Decentralised Stablecoins

Key Takeaways

- Stablecoins have become an integral part of the cryptocurrency ecosystem, rising dramatically in prominence and usage in recent years. They aim to address a key limitation preventing greater mainstream adoption of cryptocurrencies — significant price volatility. However, a series of high-profile stablecoin depeggings in recent years — where the coin permanently or temporarily loses its one-to-one pegged value with the reference asset — highlights that volatility risks still remain.

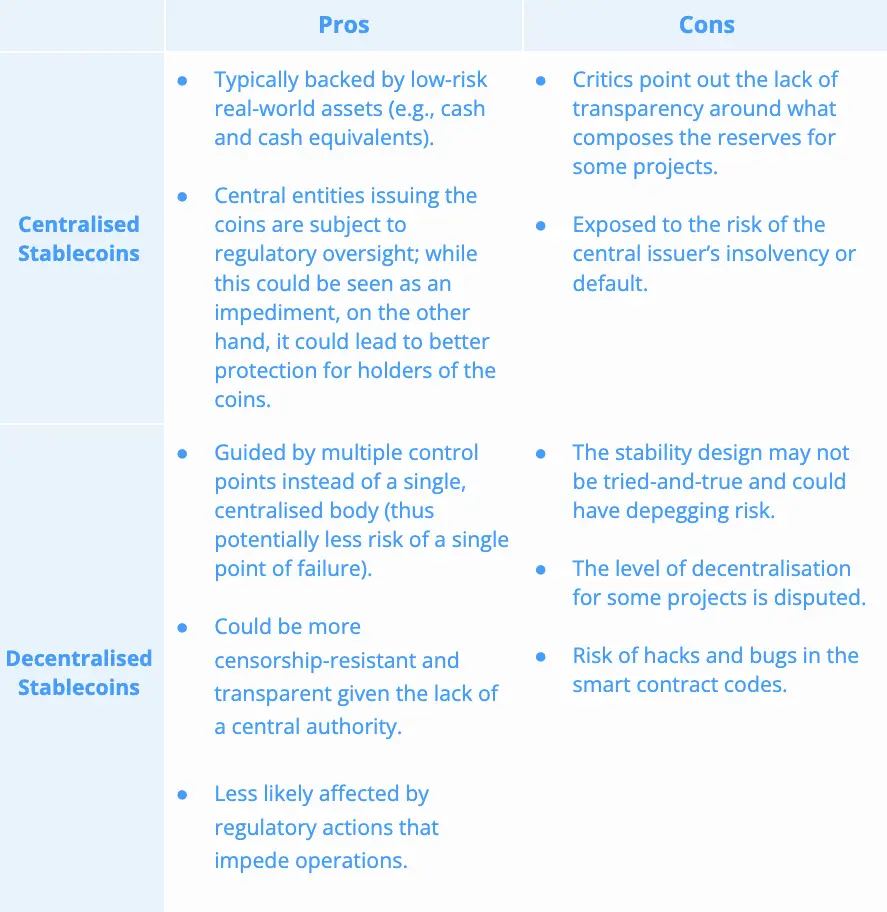

- Issued by centralised entities, centralised stablecoins typically maintain reserve assets like fiat currency to back each coin and ensure pegs are maintained. However, they present counterparty risks and other issues for the users. Decentralised stablecoins aim to provide a solution: They operate on blockchain networks without the need for a centralised authority and maintain their pegs autonomously through protocols (often involving collateralisation) and mathematical algorithms.

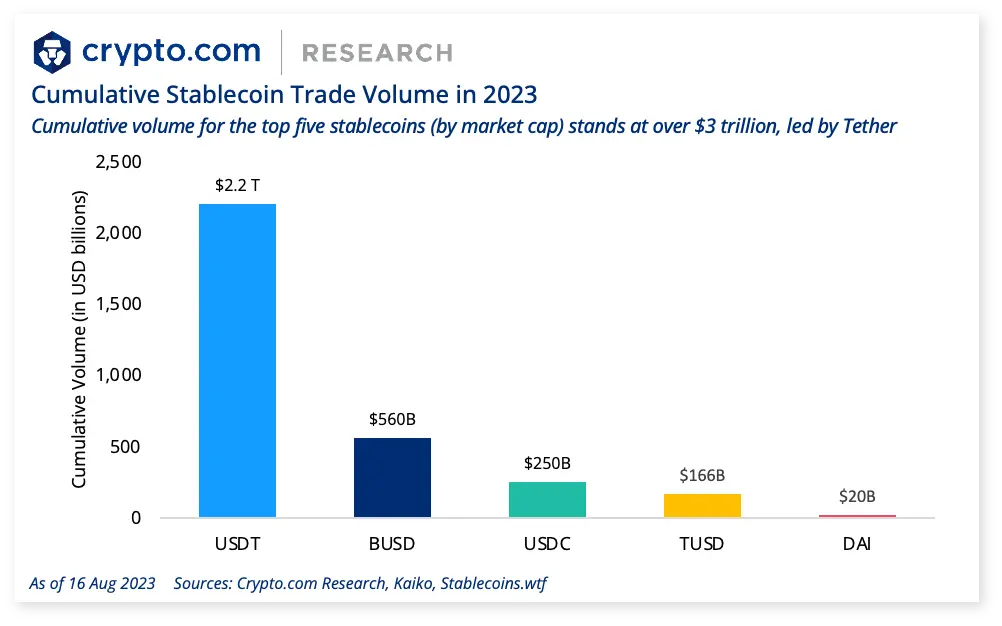

- The top five stablecoins based on market capitalisation are USDT, USDC, BUSD, TUSD, and DAI. Together, they make up about US$3 trillion in cumulative trading volume in 2023, with Tether’s USDT making up the majority within both centralised and decentralised exchanges.

- Although decentralised stablecoins employ different mechanisms for maintaining price stability, there are some common approaches:

- Over-collateralisation: Stablecoins are issued by requiring deposits exceeding the value of collateral to mitigate the risk of insolvency.

- Real-world assets: Stablecoins are backed by an equivalent amount of real-world assets (RWAs), such as US Treasuries, as reserves to maintain stability and pursue better-yielding investments.

- Popular decentralised stablecoins in the market today include DAI, FRAX, and LUSD.

- DAI is an Ethereum-based stablecoin soft-pegged 1:1 to the US dollar. It is issued by DeFi lending protocol MakerDAO, and borrowers who deposit eligible crypto collateral are issued a DAI-denominated loan. Its current market cap stands at about US$5.35 billion.

- FRAX is a decentralised stablecoin that is both crypto-backed and algorithmic. It is issued by Frax Finance on Ethereum. The protocol mainly focuses on three DeFi areas: stablecoins, liquidity, and lending markets. FRAX currently has a market cap of around US$804 million.

- LUSD is a decentralised over-collateralised stablecoin (pegged to the US dollar) issued by Liquity (LQTY), which is a DeFi borrowing protocol on Ethereum. LUSD currently has a market cap of US$293 million.

- New entrants are also gaining traction, riding the growth of their native ecosystems. While still nascent, their integration within leading DeFi protocols could give them utility advantages over stand-alone stablecoins.

- GHO applies a fixed oracle price (US$1), and interests are repaid to the DAO treasury directly.

- crvUSD employs a novel liquidation Automated Market Maker (AMM) algorithm, and the peg is maintained by PegKeeper.

- sUSD (v3) turns the stablecoin into collateral-agnostic without relying on SNX, becoming a cross-chain asset.

- In addition to the traditional approaches through reserves and collateral to establish stablecoins, there are other concepts of decentralised stablecoins, such as float-pegging (Rai), as well as delta-neutral and yield-bearing stablecoins (USDe). For more information, read about the new designs of stablecoins as discussed in our report Innovative Stablecoins, exclusive to our Private and VIP users.

- Future stability will rely on maintaining confidence through prudent design and stress testing of mechanisms. Collaboration between protocols may help develop more resilient stabilisation models, and adoption drivers — like mainstream companies launching stablecoin payment networks — could accelerate growth. Overall, as the cryptocurrency ecosystem matures, stablecoins are well positioned to facilitate broader mainstream adoption, provided protocols can consistently and reliably deliver on their core promise of price stability.

Read the full report: Decentralised Stablecoins

Original Link

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.