The Three Innovations that Tokenized Securities will Bring

Table of Contents

I. All About Security Token Offerings (STOs)

1. What is an STO?

2. Examples of Tokenized Securities

II. Three Innovations that STOs will Bring

III. How will Korean Brokerage Firms Prepare for STOs?

1. Changes in Brokerage Firms' Fundraising Methods through STOs

2. Current Status of the Domestic Securities Industry

3. Hana Financial Investment - The First Securities Firm to Establish an STO Platform

IV. How Should an STO Platform be Built?

1. Step-by-Step Approach

2. Initial STO Platforms

3. Suggestions

V. Examining STO Cases in the United States

1. BCAP, the First Security Token in the U.S.

2. INX Token Issued in the Form of Stocks

VI. Conclusion

Appendix

I. All About Security Token Offerings (STOs)

1. What is an STO?

An STO, short for security token offering, refers to the issuance of digital securities utilizing distributed ledger technology in the capital market. To gain a deeper understanding of STOs, it's crucial to grasp the fundamentals of the three main components for STOs: S (Security - the nature of securities), T (Token - tokenized securities), and O (Offering - the process of issuance).

1) S for Security

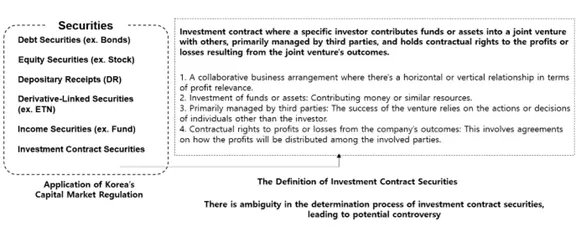

In the context of STOs, 'S' signifies securities as defined by capital market regulations. Securities encompass contracts governing rights and responsibilities concerning assets. Specifically, these include debt securities, like bonds entailing payment claims, equity securities involving investments in capital such as stocks, securities deposit certificates (e.g., DRs) where custodial institutions manage ownership and exercise shareholder rights on behalf of investors, derivative-linked securities combining derivative financial products (e.g., ELS), and income securities entitling profit reception when entrusted with management, like funds. Additionally, there's a growing focus on investment contract securities, which grant specific investors the right to invest funds or assets in collaborations and claim profits or losses based on outcomes.

According to Korea’s capital market laws, In STO, S represents primarily income securities or investment contract securities. However, typical projects mentioned in the crypto market related to security tokens are unrelated to Korea's security tokens. As the “s” in STO denotes securities according to Korean capital market laws, projects conducted by crypto companies not subject to capital market regulations cannot be recognized as STs under current Korean laws.

Figure 1. Type of Securities (Source: INF CryptoLab)

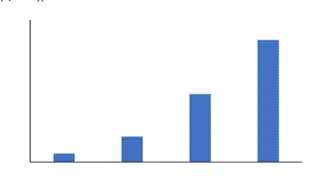

The regulatory direction of token securities overseas differs from that of Korea. In the United States, as early as April 2017, the first tokenized security (Blockchain Capital, BCAP) was issued, and tokenized security issuance is possible within regulatory boundaries through the existing Regulation D (private offering rules). Europe faces a similar situation where tokenized securities can be issued without a security filing for up to 8 million euros.

While overseas jurisdictions are adopting a direction to issue tokenized securities within existing laws, Korea is clearly identifying them as securities subject to the Capital Market Act, aiming to form the market through separate guidelines (such as Token Securities Guidelines, Fractional Investment Guidelines). Due to this difference, phenomena like ST issuance in the crypto industry, such as KKR's ST fund or MakerDAO's tokenization of U.S. Treasury bonds, and RWA (Real World Asset) tokenization, are not happening in Korea.

Figure 2. Number of STOs in the United States(Source: Cointelegraph, INF CryptoLab) / Figure 3. RWA Token Holders(Source: Dune(@j1002), Binance, INF CryptoLab)

2) T for Token

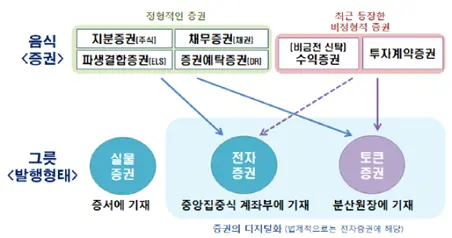

Securities can exist in various forms. Paper-based securities are physical securities, while those recorded on servers (centralized ledgers) are electronic securities. In September 2019, the Korean government introduced the electronic securities system, prohibiting physical securities of listed companies and enabling the issuance and distribution of securities like stocks and bonds through electronic securities.

On the other hand, token securities refer to securities recorded on a distributed ledger. While electronic securities are processed on centralized ledger servers, token securities imply processing on a distributed ledger within a blockchain network. According to the Financial Services Commission's analogy, physical securities, electronic securities, and token securities are like containers capable of holding various securities such as debt securities, equity securities, investment contract securities, and more.

The government aims to include relatively recent unstructured securities like income securities and investment contract securities within the token securities category. Of course, other securities can be included within token securities, and it's also possible to include income securities or investment contract securities within electronic securities.

Figure 4. Samsung Electronics' Physical Securities(Source: Korea Securities Depository, INF CryptoLab) / Figure 5. Implementation of the Electronic Securities System in Korea(Source: JoongAng, INF CryptoLab)

Figure 6. Issuance Forms for Different Types of Securities (Korea)(Source: Financial Services Commission, INF CryptoLab)

3) O for Offering

Offering refers to issuance. Issuance involves registering securities on an institution or blockchain network to enable their trading or sale. Though issuance methods vary, stocks, token securities, coins, among others, can all be issued.

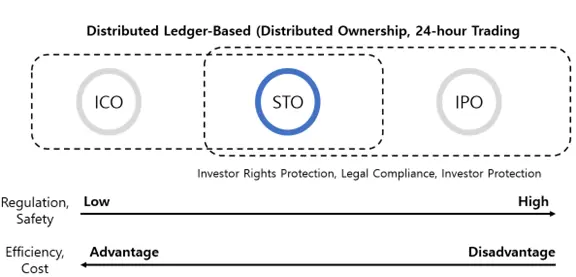

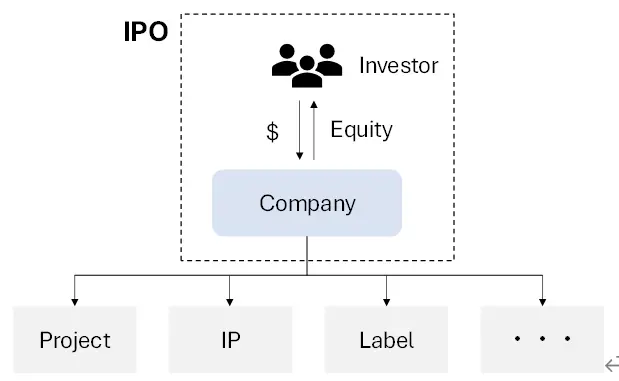

Firstly, an IPO (initial public offering) is when an unlisted company sells its stocks to the general public on the KOSPI or KOSDAQ and discloses financial information to get listed. It involves rigorous scrutiny by investors, ensures investor rights, and mandates information disclosure as per legal requirements.

An ICO (initial coin offering) is when a business issues blockchain-based coins and sells them to investors to raise funds. If this occurs on an exchange, it's called an IEO (initial exchange offering); if on a decentralized platform, it's an IDO (initial DEX offering). Simply creating tokens without an offering on any exchange is referred to as a TGE (token generation event). As it's based on a distributed ledger, it allows 24-hour trading, decentralized ownership, and a simplified issuance process, but compliance and regulatory standards may vary in comparison to IPOs.

STO refers to issuing tokenized securities. Because it's based on a distributed ledger, it allows decentralized ownership and can encompass newer forms of contracts compared to traditional securities. While it faces lower regulations compared to IPOs, it comes with a certain level of investor protection and information disclosure obligations.

In Korea, numerous fraudulent activities have occurred through ICOs. Therefore, the government is expected to bring various business ideas and investment opportunities previously issued as coins through ICOs into the framework of regulations, allowing them to be issued in the form of tokenized securities via STOs.

Figure 7. Comparing ICO, STO, IPO(Source: INF CryptoLab)

2. Examples of Tokenized Securities

The most significant advantage of issuing tokenized securities is its potential to enhance the efficiency of investor capital. The traditional IPO model involves investors investing in a company engaged in various businesses. For instance, if an investor buys shares of multinational entertainment company, Hybe Corporation (352820 KRX), it's akin to investing in all artists owned by Hybe Corporation. An investor may buy shares of Hybe Corporation because they want to invest in the growth potential of a newly debuted K-pop group like NewJeans. But in actuality, a higher proportion of his or her investment may go into Hive's subsidiaries like BTS or SEVENTEEN.

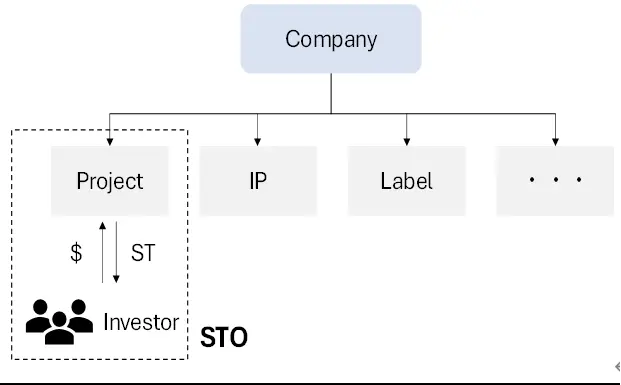

On the other hand, utilizing STOs enables investors to make more direct investments into specific areas of their choice, such as allotting 30% of their investment into NewJeans' future revenue over the next five years or specific album sales profits. Moreover, rather than diluting the company's overall stake for funding, the company can create tokenized securities representing specific rights for a particular project to raise capital.

Reevaluating the capital efficiency of tokenized securities could invigorate the financial market. Currently, there exists a 20-80% discount rate for subsidiaries in the Korean financial market. Even if a listed parent company holds a subsidiary worth 10 billion KRW (approximately 7.5 million USD), the subsidiary's value for investors is assessed between 2 billion to 8 billion KRW (approximately 1.5 to 6 million USD). The more complex the governance structure, the higher the discount rate tends to be. Tokenized securities can help alleviate such discount rates.

Figure 8. Raising Funds Through IPOs(Source: INF CryptoLab) / Figure 9. Raising Funds Through STOs(Source: INF CryptoLab)

Another advantage of tokenized securities issuance is the ability to list and liquidate various assets (such as parking lots, intellectual property, etc.) that previously had no conventional way of being listed. If diverse assets in the world are liquidated, prices could form based on trading among market participants, potentially stimulating our capital market. This could also prompt illiquid assets that have long remained dormant to emerge in the market. For instance, if a parking lot in front of a famous tourist spot is tokenized and its value becomes known worldwide, more parking lot owners might want to tokenize their properties.

Furthermore, there are distinctive differences from various existing investment methods. It's worth noting that while Korea grants permission for a few companies in the 'Financial Regulatory Sandbox' for fractional investments, with the establishment of a tokenized securities platform, every company might be able to issue various tokenized securities through brokerage firms.

|

Figure 10. Comparison of STs, Real Estate Fractional Investment, REITs, and Real Estate Funds |

||||

|

Category |

Real Estate Tokenized Securities |

Real Estate Fractional Investment |

REITs (Real Estate Investment Trust) |

Real Estate Funds |

|

Investment Target |

Single real estate investment |

Single real estate investment |

Real estate indirect investment vehicle |

Real estate-related tangible assets |

|

Investor Returns |

Dividend income, price appreciation, capital gains |

Dividend income, price appreciation, capital gains |

Dividend income, price appreciation, capital gains |

Dividend income, conditional capital gains |

|

Early Redemption |

Possible |

Possible |

Possible |

Impossible |

|

Related Ministries/ Departments (Korea) |

Financial Services Commission |

Financial Services Commission |

Ministry of Land, Infrastructure and Transport |

Financial Services Commission |

|

Basic Laws |

Electronic Securities Act, Capital Markets Act |

Trust Act, Capital Markets Act |

Real Estate Investment Company Act |

Capital Markets Act |

|

Tax |

n.a |

Dividend Income Tax 15.4% Capital Gains Tax 15.4% |

Dividend Income Tax 15.4% Capital Gains Tax 15.4% Acquisition Tax 4.6% |

Dividend Income Tax 15.4% Capital Gains Tax 15.4% Acquisition Tax 4.6% |

|

Technology |

DLT |

Server (Partial DLT) |

Server |

Server |

|

Source: Eugene Securities, INF CryptoLab |

||||

II. Three Innovations that STOs will Bring

INF CryptoLab expects three innovations to be brought to the society by STOs.

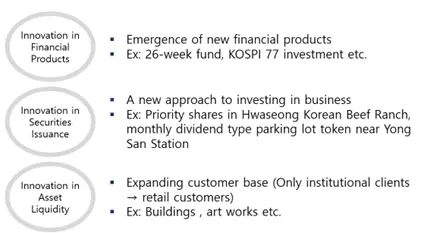

First is the innovation in financial products. Through STOs, newly packaged financial products will emerge. For instance, there will be products like a 26-week fund for investing in savings schemes for 26 weeks or an investment product diversified across the top 77 KOSPI companies based on the lucky number 7. Financial products like savings accounts existed for the last 50 years. However, in 2018, the 26-week savings product launched by an internet bank, Kakao Bank, achieved massive success with 20 million cumulative accounts opened within just five years. STO enables such innovation on a mass scale. STO-based financial products, tailored to consumer needs, are expected to make a totally new impact on the market.

Secondly, there will be an innovation in securities issuance. Previously, investing in businesses through securities meant investing in the stakes of those companies. However, regular shareholders found it difficult to exercise voting rights and to expect sufficient dividends. With STOs, a new method will emerge, allowing direct investment in businesses. Examples include investing in preferred shares of a Hwaseong Korean cow ranch, or perhaps receiving monthly dividends from parking revenue rights. Assets no one could have imagined would be able to be securitized, will be securitized through STO.

Thirdly, there will be innovation in asset tokenization. As token securities are based on distributed ledgers, heavy assets that were previously challenging to handle or luxury items difficult for the middle class to invest in can now be divided, encouraging fractional investment. This will open new investment opportunities to the products for retail investors that were previously accessible only to institutional investors.

Figure 11. Innovation of Products(Source: INF CryptoLab)

There is a possibility that the perception of “retail investors” might totally change. Trading token securities could potentially improve the negative perception surrounding tokens in the web2 industry. Additionally, the concept of quantities like five shares of Tesla (TSLA US) or ten shares of Samsung Electronics (005930 KRX) might transform into an amount-based concept such as three million won worth of Tesla (TSLA US) or one million won worth of Samsung Electronics (005930 KRX). Finally, investment destinations recognized by company names or tickers (stock codes) could be perceived as ideas such as the leading electric vehicle company or semiconductor-related stocks.

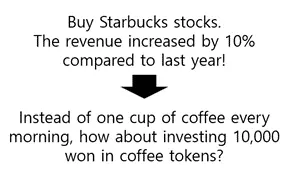

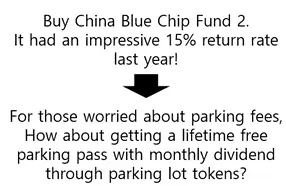

With these changes, even marketing language around stocks might shift from the traditional "Hey everyone, buy Starbucks stocks. Sales increased by 10% compared to last year, and the P/E ratio is 30x, making it affordable." to "Well, instead of a daily Starbucks coffee, invest 10,000 won in coffee tokens." Similarly, funds might transition from "Hey, buy China Blue-Chip Fund 2. Last year's yield was 15%." to "You know what? For those worried about parking fees, invest in a monthly dividend-based token for Yongsan Station parking and enjoy free parking for life."

Figure 12. Marketing Trend Change in Stocks(Source: INF CryptoLab) / Figure 13. Marketing Trend Change in Funds(Source: INF CryptoLab)

III. How will Korean Brokerage Firms Prepare for the STO Era?

1. Changes in Brokerage Firms' Fundraising Methods through STOs

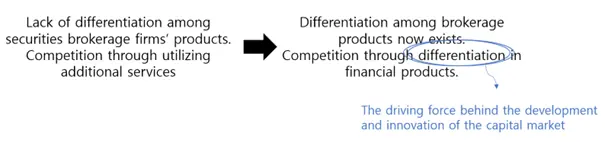

Brokerage firms are competing by selling the same financial products as stocks and funds. From a customer's perspective, buying Samsung Electronics (005930 KRX) stock from one securities firm or another doesn't make much of a difference. As a result, brokerage firms have been attracting customers by spending on marketing, reducing fees, or improving user experience.

However, this landscape could totally change with the evolution of the STO market. If a specific securities firm identifies and issues tokenized securities with competitive advantages and innovative ideas early on, customers will be able to subscribe to those products only through that firm's platform.

When companies build their value based on the inherent value they provide, they can achieve a higher multiple and realize their true corporate worth. Present-day brokerage firms are akin to movie theaters. They all screen the same movies, prompting them to spend on enhancing customer satisfaction by installing better seats or offering discounts. This leads to a scenario where they become low-growth, undervalued companies with a meager P/E ratio of just 10x. On the other hand, Netflix competes through content. It offers exclusive content not available elsewhere, allowing it to achieve a P/E ratio of over 40x.

If brokerage firms start providing exclusive financial products through STOs that aren't available elsewhere, the current competitive landscape will undergo a significant shift. A new competition centered around products will emerge, serving as a driving force for the development and innovation in the financial market.

Figure 14. Competition will begin on the basis of the "product" at the heart of brokerage firms(Source: INF CryptoLab)

Movie theaters without exclusive content (products) spend money to satisfy customers, and that expenditure serves a one-time role and then disappears. In contrast, OTT platforms with exclusive content (products) invest in intangible assets to satisfy customers. This investment transforms into intangible assets that continuously accumulate on the platform. The accumulated intangible assets become competitive advantages and act as a company's foundation.

In summary, with the emergence of STOs, fundraising methods will change. This implies that brokerage firms which succeed in effectively converting costs (marketing expenses) into intangible assets (investment funds) through leveraging this change could become the new leaders of the next securities market.

Figure 15. Cinema Advertisement (Emphasizing the services)(Source: INF CryptoLab) / Figure 16. Netflix Advertisement (Exclusive content oriented)(Source: Netflix)

Furthermore, in addition to securing a corporate network based on an IPO and generating greater profits through ECM (Equity Capital Markets) and DCM (Debt Capital Markets), there exists the possibility, through STO operations, of acquiring new corporate customers previously inaccessible, thereby generating additional revenue.

2. Current Status of the Domestic Securities Industry (Korea) for STOs

Discussions surrounding STOs in Korea commenced in 2018. However, owing to the sluggish pace of legislative action in passing associated laws, the government aims to establish distinct guidelines to foster the market. The Financial Services Commission is targeting substantial institutional implementation starting from 2024, refining specific requirements within legislations such as the Electronic Securities Act and the Capital Markets Act.

Concurrently, the Korea Exchange, Korea Securities Depository, and brokerage firms are intensifying their preparations, viewing STOs as a novel business prospect. KB Securities initiated preparations even prior to the guidelines' announcement, engaging in consultations or partnerships with blockchain companies for Proof of Concept (PoC), followed by Korea Investment & Securities, Hana Securities, Shinhan Securities, and others. INF Consulting has solidified its status as a financial and blockchain consulting firm, managing consulting projects for all brokerage firms. Technology firms like SK C&C and Lambda256 have conducted pertinent PoCs.

All brokerage firms are launching STO-related alliances to secure promising products as quickly as possible. However, disparities exist among these firms, notable disparities in whether they are associated with banks or not. Brokerage firms under banking groups aim to dominate the market through their platforms, collaborating with banks or card affiliates to capture new investor demand. Conversely, non-banking brokerage firms are exploring strategies for customer differentiation, aiming to introduce entirely fresh investment experiences via real estate, art, crowdfunding products, and more.

3. Hana Financial Investment - The First Securities Firm to Establish an STO Platform

In November 2023, Hana Financial Investment made INF Consulting, an ITCEN subsidiary, the primary contractor tasked with constructing an STO platform, initiating a substantial phase of platform development. The reported contract value for this primary contractor reaches into the hundreds of billions of won (approximately tens of millions of USD). This selection, following preliminary consultations conducted in July for the STO platform, represents a comprehensive investment in the STO business. The estimated timeframe for platform construction spans approximately one year, aiming to cover the entire spectrum of token securities, from issuance to circulation.

Hana Financial Investment aims to capitalize on synergies within the Hana Financial Group via the STO platform. Despite Hana Bank's leading position in the banking industry, Hana Financial Investment had displayed relatively weaker standings concerning securities firm rankings and customer base compared to its rivals. However, the introduction of token securities as a new asset could lead to significant and noteworthy changes.

As mentioned before, the construction and launch of the STO platform involves expenses in the hundreds of billions of won (approximately tens of millions of USD). The significance lies in being the first securities firm willing to incur such substantial costs while placing confidence in token securities. It is anticipated that subsequent to Hana Financial Investment, Mirae Asset Securities and KB Securities may consider STO platform construction in the future.

Figure 17. Hana Securities, Selecting INF Consulting as Primary Contractor for building an STO Platform(Source: INF CryptoLab)

IV. How Should an STO Platform be Built?

1. Step-by-Step Approach

Given the ongoing absence of finalized regulations and laws pertaining to STOs in Korea, an incremental strategy becomes essential. To achieve a unique business identity through product variation, it's vital to give precedence to crafting an issuance platform specifically for exclusive off-market products. Moreover, establishing linkages with current systems is critical to avoid duplicative investments. Concurrently, in pursuit of long-term objectives, there's a need to contemplate building foundational structures by interconnecting nodes with other brokerage firms and considering the incorporation of Layer 2 technologies (like subnets), contingent upon the progress and validation of public chain technology.

Figure 18. Competition will Begin Based on the Core of Financial Institutions 'Products.'(Source: INF, FNF)

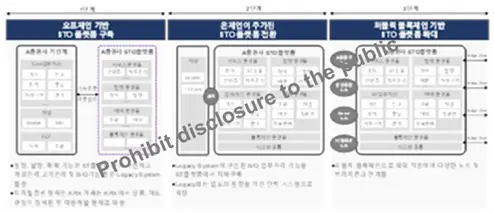

2. Initial STO Platforms

There's a growing need for standardized models in the STO platform to streamline system establishment. Despite varying IT systems across brokerage firms, they face similar hurdles and policy decisions when building STO platforms. These challenges include identifying primary customer service channels, deciding on ledger creation location (main system or STO platform), structuring accounts, managing product information (integration or separate), and determining processing locations for orders and evaluations, among other considerations. We've classified the essential system configurations for phase one as outlined below.

Figure 19. Stage 1: To-Be STO System Structure(Source: INF, FNF)

Specifically, certain domains that are anticipated to necessitate integration based on the utilization of existing legacy systems encompass customer data, contract particulars, comprehensive account setups (account initiation), cash flow management (deposits and withdrawals), financial bookkeeping, and transactional payments. Integration of these segments with the ST system using methods like API is strongly advised. Moreover, functions like evaluation (ST ledger) and payment execution are imperative for cash management activities, alongside accounting procedures involving the general ledger and interfaces with financial accounting systems. In the initial phase, it's pivotal to link the STO platform to legacy systems while ensuring they aren't overly strained, facilitating rapid adaptation to the market within a brief timeframe.

3. Suggestions from INF CryptoLab

To effectively construct an STO platform, understanding three fundamental elements and charting a long-term course is imperative.

First and foremost is grasping the objectives of the STO platform. These objectives should transcend mere short-term profit or immediate service impact; they should serve as a cornerstone in acquiring clientele and venturing into the burgeoning digital asset market.

Secondly, it's pivotal to delineate a clear target system aligned with governmental regulations. Developing an MVP (minimum viable product) while encompassing functionalities necessary for self-issuance, agency, on-exchange, off-exchange transactions, and seamless integration with external systems (such as KRX, KSD, etc.) should be a gradual progression following governmental guidelines.

Thirdly, agile validation of services becomes essential. Rather than the linear waterfall method—proceeding from problem definition to 'To-Be' process establishment to construction—embracing the agile methodology, which involves simultaneous establishment of business direction, defining 'To-Be' processes, and system construction, is crucial for effectively adapting to the evolving STO market.

Long-term strategizing shouldn't solely focus on STO strategies; it’s crucial to chart a course that encompasses entry into the crypto market by leveraging STOs as well. The crypto market offers diverse business prospects like cryptocurrencies, NFTs, DeFi, CBDCs, etc. Companies stand to benefit from reduced customer acquisition costs, global reach, heightened intangible asset value, and talent acquisition via crypto ventures. This approach lays the groundwork for future growth momentum, innovative business models, and increased corporate value.

Figure 20. Future of Security Tokens(Source: INF CryptoLab)

V. Examining STO Cases in the United States

1. BCAP, the First Security Token in the U.S.

STO issuance in the United States predates Korea by a significant margin. The inaugural STO case in the US was the BCAP token launched by Blockchain Capital in 2017. Utilizing the ERC-20 format on the Ethereum network, the BCAP token conferred ownership and entitlements linked to Blockchain Capital's third fund, the Blockchain Capital III Digital Liquid Venture Fund.

Using the BCAP token, the fund conducts investments with the raised funds, distributing investment gains as an Evergreen Fund token upon capital recovery. Twenty-five percent of the fund's profits, alongside a 3.5% management fee, are directed to Blockchain Capital. Of the remaining investment profits, 50% are earmarked for fund reinvestment, while the other 50% is allocated to token holders based on decisions made by the fund manager.

Figure 21. Blockchain Capital BCAP Token(Source: Securitize) / Figure 22. BCAP Token Sale(Source: Cointelegrah)

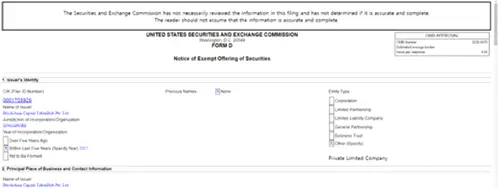

Figure 23. BCAP Token SEC Registration(Source: SEC.gov)

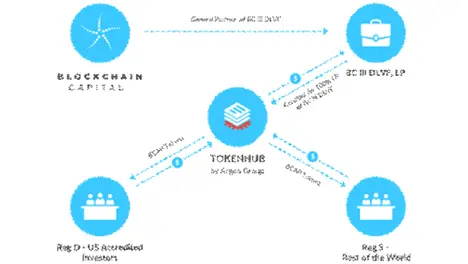

Collaborating with the Argon Group, Blockchain Capital gathered tens of millions of dollars via crowdfunding on Token Hub. The fund swiftly gained immense traction, closing a mere 6 hours after its announcement due to high demand.

Token Hub, responsible for BCAP token sales and distribution, obtained LP (Limited Partner) shares in Blockchain Capital's fund by pooling funds from diverse investors. Following this, it allocated tokens to investors according to this ownership arrangement.

Figure 24. Blockchain Capital and Token Hub Token Securities Sale Structure(Source: Cryptoninjas.net)

BCAP underwent the US securities declaration process and was marketed through Regulation D's Rule 506(c), catering exclusively to accredited US investors. Simultaneously, it was also marketed through Regulation S, streamlining sales without additional SEC registration steps for non-US investors.

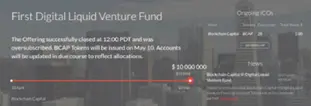

A sum of $10 million tokens was sold at $1 per token, accumulating a total of $10 million. Upon SEC registration document submission, 745 investors were confirmed as participants. While the exact ratio of accredited US investors remains undisclosed, it’s inferred that most of the investments came from non-US investors via Regulation S.

Figure 25. BCAP Token Raised Amount and Investors(Source: SEC.gov)

Reviewing the disclosure information of Blockchain Capital's BCAP token in Q3 2023 unveils the diverse portfolio held within the firm's third fund, encompassing assets like Circle, OpenSea, Ripple, among others. The Net Asset Value (NAV) reflects a multiple of 14.1 times the initial fundraising amount, mirroring the BCAP token's NAV at the point of sale, also reaching 14.1 times the sale price, totaling $14.1.

Figure 26. BCAP Token Status (2023)(Source: SEC.gov)

BCAP, as the inaugural securities token case in the US, faces notable criticism. Substantial concerns include legal uncertainties, unclear profit distributions, and the rights of token holders. The creation of an Evergreen Fund as a securities token brings complexity due to the absence of an expiry date, granting Blockchain Capital the authority to alter legal terms, posing several investor rights challenges.

Despite the initial challenges of tokenized securities, the BCAP token holds immense historical significance as it pioneered US securities tokens and demonstrated potential functionality. Presently, newly released securities tokens are undergoing distribution and issuance in an advanced format, addressing the deficiencies witnessed in BCAP.

2. INX Token

The INX token stands out as a prime example of tokenized securities granting shareholders potential rights to dividends and profits rather than adopting a venture fund structure.

Functioning as an SEC-registered platform for tokenized securities (ST) trading and IPOs, INX Token Securities Platform introduced the INX token. This security token is structured to reward token holders with 40% of the company's profits once it attains profitability.

In a distinct process from Korea's handling of securities and token securities, INX successfully raised 85 million USD from international investors through the official SEC registration procedure employing Form F-1. At present, INX remains actively engaged in supporting diverse companies and projects in their IPO endeavors through multifaceted initiatives. Additionally, it operates INXONE, a broker-registered exchange for token securities.

Figure 27. INX Token(Source: INX) / Figure 28. INX Token SEC Registration(Source: SEC.gov)

There's additional recent information concerning the Republic Note, issued by Republic, an investment firm registered with the SEC. This note offers entitlements to funds, shares, and dividends. Functioning as a tokenized security, it disperses rights related to 623 companies, 765 assets, and dividends linked to Republic's Evergreen Fund. The sale of Republic Note to non-US investors will kick off on December 6th via the INX platform.

Tokenized securities have extended their presence beyond businesses and funds, finding application in diverse realms like real estate, NFTs, high-value artworks, solar panels, and other sectors.

VI. Conclusion

Tokenized securities are still in their infancy and are on the cusp of further evolution. However, to achieve genuine mainstream adoption of blockchain, these technologies need to shift their perception from merely being tools catering to a niche group of cryptocurrency enthusiasts to being acknowledged as technologies tailored for a broader audience, spanning diverse financial sectors, Web2 companies, and the public.

At present, several services are emerging that aim to integrate real-world assets (RWAs) and a wide array of financial services with blockchain technology. For instance, initiatives like Chainlink's CCIP seek to onboard numerous existing global assets onto the blockchain by leveraging SWIFT payment networks, while MakerDAO is creating and executing systems for distributing US bond yields. Additionally, there's a range of RWA solution providers and multiple Central Bank Digital Currency (CBDC) initiatives at the national level, all showcasing this ongoing trend.

STOs stand as innovative instruments poised to introduce novel advancements in the financial market by connecting blockchain with financial institutions and offering the public experiences related to tokens. Coupled with the three innovations outlined in this article, the proactive response from brokerage firms instills hope for the growth and development of the STO market in South Korea.

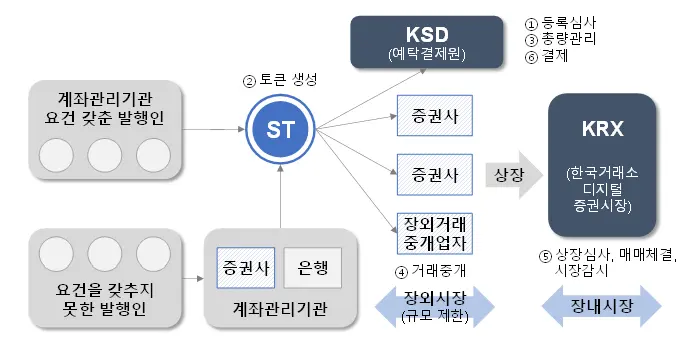

Appendix

- Issuance of tokenized securities in Korea is conducted by the issuer or an account management institution (securities firm, bank, etc.), and after assessment and management by KSD, distribution occurs on the KRX (Korea Exchange).

- Issuance Process: ① KSD (Korea Securities Depository) registration assessment → ② Token creation and transfer by the issuer or account management institution → ③ Custody management by KSD

- Distribution: ④ Over-the-counter market (brokerage by brokerage firms/OTC brokers) / ⑤ On-exchange market KRX (Korea Exchange) → ⑥ Settlement through KSD

Figure 29. Distinct Mechanism for Issuing and Dispensing Tokenized Securities in Korea(Source: Financial Services Commission, INF CryptoLab)

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article is provided by CrossAngle’s third-party research partners. CrossAngle does not have any editorial control over this article and does not warrant the accuracy and timeliness of the information contained herein. This article may contain links to third-party websites, over which CrossAngle disclaims any control or responsibility.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Tokenized Alternatives](https://resource.xangle.io/files/content/4CC9F01B59B75EE060E1CED81479662A_1784708136454.webp)

![[Xangle RWA Series] Tokenized Bonds](https://resource.xangle.io/files/content/B0441837E0B8CB1A38F95639330AAAE7_1783499602150.webp)

![[Xangle RWA Series] Custody/KMS](https://resource.xangle.io/files/content/7CC0614D2A6D1FF81A2EA31A208674CA_1782892820809.webp)

![[Xangle RWA Series] Tokenized Stocks](https://resource.xangle.io/files/content/CFCAFEC4A99C7A00EDE70BA3198A8D7B_1782366959101.webp)