTC, ETH, or USDT on fiat-enabled exchanges and then transfer them offshore. Compounding this, few exchanges yet supported stablecoin markets. Moving assets between venues usually meant relying on volatile tokens like BTC or ETH, exposing users to price swings during transfer windows.

In this unstable environment, both exchanges and users needed a stable medium of exchange, which created a natural opening for stablecoins. With USDT already listed on Bitfinex, it quickly became the preferred option for many traders, and gradually evolved into the base stablecoin and a major trading pair across multiple platforms. Momentum accelerated in August 2017, when Binance, launched just a month earlier, listed USDT. As Binance rapidly grew into one of the world’s dominant exchanges, USDT pairs became its core trading markets, creating a spillover effect across the industry. By June 2025, the number of spot pairs denominated in USDT reached 39,410—nearly 3x more than the 14,059 USDC pairs.

The combination of Bitfinex’s early adoption and Binance’s meteoric rise entrenched USDT as the de facto standard stablecoin across exchanges. This position generated a powerful network effect that extended beyond trading into payments, remittances, and DeFi, further reinforcing Tether’s dominance across the broader crypto ecosystem.

3-2. USDT’s Role in DeFi

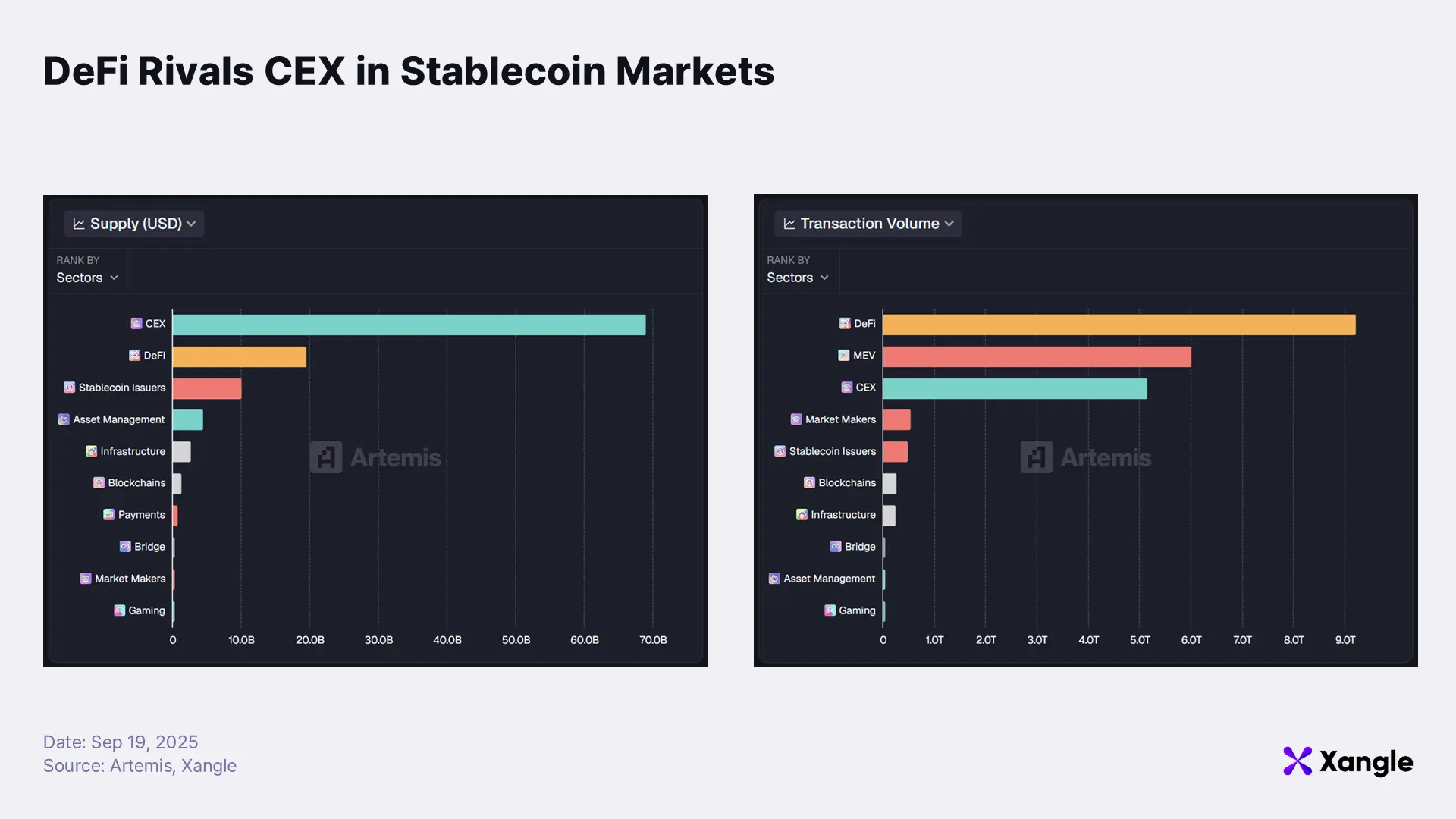

Although a large share of stablecoins is still held on centralized exchanges, on-chain transfer data suggests DeFi now accounts for the majority of stablecoin activity. It should be noted that this metric does not capture actual spot or derivatives trading within CEXs, but only transfer flows such as exchange-to-exchange or wallet-to-exchange movements, which introduces some distortion. Even so, the fact that DeFi has surpassed CEXs in on-chain transaction volume highlights its emergence as the next critical pillar of the stablecoin market.

On the lending side, Aave, currently the top protocol by TVL according to DefiLlama, illustrates how central stablecoins have become to DeFi. On Ethereum, USDT deposits total $7.41B, with $6.55B actively lent out, while USDC deposits stand at $6.02B, with $5.41B borrowed. USDT maintains a slight lead, but the data underscores that both tokens function as core collateral assets anchoring DeFi’s credit markets.

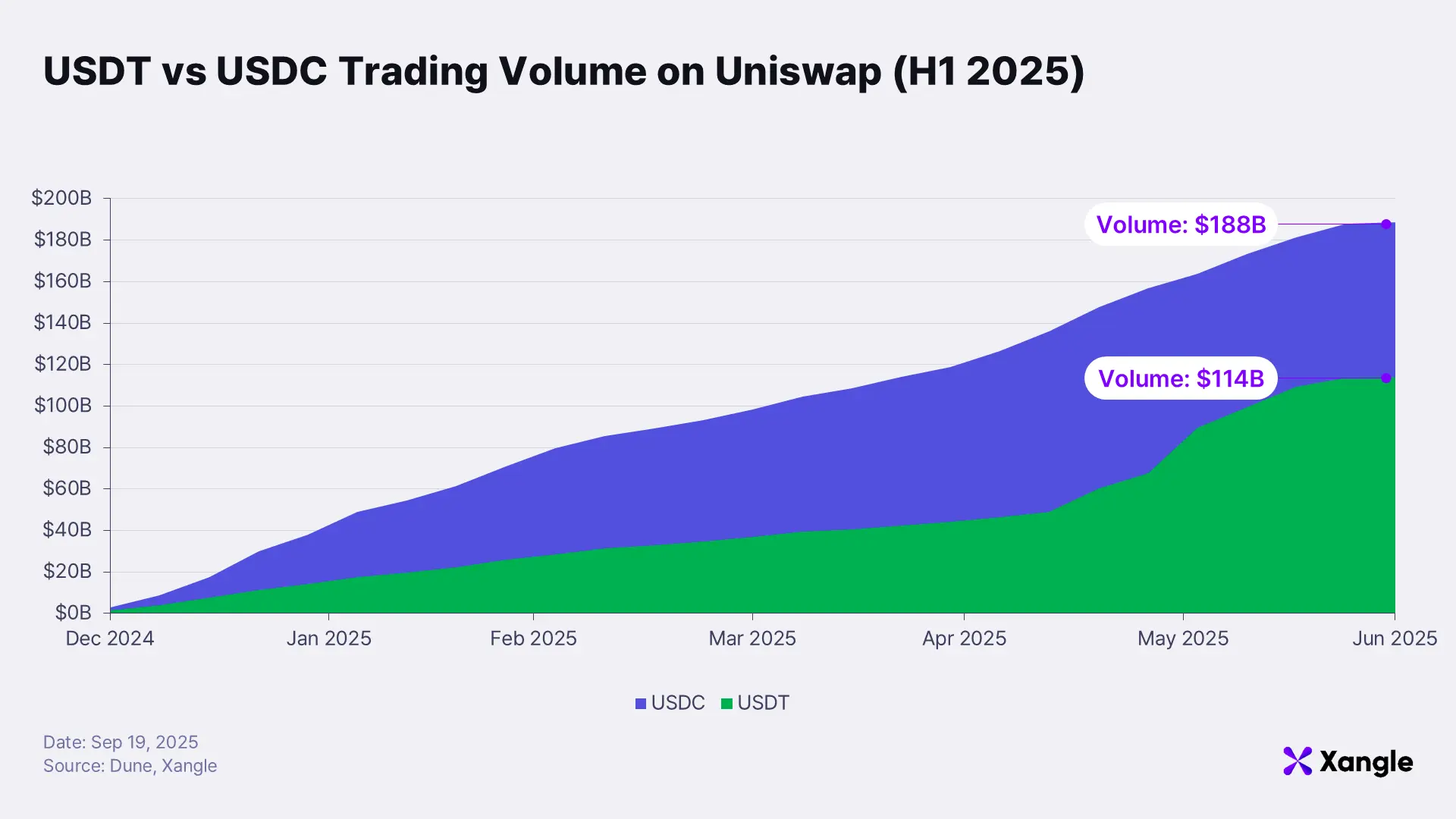

Next, consider Uniswap, the leading DEX on EVM chains. In the first half of 2025, Uniswap processed $188.7B in USDC volume compared to $114.1B in USDT—about 1.5x higher for USDC. This gap is rooted in the historical dominance of WETH/USDC pools as the protocol’s base pairs, which concentrated routing paths, order books, and LP liquidity on the USDC side. Just as USDT captured first-mover advantage on centralized exchanges, USDC’s early adoption as a core trading pair on Uniswap created a self-reinforcing liquidity loop that continues to sustain its lead.

How Hyperliquid sources asset prices from oracles

How Hyperliquid sources asset prices from oracles

Perp DEXs show yet another dynamic. Hyperliquid, one of the leading perpetuals platforms, is built on a single-collateral framework with USDC, concentrating liquidity structurally on that asset. Its spot markets are also predominantly USDC-denominated, a function of Hyperliquid’s reliance on Arbitrum, where USDC is natively supported.

An interesting nuance, however, is that while USDC serves as margin collateral, price oracles reference USDT pairs. This reflects global CEX market structure: major assets like BTC and ETH trade primarily in USDT markets, where liquidity depth and price discovery are strongest. Using USDT-based feeds mitigates manipulation risk and ensures reliable benchmarks for perpetual pricing.

As of August 19, 2025, Hyperliquid expanded support to include USDT and other stablecoins as additional quote assets. Even so, liquidity and trading activity remain heavily concentrated in USDC pairs, suggesting that USDT’s share on Hyperliquid will take time to scale meaningfully.

3-3. USDT in Emerging Markets: The Digital Dollar

Stablecoins are no longer confined to the digital space; they are now widely used in everyday life. Demand is particularly strong in developing and emerging economies where currency values are unstable and financial systems remain underdeveloped. In these regions, rampant inflation, exchange-rate volatility, and limited access to banking have turned dollar-denominated stablecoins into a practical stand-in for the “digital dollar.” Prominent cases include Argentina, Brazil, Nigeria, and Bolivia.

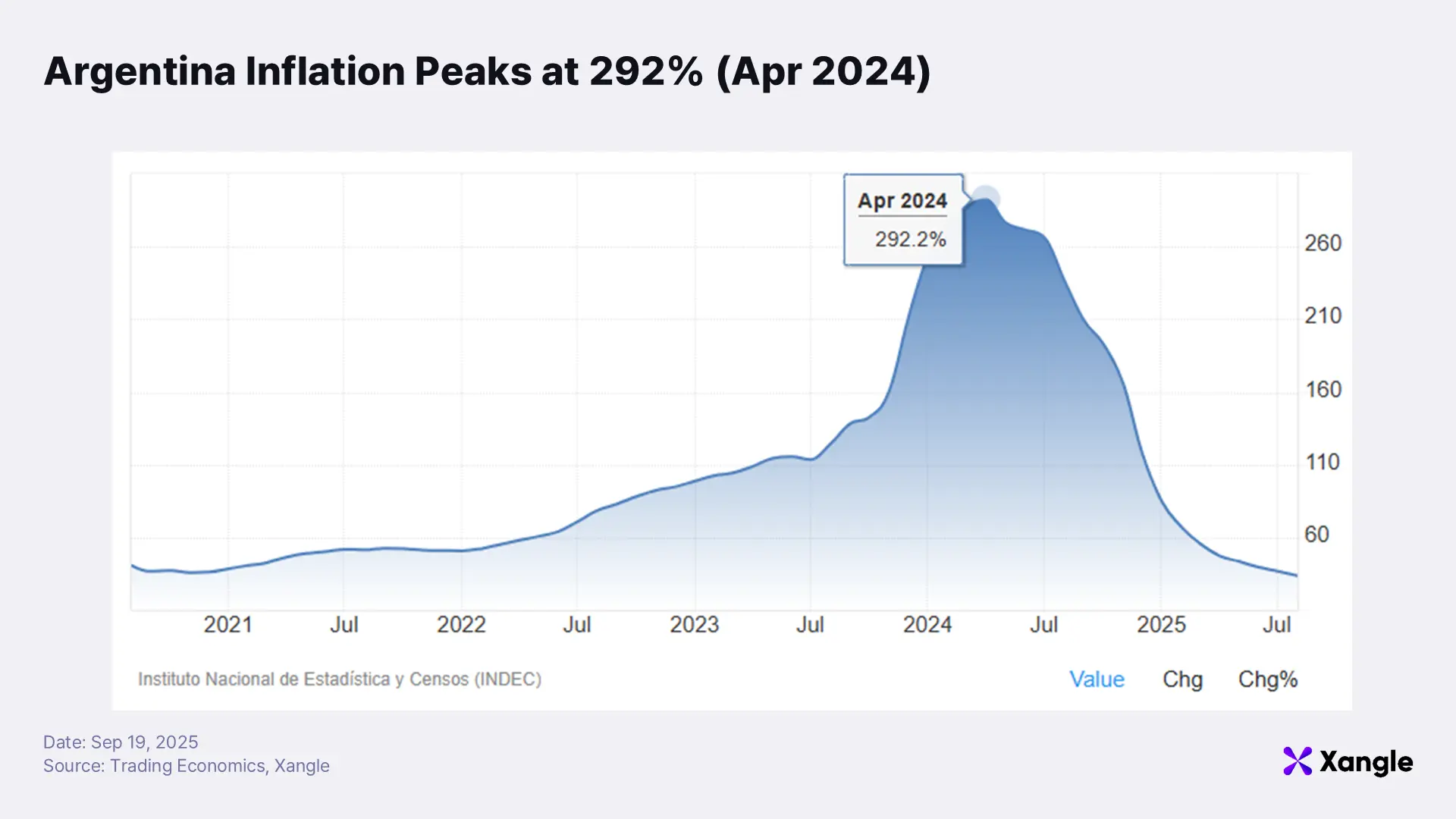

Argentina illustrates this most clearly. The peso has been subject to extreme volatility: as of April 2024, annual inflation reached 292.1%, and by August 2025 it was still running at 33.6%. To hedge against devaluation, many Argentines hold assets in stablecoins such as USDT rather than in pesos. Trust in banks and the financial system is deeply eroded. Holding pesos effectively guarantees the erosion of wealth, sustaining persistent demand for dollars. Yet even accessing dollars through banks has long been restricted—until April 2025, individuals could purchase no more than $200 per month. Worse, during the 2001 crisis, even dollar deposits in banks could not be withdrawn as dollars but were forcibly returned in pesos. These experiences drove Argentines to seek new mechanisms for securing dollar exposure, with stablecoins emerging as the most viable alternative. Today, stablecoins are used not only for savings, but also for salary payments and day-to-day market transactions, embedding themselves into the fabric of everyday economic life.

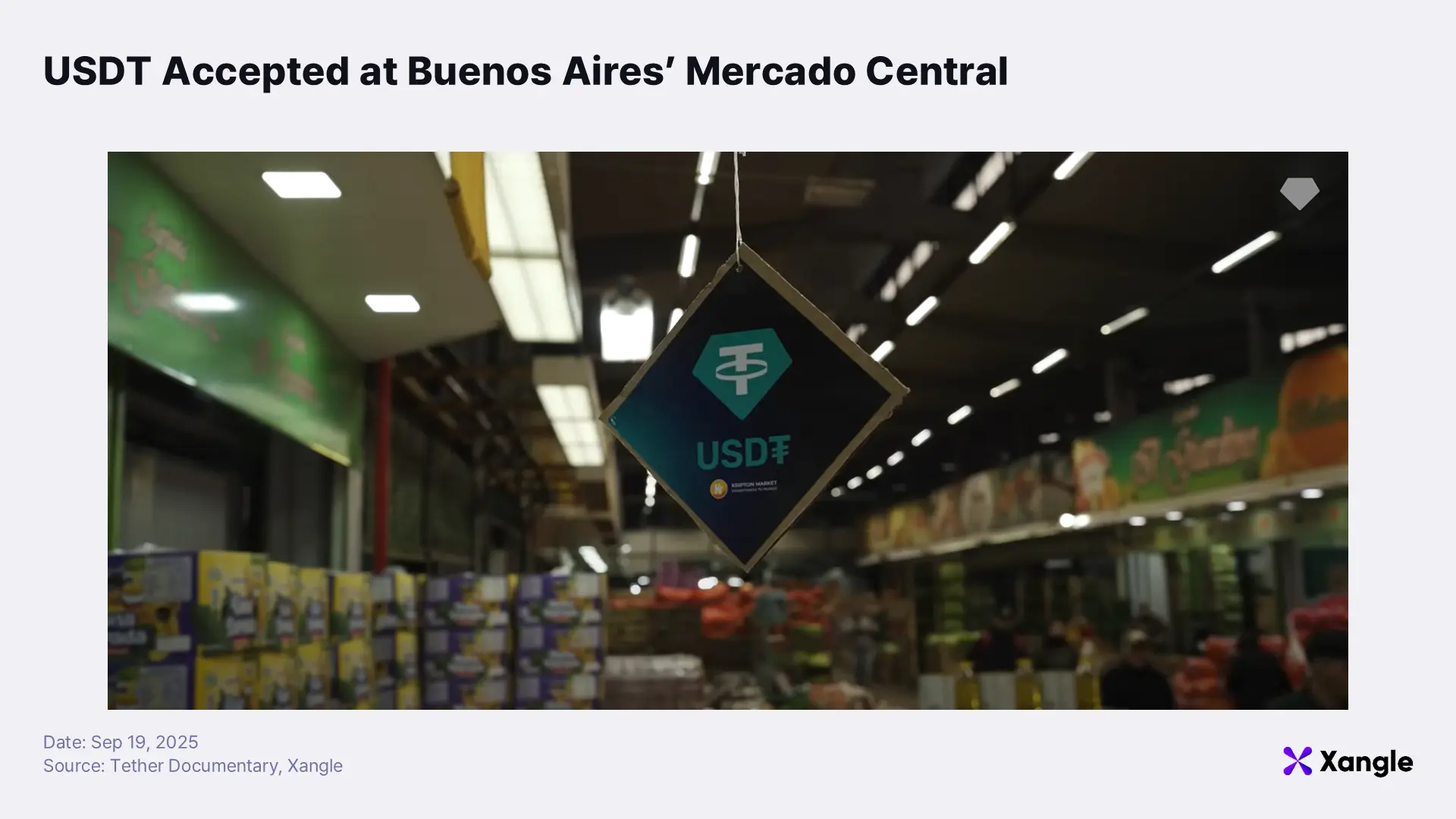

According to data from Bitso, a leading exchange widely used in Argentina, USDT accounts for 50% of trading volume and USDC 22%, far outpacing BTC (8%) and other non-stablecoins. Local crypto-fintech Kripton has also rolled out QR-code payment services, enabling Argentines to pay with USDT and other stablecoins at shops and markets—evidence of how quickly stablecoin payments are spreading into daily life.

Brazil, though not experiencing hyperinflation like Argentina, represents another key market where stablecoins—especially USDT—are deeply embedded in the financial landscape. Here, stablecoins serve not only as a hedge against uncertainty but also as an increasingly common payment method. By 2023, more than 80% of all crypto trades in Brazil were denominated in USDT, surpassing Argentina in adoption. The government-backed payments system Pix has already overtaken cash and cards as the country’s most popular payment method. Tether has partnered with local fintech SmartPay to integrate Pix with stablecoin payments, and through collaboration with TecBan, Brazil’s largest ATM operator, now enables USDT cash withdrawals at over 24,000 ATMs nationwide. These moves have dramatically expanded stablecoin usage in real-world transactions.

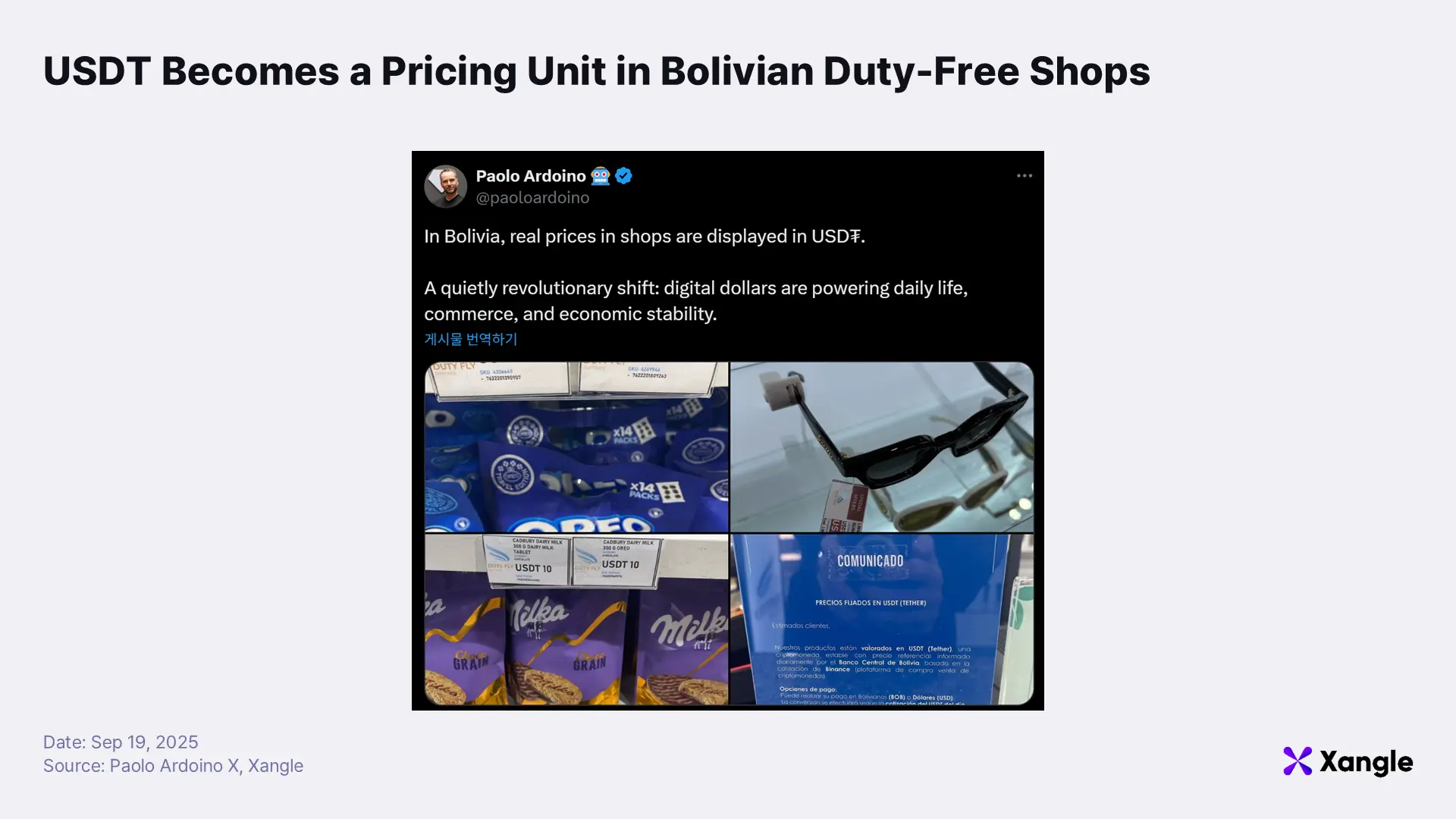

Bolivia offers another example of stablecoins entering the real economy. In June, Tether CEO Paolo Ardoino shared photos showing that Duty Fly, a duty-free store in Bolivian airports, prices goods in USDT, with payments accepted in Bolivianos (BOB) or U.S. dollars (USD). This demonstrates that stablecoins are no longer limited to exchange use but are now functioning as pricing and payment units in retail. Such cases illustrate how stablecoins can effectively substitute for local currencies in emerging markets, while also highlighting the massive growth potential these regions present to issuers. With its established network effects, Tether already commands a strong share of real-world adoption—making it increasingly difficult for latecomers to challenge its dominance.

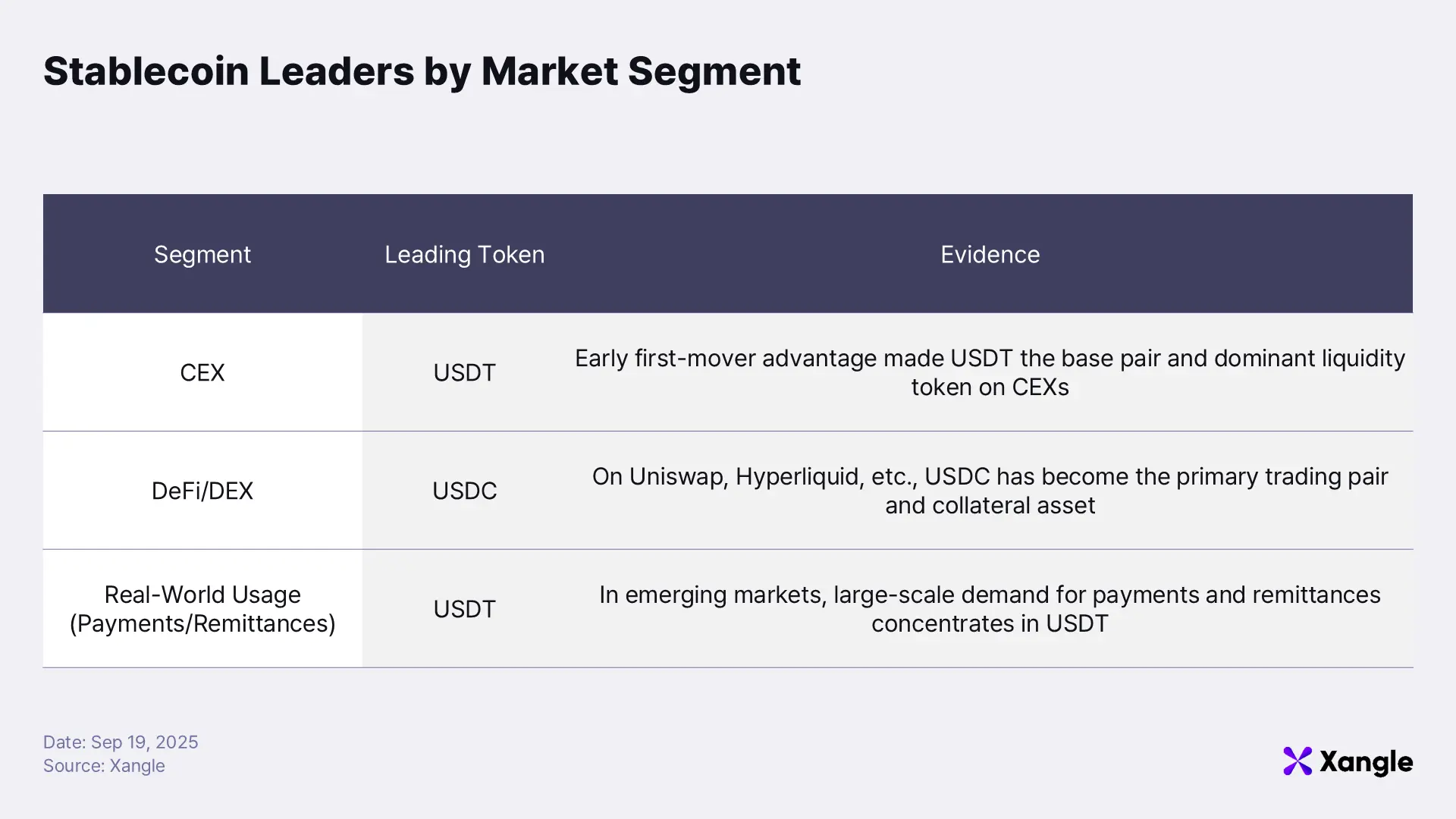

In summary, stablecoin market leadership diverges by domain. On centralized exchanges (CEXs), USDT remains dominant as the historical base currency. In DeFi, USDC has established itself as the primary trading pair and collateral asset thanks to its regulatory friendliness and robust on-chain infrastructure. But in real-world usage in emerging economies, particularly for payments and remittances, USDT leads adoption, operating as a true “digital dollar.” This reflects Tether’s ability to leverage its first-mover network effect, extending its dominance from exchanges into real-world economies. For late entrants, narrowing this gap in the near term will be extremely difficult.

4. Tether’s Path to Regulatory Trust

As discussed, Tether has expanded from exchanges and DeFi into real-world adoption across emerging markets, securing a dominant position in the stablecoin sector. But this dominance has not been maintained by network effects and demand alone. Over the course of its growth, Tether has repeatedly faced scrutiny over opaque reserves, de-pegging controversies, and regulatory pressure from governments and institutions. With the U.S. now establishing a formal regulatory framework, Tether stands at a critical juncture: beyond holding the No.1 market share, can it prove itself a trusted issuer in the regulatory era?

The most prominent example of this shift is the GENIUS Act in the U.S. Its enactment goes far beyond domestic rulemaking. Because the U.S. is the world’s largest financial and crypto market, the establishment of clear standards is set to reverberate across the entire global stablecoin industry. For jurisdictions still without dedicated regulation, the Act is likely to serve as a de facto international benchmark. This section explores what the GENIUS Act means for Tether, how the company is aligning its strategy in response, and how it is approaching markets outside the U.S.—with a particular focus on Korea and Asia. In doing so, we assess how Tether aims not just to preserve its global market dominance, but also to secure institutional trust as the foundation for its next phase of growth.

4-1. The GENIUS Act: What It Demands

To legally issue, transact, and operate stablecoin-related businesses under the GENIUS Act, issuers must comply with six strict conditions: issuer eligibility, collateral and reserve requirements, transparency and reporting/audit obligations, consumer protection provisions, AML/KYC and financial crime prevention, and a prohibition on paying interest. Each is outlined below:

-

1) Issuer Requirements

Only banks, trust companies, or specially licensed non-bank financial institutions registered with federal or state financial regulators may issue stablecoins. Issuance by unlicensed individuals or firms is prohibited.

- 1-1) Rules for Foreign Issuers: AA foreign issuer seeking to issue, sell, or broker stablecoins in the U.S. must satisfy conditions including: the U.S. Treasury Secretary’s determination that the home-country regime is “comparably regulated”; registration with the OCC; maintenance of sufficient reserves with a U.S. financial institution; and consent to U.S. legal jurisdiction.

-

2) Collateral and Reserve Requirements

All stablecoins must be fully backed 1:1 with approved safe assets. Permitted collateral is restricted to ultra-low-risk instruments such as cash, Federal Reserve deposits, short-term U.S. Treasuries, and government-backed money market funds. Commercial paper, long-term bonds, equities, and other higher-risk assets are explicitly excluded.

-

3) Transparency, Reporting, and Audit Obligations

Issuers must publish monthly reserve reports and undergo monthly attestations by a registered external accounting firm. Large issuers with more than $50B in circulation must also submit an annual audited financial statement.

-

4) Consumer Protection Provisions

In the event of issuer bankruptcy, stablecoin holders are legally guaranteed senior repayment rights, ahead of other creditors.

-

5) AML/KYC and Financial Crime Prevention

All issuers, intermediaries, and exchanges are subject to the Bank Secrecy Act (BSA), requiring full adherence to KYC procedures and Suspicious Transaction Reporting (STR) obligations.

-

6) Prohibition on Interest Payments

The Act explicitly prohibits paying interest on stablecoin holdings. Stablecoins are therefore recognized strictly as payment instruments, not as yield-bearing investment products.

The GENIUS Act allows for private issuance of stablecoins but places them under a regulatory regime comparable to bank deposits. This framework effectively elevates stablecoins to the level of sovereign money while reducing opacity and mitigating regulatory risks. As the first U.S. federal law dedicated exclusively to stablecoins, it is highly likely to serve as the de facto global benchmark for regulation. Stablecoin issuers may therefore need to restructure their business models in line with GENIUS Act requirements. For Tether, ensuring compliance with this framework has become a critical task in defending its position as the world’s leading issuer.

4-2. Tether’s Two-Track Compliance Strategy

Source: Cryptopolitan. Tether plans to issue USDT under the foreign issuer pathway while also launching a new local stablecoin.

Source: Cryptopolitan. Tether plans to issue USDT under the foreign issuer pathway while also launching a new local stablecoin.

As outlined earlier, the GENIUS Act sets requirements—licensing, 1:1 reserves, regular disclosure and audits, and a ban on interest—that are strict enough to fundamentally reshape stablecoin issuance. Tether has already begun adjusting its structure in line with these standards, conscious of its history of scrutiny over transparency and credibility. Its approach can be summarized as a two-track strategy:

-

Issuer Requirements

Tether has drawn a clear line on how it will comply. For USDT, it will maintain its existing issuance model but align it with the Act’s foreign issuer pathway, ensuring that USDT can continue to circulate legally within the U.S. CEO Paolo Ardoino emphasized:

“We’ll be working very, very hard to make sure we comply with the foreign issuer pathway within the GENIUS Act.”

At the same time, Tether is preparing to launch a U.S.-only local stablecoin tailored for institutional and corporate clients.

On September 12, Tether announced plans to launch USAT, a fully dollar-backed stablecoin designed to meet U.S. regulatory requirements, by year-end. To satisfy issuer eligibility rules, it created a dedicated entity, Tether USAT, incorporated in North Carolina, and appointed Bo Hines, former Executive Director of the White House Office of Crypto Policy, as CEO. To ensure USAT’s compliance: (i) Anchorage Digital Bank, a federally chartered digital asset bank, serves as the official issuer, meeting the Act’s requirement that only licensed U.S. financial institutions can issue stablecoins and (ii) Cantor Fitzgerald handles reserve custody, underscoring Tether’s commitment to regulatory alignment.

-

Collateral and Reserve Requirements

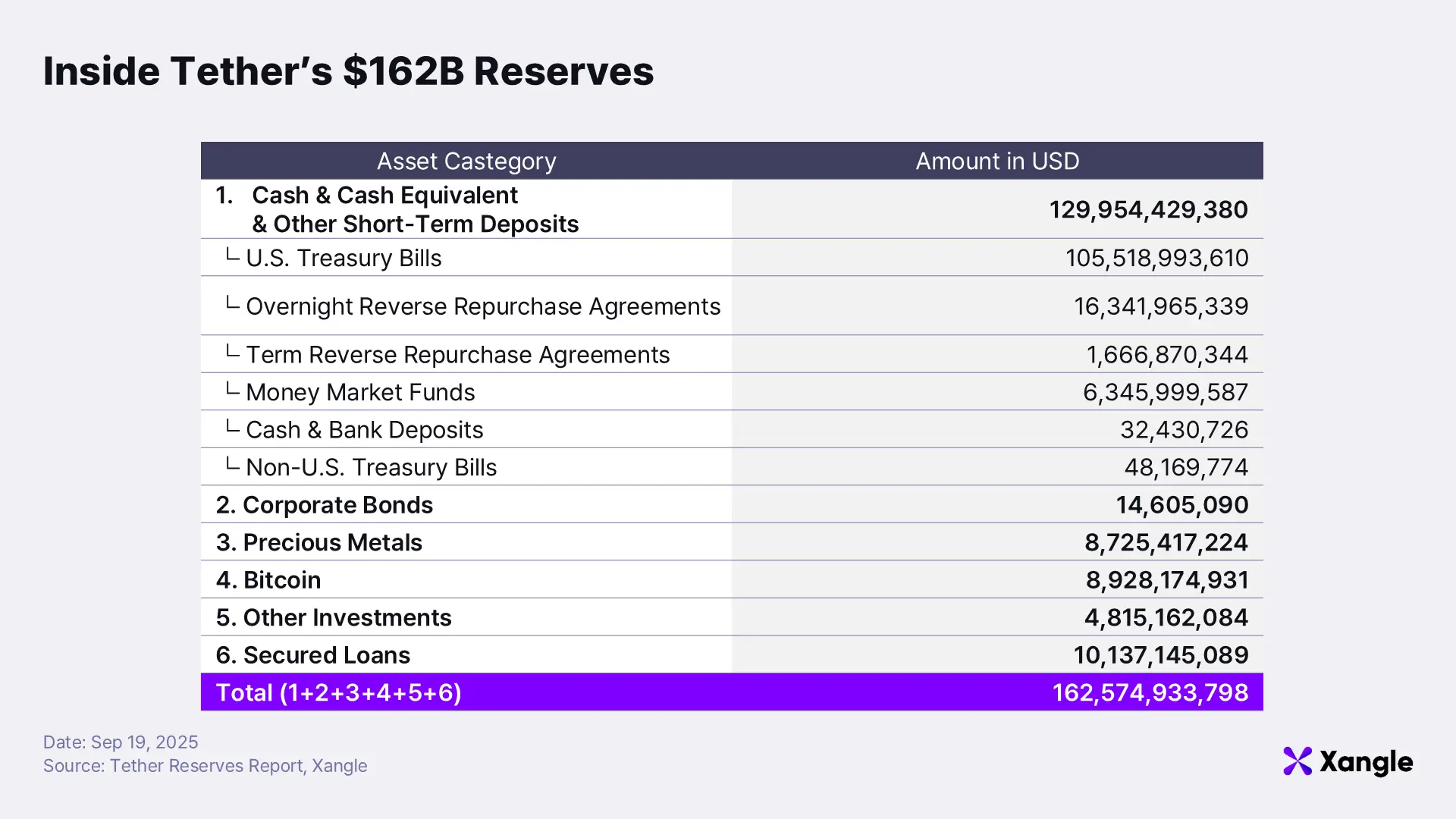

Collateralization is one of the most critical provisions of the GENIUS Act, requiring all outstanding issuance to be backed 1:1 by ultra-safe, highly liquid assets such as cash, Fed deposits, short-term U.S. Treasuries, and government-backed MMFs. Tether’s latest attestation (Q2 2025, verified by BDO) reports total assets of ~$162.5B, of which ~$129.9B (≈80%)qualify as ultra-short-term assets. These include: $105.5B in U.S. Treasuries, $18B in repos, $6.3B in MMFs, $3.2B in cash and bank deposits, and $4.8B in non-U.S. sovereign bonds.

The remaining ~$32.6B (≈20%) is held in corporate bonds, precious metals, Bitcoin, secured loans, and other investments. Under the GENIUS Act, these instruments would either be ineligible or require segregated accounting, making structural adjustments inevitable. Such changes are expected to be phased in over the Act’s three-year transition window. Reflecting confidence, CEO Paolo Ardoino told CoinDesk that they “made $13billions in profits” last year and will be able to manage it.

-

Transparency, Reporting, and Audit Obligations

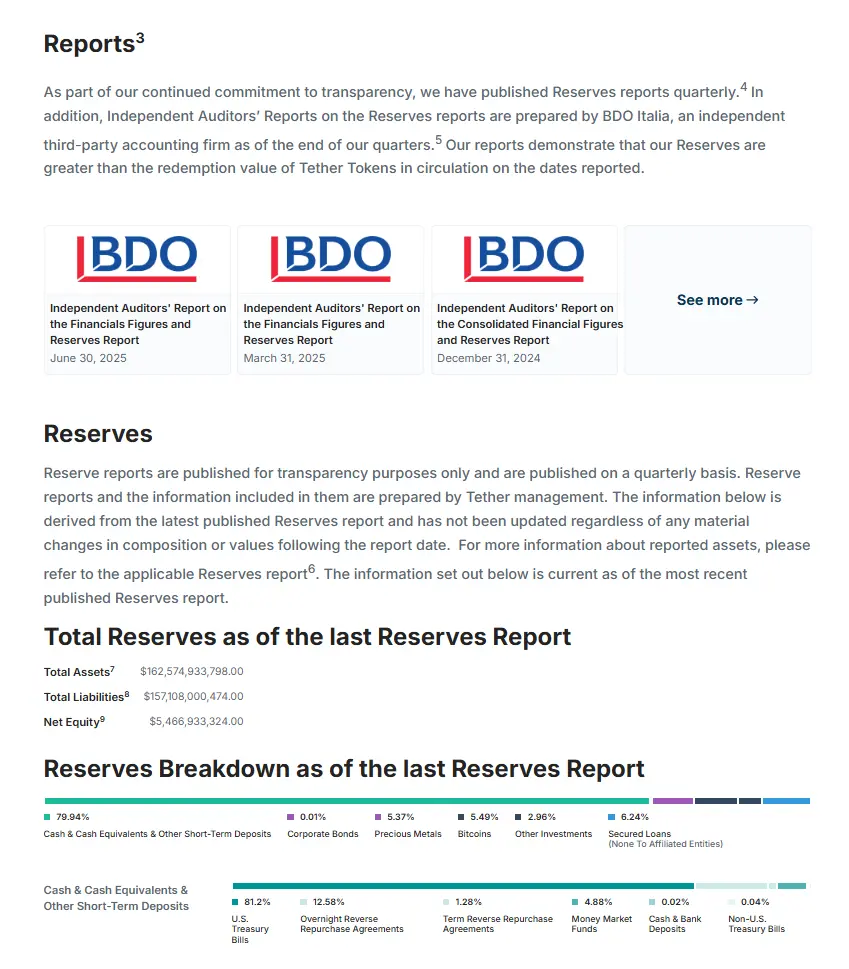

Source: Tether Transparency. Tether publishes quarterly attestation reports and a daily dashboard of circulating supply.

Source: Tether Transparency. Tether publishes quarterly attestation reports and a daily dashboard of circulating supply.Transparency has been the area where Tether has made the most visible progress. Once widely criticized for opaque reserves, Tether began commissioning quarterly attestations from BDO Italia in July 2022. BDO is part of the world’s 5th-largest accounting network, lending greater credibility to these reports. Since then, Tether has also introduced a daily reserves and supply dashboard, and is preparing to transition from quarterly to monthly attestations. This framework, quarterly BDO attestations combined with daily disclosures, has already strengthened oversight. That said, the GENIUS Act requires a full annual audit, which Tether has not yet implemented. However, CEO Ardoino has publicly committed that securing a Big Four audit is the company’s top priority, suggesting that further alignment with regulatory expectations is likely in the near term.

-

Consumer Protection Provisions

The GENIUS Act requires that in the event of issuer bankruptcy, stablecoin holders receive senior repayment rights and reserves be segregated from the bankruptcy estate. While this framework strengthens user trust, it also creates additional funding constraints for issuers navigating bankruptcy procedures. Tether’s current documentation leaves some interpretive ambiguity here, suggesting the company will likely need to refine custody and contractual structures to fully align with this requirement.

-

AML/KYC and Financial Crime Prevention

The Act also mandates that issuers, intermediaries, and exchanges comply with the Bank Secrecy Act (BSA), which enforces strict KYC procedures and Suspicious Transaction Reporting (STR) obligations. Tether has been moving in this direction for years. It enforces wallet freezes in line with OFAC sanctions lists and has cooperated with more than 275 law enforcement agencies worldwide—including the DOJ, FBI, U.S. Secret Service, and Brazilian authorities—blocking over $2.9B in illicit funds in the past year alone. Recent examples include: Freezing $1.6M tied to Gaza-based network BuyCash (July 2025), blocking $23M linked to sanctioned Russian exchange Garantex, and seizing $9M connected to the Bybit hack

By responding quickly to regulators and aligning with global AML frameworks, Tether is positioning its voluntary actions to transition into codified, standardized freeze procedures under the GENIUS Act, turning reactive cooperation into structured compliance.

-

Interest Prohibition

The prohibition on interest payments ensures that payment stablecoins cannot function as investment products. Since USDT has always been designed as a non-interest-bearing transactional token, no structural adjustment is required here.

Beyond structural adjustments, Tether has also reinforced its U.S. market strategy by appointing Bo Hines, former Executive Director of the White House Office of Crypto Policy, as both its U.S. strategy advisor and CEO of USAT. This underscores its intent to engage directly with U.S. policy and regulatory frameworks.

At this stage, Tether already aligns with much of the GENIUS Act’s intent: 1:1 reserves centered on Treasuries and cash equivalents, quarterly attestations with daily transparency, OFAC-linked wallet freezes, and a non-interest model. Key challenges remain—securing a formal annual audit, meeting the “comparably regulated” foreign issuer standard, and legally fortifying custody arrangements to guarantee senior repayment rights. Ultimately, Tether’s two-track strategy—maintaining the global USDT network while launching a U.S.-compliant local stablecoin—is designed to minimize regulatory risk and build institutional trust in the new regulatory era.

4-3. Tether’s Push Into Korea and Asia

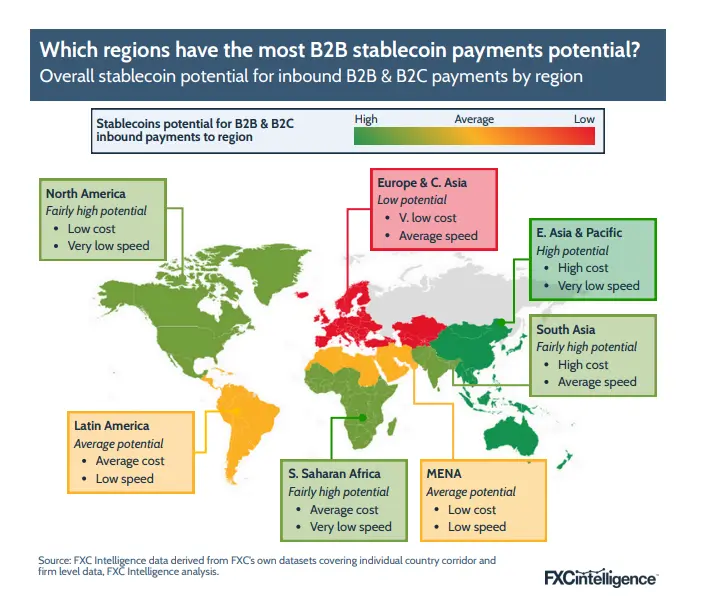

Source: FXC Intelligence, Potential for Stablecoin Payment Adoption by Region

Source: FXC Intelligence, Potential for Stablecoin Payment Adoption by Region

According to FXC Intelligence, East Asia has particularly high potential for stablecoin adoption in both B2B and B2C payments due to costly and slow legacy processes. In this region, cross-border transfers still rely heavily on multiple intermediary banks, leading to procedural delays and cumulative fees. In parts of Southeast Asia, limited foreign exchange reserves restrict access to U.S. dollars and other stable currencies, further slowing remittances. Moreover, differing AML/KYC requirements, capital movement controls, and digital asset regulations add administrative costs and recurrent delays. This makes East Asia and the Pacific one of the regions where stablecoin-based payments could deliver the greatest efficiency gains.

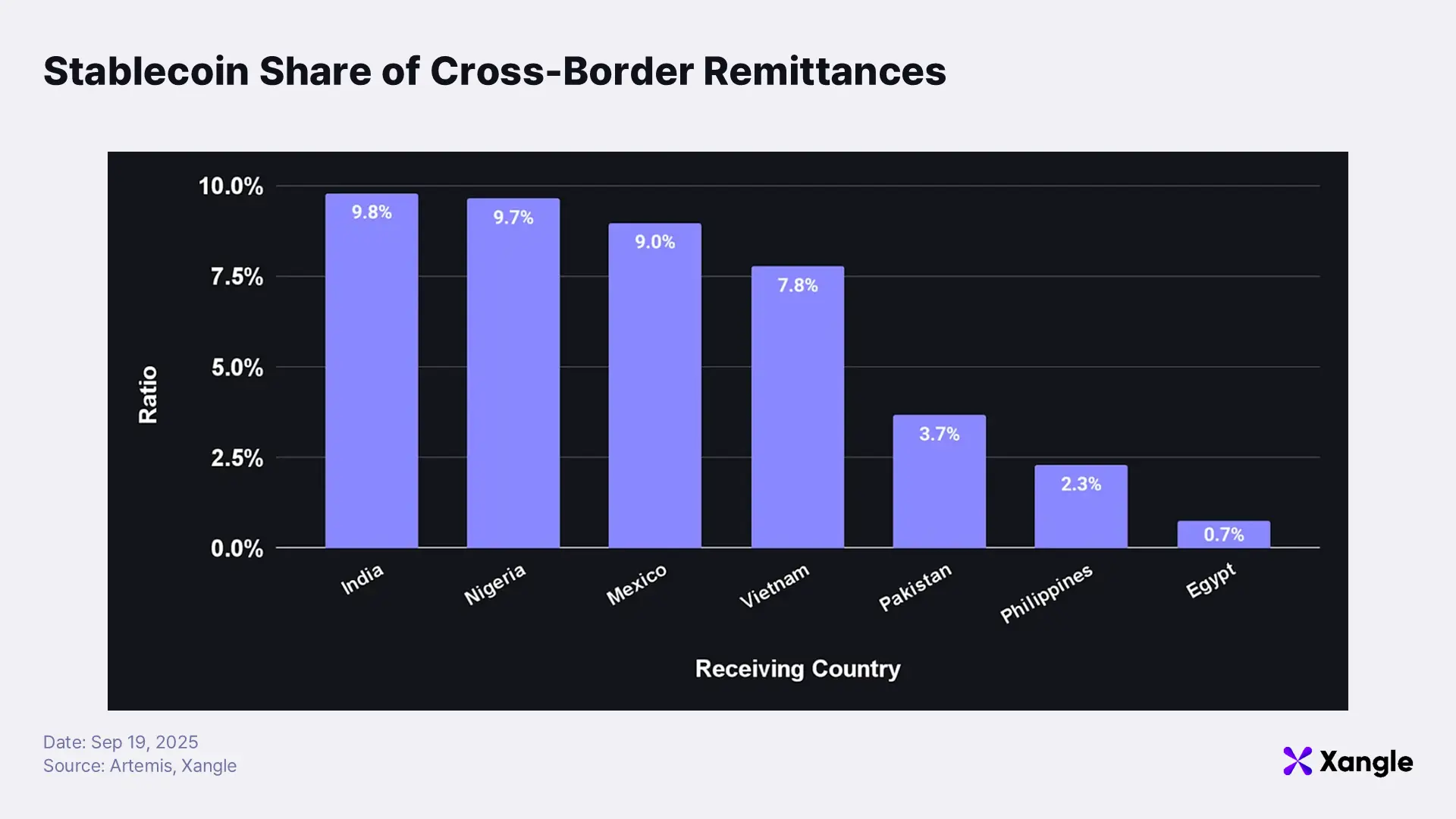

The share of remittances conducted via stablecoins is rising rapidly across major Asian emerging markets. Recent data shows that stablecoins already account for 9.8% in India, 7.8% in Vietnam, 3.7% in Pakistan, and 2.3% in the Philippines; a clear reflection of demand to bypass the high fees and delays of traditional remittance networks. In China, following tighter exchange regulations, USDT has effectively replaced the yuan as the primary settlement currency in crypto trading, with significant volumes processed daily through OTC desks and P2P markets. By Q1 2025, Asia accounted for over 45% of global USDT transaction volume, with China, Vietnam, Korea, and the Philippines emerging as the key demand hubs.

Tether is actively moving to capture this momentum. A notable example is its partnership with MetaComp, a Singapore-based cross-border FX and digital asset infrastructure provider licensed by the Monetary Authority of Singapore (MAS). In August 2025, the two companies formed a strategic partnership under which MetaComp will integrate USDT0, Tether’s unified liquidity network, into its infrastructure. Built on LayerZero, USDT0 enables USDT to operate from a single liquidity pool across chains, positioning it as a core settlement asset across global payment rails.

As part of the partnership, Tether and MetaComp set the goal of enabling real-time, low-cost, cross-chain settlement not only across Asia-Pacific, but also in the Middle East, Africa, Central & Eastern Europe, and South America. To ensure compliance, the partners will implement an on-chain AML/CFT framework incorporating wallet screening, cross-chain tracing, and real-time monitoring, establishing a settlement infrastructure that balances regulatory alignment with scalability.

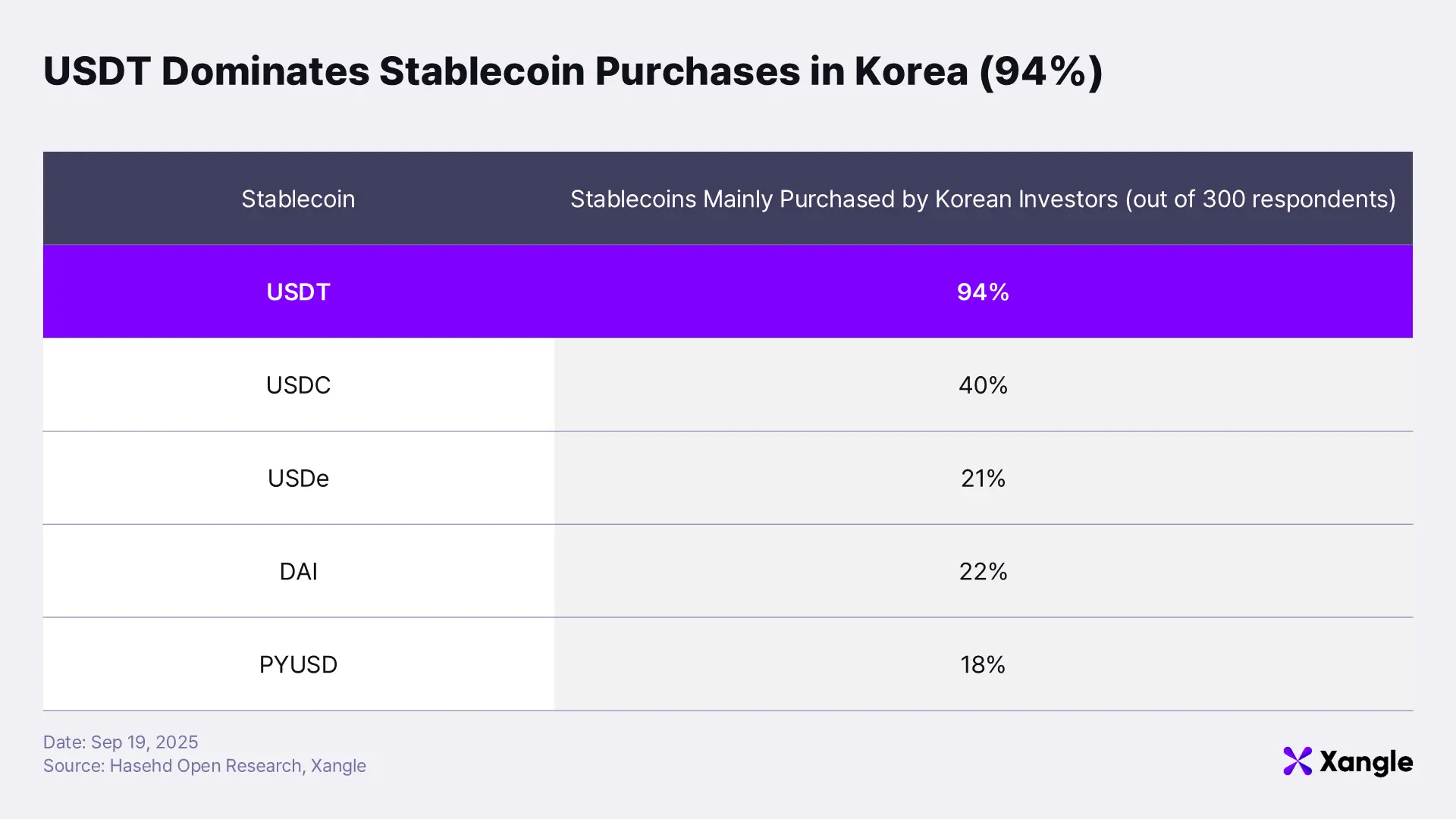

Korea in particular stands out as a strategic hub for USDT in Asia. Korea is one of the world’s largest crypto trading markets, ranking just behind the U.S. in daily trading volume. All major Korean exchanges (Upbit, Bithumb, Coinone, Korbit, GOPAX) list USDT, and Upbit even operates a dedicated USDT market alongside its KRW and BTC markets, reflecting deep liquidity. A survey of 300 Korean stablecoin users by Hashed Open Research found that 94% identified USDT as their primary stablecoin purchase, underscoring its overwhelming awareness and market share. Korean investors use USDT extensively for exchange transfers, arbitrage trading against the “Kimchi Premium,” and gaining exposure to dollar-denominated assets.

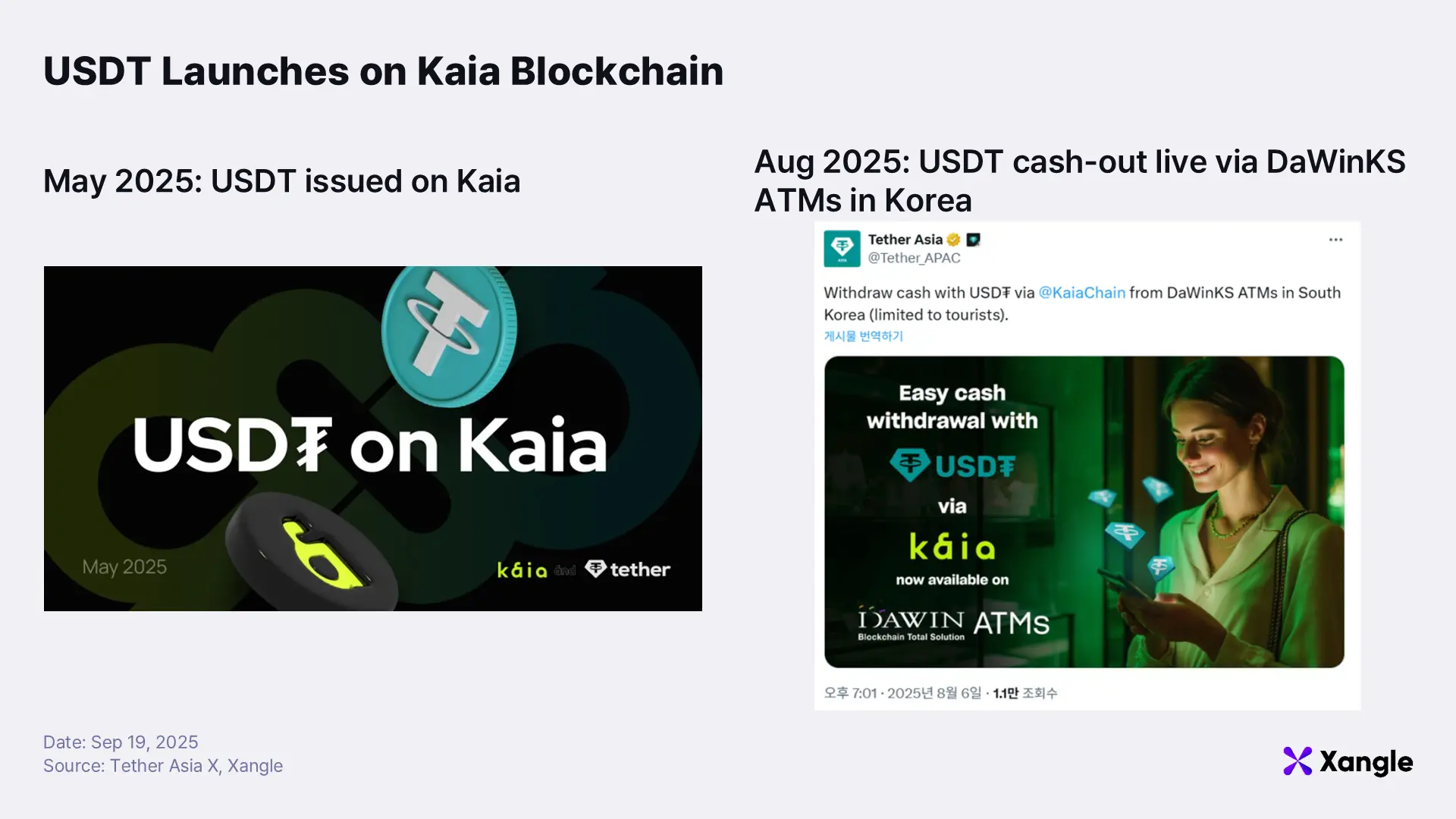

Tether views Korea not merely as a source of investment demand but as a strategic market, expanding its presence through partnerships and real-world projects. In May 2025, Tether launched native USDT on the Klaytn (Kaia) blockchain, enabling the 196 million users of the LINE messenger ecosystem to access real-time remittances, in-app payments, and DeFi services through Mini Dapps and integrated wallets. By August, Tether partnered with Korean blockchain fintech DarwinKS to introduce digital ATM cash-out services. Deployed across seven locations, including Haeundae in Busan, and Myeongdong and Namsan Tower in Seoul, these ATMs allow foreign visitors to convert Kaia-based USDT into Korean won, with plans to expand access to domestic users later in the year. This marks a milestone in directly connecting stablecoins to Korea’s real economy sectors such as tourism and retail.

Source: ETNews. Quan Li, Tether’s APAC Head, at COIN 2025 in Seoul

Source: ETNews. Quan Li, Tether’s APAC Head, at COIN 2025 in Seoul

At the COIN 2025 panel discussion in Seoul on September 3, Quan Li, Tether’s APAC Head, emphasized:

“Korea is a critical market with high adoption, trading volume, and a strong financial infrastructure.”

He also disclosed that Tether is exploring a KRW-based stablecoin, alongside partnerships not only with financial institutions but also with trading companies, fintechs, and custody providers.

If realized, such collaborations could allow export-import firms to settle trade payments with USDT at lower costs and faster speeds than traditional bank networks. Fintech and payment companies could adopt USDT as a reliable settlement asset while linking into global infrastructure. Sectors such as gaming, content, and e-commerce could leverage USDT to deliver seamless global payment experiences, helping Korean companies overcome long-standing bottlenecks in international expansion.

Korean industry leaders and policymakers share this perspective. Seochanghun Seo, Director at Toss, highlighted that stablecoins can operate seamlessly on top of existing card, PG, and remittance rails, broadening payment options. Lawmaker Byungduk Min argued that stablecoins can resolve payout issues for K-content creators, enhance payment convenience for tourists, and reduce card fee burdens for small retailers, framing stablecoins as both a livelihood technology and a growth engine. These views reflect a growing consensus that stablecoins can unlock opportunities for the Korean economy far beyond their role as investment assets.

Bo Hines, Tether Strategic Advisor, speaking at Stable stage during KBW

Bo Hines, Tether Strategic Advisor, speaking at Stable stage during KBW

Tether’s presence at KBW 2025 reinforced this focus, with Bo Hines, Tether’s Strategic Advisor, speaking on the Stable stage, underscoring the company’s strong commitment to the Korean market.

Taken together, the East Asia–Pacific region, constrained by legacy payment infrastructure and high costs, offers some of the highest potential efficiency gains from stablecoin adoption. Tether is consolidating its position quickly through a mix of partnerships, regulatory engagement, and real-world integrations, with Korea emerging as a strategic hub where USDT is already deeply embedded in trading, remittances, and retail payment use cases.

5. Closing Thoughts: Defending the Throne

Stablecoins have long outgrown their original role as trading pairs on exchanges and are now entrenched as a core layer of the global payments and settlement infrastructure. The passage of the GENIUS Act marked a decisive turning point, signaling their full-scale entry into the regulatory mainstream. From here, stablecoins must evolve from being merely fast and inexpensive remittance tools into financial infrastructure with the safety and transparency of bank deposits.

Tether has responded by strengthening its regulatory alignment: maintaining 1:1 reserves primarily in short-term U.S. Treasuries, publishing quarterly attestations and daily reserve disclosures, and advancing on-chain AML/CFT frameworks. At the same time, the company is actively diversifying its business, expanding native chain integrations for USDT, investing in Tether-backed Layer 1 projects such as Plasma and Stable, and targeting emerging marketswhere stablecoin utility is accelerating. Through Tether Ventures, it has further extended its ecosystem into adjacent sectors including artificial intelligence, biotechnology, land, and agriculture.

In a Bankless interview, Tether CEO Paolo Ardoino acknowledged that “the U.S. stablecoin market is so competitive that it is difficult to generate profits with existing business models,” adding that larger opportunities lie in emerging markets such as Nigeria. This highlights Tether’s strategic pivot toward developing economies as a key source of future growth.

Still, formidable challenges remain. Achieving full compliance with the GENIUS Act, regaining traction in DeFi, and defending against the rise of competing stablecoins are all hurdles Tether must clear. To date, USDT’s dominance has been driven primarily by its deep liquidity, sustained by first-mover advantage and powerful network effects. While these foundations make a rapid decline in liquidity unlikely, the constant entry of new stablecoin challengers ensures that competitive dynamics are shifting. For Tether, the next phase will require going beyond “abundant liquidity.” It must give users additional reasons to choose USDT—through credibility, transparency, and differentiated services. As stablecoins become formally embedded in the regulatory financial system, the key question is no longer whether Tether can maintain its lead, but how it will continue to prove its competitiveness and defend its throne.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article was written at the request of Tether. All content in this article was written independently by the author(s), and neither CrossAngle nor Tether had any editorial control or influence over the content. The author(s) may hold the cryptocurrencies mentioned in this article at the time of writing.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.