Xangle In-House Attorney's Analysis of the Ripple Ruling

Table of Contents

1. Progression of the Case

2. SEC's Arguments and Court's Decision

3. Implications of the Ruling

On July 13, 2023, the U.S. federal court rendered its ruling in the prominent legal battle known as the "SEC vs Ripple" lawsuit. This watershed moment is not only reverberating around the cryptocurrency market but is having far-reaching consequences in the stock market. This analysis will examine the progression of the case, the court's decision, and the resulting implications.

1. Progression of the Case

On July 13, 2023, the long-awaited conclusion was reached in the Ripple case, which had been widely viewed as a potential milestone to set a crucial precedent for the security status of digital assets. (Click here to read the Court’s judgment in full)

The lawsuit was initiated in December 2020 when the U.S. Securities and Exchange Commission (SEC) filed a complaint in the U.S. District Court for the Southern District of New York against Ripple Labs, Inc., its issuer, as well as its former and current executives, Bradley Garlinghouse and Christian A. Larsen. The SEC alleged that Ripple (XRP) was an illegally sold security. Ripple, on the other hand, argued that XRP is a commodity and not a security. Despite both parties filing motions for summary judgment, the case was drawn out for nearly 30 months, with the central point of contention being the question of whether Ripple should be classified as a security.

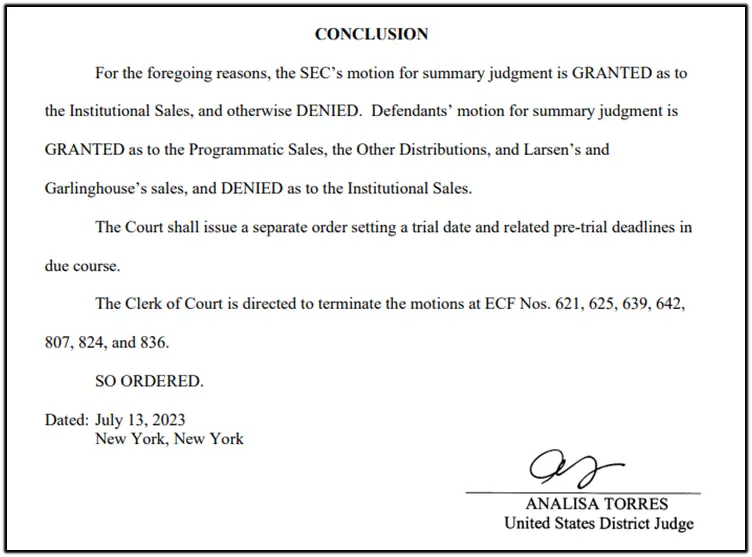

In her ruling, Judge Analisa Torres GRANTED the Plaintiff's (SEC) motion for summary judgment concerning institutional sales but DENIED it on other grounds. Further, the Defendants' (Ripple, Larsen, and Garlinghouse) motion for summary judgment was GRANTED as to the Programmatic Sales, the Other Distributions, and Larsen’s and Garlinghouse's sales and was DENIED as to institutional sales. Judge Torres proceeded to outline the formal adjudication process.

2. SEC's Arguments and Court's Decision

The SEC contended that Ripple violated securities laws by selling XRP as a “security” without complying with the registration requirements under federal securities laws. The three types of conduct that the SEC cited to support its claim include:

(1) $7.28 billion in institutional sales pursuant to written agreements;

(2) $7.57 billion in the Programmatic Sales on cryptocurrency exchanges; and

(3) $6.09 billion for non-cash consideration from the Other Distributions pursuant to written agreements.

In response, Ripple Labs asserted that it did not violate the securities laws because it did not sell XRP as a “security” and, in particular, did not sell it as an “investment contract.”

The court applied the "Howey Test" to determine whether there was an "investment contract". Under the Howey Test, an investment contract is considered to exist if all four requirements are met: (i) an investment of money (ii) in a common enterprise (iii) with the expectation of profits (iv) derived from the efforts of others.

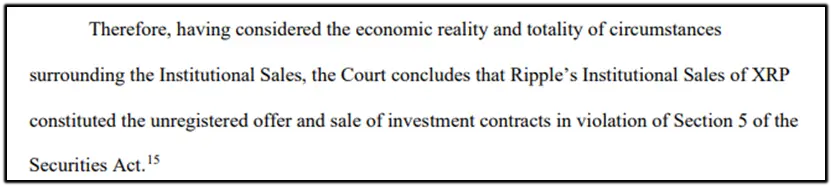

Regarding institutional sales, the court reasoned that from the perspective of institutional buyers, a reasonable investor would have purchased XRP with the expectation of receiving a return on their investment derived from Ripple's efforts. In particular, given Ripple's promotional and marketing activities and the nature of institutional sales, a reasonable investor would have understood that Ripple would use the funds received from the institutional sales to promote the XRP trading market and develop the XRP ledger, thereby increasing the value of XRP. Accordingly, the court found that Ripple's institutional sales constituted the unregistered offer and sale of investment contracts and therefore violated the securities laws.

Concerning the Programmatic Sales, the court differentiated them from institutional sales. In the case of XRP sold through cryptocurrency exchanges, it observed that retail buyers cannot be equated with institutional buyers as they engage in blind bid/ask transactions where the buyer is unaware of whether the money paid goes to Ripple or to another XRP seller. Consequently, the court concluded that Ripple's sale of XRP to retail buyers through the Programmatic Sales on cryptocurrency exchanges did not contravene federal securities legislation.

Lastly, the court determined that the Other Distributions did not satisfy the first prong of the Howey Test, which requires an “investment of money.” It observed that these Other Distributions included XRP distributed to employees as compensation or to third parties as part of Ripple’s initiative to develop new applications for XRP or the XRP ledger. Accordingly, the court held that the Other Distributions were not in violation of the securities laws.

3. Implications of the Ruling

The ruling in the Ripple case suggests that (i) cryptocurrency transactions between cryptocurrency issuers and institutional investors may qualify as investment contracts, while (ii) cryptocurrency transactions by retail investors through cryptocurrency exchanges may not. It is important to note, however, the ruling does not set forth a new rule of law deviating from existing U.S. judicial decisions. The court relied on the Howey Test to discern whether the sale of cryptocurrency constituted an investment contract, without making a definitive determination on the security status of the cryptocurrency itself, which the industry had anticipated.

This ruling may have implications for other lawsuits brought by the SEC against cryptocurrency exchanges, such as Coinbase, which are based on the premise that crypto assets themselves are securities. Additionally, it could serve as a reference for research on criteria for determining the security status of digital assets in other jurisdictions, including South Korea, from a comparative legal perspective.

With that said, it is important to bear in mind that this ruling does not represent a final judgment, and the case will proceed to a full trial and potentially an appeal by the SEC. In this regard, the future progress of this case will continue to warrant attention.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.