Upcoming Ethereum Shanghai Upgrade and What to Note

Translated by Rhea

Table of Contents

1) Withdrawal Function Completes the Staking Service, Highlighting the Role of ETH as a Capital Asset

2) Function of ETH as a Commodity Increasing Network Activity Strengthened with Gas Fee Reduction

3) Demand as a Store of Value Will Also Increase with Drop in Supply Volume

4) The Largest Risk is SEC Regulation If Considered a Security Product

On February 9, 2023, in the middle of world’s ever-growing attention on how Ethereum’s value will be assessed post the Shanghai Upgrade, the U.S. Securities and Exchange Commission (SEC) filed charges against Kraken, a centralized exchange, on the claims that its staking service is in violation of the Securities Act. Kraken was providing Staking-as-a-Service for not only Ethereum (ETH) but also other major mainnets, including Polkadot (DOT), Cosmos (ATOM), and Cardano (ADA). Kraken has since disclosed an agreement stating that it would cease offering its crypto asset Staking-as-a-Service program and pay the USD 30 million in penalties for failing to register it as a securities product.

Meanwhile, Kraken's share in Ethereum staking was about 7.42%, and market participants are now closely watching the direction of future regulations and their potential impact on Ethereum staking. Following this news, the prices of virtual assets, including Bitcoin and Ethereum, have undergone adjustments.

Although it is true that there is high uncertainty in the market regarding Ethereum staking, the Ethereum Shanghai upgrade itself has significant implications in terms of the intrinsic value and network completeness of Ethereum.

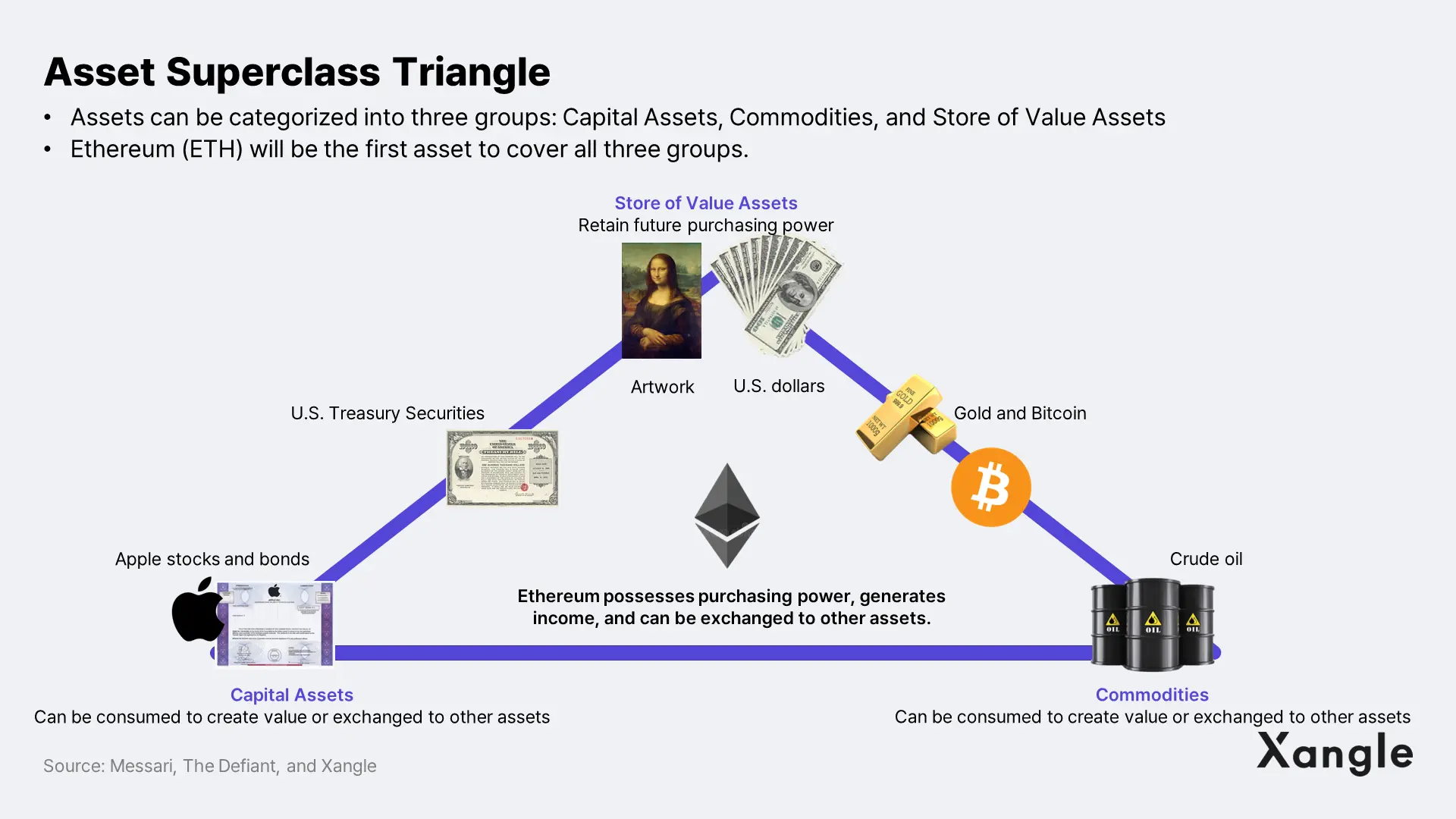

Ethereum, a Novel Asset Class

Unlike Bitcoin, which is often defined as digital gold and is considered a leading store of value in this era of Web3, it is not easy to definitively describe the characteristics of Ethereum ($Ether) as an asset. This is because Ethereum is a completely different form of digital asset that simultaneously exhibits the characteristics of various asset classes that have existed up to this point.

Firstly, owning this crypto asset – Ethereum – means acquiring a stake in the Ethereum network, and in particular, in the PoS phase, additional benefits can be expected by depositing Ethereum on the network (staking). In other words, it takes on the form of a productive capital asset.

In addition, Ethereum has played the role of a commodity that enables the execution of smart contracts on blockchain networks from the very beginning. ETH ($Ether) is used when tokenized assets are minted, moved, exchanged, or payments are made, or even when DAOs are operated on the Ethereum network.

Lastly, it is used as a means of storing value. Ethereum is widely used as a store of value asset, not only within the blockchain ecosystem, such as being used as collateral for decentralized financial services, but also in traditional industries, as attempts are made to introduce it as a payment method.

It is worth noting that the characteristics of Ethereum mentioned earlier are being further strengthened following the successful transition to a PoS consensus algorithm through the Merge, the most important upgrade in Ethereum's history, which took place in September 2022. Above all, with the upcoming Shanghai Upgrade next month, Ethereum will be able to complete its PoS transition. Therefore, let's take a closer look at the major improvement proposals (EIPs) and risk factors included in the Shanghai Upgrade, as well as how they will impact each of these asset-like characteristics of Ethereum.

1. Its Utility as a Capital Asset Highlighted

The first significant change to note after the Shanghai Upgrade would be that Ether ($ETH) will be able to fully serve its utility[KJ3] [RN4] as a capital asset, generating additional profits by being placed as a deposit. The upgrade will allow Ether that has been previously deposited in the network to be withdrawn, and the "staking" service will be completed.

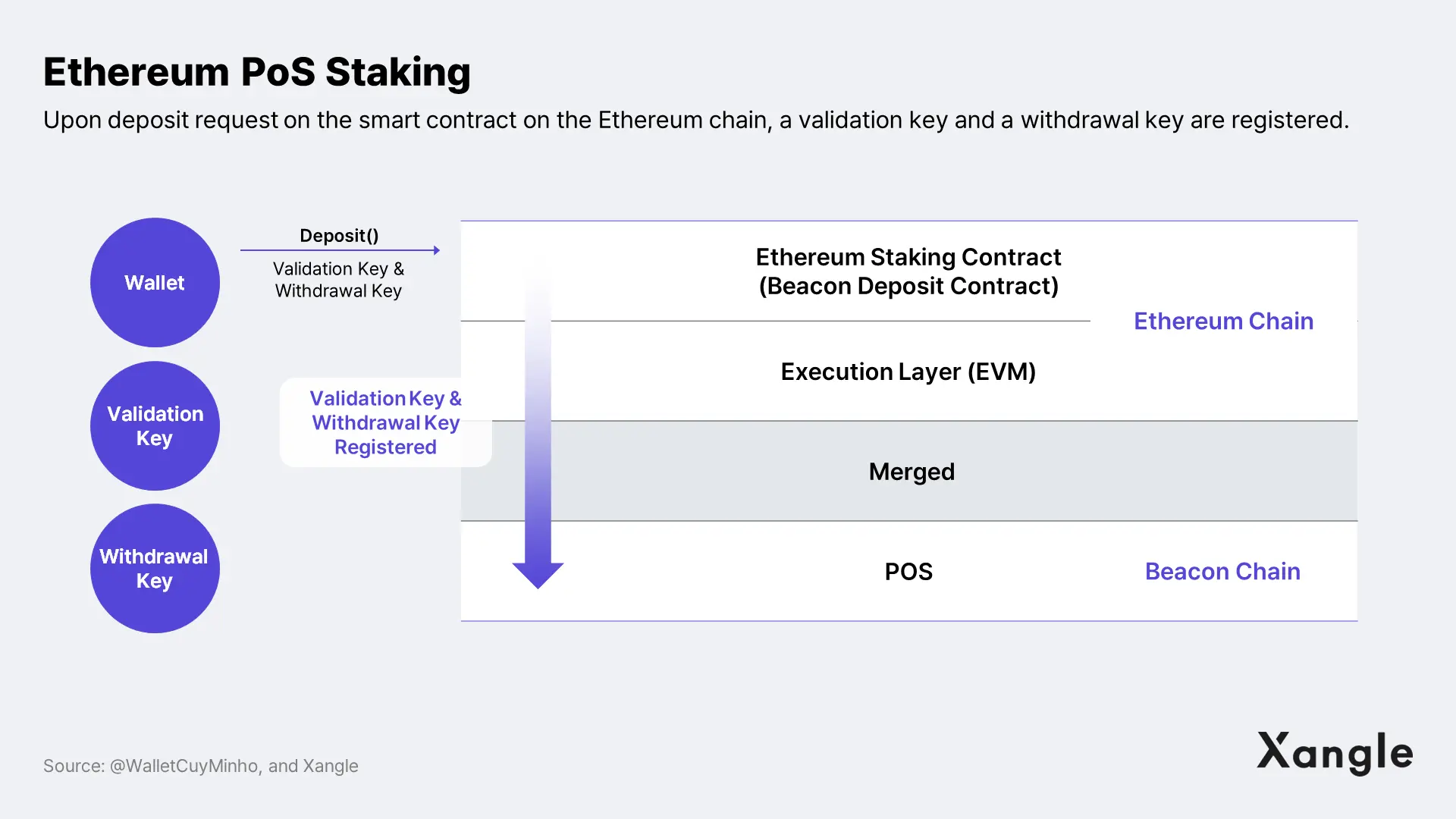

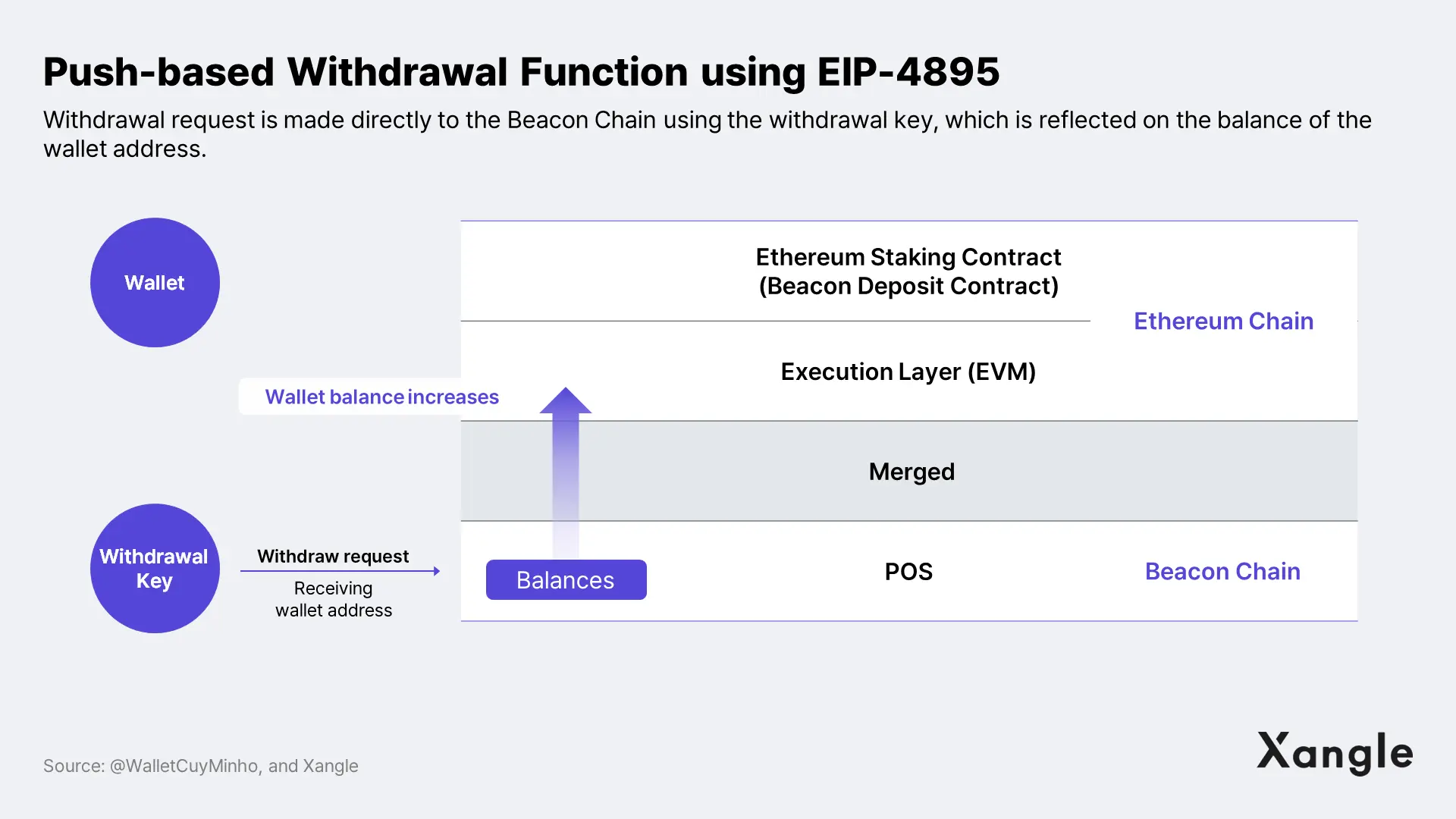

The Key is EIP-4895, Allowing Withdrawal of Staked Ethereum

The EIP-4895 is a crucial part of the Shanghai Upgrade, making withdrawals on the Ethereum network more efficient and secure. While deposit and withdrawal were relatively straightforward through smart contracts in the past, after the Merge, Ethereum has two separate layers for consensus (the beacon chain) and execution (EVM), and for staking, users will register their validation and withdrawal keys on the execution layer via the EVM.

For withdrawals, the process is typically the reverse of depositing. That is why Ethereum's major developers initially proposed a "pull" approach (EIP-4863). However, since block verification and associated rewards are taking place in the Beacon Chain, requesting a withdrawal through smart contracts in the EVM could become complicated, resulting in i) high gas fees or ii) waste of block space, and most importantly, iii) increased security vulnerabilities.

As such, the Ethereum developers have come up with a simpler "push" method for withdrawals. Instead of users requesting withdrawals through a smart contract, the new method involves using the withdrawal key to request the reward address directly on the beacon chain, updating the balance on the wallet.

In other words, EIP-4895 proposes an efficient and secure withdrawal process by implementing the withdrawal function as operations at the "system level" of the Beacon Chain and EVM, rather than requesting a new transaction format for withdrawal at the "user level." This approach ensures low cost and high stability for the withdrawal process.

Risk ① - Technological Risks to be Overcome with Focus and Thorough Verification

Similar to what happened with the Merge, one of the major risk factors with significant ripple effects that could arise from the Shanghai Upgrade, although not likely to occur, is technical faults.

The key Ethereum developers have continued to discuss technical specifications through meetups after the Merge, and have even shown a willingness to discard some of the features that were planned for the Shanghai Upgrade. The following is a summary of the excluded specifications, which are expected to be discussed again in the fall of 2023:

- Proto-Danksharding that will implement sharding to ensure Ethereum’s scalability (EIP-4844)

- Updates related to the Ethereum Virtual Machine (EVM) object format (EIP-3540, 3670, 4200, 4750, 5450)

Since the Merge, to ensure the technical stability of the Shanghai Upgrade, the Ethereum team launched the "Shandong" testnet in October, and conducted several devnet tests. In mid-January, the migration from the mainnet to the testnet through an Ethereum shadow fork was completed. Then, the public testnet "Zhejiang" was launched on February 1 at 15:00 UTC (00:00 KST on February 2) and mock withdrawals will be conducted on the Shanghai and Capella (withdrawal-related consensus layer) testnets at around 1350 epochs about six days later.

In particular, the withdrawal method proposed in EIP-4895 is a completely new attempt different from the conventional method implemented in smart contracts, requiring an even more thorough verification. With about 61,000 validators reported to be active on the 'Zhejiang' testnet as of February 2, concerted efforts are being made to minimize the risk of technical flaws after the mainnet upgrade.

Need to Focus on Investment Interest in Ethereum Staking After the Upgrade

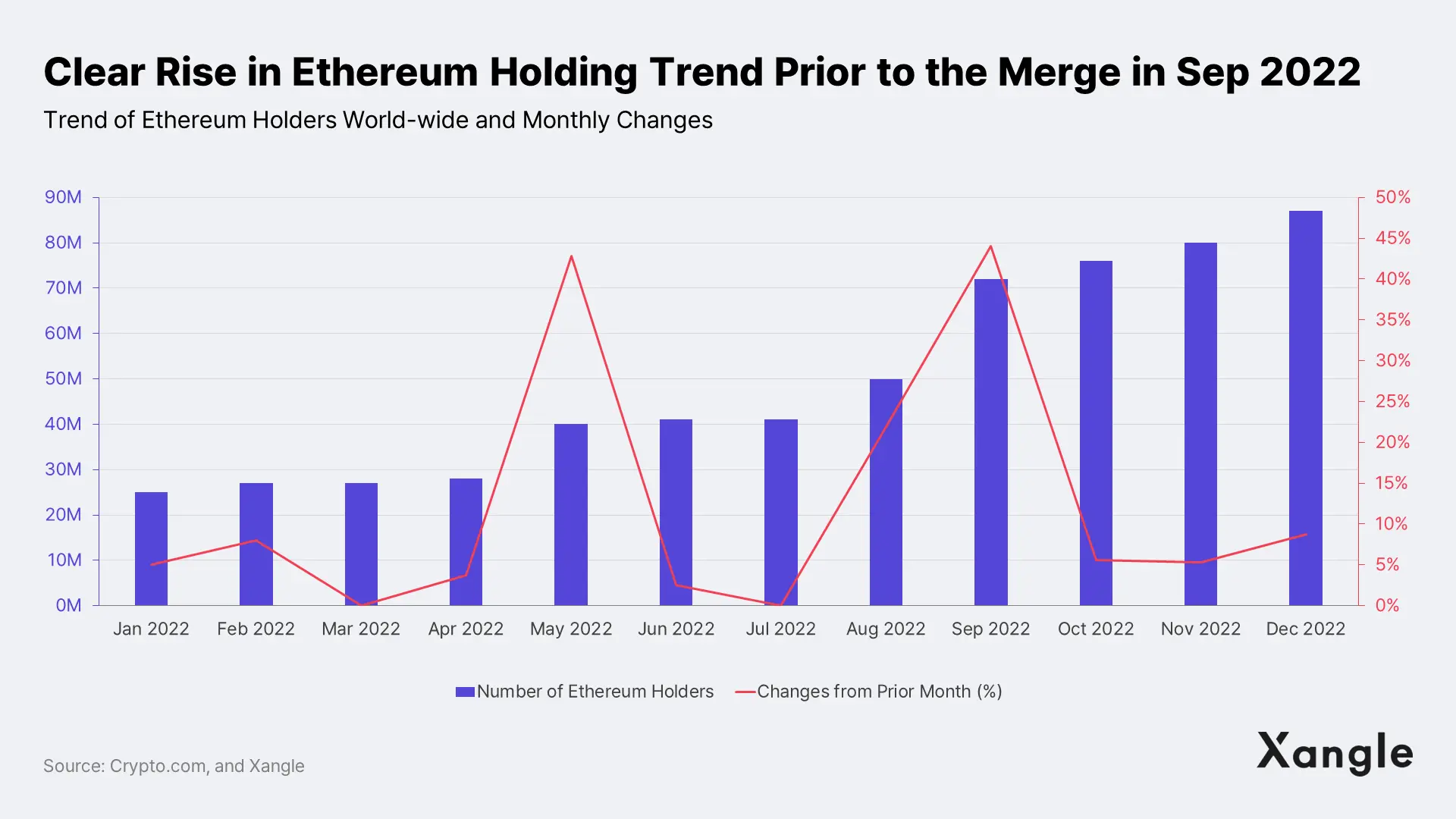

Despite the crypto market experiencing a downturn due to a series of domestic and international unfavorable incidents in 2022, interest in major crypto assets showed quite a significant increase from a long-term perspective. According to the 2022 Market Sizing report published by the virtual asset exchange, Crypto.com, Ethereum adoption increased by approximately 263% over the past year, with the analysis crediting the Merge upgrade in September to be the reason for such growth. The trend of Ethereum holders also showed a steep increase for two months leading up to the Merge, after reaching a peak of 87 million in December.

Both institutional and individual investors are also expected to show high level of interest in Ethereum and Ethereum’s staking service, in particular, after the Shanghai Upgrade.

- Increased Attractiveness as a Hybrid Bond-Like Asset: ETH holders can earn interest by leaving their ETH as deposits for a period of their choice like bonds without maturity, and additionally receive MEV rewards when the network activity increases like stock dividends. With the interest rate varying depending on the staking ratio – currently around 4% – and even with additional MEV rewards considered, the expected return on investment is relatively low compared to traditional financial products with a higher degree of stability. However, the investment attractive of ETH cannot be determined simply by looking at the interest and transaction fee profits alone since institutional investors can increase capital efficiency and easily utilize leverage through the liquidity staking service, as will be discussed in more detail later. and even the price of Ethereum itself is expected to rise.

- Replacing Bitcoin from a Portfolio Perspective: Xangle Research team has suggested in its Valuation Series that Ethereum could replace Bitcoin from a portfolio perspective. The argument suggests that as Bitcoin faces criticism for its environmental impact due to the significant amount of electricity consumed, there is a possibility that Ethereum, which has transitioned to PoS, could replace Bitcoin to some extent if the trend of applying high ethical standards to corporate activities and focusing on ESG (environmental, social, and governance) management continues.

Meanwhile, JP Morgan's analysis concluded that investors who hesitated to stake their Ethereum due to the uncertainty of withdrawal timing can now participate in staking on a large scale after the Shanghai hard fork upgrade. The report also estimated that 95% of individual investors on Coinbase could participate in Ethereum staking after the hard fork, which could bring in up to $545 million in annual revenue, indicating an expectation of increased demand once the staking service is completed. In fact, 11% of Coinbase's revenue in 3Q last year came from staking, a figure that increased by about five percentage points from 6.2% in the 3Q of the previous year. The market's interest in business models that can benefit from the Shanghai hard fork is expected to remain high for the time being.

However, given that an agreement was reached just yesterday (on February 9, 2023) to suspend Staking-as-a-Service offered by Kraken, a coin exchange, after the SEC alleging the product to be securities, it remains uncertain whether centralized exchanges can directly benefit from the staking services. It is also necessary to monitor how the discussion on whether Ethereum staking should be deemed securities will be determined.

Risk ② - Probability of a Massive Withdrawal (Bank Run) is Limited

Some are concerned about the risk of large withdrawals due to selling pressure after Ethereum withdrawals, but the likelihood of such an event occurring is considered somewhat limited.

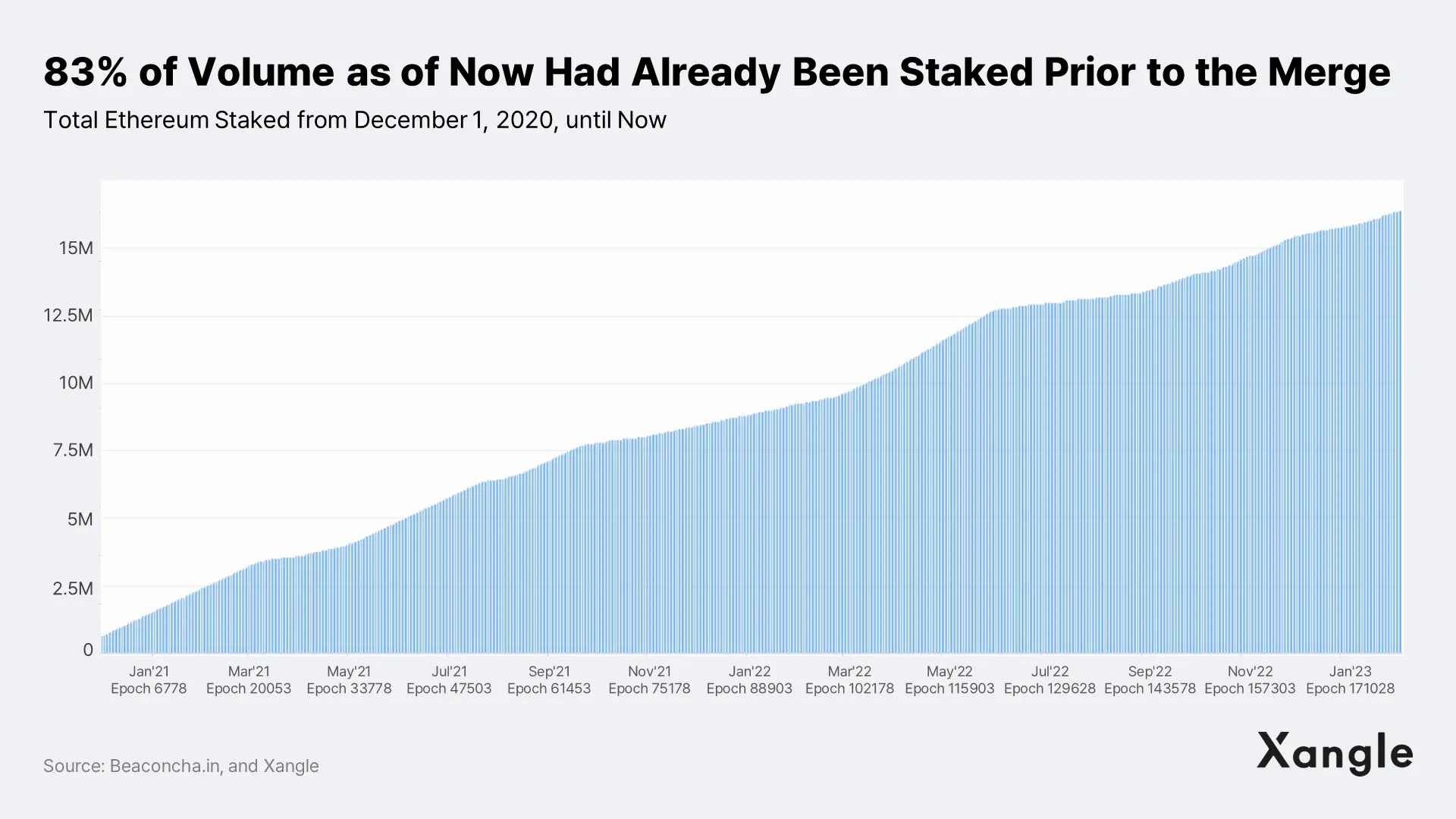

First, the cumulative Ethereum staking trend so far shows that investors who have deposited EHT in the Ethereum network have approached their investment in a long-term perspective. Staking Ethereum has steadily increased since December 2020 when the network launched the Beacon Chain that allows staking. The figure continued to accumulate even when faced with delays in the Merge schedule or when there was a high level of uncertainty about very success of the Merge itself. Before the Merge in September 2022, many people invested in Ethereum's med-to-long-term vision, along with the bullish trend of crypto assets. By September 15, when the Merge took place, about 137,000 Ethereum had already been deposited, which accounts for 83% of the staking volume as of February 7, 2023.

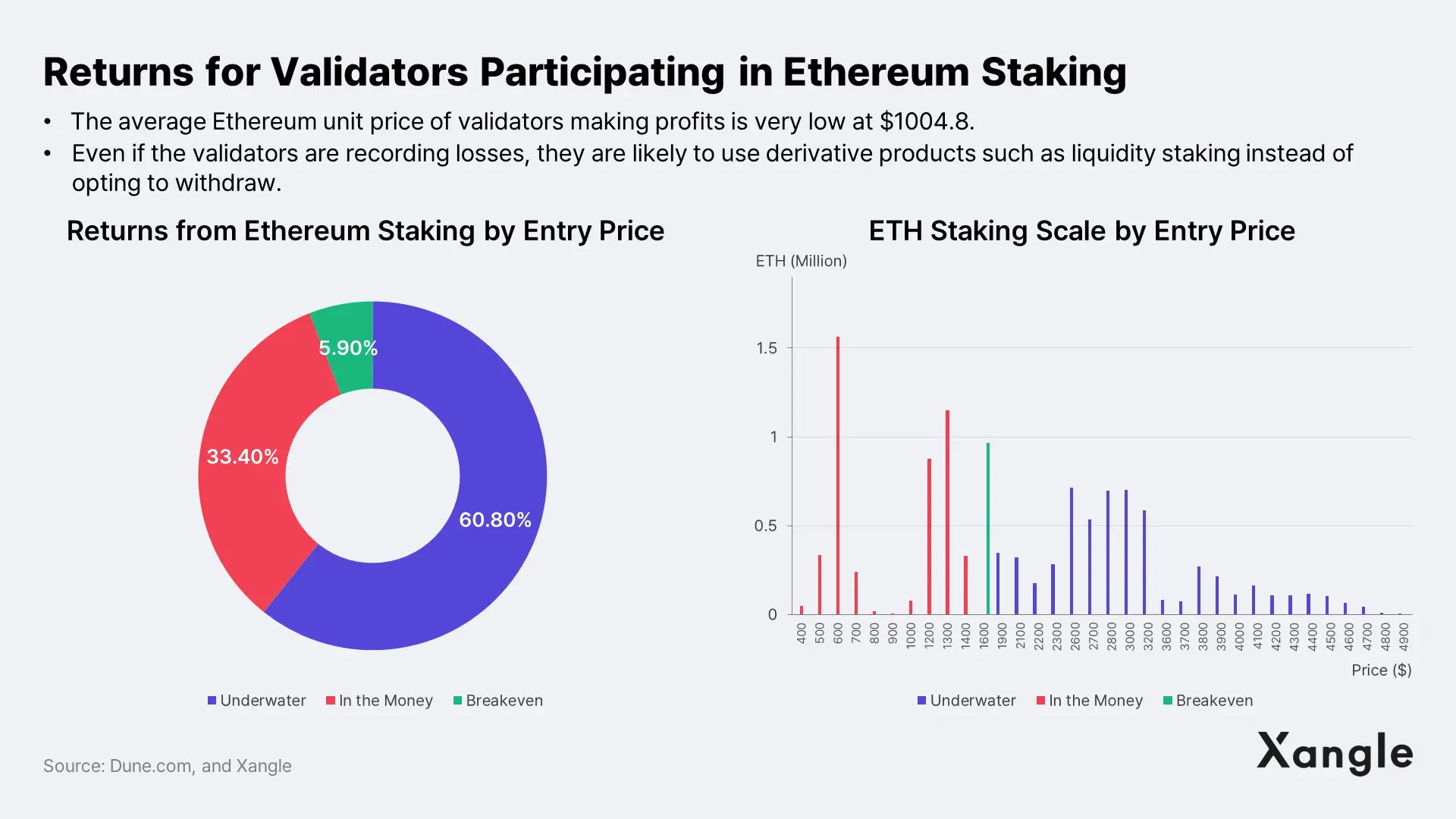

Furthermore, among the validators who have ETH deposited for staking today and are suffering losses due to the Ethereum price decline, about 33% are making profits. These are the ETH holders with significantly low purchase unit prices for their Ethereum and not much pressure to sell. Even those validators currently experiencing losses are not expected to sell their ETH nor consider the pressure to sell Ethereum from the withdrawals to become a big risk factor. Rather, they are likely to actively recover their losses through leveraging by seeking higher capital efficiency as derivative products such as liquidity staking are gaining traction in the market.

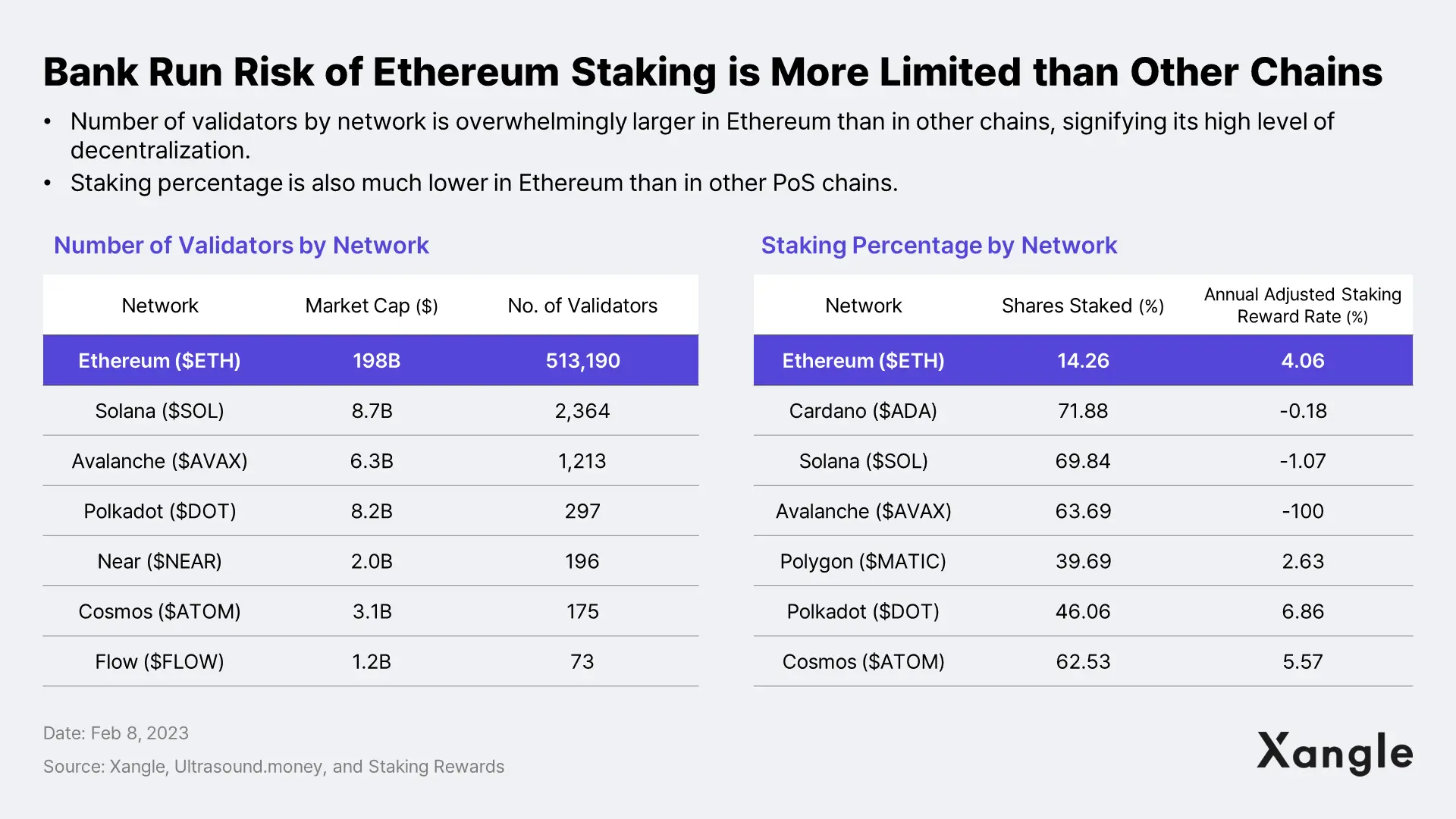

In addition, Ethereum has a relatively large number of validators compared to other chains and a relatively low number of staked tokens on the network. In terms of figures, while Solana and Avalanche have secured 2,400 and 1,200 validators, respectively, Ethereum has 513,000 validators active on the network, and the number of staked tokens on the Ethereum network is only at 14%, compared to Polygon at 40%, Cosmos at 62%, and Cardano at around 72%.

Moreover, the push-based withdrawal function also serves as a means of ensuring network stability against sudden bank runs. To initiate an Ethereum withdrawal, validators must go through an "exit queue".

Various parameters may be involved to define this, but the two most representative ones are the total number of validators and the network's "churn limit." In particular, the "churn limit" allows Ethereum to control the number of validators who can make withdrawals simultaneously. This determines the number of validators who can withdraw all the deposited amount per epoch or 32 blocks. Assuming there are about 500,000 validators, the churn limit is predicted to be 7 per epoch and increased by 1 per every 65,536th validator in the future.

In other words, after the validator finally exits the "withdrawal queue" restricted by the "churn limit," they have to input the "withdrawal period." The process is expected to take about 27 hours for validators who have not been slashed. However, the length of this period depends entirely on the number of validators attempting to withdraw at the same time. For example, if one-third of all validators were to try to withdraw their funds at once, the withdrawal period could be as long as three months. (To read more on the "churn limit," please refer to this link.)

On the other hand, the bank specializing in crypto assets, Sygnum, suggested the following scenario regarding the situation after the Ethereum withdrawal is implemented, claiming that the risk of a sudden bank run is limited:

- Assuming that the Ethereum staked is at about the current 16M, validators would wish to withdraw over 32 ETH to increase their capital efficiency.

- According to Coin Metrics, in such a case, up to 57,600 partial withdrawals can be made per day, and on average, validators can be considered to have deposited 34 ETH. Therefore, 115,200 ETH, calculated by subtracting 32 from the average 34 and multiplying by 57,600, can be made available in the liquidity market (with up to 57,600 ETH excess withdrawals made possible with around 500,000 validators for up to 10 days.)

- However, as more validators choose to withdraw the entire amount of Ethereum deposited, the withdrawal period will increase, and selling pressure will decrease.

- However, as more validators choose to withdraw the entire amount of Ethereum deposited, the withdrawal period will increase, and selling pressure will decrease.

- However, as more validators choose to withdraw the entire amount of Ethereum deposited, the withdrawal period will increase, and selling pressure will decrease.

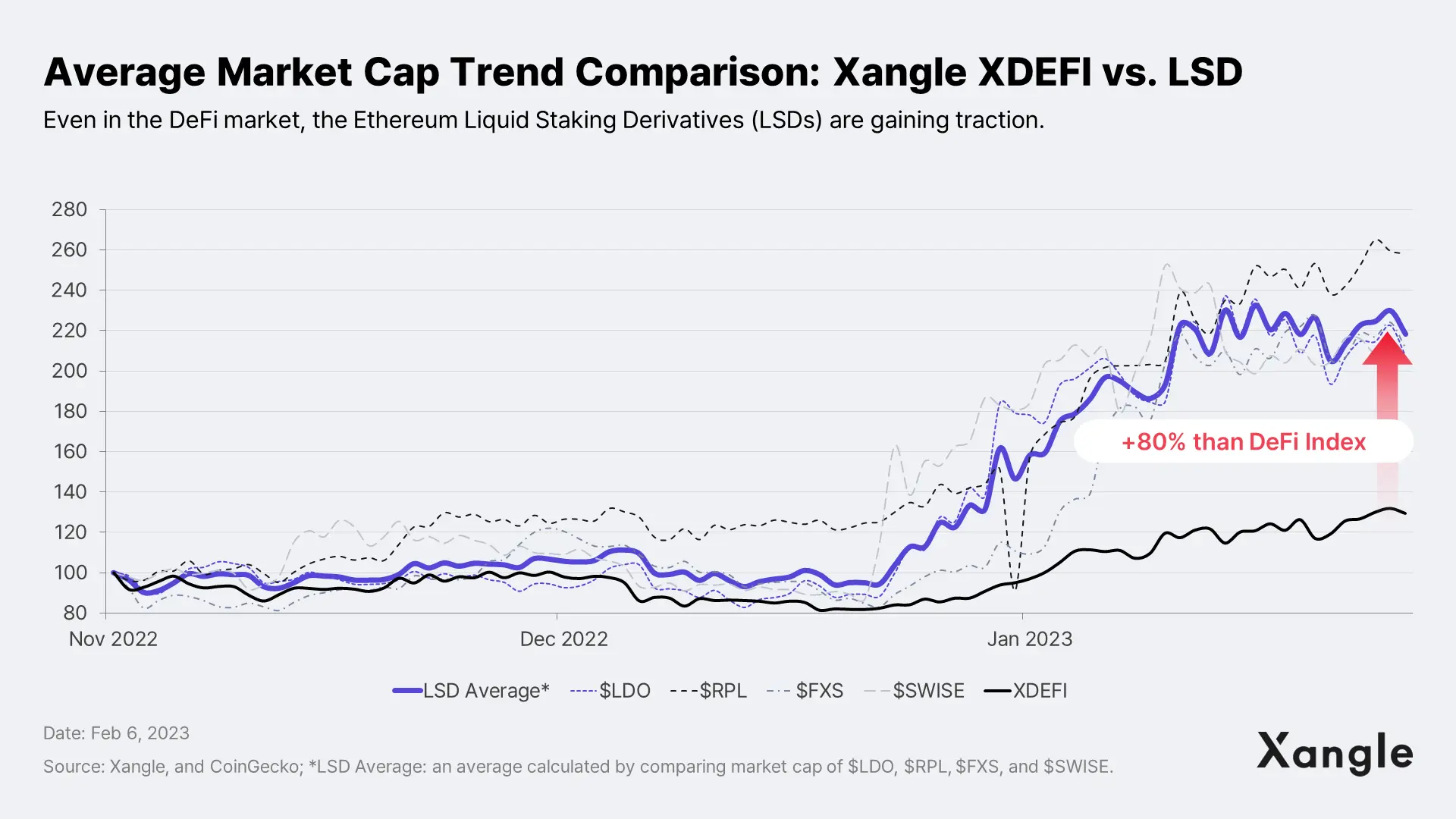

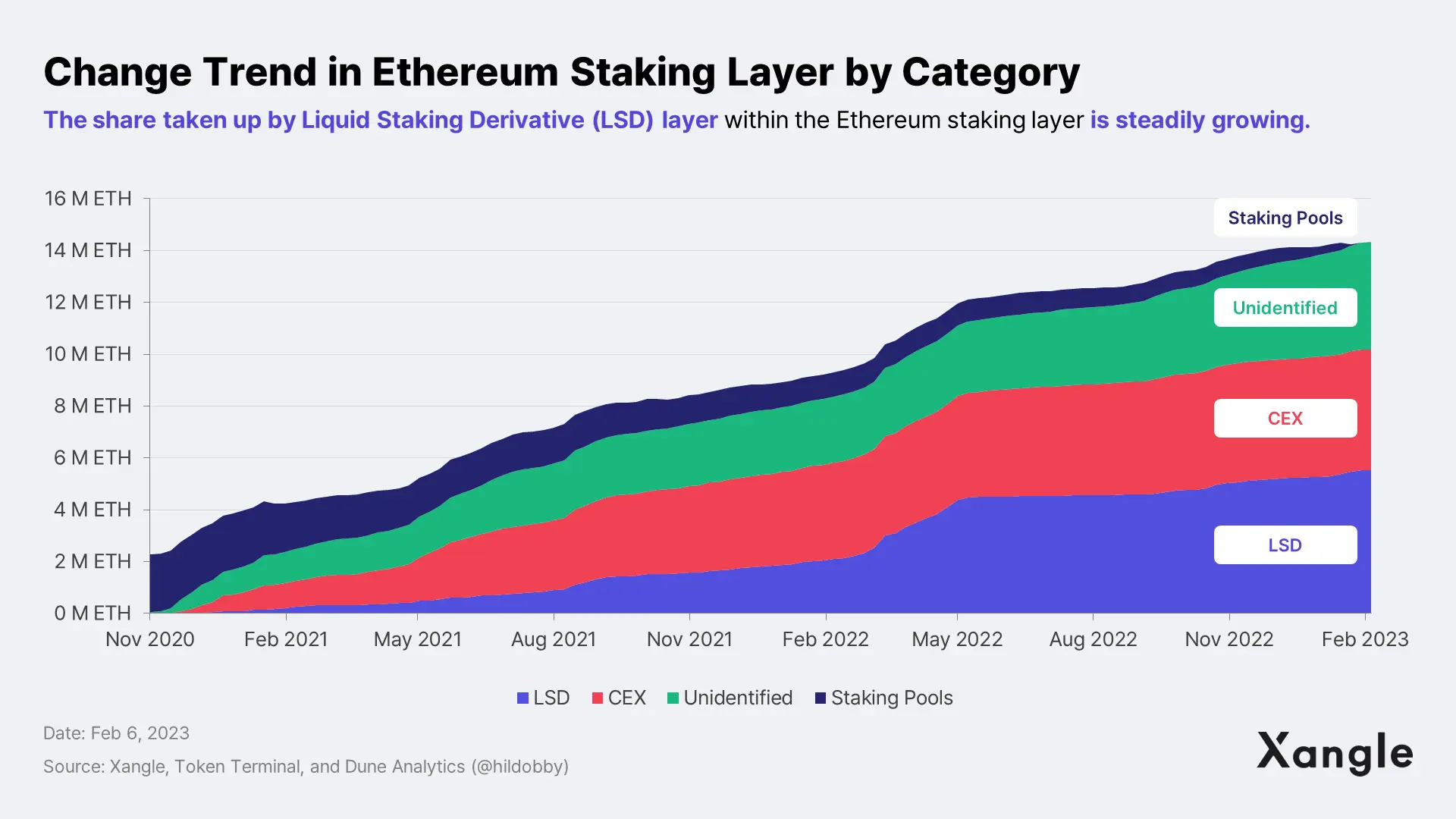

Ethereum staking liquidity service is actually attracting attention from many, as mentioned in the scenario above and as seen in the chart below. Xangle also plans to address this in more detail in our follow-up report.

2. Function of ETH as a Commodity Increasing Network Activity Strengthened

The Ethereum ecosystem is powered by Ethereum, a cryptocurrency issued on the network, also known as ETH ($ETHER). Vitalik Buterin, the co-founder of Ethereum, was inspired by Ether, also known as the fifth element. Ethereum is used as a gas fee, which powers smart contracts on the Ethereum Virtual Machine (EVM).

Gas fees in Ethereum serve as a defense against network attacks. However, they also act as a major factor that hinders the scalability of the Ethereum network by providing negative user experiences or adding operational burdens to projects when the level becomes too high due to network congestion.

Lower Gas Fee and Higher TPS Enhances Ethereum Network’s Scalability

As such, Ethereum's key developers have already designed a roadmap for scalability after the PoS transition, and the upcoming Shanghai Upgrade also includes some EIPs that can reduce gas fees.

EIPs on gas fee reduction included in the Shanghai Upgrade are:

- EIP-3855, reducing the size of smart contracts and optimizing codes

- EIP-3860, securing security and scalability during the cost measuring process

- EIP-3651, reducing the cost burden for the validators

However, above all, there seems to be significant anticipation for "The Surge," the roadmap for after the Shanghai Upgrade. "The Surge" refers to the phase where sharding is introduced, and significant data availability is provided to the roll-up network, lowering the cost of transaction processing and increasing transactions per second (TPS) to secure scalability.

After "The Surge," the Ethereum network is expected to secure scalability while ensuring a higher level of decentralization and stability than the numerous so-called Ethereum killers that have emerged, becoming the chain that solved the most blockchain trilemma as well as the basic - or even essential - infrastructure for blockchain dApps.

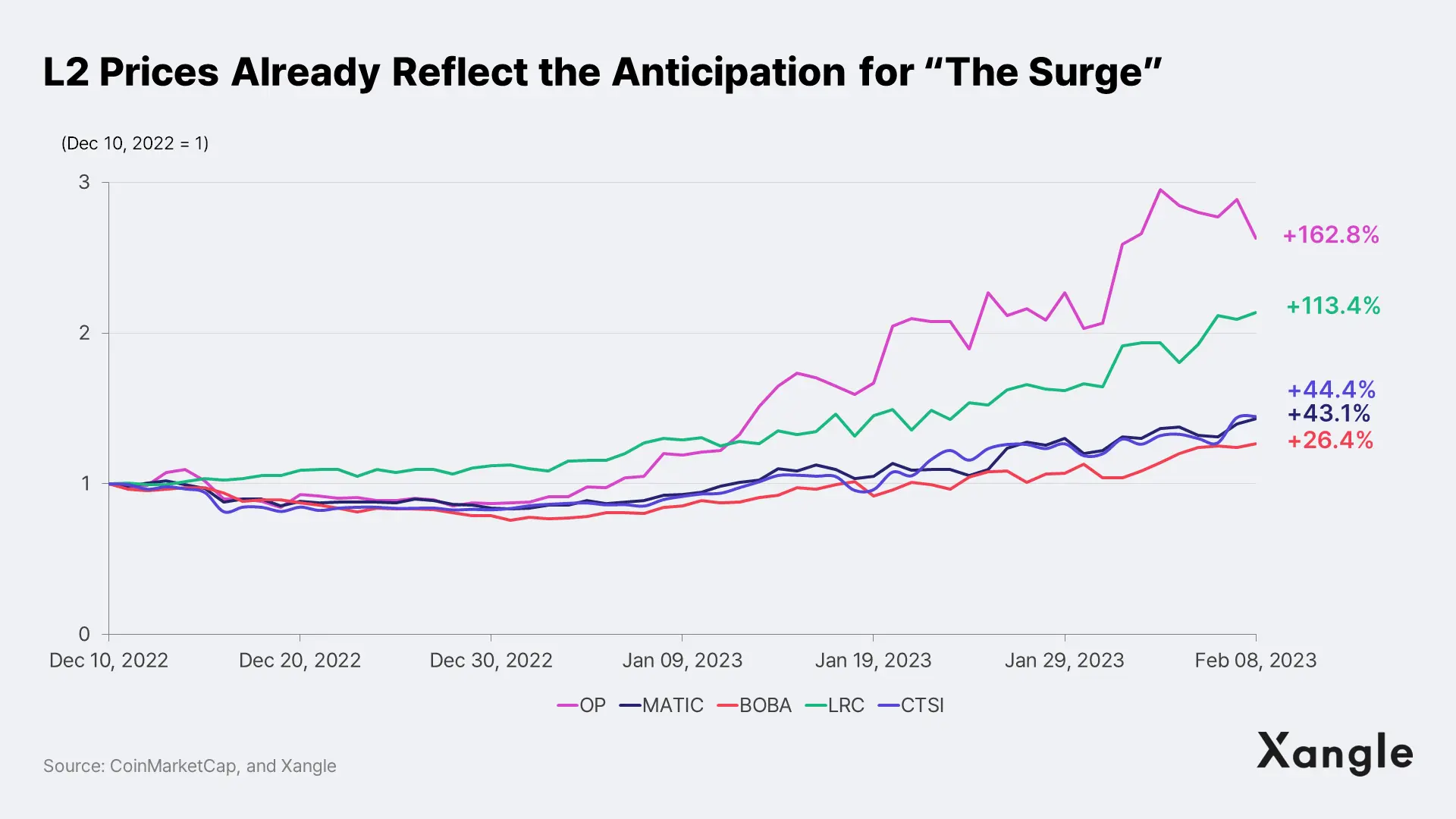

Risk ③ - Burden of Competition for the Utility with L2 Tokens is Low in Mid-to-Short-Term

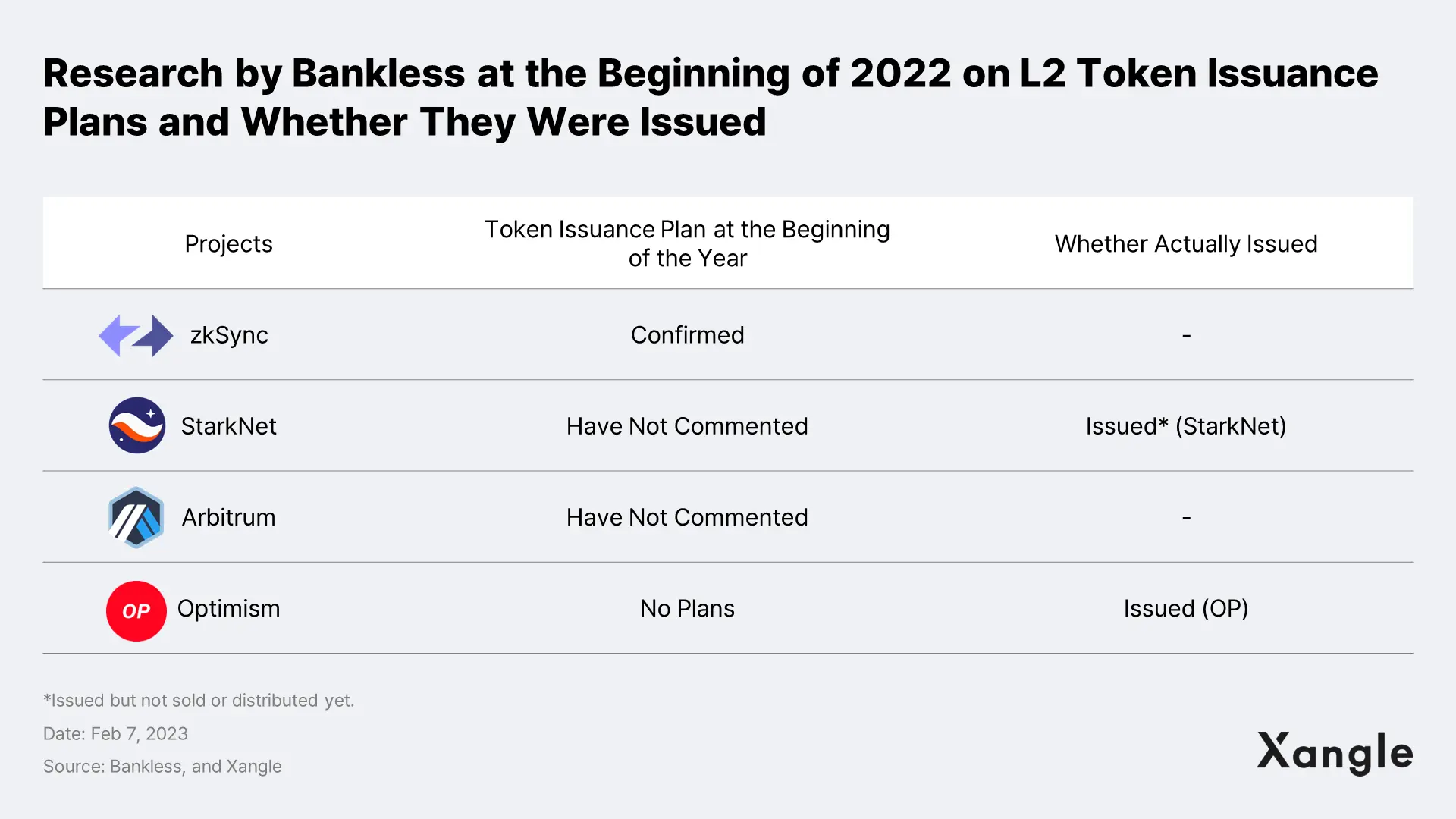

Meanwhile, if Ethereum expands its scalability with a focus on rollups, there is also a potential risk of competition with L2 tokens for utility in the long run. StarkNet, one of the major rollup projects using the Zero-Knowledge proofs, issued the "StarkNet Token" last year, announcing that both Ethereum and its native token would be used for all transaction fee payments initially, with plans to ultimately enable payment with only the native tokens.

This shows the potential conflict of interest that may arise with Ethereum if L2 solutions seek to issue their own native tokens and secure their utility once the ecosystem is sufficiently expanded.

However, it is likely not to be a major issue in the mid-to-short term, as competition to gain market share will continue within the roll-up ecosystem for the time being.

Xangle Research compared and analyzed the two representative rollup solutions, Optimistic Rollup and ZK Rollup, and found that while ZK Rollup has a clear advantage in scalability, the cost difference between the two rollups is not expected to be significant. The investigation into the factors that could affect the competitiveness of these rollups showed that it is expected to take some time for one side to clearly take the lead. (Refer to “Would Optimistic Rollup Remain as a Viable Candidate Even After ZK Rollup Is Fully Developed?”)

During that period, Ethereum is expected to secure its dominance through first-mover advantage and network effects in the utility competition. The post-sharding Ethereum is also assessed to be promising as of now.

3. Demand as a Store of Value Will Also Increase

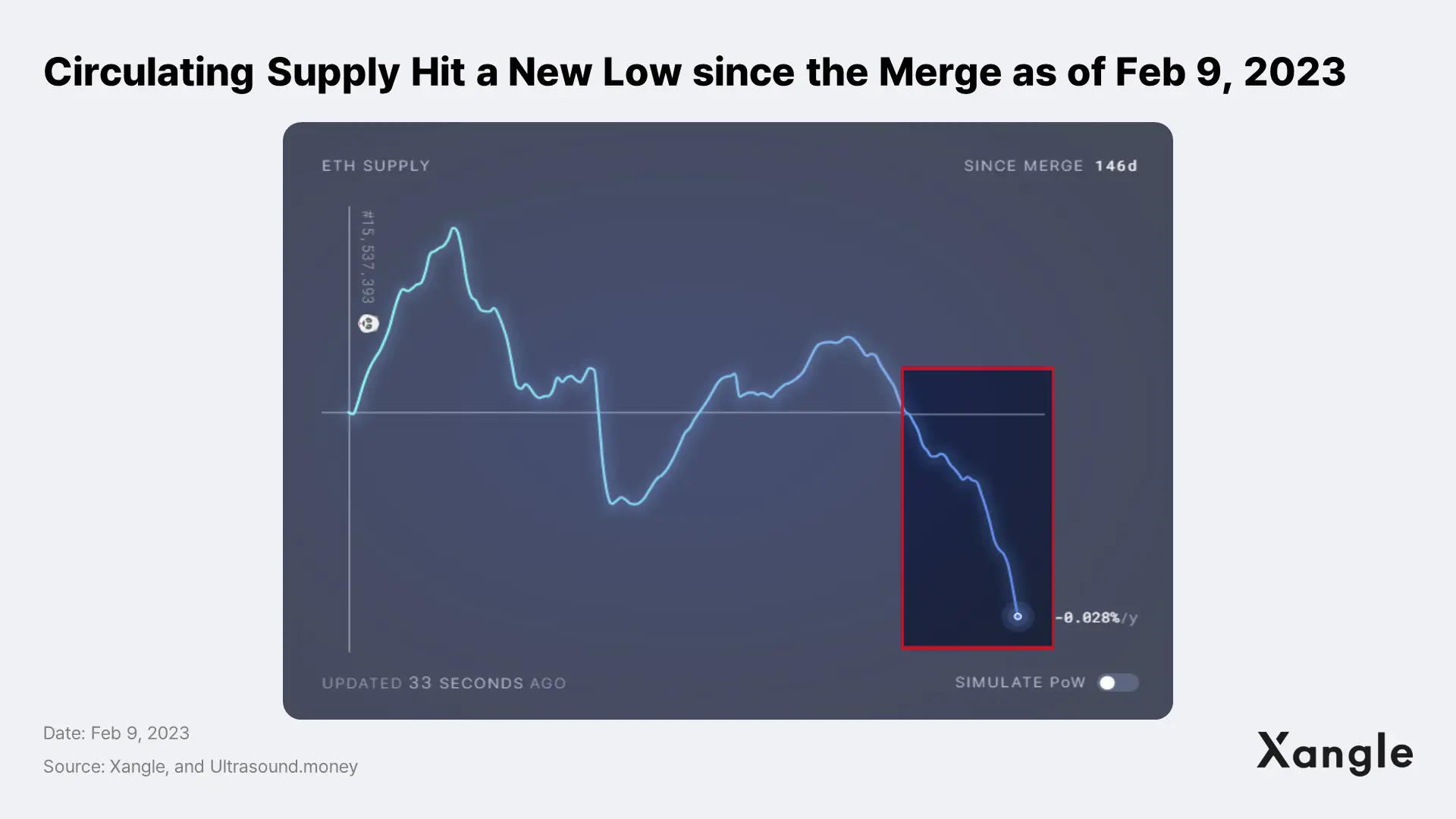

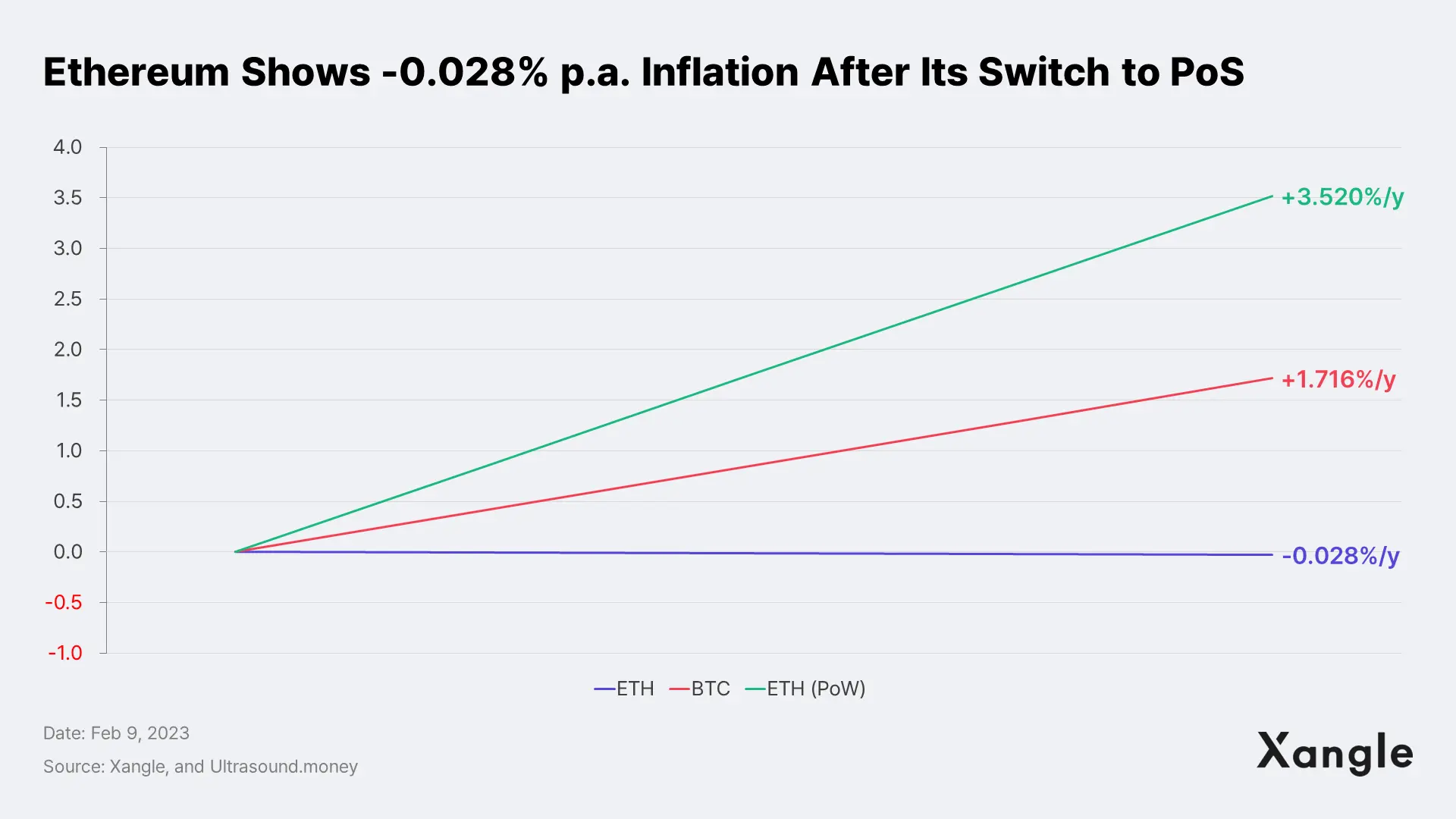

With the network burn mechanism introduced by EIP-1559 during the “London Hard Fork” upgrade in August 2020 and the sharp decrease in Ethereum’s issuance after the Merge taking effect at the same time, Ethereum has demonstrated deflationary asset properties as the network becomes more active. As of February 9, 2023, Ethereum has recorded a new bottom in supply since the Merge.

As of February 9, 2023, about five months after the Merge, according to data provided by ultrasound.money, Ethereum's inflation rate is currently at around -0.028% per annum. If the network had continued to operate under the previous PoW system, the inflation rate would have been approximately +3.520% per annum. The figure shows that the Ethereum issuance rate has actually decreased after the Merge.

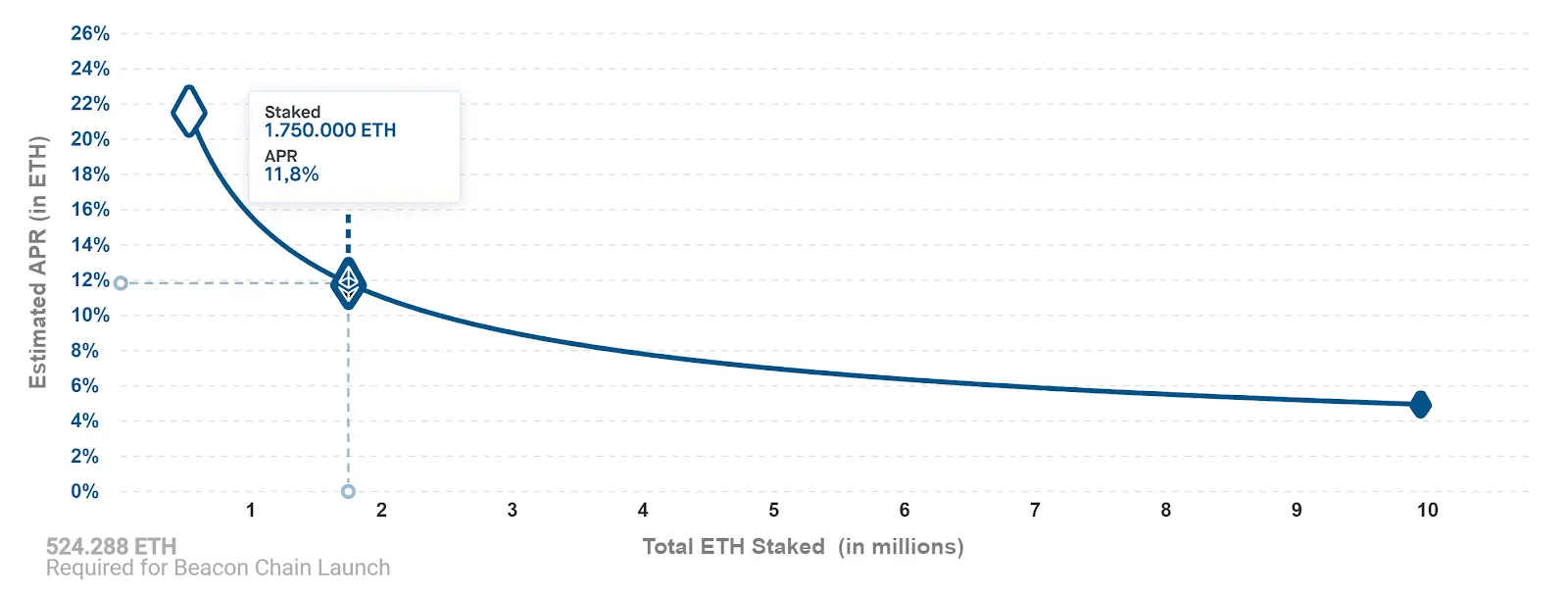

These effects are expected to become even more dynamic as the ratio of Ethereum staking increases. Below is a graph of the dynamic inflation curve for PoS Ethereum, which implements a structure that rewards validators for network security while minimizing Ethereum issuance.

As a result, with the increase in staking demand after the Shanghai Upgrade, we can expect to see a dual effect of deflation and a decrease in circulating supply as the deposited Ethereum amount grows. This could lead to a more dramatic effect than Bitcoin, which rose to prominence as a store of value through a contract that limits its maximum issuance to 21 million coins.

4. The Largest Risk is SEC Regulation If Considered a Security Product

Recently, as the crypto asset market overall has been showing signs of recovery, expectations for Ethereum's Shanghai upgrade and related projects have also been increasing. However, the market was thrown into confusion when an announcement was made on the 9th on the SEC regulation based on whether tokens are considered a security product – the largest risk. The U.S. SEC filed a lawsuit against Kraken, a centralized exchange that offered Staking-as-a-Service, accusing it of "selling unregistered securities." In response, Kraken paid a USD 30 million in penalty and discontinued its staking service. The market’s concern is rising on how far this impact will spread.

Key reasons why the U.S. SEC considers Kraken's Staking-as-a-Service as a security include the following: i) token staking is conducted in a passive manner, which results in a passive cash flow; ii) rather than individuals carrying out staking for themselves, a collective pool was formed with a promise of higher profits; and iii) the entity, Kraken, took the lead in modifying the existing staking process and the changes were carried out without sufficient transparency. While there does not seem to be any clear criteria or standard for each of these claims, it is deemed that the impact on the crypto market will be nothing but insignificant, considering that most major projects other than Bitcoin provide staking services based on the PoS consensus mechanism.

In the short term, decentralized protocol services are likely to maintain their competitive advantage over centralized staking services. However, depending on the intensity and scope of the regulation, there is a risk that it could dampen staking demand or lead to a weakening of the crypto market as a whole. Therefore, it is important to keep a close eye on the news, with high volatility expected for the foreseeable future.

In the meantime, this incident has drawn even more attention to liquidity staking protocols, which will play a pivotal role in the ecosystem after another upgrade with the upcoming Shanghai Upgrade. In addition, please keep your eyes on the upcoming Xangle report, in which we will examine i) the background of recent price increases in liquidity protocols and ii) the potential for ecosystem shifts in the future.

Meta Description: With the Ethereum Shanghai Update coming up, Xangle draws attention to forecast on Ethereum’s price and technological side, and the potential for the future Ethereum ecosystem.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.