Stablecoins, Unlocking the Future of Web3.0

Written by Miseon Lee, Dongin Kim, Minsun Cho

※ This content was originally posted on an external platform. For additional notes, please refer to the end of the main text.

Table of Contents

Executive Summary

Companies venturing into the crypto payment market

Key Variables to Accelerate Mass Adoption

1. People receiving salaries in cryptocurrencies

2. Crypto assets in mobile apps (Grab, PayPal)

3. Japan opens a 1,000 trillion-yen payment market

The Impact of Stablecoin Expansion on Existing Industries

1. Impact on the banking industry

2. Impact on the credit card industry

3. Impact on crypto exchanges (CEX vs. DEX)

4. Impact on the on-chain market (Liquidity, RWAs)

Executive Summary

Mobile wallets make it easy for users to access and perform wallet-to-wallet transactions

Companies with a global reach, such as Grab and PayPal, have begun offering in-app crypto mobile wallet services. Instead of using complicated private keys, they use PIN codes to make it simpler for users to manage their wallets and access their assets. This change is expected to boost the desire for people to store their assets independently rather than relying on third parties. As a result, the dominance of existing exchanges may decrease, as it becomes easier for users to transfer assets between wallets and buy/sell major cryptocurrencies within the app.

The increased issuance of stablecoins aims to enhance liquidity in on-chain markets.

Amendments to Japan's Financial Services Law will allow stablecoin issuance starting in June. Progmat, initially a project under Mitsubishi Trust Bank, became an independent company in October. It has formed a consortium with 214 Japanese companies to create a specialized tokenization platform. This move is expected to lead to more financial institutions in Japan and other places issuing stablecoins. This, in turn, will boost liquidity in on-chain markets, increase the market value of stablecoins, and generate more interest in Staking-RWAs.

A new financial and economic order may emerge as industry boundaries weaken

Deel, an HR platform, reports that in the latter half of 2022, 4% of total salaries were paid in cryptocurrency. Most of the recipients are from emerging economies that lack traditional banking systems. Cryptocurrency salaries can be sent directly to a personal wallet without the need for a traditional bank account. This shift could lead to the establishment of a new financial and economic system, especially as the digitally native generation, representing 26% of the world's population, engages in economic activities. To stay competitive and foster growth, banks and card companies should explore the potential of blockchain technology.

Companies venturing into the crypto payment market

Crypto economy in our daily lives - Initiating the journey toward widespread adoption

The crypto market has faced significant challenges, including the Tera-Luna debacle, FTX exchange bankruptcy in 2022, and the Silvergate and SVB bank failures in 2023. Global cryptoassets' total market capitalization, as reported by Coingecko, peaked at $2.8 trillion in November 2021 but has since dropped to $1.1 trillion, nearly two years later(as of October 17,2023). However, despite these price fluctuations, there have been significant recent developments in the blockchain industry that could signify a pivotal moment. We have covered these developments in this report, and they are likely to be remembered as catalysts for the widespread adoption of the crypto economy in the future.

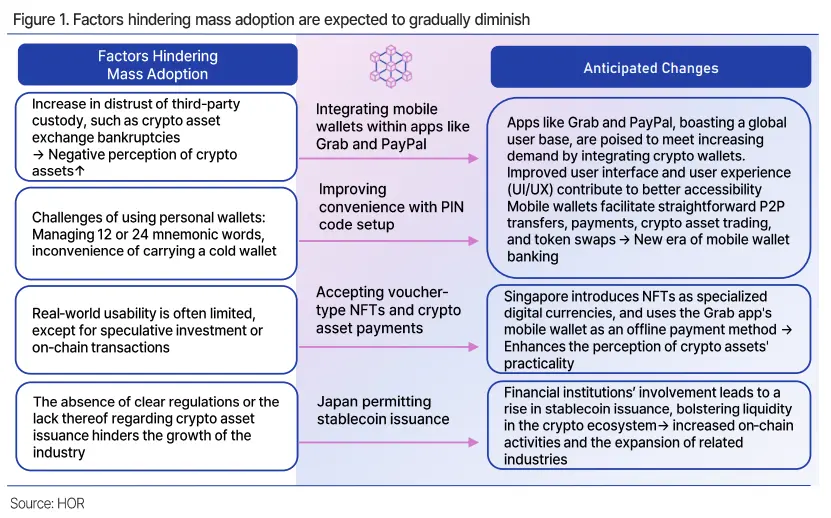

Meanwhile, let's explore why widespread adoption hasn't happened yet. The bankruptcy of major cryptocurrency exchanges has made people less trusting of third-party custody. Moreover, it has been difficult for individuals to handle their own assets because it's not easy to store the secret phrases (mnemonics) and carrying around cold wallets has been inconvenient. Also, cryptocurrencies have had limited use in the real world beyond trading, which has held back widespread adoption.

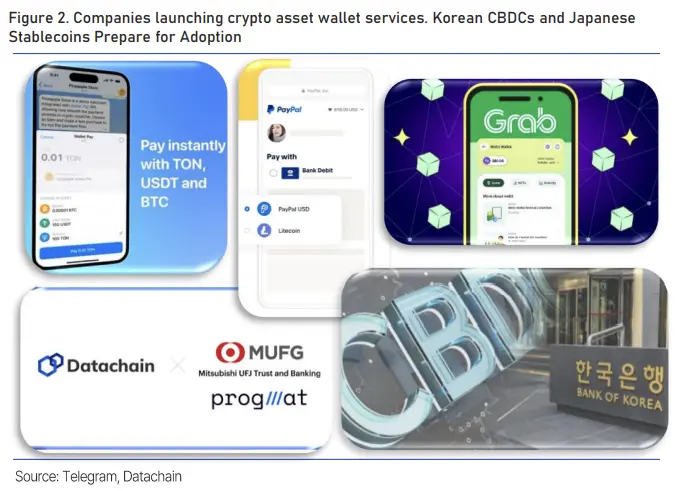

However, some recent developments are changing the game. Companies like Grab and PayPal, which have users worldwide, have integrated crypto wallets into their apps. This makes managing crypto assets much more convenient and accessible. Additionally, Japan's Mitsubishi UFG plans to start issuing stablecoins early next year. These changes are expected to make it easier for people to get into crypto, removing the obstacles that were holding back mass adoption and fostering genuine growth in the crypto ecosystem.

Exploring why big countries and global corporations are venturing into the crypto payments market

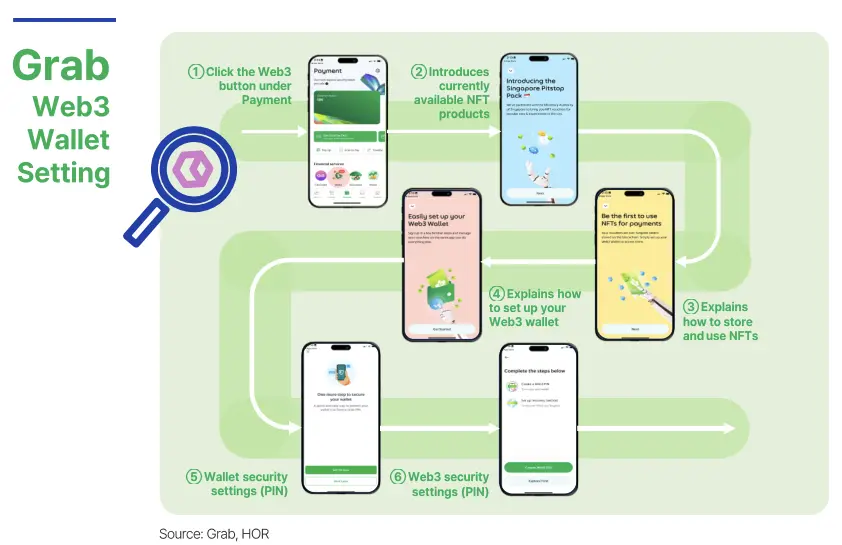

On September 14, Grab, an app with approximately 180 million active users in Southeast Asia, introduced a Web3 wallet service for storing and sending NFTs. They partnered with Circle, the issuer of the USDC stablecoin, to power this wallet. The service was initially launched as a pilot project in Singapore, and it's worth noting that the Monetary Authority of Singapore has joined this initiative. As a first step towards Central Bank Digital Currency (CBDC) development, the Monetary Authority of Singapore created Purpose Bound money (PBM), which allows you to store and use NFTs in the form of PBM within the Grab app. This move will provide Singaporeans with the opportunity to naturally use NFTs as a means of payment.

Until now, most people have seen crypto assets like stablecoins as new investments primarily for trading. But imagine if your everyday apps could be used to order food or pay for a taxi by crypto assets. What if you could send money instantly using just a mobile crypto wallet, without needing a traditional bank account? How will banks fit into this new picture? If cryptoassets can serve as both online and real-world money, they could reshape finance into something entirely new, blurring the lines between technology, finance, payments, and more.

Global companies and governments are racing to gain an edge in this evolving landscape. Grab, Telegram, and PayPal have introduced user-friendly web3 wallet services for mobile, making it easier for people to access crypto assets. In June, Japan changed its Financial Services and Settlement Law to allow qualified financial institutions to issue stablecoins. The Bank of Korea is also getting in on the action, announcing a plan for “CBDC utilization testing” in collaboration with the Financial Services Commissionand the Financial Supervisory Service on October 4.

Key Variables to Accelerate Mass Adoption

We believe the following three variables will accelerate mass adoption, some of which have already begun to change or are on the verge of changing.

Key Drivers for Mass Adoption

- More people are getting paid with crypto assets

- Easy storage and management via mobile app wallets (Seamless Access)

- Increased issuance of stablecoins by governments and large financial institutions

1. People receiving salaries in cryptocurrencies

Deel, a global HR platform that offers services like hiring and payroll, recently published a report revealing an intriguing trend in the global job market. They analyzed over 100,000 job contracts from more than 150 countries worldwide and found that about 5% of the total monthly payroll processed on the Deel platform in the first half of 2022 was paid in cryptocurrency. This is 3 percentage points higher than in the second half of 2021. Importantly, these changes in pay aren't influenced by cryptocurrency price fluctuations; it's due to the increase in the value of cryptocurrency.

The Rise of the Digital Native Generation and Cryptocurrencies

Gig Workers Digital Natives

In the second half of 2022, this share dropped slightly to 4%, which seems like a small drop considering the extreme disruption that occurred during this period, including the FTX bankruptcy. When it comes to cryptocurrency salaries, the most common options were Bitcoin (47%), USDC (29%), Ethereum (14%), and Solana (8%).

Will more workers receive their pay in cryptocurrency in the future? To answer this question, let's look at recent developments in the global job market. The term "Gig" has been around since the 1920s in the United States, used to describe performances by groups that traveled from one jazz bar to another.

McKinsey Consulting defines a gig as "temporary work traded in a digital marketplace." Gig workers are individuals seeking greater flexibility, independence, and work-life balance. They differ from "contingent workers" in that they voluntarily opt for contract work, often in specialized fields like design, IT, development, and translation. They want to set their own schedules, take time off as needed, and prefer working as self-employed entrepreneurs or freelancers, allowing them to be their own bosses without being tied down.

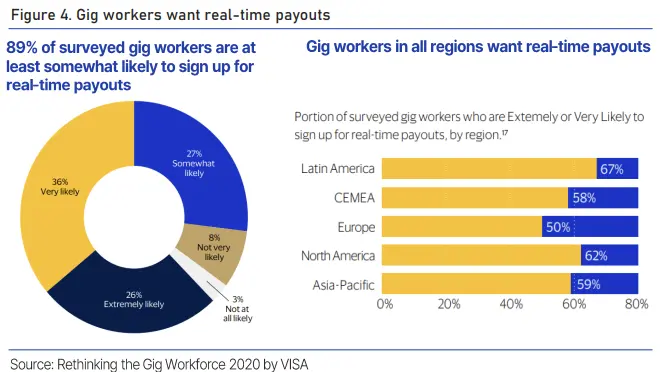

The gig worker population is growing rapidly, in line with the rise of the Millennials and Gen Z, who value autonomy and work flexibility, and are reshaping the job market. Notably, nearly 50% of gig workers express their willingness to receive part or all of their salary in cryptocurrency. This willingness is particularly high among freelance writers, designers, and developers (62%), followed by drivers (56%) and grocery shoppers (55%), according to a Berkshire Hathaway study in August 2022. One of the reasons they prefer crypto pay is the convenience of real-time transfers.

Gen Z prefers mobile payments over credit cards

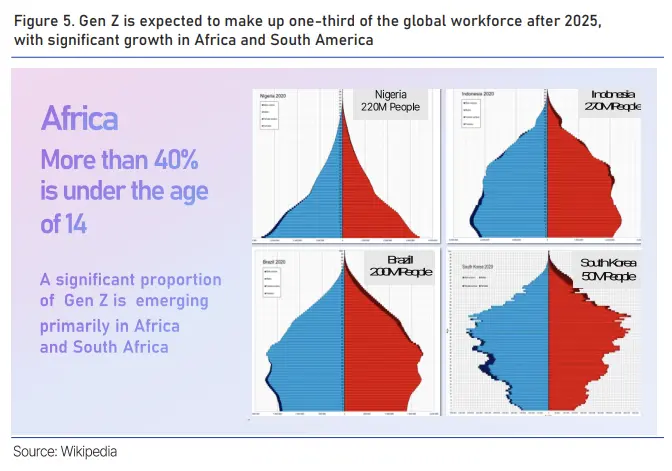

Gen Z, representing 26% of the world's population, is reshaping the economic landscape

The rise of gig workers open to crypto pay aligns with the tech-savvy Millenials and Gen Z. This generation, especially those born from the late 1990s to the early 2020s, marks the first generation of Digital Natives. They've grown up with computers and mobile devices from an early age, making them more naturally inclined than previous generations to engage in economic activities through mobile technology.

Our analysis reveals that, unlike prior generations that relied on credit cards and banks, Gen Z shows a preference for mobile payment apps and is open to alternative payment methods like cryptocurrency. Currently in their early to mid-20s, Gen Z is expected to constitute 27% of the global workforce by 2025. What if they stop favoring credit cards, use mobile payments exclusively, receive a significant part of their salaries in cryptocurrency, and conduct most economic activities through mobile wallets without the need for traditional bank payroll accounts? This presents a critical turning point for traditional financial institutions to prepare for these shifts.

Digital Natives, shaping the new economic landscape

Gen Z comprises a staggering 2 billion individuals, making up 26% of the world's population. While the global growth of Gen Z may not be as apparent in countries like Japan, with its aging population and low birth rate, the demographics of countries such as Nigeria, with a population of 220 million, resemble the structure of South Korea in the 1960s. Brazil's demographics are reminiscent of South Korea in the 1990s. Africa, where more than 40% of the population is aged 14 or younger, serves as an example of a region that has transitioned to mobile payments without prior digital banking experience. By the time Gen Z fully enters the workforce, the world's economy, finance, and methods of doing business will have transformed significantly from what we know today.

2. Crypto assets in mobile apps

Grab, Southeast Asia's largest mobility and payment service Grab, adds Web3 Wallet

The Grab and Circle Partnership

At the TOKEN2049 conference held in Singapore last September, Circle made an important announcement. Circle is the issuer of the USDC stablecoin, the second largest stablecoin in terms of market capitalization, right after Tether USDT. They are set to operate their crypto wallet service through Grab, the largest delivery, payment, and mobility service in Southeast Asia.

Grab is one of the most popular apps in Southeast Asia, offering services such as ride-sharing, delivery, e-commerce, and payments in eight countries, including Singapore, Malaysia, Indonesia, Thailand, and the Philippines. It currently boasts around 180 million users. Before the official announcement of their partnership with Circle, Grab already had the "Grab Pay Wallet" service in place, which is a straightforward payment service that allows you to add money using deposits or credit cards.

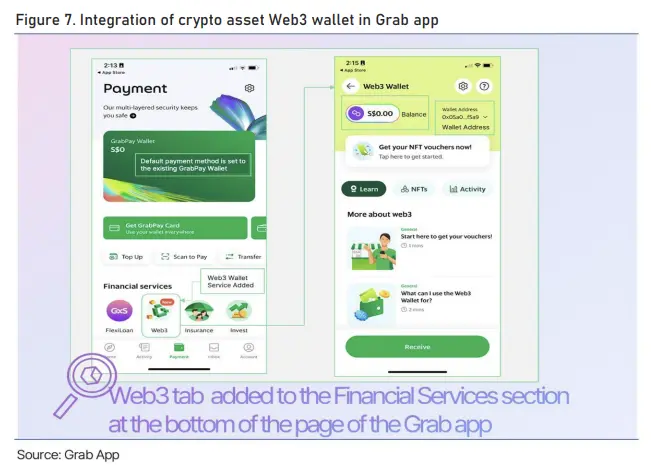

The new "Web3 Wallet" they've introduced supports crypto asset transactions, with the distinction that the transaction process occurs on the blockchain (specifically, the Polygon network). Thanks to Grab's support, users don't incur gas fees during transactions. Unlike traditional crypto wallets, there's no need to manage a private key, and the convenience of using a PIN code is enhanced.

Currently, Grab's Web3 wallet only supports NFTs designated by the Singapore government as part of a pilot program. However, it's important to remain open to the possibility that payments may soon be made using Singaporean stablecoins, as Singapore established its regulatory framework for stablecoins in August.

Singapore's Monetary Authority tests CBDC commercialization potential with Grab app

Singapore tests CBDC with Grab app

I recently created a Web3 wallet right from the Grab app, and it was surprisingly simple. Just tap the Web3 button, read about the SG Pitstop Pack, set up your Web3 wallet, create a PIN, and you're good to go. However, it's important to note that Grab's Web3 wallet is currently accessible only to residents of Singapore who have completed identity verification. So, if you leave Singapore, you won't be able to access your wallet.

This is a remarkable example of integrating crypto payments into an everyday app we use in the real world. It's also essential to recognize that the Singaporean authorities are using the Grab app's Web3 wallet as a testing ground for future CBDC adoption.

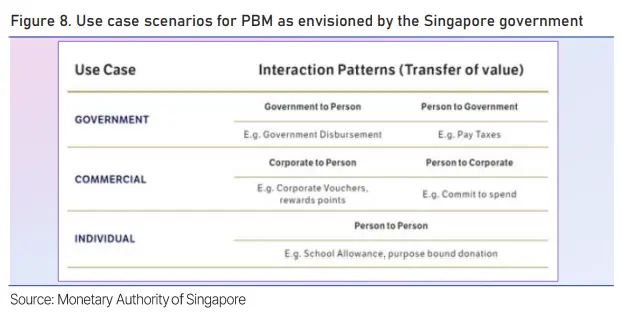

Back in June, the Monetary Authority of Singapore introduced the concept of Purpose Bound Money (PBM) as the initial step in developing a Central Bank Digital Currency (CBDC). PBM is a type of currency that lets the sender specify conditions like an expiration date and where it can be used. This is why the NFTs supported by the Grab App's Web3 wallet are also PBM crypto assets meant for specific stores.

While there were concerns raised by the EU regarding potential limitations on money use, it's unlikely that the future of currencies will solely consist of currencies like PBM with limited durations and use cases.

Singapore government envisions special-purpose currency use cases

Singapore anticipates special-purpose currency use cases

In the future, with decentralization and peer-to-peer transactions, it's likely that various assets will coexist, and users will choose based on convenience and appeal. If a currency is too restrictive or inconvenient to use, people will naturally lose interest in holding it, sparking competition for user preferences.

The Singapore government foresees and will experiment with potential applications for Purpose-Bound Money (PBM). These include: 1) government-provided vouchers or subsidies, 2) vouchers for businesses to offer consumer benefits, 3) funding for government organizations, and 4) educational subsidies. The NFTs currently available on the Grab Web3 wallet are custom-made NFTs designed to coincide with the Singapore Grand Prix Formula F1 event, fitting into the second category mentioned above.

Regulation of stablecoin issuers in Singapore

On August 15, Singapore introduced a regulatory framework for stablecoins. According to this announcement, for stablecoin services to operate officially in Singapore, issuers must maintain a stable value, hold minimum capital and liquid assets, and meet par value redemption obligations, disclosure obligations, and more. Regulation applies to single currency stablecoins linked to the Singapore dollar and G10 currencies issued in Singapore. (SCS, Single currency stablecoin)

Singapore had already regulated stablecoins as digital payment tokens (DPTs) back in 2019 under the Payment Service Act 2019 (PS Act). DPT service providers were subjected to regulations regarding money laundering, counter-terrorism, and financial risks. However, the regulatory framework specifically addressing stablecoin value stability was established in August of the current year. The Monetary Authority of Singapore makes a distinction between stablecoins regulated by them through the issuance of MPIlicenses.

PayPal, serving over 400 million people, begins issuing US dollar stablecoin

PayPal begins issuing PYUSD

In July, PayPal, a globally recognized mobile payment and money transfer service with 430 million users across 202 countries, introduced PayPal USD (PYUSD), a stablecoin backed by the U.S. dollar. This marked PayPal's entry into the stablecoin market,garnering worldwide attention.

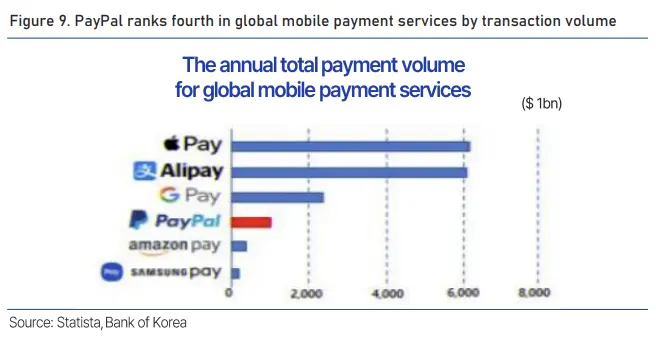

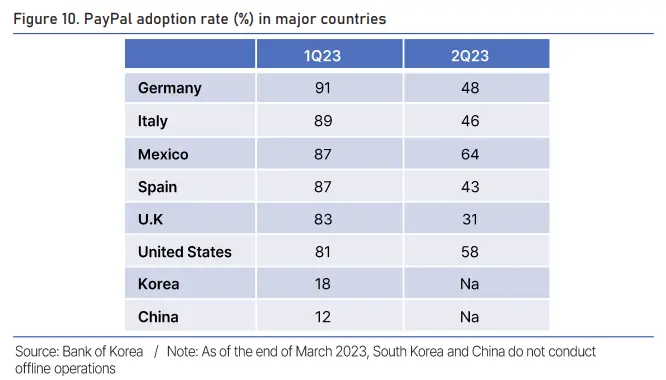

PayPal, founded in 1998, is a NASDAQ-listed fintech company that primarily offers straightforward payment and money transfer services. PayPal ranks fourth in terms of global mobile payment service transaction volume, following Apple Pay, Alipay, and Google Pay. It has achieved an adoption rate of over 80% among affiliated stores in the United States, the United Kingdom, Germany, and more.

No fees for transferring crypto assets between PayPal and Benmo wallets

Users can transfer funds between Benmo and non-PayPal wallets

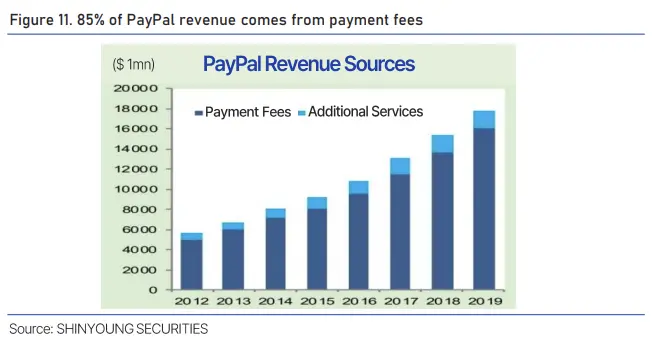

While PayPal provides a wide range of financial services, including microloans, credit, and shopping features, the majority of its revenue is derived from payment-related services, accounting for about 85% of its total earnings, with a strong focus on online commerce payments, including eBay transactions. Consequently, if crypto payments, particularly stablecoins, become widely accepted, PayPal could potentially lose a significant portion of its revenue if it doesn't facilitate payment services for them.

This explains why PayPal has been actively supporting the buying and transferring of crypto assets. In 2020, they introduced crypto trading for U.S. customers, and by March 2021, they enabled the use of crypto for payments. Since May, PayPal has allowed users to transfer crypto assets acquired through its Venmo payment app to other Venmo users, PayPal users, external wallets, and hardware wallets. Venmo, a payment app acquired by PayPal in 2013, now offers free, real-time crypto transfers between Venmo and PayPal wallets.

In August, PayPal's CEO, Dan Schulman, highlighted the need for reliable, digital tools that seamlessly connect to fiat currencies like the U.S. dollar in preparation for the transition to digital currencies. Consequently, PayPal launched a U.S. dollar-based stablecoin (PYUSD) on the Ethereum blockchain.

The issuance and reserve management of PYUSD are entrusted to Paxos Trust Company, a trust firm regulated by the New York Department of Financial Services (NYDFS). The reserves will primarily consist of cash assets such as U.S. short-term Treasury bills and deposits.

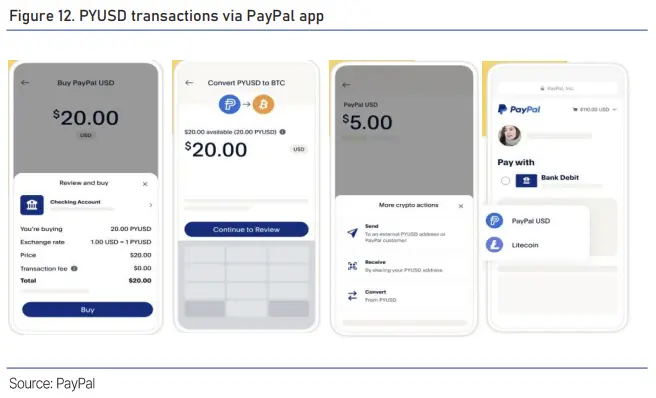

Buy, sell, pay, send, and swap PYUSD within the PayPal app

Slightly higher fees

In the PayPal app, you can easily buy, sell, exchange, and make payments with PYUSD. Sending and receiving PYUSD within the United States is fee-free. PayPal customers can buy and sell PYUSD and USD at a fixed 1:1 rate without any extra charges. However, when trading other crypto assets, apart from PYUSD, a transaction fee applies, based on the transaction size.

Transaction amount from 1 to 200 USD: A fee of USD 0.5-2.5 or 1.5% for amounts exceeding USD 1,000.Users can also swap PYUSD for four different crypto assets within the PayPal app. It's worth noting that PayPal's fees for this service are somewhat higher compared to trading on dedicated crypto exchanges.

0.1% on crypto exchange Binance vs. 0.5-2.5% on PayPal for USD 1-200, and 1.5% for over USD 1,000

PayPal has specified that PYUSD payments and transfers are currently limited to users within the United States. However, there is the potential for future expansion of service coverage and scale. If PYUSD gains global prominence as a stablecoin, it will be essential to develop a regulatory framework that aligns with global standards to prevent regulatory inconsistencies among different countries.

3. Japan opens a 1 trillion-yen payment market

Japan gets serious about stablecoinissuance

Amendment to the Financial Settlement Act allows stablecoin issuance

Japan is among the first major countries to establish a regulatory framework for the issuance of stablecoins. The Japanese government recognized the need for regulation early on, particularly after the Mt. Gox exchange was hacked in 2014 and the Coincheck exchange suffered a security breach in 2018. In June 2022, Japan passed a law on stablecoins, and in June 2023, it made amendments to the Financial Services and Settlement Law to categorize stablecoins as "electronic payment instruments." This change allows Japanese commercial banks and trust companies that meet certain requirements to start issuing stablecoins pegged to fiat currencies.

With the revision of the Financial Services and Settlement Law, a pan is now open to stablecoin issuance, and it's expected that stablecoins will be a priority for business-to-business payments. The business-to-business payment market in Japan is currently valued at 1,000 trillion yen, which is approximately 9,489 trillion KRW and three times the size of the business-to-person transaction market. Japanese financial institutions are eager to tap into the 1,000 trillion yen annual payments market, striving to take a leading role.

Mitsubishi Financial Group (MUFG), Japan's largest financial group, is looking to provide stablecoin issuance services not only domestically but also on an international scale.

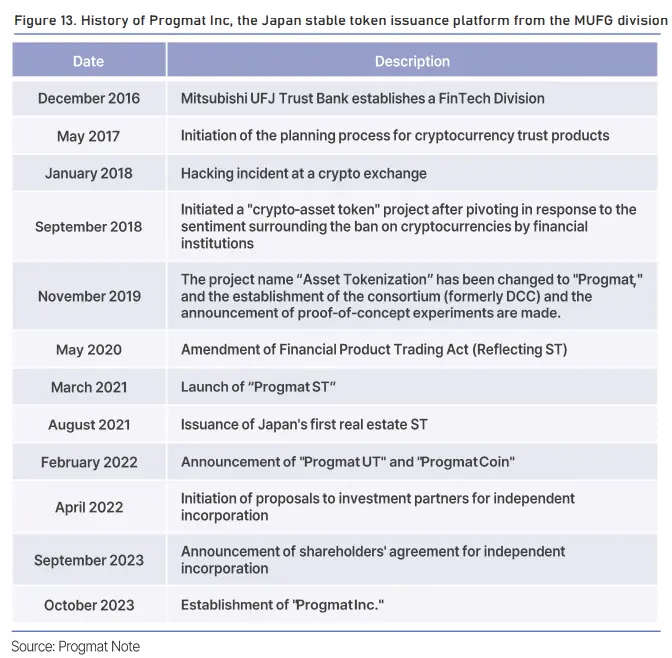

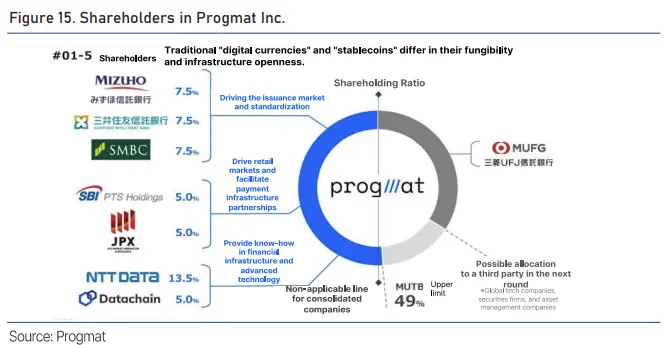

Progmat, a subsidiary of MUFG, was originally established in December 2016 as a FinTech promotion office within MUFJ Trust Bank. In 2018, when financial institutions were prohibited from dealing with cryptocurrencies, the company shifted its focus to an "asset tokenization" project, eventually rebranding as Progmat in 2019. In 2021, it successfully issued Japan's first publicly traded real estate tokenized securities, and in October 2023, it became an independent company known as Progmat Inc.

Progmat consortium, partnering with 214 companies in Japan

Collaborating with various companies

Progmat derives its name from "programmable trust," reflecting its mission to connect society through a programmable network and digitize all forms of value.

* Progmat = Programmable Trust = Creating a Programmable Trust

Progmat's business model centers on two key revenue streams: 1) license fees and 2) transaction fees. License fees are fixed monthly charges, and as more users join the network and engage in token transfers, the company's revenue increases accordingly.

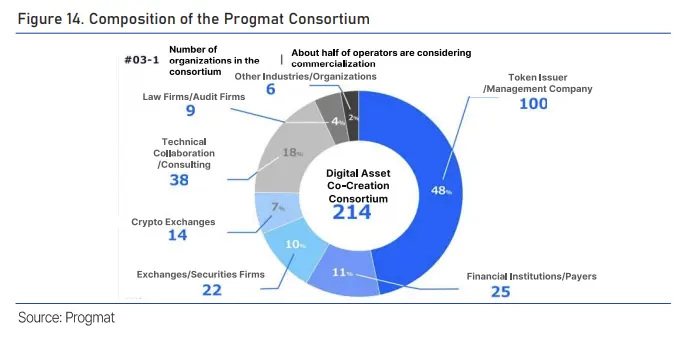

The greater the number of companies participating in the network, the larger the pool of Real World Assets (RWA) available for tokenization. Moreover, as more RWA tokens are actively traded, Progmat's income grows. To support these objectives, Progmat has formed a consortium comprising 214 diverse Japanese companies, including token issuers (such as securities and real estate firms), financial institutions, payment providers, exchanges, tech companies, law firms, and more.

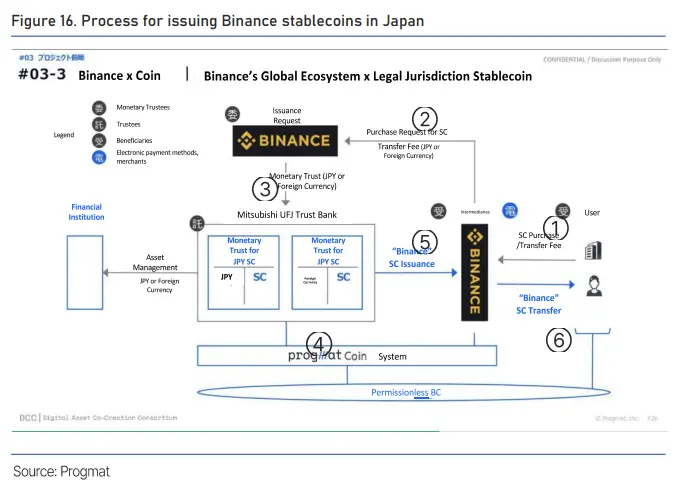

Binance's Stablecoin Plans via Progmat

Binance plans to issue stablecoins through Progmat

On September 26, reports indicated that the cryptocurrency exchange Binanceis exploring the possibility of launching a stablecoin linked to various fiat currencies, including the yen, in collaboration with MUFG, according to Coindesk. Binance Japan and MUFG are jointly researching the creation of a stablecoin tied to various fiat currencies, including the yen. The intention is to commence stablecoin operations late next year, contingent upon obtaining the necessary regulatory approvals.

Progmat recently shared insights into the process of acquiring stablecoins through Binance and distributing them through trust banks, illustrated in the figure below.

A user interested in buying stablecoins initiates the process by paying the purchase price to a Binance broker (exchange). Depending on the purchase application, Binance deposits yen or foreign currency into Mitsubishi UFJ Trust Bank. The trust bank then records yen and foreign currencies on its balance sheet's asset side, managing them through financial institutions. Stablecoins, in turn, are recorded on the liability side. The issuance of stablecoins via the Progmat system involves transferring them to users.

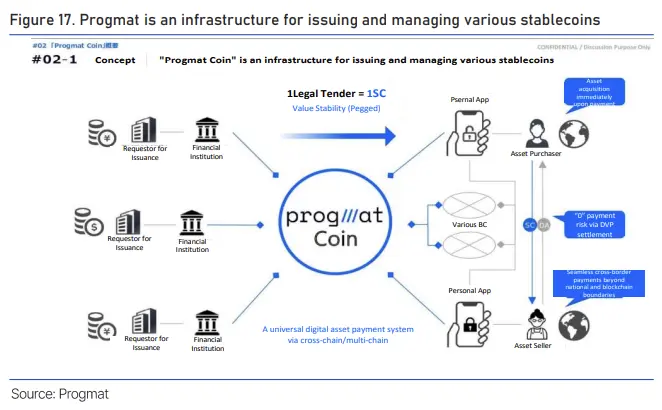

Progmat has the potential to expand its reach beyond the business sector

Progmat, the infrastructure for stablecoin issuance and management

Progmat, originally a project under MUFG, has evolved into a consortium featuring 214 Japanese companies. This consortium spearheads asset tokenization in Japan and envisions issuing various fiat currencies, not just the yen, for stablecoins. The long-term goal is to establish a foundation that facilitates universal payments across multiple blockchains.

A notable aspect is that Progmat is not restricting its stablecoin issuance clients to Japanese companies; it welcomes international companies willing to comply with Japanese stablecoin issuance regulations, implying the potential for future expansion beyond Japanese borders.

The Impact of Stablecoin Exapansion on Existing Industries

1. Impact on the banking industry

Decentralization of banks' currency exchange, lending, and deposit functions

With the growing convenience of mobile payment services, activities like money transfers, payments, and deposits are increasingly done through payment company platforms. The Millenials and Gen Z, particularly those who initiated their economic activities using mobile payment systems, prefers handling financial transactions through digital channels rather than visiting physical bank branches. According to a Consumer Insights survey in October 2022, 6 out of 10 Millenials and Gen Z combined haven't visited a bank branch in the last three months, and 87% of them opt for digital channels for their daily financial transactions.

Given their familiarity with mobile-based operations, if mobile apps simplify the storage, payment, and transfer of stablecoins and make them more accessible in the real world, the number of new bank accounts being opened may substantially decline. This is because you can make mobile payments using your existing account, and if stablecoins gain widespread acceptance, personal mobile crypto wallets could effectively replace traditional bank accounts.

Furthermore, banks' traditional domains, such as currency exchange, loans, and deposits, might undergo decentralization as they face competition from crypto-related services. If multiple stablecoins in various currencies become available, individuals are more likely to engage in peer-to-peer wallet-to-wallet exchanges or use decentralized exchanges (DeFi) for currency conversion.

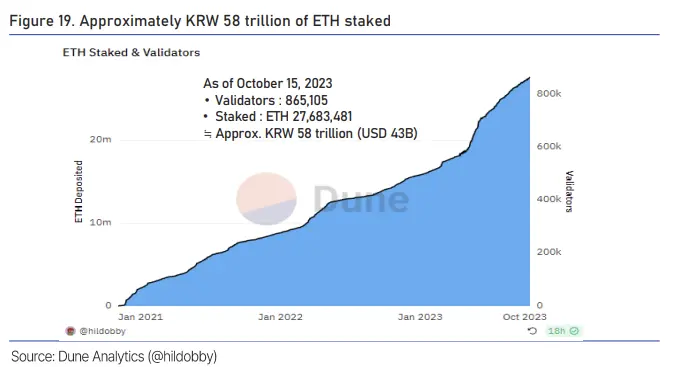

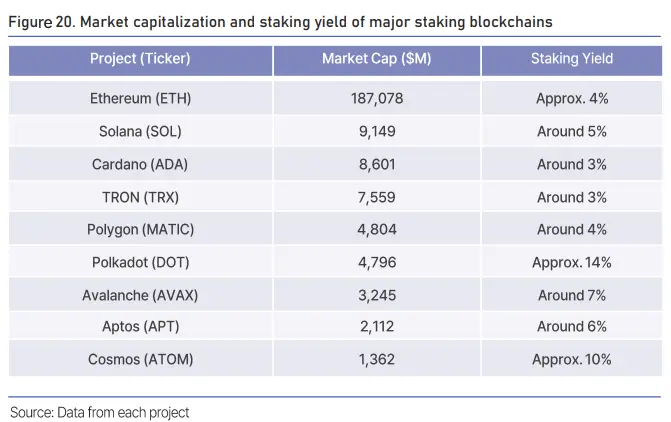

Regarding deposits, the growing crypto asset market may lead to some of the demand traditionally associated with savings accounts being satisfied through staking. Ethereum's staking volume, for example, has nearly tripled since the beginning of2022 and currently exceeds 27.68 million ETH.

Staking replaces some of the demand for interest and dividends

In addition to Ethereum, Proof of Stake (POS) blockchains like Solana and Cardano offer annual staking yields ranging from 3% to 7%, albeit lower than before. While it's crucial to consider the risks associated with crypto assets, staking on trusted chains like Ethereum has the potential to be akin to receiving stock dividends. In the case of bank loans, new alternatives such as crypto collateral and crypto peer-to-peer lending are emerging, which could weaken the long-standing dominance of traditional banks.

On the other hand, banks can stay competitive in the expanding blockchain economy by getting involved in stablecoin issuance processes, as seen with Mitsubishi Trust Bank, or by tokenizing deposits. Unlike crypto institutions, banks already have established anti-money laundering and anti-terrorist financing measures, along with deposit protection systems. This can help alleviate user concerns regarding stablecoin issuance.

2. Impact on the creit card industry

U.S. credit card companies rely heavily on network fees

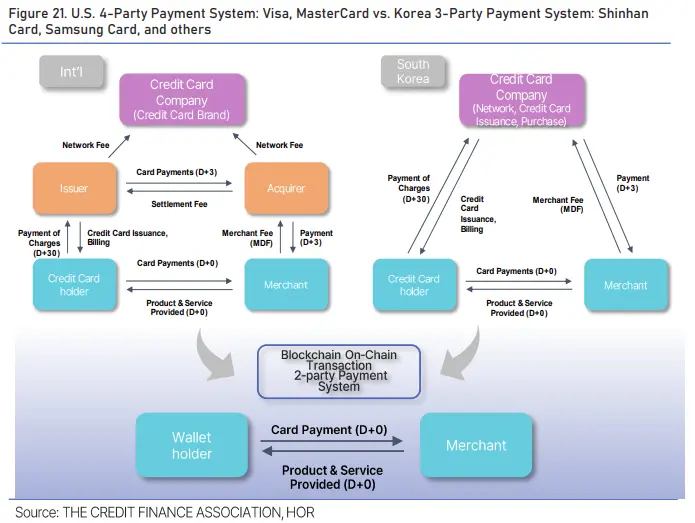

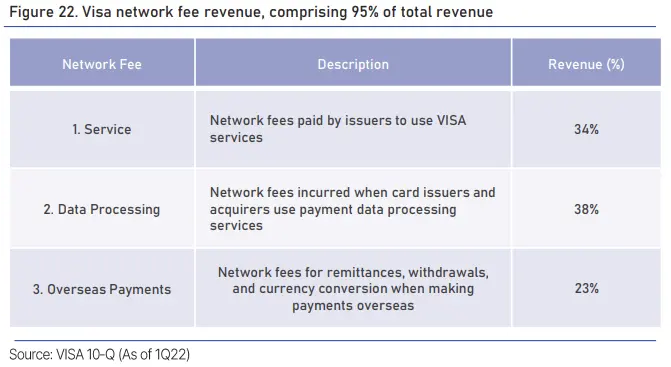

Credit card companies primarily earn their revenue from merchant fees for card transactions between credit card holders and affiliated stores, or payment network fees in the case of international card companies. As a result, the credit card industry faces a direct threat to its revenue when blockchain payment systems, eliminating intermediaries, are introduced.

The Visa and MasterCard payment systems, which dominate over 70% of the US credit card market, operate on a four-party model. Cardholders obtain cards from issuers, and when card payments occur, affiliated stores pay fees to acquirers. Acquirers and issuers then pay network fees to Visa and MasterCard, serving as the primary income source for credit card companies.

On the other hand, domestic credit card companies employ a three-party model comprising cardholders, affiliated stores, and credit card companies. Here, the merchant makes payments to the credit card company, which, in turn, earns fees from the merchant. Consequently, the rise of blockchain-based direct transactions between cardholders and affiliated stores, both domestically and internationally, poses a risk to card companies by diminishing their income from network fees and merchant fees received from acquirers and issuers. This prospect has put credit card companies on high alert and stirred concerns about the development of blockchain technology.

VISA to offer on-chain crypto asset transfers between acquirers and affiliated stores

VISA's strategy to prevent merchants leaving

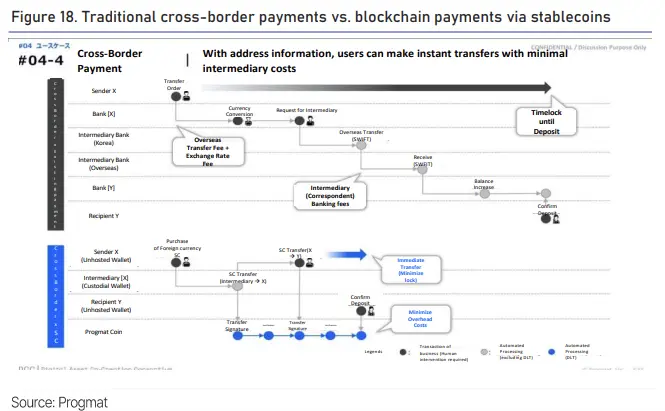

While domestic card companies face declining profits, especially due to continual reductions in merchant fees, their overseas counterparts have maintained steady network fee income. This stability, backed by a vast network encompassing over 70 million affiliated stores globally, contributed to VISA's impressive 67% operating margin in 2022.However, the advent of blockchain payments directly connecting cardholders and affiliated stores is revolutionizing the landscape. It reduces merchant payout times from an average of three days to mere seconds or minutes, while the absence of intermediaries and lower fees are luring affiliated stores away from traditional card networks. International card companies, recognizing the advantages of blockchain technology, began incorporating crypto assets like Bitcoin as payment options in 2020. More recently, they have extended support to stablecoin on-chain payments to enhance the convenience of crypto transactions for both affiliated stores and cardholders.

In this context, VISA introduced the stablecoin USDC as a payment option in March 2021 and began supporting Solana blockchain payments in September 2023, following Ethereum. VISA is further expanding its support for stablecoin payments to card acquirers like Worldpay and Nuvei. This allows acquirers to receive funds directly on-chain, significantly speeding up settlement times. Previously, even if a cardholder paid with crypto assets, they had to be converted into fiat currency before reaching the merchant. Moreover, for cross-border payments, there were additional costs for currency conversion and international transfers. Now, payments are delivered to the merchant directly on-chain in USDC, reducing both time and expenses.

Domestic card companies less dependent on merchant fees than overseas peers

Local card companies have been consistently lowering merchant fees

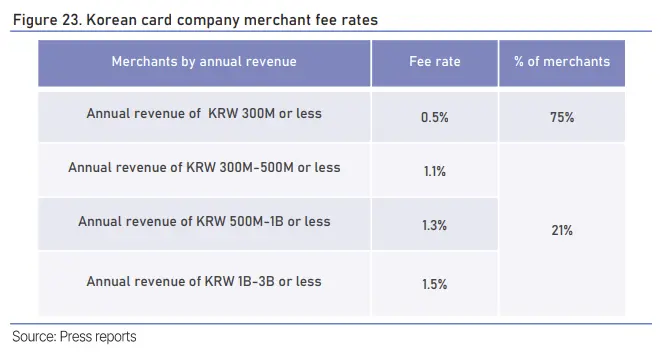

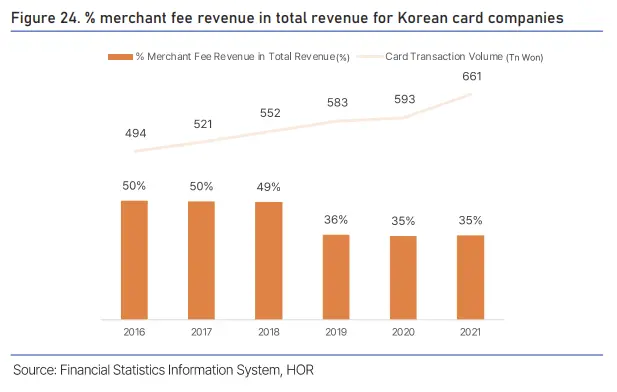

Unlike their international counterparts, local card companies have a three-party structure, where they function as a network, issuer, and acquirer. This means they provide not only the network but also issue cards and manage affiliated stores and members. Over the last 13 years, these companies have reduced merchant fee revenues on 14 occasions. The share of merchant fees in their total revenues has plummeted from 49% in 2018 to 35% in 2021. Currently, as much as 75% of affiliated stores are subjected to the lowest fee rate of 0.5%, causing losses in this segment even if there's a high card transaction volume.

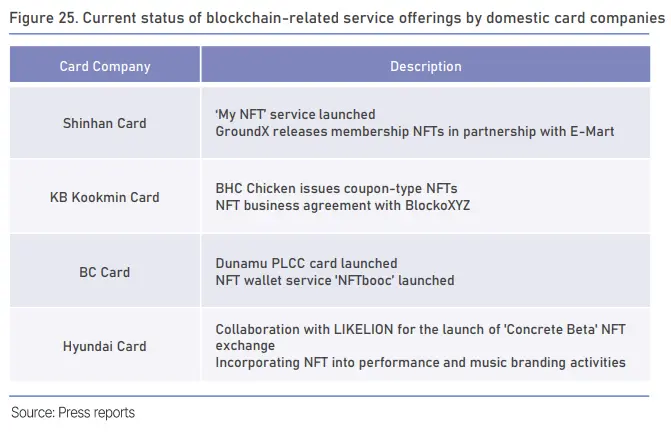

Local card companies are under pressure due to various factors, including a proliferation of payment methods and heightened competition. In 2022, out of a total of 732.6 billion won in payments, credit cards accounted for 351 billion won, marking a 17% increase year-on-year. Payments through mobile phone manufacturers like Samsung amounted to 183 billion won, showing a 35% year-on-year growth during the same period. Additionally, payments through prepaid electronic payment services reached 828.9 billion won, a 25% increase year-on-year. Despite these challenging industry conditions, local card companies have managed to compensate for reduced merchant fees by diversifying into other sectors such as loans. Therefore, they may not feel the threat of on-chain payments as acutely as their international counterparts. As a result, local card companies are directing their focus toward offering supplementary services that involve NFTs rather than actively pursuing blockchain-based payment solutions.

3. Impact on crypto exchanges

Loss of profitability by CEXs

The dominant position of Centralized Exchanges (CEX) is weakening

CEXs: Globally, centralized exchanges are seeing their revenues decline due to an increasing trend of individuals holding personal wallets, reduced trading volumes because of lower altcoin price volatility, and heightened SEC regulations. In the future, if stablecoins and major cryptocurrencies are used for buying real-world assets, we might see a perceived distinction between coins with real value or utility and those lacking it. Notably, platforms like Telegram and PayPal crypto wallets only support a limited number of coins, including Bitcoin, Ethereum, and stablecoins. Depending on the extent to which these are broadly adopted and embraced for payments, it could lead to a reevaluation of these coins, potentially impacting their demand.

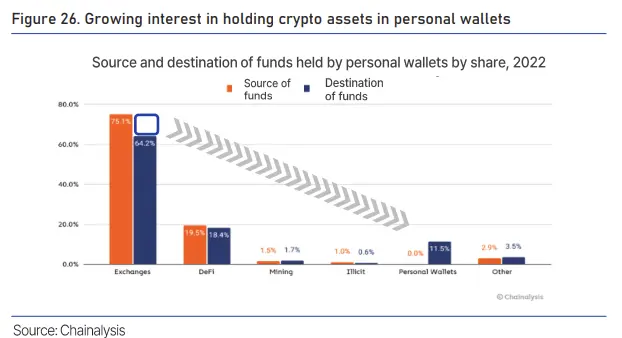

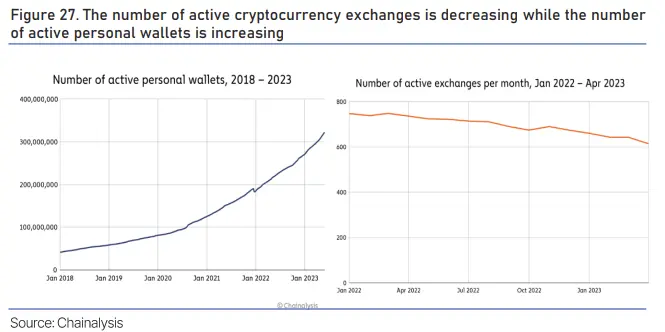

Additionally, people might become less willing to trust third parties with their assets if they can secure them using their personal wallets. The chart below illustrates that from 2020 to 2022, there were substantial inflows and outflows from exchanges, but the difference (Source of Funds - Destination of Funds) shifted towards private wallets.

Increased on-chain activity boosts DEX, DeFi markets

DEXs: If mobile web wallets facilitate swapping, buying, and selling of major cryptocurrencies, DEXs also play a role in spreading trading activity to mobile wallets. However, unlike CEXs, DEXs and DeFi are anticipated to counteract the adverse effects of reduced swap and trade transactions as the stablecoin market growth expands on-chain activities such as staking, deposits, and lending. According to analysts at Catalysis, the number of active cryptocurrency exchanges decreased by almost 20% from January 2022 to April 2023, while the number of personal wallets has been rapidly growing since 2021.

Increased on-chain activity is driving the growth of DEX and DeFi markets, and more individuals are opting to hold their crypto assets in personal wallets.

4. Impact on the on-chain market

The growing competition among stablecoins

The stablecoin market's growth will be determined by its adoption on various platforms. For instance, Circle's USDC and PayPal's PYUSD are likely to gain market share because of their adoption on platforms with large user bases. Other stablecoin issuers will seek partnerships with real-world companies to reach a borader user audience.

Effective communication between regulators and issuers, as well as enhanced transparency, is paramount to earn users' trust. A case in point is MakerDAO's decision to eliminate the USDP stablecoin from the Reserve on May 29. This move followed the New York regulators' directive in February that compelled Paxos to cease the issuance of Binance USD, which is operated by Paxos. Issuers failing to meet the requirements set by US regulators face the risk of losing their market position. Conversely, stablecoins adhering to these standards, embracing transparency, and fostering trust through disclosure are expected to gain a competitive edge.

Non-interest-bearing stablecoins, driving demand for Tokenized Treasury

As stablecoin issuance gains momentum, particularly in countries with established stablecoin legislation such as Japan and Singapore, on-chain market liquidity is projected to see substantial growth within the next year or two. In contrast, the European Union's Markets in Crypto Assets (MiCA) legislation, enacted in April, forbids stablecoin issuers from providing interest payments. This prohibition is likely to extend to stablecoin interest payments via DeFi, given that stablecoins pledged as collateral for fiat currency won't be able to accrue interest.

Consequently, this is expected to drive a surge in investments in tokenized U.S. Treasuries, offering enhanced safety. The prohibition on paying interest for stablecoin issuance is akin to maintaining a zero interest rate policy for the currency.

European regulatory authorities have classified interest payments by stablecoin issuers as akin to banking activities and have imposed a ban. In a scenario where stablecoin issuance increases, and holding stablecoins doesn't yield interest, there's likely to be an upswing in investment demand for tokenized U.S. Treasury securities as an alternative avenue for earning interest. Furthermore, the augmented on-chain liquidity is anticipated to impact the overall prices of crypto assets, including native tokens. The rationale behind this is similar to how, historically, the US Federal Reserve's adoption of a zero interest rate policy for the dollar reduced its attractiveness, resulting in higher prices for US Treasuries and stocks. The number of active cryptocurrency exchanges is decreasing while the number of active personal wallets is increasing

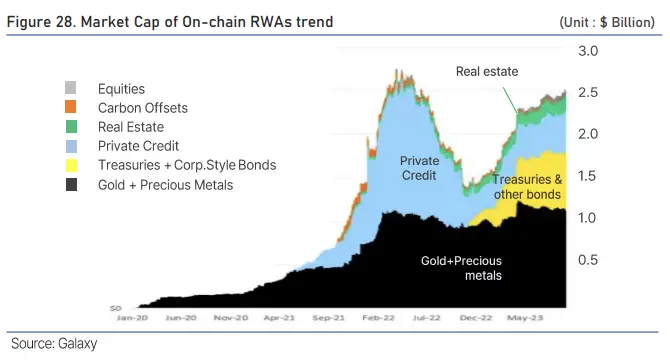

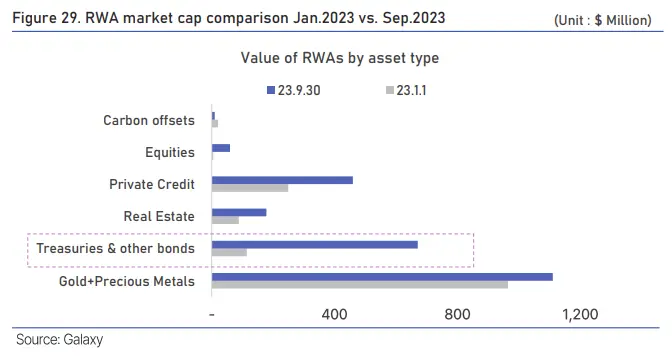

Tokenized Treasury drives recent RWA market expansion

Tokenized Treasury drives RWA growth

The on-chain market capitalization of Real World Assets (RWA) reached $2.4 billion by the end of September 2023, marking a $1.05 billion increase since the year's commencement. Notably, 56% of this growth can be attributed to the tokenization of Treasury and corporate bonds, exhibiting the most rapid expansion among all asset classes.

By September's close, the market value of tokenized US Treasuries stood at $670 million, surging by 4.9 times compared to January figures. Noteworthy issuers of US short-term Treasury tokens encompass Ondo Finance, Franklin Templeton, and Matrixdock, with their combined tokenized US Treasuries amounting to $570.5 million, constituting 85% of all tokenized Treasuries and corporate bonds. Currently, the US 3-month Treasury yield stands at 5.5%, surpassing the average stablecoin deposit yield of 3% by 2.5 percentage points this year. Forecasts anticipate that the US Federal Reserve's benchmark interest rate will remain at this elevated level for an extended period, thereby upholding the significant interest rate advantage of US short-term Treasury tokens.

Increased crypto asset market liquidity anticipated to drive market cap growth

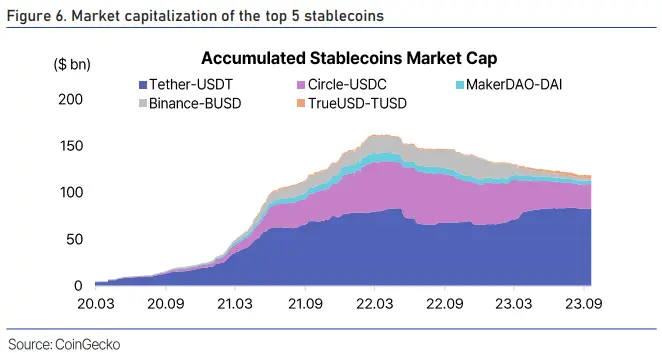

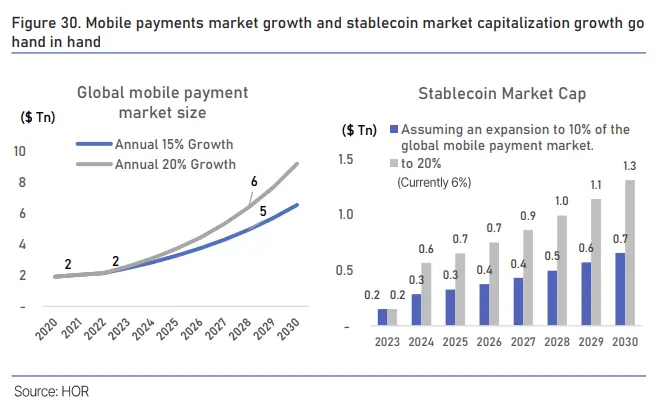

Stablecoin market capitalization poised to grow threefold or more

As of now, the collective market capitalization of the six major stablecoins is approximately $150 billion, accounting for around 15% of the overall crypto market valued at $1 trillion. Prospective drivers of future stablecoin growth encompass the green light for stablecoin issuance by major countries, active participation by financial institutions, and the expansion of the global mobile payments market. Notably, Japan and the EU were among the earliest adopters of regulatory frameworks for stablecoins, permitting eligible institutions to issue these financial instruments. Other countries are expected to follow suit in the months ahead, especially as the concept of stablecoin payments for facilitating cross-border trade gains traction.

The upswing in global mobile payments is poised to go hand in hand with the growth of the stablecoin market. Particularly in emerging economies, there is a notable rise in the proportion of the Millennials and Gen Z who are well-acquainted with mobile app payments and, intriguingly, some of them are seamlessly integrating cryptocurrencies into their daily financial lives, including opting to receive their salaries in crypto. Companies with a global user base, such as PayPal, are capitalizing on this trend by introducing cryptocurrencies as payment options within their mobile apps, thereby fostering natural adoption.

While it is difficult to accurately predict how much the stablecoin market will grow, we have calculated a rough estimate based on the conservative assumption that the global mobile payment market will grow at an average annual rate of 15%, and the share of the stablecoin market in the mobile payment market will expand from 6% to 10% to 20%. The global mobile payment market was $2.1 trillion in 2022, and if it grows at an annual rate of 15%, it will grow to about $5 trillion in 2028, five years from now. Along with the growth of the mobile payments market, if the stablecoin market share grows modestly from the current 6% to 10%, the market capitalization is expected to triple to about $500 billion, and at 20% growth to $1 trillion, about 7 times compared to the current market capitalization.

Leverage the benefits of blockchain technology and create an infrastructure that meets global standards

At present, approximately 25 million addresses hold $1 or more in stablecoins, with around 80% of them maintaining balances ranging from $1 to $100. This figure is akin to the combined number of accounts in the five largest U.S. banks. The significance here lies in the fact that the majority of these addresses manage modest sums of stablecoins, illustrating their potential to deliver financial services to individuals underserved by conventional financial systems. The rise of disintermediated blockchain technology can bring forth opportunities for those traditionally marginalized in finance, while simultaneously presenting challenges to established players in traditional financial markets.

Leveraging the benefits of the technology to create new growth opportunities

However, it is crucial to comprehend that the future remains malleable, shaped by economic actors. The collective efforts of businesses, governments, and academia in uniting their expertise to prepare and construct alternatives can lead to improved outcomes.By fully leveraging the advantages of blockchain technology to enhance societal interconnectedness and engagement and establishing regulatory frameworks and support that align with global standards, the blockchain economy can evolve into a realm of fresh opportunities, enabling the realization of individual potential and the more appropriate allocation of resources and capital.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results. This article is provided by CrossAngle’s third-party research partners. CrossAngle does not have any editorial control over this article and does not warrant the accuracy and timeliness of the information contained herein. This article may contain links to third-party websites, over which CrossAngle disclaims any control or responsibility.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.