Rising from the Depths: Resurgence of First-Gen Lending Protocols

Image source: The Powerpuff Girls

Table of Contents

1. DeFi Lending Sector Attempting to Move Up From the Bottom

2. MakerDAO - Linking Real World Assets to DeFi

3. Aave - Solid Revenue and Strong Fundamentals

4. Compound - Constant Product Innovation

5. Increased Interest from TradFi Institutions: A New Momentum

1. DeFi Lending Sector Attempting to Move Up From the Bottom

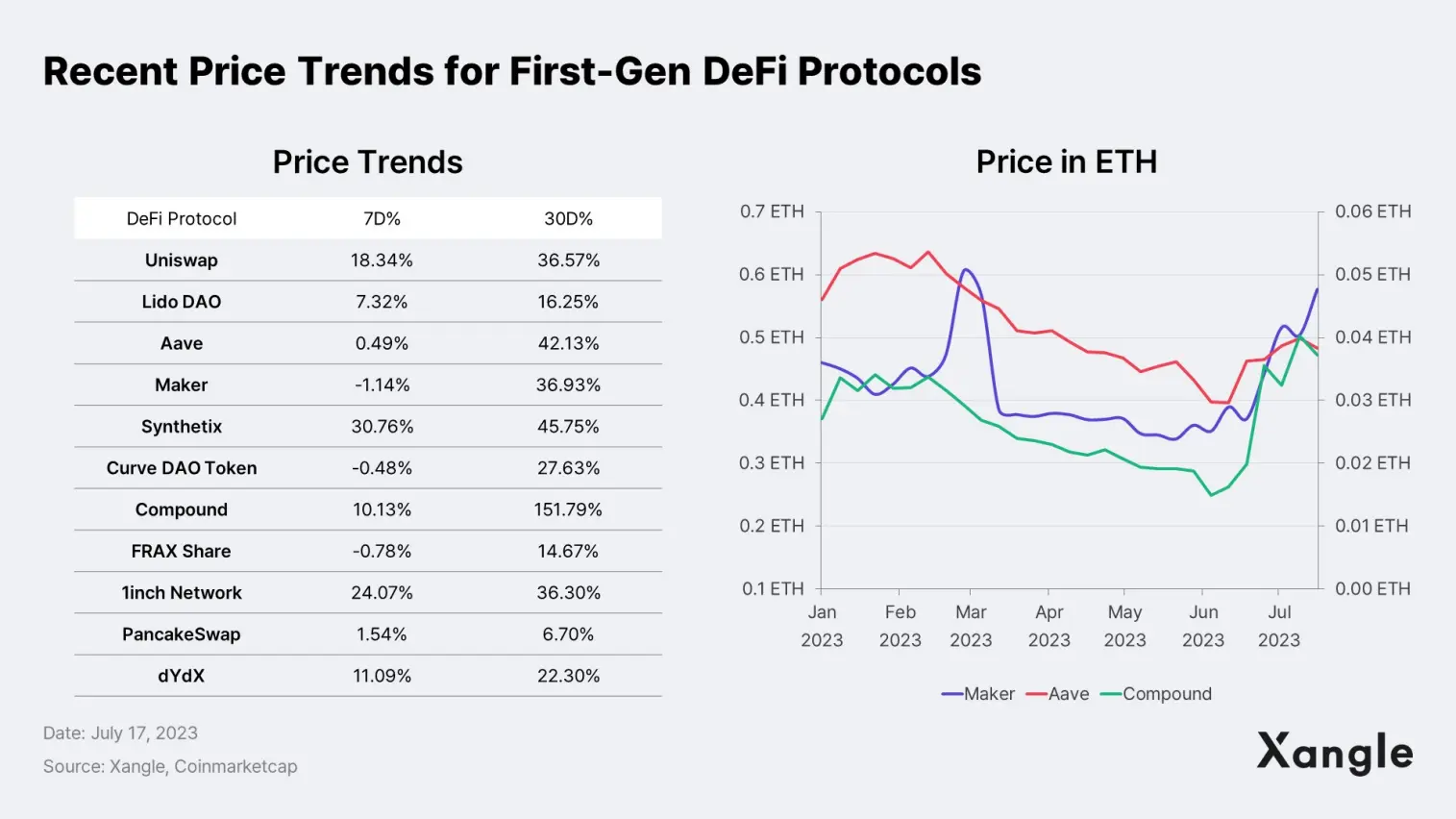

The first-generation DeFi projects that burst onto the scene around June 2020 marked the beginning of the DeFi Summer. But the boom in DeFi was rather short-lived as their prices began to plummet by more than 80 percent since a blazing streak of all-time highs in the first half of 2021. In an unexpected turn of events, however, prices of major first-generation DeFi projects have been rising sharply in recent months. Lending protocols have been the fastest-growing sector, with MakerDAO up 36.93% in the last 30 days, and Compound up 151.79% over the same period. Since June, 2023, the price of the main first-generation lending protocols in ETH terms has also been rising, indicating even faster price growth compared to Ethereum.

So what’s driving the attention towards first-gen DeFi lending protocols? In 2021, the crypto market was on fire, and many DeFi projects promised high APRs, only to fade away in less than a year. Since their APRs were tied to governance tokens issued by the protocols, rather than interest rates or transaction fees, falling governance token prices meant falling interest rates. These governance tokens had no other utility, the arrival of the bear market sent the token prices tumbling, leading to a steep decline in both interest rates and TVL.

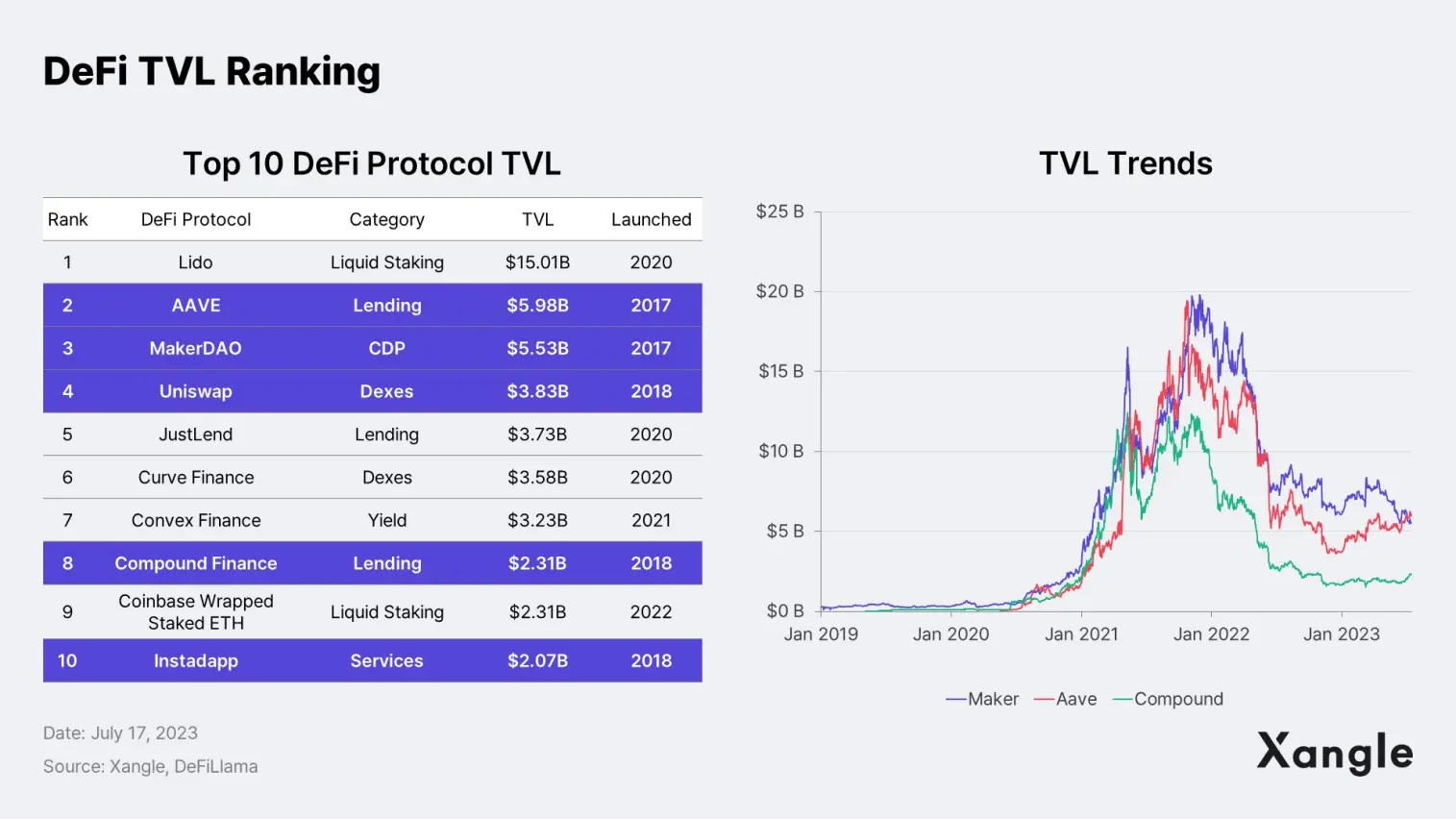

Given that the total TVL of DeFi sits at $44.4 billion as of July 17, 2023, about one-third of its peak in May 2022, it may be premature to predict a full-fledged recovery of the market. Yet, the TVL ranking of major DeFi projects reveals that eight of the top 10 protocols with the most locked-up assets were launched before 2021, and four of the top 10 were launched before 2019. This suggests that first-generation DeFi protocols that have stood the test of time are still very much alive and well in the DeFi market.

In the end, projects that failed to generate stable revenue faded away, while those that managed to secure funding based on real yields survived. Already, the first-generation DeFi protocols have established themselves as the infrastructure of the DeFi market and are well funded thanks to their high revenue.

2. MakerDAO - Linking Real World Assets to DeFi

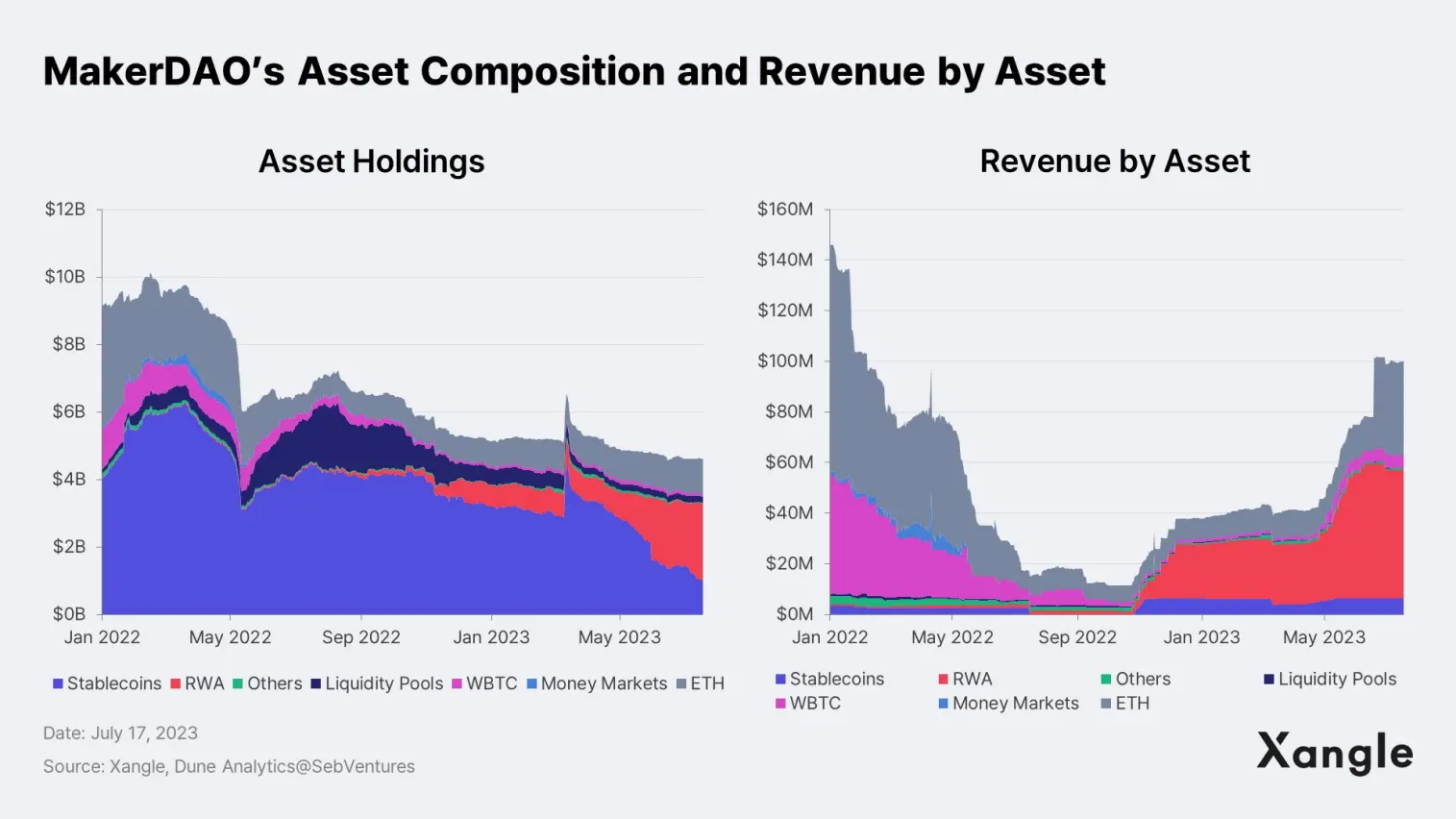

MakerDAO has rapidly increased its protocol revenue by incorporating real-world assets (RWAs) into its holdings. Currently, RWA accounts for approximately 49.4% of MakerDAO's holdings and 50.8% of its revenue, and is expected to generate 87.09 million DAI in revenue this year alone. RWAs refer to assets that exist off-chain but are tokenized on-chain, such as real estate, gold, dollars, government bonds, and corporate bonds.

MakerDAO has added RWA to its assets to 1) reduce its reliance on $USDC as collateral and 2) increase the market capitalization of $DAI. Basically, MakerDAO issues stablecoins in an overcollateralized manner, which comes with the cost of asset efficiency. The overcollateralization has restrained the market capitalization of $DAI since increasing the circulating supply of $DAI requires more assets to be pledged as collateral. To address this, in 2020, MakerDAO introduced the Peg Stability Module (PSM), allowing users to swap stablecoins ($USDC, $USDP, $GUSD) for $DAI at a 1:1 ratio without incurring any cost. Since the swap price between stablecoins and $DAI is set at $1 in the PSM module, there is a strong incentive to arbitrage when the $DAI price deviates from $1. This has led to a steady increase in the proportion of stablecoins in MakerDAO's reserve, especially $USDC, eventually resulting in 1) a reduced protocol revenue and 2) an increased counterparty risk of $USDC issuer Circle. This is also evident in the chart above, where MakerDAO's stablecoin share is quite high in the asset holdings but low in terms of revenue generated by each asset. In addition, as was evidenced during the SVB crisis, $USDC depegging led to $DAI depegging, laying bare that $DAI's reliance on centralized stablecoin collateral—no matter how it aims to become a decentralized stablecoin—inevitably inherits the risk of a centralized entity.

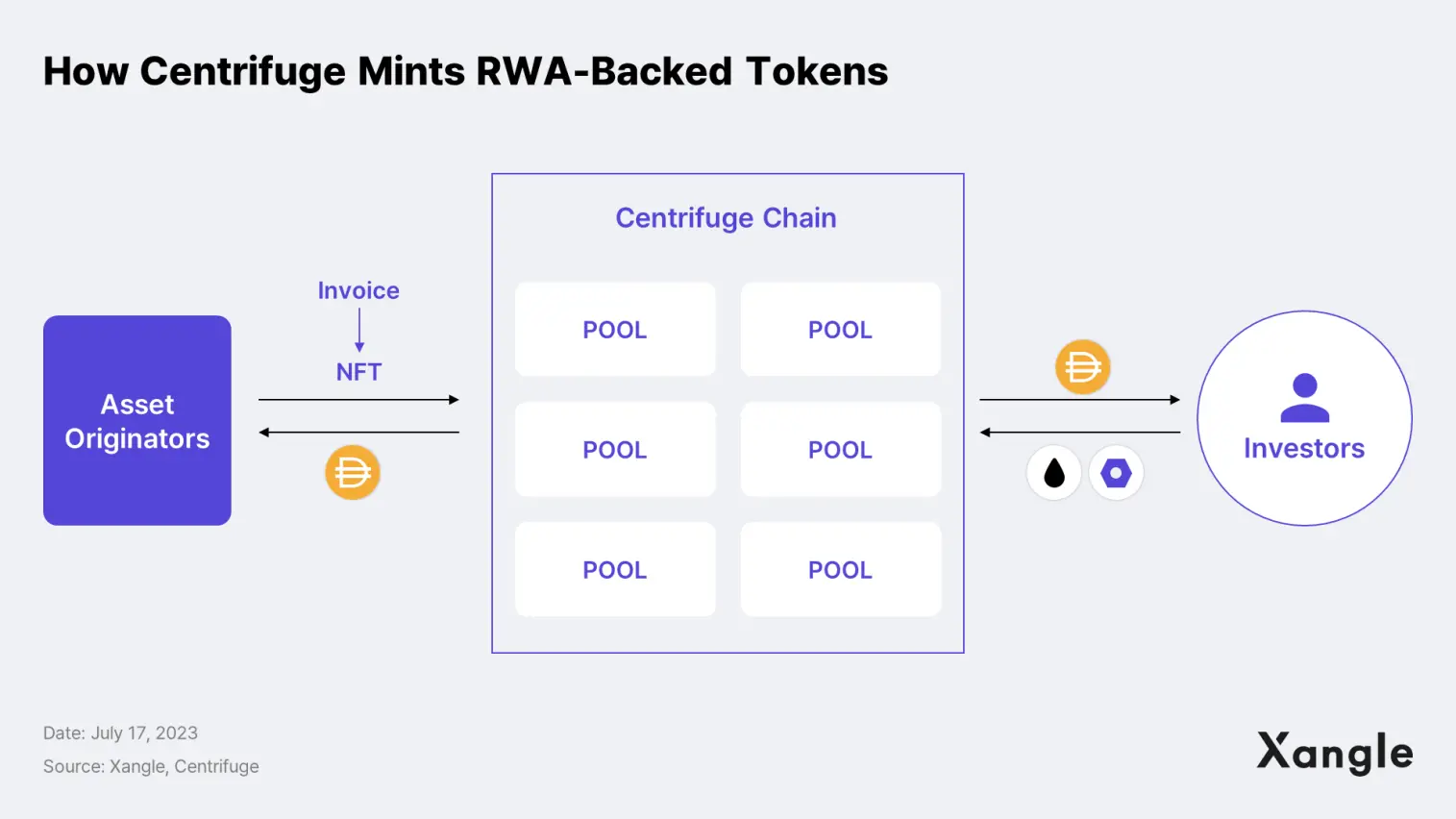

In response, MakerDAO implemented an aggressive growth strategy in March 2022 and began operating a Vault where $DAI can be borrowed against RWA tokens created through Centrifuge. MakerDAO has increased the use of $DAI and protocol revenue by issuing loans in the form of $DAI to financial institutions investing in real estate and infrastructure projects. At the same time, it has kept the default risk of the loans below the interest rate offered to users in a bid to mitigate default risk and ensure the stability of $DAI’s peg. By adhering to this principle, MakerDAO strived to minimize the likelihood of a large-scale liquidation or bankruptcy.

In mid-June this year, driven by stable revenue generation, the MakerDAO community voted to raise the DAI Savings Rate (DSR), the rate of return for holding and lending DAI, from 1% to 3.49%. The decision was well-received by the community, with the MKR token price climbing by over 5%. With a 3.49% interest rate surpassing the mid-2% rate currently offered by Aave and Compound, MakerDAO is expected to attract significant funds.

In addition to stable fundamentals, MakerDAO has evolved since its inception by continuously developing and upgrading features of its existing model and launching new products. Such efforts have translated into increased revenue and TVL, creating a virtuous cycle.

In May 2023, MakerDAO launched the Spark Protocol, a lending protocol like Aave/Compound, for wider use of DAI. Through Spark Protocol's credit line called DAI Direct Deposit Module (D3M), users can borrow DAI at a lower rate than what used to be their go-to lending platform, Oasis, while enjoying a higher loan-to-value (LTV) for loans between assets that share an underlying asset (e.g. DAI-USDC-USDT). While the TVL stands below $50 million, these advantages are expected to draw an increasing number of DAI holders to the Spark protocol as it gains recognition. Once it starts to absorb some of the revenue previously directed to other lending protocols, MakerDAO's financial health will improve further.

3. Aave - Solid Revenue and Strong Fundamentals

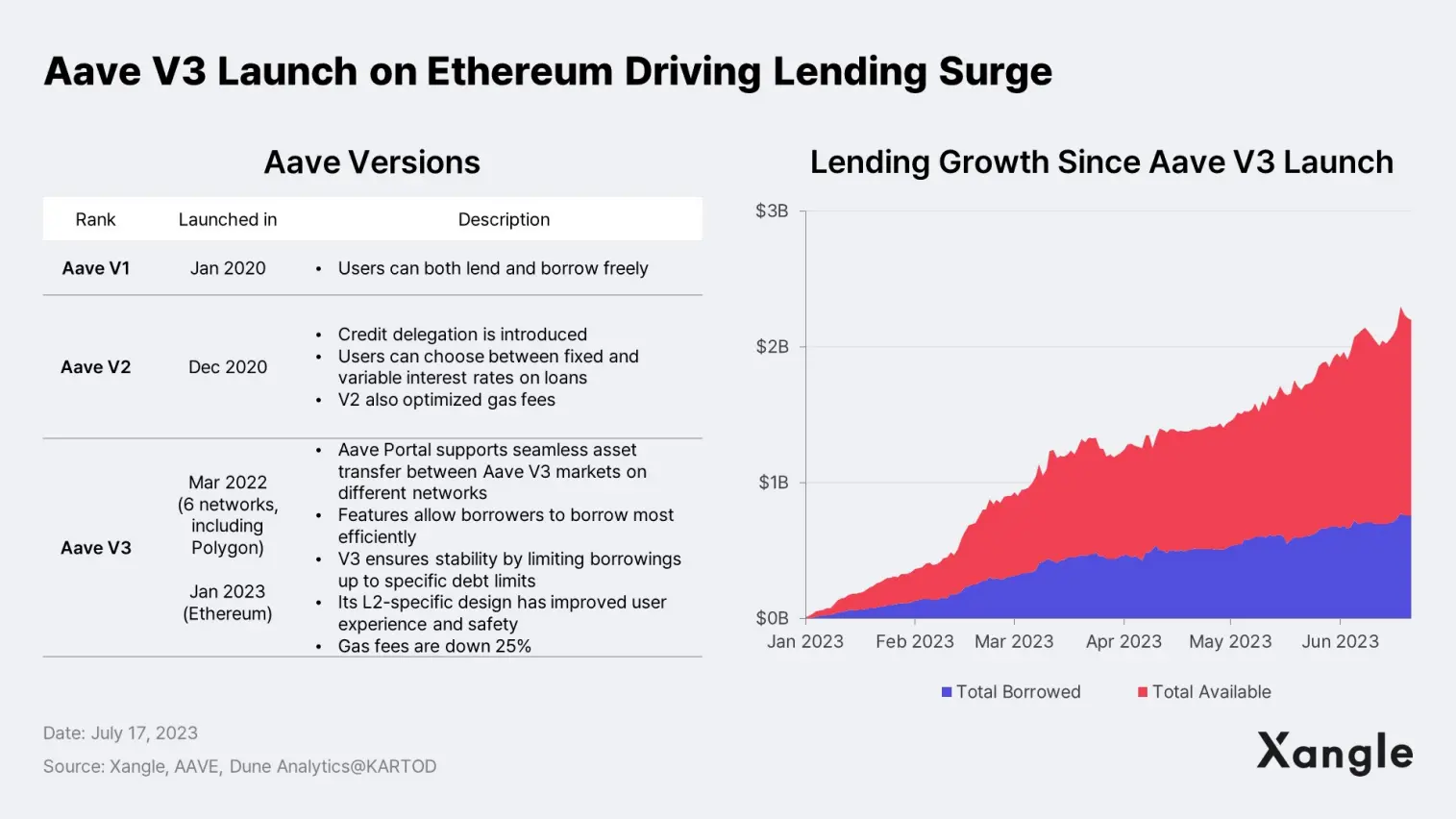

Aave has maintained stability with solid revenue and ongoing protocol updates. In January 2023, it launched Aave V3, improving capital efficiency and protocol stability. With this update, users can borrow more by providing collateral correlated to their deposited assets via E-Mode, borrow assets using only one asset as collateral, and save up to 25% on gas fees for all features. As a result of the Aave V3 launch and Arbitrum’s airdrop in Q1 2023, Aave’s TVL has surged by 59%, increasing from $3.7 billion as of January 1, 2023 to $5.9 billion as of July 24, 2023.

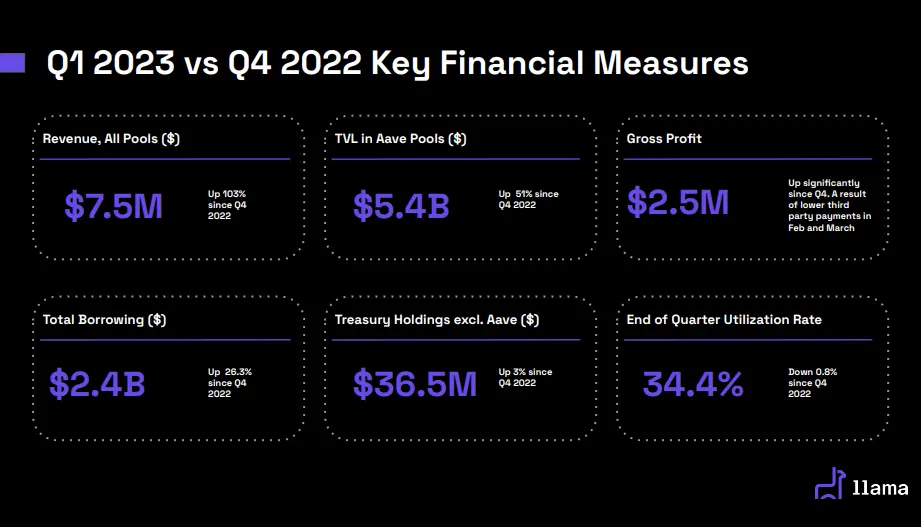

Alongside this, Aave saw a substantial increase in its revenue, reaching $7.5M in Q1 2023, a staggering 103% surge compared to the previous quarter. Its gross profit also shot up in February and March 2023, amounting to $2.5M, thanks to reduced fees paid to third parties. Driven by the increased quarterly revenues, Aave’s cash flow has turned positive.

In response to the steep decline in TVL following the Terra-Luna crash, Aave held a governance vote in July 2022, leading to the introduction of a new decentralized stablecoin called GHO. On July 16, 2023, GHO was launched on the Ethereum mainnet. Unlike other stablecoins, GHO allows Aave to retain all interest revenue without having to share it with depositors. Considering that an estimated 78% ($145 million) of Aave's interest revenue came from stablecoins in 2022, the launch of GHO is expected to significantly bolster the company's profitability, even by capturing only a fraction of the demand for stablecoins.

4. Compound - Constant Product Innovation

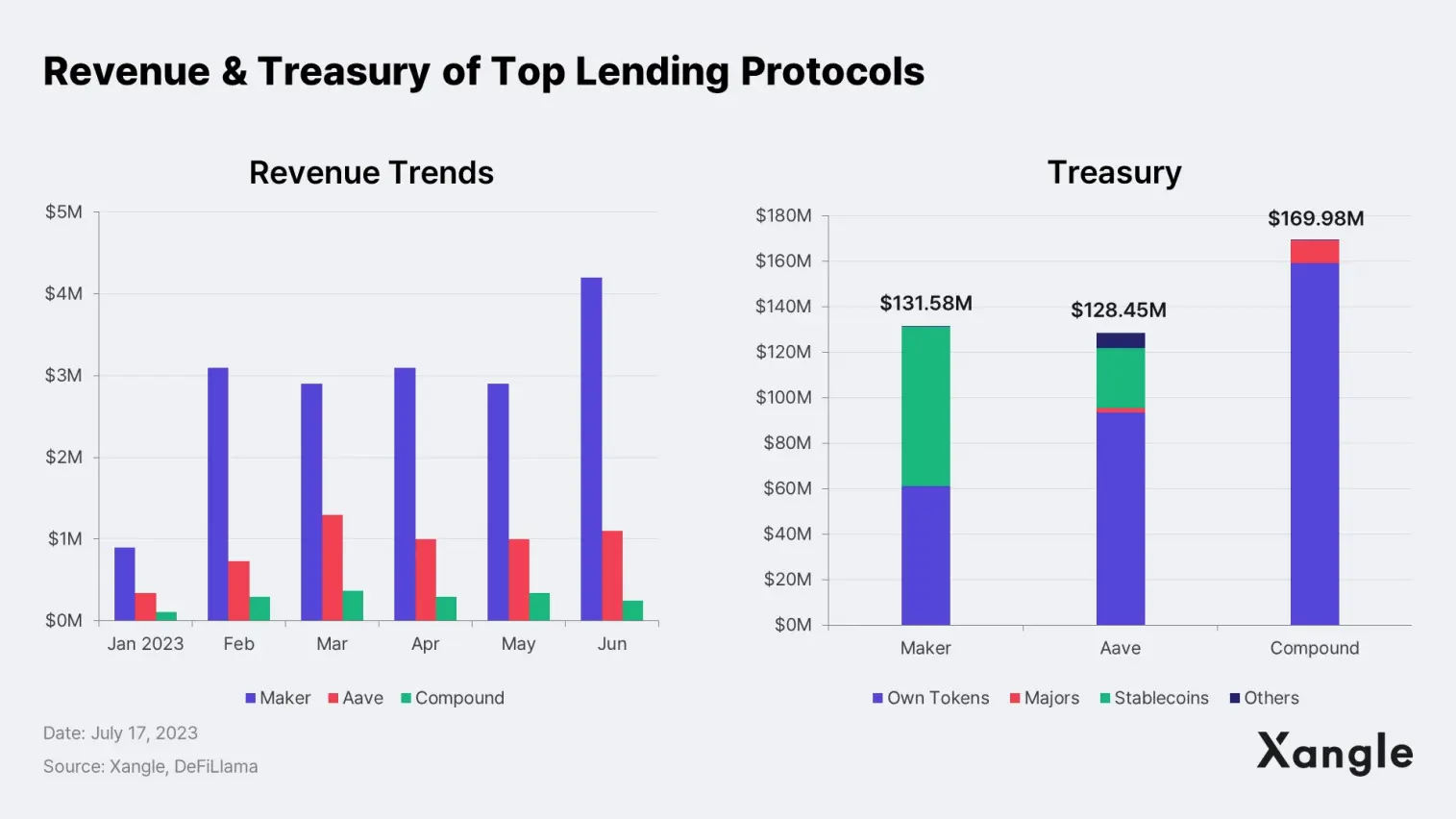

Among major first-generation lending protocols like MakerDAO and Aave, Compound's revenue remains relatively low, generating around $200K monthly with over $1M in $COMP tokens distributed as incentives. However, Compound stands out with the largest treasury among the three protocols, allowing it to secure ample funds for development. Considering their own token holdings, Compound's treasury holds $169.98 billion, surpassing MakerDAO's $131.58 billion and Aave's $128.45 billion.

Similar to Aave, Compound rolled out V3 on August 26, aiming to improve the protocol's security, capital efficiency, and user experience. The most notable change in Compound V3 is the shift away from borrowing assets from a pool of mixed assets to allowing users to borrow only one "base asset." USDC serves as the base asset, while ETH, COMP, LINK, UNI, and WBTC are accepted as collateral.

The strategic move by Compound aims to safeguard users' assets: In the past, pooling multiple assets together could create bad debts if the price of a single "bad asset" dropped, jeopardizing the whole system. Still, the heightened security comes at a cost. While Compound V3 doesn't offer interest on deposited assets other than the underlying asset, and the underlying assets act only as collateral for loans, users can earn interest by supplying low-risk underlying assets.

Although the yield on USDC deposits has risen to at least 3% since the launch of V3, the impact on TVL has been minimal. Since August 2022, Compound's revenue has remained low-key, and its Arbitrum and Polygon distribution strategy hasn't had a substantial impact on revenue either. Hence, the recent surge in $COMP price and TVL cannot be credited to Compound's product enhancements. Instead, it appears to be driven by the anticipation surrounding the association of the $COMP token with Superstate, the venture recently launched by Compound's former CEO.

5. Increased Interest from TradFi Institutions: A New Momentum

1) Bridging the Gap with Traditional Finance

In addition to their regular protocol updates, lending protocols are actively engaging with the traditional financial sector by tokenizing traditional assets on-chain and offering services for traditional institutions.

- MakerDAO has been generating high revenue based on RWA, and 49% of its assets are collateralized by RWA.

- Aave launched Real World Assets (RWA) Market in December 2021, providing a real-world asset-backed lending service. Aave Arc, introduced in January 2022, became the first enterprise-only crypto lending service among major DeFi protocols. In November, a trade conducted by JPMorgan on the Polygon blockchain utilized a modified smart contract on the Aave protocol.

- Compound launched Compound Treasury in September 2022, a service that provides loans to traditional institutions. Compound Treasury was the first blockchain service to receive a B- rating from S&P. Also, in June, Compound founder Robert Leshner announced the launch of Superstate, a new venture to create regulated financial products that bridge traditional financial markets and the blockchain ecosystem. Superstate filed a preliminary prospectus with the U.S. SEC for the Superstate short-term treasury fund.

The 145.99% surge in $COMP price over the past 30 days can be partly attributed to the excitement surrounding its use in the new protocol. The market is keen on exploring the integration of traditional asset classes with blockchain, and the tokenization of traditional assets is expected to significantly expand the DeFi market.

2) DeFi Advantages: Cutting Overheads, Promoting Collaboration, and Making Finance More Accessible

According to Oliver Wyman, 88% of global institutional investors are already acquainted with digital representations of cash using blockchain-based technologies, and 91% are interested in investing in tokenized assets. Institutional investors expect DeFi adoption to 1) reduce overheads, 2) open up collaboration possibilities as transactions are recorded on a single ledger, and 3) improve access to financial assets.

Blockchain has the power to address these inefficiencies by recording transaction and ownership information on a single ledger. This means multiple parties can share and reconcile same information without intermediaries, making transactions more reliable and efficient. Additionally, tokenized assets tradable on the blockchain opens doors for seamless collaboration between companies. Imagine a tokenized asset issued by JP Morgan being deposited into a DeFi protocol created by UBS. Moreover, blockchain can revolutionize access to assets in other countries by overcoming the limitations of traditional financial instruments, which are often confined to within a country's borders. This enhanced access to assets will be particularly beneficial for developing countries, where the adoption of CBDCs is progressing more rapidly than in developed countries to address the lack of financial infrastructure and bring the financially excluded into the financial system.

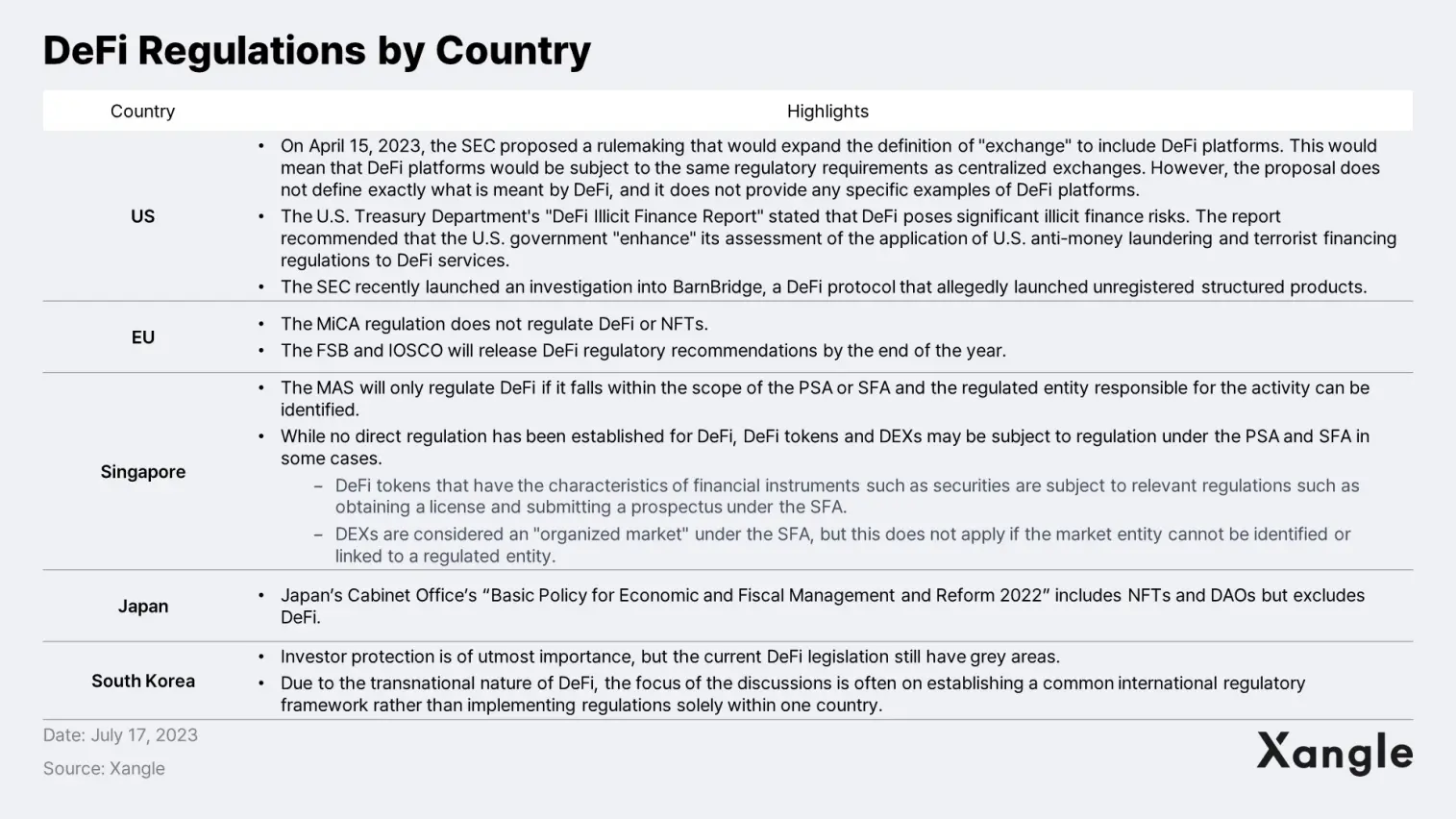

3) Regulation, a Prerequisite for Greater Institutional Participation

That said, it seems evident that the open floodgates of institutional participation will likely be preceded by due rules and regulations. The Terra-Luna implosion highlighted the importance of regulating DeFi, yet comprehensive DeFi regulation remains a work in progress. The decentralized nature of DeFi transactions, where smart contracts allow users to directly engage in financial activities on blockchain networks presents unique challenges in determining responsibility and applying traditional financial regulations. These intricacies underscore the need for continuous research on DeFi.

DeFi projects are bringing traditional assets on the chain to provide users with safer and more lucrative opportunities. Still, many traditional financial institutions remain cautious mainly due to regulatory uncertainties as BlackRock, the world's largest asset manager, once pointed out. Largely, the hesitancy stems from the highly regulated nature of traditional finance, which stands in contrast to the underregulated DeFi.

Yet, once the challenges associated with privacy, anti-money laundering (AML), and know-your-customer (KYC) are resolved, the first generation of DeFi protocols look well-positioned to gain momentum. Though traditional financial institutions might develop their own proprietary systems, the greater likelihood is that they may use existing protocols, like JPMorgan’s use of a fork of Aave Arc, to expedite parallel development and reduce the time and cost involved in creating new services (Source: Oliver Wyman, Institutional DeFi). Once regulations are in place and the stage is set for institutional investors to enter the DeFi space, the first-gen DeFi protocols may walk back into the spotlight.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle Valuation Series] ④ Lending Protocol](https://resource.xangle.io/content/thumbnails/711/content_711_thumbnail_adb18197.webp)