The Stablecoin Bridge Almanac (2023)

Written by Arjun Chand and Mark Murdock

Preview

Twitter threads, conference talks, and whispered conversations among those building in the “multi-chain reality” are riddled with all sorts of questions about stablecoin bridges.

Do stablecoin bridges represent the potential solution, or end-game, for interop? Will stablecoins bridges dominate cross-chain volume and render liquidity networks obsolete? Could stablecoin bridges actually complement existing bridges by boosting capital efficiency and improving user experience? Are the trust assumptions that come with relying on centralized stablecoin issuers for cross-chain transactions worth the upgrade in capital efficiency and UX?

This article analyzes these questions by examining different stablecoin bridge designs based on how they work, their benefits, roadmap, adoption rate, and potential risk factors. By providing a comprehensive analysis, we aim to give readers an informed perspective on how stablecoin bridges may shape the future of bridging in crypto.

Let’s dive in!

What Are Stablecoin Bridges?

As the name suggests, stablecoin bridges facilitate the transfer of stablecoins across chains.

Specifically, stablecoin bridges move stablecoins from one chain to another via burn and mint mechanisms controlled by the stablecoin issuer. In other words, a stablecoin bridge is the native (sometimes called canonical) bridge for a certain stablecoin that acts as the single source of truth for minting stablecoins on different chains. This is powerful because having a single entity (centralized or decentralized) in charge of minting a stablecoin enhances capital efficiency for the stablecoin, as there is no longer a need for third party bridges to wrap, lock, or provide liquidity for said stablecoin.

In a way, one can think about stablecoin bridges as systems that ‘teleport’ assets from one chain to another.

Why Are Stablecoin Bridges Being Created?

Stablecoin bridges were developed to address several crucial inefficiencies in the multi-chain reality:

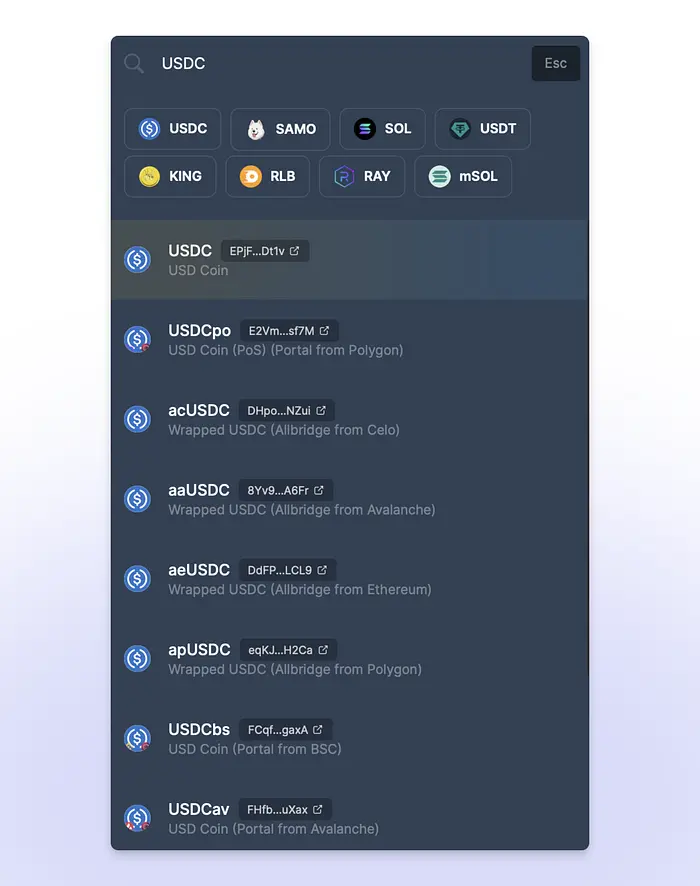

- Numerous wrapped or synthetic versions of stablecoins exist across chains — The existence of multiple wrapped stablecoins on a single chain creates confusion for users and developers, as it can be difficult to identify which wrapped stablecoin is being used for the majority of DeFi activities there. For example, at the time of writing, 11 different versions of USDC exist on Solana’s Jupiter Exchange.

Stablecoin bridges are the single source of truth for what stablecoin should be used for DeFi activities on each chain the bridge supports. This is helpful because it decreases confusion for users and mitigates third-party bridge risk associated with wrapped stablecoins for developers, users, and dApps (which we will go into more detail on below).

- Users need to trust third-party issuers (lock and mint bridges) on different chains — Without stablecoin bridges, users need to rely on third-party bridges to facilitate stablecoin transfers across chains. If these third-party issuers are compromised or paused due to maintenance, it can have severe repercussions for the users in the form of loss of funds and the stablecoin’s reputation. For instance, a compromised third-party bridge could potentially mint an unlimited amount of wrapped stablecoin, leading to substantial losses for users and negatively impacting an entire blockchain. The reliance on third-party entities is eliminated by stablecoin bridges, as users instead depend directly on the stablecoin issuer, which they are already doing by holding the stablecoin initially.

- Evident demand for stablecoins on different chains and industry buy-in — While the availability of wrapped stablecoins on different chains poses UX challenges, it serves as an indication of customer demand for these stablecoins on specific chains. Stablecoin issuers like Circle and Maker have received feedback from large ecosystem participants (Circle’s Joao Reginatto here and dYdX’s Antonio Juliano here) indicating that many chains want to adopt a stablecoin bridge, if possible. Additionally, the heavy use of wrapped stablecoins further validates the necessity of stablecoin bridges and motivates their implementation.

- Liquidity pools are inefficient — One of the common ways stablecoins are moved across chains is via liquidity pool based bridges, wherein (and this is a generalized explanation) bridges incentivize liquidity providers to deposit large amounts of a stablecoin in smart contracts on multiple chains. From there, users who want to bridge stablecoins can do so by paying the LPs a fee to lock and unlock stablecoins from this big pool on their behalf. LP-based bridges are good for users because they allow for users to get exposure to native stablecoins without wrappers. However, incentivizing LPs to deposit stablecoins into a bridge mechanism is expensive for the protocol (and, therefore, the end-user). Additionally, total stablecoin volume is constrained by the amount of a stablecoin found in a certain pool and a certain time.

Benefits of Stablecoin Bridges

The benefits of stablecoin bridges mirror the difficulties listed above. Overall, the ability to mint stablecoins across different chains enables the following:

- Capital efficiency — It is possible to bridge virtually unlimited amounts of stablecoins between chains without having to maintain liquidity pools or rely on wrapped tokens (which require LPs to lock their assets and bridges to not get hacked, respectively).

- Zero fees — Users can transfer stablecoins between chains without incurring any additional fees other than gas fees, as stablecoin bridges eliminate the need for fees paid to LPs and third-party bridges. (Note: stablecoin bridges may implement their own transaction fees, though this is not industry norm as of now.)

- Fungible assets — Stablecoin bridges lets users hold native assets that are fungible with other assets on different chains, as opposed to holding wrapped or synthetic versions of the asset.

- No slippage — Transactions via stablecoin bridges do not experience slippage, which is typically associated with transferring assets on liquidity pools, because there’s no ‘exchange of assets’ here between LPs and users.

- Minimal trust assumptions — Stablecoin bridges are operated by entities that users are already trusting when using a stablecoin, i.e., the stablecoin issuers. For example, users already trust Circle when they use USDC and MakerDAO when using DAI. In other words, the third party risk for a stablecoin is already baked into the minting process of the stablecoin. With that being said, having the stablecoin issuer also manage permissions for cross-chain transactions is still, in our opinion, a somewhat small additional trust assumption.

An Onchain Use-Case

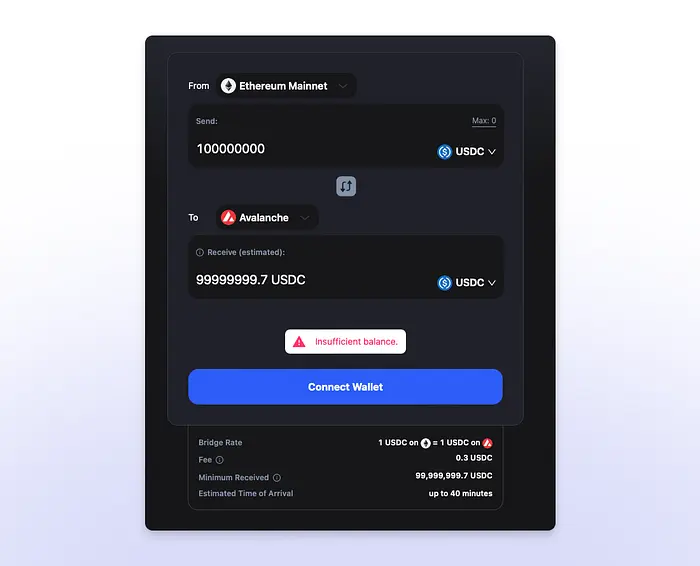

To fully understand the impact of stablecoin bridges, let’s consider a dApp that wants to bridge 100M USDC from Ethereum to Avalanche.

If a dApp wanted to move 100M USDC between Ethereum and Avalanche, no single liquidity pool-based bridge would be able to handle such a transaction. Take Stargate, which has seen the most volume among LP-based bridges this year. Stargate has over $410M in total value locked on the bridge and has handled millions upon millions of transactions in 2023.

However, Stargate’s top liquidity pool for USDC only holds approximately $55M in liquidity (for example, the largest USDC transaction we were able to generate on Stargate’s frontend while writing this article was worth roughly $20,000,000). Therefore, attempting to bridge 100M USDC from Ethereum to Avalanche via Stargate or a different liquidity-pool based bridge is typically not feasible, as there is insufficient liquidity available — forcing a dApp or user to manually bridge multiple times to transfer the required amount.

Alternatively, the dApp could attempt the 100M USDC transfer through third-party bridges that use wrappers (such as Multichain’s anyUSDC or Axelar’s axlUSDC). These bridges essentially allow an unlimited number of tokens to be wrapped onto a new chain at any time — with the tradeoff that said wrapped-token is not guaranteed to have liquidity or usefulness once settled on the destination chain. This makes wrapped USDC alternatives a tough pill to swallow for such a large transaction.

On the other hand, stablecoin bridges, which rely on the stablecoin issuer to lock/burn and mint tokens, theoretically offer a clean resource for large scale stablecoin movements. For instance, by using a stablecoin bridge, a dApp could burn 100M of the stablecoin on Ethereum and mint the same amount on Avalanche as soon as the stablecoin issuer (be it centralized or decentralized) confirmed the transaction. This process ensures that the stablecoin can be seamlessly transferred between the two chains without the need for intermediate steps or complex wrapping procedures.

And this is not theoretical — it’s possible for a dApp to do this now via Celer Network’s cBridge, which has integrated the USDC stablecoin bridge CCTP.

This is made possible because cBridge utilizes CCTP’s burn and mint mechanism as the underlying mechanism for facilitating the transfer with a ‘base fee’ of 0.3 USDC. This fee is applied to cover the gas cost associated with the transaction, regardless of the transfer amount.”

So What Do Stablecoin Bridges Mean for Other Bridges?

Contrary to the initial expectations of Crypto Twitter, the advent of stablecoin bridges doesn’t necessarily indicate the end for liquidity pool-based bridges.

While stablecoins make up a large portion of bridging volume, they are not the sole assets users want to bridge. Native tokens like ETH, MATIC, SOL and other bluechip assets like BTC also comprise a significant portion of historical bridging volume, thereby even if stablecoin bridges end up taking 100% of the share of bridging of their token, there’s a sustainable case for liquidity-pool based bridges.

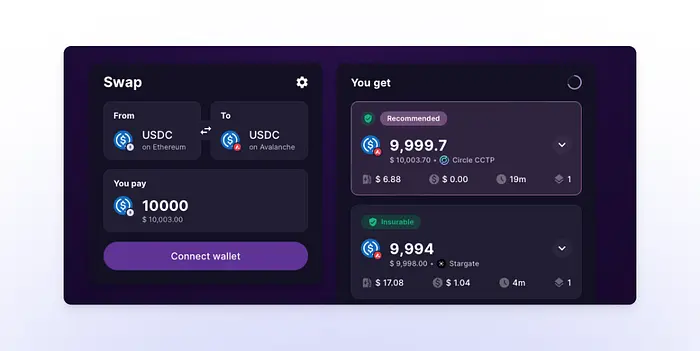

However, it’s unlikely that stablecoin bridges will make up 100% of bridging volume. For example, stablecoin bridges, due to their finality requirements, are slower compared to liquidity pool bridges. For example, in the scenario below, transferring 10,000 USDC from Ethereum to Avalanche can be done at a lower cost via Circle’s CCTP. However, this route is slower compared to liquidity-pool based bridges like Stargate.

With CCTP, users need to wait for finality confirmation on Ethereum before they can bridge their funds, whereas with Stargate LPs can front the liquidity instantly without waiting for finality confirmation. This preserves the value proposition of speed that liquidity pool bridges offer.

In addition to liquidity pool-based bridges, there is also a way to survive for wrapped-asset based bridges like Multichain due to systemic arbitrage. For example, if Multichain can move fast enough and deploy endpoints on a new chain before a stablecoin bridge supports that chain, Multichain could see stablecoin volume through their bridge during the period before the stablecoin bridge launches support there.

Moreover, it is worth noting that native bridges have been present in the ecosystem from some time that provide comparable cost-to-speed trade-offs, characterized by low cost but slow execution, similar to stablecoin bridges. Despite that, liquidity-pool based bridges continue to play a vital role in the ecosystem

In fact, stablecoin bridges can benefit liquidity-network bridges by enhancing their capital efficiency. This is best illustrated by the example by the Across team:

“In the optimistic roll-up case, we currently rely on the 7 day canonical bridge to move funds back from L2 to L1 to keep our pools at their targets; we expect that stablecoin proprietary bridges will have a much quicker bridge time than some of the canonical bridges (especially L2->L1, as evidenced by the speed of CCTP) and we can use these proprietary bridges without introducing any additional security assumptions since users are already holding the token.”

Moreover, stablecoin bridges will remove the burden of fees paid to LPs for maintaining liquidity.

This, in turn, allows bridges to allocate their revenue more effectively and redirect it to other areas. For instance, for bridges that compensate LPs with their own tokens (e.g, Stargate with $STG), this would result in reduced emissions of the STG token to pay out LPs, benefiting both the protocol and its tokenholders — by reducing reliance on the emission of new STG tokens into circulation, the functioning of the protocol becomes less dependent on this mechanism. Bridges could also choose to redirect token emissions to other pools, thereby incentivizing deeper liquidity for non-stablecoin assets.

We anticipate that in the future, liquidity pool-based bridges will integrate stablecoin bridges like CCTP and Maker Teleport, replacing the liquidity pools for the stablecoins, resulting in substantial cost savings on liquidity maintenance (we’re already seeing this being done by bridges like cBridge).

Although this vision is currently constrained by the limited number of supported chains by most stablecoin bridges, we expect that as stablecoin bridges make progress on their roadmaps and expand connectivity across various chains, integrating them will become a no-brainer for any liquidity-pool based bridge. This development could have several positive outcomes for the ecosystem as a whole:

- Stablecoin bridges would witness increased adoption, leading to an expansion of stablecoin supply — a win for stablecoin issuers.

- Liquidity pool-based bridges could reduce their expenses and become more capital efficient by eliminating the need for maintaining liquidity for stablecoins through LP fees.

- LPs of liquidity-pool based bridges can use stablecoin bridges to rebalance assets on different chains.

- Users would benefit from more cost-effective and in some cases (depending on the chain’s finality times), faster bridging of stablecoins, enhancing their experience.

- Bridge aggregators, such as LI.FI, would benefit from reliable, low-cost, and efficient routes for stablecoins (currently the preferred assets for bridging activities). For example, USDC has accounted for 37% of cross-chain transactions at LI.FI since 2022.

- dApp developers would be able to leverage stablecoin bridges through aggregators and messaging protocols to build cross-chain experiences with stablecoins.

In the long run, the emergence of stablecoin bridges and bridge token standards like LayerZero’s OFTs may have the potential to reduce the prominence of liquidity pool-based bridges as they have clear benefits for the overall ecosystem. However, it is important to note that liquidity pool-based bridges will remain relevant within the multi-chain ecosystem due to their notable advantages in terms of asset support flexibility and speed. Thus, while their influence may be somewhat diminished, liquidity pool-based bridges will continue to serve a valuable role in facilitating seamless cross-chain transactions.

Closing Thoughts

Stablecoin bridges are a noteworthy innovation holding the potential to bring significant benefits to the crypto ecosystem and shape the future of how assets are bridged across chains. As these solutions mature and become more comprehensive, we expect them to witness substantial adoption, benefiting both stablecoin issuers and the overall ecosystem. Like with Circle and CCTP, we see a future where many stablecoins will adopt a burn-and-mint mechanism to control their stablecoin supply across chains, enabling native availability and transferability across multiple chains. However, rather than all stablecoin issuers developing their own stablecoin bridging solutions, there is a strong possibility of them leveraging bridge token standards to achieve similar advantages, much like how Abracadabra decided to utilze the OFT standard.

We foresee a future where asset-based bridges (stablecoin bridges for stablecoins and other assets leveraging token bridge standards offered by the many messaging protocols) and liquidity-pool based bridges benefit from each other, and improve efficiency of asset flows across the multi-chain ecosystem.

Ultimately, we believe that for user-centric bridging protocols, it will effectively come down to which front-end is able to attract the most users. Right now, this ability greatly varies across bridges depending on fees, liquidity, slippage, tokens, chains, etc. But, in the future, as burn-and-mint mechanisms gain adoption across multi-chain assets, these differences would likely be mitigated, leading to competition among bridges and bridging-related interfaces based on factors like user experience and convenience. In this regard, we believe aggregation protocols like Jumper.Exchange possess a notable advantage due to aggregation superpowers, positioning them as the preferred platform for users requiring fund bridging. This enables them to build strong user retention strategies by becoming the hub for all bridging activity.

Note: Currently, bridge aggregation protocols have not been able to establish this dominance as bridges like Stargate continue to maintain a significant share of volume and user adoption in the bridging niche.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.