NFT Annual Summary: 17 Key Takeaways You Need To Know

[Xangle Digest]

※ This article contains content originally published by a third party on February 16, 2023. Please refer to the bottom of the article for the copyright notice regarding this content.

Introduction

Over the past year, we have seen many new changes in the NFT space. NFTGo Research has teamed up with well-known researchers and NFT degens to co-write a 100-page report that includes macro and micro data trends, user profiles, whale trends, and outlook for 2023.

Four Trends

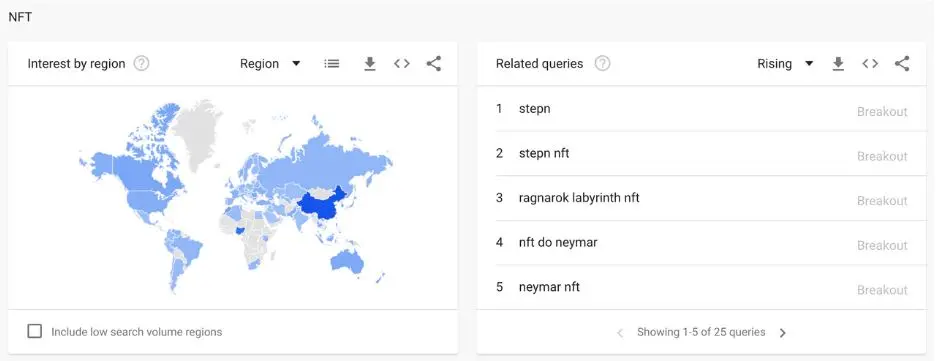

In 2022, the top 10 topics related to "NFT" are: Stepn, azuki, labyrinth, and neymar. The World Cup and move-to-earn has attracted many newcomers who are willing to participate in the NFT ecosystem.

Of all the cases where web2 brands and NFTs have been combined, sports brands have performed the best, especially Nike. After the acquisition of RTFKT Studios, the secondary market trading volume exceeded $10 billion and generated up to $185 million in revenue, including $93.13 million in primary market revenue and $92.81 million in royalties.

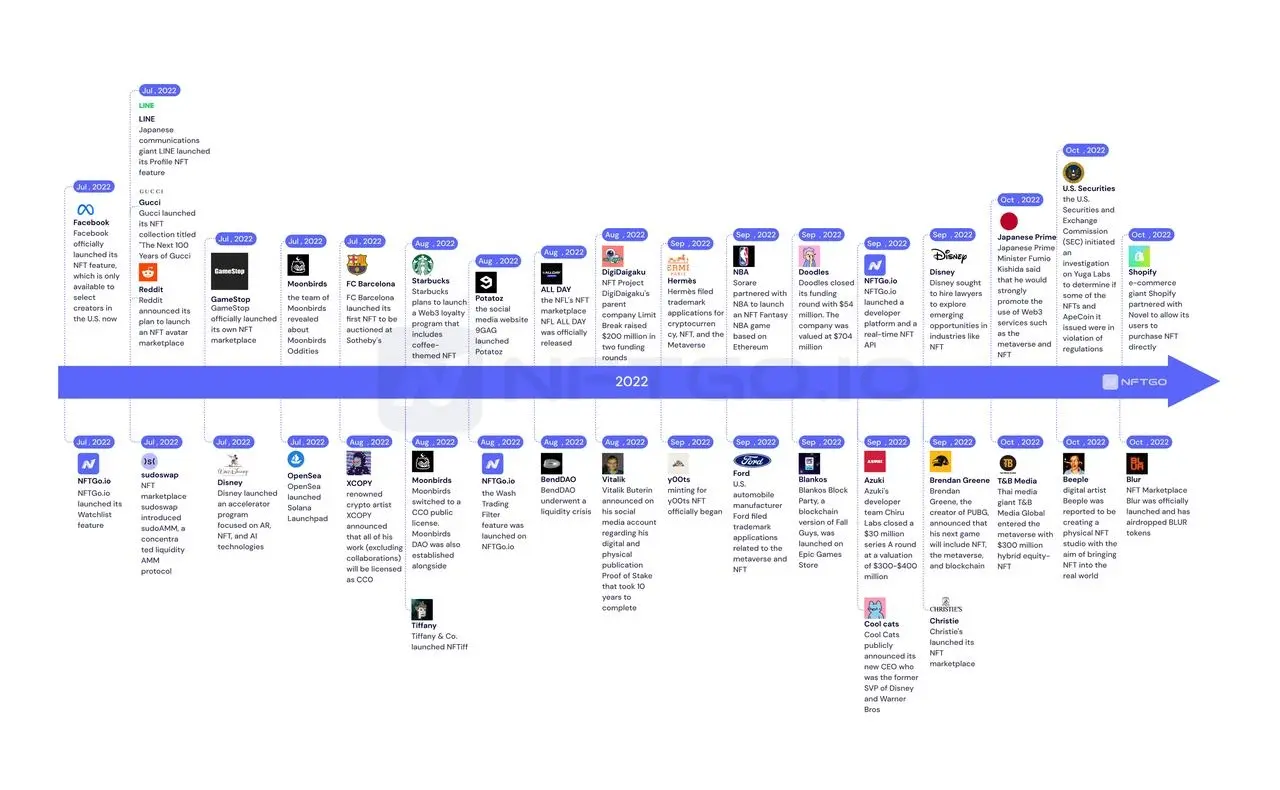

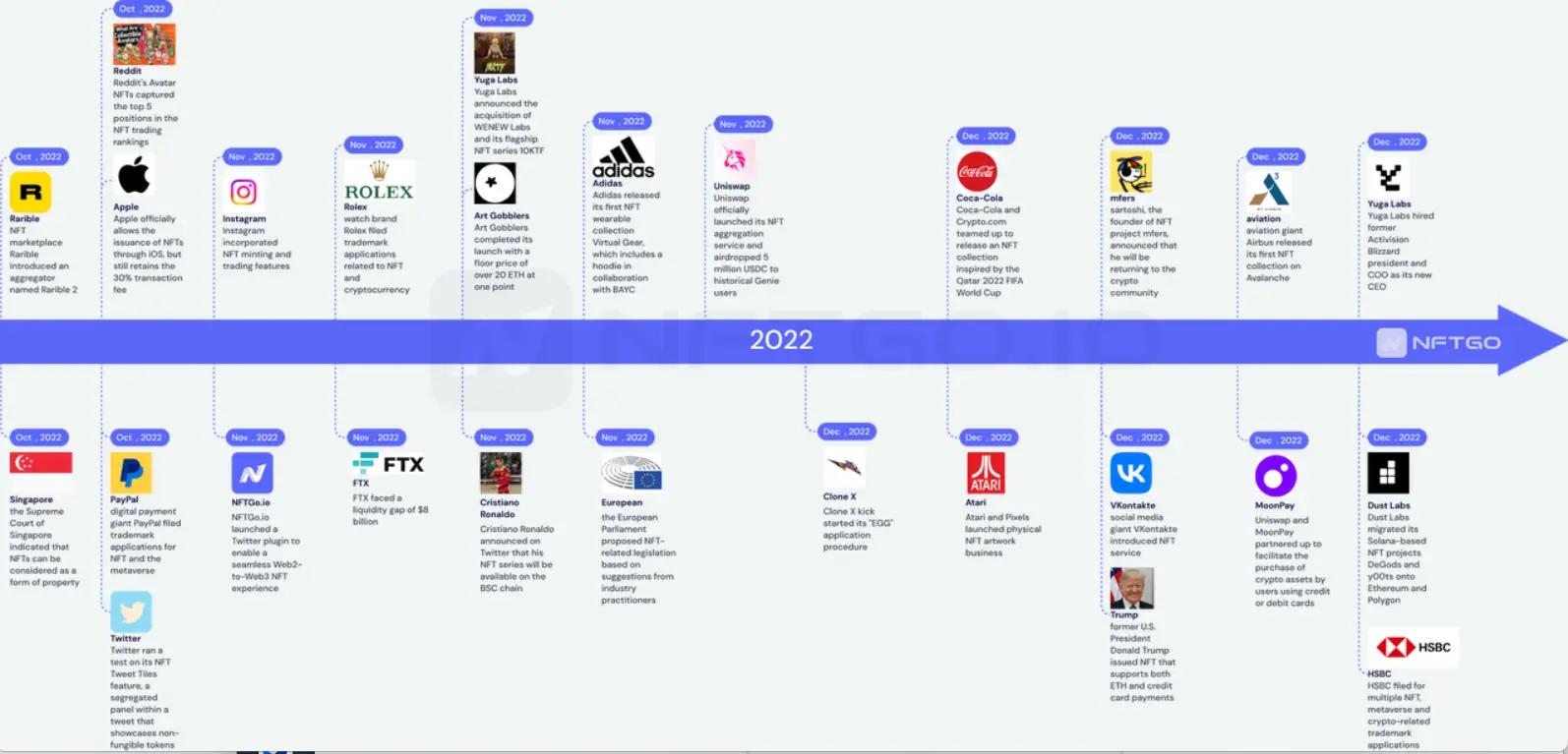

This year NFT has triggered unprecedented discussions, which greatly accelerated the birth of NFT application scenarios, such as: the digital identity storm triggered by SBT, the fragmentation wave and lending crisis, trading platforms to divide market share, creators' copyright opening and royalty income, Pass empowerment and O2O marketing.

The NFT ecosystem is expanding in spurts, the protocol layer is blossoming, the underlying public blockchain continues to be "one super and many strong", and the financial attributes give rise to more derivative projects, which are ahead of the application scenario-based projects.

Some blue chip NFT projects have started to gradually put their ideas into practice, and many of them have been using the additional issue of derivative NFT to expand their user base.

12 Data Facts

The trend we observed in the second half of the year was drastically different: traders were rushing to sell their NFTs. According to NFTGo.io, as of December 15, 2022, there were only 25,563 addresses with trading activities, of which 13,863 were buyers and 16,876 were sellers. Fortunately, the number of NFT holders grew 187.18% over the year and now amounts to 3.73 million holders.

In terms of the trading volume of the NFT market, blue chip NFTs have always held a significant advantage. Looking at the comparison of total trading volume of NFT collections in the past year, BAYC topped the list with a trading size of 639K ETH, occupying 7% of the total. Close to it are Otherdeeds and MAYC, both belonging to the Yuga Labs ecosystem, accounting for 5.47% and 5.07% of trading volume respectively.

We have analyzed the correlation between the market caps of Ether and the NFT market. In short, the correlation coefficient of the two markets was about 0.8 in 2022, which is relatively correlated. Then in 2022 Q2, the number shot up to a high of 0.98, which was followed by a drop to the 0.4-0.5 range.

The total amount of wash trades in 2022 is about 9 million ETH, accounting for about 35% of the total trading volume for the year. Previously, in August 2022, NFTGo.io reported that more than 82,000 addresses were involved in wash trading, and the number of wash trades reached more than 250,000.

The spate of new projects demonstrated steady growth. Despite the market downturn, the number of NFT projects maintained a monthly growth rate of 11.86%. The market downturn has affected the pace of project launches.

The NFT hype is usually led by new concepts which draw interest from the media. Many then start to copy the concepts and the marketing strategy, which eventually triggers a widespread discussion. Other projects will follow and imitate, which leads to an increase in market value in turn for the top few projects. The price of many NFTs has reached its all-time high during the market hype. When the market becomes more stable, the price declines.

The majority of projects are worth around 100 - 200 ETH. Only 4% of the projects have over 10KETH of total trading volume. The majority of projects have floor prices ≤ 0.1ETH, accounting for 74%. Most of the trading activities concentrate on high-quality projects.

We have selected 748 NFT projects from projects with trading volume above 1,000 ETH and with more than 1,000 partakers. In a single project, the average assets per capita is $4,137 and the median is $1,461. It means the "rich" have lifted the numbers, resulting in a widening wealth gap. The huge wealth gap allows the developers of NFT projects to design products that fit the needs of different users based on their purchasing power.

The market is the most liquid in January and April. It becomes less liquid in May and gets to the lowest point in September, and some NFTs must be discounted in order to be sold quickly.

Whales are often a barometer reflecting market trends. As of today, whales possess 1.25 million ETH worth of NFT assets, accounting for 12.11% of the total market share.

May and June were impacted by the general market as whales significantly withdrew their capital commitment from the NFT market, but there is still $160 million left in the NFT market. Most of these funds are long-term assets and utility assets made up of blue chip NFTs, which have laid the groundwork for future NFT development.

This year, users prefer PFP, Pass and Art, which account for a large proportion of the capital of the Giant Whale this year. This is related to the corresponding investment targets of these types of NFT in reality. Pass cards cater to the preference of whales as celebrity club memberships do to socialites in real life. The same consumer preference happens in the NFT market.

→ Click here to read the full report.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.