ETH Spot ETF Approval: Inside Gary’s Head

Summary

-

We evaluate the outlook for ETH spot ETF approval through the Gensler’s lens, focusing on his assessment of the risks and rewards associated with his choices.

-

If rejected, our base-case scenario assumes only a 30% probability for the SEC being sued, wherein there is an 80% probability of the SEC’s loss. The incentive for the applicants to bring a lawsuit against SEC is low in our view, given 1) relatively modest upside from the ETH spot ETF listing, 2) Grayscale’s presumed lack of appetite for assuming another $100mn+ legal cost, 3) TradFi giants’ relationship with regulators. Consequently, Gensler is likely to find the reward for rejecting the applications outweighs the risk of another loss in court.

-

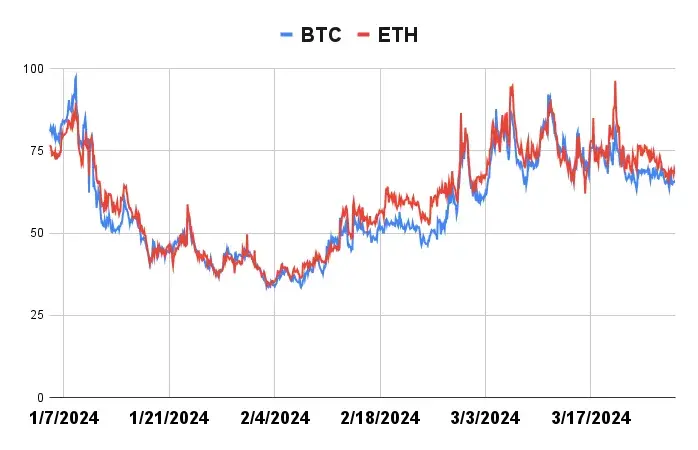

Approval or disapproval, expect ETH’s volatility to increase with the May 23rd deadline fast approaching. Currently BTC and ETH's implied volatilities are at par, suggesting the market hasn't yet priced in the ETH’s expected volatility shift.

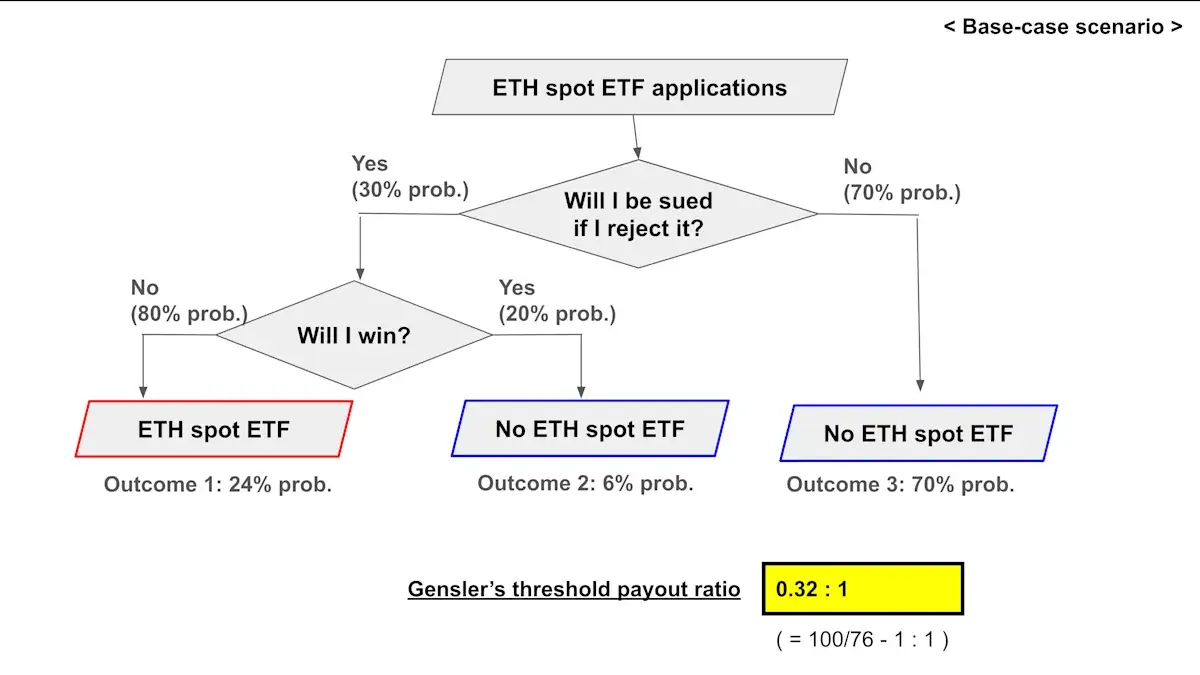

Figure 1: The reward outweighs the risk

(Source: Presto Research)

The narrative surrounding the approval of ETH spot ETF applications has significantly shifted from earlier this year, with a growing view that the approval might not be the "slam dunk" many were initially led to believe. The concerns range from the risk of the ETH’s potential security status to the possibly inadequate correlation between the ETH’s spot and futures markets. The latter was a key factor in the US district court’s ruling that SEC’s approval of a BTC futures ETF - but not a spot ETF - was ‘arbitrary and capricious.’

One Man Show

It’s painfully clear that the outcome ultimately hinges on the decision of one individual - Chairman Gensler - as demonstrated in his decisive vote in the 3-2 approval of BTC spot ETFs. Given this context, instead of getting lost in technical details with no definitive answers, a more pragmatic approach to assessing the approval outlook is to view it through Chairman Gensler’s lens, focusing on how he would weigh the risks and rewards of his decisions.

It’s well-acknowledged that Chairman Gensler’s approval vote of the BTC spot ETF was a very reluctant one. The approval was immediately followed by his begrudging statement that it “is cabined to ETPs holding one non-security commodity, bitcoin” and that it in no way signals “the Commission’s willingness to approve listing standards for crypto asset securities.” His subsequent media interviews also show that his decision was forced by the afore-mentioned US court decision favoring Grayscale - a crucial factor that is absent in the case of the ETH applications.

Am I getting enough odds?

Against this backdrop, we've modeled how Gensler might approach the ETH spot ETF applications. Figure 1 above illustrates his possible decisions and their respective outcomes, complete with assigned probabilities. The analysis suggests there's a 24% chance that disapproval leads to an unfavorable outcome for Gensler - i.e. the SEC being sued for breaching the Administrative Procedure Act and losing in court, as happened in the Grayscale vs SEC.

Essentially, for him to justify disapproval, he must believe he’s getting sufficiently compensated for the 3-to-1 (or 76:24) odds he’s taking. Put it another way, his disapproval can be viewed as wagering on the 76% probability outcome with the fair payout ratio of 0.32-to-1.

The probabilities assigned to each path is the key in this analysis. The easier one to estimate is who will win in case SEC is sued. We subscribe to the view that the court’s reasoning in the Grayscale lawsuit stands for the ETH spot ETF applications as the correlation between ETH spot and ETH futures are sufficiently high - a stance well-advocated by the Coinbase Chief Legal Officer Paul Grewal in his recent letter to the SEC(Figure 2). The harder one to judge is whether someone will actually bring a lawsuit against the SEC in the first place. Grayscale has done it once already, picking up the tab for the $100mn+ legal cost along the way. It’s hard to imagine them repeating the feat.

Figure 2: Hard to tell them apart

(Source: Coinbase)

For the remaining 6 applicants, the motivation to fight in court would be low if the ETF sponsors expect only modest upside from the ETH spot ETF approval. There are reasons to believe that this may indeed be the case. The high price correlation between BTC and ETH suggests that asset allocators may not feel the strong urge to add a second crypto exposure after having already allocated to BTC, as the incremental diversification benefit would be much smaller. This, coupled with the TradFi giants’ historically cozy relationship with regulators, would mean quiet backdoor solutions or compromise rather than public legal confrontation is a more likely path for them.

Figure 3: Take one for the team, anyone?

(Source: Bloomberg, Presto Research)

It’s all about assumptions

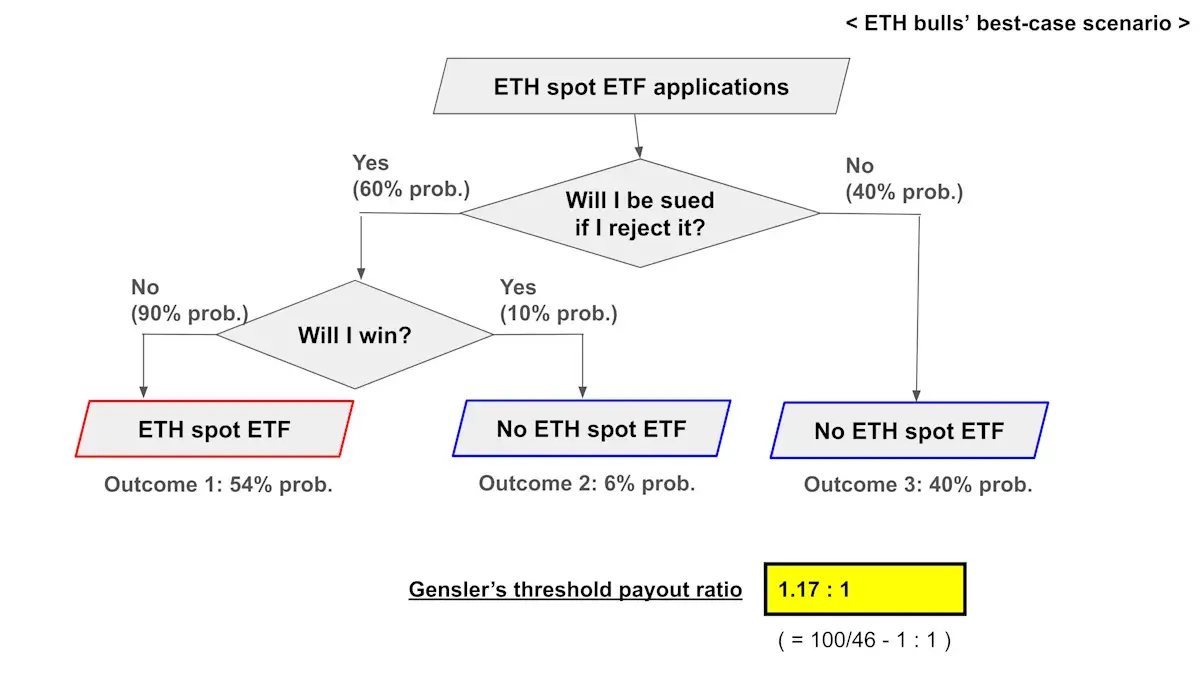

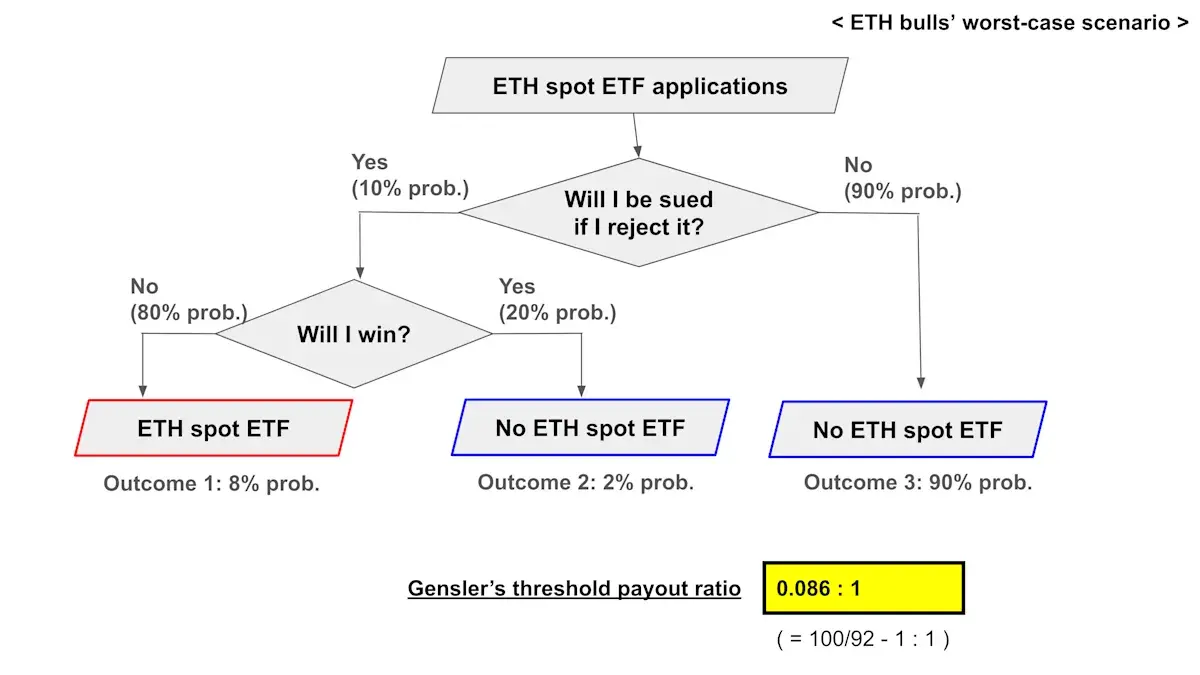

All of these serve as our justification for assigning only a 30% chance for the SEC actually getting sued. Under this scenario, Chairman Gensler will reject the applications if he believes his payout is better than 0.32-to-1. One can only guess what sort of things he’d value as a ‘sufficient compensation’ - maybe it's a stronger political foothold within the Dems, nomination as the next Secretary of Treasury, or something else equally grandeur on his agenda unknown to the public. Judging from the progression of his career in the public sector, we are inclined to believe that he’s getting sufficient odds - i.e. the reward for rejecting the applications outweighs the risk he’s taking. That said, readers are encouraged to play around with different assumptions to arrive at your own conclusions. We’ve shown different reward thresholds under various probability assumptions for your reference.

Figure 4: ETH bulls’ best-case (“Rewards not big enough”)

(Source: Presto Research)

Figure 5: ETH bulls’ worst-case (“Priced in”)

(Source: Presto Research)

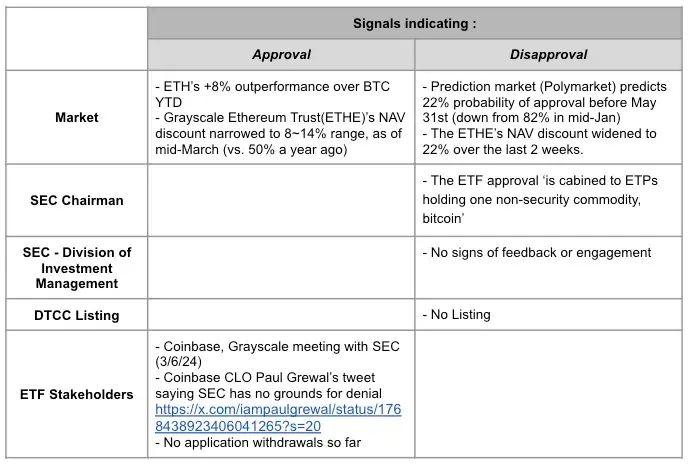

Despite the recent shift, the signals thus far are split at best (Figure 6). With less than 2 months to go before the May 23rd deadline, more credible signals will emerge in the coming weeks, causing commotions in the related instruments. Considering the ETH’s volatility outlook, the fact that options market is pricing ETH’s and BTC’s volatility at parity is perplexing and may represent opportunities for vol traders(Figure 8). If not for anything else, understanding the Gensler’s risk-reward calculus can be a useful framework when thinking through appropriate ETH’s portfolio position.

Figure 6: Emerging signals

(Source: Presto Research)

Figure 7: Grayscale Ethereum Trust’s NAV Discount

(Source: YChart.com)

Figure 8: Implied vols at parity

(Source: The Tie)

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article is provided by CrossAngle’s third-party research partners. CrossAngle does not have any editorial control over this article and does not warrant the accuracy and timeliness of the information contained herein. This article may contain links to third-party websites, over which CrossAngle disclaims any control or responsibility.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.