Web3 Must-Read! FSC Digital Asset Accounting Guidelines

Translated by Clara Kim & Lani Oh

Table of Contents

1. Introduction

2. Accounting Supervisory Guidelines

2-1. Token Issuers

2-2. Token Holding Companies

2-3. VASP

2-4. Fair Value Measurement of Digital Assets

3. Mandatory Disclosures of Notes

4. Final Thoughts

1. Introduction

South Korea’s steadily growing interest in Web3 is prompting various listed companies—not only the gaming industry, the OB in the Korean crypto industry—to venture into the crypto asset business. By 2022, these companies raised approximately 79.8 billion KRW through the issuance and sale of tokens, and listed companies held third-party issued tokens with a market value of around 20 billion KRW.

Though crypto assets have increasing impact on the accounting practices of listed companies, there has been a lack of clear guidelines for digital asset accounting treatment in Korea. This is primarily due to the adoption of Korean International Financial Reporting Standards (K-IFRS) by domestic listed companies.

The International Accounting Standards Board (IASB) took a reserved approach in its 2022 five-year plan by excluding the accounting policies for crypto transactions, in contrast to the proactive stance of the U.S. and Japan in issuing accounting guidelines of crypto assets by respectively adopting US-GAAP and J-GAAP. On July 11, the Financial Services Commission (FSC) made a significant announcement that mandates guidelines for crypto accounting and note disclosures. This article explores the key points of this announcement and its potential impact on corporate accounting.

2. Accounting Supervisory Guidelines

The existing international accounting standards only provide accounting treatment standards for holding digital assets. On the other hand, there were no standards for the issuance of cryptocurrencies. As a result, listed companies that issue, distribute, and manage their own tokens had considerable difficulties in accounting in the absence of clear guidelines. Although the new guideline is not a new accounting standard nor a new interpretation, it is expected to resolve accounting uncertainties by providing specific guidelines on issuing and holding digital assets within the scope of international accounting standards.

2-1. Token Issuers

Token sale proceeds received in advance as liability, and recognized as income after completion of obligations

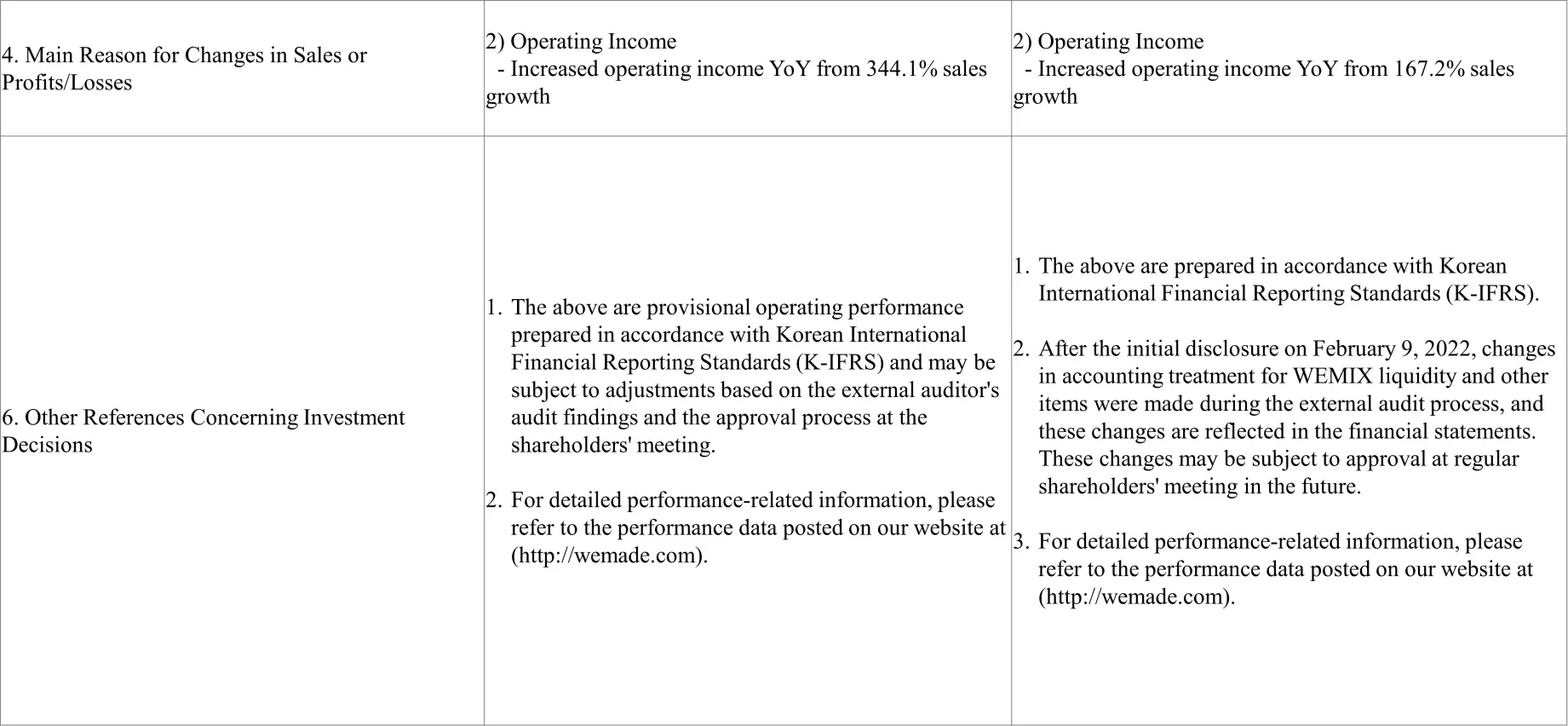

First, when a company sells its own tokens to customers, it is required to recognize the sales revenue as income only after fulfilling all obligations to the token buyers. Even if the payment is received in advance, if the company has not fulfilled all of its obligations, the payment received will be recognized as a liability until after all obligations are fulfilled. As previously mentioned, there was no specific guideline on when an entity should recognize revenue from the sale of its own tokens, which led to disagreements between companies and auditors on the timing of revenue recognition, such as in the case of WeMade's restatement of revenue in March last year—the company excluded KRW 225 billion in WeMix liquidity from revenue and recognized them as a liability.

WeMade’s Correction of Revenue Fluctuation Disclosure, Source: DART

The introduction of this guideline means that the recognition timing of revenue from token sales will be determined by the issuing company's performance obligations, which will be determined by the nature of the token as describe in the white paper. Currently, most of the tokens issued by domestic listed companies are utility tokens, and companies promise to provide services, platforms, etc. that can utilize tokens rather than simply issuing tokens to form the utility of tokens. Therefore, in order for a company to recognize token sale proceeds as income, it must fulfill all the obligations promised in the white paper. By fulfilling the performance obligations, the company can transition from recognizing the token sale proceeds as liabilities to recognizing them as revenue, based on the extent of obligation fulfillment.

Excluding exceptional cases, self-issued tokens are not recognized as assets

As will be discussed in 2-2, Token Holding Companies, companies that hold digital assets will recognize most of them as intangible assets, with some exceptions. Therefore, companies that issue tokens will be subject to the same accounting standards as companies that develop intangible assets. In the intangible asset standards that most digital assets will be subject to, there is a concept called development activities. Some examples are as follows:

- Activities that design, build, and test prototypes and models prior to production or use

- Activities that design tools, jigs, molds, dies, etc. related to new technology

- Activities that design, construct, and operate pilot plants that are not economically feasible for commercial production purposes

- Activities that design, fabricate, and test the final selected design for a new or improved material, device, product, process, system, or service

If the costs incurred to develop an intangible asset qualify as development activities described above, the costs can be capitalized and included in the acquisition cost of the intangible asset. If the costs incurred in the process of developing the intangible asset do not qualify, they are all accounted for as expenses. The same goes for tokens as well. Unless the company can provide clear evidence that the costs incurred in developing and issuing the platform and token constitute development activities under the intangible asset standard, all such costs should be expensed and not included in the cost of the token. Since token issuance can be done with minimal transaction fees, most self-issued tokens are not expected to meet the development activity criteria and will be expensed rather than capitalized.

Also, tokens that are internally reserved after issuance are not recognized as assets. However, in exceptional cases where direct attributable costs arise during the token issuance process, they can be recognized as assets. The supervisory guideline defines utility tokens as those that can generate economic benefits by providing goods and services in the future. Therefore, at the time of development, it is unlikely that utility tokens will meet the definition of an asset as defined by accounting standards. In other words, no issuance costs will be incurred except in very exceptional circumstances. These accounting guidelines seem to aim at preventing developers from inflating token issuance-related costs, capitalizing them, and distorting the financial statements.

2-2. Token Holding Companies

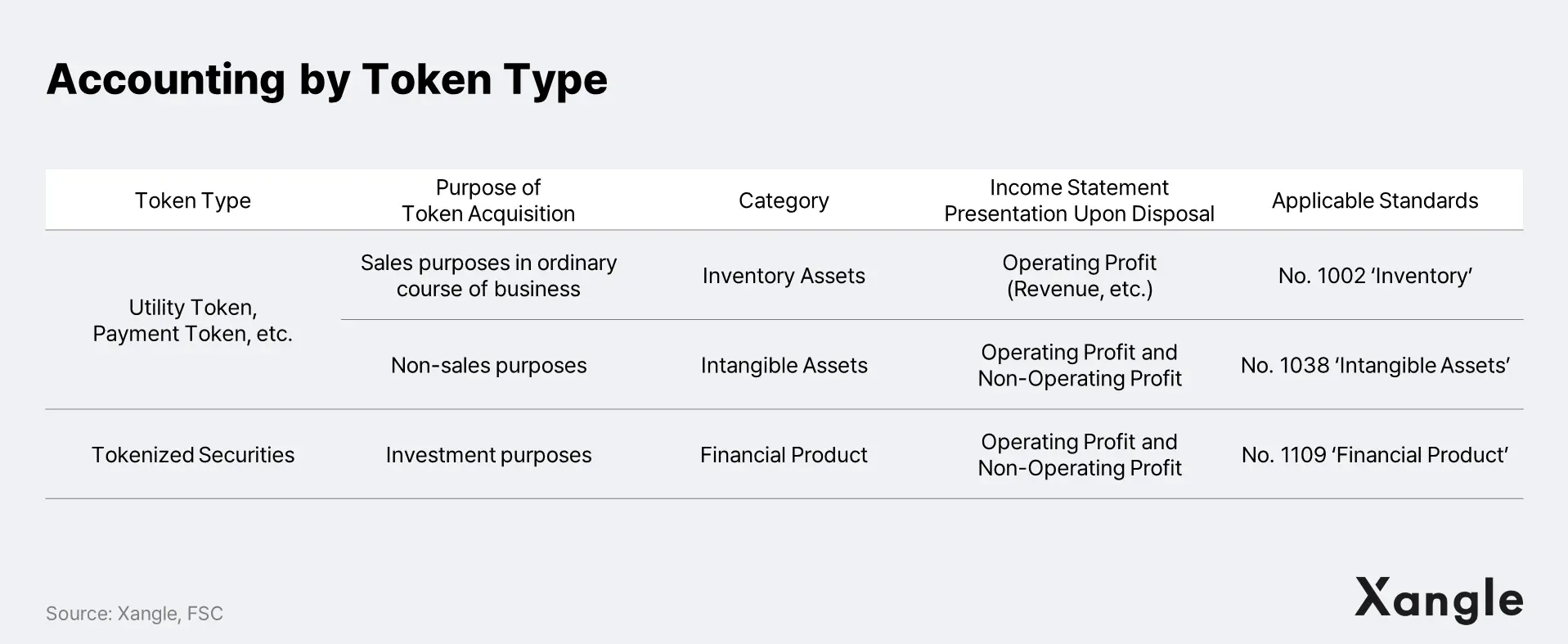

Utility tokens are intangible assets and token securities are financial instruments

In the future, most digital assets, excluding security token, will be treated as intangible assets. Digital assets are classified as intangible assets, except for exceptional cases where they are held for sale in the ordinary course of business. Security tokens are securities governed by securities laws and will be accounted for as financial instruments under the Financial Instruments Standard, just like other securities.

The supervisory guidelines also define the subsequent measurement of tokens held by a company. It can choose to measure a token held as an intangible asset using either the cost model or the revaluation model, similar to the method proposed in existing international accounting standards. However, under the revaluation model, if the fair value of the asset is higher than its cost at the end of a quarter, the company is not required to recognize the increase in price. But the guidelines allow the company to recognize the increase as other comprehensive income. It appears the guideline aims to classify digital assets, except for exceptional cases, and apply the same accounting treatment as other intangible assets to ensure clear and uniform financial reporting.

2-3. VASP

Customer-entrusted digital assets recognized as asset or liability based on economic control

Exchanges, major representative of cryptocurrency businesses in Korea, currently disclose the status of customer-entrusted assets through notes, but do not recognize them as assets or liabilities of the exchange.

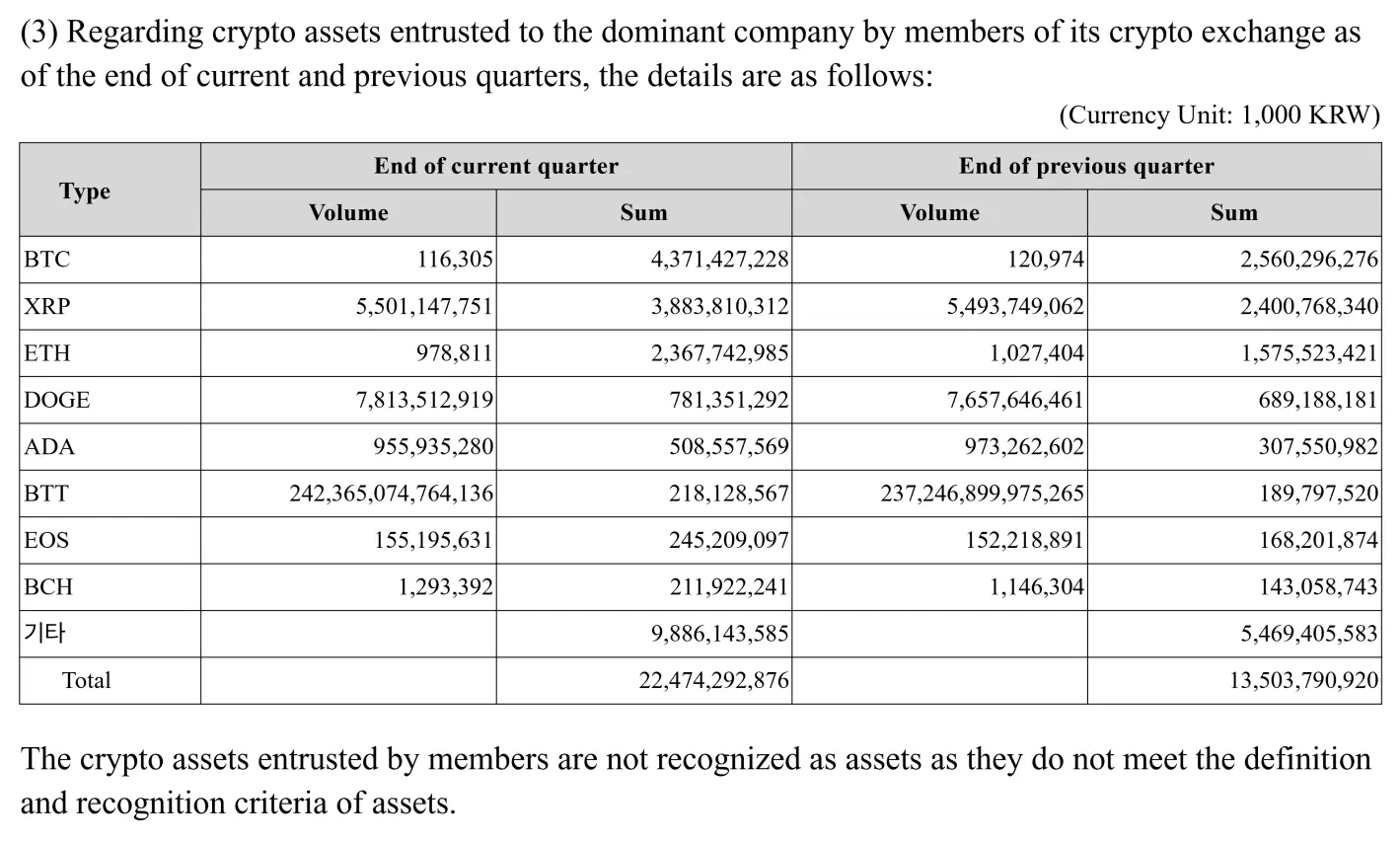

Dunamu Quarterly Report (2023.03), Source: DART

As mentioned in the notes, the reason for not recognizing customer-entrusted assets as assets and liabilities was that these assets did not meet their definition and recognition criteria. On the other hand, Japan and the U.S. already require exchanges to recognize customer-entrusted assets held by crypto exchanges as assets and liabilities of the exchanges from 2016 and 2022, respectively. This is because exchanges are obligated to protect their customers' assets from risks related to cryptocurrencies, so they are required to reflect them in their assets and liabilities. In other words, the decision was made by prioritizing the protection of customers' property rights.

The supervision guidelines clarify that whether a virtual asset service provider should recognize the tokens entrusted by customers as asset or liabilities depends on the economic control over the token. Economic control is defined as the right and ability to direct the use of the digital asset and to gain economic benefits from it. In line with overseas trends prioritizing the protection of customers' property rights, the guidelines also require the determination of economic control to consider the extent of customers’ property rights protected under laws. The determination of economic control is based on a combination of the following criteria:

- Private contracts between the business and the customer

- Laws and regulations overseeing the operator, such as the Virtual Assets Act and the Act on Reporting and Using Specified Financial Transaction Information.

- The scope of management and custody of tokens entrusted to the business by the customer

When it comes to private contracts, several factors come into play, such as whether the ownership of the tokens is transferred to the business, who will benefit in the event of a hard fork, and whether the business is allowed to sell or pledge the deposited tokens.

As for laws and regulations, the focus shifts to whether the law specifies who owns the tokens, the legal rights of customers in the event of the operator's bankruptcy, and whether the customer can withdraw the tokens at any time.

Regarding the management and custody scope of the operator, the focus is on who bears the loss if the private key is stolen in a hack or cyberattack and the tokens cannot be recovered, whether the customer's tokens in custody are stored separately from other customers' assets, and whether the tokens are in a third party custody.

The determination of economic control will vary depending on the specifics of each business and contract. If a business has economic control over the custodial tokens and recognizes them as an asset or liability on its books, it will be held more accountable for safeguarding customer assets. Given the complexity involved in determining the existence of economic control, the Commission is expected to provide further guidelines on the criteria over time.

2-4. Fair Value Measurement of Digital Assets

The fair value will be determined based on the active market (If it exists)

The guidelines state that digital assets will be measured at fair value and provide relevant details to consider.

Generally, if a particular crypto asset has an active market, its fair value will be determined based on the active market. An active market is where assets or liabilities are traded frequently and on a large scale, enabling constant availability of pricing information. To meet this definition, 1) the cryptocurrency must be traded frequently enough to provide continuous pricing information (quantitative assessment), and 2) the data source for that pricing information must be highly reliable, and the cryptocurrency must be exchangeable for fiat currency (qualitative assessment). As a result, price data generated by small liquidity pools on decentralized exchanges or token pools listed exclusively on exchanges with low trading volume will not be used.

Meanwhile, the assumptions for measuring fair value are that: the asset, at the time of measurement, is exchanged i) in an accessible market, ii) either principal or most advantageous, iii) between market participants iv) in arm’s length transactions. Here are the considerations for each element:

- Accessibility: The active market must be accessible for the company. The prices on price data providers’ websites are averages across exchanges, and therefore the assets cannot be traded at those prices. Therefore, they are not considered as accessible.

- Market: The market should have a high trading volume and frequency for the cryptocurrency, allowing it to be sold at the highest price.

- Market participants: Prices formed by related-party transactions or in wash trading are not applicable.

- Arm's length transactions: Prices that are not formed through normal transactions, such as when a seller is experiencing financial difficulties or is selling to fulfill a legal requirement, are not eligible.

The intention behind defining these criteria for active market and fair value measurement appears to be enhancing accounting transparency by preventing accounting irregularities associated with manipulated prices of self-issued tokens with low trading volume.

3. Mandatory Disclosures of Notes

With the adoption of K-IFRS, the significance of note disclosures to the financial statements has grown exponentially. These notes serve as essential supplements to the main body of the financial statements, providing vital information that might be absent in primary sections. They help users of accounting information be better informed of the financial state of the company. As the issuance and holding of digital assets by companies continue to rise, so does their impact on corporate accounting. Consequently, amendments to K-IFRS 1001 "Presentation of Financial Statements" have been introduced, making it obligatory for companies to disclose important information to users of financial statements. This includes the company's accounting policy concerning the issuance and holding of digital assets and their impact on financial statements. In response, South Korea’s Financial Supervisory Service (FSS) has released the following key disclosure rules and best practices for digital assets, providing guidelines for companies to follow.

Disclosure Rules for Token Issuers

Currently, the primary information on digital assets is contained in the white paper, but the accuracy, reliability, and enforceability of the information are not guaranteed. While the guidelines do not mandate disclosing the white paper itself, they do require that the main points in the white paper be communicated to information users through note disclosures.

Firstly, token issuers must disclose development expenses, issuance costs, token sale revenue recognition policies, and reserve or retention policies, as previously discussed in the supervision guidelines. In simpler terms, the disclosure rules mandate transparent disclosure of accounting policies, encompassing the treatment of costs and revenue that arising from token issuance. Additionally, they must disclose essential information about the contract related to the tokens they have issued—mainly the information contained in the white paper—and provide details about the overall business related to digital assets, such as the project’s success, progress, and fulfillment of obligations.

Disclosure Rules for Token Holding Companies

Companies that hold digital assets are required to disclose to investors the potential impact that their cryptocurrency holdings may have. The Financial Services Commission mandates companies to disclose the accounting policies applied to their digital assets, the process of acquisition and price information for each digital asset, and the amount of profit or loss recognized through digital asset transactions.

Disclosure Rules for VASPs

For digital asset operators, the same disclosure rules as token holders extend to the tokens held by the company while there are additional disclosure obligations for customer assets. Virtual asset service providers (VASPs) must disclose the accounting policy as per their economic control of custodial assets. It also requires disclosure of information about customer assets in custody even if the customer has the economic control and they do not recognize the assets on their books. Such information includes the market value of the custodial digital assets, material risks, and risk management activities. In addition, if customer assets are stored in cold wallets or externally, they must provide a description of the type, quantity, market value, and custodian of the assets.

4. Final Thoughts

Several years have passed since listed companies in South Korea have ventured into the crypto market by issuing and holding tokens, but there has been an absence of clear accounting guidelines on digital assets in the country. While the Financial Services Commission's accounting supervision guidelines might have arrived somewhat later compared to the United States and Japan, they have set forth crucial accounting guidelines for token issuers, token holders, and digital asset operators.

The draft guidelines are likely to undergo some revisions in the course of forthcoming consultations with digital asset experts, but the overarching principles are expected to be maintained. The finalization of the mandatory note disclosures through amendments to K-IFRS 1001 will come after deliberations and resolutions by the Securities and Futures Commission (SFC). The accounting supervision guidelines will be implemented and applied to corporate annual reports immediately after finalization whereas the mandatory note disclosures will be applied to the beginning year of the business after January 1, 2024. The expectation is that these supervision guidelines and mandatory disclosures are likely to contribute to a healthier cryptocurrency market by providing comparable and reliable information for accounting information users.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.