Table of Contents

Introduction

-

Crypto Business Models

-

Core Values of Stablecoins

-

Stablecoins and Their Revenue Models

-

How Are Stablecoins Made? – Types of Stablecoins

-

Key Resources of Stablecoins

-

Key Process of Stablecoins

-

What’s Next for Stablecoins?

Conclusion

Introduction

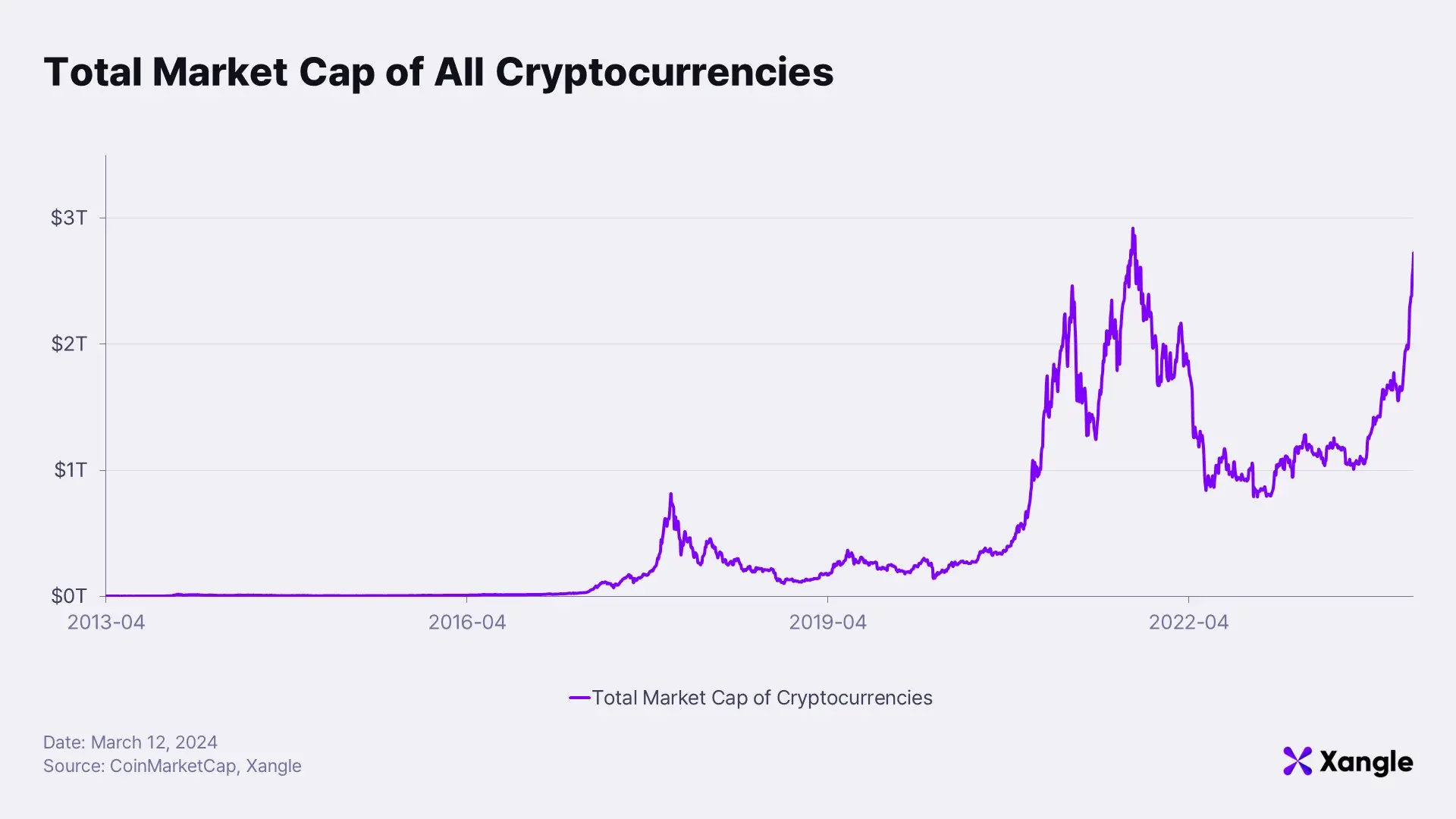

The price of Bitcoin is surging to nearly $69,000, marking an all-time high. The so-called “bull market” has returned after two years with the approval of Bitcoin spot ETF. Thanks to the rise of Bitcoin, the total market capitalization of all cryptocurrencies returned to its glory days by surpassing $2 trillion.

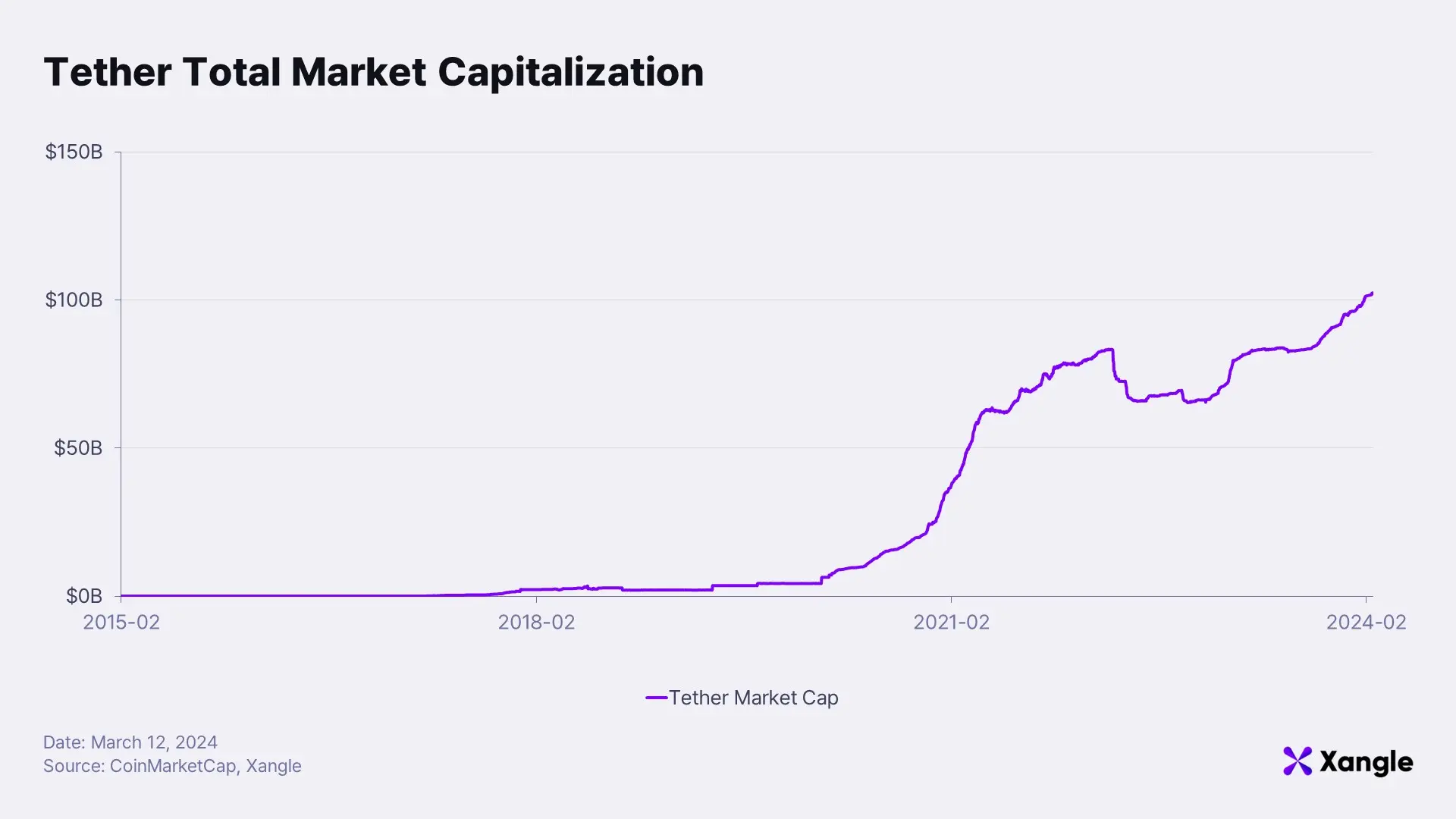

The leading stablecoin, USDT, is also experiencing remarkable growth. On the 5th of last month, the market capitalization of USDT surpassed an all-time high of $100 billion. So why are stablecoins growing as well? While other cryptocurrencies rally based on the expectation of price increases, the point of stablecoins is having their value pegged to $1. The reason behind the increasing demand for stablecoins, whose value is unlikely to rise, is actually due to them being established as a key currency for investing in other cryptocurrencies. Therefore, as demand for cryptocurrencies increases, the more need there is for stablecoins to purchase the coins.

Over the past few years of a bear market, the crypto community mockingly reflected that the price fluctuations of cryptocurrencies were based on no reason. However, stablecoins do have a clear reason for their growth. Unlike other crypto projects, stablecoins have solid business models and provide a safe haven in the volatile crypto market by maintaining stable prices. Now, stablecoins are the first thing people secure before investing in cryptocurrencies. It serves as a kind of reserve currency enabling investment in various cryptocurrencies. Not only that, stablecoins are expanding their usage as alternative currencies in countries experiencing economic crises. They identified the biggest pain point for customers and provided a solution, and have faithfully followed the formula for success.

1. Crypto Business Models

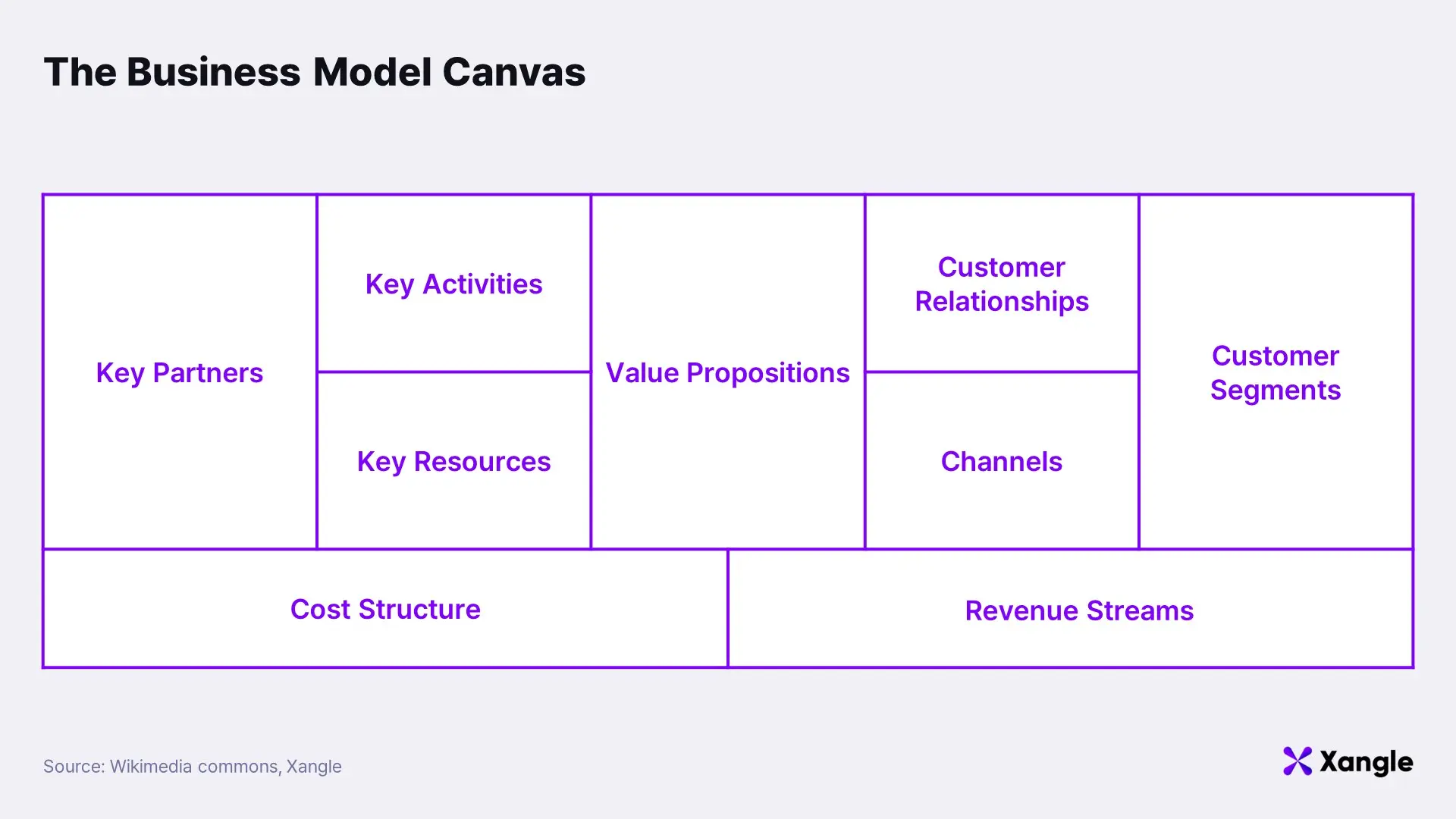

1-1. Why are business models important?

Entrepreneurs at startup education institutions are most recommended with the Business Model Canvas. It represents nine core elements for operating a business in a template format.

Technology drives innovation in the world. However, if we cannot find ways to utilize new technology, it becomes obsolete. If no profit is generated, the drive for the technology to advance loses momentum. Conversely, innovative business models can drive new technological developments. After the web, the greatest innovation was going mobile. Apple's smartphone itself was a tremendous innovation, but the new business model it presented, the App Store, also drove the development of mobile app technology. A new ecosystem called the App Store emerged along with smartphones, encouraging the development of new types of businesses like Uber, which were never imagined before.

1-2. The need for dApps with new business models

The biggest issue in the blockchain industry is "mass adoption." It is the assertion that blockchain technology should be used in everyday life. However, until now, the crypto business has largely been heavily tech driven. Thus, the area of development has been focused on blockchain infrastructure, like mainnets. However, there has continued to be calls for decentralized applications (dApps) that can be applied to real life since no matter how great the technology is, it is useless if it does not permeate our daily lives. For example, the decentralized financial (DeFi) service model, which dominates the crypto industry, requires the user to have basic knowledge of DeFi to benefit from the service properly. Comparing this reality to users utilizing financial service apps from banks and securities firms without knowing a whole lot the technology, it is evident how far away from mass adoption the blockchain industry currently is.

Source: Axie Infinity

Source: STEPN

P2E’s lead Axie Infinity and M2E’s lead STEPN

The blockchain space has also seen significant turning points with important business models. Particularly noteworthy is the recent advent of X2E (X to Earn), which is praised for bringing crypto technology from the virtual world into reality. X2E represents a business model where individuals are rewarded in crypto for specific real-world activities. Play-to-Earn (P2E) games and Move-to-Earn (M2E) activities stand as prime examples. Currently, X2E faces challenges in its growth trajectory due to various issues such as token inflation. Nevertheless, anticipation is high for the emergence of new dApp business models to propel mass adoption forward. Through the "Crypto Business Models" series, we aim to continue exploring meaningful blockchain business models.

2. Core Values of Stablecoins

Blockchain technology is rooted in finance. The very inception of Bitcoin, after all, was driven by monetary motives. Satoshi Nakamoto envisioned a system where individuals could transact peer-to-peer without third-party interventions like banks or financial institutions—hence the birth of Bitcoin. Now blockchain technology, particularly Bitcoin, is widely used by countless individuals, and has essentially made hacking the system nearly impossible. Which means, secure financial transactions among individuals are now available via Bitcoin. However, challenges persist. The fluctuating value of Bitcoin remains a significant issue. You might intend to send $100, but if Bitcoin's price drops the moment you hit the send button, you end up sending less than $100 unintentionally. Hence, stablecoins emerged, having the same value as fiat currency, typically the dollar, to address this volatility. Stablecoin-crypto pairs have become fundamental on coin exchanges. In other words, one must hold stablecoins to purchase desired cryptocurrencies.

2-1. Core Values of Stablecoins — (1) Stability

Stablecoins are the only coins whose value is pegged to the dollar. While the value of all other coins fluctuates significantly in real-time, stablecoins provide immense benefits to crypto users solely by ensuring stable value comparable to the dollar. Simply put, having the same value as the dollar sufficiently proves the need for stablecoins. Ultimately, what people desire is to preserve the value of their assets. Investing in coins is a challenge that comes after that. Hence, even if one plans to invest in coins soon, they prefer to hold their assets in stablecoins until execution. Stablecoins precisely address this pain point of crypto investors.

Source: Xangle

Source: Glassnode

The desire for stability among crypto investors is evident in market capitalization as well. Stablecoin USDT, ranks third, and USDC ranks seventh in total crypto market capitalization. Furthermore, stablecoins collectively hold approximately 17% of the market share (as of February 29, 2024). Since people consider stablecoins as equivalent to dollars, some think that they should hold stablecoins when they’re not investing. However, if we look at stablecoins as one of many coins, and not fiat currency, we can see how high the demand is for coins with stable prices.

2-2. Core Values of Stablecoins — (2) Facilitates crypto investments

The initial gateway for purchasing coins is centralized exchanges (CEX). Most exchanges enable coin trading with stablecoins as seen in the typical pairing, BTC-USDT. This establishes stablecoins as a key currency in the crypto space. This may not resonate well with Korean investors since crypto asset exchanges in South Korea do not provide stablecoin markets. In South Korea, investors deposit Korean won into bank accounts affiliated with each exchange and purchase coins with it. However, when using overseas exchanges, the Korean won is not an option, and purchasing coins with credit cards is also prohibited. This applies not only to South Korean users but also globally since overseas exchanges are registered in different countries, subject to varying regulations. Moreover, more people from different countries use overseas exchanges than citizens of the country where the exchange is registered. Thus, trading coins with fiat currencies like the dollar is virtually impossible.

Then, why do exchanges establish markets with coin-stablecoin pairs like BTC-USDT? It is akin to exchanging currency upon arriving in a foreign country after converting to dollars beforehand during international travel. You would see that every bank branch in South Korea hold dollars, and any country you may travel to will acknowledge the currency as well. This is because the abundance of dollar liquidity ensures such wide acceptance. In the same vein, trading does not occur if there is a lack of liquidity on exchanges. Thus, securing sufficient liquidity through single key currency is essential to facilitate easy trading of various coins.

2-3. Core Values of Stablecoins — (3) Alternative currency

Stablecoins are widely used as a practical alternative in third-world countries where the value of local currency is unstable. It's widely known that due to rapid depreciation of the Turkish lira and escalating inflation in Argentina, the peoples prefer dollars or cryptocurrencies over their local currency. Apart from sudden economic upheavals, in Africa, where financial infrastructure lacks and currency values fluctuate incessantly, mobile money service "M-PESA" gained wide usage. It involves recharging money at various M-PESA phone agent locations and transferring money to others via mobile phones. Recently, there's a growing trend of mixing M-PESA with stablecoins. Locals transact with M-PESA among themselves and resort to using USDT via Binance when dealing with foreigners. In case domestic economic situation deteriorates, they swiftly convert cash to USDT. Similar to the past Turkish lira crisis, people in third-world countries generally prefer USDT transactions via Binance because of its fastest transaction speed and low fees.

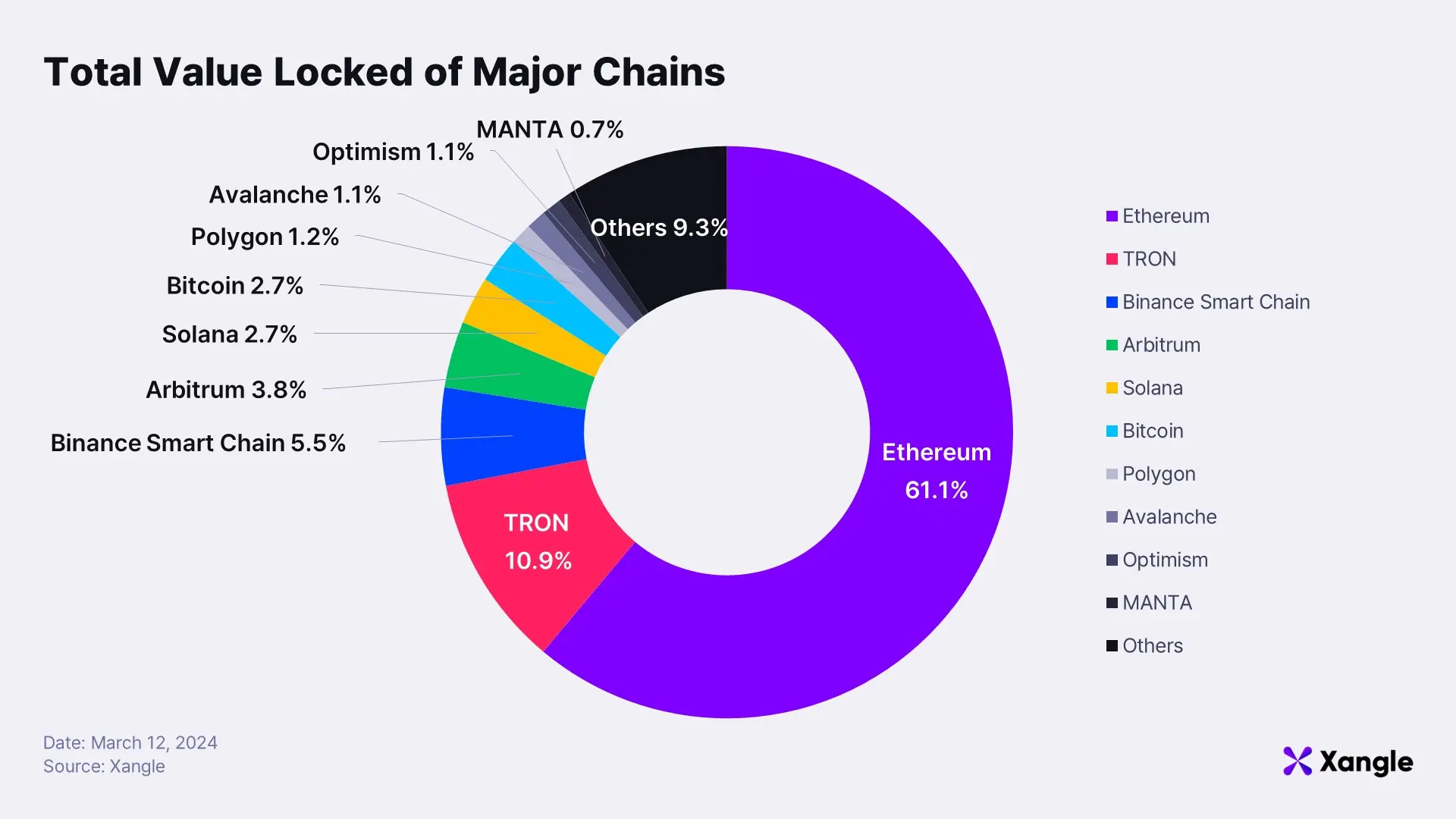

Typically, when assessing the usage of each chain, one looks at the Total Value Locked (TVL) per chain. The higher the amount deposited on a chain, the more it's considered in use. It may come as a surprise, but TRON boasts the second highest TVL after Ethereum despite TRON not being particularly popular among crypto builders and not having many prominent projects. Up its high rank indicates the significant usage of the TRON-based USDT. This is further supported by the fact that citizens of third-world countries commonly use USDT in their daily lives.

3. Stablecoins and Their Revenue Models

3-1. Stablecoins and Their Revenue Models — (1) Collateral asset investment

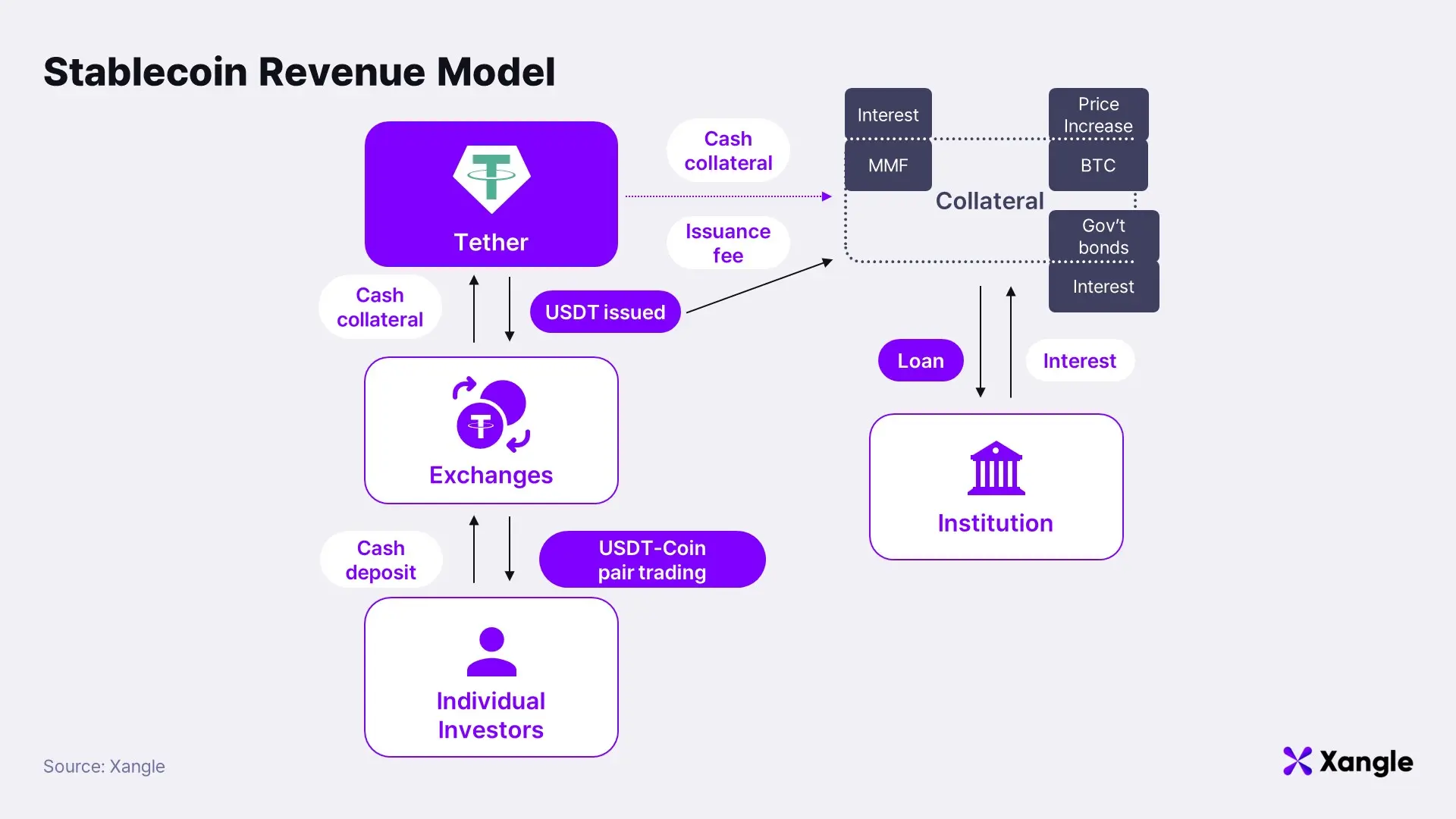

In this context, we refer to the most commonly used fiat-backed stablecoins. The revenue model of stablecoins is straightforward. Stablecoin issuers generate profits by utilizing the deposits collateralized by customers. For example, USDT, which is based on fiat currency, holds collateral such as government bonds, corporate notes, and crypto assets, generating investment returns from these holdings. Despite being termed as “investments,” the structure of fiat-backed stablecoins necessitates holding liquid assets. As illustrated in the Figure above, when the customer deposits $1 with Tether, $1 in cash assets enters Tether's vault, and the customer receives 1 USDT. Conversely, when a customer redeems 1 USDT, Tether must return the $1 cash deposited by the customer.

To ensure the ability to return customers' funds, it is imperative to hold cash assets, and this is where money lies. Rather than simply holding deposited dollars in cash for customers to exchange back and forth, stablecoin issuers invest in short-term government bonds or other liquid assets, sometimes even acquiring gold or Bitcoin. Holding assets typically classified as safe is crucial not only for facilitating immediate reimbursements when customers withdraw dollars but also for instilling trust possessing secure assets, which can avert a bank run.

In 2023 alone, Tether recorded a net profit of $6.2 billion, with a profit of $1 billion in the fourth quarter, primarily due to the rise in short-term U.S. bond interest rates and the prices of Bitcoin, gold, and other assets. Even with just holding the safest bonds, the structure allows for passive income as long as people continue to use USDT. However, to increase profits further, diversifying the portfolio is necessary. Nevertheless, investing in high-risk assets could jeopardize the stability, which is the whole point of stablecoins.

3-2. Stablecoins and Their Revenue Models — (2) Fees

Tether charges fees for both deposits and withdrawals, as well as account verification. A fee of %150 is required to undergo account verification directly with Tether for purchasing USDT. Additionally, there are fees for deposits and withdrawals; one can withdraw at least $100,000 directly from Tether with a 0.1% fee. Mostly, exchanges or institutions that provide USDT liquidity issue USDT directly and pay fees. Thus it’s practically impossible for individuals to purchase USDT directly from Tether in reality; instead, they can acquire USDT through exchanges. When transferring USDT from one exchange to another, there's a fee of approximately 1 USDT, which is not a USDT transaction fee but a transaction gas fee as Tether does not charge fees for transfers between accounts.

3-3. Stablecoins and Their Revenue Models — (3) Loans

Tether also offers institutional loan services. However, its loan risks have raised significant doubts. In October 2021, Tether loaned $1 billion to the crypto investment firm Celsius. The interest rate for this loan was reported to be between 5% to 6% per annum. However, Celsius subsequently collapsed and triggered the FTX incident. Additionally, Tether faced criticism for lending tens of billions of dollars to Chinese companies with questionable payment capabilities.

4. How Are Stablecoins Made? — Types of Stablecoins

In the previous sections, we focused mainly on USDT, a stablecoin pegged to fiat currency. The second biggest stablecoin, USDC, also operates on a fiat currency basis and its structure isn’t significantly different from USDT. However, the dominance of fiat-backed stablecoins as the mainstream can largely be attributed to the Terra-Luna debacle. Understanding the principles behind different types of stablecoins should provide a better insight into the differences their business models.

4-1. Fiat-backed (Ex.: USDT, USDC)

Both USDT and USDC, which currently dominate the stablecoin market, are fiat-backed. When a customer deposits one dollar, they receive 1 USDT or 1 USDC in return. Upon withdrawal, the customer receives one dollar in cash for each USDT or USDC returned. Essentially, the assurance that Tether will redeem one dollar for every USDT issued is what gives 1 USDT its one-dollar value. Therefore, Tether must hold reserves equal to or greater than the total amount of USDT issued, ensuring the pegging of 1 USDT to 1 dollar.

4-2. Collateral-backed (Ex.: DAI)

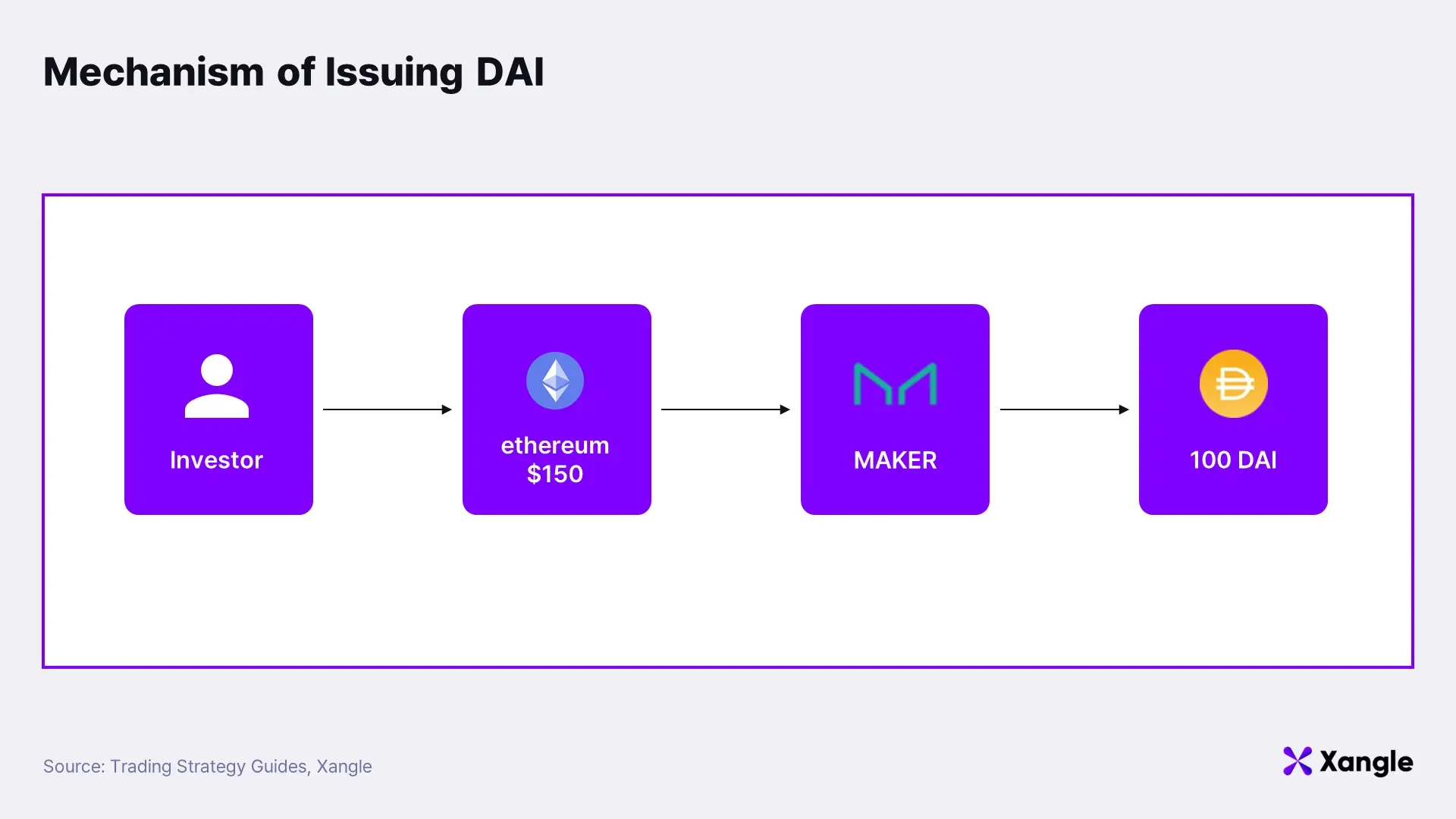

While fiat-backed stablecoins are backed by traditional currencies like the dollar, DAI is a stablecoin collateralized by cryptocurrencies. Tether issues USDT against dollars deposited, whereas MakerDAO issues DAI, pegged to 1 dollar, against cryptocurrencies deposited as collateral. The cryptocurrencies in question are primarily Ethereum but also other various coins. DAI is not readily available for trading against other cryptocurrencies on centralized exchanges (CEXs) where general consumers easily flock to, so individuals typically acquire DAI for trading purposes on decentralized exchanges (DEXs) or DeFi platforms.

The key to DAI stablecoin issuance lies in over-collateralization. The current minimum collateralization ratio is 150%. When investors deposits $150 worth of Ethereum into a vault made by MakerDAO, they get issued $100 worth of DAI. Upon repayment of the $100 DAI, the depositor receives back the $150 worth of Ethereum.

Such over-collateralization is necessary because assets like Ethereum, which serve as collateral, are subject to high price volatility. Say an investor deposit $150 worth Ethereum in the vault. If the value of the said Ethereum plummets to below $100, MakerDAO’s vault suffers losses. Thus, if the price of the collateralized Ethereum drops below the minimum collateralization ratio of 150%, the Ethereum is automatically liquidated, converting it into safer assets like USDT to prevent losses. Since the user over-collateralized at 150%, the vault does not suffer losses as long as it converts to safer assets before the collateralized Ethereum price falls even further.

So how is the peg of 1 DAI to 1 dollar maintained?

- $1DAI < $1

- If the price of 1 DAI is lower than 1 dollar, people will buy the cheaper DAI. Who wouldn’t rather pay 0.8-dollar DAI that usually costs a full dollar? They would then take the cheaply purchased DAI to pay back their debt to the MakerDAO vault. This means that they collateralized Ethereum to initially get 100 DAI issued, and now they can pay back 100 DAI at a cheaper price and also get their collateralized Ethereum back. As people buy and pay back DAI, reducing the circulating DAI in the market, its value rises again, adjusting to the price of $1.

- $1DAI > $1

- The situation is the complete opposite if the price of 1 DAI is higher than $1. People will try to collateralize more of their Ethereum to get more DAI issued. $1, more people deposit Ethereum in the MakerDAO vault to issue more DAI. This will in turn increase the number of DAI in circulation, which brings down its value—which results in DAI’s price dropping back down to $1.

4-3. Algorithmic (Ex.: UST)

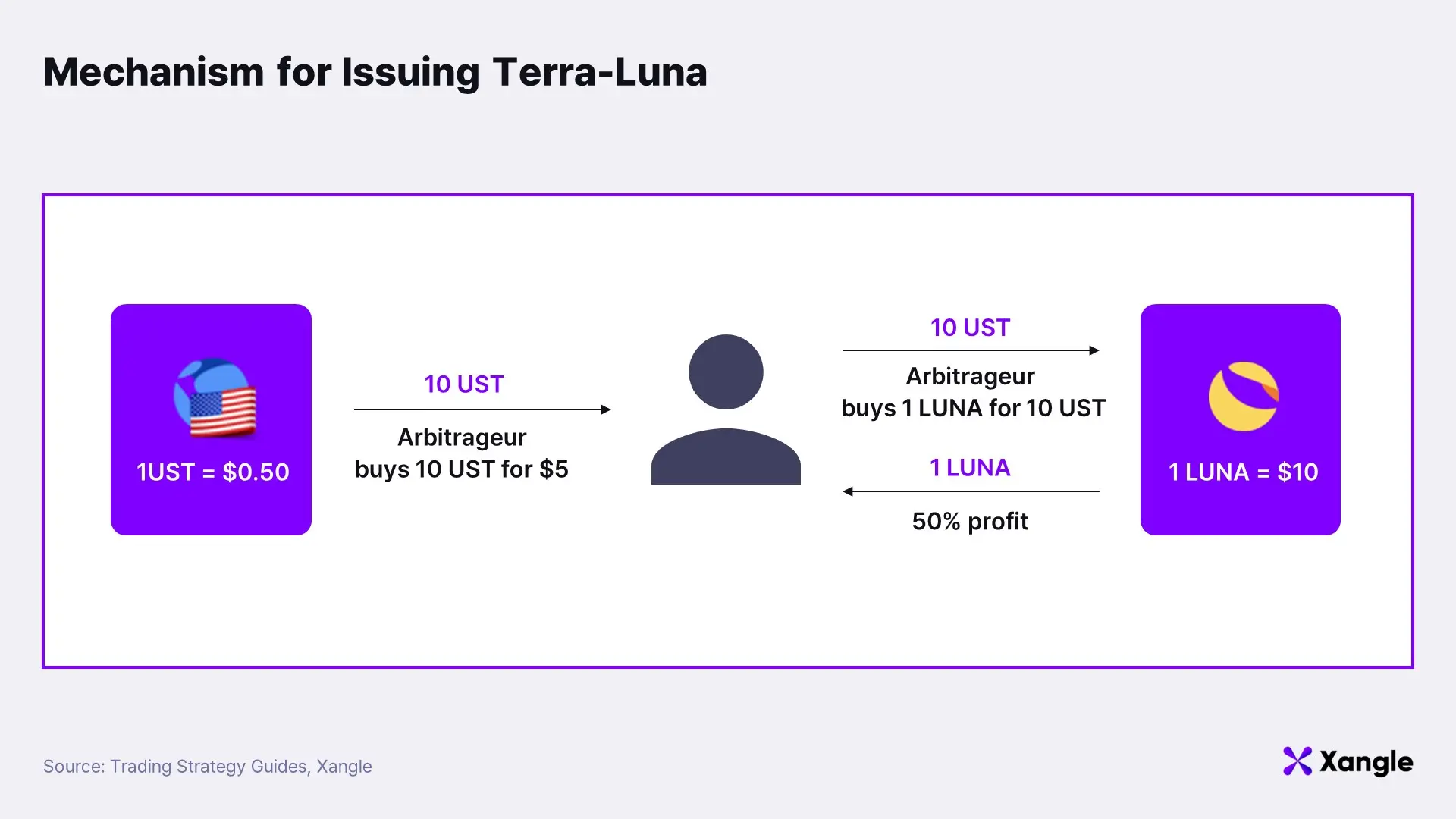

Algorithmic stablecoins, also uncollateralized stablecoins, are a significant departure from fiat-backed and collateral-based stablecoins. While the former types rely on assets as collateral, algorithmic stablecoins achieve a peg of $1 through various algorithms without any collateral. Terra's (UST) structure stands out as the most prominent among them, so let’s delve into the workings of Terra. Terra's stablecoin, UST, operates in conjunction with a token called LUNA. Users can exchange UST and LUNA on a platform called Terra Station, acting as a sort of exchange. UST, pegged to $1, serves as the stablecoin, while LUNA functions as a supplementary token to support it.

- $1UST < $1

- Let's assume that 1 UST falls below $1 to $0.9. Luna is valued at $10. People would opt to buy the cheaper UST and exchange it for Luna. Originally, one could purchase Luna for $10, but with the decreased UST price, one can obtain the same Luna for only 9 UST. As people buy UST to exchange for Luna, the circulation of UST in the market decreases, causing its price to rise back to $1..

- $1UST > $1

- Conversely, if 1 UST becomes more expensive at $1.1, people would prefer UST more since it's now pricier than $1. They would now opt to purchase Luna and exchange it for the higher valued UST. Originally, exchanging Luna would yield 10 UST, but now, due to the increased UST price, exchanging Luna would yield 11 UST. As people opt for UST, the circulation of UST in the market increases, causing its price to drop back to $1.

There have been several attempts by algorithmic stablecoins even before Terra, but they faced failures. However, Terra aggressively attracted users by launching the Anchor Protocol, which claimed to guarantee a high annual interest rate of over 20% when users deposit their tokens on the platform. Then in May 2022, a depegging of UST initiated a collapse in the LUNA’s price. Some analyze that the reason for Terra's downfall lies in the initial promise of high interest rates that the Anchor Protocol couldn’t sustain, which is akin to a Ponzi scheme. Moreover, criticisms point to the vulnerability of algorithmic stablecoins, which rely on the arbitrage trading by participants. The Terra debacle heightened market distrust toward algorithmic stablecoins, paving the way for fiat-backed stablecoins like USDT and USDC to dominate the market completely.

5. Key Resources of Stablecoins

5-1. Trust

Trust, though intangible, stands as the most crucial resource for stablecoins. From the outset, stabilizing the price volatility of coins was the primary need for stablecoins. Just as banks collapse when trust is lost, stablecoins also meet their end when trust diminishes. The downfall of Terra’s stablecoin UST is the perfect example that demonstrates that stability crumbles in an instant when trust wavers.

5-2. Collateral

Terra seemed to validate that algorithms are more trustworthy than collateralized fiat or highly volatile crypto assets. However, with the complete collapse of algorithmic stablecoins, people leaned towards stablecoins backed by secure collateral, shifting the paradigm toward USDT and USDC. Thus, collateral became the cornerstone backing stablecoin trust. The greatest risk for stablecoins is the risk of bank runs, where all customer deposits are withdrawn. As such, possessing secure assets as collateral, as in the case of fiat-backed stablecoins that rely on safe assets like government bonds as collateral, allows customers to hold stablecoins with confidence.

5-3. Convenience

People hold stablecoins for stability and the convenience they offer in crypto investments. Particularly, they prefer stablecoins that are easiest to purchase. However, it's practically impossible for individuals to directly purchase USDT or USDC. From the issuer's perspective, there's concern that individuals with uncertain identities may issue stablecoins for malicious intent. Therefore, people access stablecoins by trading coins and stablecoins on exchanges. Naturally, they trade on the coin-stablecoin pairs with the highest liquidity, then wait for favorable investment timings after converting to widely used stablecoins. Ultimately, the convenience for regular users depends on the richness of liquidity available.

6. Key Processes of Stablecoins

6-1. Key Processes of Stablecoins — (1) Arbitrage

Stablecoins are not fiat currencies themselves, so some degree of pegging deviation is inevitable. Traders attempt arbitrage whenever there is a slight disparity between the price of stablecoins and the dollar. This involves buying stablecoins when they are cheaper than $1 and selling them when they worth slightly more than that. And through arbitrage trading, the stablecoin’s peg to $1 is maintained. In other words, it's the traders aiming for arbitrage opportunities during peg deviations who ultimately realign the price back to $1, and they are usually institutional players that execute rapid-fire trades of stablecoins using bots.

However, the Terra-Luna incident proved that relying solely on arbitrage trading is open to vulnerability. While peg deviations lead to realignment to $1, if trust in the stablecoin diminishes, peg deviations could worsen. As demonstrated by Tether and Circle, which have consistently maintained their positions as the top two stablecoins, trust is backed by reliable collateral such as cash and government bonds. Through the price disparity between stablecoins and the dollar, someone gains profit, thereby ensuring stability. Yet, ultimately, there must be trust that upon surrendering USDT, one will receive $1 in return, and this trust hinges on confidence in adequate dollar reserves and bonds. This belief is essential to execute arbitrage trading with the expectation that even during peg deviations, prices will realign to $1.

6-2. Key Processes of Stablecoins — (2) Risk Management

Operational Risk

Stablecoin issuers, resembling investment managers in structure, must manage operational risks. While government bonds are the safest assets, reducing their weight can enhance returns. However, understanding how customers will perceive a decrease in the proportion of safe assets is crucial. In May 2023, Tether decided to regularly purchase Bitcoin as excess reserves. This move was welcomed amidst a Bitcoin price rebound and the occurrence of USDC peg deviations due to the SVB’s bankruptcy. Conversely, Circle, adhering to U.S. regulations and depositing assets transparently in U.S. banks, faced a crisis amid worsening market conditions. Terra, upon experiencing UST peg deviations, bought Bitcoin to defend its price. However, suspicions arose regarding the rationale behind Bitcoin purchases, further eroding trust and turning the Bitcoin acquisition into a liability.

Trust Management

Maintaining the issuer's credibility is also crucial. In 2021, Tether was fined by the U.S. for providing inaccurate information about collateral assets, and is still being faced with market skepticism for releasing confirmation reports instead of official audit reports. Additionally, there are persistent allegations of Tether holding Chinese distressed corporate notes as assets. In contrast, Circle, issuer of USDC, operates in strict compliance with U.S. regulations. However, crypto investors favoring decentralization view USDC as more unstable due to its susceptibility to U.S. regulations, and some even interpret USDC's peg deviations during the Silicon Valley Bank's bankruptcy as stemming from excessive reliance on central banks.

6-3. Key Processes of Stablecoins — (3) Portfolio composition

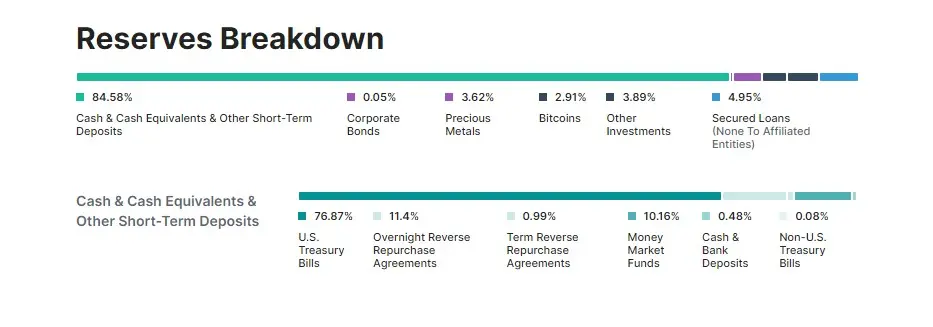

Tether’s Collateral Composition Status

Source: Tether

A key process for fiat-backed stablecoins is how they compose their collateral assets. Managing collateral assets well is crucial as the issuer must always possess more assets than the amount deposited by customers. The company's portfolio not only impacts customer trust but also influences the issuer's actual profits. Instead, stablecoins must construct portfolios with safe assets to ensure they can return $1 for every 1 USDT brought in. However, it is also important to find a find balance with aggressive investments as they expand the overall asset pool with increased profit. In 2023, Tether pursued stability by selling corporate notes from its portfolio, increasing the proportion of short-term bonds, and diversifying by purchasing Bitcoin. Initially, DAI primarily collateralized with digital assets, but with the growing importance of RWAs, DAI's collateral portfolio now includes real assets. Since constructing collateral with 100% cash is impractical, adopting a plausible portfolio strategy is essential and the key to operating stablecoins.

7. What’s Next for Stablecoins?

7-1. Regulation and the U.S. stance

The direction of U.S. regulation regarding stablecoins remains uncertain. Consequently, European and Asian countries are also waiting while keeping a close eye. In the U.S., there are opposing arguments regarding stablecoins: one suggests that expanding the use of USDC could actually strengthen the dominance of the dollar, while the other expresses the concern that stablecoins could weaken the Federal Reserve's control. With USDC's market share declining after the SVB's bankruptcy, USDT's popularity is rising rapidly. Given Tether's longstanding association with Chinese capital, U.S. authorities are concerned that stablecoin dominance may shift toward Tether—case in point, Tether’s market share has recently exceeded 70. Despite ongoing debates over the securities issues of cryptocurrencies and the lack of a clear stance on CBDC, U.S. authorities have yet to definitively propose stablecoin regulations. However, amid the soaring market share of USDT, there are indications that stablecoin regulations will soon be approved.

7-2. CBDC (Central Bank Digital Currency)

The U.S. government's stance on stablecoin regulation is closely intertwined with the issue of CBDC, thus the direction of CBDC will significantly impact stablecoins. Domestically, there are contrasting views on CBDC: some argue that CBDC will infringe on individuals' financial freedom, while others believe it will enhance the global status of the dollar.

From the perspective of maintaining the dollar's dominance, approving CBDC could allow the government to more actively intervene in finance and increase accessibility to the dollar, thus strengthening its dominance. However, there are concerns about security, as a single hacking incident could cause damage at national level. Moreover, there are concerns that CBDC approval could compromise the cherished American value of privacy protection, leading to never-ending political debates. As the debate for legalizing cryptocurrency remains a hot potato, it won’t be easy for the U.S. to decide its stance just yet. The internal turmoil regarding CBDC are even more complex in China, which has been pursuing CBDC since 2014 and conducted the world's first digital yuan tests in selected cities. China has repeatedly relaxed and tightened cryptocurrency regulations, recently imposing a blanket ban on cryptocurrencies. It is believed that the blockade of the private cryptocurrency market is aimed at commercializing CBDC. The Chinese government is likely to be aiming to deepen its intervention in the financial economy and challenge the dominance of the dollar through CBDC. However, there may also be side effects, such as the potential contraction of the private financial market, which is why China has also been cautious about accelerating CBDC implementation.

Conclusion

Stablecoins have become a stable fixture in the crypto industry. It is now unimaginable to think of the blockchain market without stablecoins, though risks and trust issues regarding issuers persist. Despite experiencing setbacks, such as the downfall of algorithmic stablecoins like UST, competition among stablecoins has intensified with new builders also jumping into the guaranteed market of stablecoins.

Something that’s expected to have the greatest impact on stablecoins is CBDC. Both the United States and China are engaged in a tug-of-war over the adoption of it, while its adoption is inevitable. The reduction of cash usage in daily life is a global trend. Introducing digital currencies can innovate payment systems and reduce costs associated with inter-country remittances and payments. Thus, governments worldwide are eager to introduce CBDCs to intervene more actively in the financial economy. Stablecoins are seen as unwelcome because they fall outside the government's control.

However, it is difficult for central banks to take on all the tasks traditionally performed by private banks. It is almost impossible for a central bank to process all transaction data, including both large and small payments. Therefore, there are prospects that large transactions, such as reserve payments, could be managed by central banks using CBDCs, while smaller payments could be handled by private banks or stablecoins. As finance becomes more digitalized, the role of private banks diminishes, and fintech fills the gap, which is why it is now possible to enjoy financial services conveniently without physical cash. If CBDCs and stablecoins coexist, stablecoins can also help financially marginalized populations lead stable financial lives as fintech solutions. Already, there is a phenomenon in third-world countries where stablecoins are preferred and used in daily life, and we hope that more stable stablecoin solutions will survive to offer safer stablecoin services.