Decoding the growth patterns and future directions of stablecoins

Authored by Jeff Ren, Paige Xu, Veronica Zhao and Bingcheng Zhong from OKX Ventures. Edited by Kelvin Lam, CFA

This article represents the personal views of the authors and isn’t intended to provide any investment advice or solicitation to buy, sell or hold digital assets. For full report, please go to https://www.okx.com/learn/decoding-the-growth-patterns-and-future-directions-of-stablecoins

I. Summary

From the bull market of 2021 to the bear market of 2023, the cryptocurrency market has undergone significant changes. The total market value decreased from 3 trillion to 1 trillion US dollars, but the market value of stablecoins only decreased by 30%.*

From the bull market of 2021 to the bear market of 2023, the cryptocurrency market has undergone significant changes. The total market value decreased from 3 trillion to 1 trillion US dollars, but the market value of stablecoins only decreased by 30%.*

As of December 2023, CoinGecko data shows that the stablecoin market’s total capitalization is about $130 billion. Tether (USDT) dominates with a 70% share, USDC holds around 20%, and the rest is spread across various other stablecoins. In the current context of high government bond yields (>5%), Tether reported $1.48 billion of net profit in Q1 2023 and quarterly returns from Cash and Cash Equivalent investments were once again at close to US $ 1 billion in Q3 2023, highlighting the market’s profitability.

Besides Tether and USDC, we have seen the emergence of many on-chain stablecoins, reflecting the DeFi field’s demand for different types of stablecoins, both centralized and permissionless. The innovations of these emerging stablecoins include diversified collateral, collateral liquidation mechanisms, and profit-sharing mechanisms that give back to the community. Their success depends on maintaining liquidity and attracting major DeFi protocols.

Although new on-chain stablecoin protocols continue to emerge, over 90% of the market value is still concentrated on centralized stablecoins.* Some startups are trying to use payout yields generated from US government bonds to challenge the dominance of Tether and Circle, but I believe the long-term development of centralized stablecoins needs more cooperation with traditional financial institutions and regulatory authorities. This includes working with compliant custodians, sufficient capital injections, and obtaining relevant licenses.

To create the next “super stablecoin” akin to USDC and USDT, we believe that at least the following four key conditions need to be met to fully leverage the advantages of centralized and decentralized stablecoins:

- USD-based stablecoins: The US dollar has a wide global acceptance, and its supporting assets have broad applicability.

- Global regulatory recognition and licenses: Super stablecoins need to be globally positioned from the start and obtain recognition from US regulatory agencies and global licenses.

- Innovative financial attributes: Super stablecoins should have innovative financial attributes, such as profit-sharing mechanisms, to build community support and sustainable growth.

- Seamless integration into the DeFi ecosystem: Super stablecoins need to become an integral part of DeFi Lego to achieve widespread adoption within the DeFi landscape.

- The stablecoin market plays a vital role in the cryptocurrency ecosystem and is expected to continue to develop and expand. To successfully create the next super stablecoin, we believe it may be necessary to meet a series of DeFi gameplay advantages and establish cooperative relationships.

- Source: DefiLlama, OKX

II. Classification of stablecoins

Decentralized stablecoins

To address the issues of centralized stablecoins, decentralized stablecoins have introduced innovative solutions. These new stablecoins are built on blockchain protocols, making them more transparent. For example, Curve’s crvUSD, AAVE’s GHO, and Dopex’s dpxUSDSD are all on-chain protocol-based stablecoins, reducing the centralized element. Decentralized stablecoins can be divided into two major categories:

Overcollateralized stablecoins:

- Collateralized stablecoins are the most common type of decentralized stablecoins. Their asset backing typically comes from other cryptocurrencies, such as Ethereum or Bitcoin, to maintain their relative value stability. For example, MakerDAO’s DAI is backed by Ethereum as collateral. The latest trend is to shift collateral from traditional centralized stablecoins and major traditional digital currencies to a broader range of digital currencies or multi-layer nesting, to increase liquidity and provide more application scenarios. For instance, the largest collateral in Curve’s crvUSD is stETH and Ethena’s stablecoin is also based on Ethereum and the liquid staking tokens (LSTs).

- Potential advantages: collateralized stablecoins may be able to transcend their role as mere payment tools and evolve into more comprehensive digital asset management tools, empowering users with a wide array of choices and flexibility.

- Potential disadvantages: a main issue with collateralized stablecoins is the risk of reduced asset utilization rates caused by excessive collateral, especially when backed by volatile assets like Ethereum. This volatility introduces the possibility of forced liquidation, presenting a significant challenge.

Algorithmic stablecoins:

- Algorithmic stablecoins are one of the most decentralized types of stablecoins. The idea is to use market demand and supply to maintain their fixed prices without actual collateral support. These stablecoins use algorithms and smart contracts to automatically manage supply to maintain price stability. For example, Ampleforth is an algorithm-based stablecoin designed to keep its price close to 1 US dollar. It aims to adopt an elastic supply mechanism, automatically adjusting the supply based on market demand to balance the price. When the price is above 1 dollar, the supply increases, and when the price is below 1 dollar, the supply decreases.

- Additionally, there are some hybrid algorithmic stablecoins that seek to combine algorithms and fiat reserves. For instance, Frax is an algorithm-based stablecoin aimed at maintaining a price close to 1 US dollar. It adopts a mixed stablecoin mechanism, partly supported by fiat reserves and partly managed by algorithms to maintain price stability.

- Potential advantages: algorithmic stablecoins aim to create decentralization. Compared to other solutions, we believe stablecoins may have an advantage in scalability. Algorithm-based stablecoins use transparent and verifiable code, which can make them attractive.

- Potential disadvantages: algorithmic stablecoins, like all digital assets, are susceptible to market sensititivity. When market demand for algorithmic stablecoins drops, their prices can fall below the target value. Additionally, the operation of algorithmic stablecoins relies on smart contracts and community consensus, which may pose governance risks such as code defects, hacking attacks, human manipulation, or conflicts of interest.

Centralized stablecoins

Centralized stablecoins usually have fiat currency as collateral, held in off-chain bank accounts, serving as reserves for on-chain tokens. They address the value anchoring issue of virtual assets, linking digital assets to physical assets (such as the US dollar or gold), stabilizing their value. At the same time, they resolve the access issues of virtual assets under regulatory environments, providing users with more reliable digital asset storage and trading methods. Centralized stablecoins still hold over 90% of the market share.*

Currently, besides the US dollar and British pound, many centralized stablecoin projects have US Treasury bonds as collateral. US Treasury bonds are usually held in custody by institutions, providing redeemability, while tokenization increases the liquidity of underlying financial assets. Additionally, they provide interaction opportunities for DeFi components, such as leverage trading and lending. This allows projects to obtain US dollars from crypto users at zero cost to purchase US Treasury bonds and directly benefit from bond yields.

However, centralized stablecoins also come with certain potential limitations. One of these is limited yield opportunities. Since centralized stablecoins depend on reserves held by trusted entities to ensure stability and value, users might not have access to earning native yield. This limitation arises from centralized control and management of collateral.

*Source: DeFiLlama

III. Recent rise of popularity of the stablecoin market

- Rising US bond yields exceeding DeFi protocol yields

The surge in government bond yields has contributed to significantly higher returns in TradFi compared to DeFi. Currently, the total market value of stablecoins has reached $130 billion, making them the 16th largest holder of US Treasury bonds, with an annual yield of 5% or higher.* However, in the DeFi ecosystem, platforms like Aave and Compound allow users to lend stablecoins to others for interest, with loan yields around 3%, while decentralized exchange platforms like Uniswap offer around 2% returns through Automated Market Makers (AMM)**. This situation reflects that the fall in bond prices and rise in yields may be driving some investors to seek higher returns in traditional financial markets, potentially leading to lower yields in DeFi.

*Source: DefiLlama, The Block **Source: DefiLlama

2. Emergence of stablecoin projects with profit-sharing mechanisms

Most profits from centralized stablecoins currently flow to their issuers and related investors. For example, USDC shares part of its profits with its investors like Coinbase. Coinbase then allows users storing USDC on the platform to earn rewards, thereby attracting more users. However, there’s been some innovation in the market that revenue shares extend beyond investors and ecosystem participants.

3. TradFi companies are gradually entering the stablecoin market

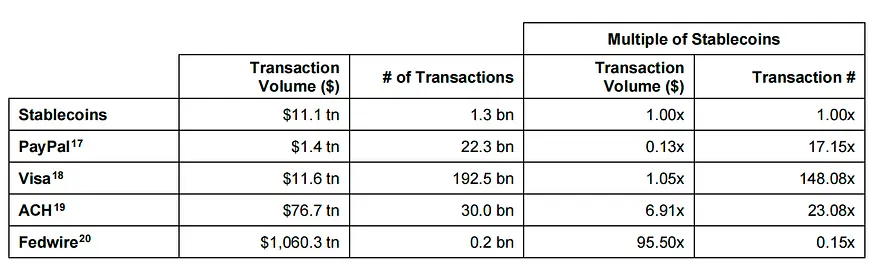

According to a research report by Brevan Howard, in 2022, the on-chain settlement volume of stablecoins reached $11.1 trillion, surpassing PayPal’s $1.4 trillion and comparable to Visa’s $11.6 trillion. This highlights the significant potential of stablecoins in the payment sector, especially in providing efficient on-chain settlement systems. Moreover, in developing countries with underdeveloped payment and banking systems, the application of stablecoins is particularly crucial, meeting the demand for efficient, low-cost payment solutions. Therefore, stablecoins are playing an increasingly important role in the global financial ecosystem, particularly in promoting financial inclusivity and economic growth.

Source: The Relentless Rise of Stablecoins, Brevan Howard Digital 2023

Several companies, including PayPal and Visa, are venturing into the stablecoin market. PayPal has partnered with Paxos to launch PYUSD, a stablecoin backed by US dollar deposits, short-term government bonds, and cash equivalents. PYUSD can be exchanged within the PayPal app and is interoperable with Venmo and other cryptocurrencies. It aims to provide PayPal’s 431 million users with an entry point into the Web3 world. Currently, PYUSD has a circulation of about $114.46 million, ranking fourteenth and representing 0.1% of the total stablecoin market. Its introduction by PayPal could significantly influence widespread adoption of cryptocurrencies, bridging traditional financial convenience with digital currency innovation.*

*Source: DefiLlama

IV. Impact of ecosystem participants on stablecoin projects

1. Exchanges

USDC accounted for nearly half of Coinbase’s revenue in the first half of 2023, totaling around $399 million.

Source: Coinbase

A. Collaboration between exchanges and stablecoins yields revenue growth

- In the first half of 2023, part of Coinbase’s revenue came from a profit-sharing agreement with Circle. By the end of Q3 2023, USDC balances on Coinbase reached $2.5 billion, up from $1.8 billion at the end of Q2. Circle and Coinbase manage USDC jointly through the Centre Consortium and distribute income based on USDC holdings. In August 2023, Coinbase Ventures acquired a minority stake in Circle, strengthening their partnership.

Source: Coinbase

- Additionally, Circle has announced that it is expanding its Web2 business by using USDC for cross-border settlements. In September 2023, Visa expanded using Circle’s USDC stablecoin settlement to the Solana blockchain to increase cross-border payment speed, becoming one of the first major companies to use Solana for settlements and boosting Solana token prices in the short term.

- The market shows USDT is primarily used in derivative trading on centralized exchanges, while USDC is more prevalent in Web3 DApps. Choosing a trustworthy stablecoin issuer is essential for exchanges. Traditional institutions like BNY Mellon have high credibility, whereas major crypto-native issuers like Tether and Circle are in a relatively stronger financial position. Factors like third-party custodial services, auditing firms, and licensing are also important. Following BUSD and TUSD examples, using multiple custodians can reduce counterparty risk.

B. The potential of stablecoin payments drives increased traffic for exchanges and issuers

- Stablecoin payments, particularly for cross-border transactions, hold significant potential, driving traffic to exchanges and issuers. Issuers can integrate stablecoins into payment processes through collaborations with Web2 payment companies. For example, as of Q4 2023, PayPal has 433 million active retail accounts and 35 million active merchant accounts globally. PayPal allows PYUSD settlements, with PYUSD being purchasable, holdable, and sendable by merchants on PayPal, Venmo, and Xoom. Venmo has about 80 million users in the US, contributing to PayPal’s 320 million global users.* Currently, PYUSD is only supported by PayPal’s US accounts due to licensing constraints, but it has growth potential given PayPal’s extensive user base. However, PYUSD faces risks from its issuer, Paxos, which is the same issuer that stopped minting BUSD Token after NYDFS Guidance in Feb 2023.**

*Source: PayPal

**Source: Bloomberg

2. Layer 1 and 2s

A. Impact of BUSD on BSC’s Total Value Locked (TVL)

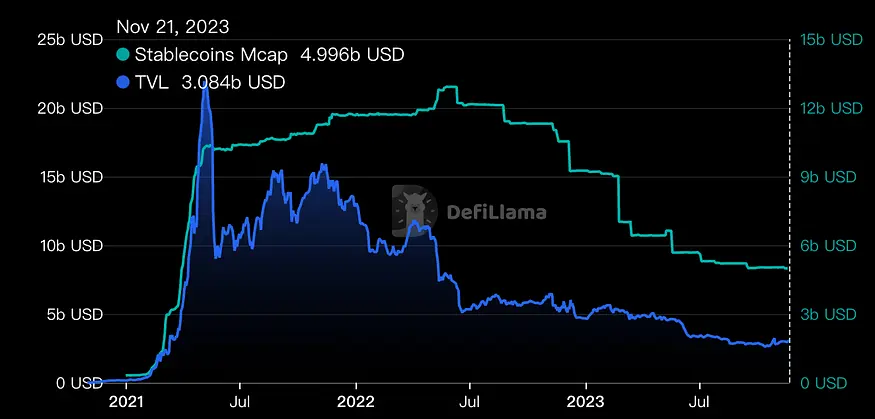

- The decline in BUSD’s market value, which supports six public blockchains and is mainly active on Ethereum and BSC, has led to its market cap dropping to $2 billion. This decrease has significantly impacted the Binance Smart Chain (BSC) ecosystem, as the reduction in BUSD’s value contributed to a 44% fall in stablecoin value and a 66% decrease in Total Value Locked (TVL) in BSC’s protocols, highlighting the critical role of stablecoins in blockchain ecosystem health.

*Source: DefiLlama, 2023 November

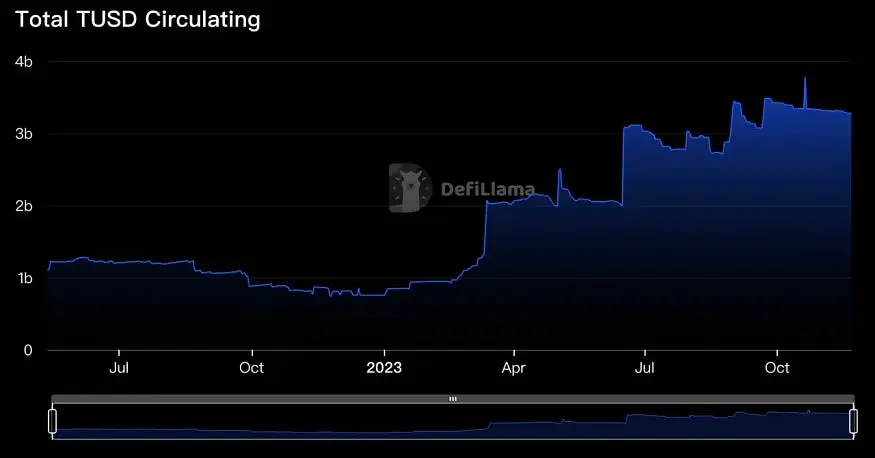

B. Impact of TUSD on the Tron ecosystem

- After a series of maneuvers post-February 2023, the market value of TrueUSD (TUSD) increased from around $1 billion to between $2 and $3 billion.

- February 2023: TUSD implemented the Chainlink Proof of Reserves mechanism to ensure the security of its minting process and further guarantee transparency and reliability.

- March 2023: TUSD hired The Network Firm LLP, an independent U.S. accounting firm specializing in the blockchain industry, to provide real-time verification of its U.S. dollar reserve coverage.

- April 2023: TUSD introduced native support on the BNB Chain.

- There is also a positive correlation between the market capitalization of stablecoins on a public blockchain and the Total Value Locked (TVL) on that blockchain, as illustrated in the chart below for the TRON blockchain.

Source: DefiLlama, 2023 November

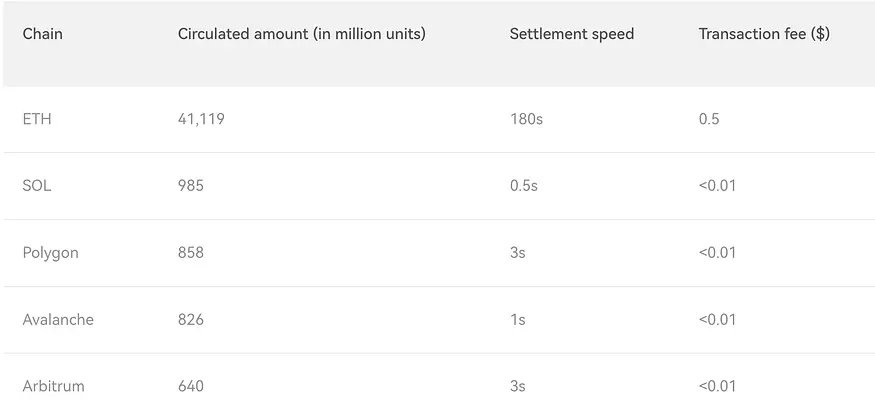

C. USDC on different blockchains

USDC has been issued on over 15 public blockchains, with its highest Total Value Locked (TVL) rankings on Ethereum, Solana, and Polygon. USDC is actively seeking to expand its application scenarios, primarily focusing on payments, especially cross-border payments.

Table: distribution of USDC’s TVL across different blockchains

Source: State of the USDC Economy, Circle Annual Report, 2023

- USDC and Solana: Visa partnered with Circle to use USDC on the Solana blockchain for on-chain settlements, aiming for faster, cheaper cross-border payments due to Solana’s high throughput and low transaction costs.

- USDC and Polygon: In October 2023, Circle supported native USDC on the Polygon PoS mainnet. Major Polygon protocols like AAVE, Compound, Curve, QuickSwap, and Uniswap announced development support for native USDC, with plans for cross-chain interoperability by the end of 2023.

- USDC and Sei Network: In November 2023, Circle invested in Sei Network to support native USDC on-chain, noting Sei’s performance superiority with a transaction finality time of 0.25 seconds, surpassing Sui, Solana, and Aptos.

D. Dapp-Issued Stablecoins

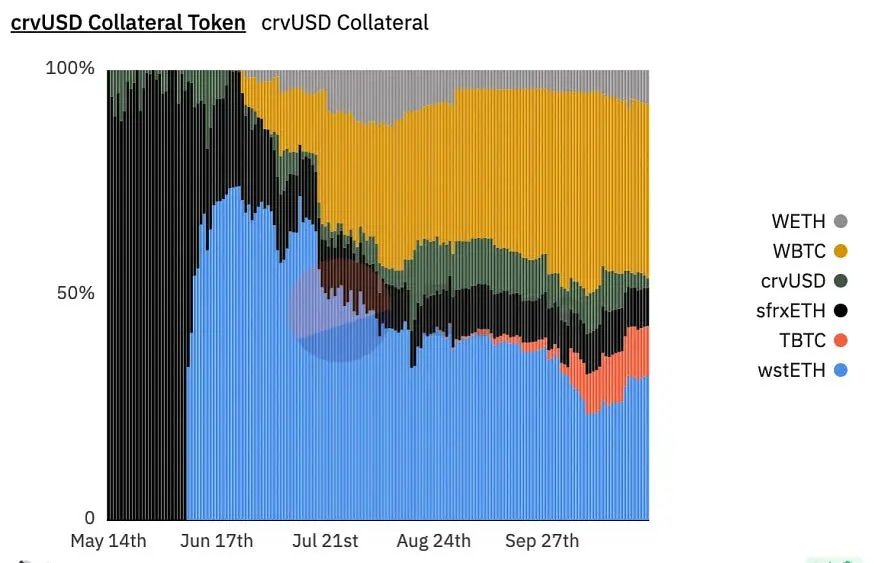

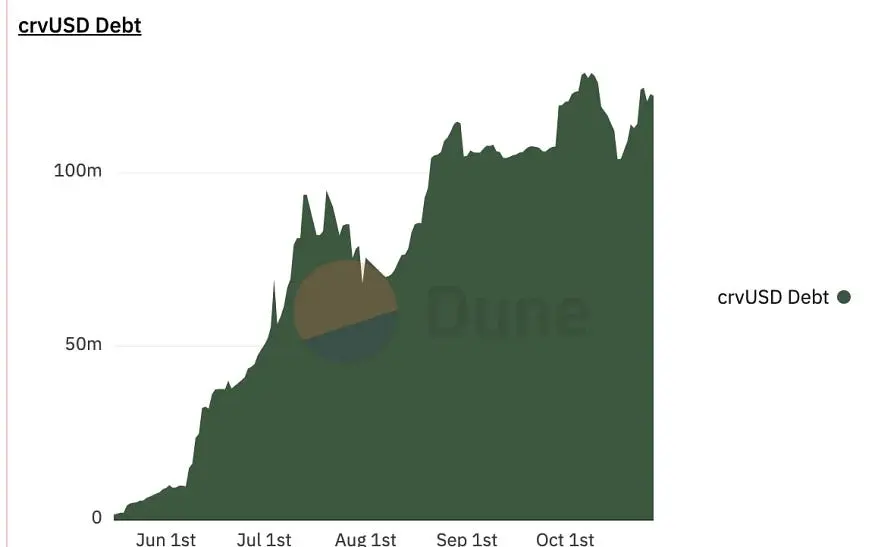

The impact of stablecoins issued by top DeFi protocols like MakerDAO, Curve and Aave on public blockchains is significant. Here we take examples of uprising stablecoin crvUSD and GHO for reference.

Curve’s crvUSD, launched in May 2023, allows users to mint stablecoins using various crypto assets as collateral, with WBTC notably boosting its growth. The protocol’s addition of collateral like Lido’s wstETH and BitGo’s WBTC quickly gained market dominance, showcasing Curve’s influence in the DeFi space. These developments not only enhance Curve’s DeFi presence but also affect asset liquidity and stablecoin use on public blockchains. This trend highlights the innovation and importance of leading DeFi protocols in the crypto ecosystem and suggests their evolving role could bring new dynamics and challenges to blockchain usage and market stability.

Source: Dune Analytics, 2023 November

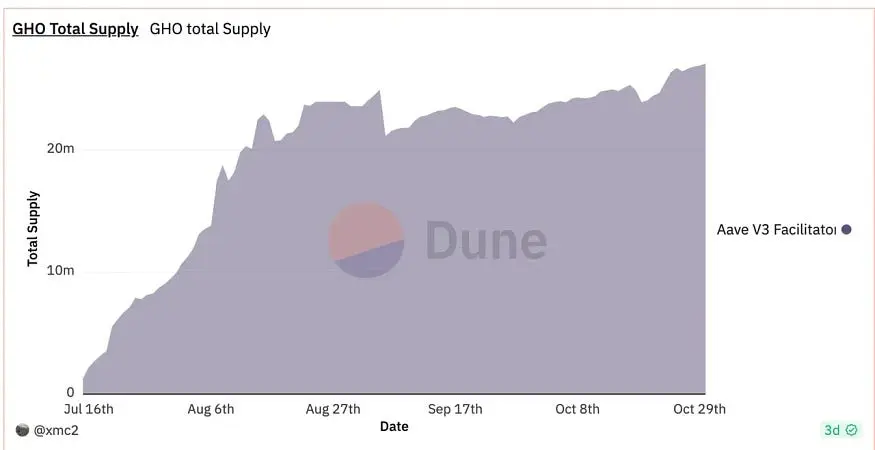

As the largest lending protocol*, Aave, with a Total Value Locked (TVL) of $5.64 billion, launched GHO, an over-collateralized stablecoin. Therefore, all tokens supported by the Aave v3 protocol can serve as collateral for GHO, and this collateral continues to generate revenue within the lending protocol. Since its launch in July, the accumulated TVL for GHO has surpassed $20 million.

*Source: DefiLlama

Source: Dune Analytics, 2023 November

3. Stablecoin issuers

Currently, the majority of stablecoins supply is backed by highly liquid short-term assets like US dollars and Treasury bills, with a very low risk of default. The primary risk for centralized stablecoin issuers is ensuring smooth channels for users to purchase and exit; the ecosystem could collapse if the issuer fails to redeem during user exits.

Finding trustworthy stablecoin issuers is crucial for ecosystem participants. Analyzing the cryptocurrency ecosystem and traditional financial market systems, crypto-native custodians, traditional financial custodians, banks, and asset management platforms hold absolute credibility. For instance, institutions like Fireblocks, BitGo, BNY Mellon, and BlackRock are more suitable as stablecoin issuers.

The management of ETF assets can serve as a model, wherein multiple parties ensure the openness and transparency of fund storage and liquidity through a “monitoring sharing agreement,” enhancing credibility. Additionally, third-party on-chain audits and on-chain data tracking platforms like OKLink can jointly supervise fund safety.

4. Custody service providers

The brief de-pegging incident of USDC in 2023 due to SVP’s bankruptcy highlights the importance of balance sheet risk management. Some stablecoin projects, like PYUSD, entrust asset management to Paxos, a custodian service provider holding a New York BitLicense and regulated by the New York State Department of Financial Services (NYDFS), mitigating certain risks by handing over assets to a third-party compliant custodian.

Additionally, Circle has partnered with BlackRock, one of the world’s largest asset management companies, to create the Circle Reserve Fund, registered with and regulated by the SEC. The primary goal is to manage USDC’s reserves, with about 94% of the reserves currently held by this institution.

5. On-chain infrastructure

M^ZERO Labs offers an example of blockchain infrastructure. M^ZERO Labs is dedicated to establishing a decentralized infrastructure that allows institutional participants to allocate and manage assets on the blockchain. The platform is open-source and it connects financial institutions with other decentralized applications, facilitating on-chain value transfer and collaboration among participants.

Source: M^ZERO Labs

V. Conclusion

As the cryptocurrency landscape evolved from its 2021 peak to the bearish tides of 2023, stablecoins have uniquely underscored their resilience and critical role within the broader crypto ecosystem. While the market contracted from $3 trillion to $1 trillion, the relative stability in the market value of stablecoins underscored their potential as safe harbors amid the volatile nature of cryptocurrencies. Dominant stablecoins, like USDT and USDC, have solidified their status in the market.

The swift growth and diversification of the stablecoin sector is a testament to the continuous innovation within the realm of cryptocurrencies. The market’s evolution, spanning from over-collateralized to algorithmic stablecoins, demonstrates a dynamic response to diverse financial demands. The ingenuity inherent in these burgeoning stablecoins, including their varied collateral types, liquidation processes, and revenue-sharing mechanisms, has not only bolstered the DeFi ecosystem’s resilience but has also established a laboratory for potential market evolution.

In the foreseeable future, stablecoins are poised to extend their influence within the crypto ecosystem significantly. With the progression of technology, we anticipate witnessing an expansion of stablecoin applications in financial services, particularly in areas like cross-border payments and settlements. Realizing this potential calls for the industry to intensify efforts in enhancing transparency, security, and integration with existing financial infrastructures.

To conclude, stablecoins transcend being merely a subset of the crypto market; they are pivotal in bridging traditional finance with the digital currency domain. Their journey is one of continuous evolution, necessitating relentless innovation, adaptation, and collaboration to navigate the dynamic tides of market and regulatory changes. For market participants, grasping and adapting to these shifts is crucial for securing long-term success in this ever-evolving landscape.

Original Link

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article is provided by CrossAngle’s third-party research partners. CrossAngle does not have any editorial control over this article and does not warrant the accuracy and timeliness of the information contained herein. This article may contain links to third-party websites, over which CrossAngle disclaims any control or responsibility.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.