Evaluating Altcoins as Long-Term Holds

Powered by Ruceto

Evaluating Altcoins as Long-Term Holds

Bitcoin has been up 154% in 2023! With reignited activity in the industry, some think we are in the early stages of a bull market. Given the increased interest in the industry, now could be an interesting time for investors to look at altcoins. But how does one approach altcoins when there are such a large variety of projects, spanning across finance, social media, gaming, logistics, and more? This article will discuss how to evaluate altcoins in a long-term framework.

Crypto investments in its current state is heavily technical analysis based – even institutional investors largely employ their analysis on technical trends. Due to the volatility of crypto, technical analysis can be an extremely high-risk high-reward business. Social metrics are also heavily followed by retail investors. If a coin generates hype, or is a popular “meme coin”, it is often a candidate for short-term buying and selling.

But when evaluating the long-term prospects of alt-tokens, a mix of fundamental analysis and macro analysis should be considered. Traditional methods combined with various economic metrics can give investors an idea of the long-term prospects of a project. More specifically, the methods that we will discuss in this research article consists of analyzing the technology and use case of a project, reviewing tokenomics and governance, evaluating token prices, and considering macro trends.

Analyze the Technology and the Use Case

When looking at a project’s long term prospects, fundamental analysis should be considered. Fundamental analysis is using financial, industry, and market data to evaluate a company. A common objection is that fundamental analysis is difficult to perform on many crypto projects because they are still at such an early stage. For example, trying to run a discounted cash flow analysis often doesn’t make sense – it is not possible to conduct cash flow analysis on a project that has no cash flows. Also, sometimes being a token holder does not necessarily equate to being a shareholder, so this is where fundamental analysis will not be applicable.

However, there are instances where using fundamental analysis makes sense. This is because ultimately, crypto needs fundamentals to flourish. It has to actually be used for something. When there is a utility and financials related to a project, it is generally possible to use fundamental analysis. Therefore, the first question when looking at a project should be: what problem is it solving? Furthermore, is blockchain the right solution for this particular problem? In other words, when evaluating any blockchain project it is important to ask if this project makes sense to be in web3 and is it easy to use?

Furthermore, there could be a situation where blockchain technology is the ideal use case, but existing technology and infrastructure cannot efficiently address it yet. SocialFi is an example of this. SociaFi is tying social media profiles and personal data to blockchain. This in theory could compete against traditional social media like Facebook because there is a natural demand for users to own their data, and blockchain technology is an effective way to address this demand.

However, the problem that SocialFi projects have faced to date is their inability to gain traction or generate a sustainable revenue stream. The blockchain is too visible - for example users need to know how to use wallets to sign up for the project. It is still easier for most users to sign up using an email than learning how to use a wallet. Although the demand for web3 social media exists (own your own data and monetize it yourself, etc.), the user experience is currently too cumbersome for mass adoption.

On the flip side, there are some projects where blockchain technology is already better than off- chain alternatives. For example, XRP is a cryptocurrency that was designed specifically to be used for cross-currency payments. The XRP Ledger can settle transactions across the world in 3-5 seconds with transaction fees that are less than one cent. Non-blockchain alternatives currently employed by banks are far slower, more expensive, and require capital to be tied up in pre funded accounts. Of course, there are a number of challenges to the widespread use of XRP as a payment method in the real world, but if we consider only the technical characteristics of the blockchain, we can expect to see improvements to the current remittance system.

Another example of a strong use-case is layer-1 infrastructure built for gaming. Building a game in a layer-1 naturally facilitates a secondary market as items can be NFTs that are transferable between users. Additionally, this enables collaboration between different games since an in-game item (that is a NFT) can in theory also be used for another game. If great games are developed in the crypto space, there is a clear use case for gaming layer-1 infrastructure.

In conclusion, Investors should answer these two questions as the first step of analyzing the long-term prospects of a project:1) what problem is it solving; 2) Is blockchain the right solution for this particular problem. If a project has long-term viability and gains massive adoption, the price of its token is almost sure to increase.

Tokenomics and Governance

The tokenomics of a cryptocurrency refers to its utility, supply, and distribution. For a project to have “good tokenomics,” it essentially means that it has good incentives in place for stakeholders to create economic value.

A token’s utility can include voting/governance, staking, use as a currency, or any other project specific utility. Meanwhile, when estimating the economic value of a token, it’s important to determine if a token has some form of dividend-like revenue sharing capacity, or if token holders can at least vote to capture a portion of revenue in the future.

Similarly, it's important to look at the concept of quantity as well when estimating the economic value of a token. So when referring to the supply of a particular token, one can refer to the number of tokens in circulation today and held in public hands (“Circulating Supply”), or the maximum number of tokens in circulation after all tokens have been unlocked and distributed, less the tokens which have been burned (“Total Supply”). Market capitalization (“MC”) equals the current token price multiplied by the Circulating Supply, and fully diluted market capitalization (“FDMC”) equals the current token price multiplied by the Total Supply. MC will fluctuate as tokens are unlocked, so FDMC will be a more stable metric for long-term investors when estimating the value of an altcoin.

Examining the distribution of a token makes it possible to determine if governance is truly decentralized, and if there is significant risk of major selling pressure from an individual or small group. For example, maybe an institution purchased a large number of tokens early at a significant discount and is incentivized to sell soon to lock in a profit. Perhaps the founders hold a large share of the tokens and are looking for an opportunity to reduce their personal economic exposure to the project. Also, if most of the voting rights are held by a small group, there is a risk that they will intentionally or unintentionally behave in a way that is detrimental to other token holders.

Making Sense of the Token Price

Token prices are extremely volatile in the crypto industry. But fundamental analysis can help investors make sense of what the price means. For example, market comparables (“comps”) are a great way to gauge what the value of a token is compared to competitors or more established projects. Comps is the traditional finance method of using similar projects as a benchmark to measure value. It’s similar to looking at how much your neighbor’s home sold for to gauge what your home should be worth. It’s also similar to the analysis of stocks in the public equities market and considering the potential upside/downside of a token.

To calculate a multiple, a numerator (the top number) and denominator (the bottom number) must be selected. For the numerator, FDMC is often used since this is in theory what the project would be “worth” if all tokens were fully released.

What is used as the denominator is just as important, but typically varies a little more:

-

One metric that is sometimes used as the denominator when comparing crypto projects is Total Value Locked (TVL). TVL refers to the value of all assets staked on a specific protocol. A high TVL indicates that a project is popular and liquid, so the expectation of TVL growth is considered bullish for the token price, thus increasing the FDMC of the associated project. FDMC/TVL is one multiple that can be compared across multiple competing chains.

-

Another denominator that is used sometimes is user count or transaction data. For example, how many daily active users are there for this project? How many potential daily active users can this project reach? What are some other projects that have daily active users and how do they compare? This metric can also give you an idea of the potential market size and the project’s potential.

When using FDMC as the numerator, a lower multiple typically suggests that the project could be seen trading “cheaper” compared to a higher multiple. For example, a lower FDMC / TVL suggested that the ratio of staked assets as compared to the total value is high. But a lower multiple does not always mean the project is better. We can explore this concept more below with three examples of evaluating token prices using comps

Comps Using User Count

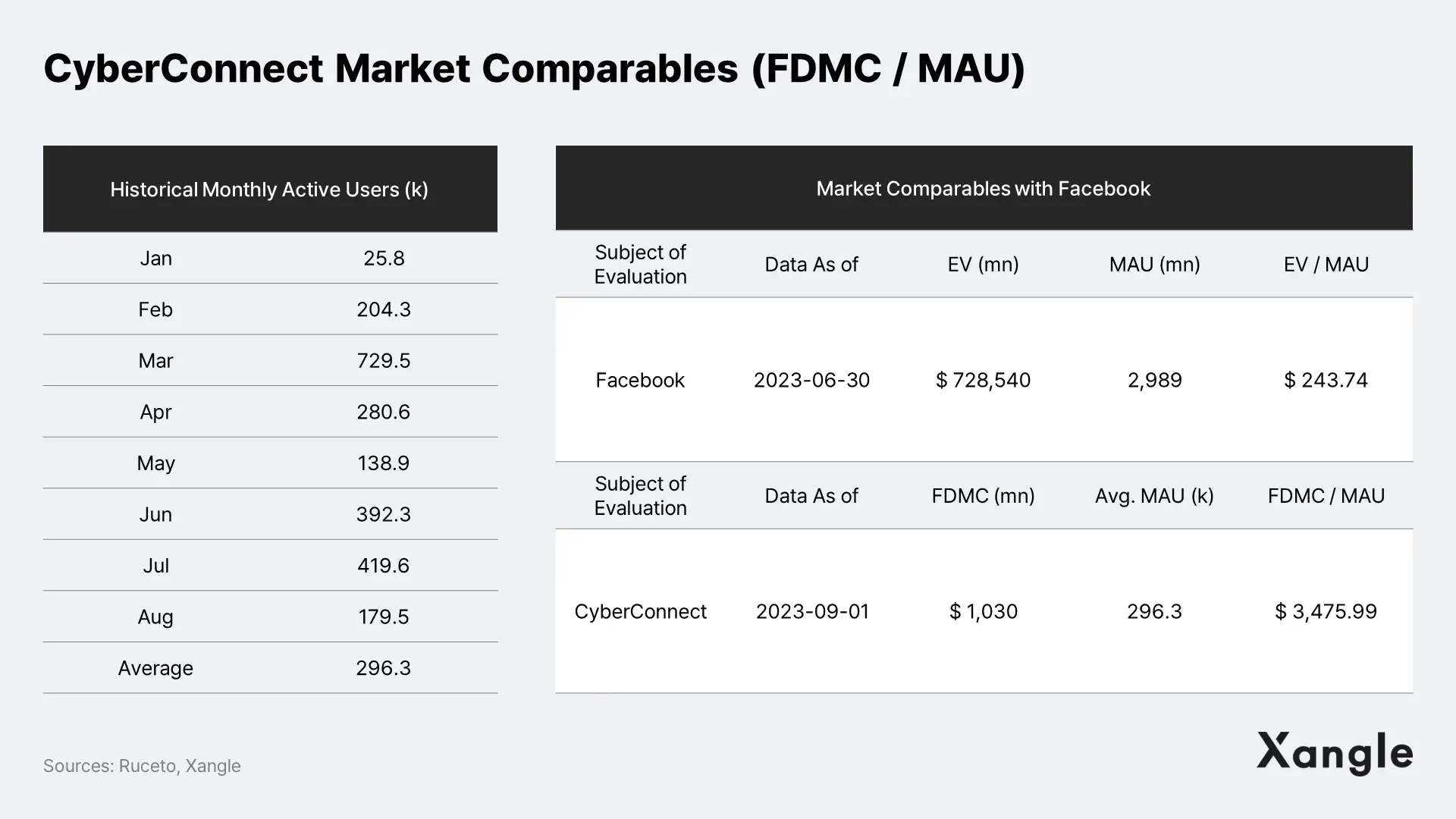

CyberConnect is a web3 social blockchain protocol, where developers can create decentralized social projects giving users control over their own digital identity and data. Ruceto, an institutional and retail research platform, conducted an analysis of CyberConnect’s token price in September 2023 (the tokens were trading at around $10.30). Comps were utilized to compare CyberConnect to a web2 social media app, which suggested that it was overvalued.

To conduct a comp analysis, CyberConnect’s historical monthly active users (“MAU”) for the year were tracked. Monthly active user data was then compared to a web2 project that was also a social network, in this case Facebook (Meta). There was a calculation on what the company value per user was for Facebook (enterprise value divided by average MAU), and then this number was compared to CyberConnect. Cyberconnect’s value per user was calculated by dividing the FDMC by its MAU, which was over 10 times Facebook’s value per user. This implied that Cyberconnect either needed explosive growth to justify its token price or conversely the price needed to come down.

Comps Using Total Value Locked

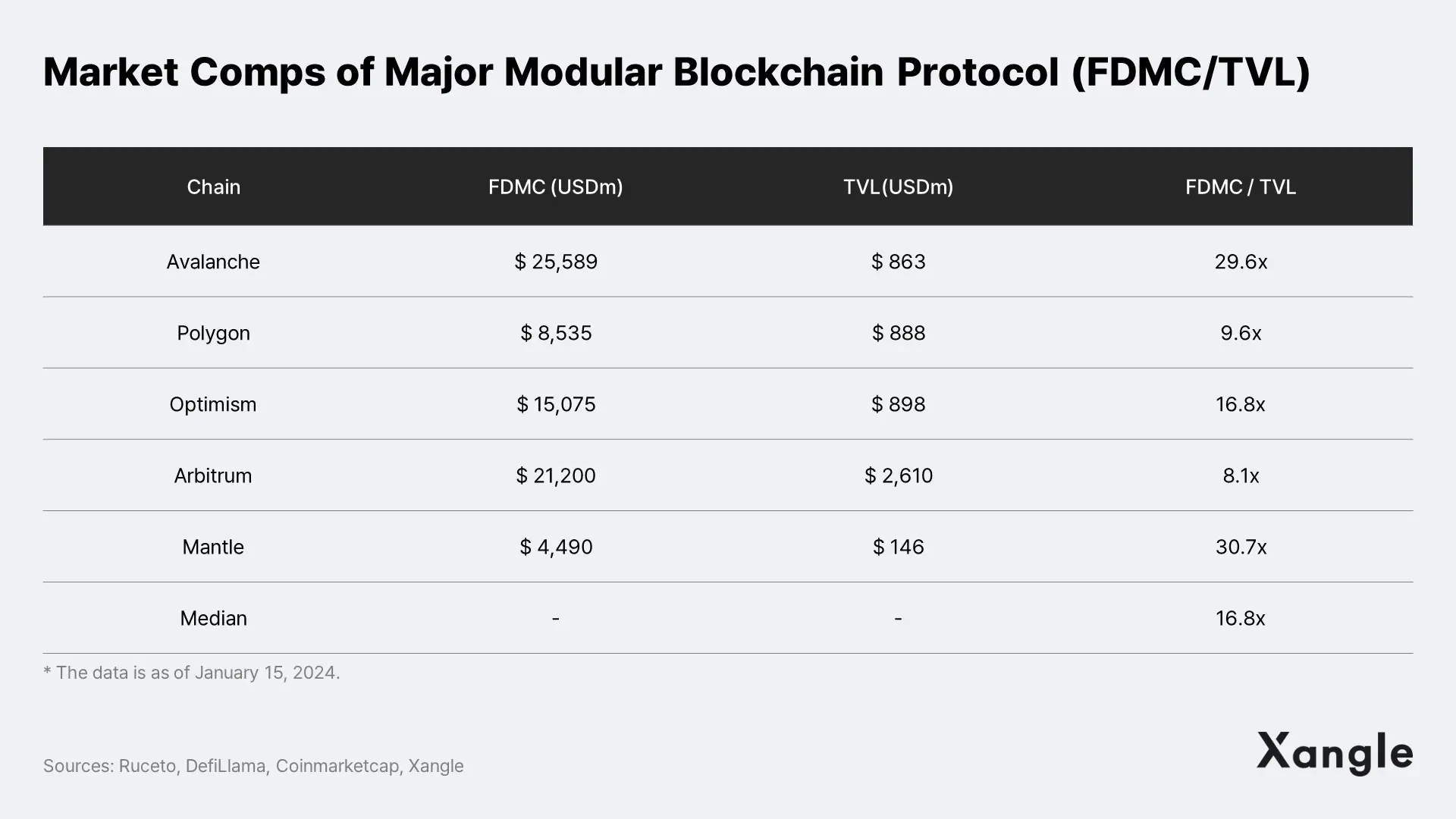

Avalanche is a decentralized proof-of-stake layer-1 blockchain protocol where using FDMC over TVL for comps could be insightful. The process of selecting the right comps is part science and part art. It is similar to selecting comps for homes. For example, if one is attempting to measure the value of a 3 bedroom home, the selected comps will also likely be 3 bedroom homes.

For comps, it is important to not just select any blockchain protocol as a comp, but one that is a peer. Blockchain can be categorized as modular or monolithic. Modular blockchains typically specialize in certain functions and emphasize adaptability as well flexibility by spreading functions over multiple chains. Monolithic blockchains are where everything is done on a single chain. Since Avalanche is a modular blockchain, we utilized the criteria of selecting modular blockchain protocols with at least a TVL of $100 million as a peer group for Avalanche. It is also noteworthy that we were not too specific either (for example selecting only layer-1s) as that may limit the universe of comps.

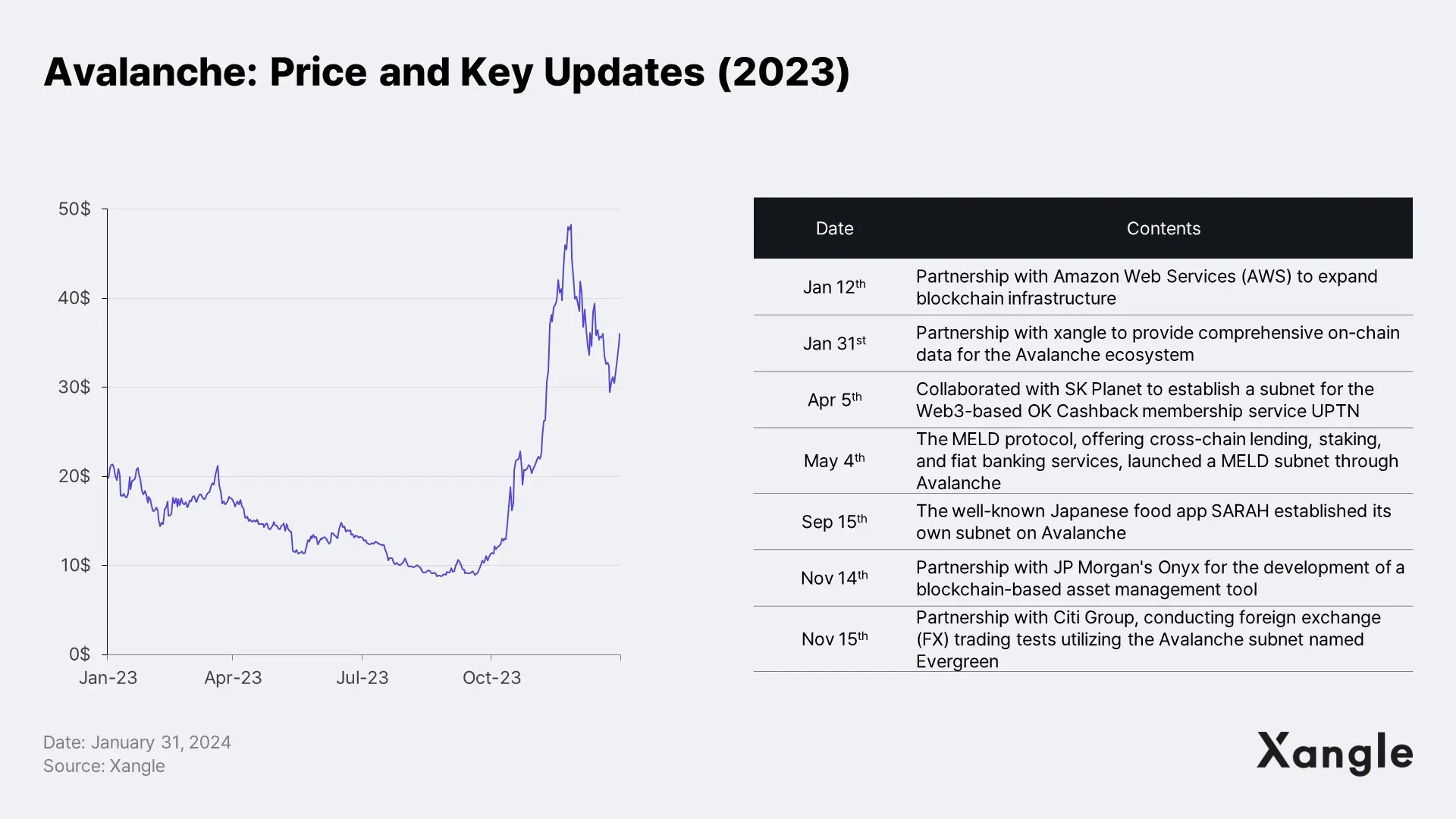

The comps above demonstrate that the range of potential FDMC/TVL multiples is often very wide. Additionally, any wide variation from the group median must be understood and explained. For example, Avalanche (AVAX) is trading at a comparatively high multiple (29.6x) after a major price rally that began towards the end of 2023. A high multiple should not necessarily discourage an investor from buying, but diligence should be done to determine whether it is justified. It’s likely that AVAX’s rally was boosted by announced partnerships with major institutions like JP Morgan and Citigroup, contributing to a market expectation of much higher TVL and usage in the future. But it will be up to the investor to determine if the high multiple is justified.

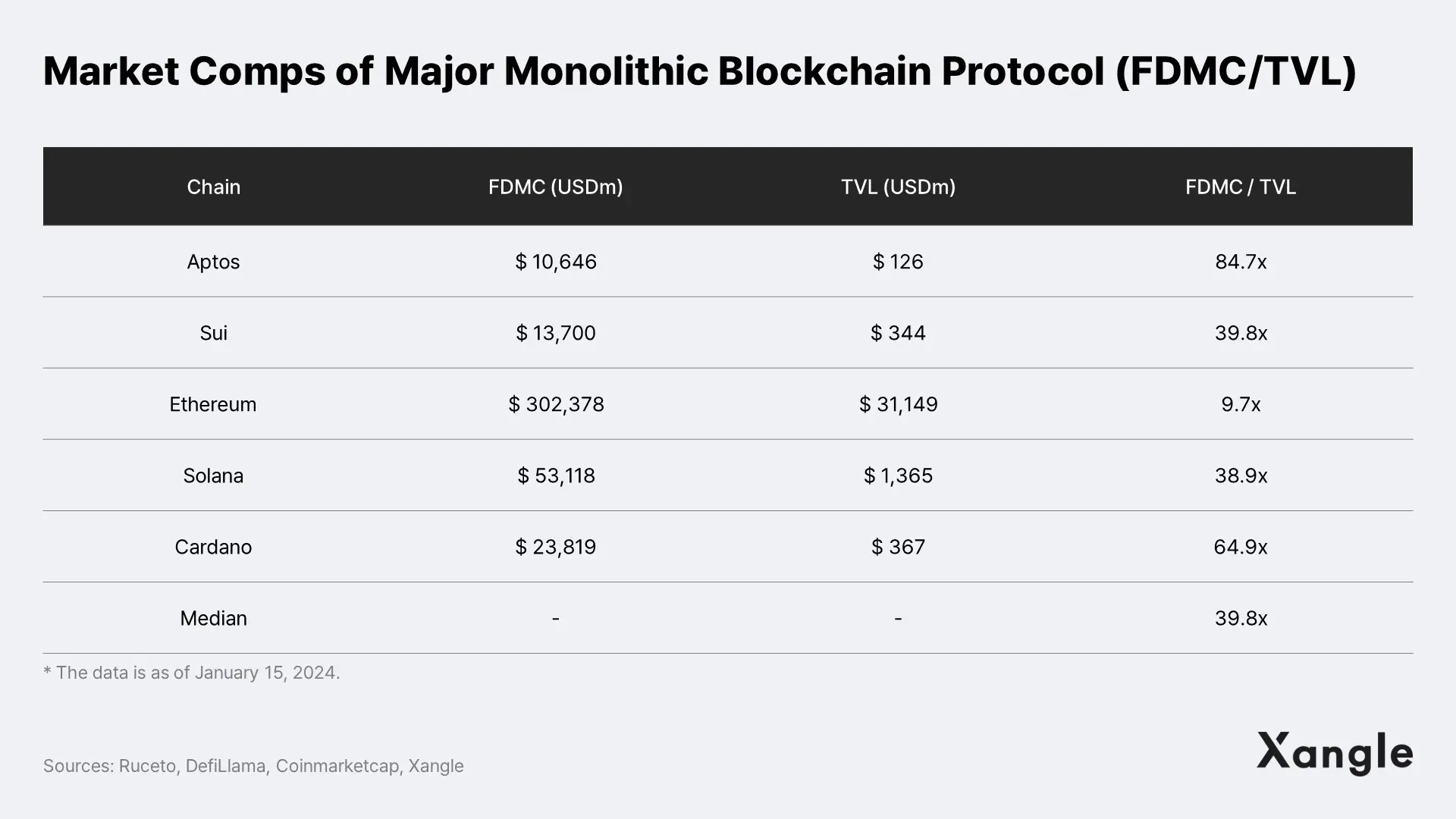

Aptos is a monolithic layer-1 blockchain with a strong focus on scalability, security, and reliability. We selected the below group of monolithic chains based on having at least $100 million of TVL. The results also show a very wide range of FDMC/TVL multiples.

Aptos has a FDMC/TVL of 84.7x, much higher than peer median of 39.8x. Although each of the above chains have shown substantial TVL growth in recent months, it will be difficult for a bigger chain such Ethereum to grow as much as the others on a percentage basis because its TVL is already relatively high.

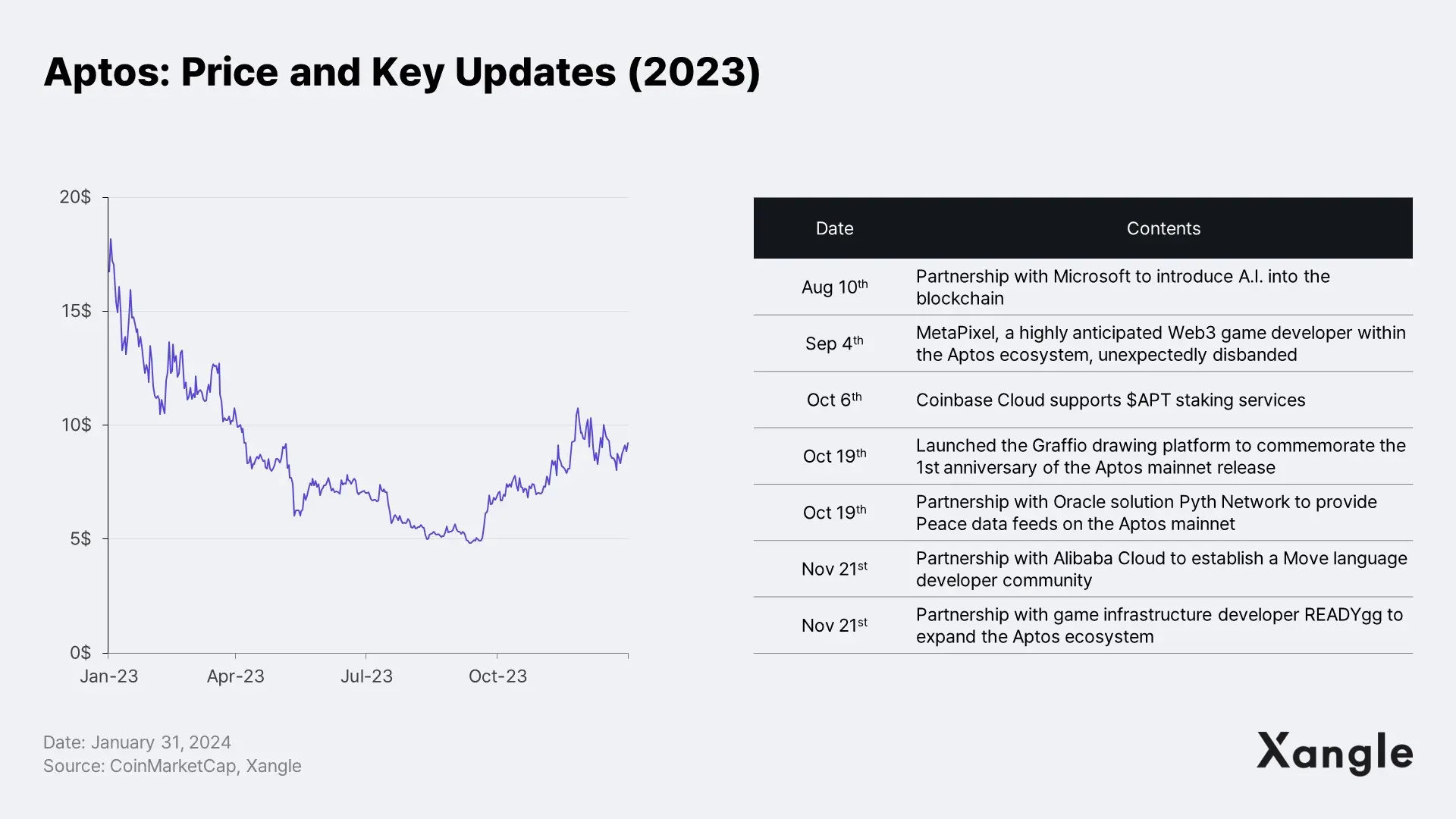

Aptos was developed by former Facebook employees and utilizes the Move, a unique programming language developed at Facebook specifically to scale blockchain projects. Graffio, an NFT art platform developed by Aptos Labs, was also well received by the market upon its launch. Aptos Foundation, Aptos Labs has also established partnerships with prominent companies such as Alibaba, Coinbase Pay, and Microsoft.

The comparatively high multiples from Aptos reflects the expectations that Aptos may become a major layer-1 player. If Aptos can one day grow to Ethereum’s size, the upside is massive despite the currently high multiple of 84.7x. Again, it is up to the investor to determine whether such upside is possible and worth the risk.

Our examples of using comps to measure potential value illustrates that token prices can vary significantly despite having similar functions. Since crypto is in its early stages, investors will have to accept that token values can be volatile and unpredictable.t conducting these exercises can still be extremely helpful to evaluate prospects of tokens in the long term.

Roadblocks to Making Sense of Token Price

Fundamental analysis has some roadblocks that are somewhat specific to crypto. For example, comparing web3 projects to web2 projects will often imply that the web3 project is overvalued.

Additionally, many blockchain projects that have raised capital are not generating any meaningful financial or user metrics. It is also difficult to see the path to profitability for many projects unless mass adoption occurs. Many existing traditional companies that can be used for benchmarks have long standing cash flows. It can be a bit of apples to oranges to compare the two. This makes benchmarking blockchain projects difficult, though one potential solution is adding an additional discount or adjustment after utilizing comps.

Additionally, supply is a significant issue when evaluating alt tokens. For example, projects are often subject to token unlocks, which can put heavy downward pressure on prices. Even institutional investors like venture capital firms pay attention to token unlock dates and how it may impact their investments. This can put the token on a downward spiral if there is not sufficient demand and liquidity. The effects of unlocks are difficult to predict and add uncertainty to the project. For example, SUI’s token unlock in November 2023 caused a 8.8% drop in a single day.

Conversely, “meme tokens” that have no utility or apparent intrinsic value can skyrocket due to pure hype and retail investors buying the coin. Since “meme tokens” have no actual use, it cannot be analyzed from a fundamental perspective. Though their prices often drop back down when users decide to realize short-term gains, some can remain elevated for extended periods of time.

Macro Trends

Industry trends and regulations are extremely important factors for token prices. Altcoins are very sensitive to the sentiment and macro environment. In the bear market during 2022, 72 of the top 100 tokens went down by 90% from their November 2021 highs.

Therefore, understanding macro trends and potential catalysts should be part of the analysis in evaluating altcoins. For example, if a bull market hits the crypto, it is likely that all altcoins will see a significant spike. Conversely, in a bear market it is likely that an altcoin project will see a significant drop even if it has strong fundamentals.

Below are some thoughts on what macro factors could trigger a bull and bear market.

Bull Market

With Bitcoin up 154% in 2023, some believe 2024 will mark the early stages of a bull market. Below are a few other factors to consider when thinking about catalysts for a long-term bull market in crypto:

-

Real use cases still exist – blockchain and crypto offers an extremely convenient way for micro payments and money transfers. For games, a layer-1 infrastructure is a natural platform for trading items and collaboration between games. For various protocols, being able to connect wallets offers a natural way for users to vote on issues that can be seen by all on the blockchain.

-

Adoption and innovation at the institutional level is still happening – Though retail activity has slowed, institutions are still active in the space. For example, the SEC has finally approved the Bitcoin ETF which included large institutions such as Blackrock and Franklin Templeton.

-

Regulatory and other headwinds are largely unrelated to the use case of blockchain – while waiting for governments to come up with clear rules for crypto has negatively impacted the crypto industry in some cases, none of these headwinds is due to blockchain technology not working.

Bear Market

Given the volatility in the crypto space, investors have to be prepared to lose everything that they invest. Below are a few factors to consider for the bear case:

-

Too many crypto projects - As of November 2023, there are over 10,000 cryptos in existence. It is unlikely that all of these projects have meaningful utility and can gain significant adoption. This could mean that many alt-tokens may not gain massive adoption or even cease to exist.

-

Substantial growth is baked into current valuations – Multiples for many alt-tokens are substantially higher than multiples in the stock market. This could imply that even if a project has strong growth prospects, it already has significant upside incorporated and needs to outperform those expectations for investors to realize significant gains. This could also imply that the alt-token prices need to decrease if it is to be comparable to the stock market.

-

Inconveniences of current technologies – Current blockchain projects still have inconveniences that act as roadblocks to mass adoption. Some examples include:

-

Creating a wallet and transferring tokens using wallet addresses can be a cumbersome process.

-

Buying and selling tokens across different chains is confusing for new users.

-

Gas fees are a hindrance to transactions and often require owning specific tokens.

As macroeconomics have historically greatly impacted the prices of alt tokens, it is necessary to have a view or at least understand potential catalysts that can influence token prices one way or another.

Conclusion

Crypto is extremely volatile and notoriously difficult to navigate for investors in both the short-term and long-term. However, for investors who believe in the technology are willing to hold for the long-term, it is important to analyze the viability of projects in a methodical way.

Analyzing factors like project viability, tokenomics, price, and macro trends can give investors a sense of what the success of a project hinges on. Even though these methods are not perfect and have their own shortcomings, they can provide a framework to evaluate these alt-tokens.

Looking for a great alt-token investment is a bit like looking for a needle in a haystack, but the methods described in this article can provide investors with a toolbox to do a thorough analysis.

*Disclaimer: The content presented is for informational purposes only and does not constitute financial, investment, tax, legal, or professional advice. Nothing contained in this report is a direct or indirect recommendation or suggestion to buy, sell, make, or hold any investment, loan, commodity, or security, or to undertake any investment or trading strategy with respect to any investment, loan, commodity, security, or any issuer. Ruceto does not guarantee the accuracy, completeness, sequence, or timeliness of any of this content. Please see our Terms of Service for more information.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.