LINE LINK (LN) Ushers in the New Era of Zero Reserves

Translated by Rhea & LC

Table of Contents

1. LINK (LN) by LINE, a Perennial Hopeful

2. Seeking a Rebound with the New Mainnet, Finschia

3. LINE Develops Its Own Key Services

4. Zero Reserves Tokenomics

5. Possible Delay in Building Infrastructure and Attracting Killer DApps Remain as Challenges

1. LINK (LN) by LINE, a Perennial Hopeful

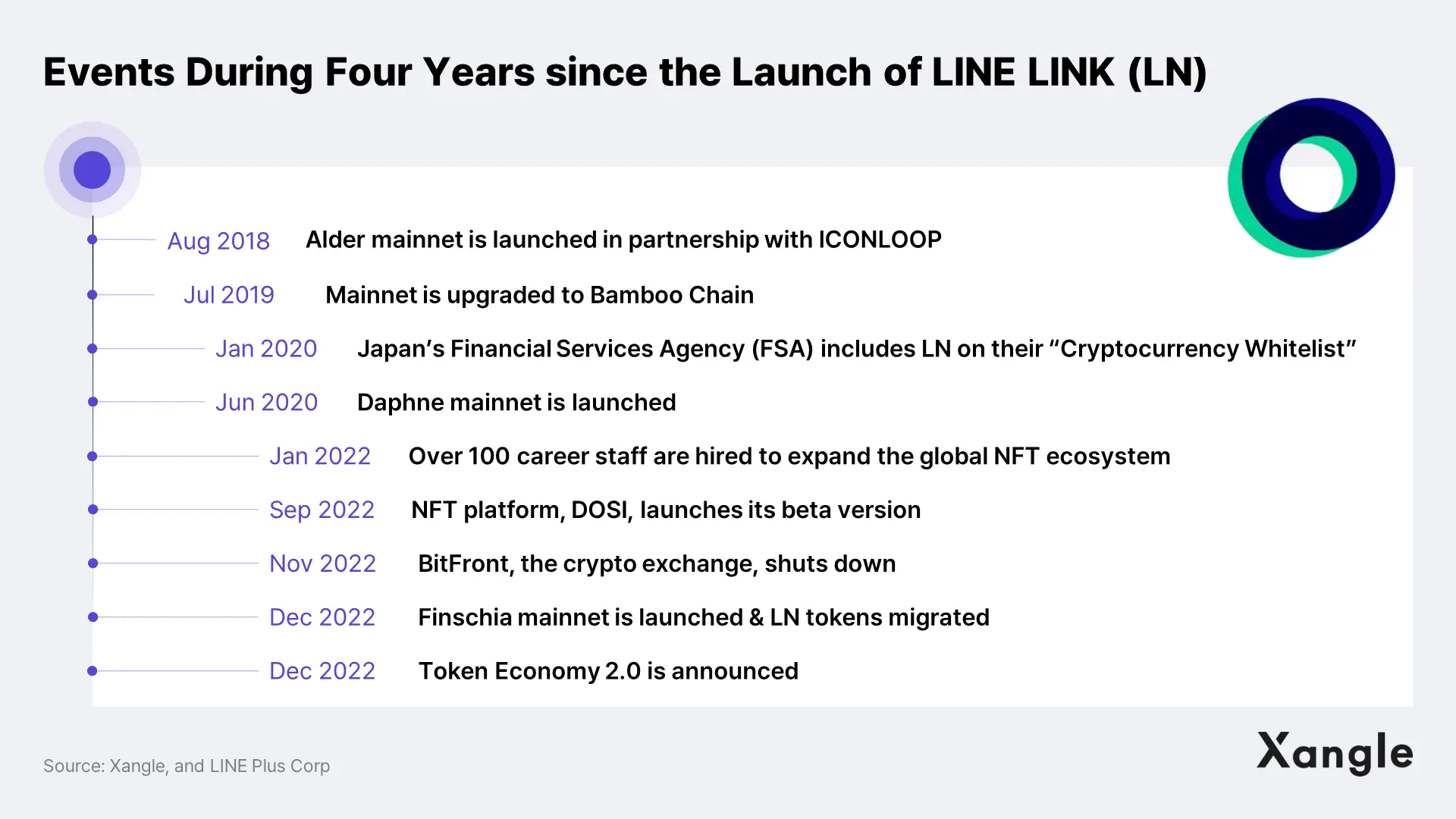

LINK is a Layer 1 (mainnet) coin issued in 2018 by LINE, one of the most prominent messenger applications in Asia. It was back when a number of messenger super apps, such as Facebook, Telegram, and KakaoTalk, were making their moves into the crypto industry. LINE also sought to enter the world of crypto around the same time. As a result of such efforts, LINE launched its own mainnet through a partnership with a Korean blockchain startup, ICONLOOP, and started on a full charge-ahead with its projects by issuing the coin – LINK (LN).

However, three years since its mainnet launch, LINE LINK has yet to produce significant results. Its Layer 1 ecosystem was never fully established due to i) tough regulations in Japan and ii) the operation of closed-off private mainnets.

First, LINE’s early plans to fire up its FinTech business through LINK were dampened by the Japanese financial authority’s strong regulations. Note that LINK is not the first of LINE’s services to be put under the control of financial regulators. LINE already had other financial services in operation, such as LINE Bank and LINE Pay. It happens to be the Japanese government’s unwelcoming stance toward blockchain projects that pushed LINK down the priority. Despite such unfavorable conditions, significant achievements were made; namely, LINE’s own exchanges, BitMax and BitFront, obtaining licenses in September 2019, and LINK token getting on the whitelist of Japan’s Financial Services Agency (FSA) and becoming available on Japanese exchanges for trades.

Another reason for LINK’s stunted Layer 1 ecosystem is the operation of closed-off private mainnets. By having private mainnets that structurally limit dApp developers from freely developing services, new services could not be built on the LINK ecosystem, nor could a community of supporters be formed. Naturally, other services that had launched on various other Layer 1s, including Ethereum, were never built on the LINK ecosystem, and no “killer dApp” ever emerged. All of these factored in to hold LINK back in the Layer 1 race, which was clearly represented by its considerably underperformed coin market cap compared to other competitor projects.

Coming out of the past three years of its dark ages, LINK restructured its governance and started to pick up the speed for its business development in 2022. The strategy was to pick its battles and fully support the selected few businesses. LINK made decisions to reduce the number of its business fronts by pulling out its BitFront Exchange while focusing on the NFT business and revamping the mainnet roadmap. In particular, to drive its blockchain business around NFTs, LINE NEXT, DOSI’s developer, hired a large number of career staff in early 2022 and launched DOSI, an NFT metaverse, in September. Moreover, Cosmos-based Finschia mainnet was launched in December 2022, gearing up to leap from the existing structure with a private chain to one with a public chain.

2. Seeking a Rebound with the New Mainnet, Finschia

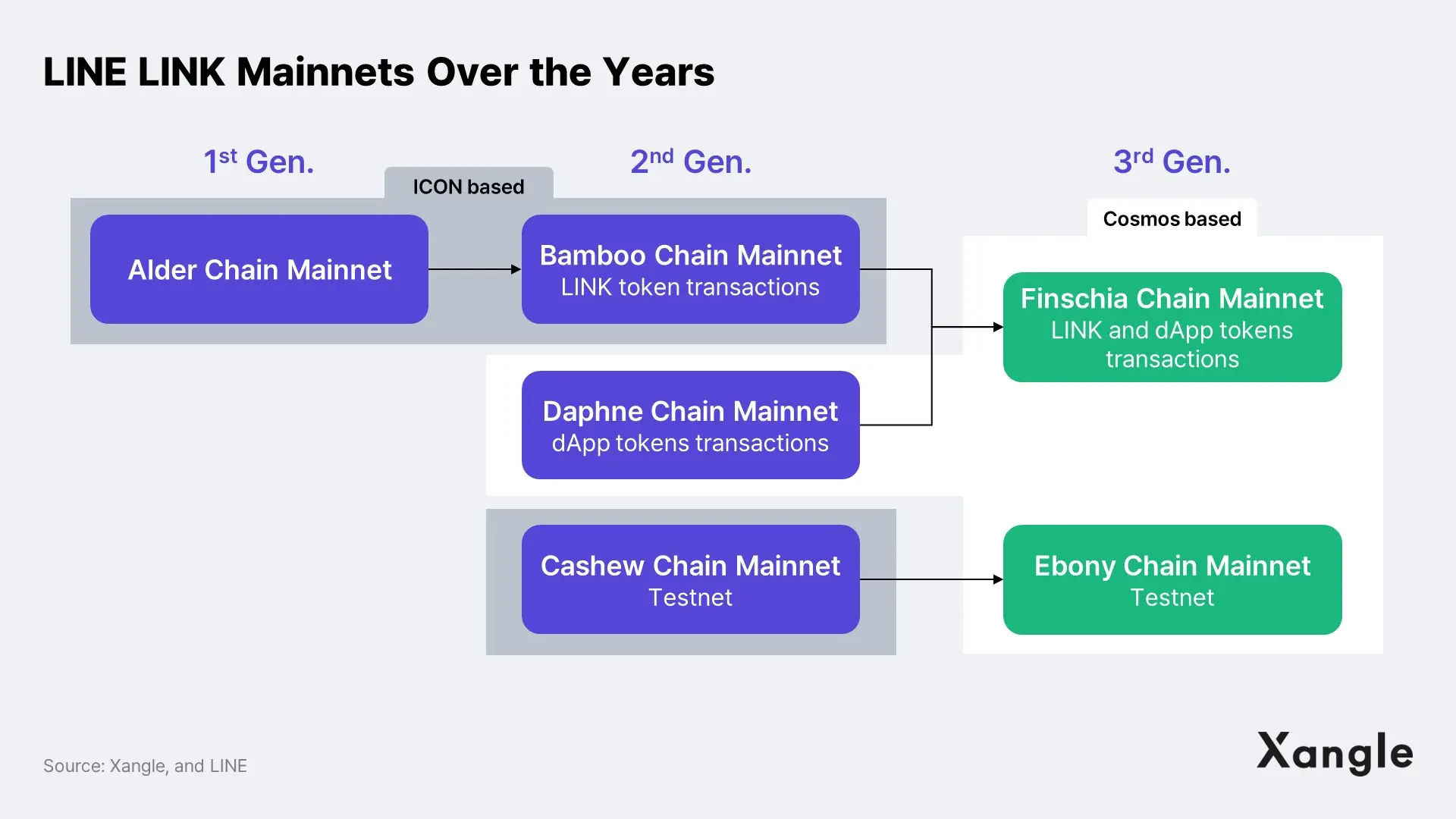

There are three generations of LINK mainnets so far. After the first generation of the Alder mainnet, LINK operated under a dual-mainnet structure with its second-gen mainnets: the Bamboo and the Daphne mainnets. The reason they opted for such a unique system that runs on two different mainnets was the regulations in Japan. Japan has been adamant in its restriction against swapping between mainnet tokens and dApp tokens for anti-money laundering purposes. To comply with such regulations, LINK had to separate its mainnets into the Bamboo chain that governs LINK tokens and the Daphne chain that governs dApp tokens. Moreover, how these mainnets are structured becomes all the more strange when you consider how the Bamboo mainnet is based on ICON while the later-developed Daphne mainnet is based on Cosmos, which means the two mainnets are based on different programming languages and development environments. However, with the third-gen mainnet, Finschia, the two separate mainnets were integrated to oversee the issuance and transactions for both LINK tokens and dApp tokens under a more efficient and normal mainnet structure.

The Bamboo mainnet had certain limitations that come with the fact that it was based on the ICON network. First of all, because it was developed using Python as its programming language, it has a low speed and is limited in dApp adoption due to the lack of support for virtual machines such as EVM and WASM. For the new and improved Finschia mainnet, LINK opted to base it on the Cosmos network and introduced CosmWasm, resolving the issue of speed and efficiency of the developing language and enabling the adoption of WASM-based dApps at the same time.

So, why was Finschia designed for the Cosmos network? The choice was likely based on i) the view that WASM shows more promise than EVM in the long run and for ii) business continuity. First, even though EVM is dominating the blockchain development scene today, WASM has a chance to take over as the favorite in the long run since it offers more language options and higher efficiency. (Please refer to the Xangle research article, “From EVM to eWASM” available in Korean, for more details.) In terms of business continuity, it is important to note that the previous mainnet for dApps – Daphne – was Cosmos-based. This implies that the developers in LINK are likely more familiar and comfortable with Cosmos-based programming languages. Since LINK plans to develop and onboard key dApps themselves, it would have been only natural to choose the environment their own developers are already familiar with – Cosmos-based – over the EVM-based one.

Next up for the list of challenges LINK needs to overcome on Finschia mainnet are i) securing validators and ii) onboarding dApps. In regard to recruiting validators, LINK is expected to operate its network as a permissioned blockchain for some time in the early phase. It is the same strategy used by many PoS chains, such as Cardano and Solana, in which the network operates under a permissioned blockchain scheme until securing a certain number of nodes and gradually switches to a permissionless type. As for dApp onboarding, the onboarding of DOSI NFTs currently in service would be the key. DOSI NFTs are currently issued on the Daphne mainnet but traded on Ethereum, and the transactions are sent through off-chain servers and finally recorded on the Daphne mainnet. The integration of Finschia and Daphne chains is anticipated to put an end to such an unorthodox way of handling transactions.

3. LINE Develops Its Own Key Services

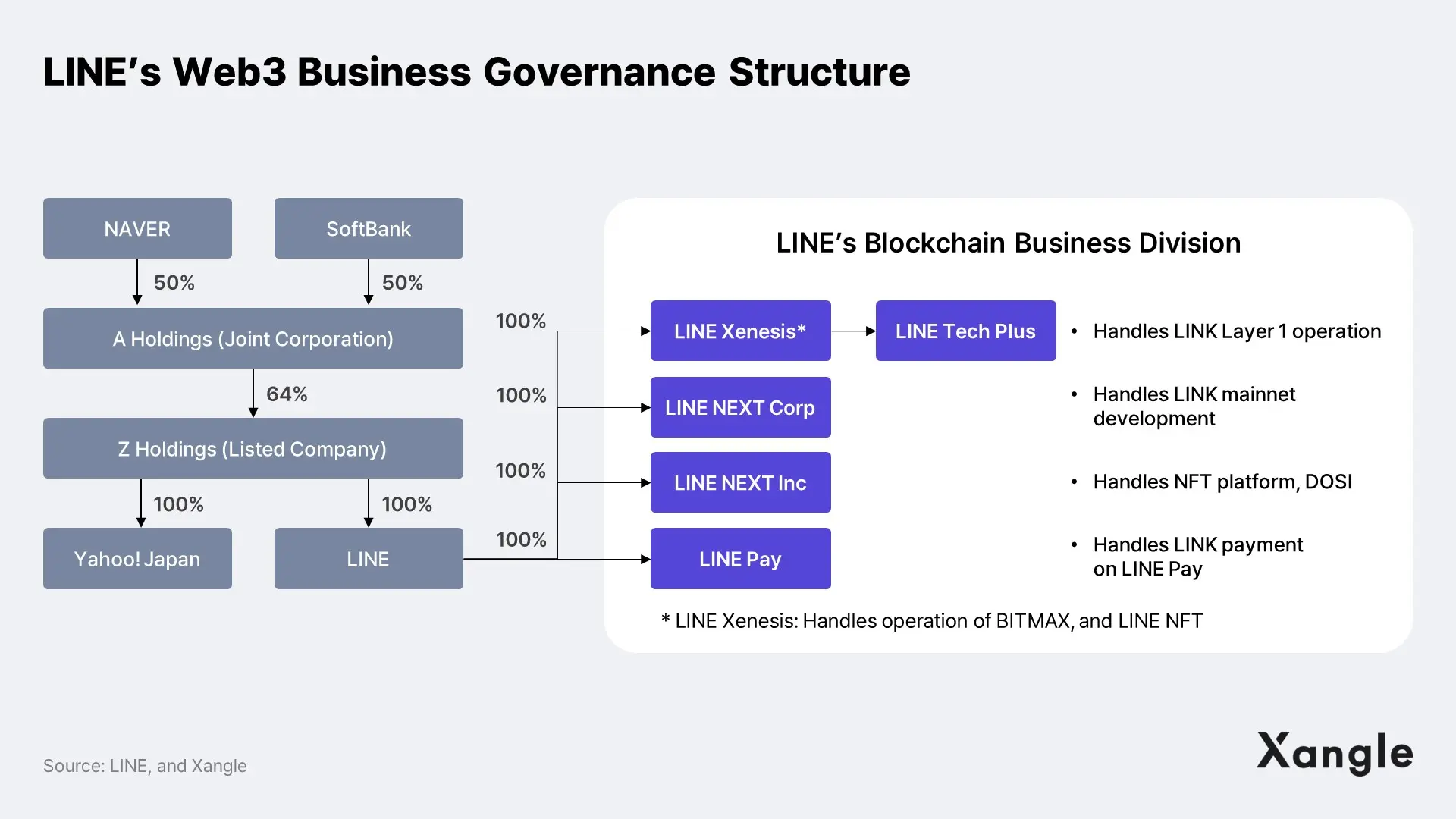

Although LINE LINK launched Finschia, a new Cosmos-based Layer 1 mainnet, its blockchain strategy is unlike any other Layer 1s. The biggest difference is that LINK develops its own key application services through its subsidiaries. For example, for the NFT sector where LINE is focusing its efforts, LINE NEXT took charge of developing “DOSI,” the NFT marketplace and the service critical to LINE’s NFT business, while LINE Pay and LINE Xenesis conduct businesses for payment services using LINK. LINE is taking a completely different perspective and approach in developing its ecosystem compared to other Layer 1s that develop their services through third party dApp development projects and focus on supporting them once developed.

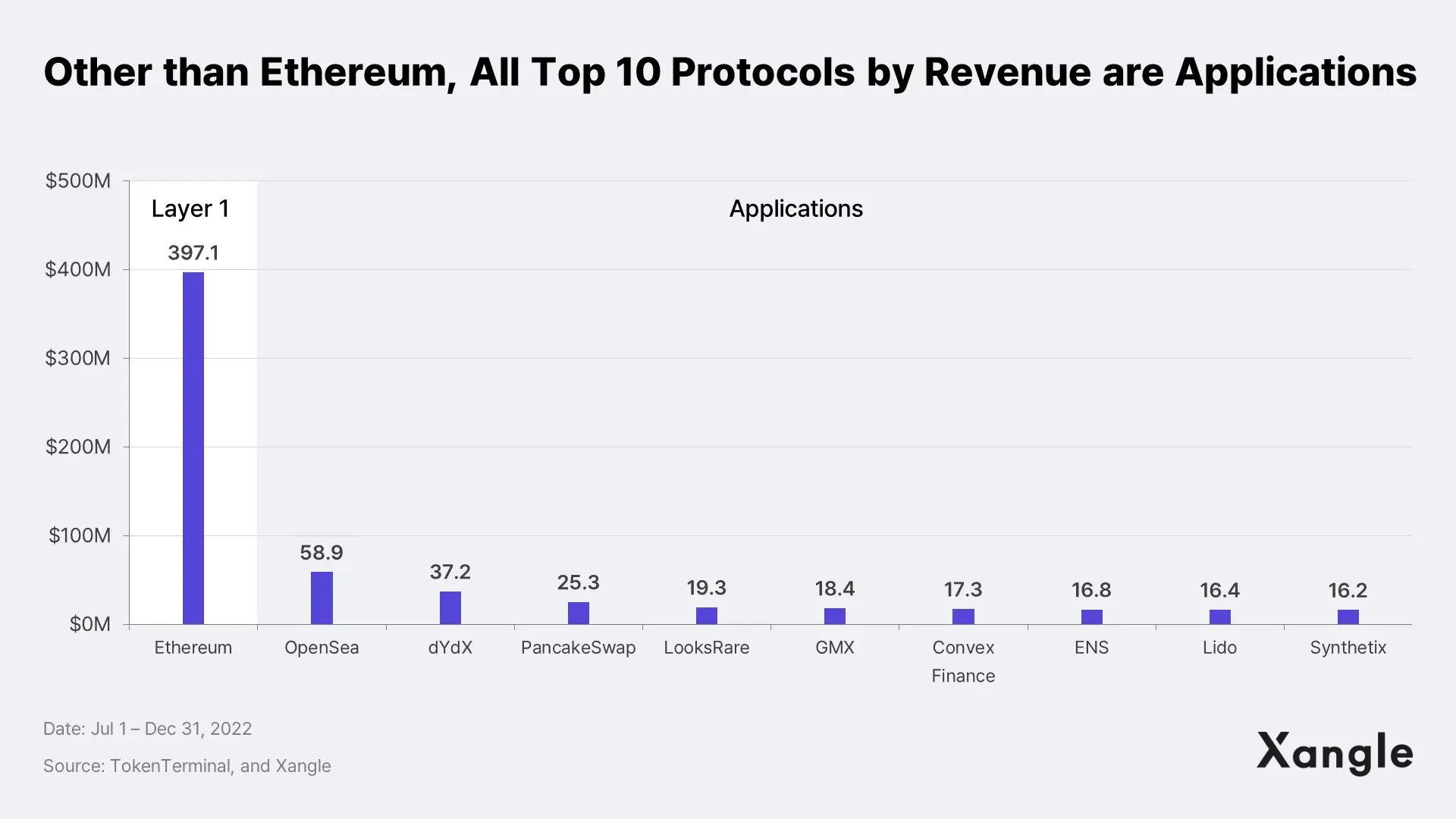

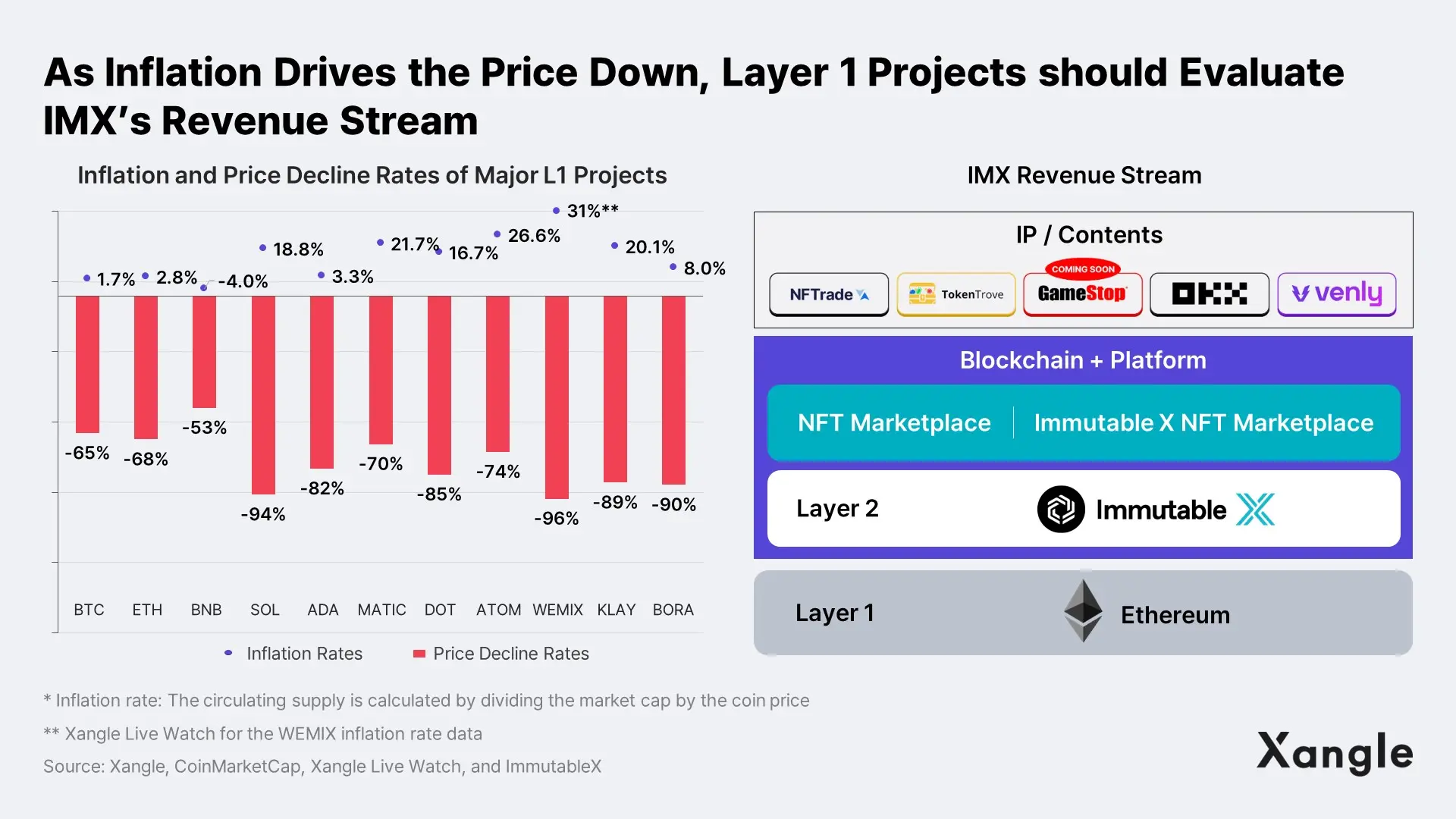

This approach seems convincing based on the Fat Protocol Thesis, which claims value is concentrated at the application layer rather than the Layer 1 protocol (For complementary reading, check out “Fat Protocols vs. Fat Applications”). Based on the cumulative revenue in 2022, except for Ethereum, as it has a high transaction fee, nine out of ten projects turned out to be applications such as NFT marketplaces. Leveraging dApps to generate profit while separately operating a Layer 1 protocol are ways to minimize conflicts of interest for a listed company like LINE, which has to prioritize shareholders’ interests to increase shareholder value.

The fact that Layer 1s have not been able to generate sufficient profits due to the recent drop in their transaction fees also gives more weight to the strategy. Issuing more tokens to cover operating costs and to leverage them as incentives to maintain the Proof-of-Stake (PoS) protocols would not serve as long-term solutions – both solutions would eventually drive the price down and necessitate the sacrifice of existing holders. Just as Immutable X has its own NFT marketplace to fund itself, Layer 1 protocols should consider building new revenue streams internally to support organic growth.

As the service is built by a traditional Web2 company, it takes a different strategy from Web3 natives. To use DOSI, users can sign up for a DOSI Wallet and log in using various social media accounts, including a Naver ID, through which users can store and sell NFT without storing any seed phrases. Users can pay with Naver Pay and other payment options to trade NFTs. Though different from the Web3 approach, DOSI offers an easy and simplified process designed to shape NFT popularization. DOSI continues to offer a frictionless user experience and showcase arts and culture content. Amassing over 710,000 wallets issued since launch as of writing, DOSI is expected to become a significant player in the expanding LINK ecosystem.

4. Zero Reserves Tokenomics

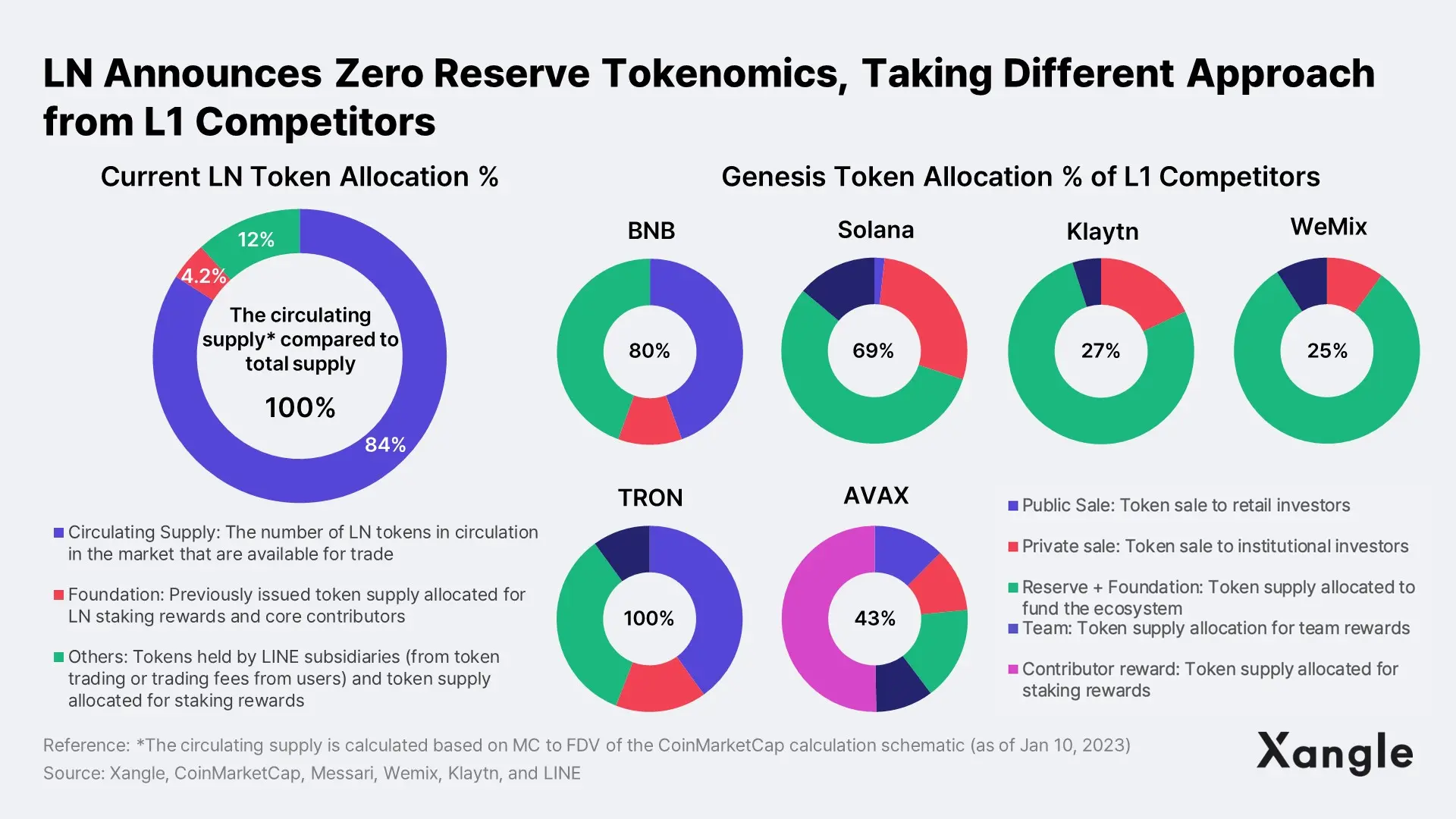

At the end of 2022, LINK announced the Zero Reserves strategy*, which presented a disruptive idea to the industry mired in controversy due to misreports on the token’s circulating supply. Under the current Layer 1 tokenomics, a certain percentage of the token supply is held in reserve to pay incentive rewards to PoS node operators and support dApps developers. As for domestic Layer 1 competitors, Klaytn allocated 53% of the token supply to its reserve fund, and Wemix allocated 74% of the tokens to its ecosystem fund. Polygon allocated 23% of the token supply to support its ecosystem, and Solana allocated about 50% of the tokens for investment and support funds. With the Zero Reserves strategy, LINK suggests an entirely different tokenomics modeling as it does not allocate a portion of the initial token supply to the reserve.

*Zero Reserves strategy: An inflation mechanism under which LN tokens are issued in line with an inflation system, meaning that there will be no issuance or distribution of tokens in the future except for the LN tokens (about 6.73M tokens) that are either in circulation or allocated to those who participated in block generation.

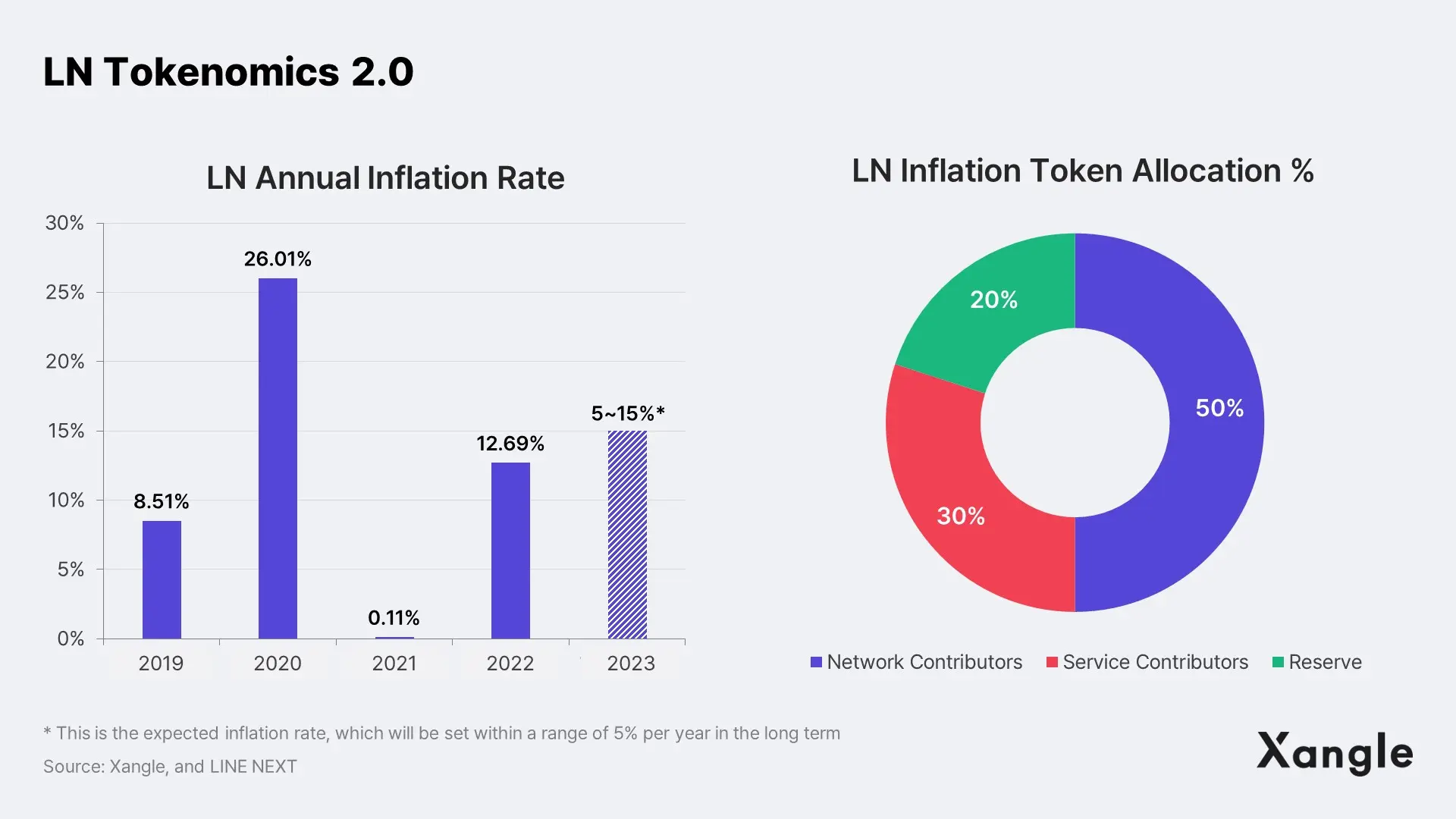

LINE’s third generation Finschia mainnet presents a new tokenomics under which the inflation rate will decrease in stages (15% → 5%). Of the total inflation, 50% will be allocated to network contributors including validators, 30% will be used to incentivize service developers that contribute to LINK payments and transactions, and the remaining 20% will be held by the reserve to support the ecosystem and R&D.

The Zero Reserves strategy will i) emphasize the significance of transparent disclosure and management of token supply and ii) highlight issues surrounding the current grant programs of Layer 1 blockchains. As there is no pre-minted supply, projects will no longer be able to use tokens to their benefit – with the Zero Reserve strategy, the project team will not be able to commit fraud involving tokens, as SBF did with FTT tokens. Furthermore, tokens will be issued in line with an inflation system, preventing any misreports on circulation numbers for the token. Another advantage of the strategy is combining different market cap calculation methods (FDV, MC, etc.), allowing projects to estimate the market cap using a single method.

One of the drastic changes is that LINK did not implement the Layer 1 tokenomics and its developer grant program. In many cases, developer grant programs did not bring significant contributions to the ecosystem, and in worse cases, developers pulled the rug out from under the projects. In this regard, LINE blockchain's Zero Reserves is expected to construct a healthier ecosystem. However, it still needs to be clearly presented on what basis the issued token will be distributed; the project team should be able to convince the LINK community and ecosystem participants that the proposed guidelines bring value to the ecosystem.

5. Possible Delay in Building Infrastructure and Attracting Killer DApps Remain as Challenges

As mentioned earlier, LINK's development strategy and Zero Reserves tokenomics differ from the current Layer 1 designs. Based on these approaches, LINK is expected to i) build a relatively sustainable Layer 1 ecosystem and ii) design tokenomics with less inflation. On the other hand, LINK's development strategy may cause a delay in building the blockchain infrastructure, and the Zero Reserves tokenomics may pose a challenge for the project to attract killer dApps.

Blockchain projects need Layer 1 infrastructure to build and utilize dApps, including block explorers, wallets, bridges, oracle, and DeFi services. Most of Layer 1 protocols offer a variety of grant funds to sponsor external developers to build their blockchain infrastructure. However, LINK runs its own developers to build every service, which may cause slow development progress. In addition, the Zero Reserves strategy is designed to minimize the number of external developers, indicating that LINK will take more time to launch killer dApps than other Layer 1 competitors. LINK blockchain’s disadvantages could potentially affect the competitiveness of Layer 1 protocols, and it seems necessary to prepare countermeasures to alleviate such concerns.

Leveraging the popular messaging platform LINE, operated by the parent company, could play an impactful solution in onboarding dApps. The recent governance restructuring has increased the possibility of support from the group, which is encouraging. LINK has woken up from a long slumber – I look forward to seeing LINK leaping forward using the lessons learned from other competitor projects that already went ahead.

Disclaimer

I confirm that I have read and understood the following: The information contained in this article is strictly the opinions of the author(s). This article was authored free from any form of coercion or undue influence. The content represents the author's own views and does not represent the official position or opinions of CrossAngle. This article is intended for informational purposes only and should not be construed as investment advice or solicitation. Unless otherwise specified, all users are solely responsible and liable for their own decisions about investments, investment strategies, or the use of products or services. Investment decisions should be made based on the user’s personal investment objectives, circumstances, and financial situation. Please consult a professional financial advisor for more information and guidance. Past returns or projections do not guarantee future results.

Xangle or its affiliated partners own all copyrights of the written or otherwise produced materials and content provided on the platform. Any illegal reproduction of such content, including, but not limited to, unauthorized editing, copying, reprinting, or redistribution will result in immediate legal actions without prior notice.

![[Xangle RWA Series] Solana RWA: A Look at the Key Players](https://resource.xangle.io/files/content/F779A005246C0299246537AACB3A39F2_1782287059970.webp)