Market Spotlight: Has Ripple’s Ruling Changed the Narrative?

Written by Jacob Joseph, CCData

State of the Market

The State of the Market for July has been mostly positive, despite a negative month-to-date performance by BTC (-3.7%) and the wider market (-1.2%), represented by CCData’s MVDA index.

Certain assets that were deemed securities by the SEC in last month’s lawsuit filing against Coinbase and Binance have rallied and outperformed the market drastically. Ripple and Solana, for example, dominated the altcoin space for volume and returns, drawing liquidity and interest from other baskets, such as Layer2s and AI, which have seen a large decline in their ability to command the current narrative and consequent capital flows.

The positive performance of the basket that contains the assets that were deemed securities follows the recent ruling by Judge Torres on the status of XRP, and by extension, other altcoins.

Although XRP may be a security when sold to institutional investors, it is not a security when sold to the general public. This decision has been hailed as a win for the industry, as it sets a precedent which classifies altcoins as non-securities on the secondary market.

This is a huge boost to exchanges, market makers and retail investors, who have been waiting for an outcome since the case started back in December 2020. As a result of this positive boost to the altcoin sector, we have seen Bitcoin Dominance (as a % of the overall market cap) decline.

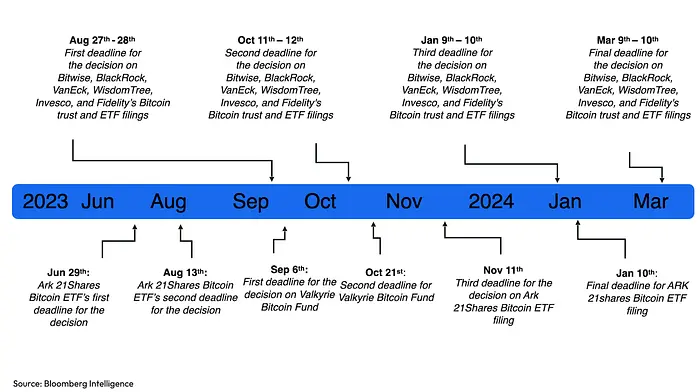

Despite BTC’s negative MTD performance, its newsflow remains cautiously optimistic. Last month saw a flurry of Bitcoin Spot ETFs, which catalysed last month’s bullish sentiment and confidence in the industry. This month, however, new updates have emerged.

The SEC has accepted applications from six firms, including BlackRock, for review. This indicates the commencement of the official review process for these ETFs, which now follows a strict timetable, as can be seen below.

One of the biggest beneficiaries of the month has been Coinbase, deriving positivity from Judge Torres’ ruling in the XRP case, as well as being named in the Surveillance Sharing Agreement as a (SSA) counterparty for some of the largest ETF filings, including BlackRock, CBOE, Fidelity and Valkyrie. These outcomes weigh positively on Coinbase’s chances against the SEC for two reasons.

Firstly, they have been sued for selling unregistered securities. If XRP is deemed to be a non-security on the secondary market, then the SEC’s case against Coinbase suffers as a result.

Secondly, if most of the ETF filings are listing Coinbase as an SSA partner, then there is a high degree of confidence in Coinbase by some of the largest financial institutions in the world, which bodes well for its future and reiterates optimism in their legal case.

Coinbase’s stock, COIN, has significantly outperformed BTC since the ETF announcements were made. As a result of this renewed optimism within the institutional/TradFi periphery of digital assets, other crypto-related equities have seen strong outperformance of digital assets themselves, with Microstrategy, Marathon and Hut all putting in strong MTD returns, outpacing Coinbase in some cases.

Considering recent macroeconomic news, the Federal Reserve raised rates by 25bps, which brings the current rate up to 5.5% from 5.25%, marking the highest level in 22 years. Although the FED opted to pause in the previous rate decision, with inflation still sitting above their target 2% level, the continuation of hikes this month was widely expected.

The FOMC press conference clearly left the door open to further rate hikes if deemed necessary. This has led to a 75/25 split on probabilities for the target rate remaining unchanged or hiked by 25bps respectively.

Exchange Analysis: Is Centralised Exchange Dominance Under Threat?

Trading activity on centralised exchanges has taken a blow as a result of the lack of volatility, with Q2 2023 marking the lowest quarterly volume since Q4 2019. Given that Q3 has historically seen the lowest average volumes during the year, as a result of seasonality effects, we could see a sustained period of low trading activity ahead of key decisions surrounding the spot ETF applications.

Meanwhile, with markets remaining highly speculative and external institutional capital yet to flow in, derivatives market share on centralised exchanges continues to remain at an all-time high, reaching 81.7% in July (as of the 24th). Derivatives volume is on track to record the lowest monthly volume since the start of the year with $1.75tn traded as of the 24th of July.

With speculation at an all-time high and trading volumes on centralised exchanges at a historically lower level, the scene has been set for more on-chain activity.

In the last couple of months, we have seen short-term narratives involving ‘meme tokens’ such as $PEPE and $BITCOIN (not the original one) hitting $1bn and $100mn in market cap respectively.

Recent innovations in the on-chain trading world involving Telegram bots, such as Unibot, have further fuelled the growth of DEX trading. Participants are now able to conveniently trade from their mobile phones using their Telegram app, rather than having to connect to multiple dApps and wallets.

In July, DEXs traded $54.0bn (as of the 24th), with market dominance compared to CEXs reaching 12.1%. This is the second-highest market dominance for DEX trading, behind the all-time high of 13.8% recorded in May.

With centralised exchanges under threat from regulatory scrutiny, and recent innovations in the on-chain trading world aiding trading activity, we could see the beginning of the decline in CEX dominance in crypto trading.

Asset Focus: Bitcoin — The Good, Bad and the Ugly

In July, Bitcoin has been consistently trading within a tight range, oscillating between $31,840 and $28,864 (according to CCData’s CCAGG reference price). This tight range has led Bitcoin to register an exceptionally low level of volatility, with an average volatility of 37.7% in July (as of the 25th) — a level only previously seen in January 2023.

The resilience has manifested in BTC open interest, which saw a notable increase of 8.37% in July, reaching $9.80 billion (as of the 24th of July). Funding rates also remained consistently positive throughout the month and the leverage ratio saw an increase, signalling a growing appetite for leverage within the digital asset markets.

Despite the increased appetite and optimistic sentiment, driven by factors like ETF filings and positive regulatory news, many digital assets failed to make significant short-term gains.

Liquidity has played a crucial role in this, with liquidity recording lows every month and declining by 17.6% in July (as of the 24th). Liquidity year-to-date, however, has seen an even more severe decline, falling by 33.8%.

However, Bitcoin options have shown a predominantly bullish trend, with the Put to Call Ratio declining in the long term, reaching 13% for options expiring on the 29th of March 2024.

Away from Bitcoin, some assets have made impressive gains in July. Below we share a snapshot of the stand-out performers of the top 100 assets by market capitalisation.

- XDC Network, a layer1 EVM–compatible blockchain, saw its price surge on the 20th of July. The asset has recorded an increase of 566.0% (up to the 26th of July).

- XRP, SOL and XLM, which all benefited from the non-securities narrative, saw returns of over 20%.

- DOGE has also performed well over the past couple of days, increasing by 9.81% following Twitter’s rebranding to X (from the 24th of July till the time of writing)

- BNB, however, has seen its futures trading encounter severe shorts, as illustrated in the chart below.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.