5 Crypto Sectors That Will Lead the Market in 2024 — Part 1: Derivatives

On-chain derivatives have made significant improvements in user experience, and products have become increasingly competitive compared to their trading counterparts on CEXs. Despite this, on-chain derivatives still have a long way to go.

Key Takeaways

- On-chain derivatives have made significant improvements in user experience, and products have become increasingly competitive compared to their trading counterparts on CEXs. Despite this, on-chain derivatives still have a long way to go.

- With increasing regulatory developments including the highly-anticipated Bitcoin ETF, the crypto space can expect large inflow of capital and liquidity, if the ETF is approved. This renewed interest in the space emphasises a need for more structured and sophisticated financial tools such as derivatives like perpetuals and options.

- Derivatives are a key tool to capture the influx of RWAs into the space, allowing users to gain more exposure from sectors that are currently gaining mainstream attention.

- A significant proportion of trading volume in TradFi and CEXs is dominated by the derivatives market. As DeFi continues to grow, so will the on-chain trading of derivatives.

- Derivatives tend to do significantly well when there is market volatility. With many events lined up in 2024 for the crypto space — Bitcoin Halving, Bitcoin ETF etc. — the derivatives sector will benefit greatly from speculation and outcome of these events. Furthermore, derivatives platforms are more effective in generating fees from trading activities compared to spot.

CEX vs DEX

In this article, our focus will be on perpetuals, undoubtedly the most prolific type of crypto derivative.

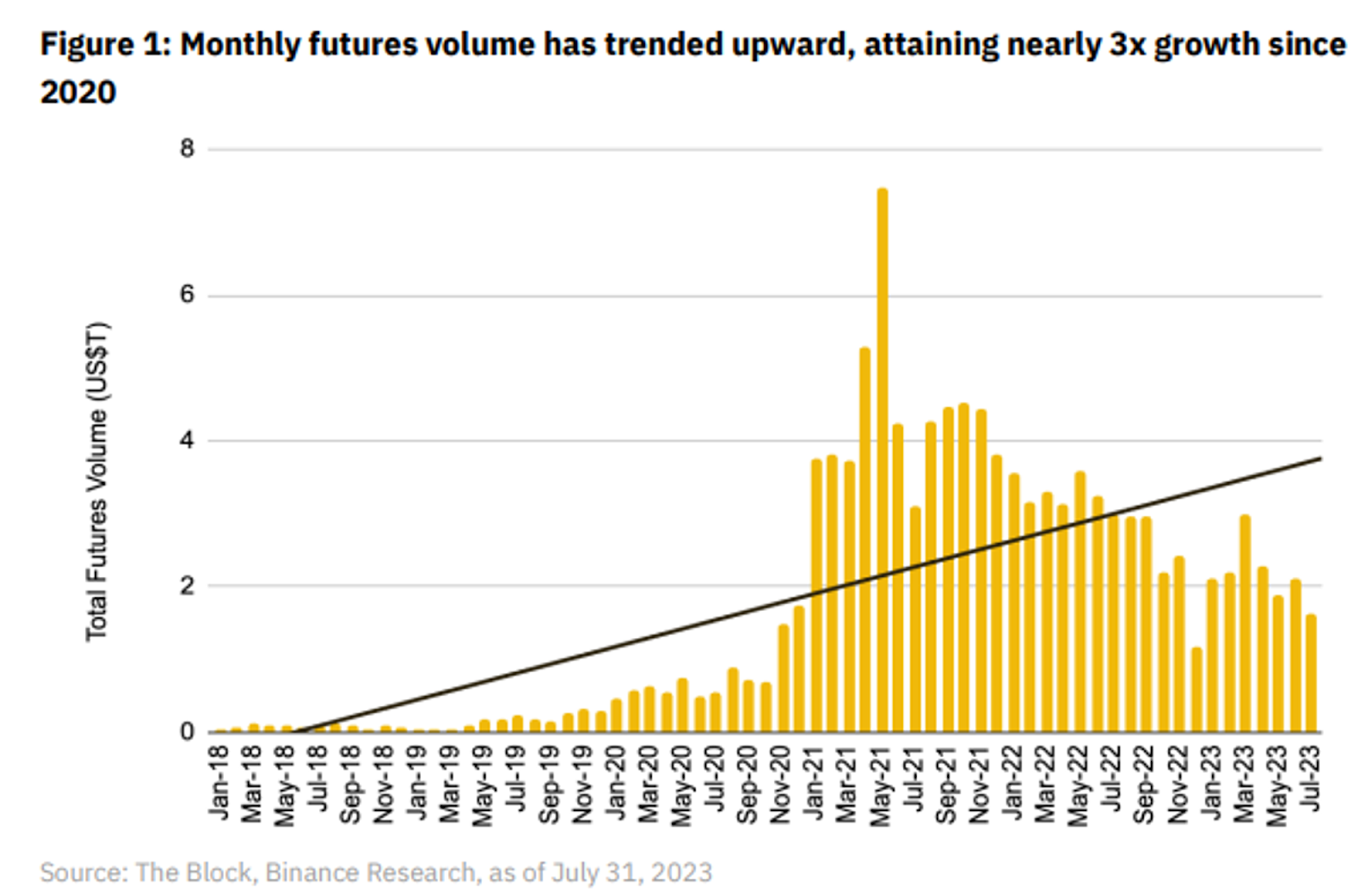

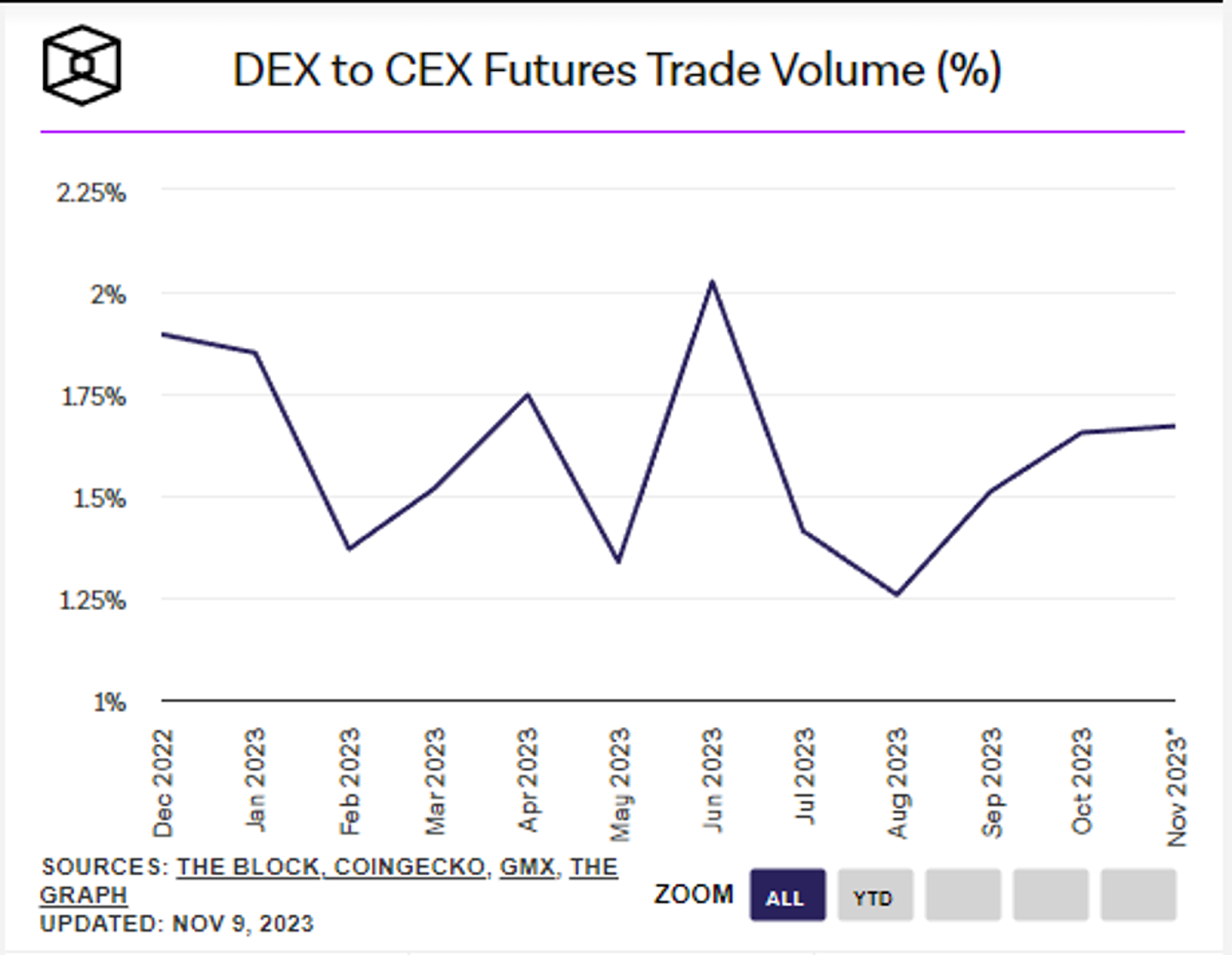

Perpetuals have garnered significant traction in recent years, achieving much higher trading volumes compared to any other financial instrument, forming one of the largest verticals in crypto. Majority of perpetual trading volume in crypto occurs on CEXs.

Despite significant UI/UX and liquidity improvements made by decentralised on-chain perpetual platforms, CEXs still dominate trading volume by a huge margin. As seen in the graph below by The Block, DEXs have not been able to increase their foothold in the perpetuals market despite making significant improvements. The ratio of DEX to CEX Futures Trading Volume has also remained relatively stagnant in the past year

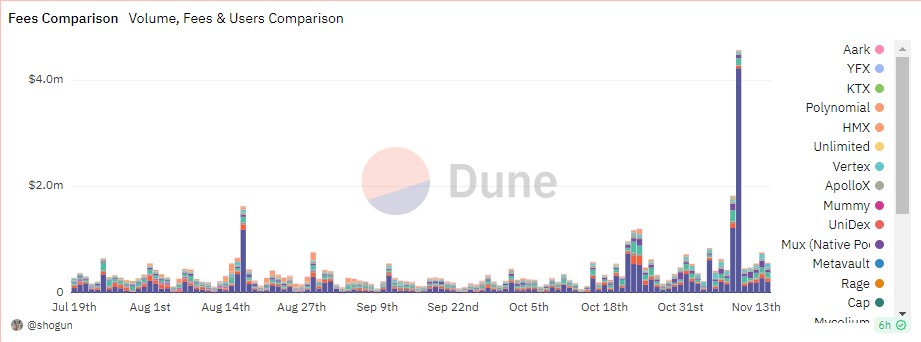

When looking at the fees generated by perpetual DEXs, perpetuals thrive during periods of market volatility. This can already be seen in the current market, with fees for perpetual DEXs skyrocketing due to recent price movements of the industry in general.

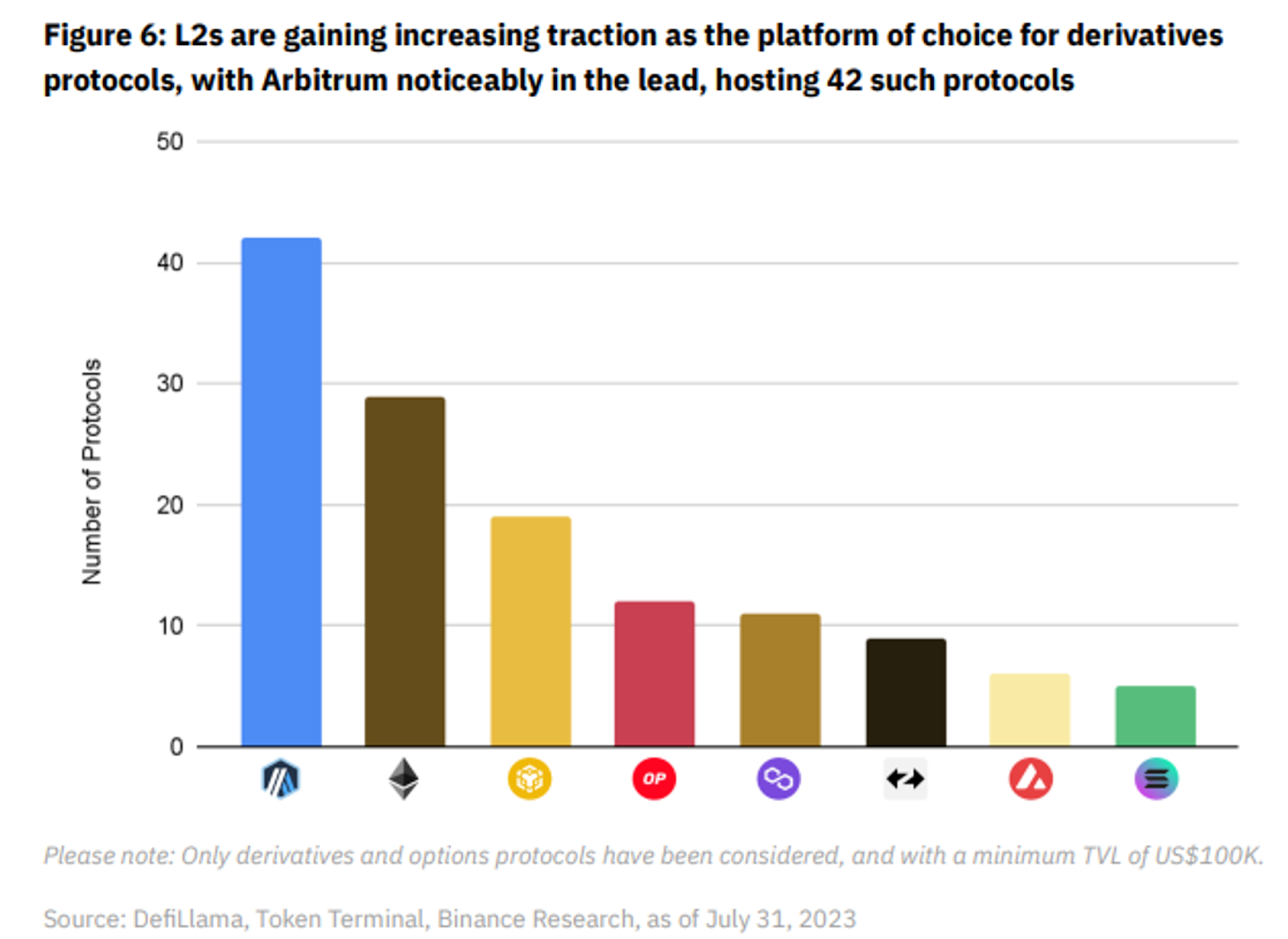

For derivatives to thrive in the ecosystem, there needs to be sufficient infrastructure in place to support the growing market. Layer 2 and Layer 1 protocols have been competing to attract new launches of derivatives platforms that look to provide the best environment for users. Key considerations include security, available liquidity, speed and affordability.

As Ethereum is the leading blockchain ecosystem in terms of adoption, Layer 2 protocols are finding great success in attracting major DEXs. Layer 2s like Arbitrum and Optimism are consistently attracting more derivatives to launch compared to earlier projects focusing on Layer 1s. The increasing popularity can be attributed to the development of Layer 2s tailored to optimize for specific use cases and user activities, while leveraging Ethereum's security.

This provides a more suitable environment for derivatives that allows users to interact with the platform without the need to break the bank for gas fees..

The State Of Perpetual DEXs

dYdX

Introduced dydx v4 to improve token utility through revenue sharing for token holders, bringing more value accrual.

dYdX is one of the early movers in the perpetual derivatives sector, boasting one of the highest trading volumes amongst derivatives platforms. In the past, key concerns have been brought in regard to a few main areas:

- Lack of token utility

- Scalability

- Centralization of the order book mechanism

The launch of dYdX v4 was aimed to combat these issues.

The dYdX token was originally intended for two main purposes: governance and fee discounts through staking. These utilities caused the community to actively question the long-term value accrual for token holders. dYdX v4 tackles this by having fees generated on dYdX’s chain and collected from the protocol distributed to both validators and stakers.

To solve the issue of scalability, dYdX v4 migrated from Starkware to its standalone dYdX chain built atop the Cosmos SDK and Tendermint’s PoS consensus protocol, enabling dYdX to improve future scaling of its order book mechanism thereby allowing throughput long-term.

The last improvement dYdX v4 enables is further decentralization of the protocol, with dYdX’s order book and matching engine now committed to be fully on-chain.

GMX

GMX v2 approaches liquidity differently and offers synthetic positions to broaden its asset offerings — something previously limited by the design of GLP. On GMX v1, GLP is composed of 50% stablecoins and 50% risk assets (ETH, BTC, and others). However, the upcoming GMX v2 will bring about a change to this model with the introduction of GM pools. In contrast to GLP and its multi-asset baskets, GM pools will only hold two types of assets: a long asset and a short asset. Depositors can decide to deposit either only the long/short asset or both in balance. However, if the deposits affect the skew of the pool, depositors will be faced with a price impact upon adding assets.

The introduction of GMX v2 will aim to drive more benefits to specific traders and LPs.

The Shift to Isolated Markets

The shift to isolated markets as mentioned above causes some key points of discussion for liquidity providers (LPs) within GMX’s ecosystem. On one end, LPs have now been given more autonomy and control over their own risk management when supplying liquidity as well as the specific assets deposited. On the flip side, fragmented liquidity long-term has been a cause for concern, and long-tail assets are more likely to suffer from the change to fragmented liquidity.

Exploring the introduction of Price Impacts and Funding Fees

Vulnerability to price manipulation, as well as an imbalance between long and short positions was a key concern brought up when looking at GMX v1. The introduction of price impacts and funding fees helps introduce a balance between trading sentiment, ensuring that liquidity providers (LPs) have reduced risk and are safeguarded through equal risk distribution. One key concern here is that the introduction of price impacts and funding fees could lessen GMX’s appeal for larger traders who benefit from zero slippage swaps and trades through GMX’s v1 design. Nevertheless, since GMX v2 doesn't replace v1 but essentially operates in tandem, it enables GMX to consistently secure market share in the long run, catering to both small and large traders.

Fee Reduction Strategy

With the concept of higher fees through the introduction of price impacts and funding fees discussed above, GMX v2 has been able to strike a balance through reducing trading fees to 0.05%, half of the initial fee introduced in GMX v1. The question as to whether this will eat into GMX’s lead as the highest fees earned by Perpetual DEXs is a key point to consider.

What Is Needed For Derivatives To Succeed?

When looking at the recent changes within industry leaders for decentralized perpetual DEXs, there are some key trends that can be identified as to how industry leaders are aiming to capture more market share from CEXs, and what exactly is needed for derivatives to succeed going forward long-term.

High Liquidity and Efficiency

The significance of liquidity in perpetual decentralized exchanges is a key factor in attracting and retaining traders for the long term, as trades must be executed swiftly and efficiently. Balancing the need for liquidity in perpetual DEXs involves finding a delicate equilibrium between encouraging liquidity, mitigating risks for liquidity providers, and ensuring ample liquidity for all assets, including those considered long-tail. As previously discussed, the enhancements to the quality of life for liquidity providers in GMX v2 are likely to stimulate stronger liquidity for specific pairs. However, the lingering question remains whether long-tail assets will continue to face challenges with fragmented liquidity. In summary, it is evident that traders tend to favor perpetual platforms with the highest liquidity, as it plays a pivotal role in delivering a robust user experience during trading.

Low Fees

Traders frequently seek platforms with competitive fee rates to optimize the profitability of their trades, underscoring the clear necessity for low fees to ensure users have a robust trading experience.

When comparing the top 4 perpetual exchanges (CEXs & DEXs) by 24-hour trading volume, and their Maker/Taker fees (Table below), we can observe that the fees for decentralized perpetual platforms have decreased significantly, and are relatively on-par with the fees quoted by CEXs.

|

Maker Fees |

Taker Fees |

|

|

Binance |

0.02% |

0.05% |

|

Bybit |

0.02% |

0.055% |

|

OKX |

0.02% |

0.05% |

|

Bitmart |

0.02% |

0.06% |

|

dYdX |

0.02% |

0.05% |

|

GMX |

0.05% |

0.05% |

|

Kwenta |

0.02% |

0.1% |

|

Vertex |

0% |

0.04% |

|

Hyperliquid |

0% |

0.025 |

|

Gains |

0.024% to 0.16% |

0.024% to 0.16% |

|

MUX |

0.12% |

0.12% |

|

Perpetual Protocol |

0% |

0.1% |

|

APX Finance |

0.04% to 0.16% |

0.04% to 0.16% |

|

Level Finance |

0.05% |

0.05% |

|

RabbitX |

0% |

0.025% to 0.07% |

|

Drift |

0% |

0.03% to 0.1% |

*Maker and Taker Fees comparison looking at the lowest tier of trading volume for each platform

Comparing the Maker and Taker fees for the different platforms, we can conclude that fees are much more competitive in the current market. Low fees are now expected on perpetual platforms to acquire users. Considering this, attracting and retaining new users hinges on low fees. Given that all platforms are essentially adopting highly competitive rates, the question arises as to what additional factors perpetual DEXs can incorporate to continually enhance user experience and compete on an equal footing with CEXs.

Inclusion of Long-tail Assets

The inclusion of long-tail assets and a more diverse range of assets available for trading through perpetual DEXs is a massive competitive advantage compared to CEXs.

The idea of permissionless asset listing in perpetual DEXs theoretically enables them to consistently add suitable assets, provided there is sufficient liquidity available to be accessed and leveraged. This is a huge advantage over CEXs that are often unable to list pairs due to conflict of interests, or regulatory reasons or concerns.

The key question here is how perpetual DEXs are able to provide a safe and efficient trading ecosystem for long-tailed assets when there is sufficient liquidity available for trading. This is another key benefit introduced in GMX v2, in which the silo-ed pools introduced can continue pushing the narrative of permissionless listings for perpetual DEXs. This has a huge potential to further capture market share from CEXs, with perpetual DEXs now having first mover advantage in listing new pairs and protocols. However, there are also key risks like sufficient liquidity, market manipulation, and other mitigations have to be put in place to ensure protection of liquidity providers.

Impossible’s Predictions for 2024

90% Prediction: Improvement of Liquidity Infrastructure for Perpetual DEXs in order to capture more traders

Improvements of infrastructure to provide perpetual DEXs with the most important resource: Liquidity. Introduction of protocols with vaults that allow for omni-chain liquidity deposits, with the improvement of infrastructure for multi-chain asset transfers will allow for easier deposits for LPs long-term, whilst also being able to attract different LPs through different vault strategies.

50% Prediction: Perpetual DEX volume in 2024 to increase by more than 3x the volume compared to 2023

When looking at the narratives for perpetuals DEXs above, aligned with the increasing number of macro catalysts introduced in 2024 (BTC ETF, ETH ETF, EIP-4844) we believe a 3x increase in trading volume for perpetual DEXs is relatively feasible, with improvements and introductions of new models for perpetual DEXs continuing to eat into CEX perpetual market share.

10% Prediction: Innovative new models as LPDFi will allow for more competitive coverage and volume for on-chain derivatives trading of long-tail assets

When comparing the number of trading pairs on popular perpetual DEXs such as Kwenta and dYdX, traders are able to tap into 74 and 33 different pairs respectively. When compared to CEXs such as Binance Futures, Bybit Futures and OKX Futures, trading pairs are at 323, 378 and 511 respectively. However, we believe the innovation and introduction of new perpetual DEX models based on LPDFi can enable Perpetual DEXs to catch-up to CEXs in terms of number of active trading pairs, and potentially capture a significant share (up to 10%) of total volume for long-tail assets.

Oracle reliant vAMMs and Pool-Based Models

Pool-oriented DEXs undeniably carve out a niche within the on-chain perpetuals sector, presenting enticing attributes for both the supply and demand side of a decentralized perpetual platform. Liquidity providers can be attracted from both private and public capital. Overall, vAMMs provide a good option for traders who are looking for decentralisation and instant liquidity.

The drawbacks associated with vAMMs and pool-based models are multifaceted. Firstly, these models necessitate a significant amount of capital that often remains idle as open interest is restricted from potential losses, leading to inherent underutilization. Liquidity providers face the challenge of counter-trading positions, and the open interest is constrained to the protocol's ability to pay out in total loss scenarios. Moreover, the reliance on oracle support limits available pairs, exposing the system to vulnerabilities associated with potential oracle exploits. Additionally, liquidity providers are at high risk during periods of extreme market volatility, particularly in trending bull markets, making them prone to substantial losses. This heightened risk introduces the possibility of a "death spiral," where liquidity providers withdrawing liquidity triggers a cascading effect, diminishing exchange liquidity, deterring user participation, and prompting further liquidity pool withdrawals, creating a potentially destabilizing cycle for the platform.

Request-for-Quote (RFQ) Models

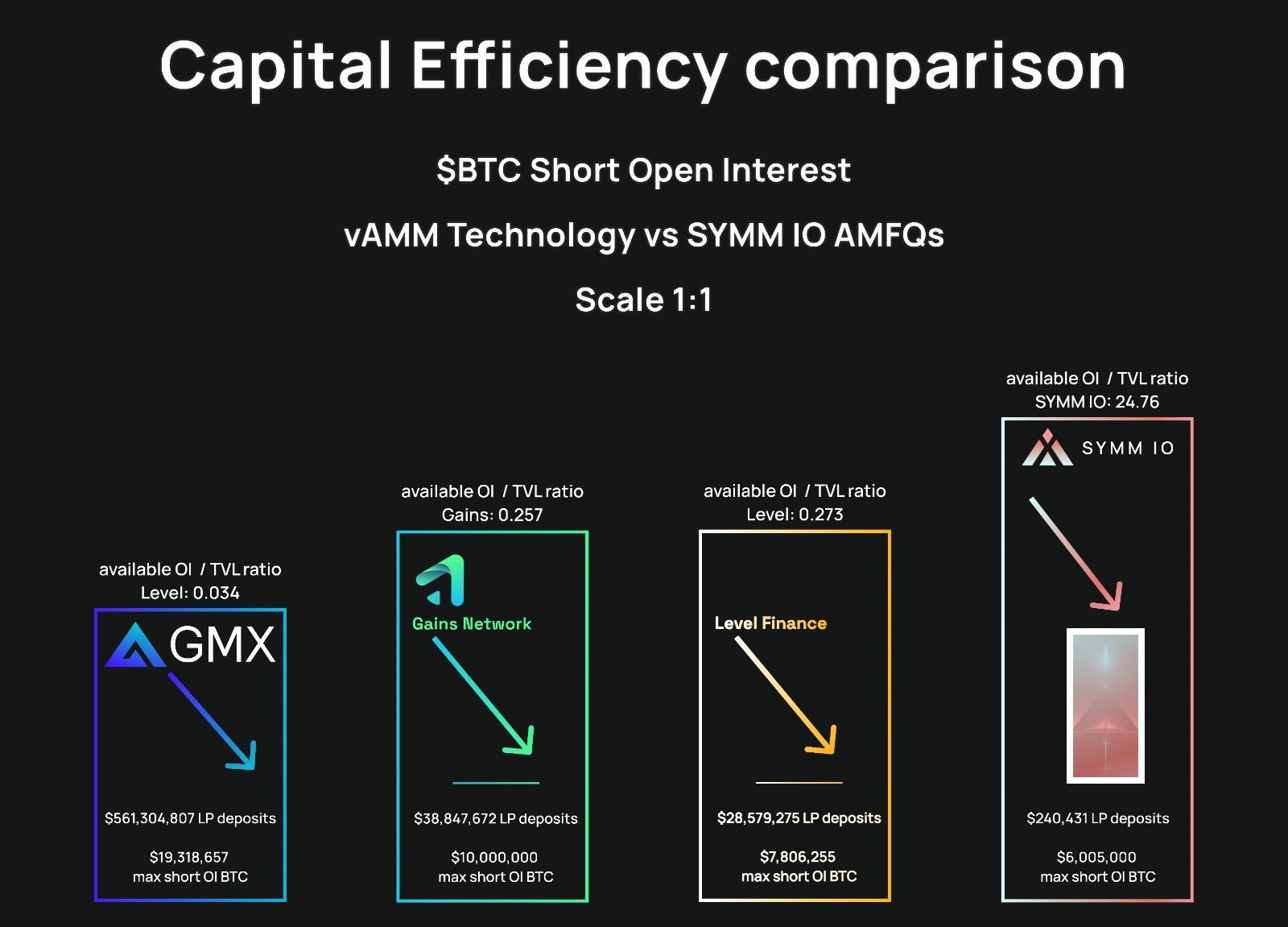

The Request-for-Quote (RFQ) model introduces a paradigm shift in the decentralized trading landscape, offering a host of advantages. One primary benefit is the liberation of liquidity providers from the obligation to lock liquidity in advance. Unlike derivative trading protocols dependent on order books or liquidity pools, the RFQ model enables liquidity providers to deploy capital only when requested, optimizing efficiency by ensuring that capital is consistently active. This unique feature allows liquidity providers on RFQ-based platforms to seamlessly offer liquidity across multiple platforms simultaneously, accepting trades from various sources. Furthermore, the RFQ model addresses concerns related to Miner Extractable Value (MEV) and Sandwich Opportunities, mitigating the risk of traders encountering prices different from what they initially observed. Capital efficiency is a cornerstone of the RFQ model, offering more volume on less capital and guaranteed price executions compared to more familiar vAMM models. This can already be seen down below within perpetual platforms leveraging the RFQ model such as Symmio.

Source: https://docs.symm.io/overview/introduction-to-symmio/comparing-capital-efficiency

From the diagram above, we can see that Symmio highlights the efficiency of RFQ models compared to AMMs through comparing Total Available Open Interest and TVL or LP deposits. In simple terms, the same amount of TVL will allow for higher volume through more positions able to be open. For example, on Symmio, $240,431 worth of LP deposits allows for a maximum short Open Interest for BTC of $6,005,000, but comparing to other Perpetual platforms leveraging the vAMM model such as Gains (GNS), $38,847,672 worth of LP deposits allows for a maximum short Open Interest for BTC of only $10,000,000. The main reason for this disparity in capital efficiency would be that for vAMMs, in extremely volatile market conditions, can cause significant losses for LPs, and thus vAMM designs are required or forced to have a substantial surplus of capital in order to help cushion these losses or setbacks. On the flipside, RFQ models such as Symmio’s approach enables a higher portion of capital to be allocated and used, rather than merely serving as a form of precaution.

However, like any model, the RFQ approach is not without its drawbacks. One notable concern revolves around the decentralization of counterparties, an essential aspect for RFQ models, especially concerning perpetuals. The efficiency of the system relies on robust competition among the quotes provided, emphasizing the need for a diverse and decentralized pool of counterparties. While the RFQ model offers a plethora of advantages, the maintenance of these key principles is crucial for its sustained success in the dynamic and evolving landscape of decentralized finance.

Orderbook Models

Orderbooks are widely known for their use on CEXs, as well as leaders such as dYdX utilising order book mechanisms within the decentralized perpetual platform space. One of the main benefits of the order-book model would be a familiar user experience for both traders and market makers similar to that of a centralized exchange. Furthermore, they provide transparency in the market, exhibit high efficiency concerning fees and liquidity, and facilitate a significant level of internal price exploration.

However, on-chain orderbook models have disadvantages that must be addressed to provide a stable trading environment for users and liquidity provideres. On-chain infrastructure often lacks what is required for efficient order books due to their limited throughput, with orderbooks needing high speed and low latency due to the frequencies at which orders are inputted and edited. On-chain orderbook perpetual platforms such as dYdX have aimed to mitigate this drawback through the move from StarkEx to their very own Cosmos standalone chain. Another drawback of on-chain orderbook perpetual platforms is that liquidity providers onboarded are often institutional capital from market-maker that must be beforehand, and are often underutilized, much like vAMMs and pool-based models . Maintaining orderbooks requires extensive amount of capital commitments, with maker orders needing to be committed capital.

LPDFi

LPDfi serves as the term for the emerging landscape of Liquidity Provision Derivatives (LPDs). It delineates the frameworks within current DeFi offering, by leveraging Uniswap V3 LP positions and crafting innovative offerings, including but not limited to options and perpetuals.

One of the main benefits introduced by platforms offering perpetuals through LPDFi is their approach to liquidation for traders, and the introduction of protected perpetuals. Protected perpetuals represent a trading instrument enabling users to assume either long or short positions without facing liquidation due to price fluctuations. In practical terms, this implies that in the event of a substantial market price decline, traders are shielded from position liquidation and are spared from incurring negative profit and loss (P&L). Consequently, if a trader adopts a long position and the market trends in the opposite direction, their underlying thesis remains intact without incurring significant losses. Furthermore, liquidation in this context doesn't hinge on price fluctuations but transpires gradually over time. As positions remain active, traders cover the cost of safeguarding their positions in a step-by-step manner, drawing from their margin. In addition, perpetuals built on top of LPDFi eliminates counterparty risk, as each position traders engage in aligns directly with liquidity in a single tick. In essence, the impermanent loss incurred by a liquidity provider translates into impermanent gain for the trader in itself. This may seem like a disadvantage for LPs, but in essence allows LPs to have higher earning potentials through trading fees on the platforms itself.

Project Highlight — Fluo

With the breakdown of perpetual platforms above, one of the key constraints and challenges faced by perpetual platforms is still the battle for liquidity. We are excited to highlight one of Impossible Finance’s portfolio companies that aims to tackle liquidity challenges and further grow the perpetual DEX market, earning more market share from CEXs.

Fluo Finance is the first omnichain liquidity platform, uniquely positioned to assist liquidity providers in executing market-making strategies across any blockchain and on any decentralized exchange in an automated and dynamic manner, with a particular focus on perpetual markets. Fluo’s value proposition for the perpetual space is clear: the ability to provide benefits for all stakeholders and participants.

Firstly, LPs are able to direct deposits into Fluo’s vaults that automatically deploy market making strategies, allowing LPs to earn higher yields whilst receiving direct incentives. DEXs can leverage higher liquidity and added assets to attract more traders and earn higher fees, and Traders on perpetual platforms are able to benefit from higher liquidity through lower spread and slippage more comparable with CEXs, as well as a wider range of assets to be traded.

In essence, as the thesis for on-chain perpetuals to continue growing and capturing market share, fragmented liquidity is often a problem for both platforms and on-chain traders, and thus Fluo has positioned itself to be able to create and divert more efficient streams of liquidity, allowing all stakeholders to benefit from this. To conclude, Fluo has positioned itself to democratize market making with automated vaults, enabling public liquidity the opportunity to earn market making fees, and become the go-to liquidity layer for perpetual DEXs going forward.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article is provided by CrossAngle’s third-party research partners. CrossAngle does not have any editorial control over this article and does not warrant the accuracy and timeliness of the information contained herein. This article may contain links to third-party websites, over which CrossAngle disclaims any control or responsibility.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.