Where has all the (Crypto) Alpha Gone?

[Xangle Digest]

※ This article contains content originally published by a third party on May 25, 2023. Please refer to the bottom of the article for the copyright notice regarding this content.

※ This is a summary of the weekly research published by Matrixport on May 25th.

Executive Summary

Bitcoin (BTC) prices are struggling as the 10-year Treasury yields have climbed above the critical 3.5% level — previously we had identified this level as the make-or-break level for Bitcoin, and prefer to be neutral or even short Bitcoin IF the Treasury yield climbs above that level. As prices are now at 3.7%, we are not surprised that Bitcoin is selling off.

According to our ‘Crypto Markets at a Glance’ section, trading volumes have declined and as a consequence, Bitcoin price is experiencing downside pressure. Overall, network activity is mediocre, momentum is slowing and prudent risk management is advised.

Nevertheless, as negative investor positioning is extreme in equities, the SP500 could experience a large short-squeeze rally which would also help crypto. Overall, we still believe that risk assets (stocks + crypto) could rally this year as inflation will come down — based on our inflation model which we had previously shown.

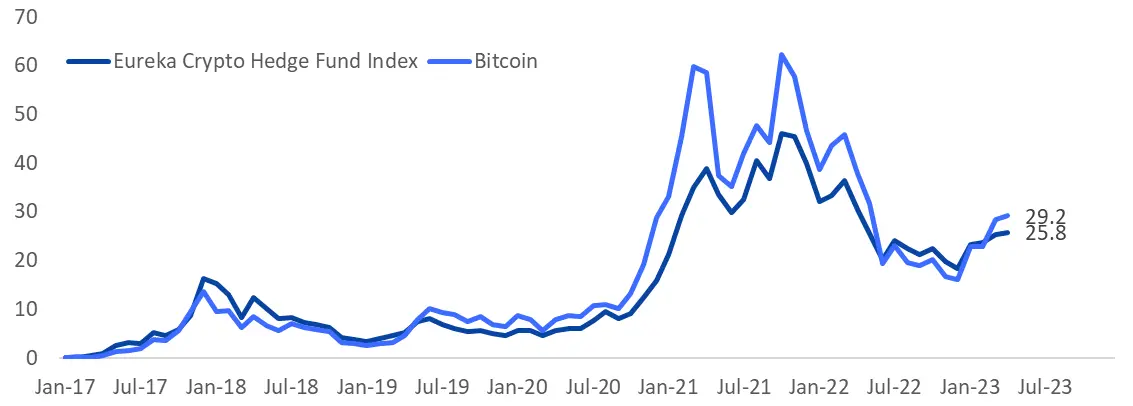

Surprisingly, Crypto Hedge Funds are underperforming Bitcoin for the fifth out of the last eight years, and investors likely demand stronger performance. The Eurekahedge Crypto-Currency Hedge Fund Index is up +36% year-to-date while Bitcoin prices have rallied +66%. The ‘Alpha’ has declined over the last few years and this requires Crypto Hedge Funds to take a more active (Long / Short) role in managing their portfolios. This would require Crypto Funds to incorporate macro variables and active risk management in order to outperform the market as drawdowns of -60-80% are unacceptable for institutional investors.

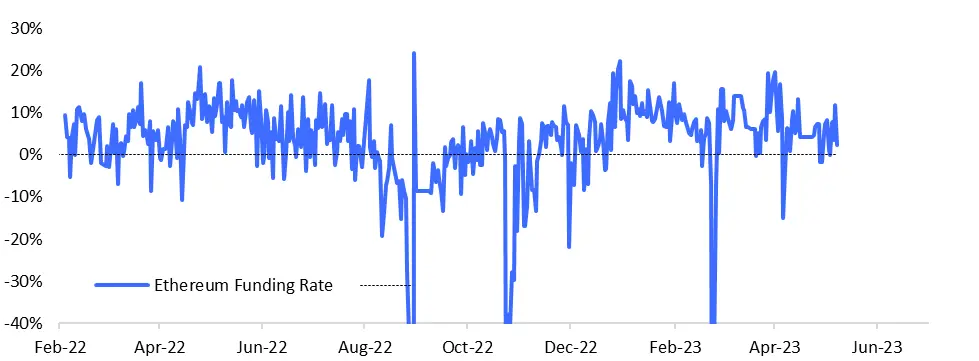

The premium compression of the perp funding rates is also a sign that traders are less optimistic about a price rally. We are entering the summer where volatility will likely decline.

Ethereum’s funding rate is trading closer to zero as traders cut their upside leverage. Source: Matrixport Technologies

Where has all the (Crypto) Alpha Gone?

According to the Eurekahedge Cryptocurrency Index, a benchmark index with 14 equal-weighted constituents, crypto hedge funds are underperforming Bitcoin for the fifth year out of the last eight years. This is a very poor representation of crypto fund managers. Even in 2023, crypto fund managers have underperformed in January and March — both months saw Bitcoin returns of +39% and +23% returns respectively.

Eureka Crypto Hedge Fund Index minus Bitcoin performance (Jan 2016 to current). Source: Matrixport Technologies

Investors in those funds certainly demand stronger performance as the managers appear to underperform even the most straightforward crypto investment — namely Bitcoin itself. Why should investors allocate to crypto fund managers if they consistently underperform the benchmark?

Normalised returns for Eureka Crypto Hedge Fund Index vs. Bitcoin (Jan 2017 to current). Source: Matrixport Technologies

It seems that managers are simply tracking the price of Bitcoin; adding management costs and performance fees on top, et voila, the underperformance can easily be explained. In addition, as regulatory requirements increase, operating costs will increase and could hurt fund performance even more.

But understanding the cyclicality of digital assets, combined with a flexible mindset of riding the winners and selling the losers, investors could make sizable returns — not even in bull markets, but also in bear markets. True, the ‘Alpha’ has decreased over time, and this has made active, discretionary crypto fund management more difficult.

The disappearance of ‘Alpha’ appears to be a shifting market structure narrative whereas macro factors have become more important as the liquidity within the crypto universe fails to expand. This itself is due to the regulatory overhang and the lack of sizable capital that institutions were expected to provide. In that environment, there should be a focus more on winners and losers, instead of broad exposure that depends on a rally in the Bitcoin price. This is the time for active crypto fund management.

-> 'Click' here to read the full report.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.