Ethena Is Not a Stablecoin: Ethena as an On-Chain Investment Bank

Table of Contents

1.Introduction: Why Institutions Struggle to Access DeFi

2. USDe: Building a Safer Ethereum

3. Risks of USDe: Liquidation and Demand Gaps

4. Ethena’s Vision: Bridging TradFi and On-Chain Finance

5. Bottom Line : Ethena as an On-Chain Investment Bank

1.Introduction: Why Institutions Struggle to Access DeFi

DeFi protocols built on the Ethereum ecosystem were designed to address the centralization and inefficiencies of traditional finance. Anyone can freely supply liquidity, borrow funds with collateral to apply leverage, or swap instantly into their desired token. Because these systems operate continuously, 24 hours a day, they hold the tremendous advantage of linking global capital markets without the constraints of time or geography.

Despite these advantages, DeFi remains far less developed than TradFi for one fundamental reason: the price volatility of Ethereum, the ecosystem’s reserve currency. While access to DeFi may be attractive, using Ethereum as the underlying asset inevitably exposes participants to its price risk. As a result, even though Ethereum’s DeFi ecosystem holds enormous potential to transform finance, the volatility challenge has made it extremely difficult for institutions to design viable financial products on top of it.

Stablecoins such as USDT and USDC exist as alternatives, but they are far from a complete solution. If Ethereum is treated as the native currency of DeFi, then stablecoins function more like a currency exchange. In eliminating Ethereum’s price risk, they also strip away the key advantages of using Ethereum itself, such as the yield guaranteed through staking.

Consider instead a protocol that could neutralize price exposure by hedging Ethereum with derivatives such as futures—essentially operating like an FX hedge. This would allow investors to preserve all the benefits of holding spot Ethereum while minimizing price risk. If such a structure were to further establish a price band that dampens volatility, Ethereum could ultimately evolve into a genuine on-chain reserve currency, serving as money on-chain without exposing holders to the price risk of any underlying asset.

No protocol has fully achieved this vision to date. The core reason is that Ethereum derivatives such as barrier options or currency swaps are not yet actively traded. By contrast, commodities and FX have long benefited from robust physical demand, abundant liquidity, and decades of market history, enabling the development of a wide spectrum of derivative instruments. Ethereum, however, remains a relatively new asset, with hedging demand still far less established. That said, one protocol has gone further than any other in overcoming these limitations: Ethena’s USDe. By maintaining delta-neutral positions—taking perpetual short contracts across multiple exchanges to offset Ethereum’s price risk—USDe is able to guarantee value stability. In doing so, Ethena has introduced the first protocol that meaningfully addresses the core structural weakness of Ethereum-based DeFi.

2. USDe: Building a Safer Ethereum

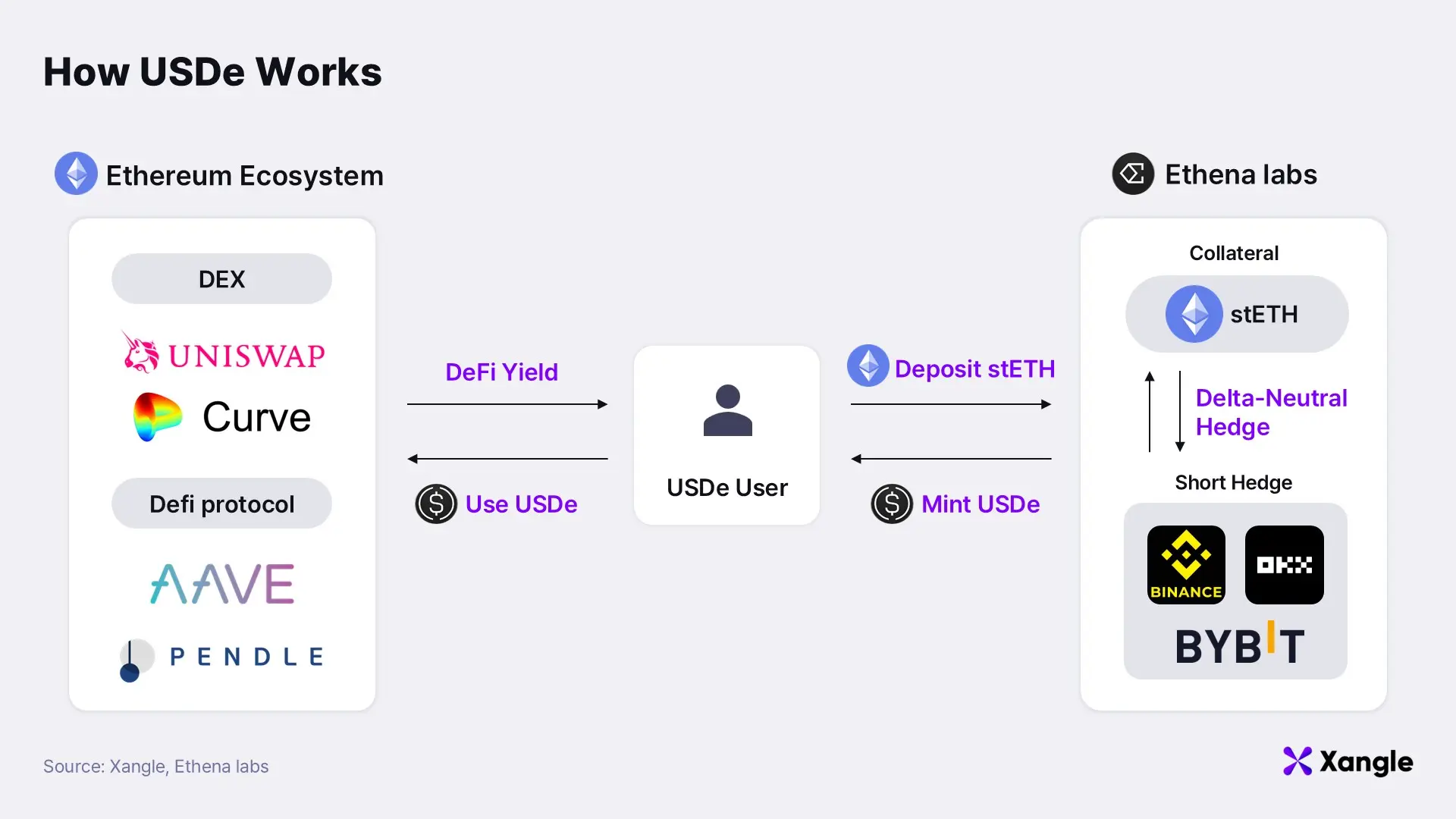

Ethena operates two core products: the synthetic dollar protocol USDe and sUSDe, a financial instrument that delivers yield on USDe. The value of USDe is kept close to $1 through a delta-neutral hedging strategy; a portfolio construction method in which futures positions that move inversely to the underlying asset offset its price fluctuations, ensuring that changes in the asset’s value do not affect the overall portfolio.

When a user mints USDe by depositing staked Ethereum as collateral, Ethena simultaneously opens a perpetual futures short position of equivalent size on derivatives exchanges. Price movements in the collateral are neutralized by the opposite movements in the short position, resulting in a delta-neutral position.

On top of this, *sUSDe redistributes the staking rewards from Ethereum and profits from funding fees, delivering high yields. This strategy not only stabilizes value but also leverages the liquidity of centralized exchanges to improve capital efficiency without requiring excessive collateral. Thanks to this structure, Ethena’s stablecoin demonstrates lower volatility compared to other crypto dollars.

*Funding Fee: When the futures price of a perpetual contract diverges from the spot price, a fee is imposed on traders holding the mispriced position to bring prices back in line. If the futures price is lower than spot, the funding fee is negative; if higher, the fee is positive. In the case of Ethereum, shorts typically receive the funding fee.

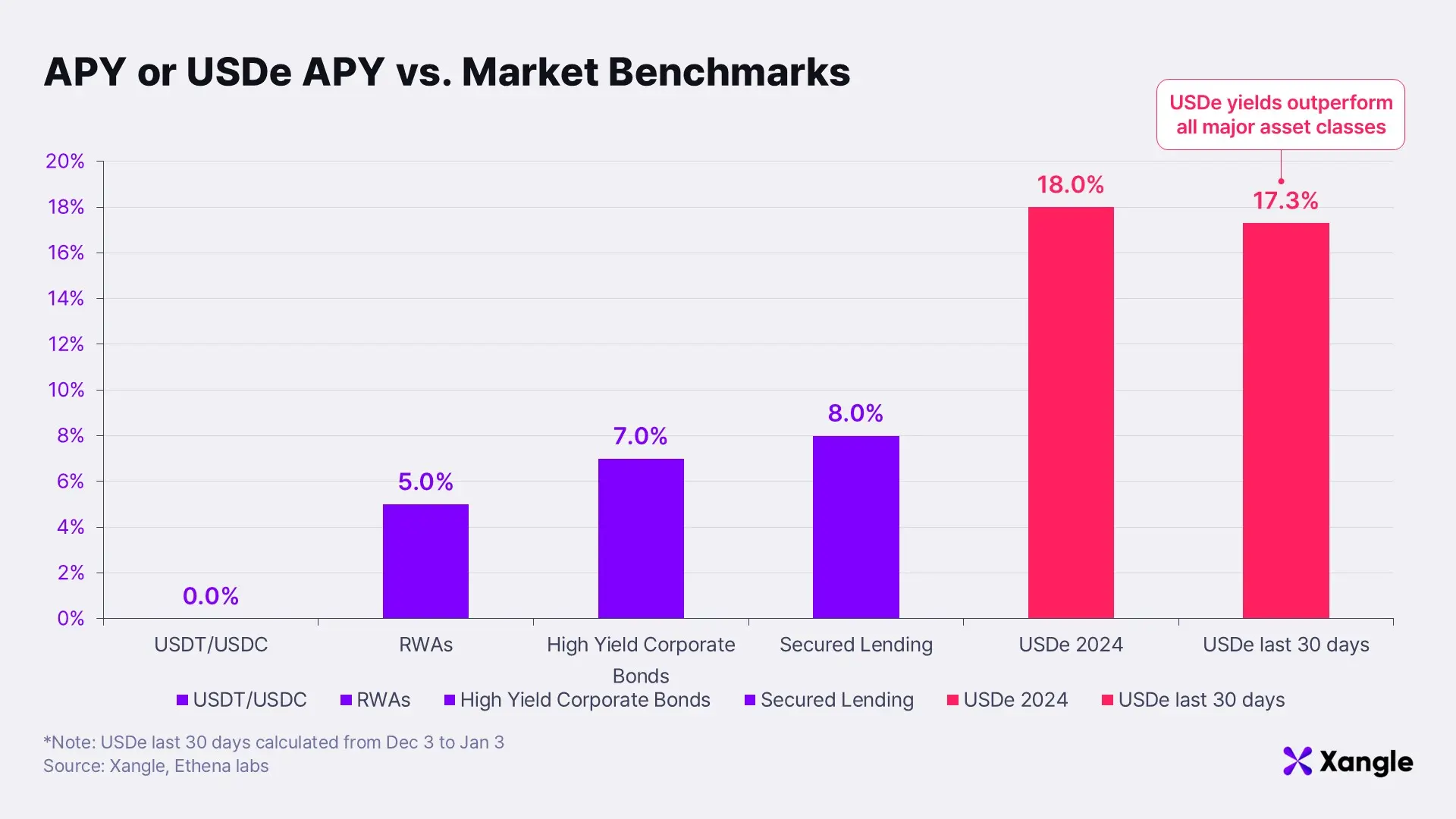

In practice, Ethena’s strategy has been highly effective: in 2024, the average APY of sUSDe was 18.0%, and in December 2024 alone, sUSDe achieved 17.3% APY. Compared with RWAs or bonds, this represents an overwhelmingly higher yield. In this way, Ethena’s USDe and sUSDe combine the effectiveness of the delta-neutral model with multiple mechanisms to minimize risk while guaranteeing exceptionally high yields. Yet the true strength of sUSDe is not merely that it is both safe and high-yielding. Since sUSDe functions not simply as a stablecoin but as a derivative-backed token anchored to Ethereum, it enables a wide array of DeFi strategies to be built on top of it.

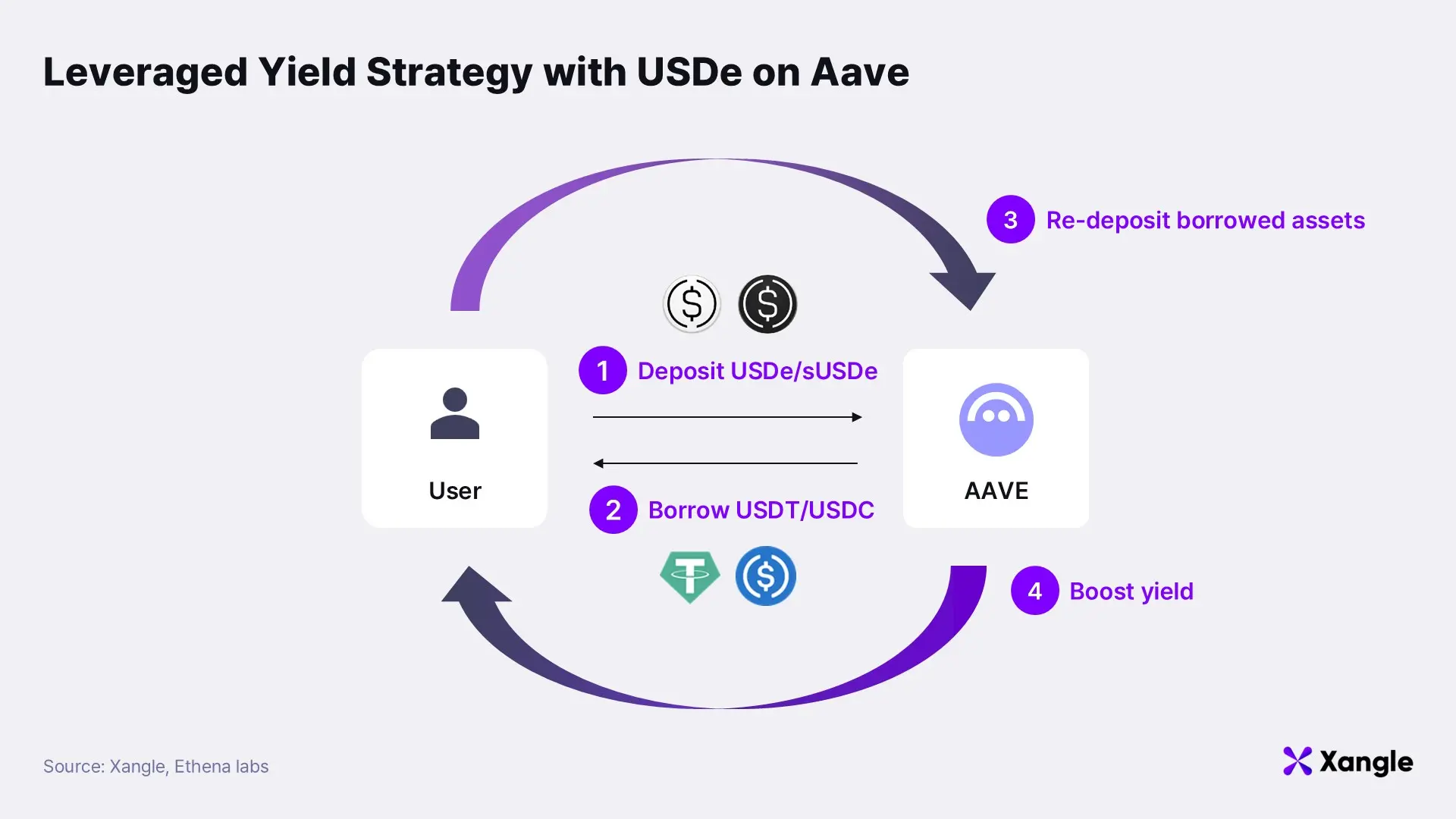

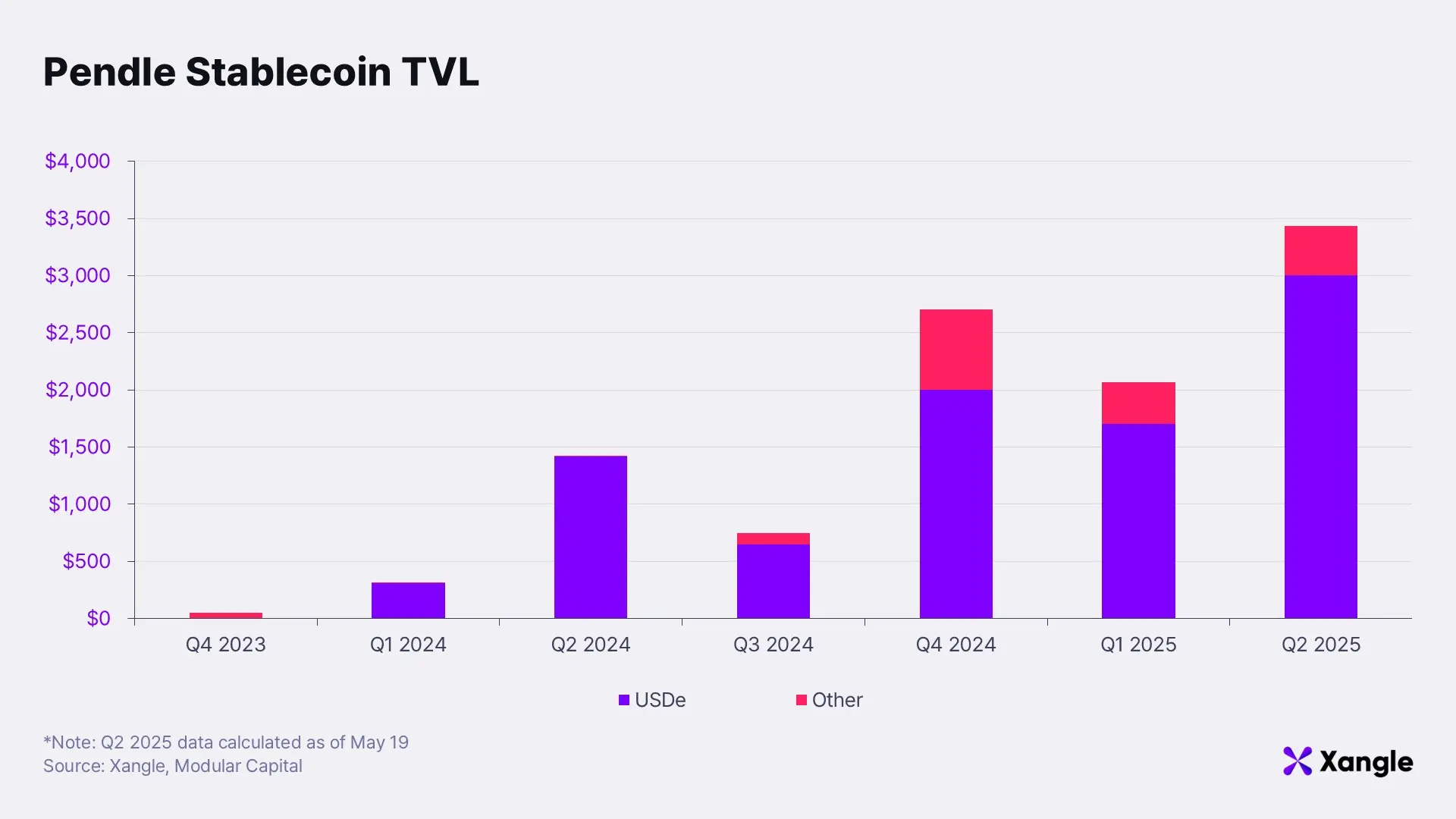

For instance, Ethena and Aave introduced “liquid leverage,” a strategy in which sUSDe can be deposited as collateral, borrowed against, and redeployed to maximize yields. Likewise, Pendle, a protocol that tokenizes DeFi yields, shows significant TVL in USDe. Yield tokens allow users to farm leverage points, while principal tokens enable them to capture stable yields. The very existence of such yield-maximization strategies is what decisively sets USDe apart from other stablecoins. Whereas most stablecoins serve merely as an FX-like entry point into on-chain assets, USDe and sUSDe open the door to significantly amplifying returns through diverse strategies. This allows investors to achieve yields comparable to other DeFi instruments like Aave or Pendle, but with far lower risk.

These attributes position USDe as a powerful tool for institutions. Directly holding Ethereum while engaging with DeFi protocols leaves them fully exposed to ETH’s price volatility. Conversely, relying solely on stablecoins minimizes risk but makes it difficult to access many of Ethereum’s native DeFi strategies, such as restaking. With sUSDe, however, institutions can stake USDe to boost yields and simultaneously deploy strategies across multiple DeFi protocols—something not possible with other stablecoins. For institutions, this makes sUSDe a highly compelling product that combines safety with attractive yield opportunities.

Thus, while USDe and sUSDe function as stablecoins pegged to the dollar, staking USDe allows users to generate returns in exchange for liquidity, or to pursue returns beyond simple staking by leveraging DeFi protocols. In this sense, they possess characteristics more akin to a native token than to an ordinary stablecoin. Put differently, USDe represents not just a stablecoin, but rather a “price-stable Ethereum” that can be used in core DeFi strategies such as lending and APR tokenization. For institutions that wish to enter the Ethereum ecosystem safely, without bearing the burden of its high volatility, USDe offers an extremely compelling option.

3. Risks of USDe: Liquidation and Demand Gaps

Despite its strengths, Ethena carries two key risks. The first is liquidation risk. Ethena minimizes exposure by benefiting from price increases in Ethereum and capturing funding fees on short positions when prices fall. Yet in scenarios where Ethereum crashes or surges rapidly, collateral value can erode sharply or positions may be liquidated on exchanges, putting pressure on the dollar peg. Even if the peg itself remains intact, market fear alone could trigger redemptions of USDe back into dollars.

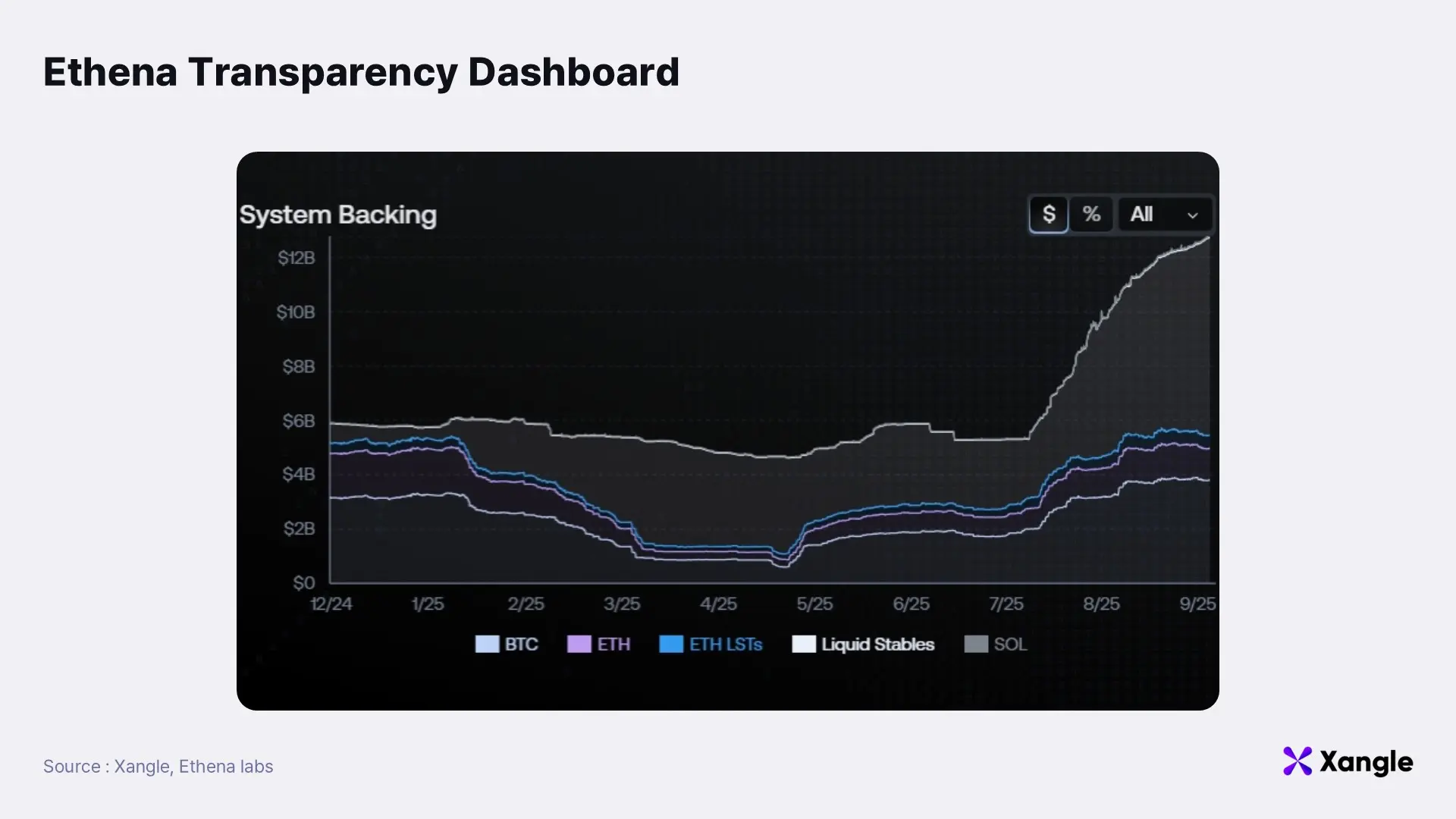

The Ethena Foundation is acutely aware of this risk and proactively mitigates it. The composition of USDe’s collateral is disclosed transparently via a public dashboard. In addition, collateral and hedges are distributed across multiple exchanges rather than concentrated in one venue—reducing exposure to exchange-specific failures. As a result, even during the Bybit hack of February 21, 2025, no USDe de-pegging occurred. This resilience reassured investors who remained skeptical of synthetic dollar protocols after the Luna–Terra collapse, proving that funds could be entrusted to USDe with confidence. Thanks to these safeguards, USDe has established itself as a rare combination: a product that is both high-yielding and secure.

The second risk is lack of sustained demand. For USDe to operate on a stable footing, it requires consistent demand channels. At present, usage is concentrated in DeFi protocols and centralized exchanges such as Bybit. This reliance makes USDe vulnerable to changes in DeFi policy frameworks, which could curtail demand. Unlike USDT, which is firmly entrenched as a remittance medium, or USDC, which circulates actively in both exchange and payment markets, USDe still lacks comparably stable sources of organic demand.

The Ethena Foundation has acknowledged this issue and introduced several safeguards. A central piece is USDtb, developed in partnership with BlackRock. Backed by BlackRock’s BUIDL fund, USDtb acts as a strategic buffer for USDe. For instance, when funding rates turn negative, reserves can be converted into USDtb, reducing perpetual futures exposure while shifting into U.S. Treasuries as collateral. This effectively operates as a currency swap, blending safe-haven assets like Treasuries with Ethereum collateral to minimize systemic risk.

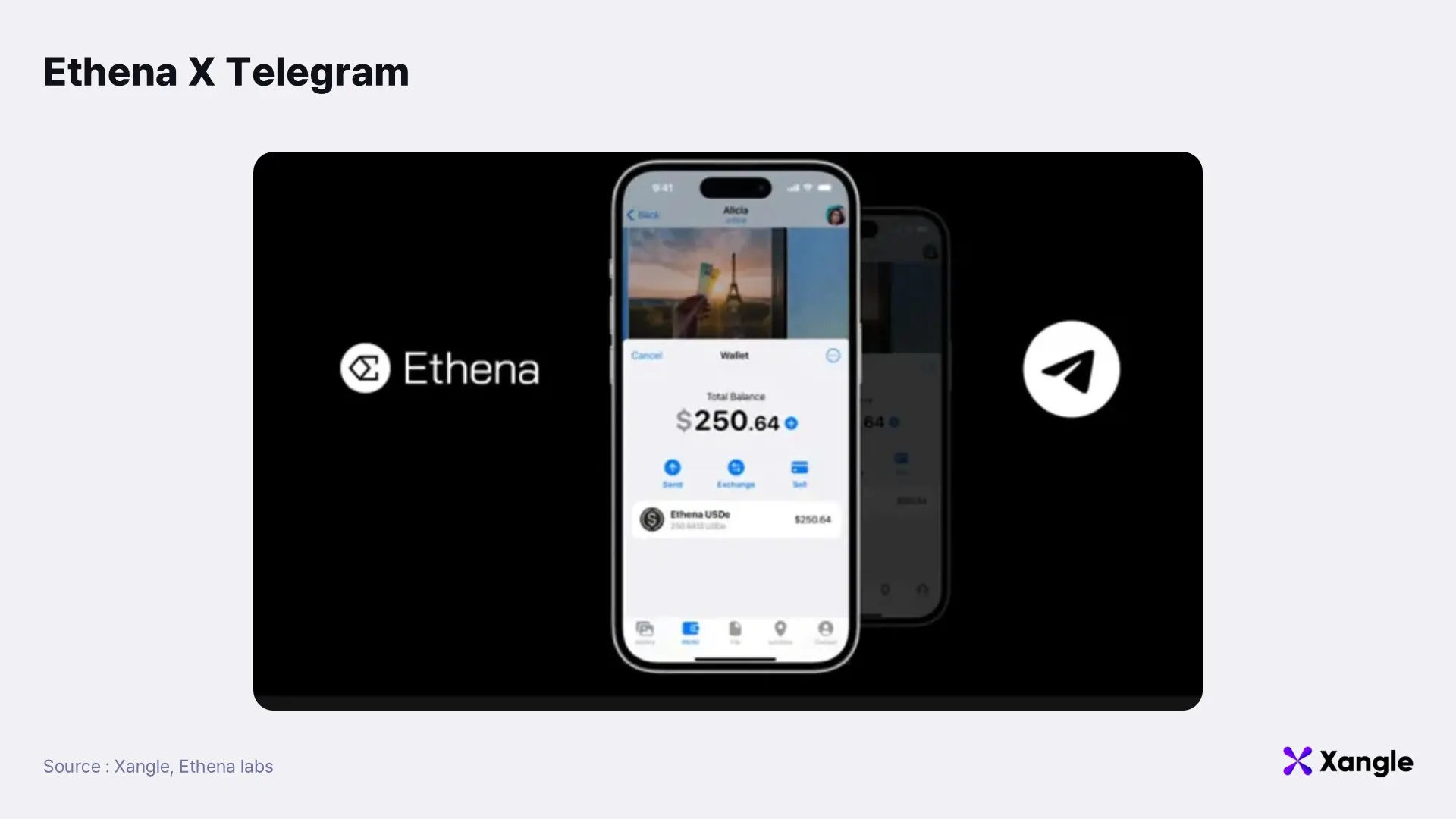

Beyond safety nets, Ethena is also working to expand demand. The first initiative is a collaboration with Telegram, aiming to position USDe as a payment medium within the messenger ecosystem.

Other payment-focused stablecoins, such as PYUSD or USDC in applications like Robinhood, have attempted to gain traction but achieved limited success relative to established payment gateway providers. By contrast, adoption within Telegram (an app with over 1 billion global users) could secure a deep and enduring base of retail demand.

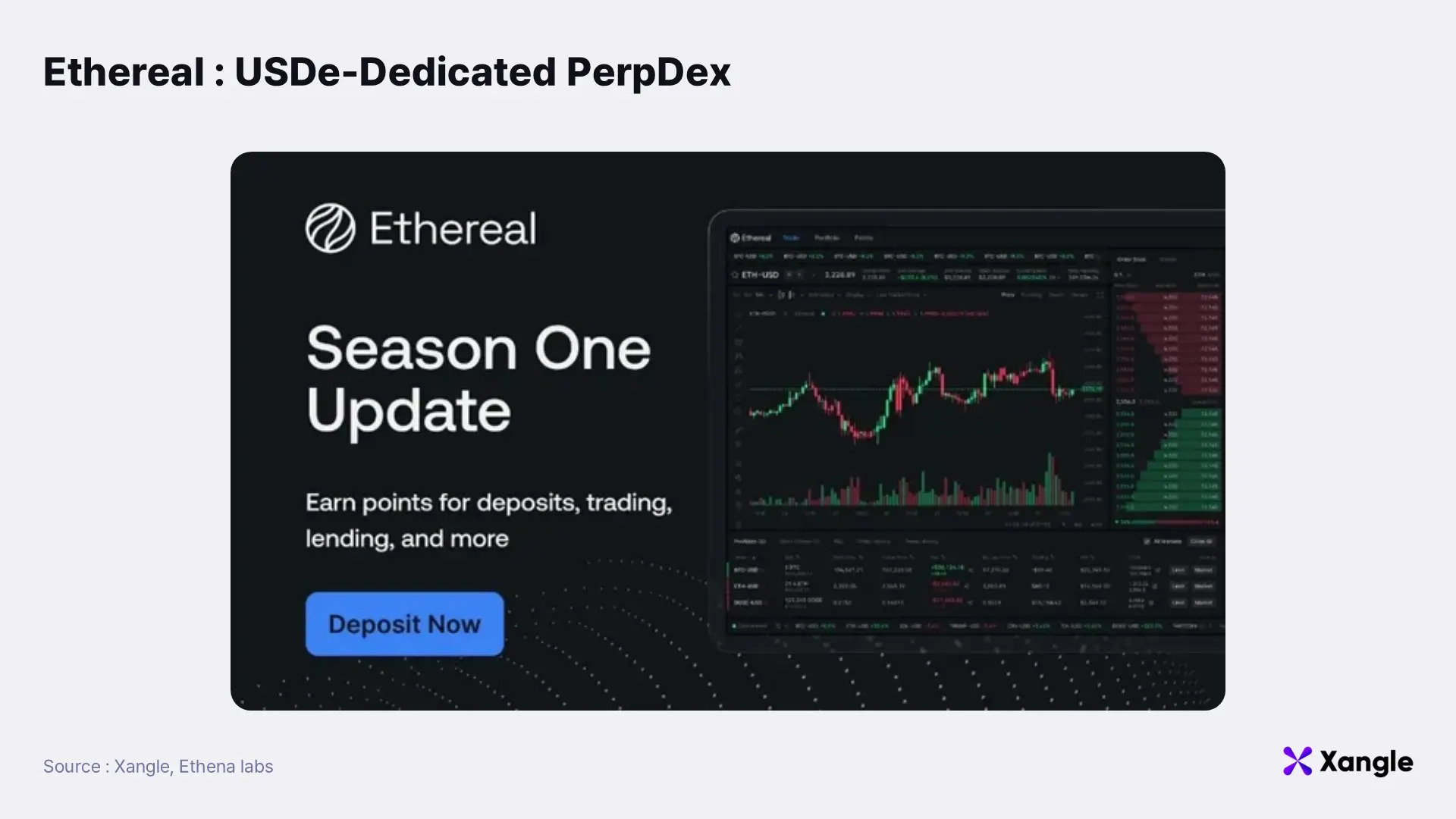

Ethena is also preparing to launch its own exchange, Ethereal. Built on a proprietary appchain, Ethereal is designed as a perpetual futures and spot venue, fully integrating sUSDe and native rewards into the order book. Liquidity and hedging flows will be supplied directly by Ethena. This initiative provides three key advantages: it enhances the safety of maintaining perpetual shorts, mitigates the systemic risk of exchange bankruptcies, and creates a new, durable demand channel for USDe.

4. Ethena’s Vision: Bridging TradFi and On-Chain Finance

Ethena has already established USDe and sUSDe as a “risk-free Ethereum” stripped of volatility, integrated them into DeFi protocols to drive adoption, and secured durable demand channels through initiatives such as Telegram and its in-house exchange, Ethereal.

But this is only the beginning. According to its 2025 roadmap, “Convergence,” Ethena’s long-term ambition is the full fusion of TradFi and DeFi. For institutions seeking access to the Ethereum ecosystem, Ethena’s model provides a form of Ethereum that eliminates price risk. At the same time, partnerships with institutions, such as the USDtb collaboration with BlackRock, position Ethena both as a gateway for institutional buyers and as a liquidity provider for ETH short positions across exchanges.

To further this vision, Ethena plans to launch iUSDe, a new product designed as a regulatory-compliant wrapper of USDe that enables the export of sUSDe-like yield to traditional institutions. Functionally identical to sUSDe, iUSDe adds token-level transfer restrictions so it can be held within regulated environments. Managed through segregated SPVs (Special Purpose Vehicles) overseen by licensed investment managers, iUSDe allows institutions to access yields efficiently without touching crypto rails directly. In this way, Ethena is engineering tokens that serve as connective tissue between traditional finance, exchanges, and DeFi—tokens that, within TradFi systems, operate much like structured financial products.

Yet Ethena’s ambitions go further. The ultimate goal is to unify its growing ecosystem, including the Ethereal exchange and institution-focused iUSDe, onto a single chain. By onboarding the full range of TradFi assets into an on-chain environment, Ethena aims to deliver the complete convergence of traditional markets and blockchain infrastructure.

To achieve this, the Ethena Foundation is developing Converge, a dedicated Layer-1 blockchain. Converge is envisioned as an on-chain financial layer where digital assets, RWAs, and stablecoins can freely trade and interact. The chain will host Ethena’s USDe infrastructure while using USDe and USDtb as native gas tokens. By requiring USDe for accessing on-chain financial infrastructure, the plan is to position it as a true “on-chain reserve currency” for finance.

In effect, Ethena already functions as an on-chain investment bank, designing and distributing innovative financial products that bridge traditional finance, centralized exchanges, and DeFi. Looking ahead, its ambition is to consolidate all these products onto a single chain, positioning Converge as the most efficient and accessible entry point into on-chain finance—the “only on-chain investment bank.” Ethena is steadily moving closer to this vision, growing faster than any other DeFi protocol and winning adoption from both retail and institutional investors.

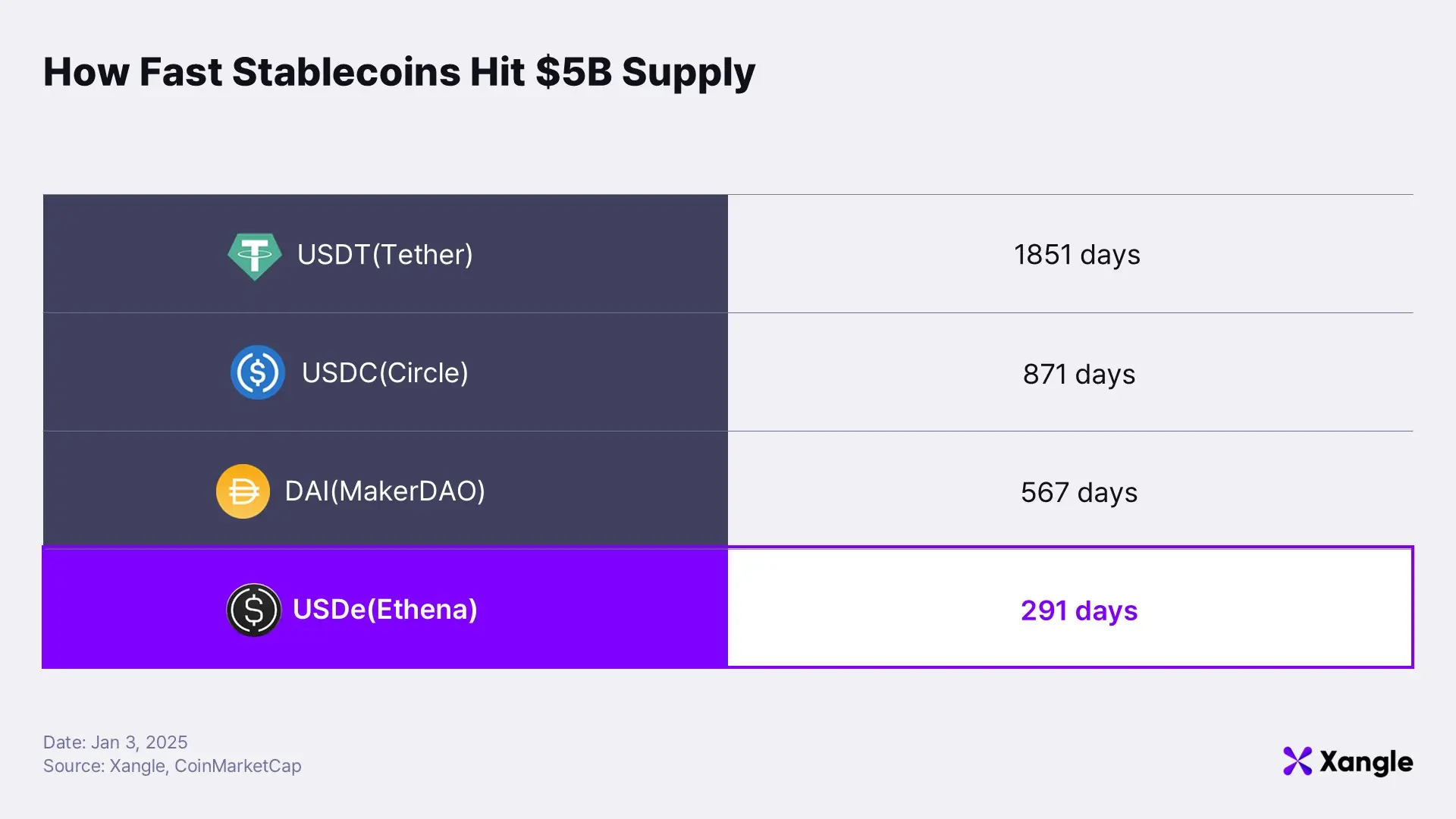

The market adoption has been explosive. USDe’s circulating supply reached $5 billion within 291 days of launch, with the threshold already surpassed intraday by day 275. No stablecoin in crypto history has ever scaled this quickly. For context, Tether (USDT) needed 1,851 days to reach the same milestone, and even Circle’s USDC, which grew far faster than USDT, still required 871 days. Ethena’s trajectory is therefore not just impressive, but historic in scale.

This hypergrowth is not a function of market luck. It is a powerful signal of the breadth and conviction of market support for Ethena’s model. By introducing a synthetic dollar backed by a delta-neutral architecture, Ethena has unlocked demand through yield opportunities that no other stablecoin has been able to replicate.

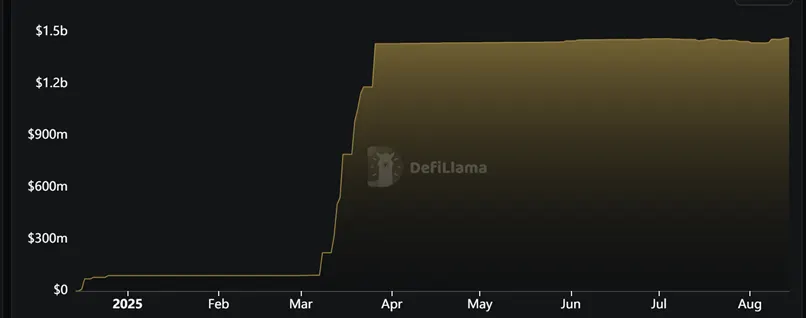

source : defilama

Momentum extends beyond USDe. USDtb, Ethena’s U.S. Treasury–backed stablecoin, already holds $1.5 billion in TVL. With Ethereum’s total TVL around $90 billion, USDtb accounts for nearly 2% of the network—a notable share for a new asset. Together, USDe and USDtb demonstrate how Ethena is advancing toward Convergence by delivering yield-bearing products that appeal to both retail and institutional investors.

5. Bottom Line: Ethena as an On-Chain Investment Bank

The DeFi ecosystem has advanced rapidly on the back of constant innovation, but its long-term sustainability depends on securing stable liquidity. For institutional investors, Ethereum’s volatility remains a significant hurdle, limiting direct participation.

Ethena addresses this challenge by designing protocols that connect traditional finance with DeFi, much like an investment bank creating products tailored to the needs of corporates and funds. As an on-chain investment bank, Ethena develops and distributes products that minimize risk while delivering stable returns, positioning itself as a vital bridge between institutions and DeFi.

Beyond that, Ethena is building USDe-based DeFi infrastructure and architecting its proprietary Converge chain, pursuing a strategy to secure a first-mover position in the large market of traditional assets migrating on-chain. If realized, this plan would position Ethena as a key player opening a new era of on-chain finance.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.