Upcoming Launch of RWA — Frax’s Future Product Planning and Potential Impact

Written by Yuuki, LD Capital

During the FXS turbulence in CRV, FraxLend’s dynamic interest rate design that protects borrowers received positive feedback from the market. Additionally, a governance proposal launched by Frax Protocol founder, Sam, on August 4th to advance RWA business attracted some market attention. This article aims to outline Frax’s future product plans (FRAX V3, frxETH V2, and Fraxchain) and analyze the potential impacts.

I. Frax V3 — Focusing on RWA Business Launch (Launching in August)

Currently, Frax founder Sam has initiated a proposal on the governance forum to expand the RWA business through FinresPBC, which is expected to launch within August. Key points include:

1. Established earlier this year, FinresPBC is a non-profit organization. Thus, all profits from assets held by Frax Protocol, after covering operating costs, will be returned to the protocol.

2. FinresPBC does not participate in the development, operation, or governance of the Frax Protocol. It also refrains from any other profit-making activities (mortgages, loans, pledges, or other business activities) to ensure purity and stability in operations.

3. Lead Bank is currently the cooperating bank for FinresPBC, providing compliant financial services for Crypto protocols. FinresPBC is also actively expanding partnerships with more crypto-friendly financial entities.

4. Future business operations of FinresPBC will include: minting/redeeming USDP and USDC; earning USD deposit yields in IntraFi savings accounts insured by FDIC; purchasing US Treasury Bonds in separate accounts to earn interest.

5. FinresPBC will disclose asset details, reserve reports, and operational costs monthly. They can provide 24/7 custody asset access for the Frax Protocol and use reserves to buy back and burn FRAX or mint USDP, USDC to send to Frax Protocol AMO as needed.

Regarding the detailed architecture of FRAX V3, official details have yet to be disclosed. However, information gleaned from team discussions on Telegram, forums, and interviews suggest:

1. Sam mentioned that FinresPBC’s operational costs would be significantly lower than Maker or other RWA protocols. If FinresPBC holds $500 million in assets for Frax Protocol, the annual fee is expected not to exceed $200,000.

2. In an interview with Ourodoros Capital on July 28th, Sam mentioned that Frax V3 would be launched within 30 days. Given that FinresPBC and basic banking relationships have already been established, it’s inferred that the RWA business will also launch in August, awaiting DAO proposal voting and initial parameter determination.

3. FraxBonds will be introduced in FRAX V3: Frax Protocol will continuously issue 4 bonds that anyone can purchase. Upon maturity, these bonds will automatically convert to FRAX stablecoins. Through FinresPBC, there’s no limit to the scale of FraxBonds. Furthermore, FraxBonds will be standard ERC20 tokens, and Frax Protocol will deploy liquidity for them on Curve, enabling secondary market trading.

4. In FRAX V3, the Borrow-AMM design targeting FRAX liquidity won’t require oracle price feeds, eliminating oracle risks.

Possible Impacts:

1. The scale of the FRAX stablecoin is currently declining due to the aggressive promotion of RWA business by Maker, especially with Maker’s DSR deposit interest rate now as high as 8%. Some market participants are switching to hold Dai for interest. The reason DSR yields are currently much higher than US Treasury yields is because there’s a discrepancy between Maker’s purchase of government bonds and the interest earned from depositing Dai in the protocol. This high yield seems unsustainable for now. The details of Frax’s RWA business have not yet been disclosed. However, due to its similarity to ETH collateral operations, combined with currently available information, it’s speculated that Frax’s early RWA business will achieve high yields from combined treasury bond yields and Crv incentives, facilitating product launch. In the medium to long term, if, as Sam suggests, the operational costs of FinresPBC are significantly lower than competitors, then Frax’s RWA business may gain long-term competitiveness, helping to increase the market share of FRAX stablecoin.

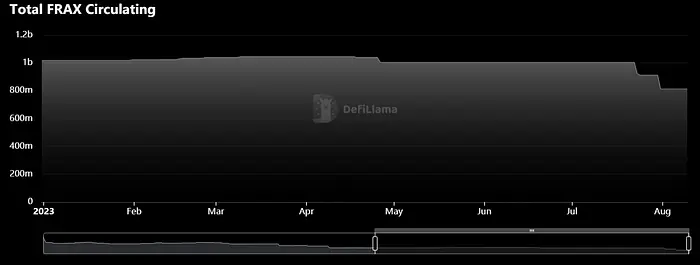

Frax’s market cap recently dropped from 1 billion to 813 million

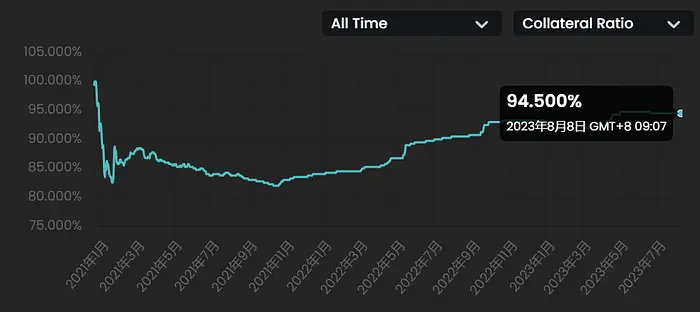

2. Maker has made substantial profits through its US Treasury RWA strategy and has been buying back MKR on-chain, a key factor in the recent MKR price rise. Frax, given its partially collateralized nature for its stablecoin, uses its protocol income to improve the collateral ratio (CR) of the FRAX stablecoin. If the RWA business brings additional income to the Frax protocol, accelerating collateral replenishment, and if protocol revenues are redirected towards veFXS holders or used to buy back FXS, it will support the price of FXS. Currently, FRAX’s collateralization ratio is 94.5%. The Frax Protocol holds 280 million idle USDC. With a 5% yield, this can generate an annual income of 14 million, accounting for 75% of Frax’s current annual income.

The current collateral rate of FRAX is 94.5%.

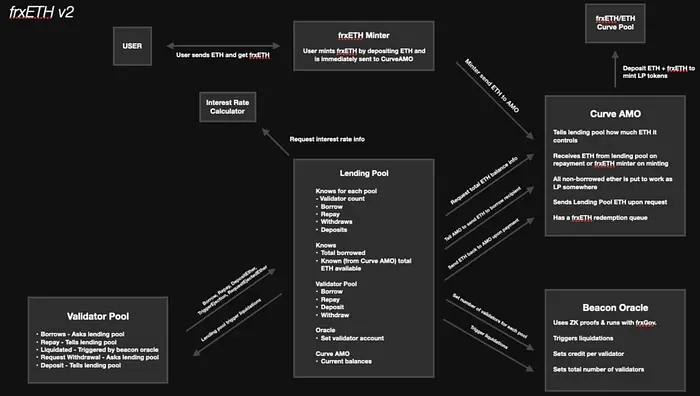

II. frxETH V2 — Focus on Decentralization and Collateral Attraction (launching in 50 days)

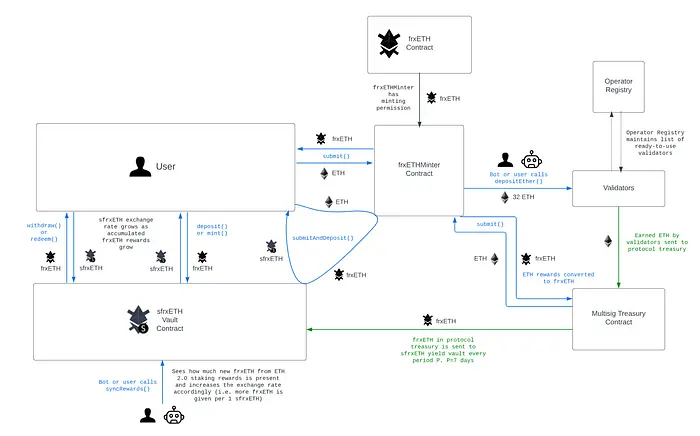

Sam mentioned in a Twitter space that frxETH V2 will launch in about 50 days. In the current frxETH V1, users’ ETH is staked by team-operated nodes, with the protocol taking a 10% fee. The strength of frxETH V1 lies in leveraging its governance power within the Curve ecosystem to effectively direct frxETH liquidity. The dual-token model of frxETH and sfrxETH offers Frax Ether the market’s highest yield. This has allowed Frax Ether, a newcomer, to rank among the top three LSD protocols.

frxETH V1 Staking Flowchart:

In the upcoming frxETH V2 by Frax protocol, the team aims to maintain high annualized returns while addressing centralization issues. The overall design logic of frxETH V2 is similar to Rocket Pool, but with unique features specific to Frax. Key differences include:

1. In Rocket Pool, user-deposited ETH accumulates in a deposit pool, yielding no returns until activated for validation. This can drag down the overall yield of rETH. The deposit pool currently has a cap of 18,000 ETH. In the design of frxETH V2, user deposits are first allocated to Curve AMO and only redirected to the Lending Pool when nodes require user-side ETH pairing. Thus, idle ETH can earn transaction fees and mining rewards in Curve AMO, improving its overall yield compared to Rocket Pool.

2. After Rocket Pool’s Atlas upgrade, the node fee is basically fixed at 14%. In contrast, frxETH V2 plans to determine node fee ratios through market adjustments. In frxETH V1, Frax is among the most efficient and stable node operators in the market, and it will also join frxETH V2 to compete for node fees in a market-driven manner. The introduction of this competitive mechanism, combined with the participation of an efficient team, is expected to further benefit users, providing them with higher returns.

Currently, Frax Ether offers the most efficient staking.

Product Flowchart for frxETH V2

Regarding the frxETH product, apart from focusing on frxETH V2, attention also needs to be given to the launch of the redemption feature. At present, sfrxETH offers the highest yield in the entire market. However, its growth rate over the past month of 4.56% is behind that of Lido’s 5.17% and Rocket Pool’s 7.47%. The primary reason is that frxETH cannot currently be redeemed. It can only be exchanged for ETH in the secondary market via Curve. This has amplified the concerns of large investors and some users, leading them to turn to Lido or Rocket Pool.

III. Fraxchain — Focus on its Ecological Development and frxETH Consumption and Accumulation (Launching at the beginning of 2024)

Fraxchain is a Layer 2 network based on Ethereum. It plans to adopt a hybrid rollup approach (a combination of op rollup and zk rollup). This provides developers with the easy coding environment of op, while offering users the finality, security, and decentralization benefits of zk. As one of the top three LSD protocols, there will be synergies between Fraxchain and frxETH. Fraxchain will use frxETH as its GAS fee, and the resultant holding of frxETH will reduce its conversion to sfrxETH. This will further help the Frax protocol to provide a higher staking yield to compete for market share. In future plans, the complete DeFi product matrix of the Frax protocol will migrate to Fraxchain to reduce Gas and bring initial traffic and funds to Fraxchain. It’s important to note that Fraxchain is not intended to be an application chain. While it supports the current stablecoin ecosystem of Frax, it also aims to expand the ecosystem and enhance adoption to better benefit its native protocol.

In summary, Frax has a streamlined and strong individual combat capability team, with efficient execution and fast product implementation. With the current launches of FRAX V3 and frxETH V2, it deserves corresponding attention.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.