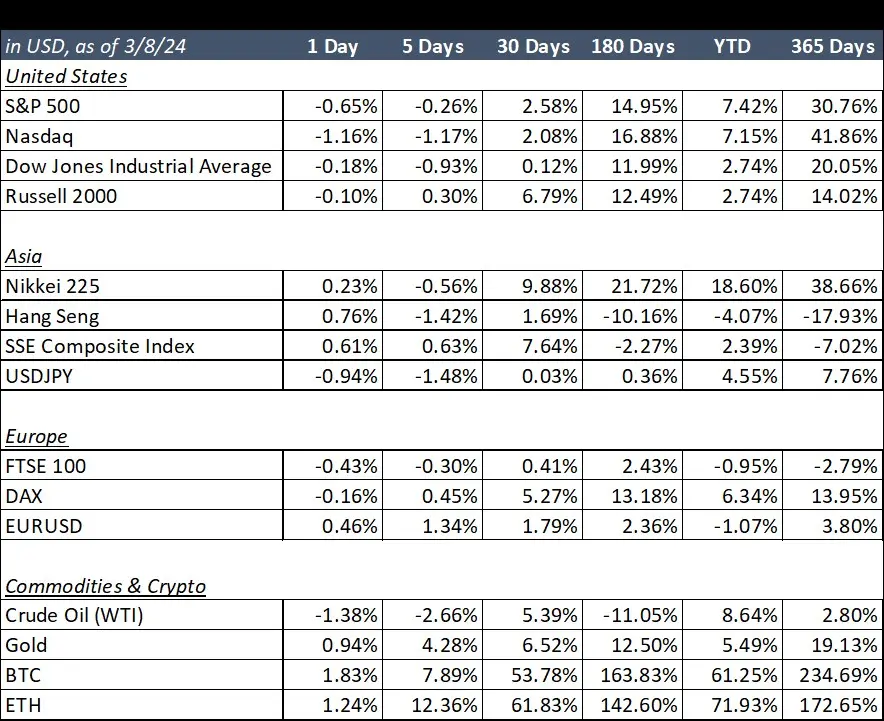

Ruceto Market Recap: US Employment Showing Mixed Signals

US employment data for February

The much anticipated Nonfarm Payroll (“NFP”) data was released by the Bureau of Labor Statistics on Friday. Per Reuters, “Nonfarm payrolls increased by 275,000 jobs last month [in February 2024], the labor Department said on Friday.” However, both January 2024 and December 2023 numbers were revised down substantially, 167,000 lower than previously reported. The unemployment rate jumped to a two-year high of 3.9%.

Much of Wall Street took the latest NFP report as a strong headline number with some weakness hidden in the details, which would lead to the expectation of a rate cut in the middle of 2024. As reported by FT, “Pricing in the futures market shows traders believe the Fed will cut interest rates for the first time as early as June, followed by two or three more cuts later in the year.”

Speaking of rate cuts, President Biden signaled that he believes Fed rate cuts are incoming during a campaign event in PA when he said, “that little outfit that sets interest rates, [the Fed]”… “I can’t guarantee it but I bet you those rates come down.” While the Fed is supposed to be independent and we obviously can’t determine how much sway President Biden’s personal preferences have on their decisions, it’s at least noteworthy that he is betting on lower rates.

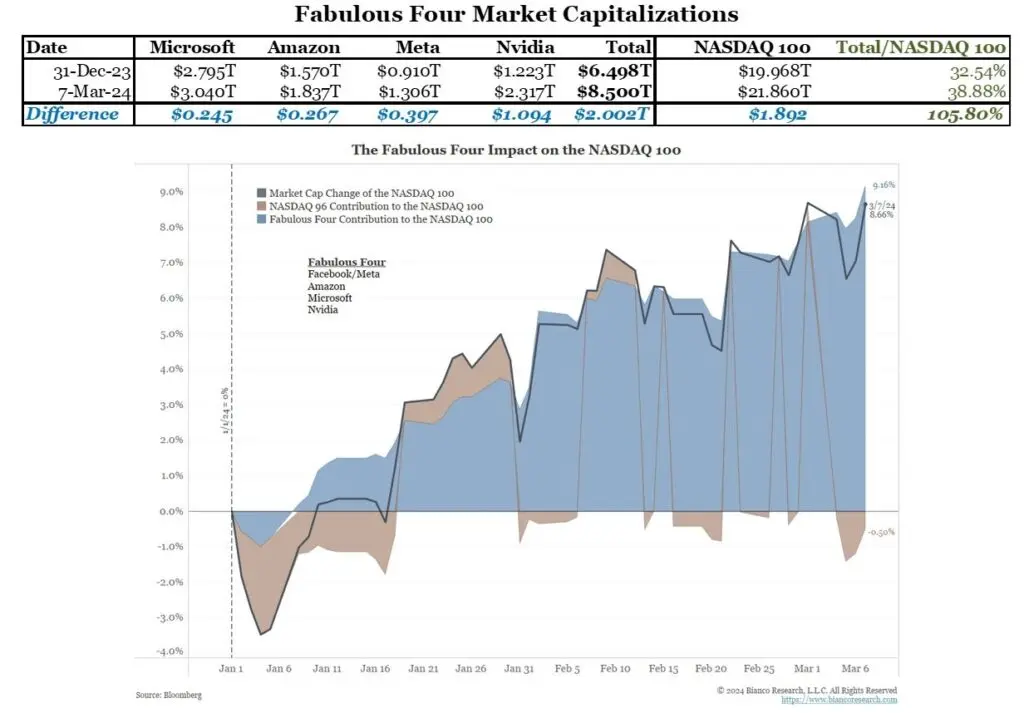

US equity indices are getting more top-heavy

Some eye-opening tweets from Jim Bianco underscored the fact that the Magnificent 7 Fabulous 4 are driving this year’s strong US equity returns, and US indices are getting incredibly top-heavy as a result. “Year-to-date, the “Fabulous Four” have increased the NDX [Nasdaq 100] total market capitalization by 9.16% (blue). The “other 96” have dragged it 0.50% lower (brown).”

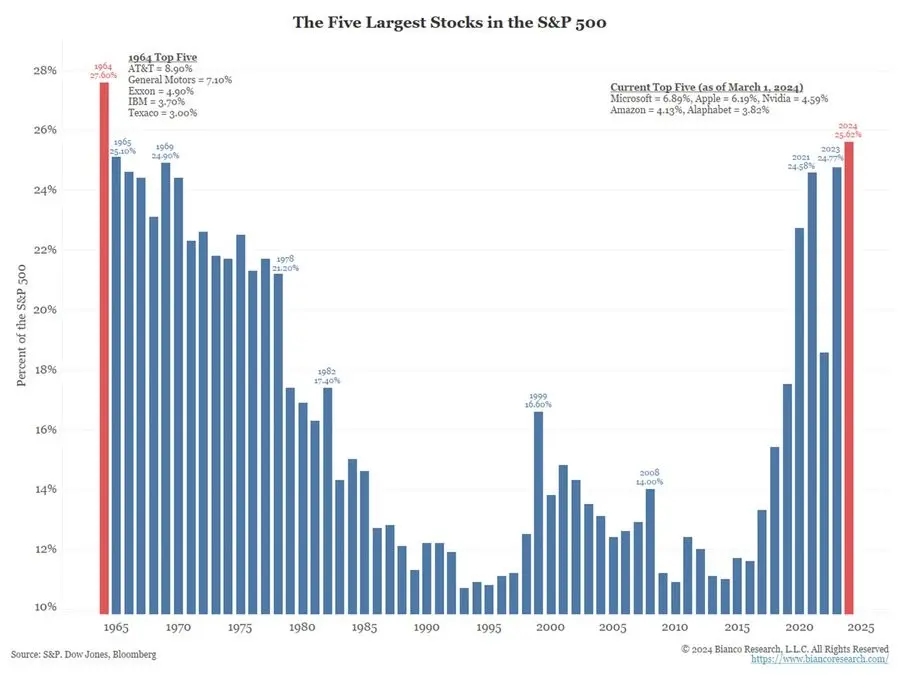

The below shows that the S&P 500 is more concentrated in its top 5 stocks than any other time in the past 60 years.

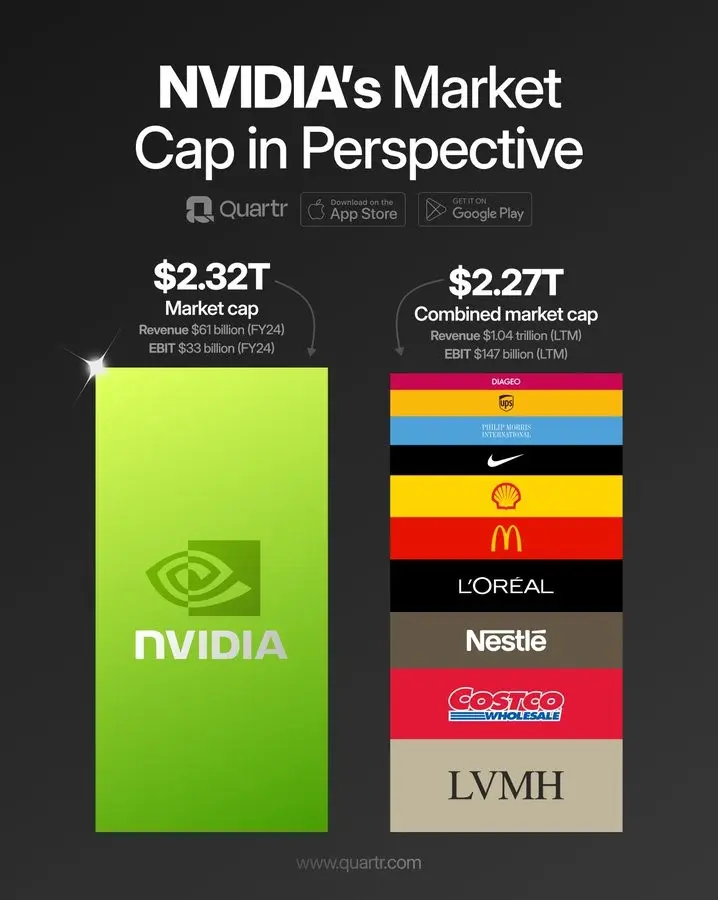

Also, just for fun, the below (as tweeted by Quartr) provides some perspective on the market cap of NVDA compared to other household names:

The good news is that investors didn’t need to pick the top 4 or 7 stocks to benefit from their meteoric rise, they just needed to be invested in the S&P 500 and/or Nasdaq. The bad news is that high market cap concentration can serve as a bad omen going forward. David Rosenberg drew a comparison between the Magnificent 7 and the Nifty 50, “This infamous group of 50 companies were considered strategic ‘buy and hold forever’ picks before their crash in 1973 and ensuing abysmal performance,” … “These were real companies with real investment themes behind them, but investor sentiment turned to euphoria and fueled prices and valuations into bubble territory beyond what the fundamentals justified.”

Comparisons like this to past bubbles are getting more common, so how might those comparisons be wrong? Generative AI hype has led to massive profit growth for NVDA, if the current degree of hype is justified (that’s a big “if,” given the level of market euphoria right now), higher profitability from future AI use cases should eventually flow to a higher number of companies. In other words, the current concentration problem might be solved not necessarily by the Mag 7 going down, but by other companies going up. That optimistic outcome might not necessarily be bullish for a company like NVDA, because investors will have more options when betting on generative AI (see our newsletter from last week when we explained how the generative AI boom has finally driven the Nikkei to a new record high).

Bank of Japan (“BOJ”) may be ending Yield Curve Control (“YCC”)

ForexLive reported that “From Japan over the weekend was a JiJi report saying the Bank of Japan will drop its YCC policy at the March 18 and 19 meeting, replacing it with a program indicating in advance the amount of Japanese Government Bonds it plans to purchase.” YCC refers to a central bank strategy of targeting specific longer-term interest rates by buying or selling bonds. The BOJ has utilized YCC to suppress domestic interest rates, and this has incentivized Japanese investors to invest internationally to obtain yield.

So what does this mean for markets? The BOJ has manipulated the yield of Japanese government bonds lower, so Japanese yields would likely rise if the BOJ steps back. Japanese investors, who are major holders of US debt, would also be less compelled to search for yield outside of Japan. If Japanese investors keep more of their money in Japan, the Japanese Yen should strengthen.

Ethereum is surging

The price of Ethereum hit $4k last week for the first time since December 2021. As reported by Yahoo Finance, “IntoTheBlock data shows that Ethereum mainnet’s revenue from network fees reached $193 million this week, the highest figure since May 2022 and a 78% increase from last week.” In the case of last week, multiple Ethereum-based meme coins more than doubled in price. Additionally, Ethereum-based decentralized exchanges saw a major increase in trade volume. This supports what we said in our previous newsletter, “much of the altcoin universe runs on Ethereum, so it could be viewed as an entrypoint into that market for newbies.”

Want our free weekly newsletter delivered straight to your inbox? Sign up here to stay on the cutting edge of global markets.

Disclaimer: The content presented is for informational purposes only and does not constitute financial, investment, tax, legal, or professional advice. Nothing contained in this report is a direct or indirect recommendation or suggestion to buy, sell, make, or hold any investment, loan, commodity, security, or token, or to undertake any investment or trading strategy with respect to any investment, loan, commodity, security, token, or any issuer. Ruceto does not guarantee the accuracy, completeness, sequence, or timeliness of any of this content. The authors of this article may hold any crypto, securities, or assets mentioned in this article. Please see our Terms of Service for more information.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article is provided by CrossAngle’s third-party research partners. CrossAngle does not have any editorial control over this article and does not warrant the accuracy and timeliness of the information contained herein. This article may contain links to third-party websites, over which CrossAngle disclaims any control or responsibility.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.